Hammond’s innovative signature products, GravityGuard® and Treated SureCure®, are two of more than 150 customized additives that are improving battery performance and lowering manufacturing costs for battery manufacturers around the world.

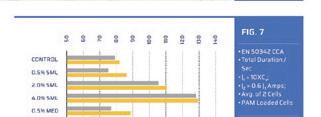

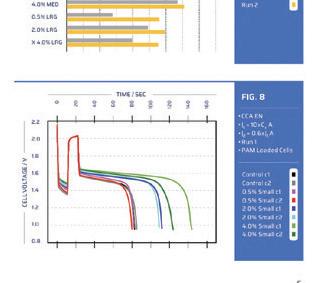

Hammond has released a comprehensive whitepaper detailing exciting findings of new benefits of the antistratification additive GravityGuard ® New research shows that the BCI Innovation Award winning product also offers significant serendipitous improvements that may provide additional value to battery manufacturers and their products. Specifically, the results show GravityGuard® used

in the PAM and NAM can improve CCA performance, 2C Capacity, and extend PSoC Cycle life. The paper presents notes on evaluation methods, specific comparative data, and more than a Independent GravityGuard ® Testing Reveals Improved CCA & PSoC Cycling

dozen charts and graphs with detailed analysis of a wide variety of test results. A PDF is available online. Just snap the QR code above to go to the publication download page.

As the world’s largest family-owned lead battery manufacturer celebrates almost 80 years in the industry, we speak to new CEO, Pete Stanislawczyk, and incoming president, Christy Weeber, on their joint strategy for the future.

The energy storage industry isn’t the best at communicating its good news — but now is the time for us to shout. We are the future!

Tributes paid to Urs Bühler • Lyten names executive team to revive Northvolt

• Microvast reveals departure of CFO Carl Shultz • MAC Engineering promotes Bret Stern and Nick Dailey • Sandia’s Rosewater admitted to Battcon Hall of Fame

• East Penn among ‘best US employers’ for women • Ateios awarded Battery Show honour for electrodes tech • Pure Lithium award for ‘Brine to Battery’ tech

EnerSys in $1bn share buyback increase • Leoch mulls new US plant and Mexico expansion despite profit fall • Exide closing France site amid ‘economic challenges’ • Batteries supercharge $140m tax refund for EnerSys amid restructuring and jobs lost • Yuasa hails ‘strong lead business’, hints at investment boost • ExxonMobil acquires Superior Graphite to enter battery anodes market • BESS investment major Gresham to acquire Switzerland’s SUSI • FlexGen secures court approval for Powin assets acquisition • Swiss ‘membrane-free’ RFB tech secures pre-seed finance

THE SITE VISIT: ABERTAX: IN DIVERSITY LIES STRENGTH

Batteries International flew to Malta to meet a company that continues to prove that focusing on research and development is the clear path to product innovation.

I Squared takes majority stake in ENTEK • Battery leaders put pressure on EU heads over foreign competition • Porsche drops EV battery plans amid sales slump • EPA chief attacks ‘delusional’ BESS expansion amid Li battery fire fears • Exide Technologies ‘enhances’ commercial vehicle battery range • East Penn unveils Armor Alloy battery tech • Korea’s SM Group develops lead acid BESS alongside lithium storage systems • DRC cobalt quotas ban to be lifted • Nyrstar in Australia aid boost for antimony, critical metals • US to designate lead as critical mineral • EU in €1.8bn ‘battery booster’ as new report warns of China dependency • Neptune Energy hails major lithium find in Germany • Batteries supercharge $140m tax refund for EnerSys amid restructuring and jobs lost

NEWS CONTINUED

• Amara Raja: LABs dominate sales but lithium investment rising • CATL drives further into Europe’s EV battery market with LFP launch • Tesla issues Powerwall 2 ESS recall in Australia citing fire risk • Waste reforms call as UK faces ‘epidemic’ of battery fires • Datacenters, AI ‘drive LAB growth optimism’ — BCI • VRLA nuclear plants safety study to report in December • EU-Indonesia battery materials trade deal • Virtual power plant market uptick in North America but ‘market barriers remain’• Investment firm Aurelius to acquire Italy’s Fiamm • New EV tests reveal ‘unreliable’ battery range claims, says AAA • Microporous opens Li separator line in Tennessee • InoBat secures €55m loan and grant deal for Spanish gigafactory • Campine probes Russia sales claim, hails H1 sales boost • Swiss ‘membrane-free’ RFB tech secures pre-seed finance

Ecobat disposes of last European lead recycling deal with UK sale — US facilities coming next • Ace Green to offer grid metallics processing system • East Penn sustainability report highlights recycling, emissions milestones • $1.5m boost for lead and Li battery recycling

Balancing the cost of transparency against the needs of business

The flames of a thermal runaway are dangerous but, the vapors, though they look less harmless, are actually far worse.

ICBR 2025, Valencia, Spain — September 10-12 • 100Recycle, the 9th International Secondary Lead & Battery Recycling Conference and 21ABC, September 3-5, Kota Kinabalu, Borneo

Publisher Michael Halls

editor@batteriesinternational.com +44 7342 890 592

Editor Shona Sibary shona@batteriesinternational.com +44 7585 280152

Finance administrator

Juanita Anderson

Juanita@batteriesinternational.com

Subscriptions, enquiries

subscriptions@batteriesinternational.com admin@batteriesinternational.com

Production/design

Antony Parselle aparselledesign@me.com

Content researcher Matt Halls Matthew@batteriesinternational.com

International advertising representation editor@batteriesinternational.com

The contents of this publication are protected by copyright. No unauthorized translation or reproduction is permitted.

ISSN 1462-6322 © 2025 Mustard Seed Publishing UK company no: 5976361. Printed in the UK via Method

Disclaimer: Although we believe in the accuracy and completeness of the information contained in this magazine, Mustard Seed Publishing makes no warranties or representation about this. Nor should anything contained within it be construed as constituting an offer to buy or sell securities, or constitute advice in relation to the buying or selling of investments.

Shona Sibary • editor@batteriesinternational.com

“If I went back to college again, I'd concentrate on two areas. Learning to write and to speak before an audience. Nothing in life is more important than the ability to communicate effectively.”

So said Gerald Ford, 38th president of the United States, who, it is widely acknowledged, presided over the worst economy in the four decades since the Great Depression, with growing inflation and a recession. In one of his most controversial acts, he granted a presidential pardon to Nixon for his role in the Watergate scandal.

You can probably understand why he might have wished he’d brushed up on his messaging. But his appreciation of the power of communication is something none of us can afford to ignore. And, much as I hate to point a finger, our entire industry could really do with sitting up and taking notice.

Obviously, as publishers of your news, we’re in the business of words and telling stories. We like to think we’re pretty good at it. But it can sometimes feel like pushing a very large rock up a hill trying to get any salient information from the battery world at all. And this inability to shout from the rooftops affects the whole energy storage industry – all chemistries, all technologies.

It's hard to understand how our industry, valued at something in the region of $60 billion a year, can be so coy about stepping out of the shadows and blowing its own trumpet. As a journalist for over 30 years, I’ve never encountered companies less willing to pick up the phone or answer a call. Whenever we commission freelancers to write pieces, they always say “but nobody returns calls”.

Perhaps this inability to communicate is actually a reluctance to communicate? Either way,

The power of communication is something none of us can afford to ignore. And, much as I hate to point a finger, our entire industry could really do with sitting up and taking notice

things need to change. And fast. Nobody can deny that we are centre stage of a brave new world. Our industry, now a cornerstone of the global economy, has an influence that extends beyond commerce taking a starring role in climate policies and energy security strategies, with a demand that is expected to explode, quadrupling to 4,100GWh by 2030.

Exciting times! And with this fast-moving maelstrom of opportunity there is a tsunami of news and unfolding events. Our industry has become the story that never stops giving and it can be hard to make sense of it all.

But make sense of it we must. This requires everybody to do two things. Firstly, really understand the value of communication. And secondly, to actually communicate in an impactful way.

A quick glance through conference speeches over the last 20 years shows a woeful decline in the quality of the presentations. Delegates just aren’t challenged by the content anymore. We’re getting half-baked thoughts and ideas — I could even go as far as deceptions — and there is so much repetition.

As George Bernard Shaw once famously said: "The single biggest problem in communication is the illusion that it has taken place." I have lost count of the number of times I have walked out of a talk into the coffee break with a blank notepad and a sinking heart.

How many times do we see presentations where the purpose of the discussion is to focus on the importance of the institution giving it. The message is the speaker not the content.

A good example is a talk I heard a few years ago, where the presenter discussed various company structures and purposes his organization had. He used a welter of words to give the illusion that the firm had been operating for years.

To my shame I didn’t challenge the speaker even though I knew that two of the companies being discussed had only been set up a a mere two months beforehand. (I had even checked them out at Companies House in the UK.) It was a study in smoke and mirrors.

And we see this in other ways too. How many

times do we listen to a 20-minute presentation where the first 10 minutes are spent talking about the firm and not the topic we really want to hear about?

Why do we allow this to happen? It’s hard to puzzle. Has social media dimmed our attention span to such a point that we all, now, just accept that with any spoonful of sugar the marketing must also go down?

Perhaps the perfect example of this is the battery industry’s obsession with talking about the recyclability of lead. Ever since 2010 and the emergence of lithium batteries in EVs, it’s been impossible to attend any gathering without at least a dozen speakers claiming 99% of a lead battery can be used again and again.

In actuality, it’s far less than 99% but does the validity of this matter anyway? This is a new variant of Orwellian double-speak, where sense is subordinated to repetition.

Either that, or the real nub of a point is so buried in obfuscation — using perissological periphrasis and obumbrate language to hide denotation in a caliginous somewhat inspissated sea of pleonastic verbage.

You get my point. Using big words to hide real meaning has serious consequences. You only have to look at famous miscommunications in history to see where things can go horribly wrong. Take the Charge of the Light Brigade during the Crimean War in 1854. Due to a miscommunication in the chain of command and a series of gaffes thereafter, the Light Brigade rode directly into a heavy artillery battle scene – which they weren’t suited for. The result? Brutally high casualties. (But as a plus a memorable poem by Alfred Lord Tennyson.)

Historical accounts say that when the original order was relayed to the troops, it lacked insight into the bigger picture or purpose of their strategy. It was also one of those miscommunications that became so convoluted, no one knew exactly who gave what orders and why. For years after the war, some of the higher-ups continued to point fingers and mitigate themselves of responsibility.

Okay, so none of us are going into battle on

horseback, but I see this kind of miscommunication happening all the time in the battery world and there is now an urgent need for clarity.

As an industry we don’t need to be lobbying our elected officials, nor the average people on the street. Instead, our collective messaging has got to be targeted to the decision makers, that’s not the government itself but its advisers.

But what should this message be? Perhaps if we want to communicate the advantages of lead over lithium or vice versa we need to think hard and fast about what we say and how we say it.

The whole world is going through times of turmoil on a huge variety of fronts. And all this is against a background of possibly the most important change to affect humanity — the great energy transition.

From a publishing perspective, a subject such as better start-stop batteries for European automobiles isn’t going to make anyone’s heart zing. But it is important and if we can frame issues like this into a larger context everybody might start sitting up to listen.

All of us, not just Batteries International, have the power to communicate the bigger picture — that is, how batteries are the secret force behind the energy transition. And we need to embrace that old adage that wise men speak because they have something to say. Fools because they have to say something.

Shona Sibary, editor

It is with sadness that Batteries International reports that Gerry Woolf, a batteries and energy storage journalist for more than 30 years, passed away on October 13. He was just 71 years old.

Gerry spent almost all of his life as a technical writer, editor and finally business person involved in the energy storage industry. After graduation he joined the BBC where he was trained as a journalist and he worked on the World Service radio broadcasts for several years.

In the 1990s he was recruited to work as the editor of Batteries International which he left in 2004 to set up his own magazine, Best. (Batteries & Energy Storage Technology).

Hugh Cullimore, one of the original founders behind Batteries International, recalls: “He was a fast learner and within months of joining us was fully up to speed. In total I worked with Gerry for the best part of 20 years and together we helped make Batteries International and later Best a success.”

For the next 14 years Gerry built up a small magazine business launching a Chinese title in Mandarin and a magazine on back-up power. He made unsuccessful attempts to enter the conference business but found better traction with a weekly newsletter that continues to this day.

After stepping back from day-today editorial duties in 2018, when he announced “a new chapter” for Best, Gerry remained non-executive chairman and continued to lend his voice and experience to the business.

In later years he faced personal medical challenges, by accounts from friends and colleagues which he approached with characteristic determination and dignity.

He was respected — and frequently feared — for his trenchant directness in getting answers to his questions.

Andy Bush, executive director of ILA, said: “Gerry was a larger-thanlife figure in the industry, and while he could come across as critical, he was usually just probing a subject for greater insight, which was his passion as well as his job. He had affection for the lead battery industry and always wanted to see it succeed — a critical friend.”

Mark Rigby, managing director of UK Powertech, a firm specializing in battery formation equipment, said: “I was Gerry’s friend for over 30 years and knew him well. He was a courageous man in the way he approached life and someone to be respected for the depths of his knowledge about the battery business.”

Gerry’s legacy lives on countless issues of Best distributed around the world, in the debates he sparked, and

in the network of industry relationships he helped build.

Among those who feel his influence are his former competitors and collaborators, including Mike Halls and the team at Batteries International, who respected the editorial benchmark Gerry set—even in the spirit of friendly rivalry.

Mike McDonagh, an industry veteran, battery consultant and also technical editor of Best recalls how Gerry helped him at the beginning of his writing. “I owe a lot to him personally for the way he developed my writing skills. The first time I wrote something for him he said ‘this is not good. It’s bloody good!’ but he also could be blunt comparing my writing style to Enid Blyton [a popular UK children’s author of the 1960s]. He was tough but fair.”

He leaves behind his son Oliver and his wife Catia and grandson Thomas, and many others who were touched by his mentorship, editorial leadership and willingness to engage with the international battery community.

He remains a notable figure in the battery-storage sector, whose contributions helped shape the conversation around energy storage during a period of rapid change.

An announcement of his funeral service will be made shortly.

NEGATIVE EXPANDER The expander may be negative, but your experience will be entirely positive.

The job of negative expander is to reduce strain, maintain capacity and improve performance. In a way, that’s our job, too.

At APG, we deliver the best products and customer satisfaction in the industry through unwavering focus and personal relationships.

We offer the best pre-blend negative expander on the market, brought to you by a certified Women’s Business Enterprise and family-owned company you know and trust.

Find out more at atomizedproductsgroup.com info@atomizedproductsgroup.com

Swiss extruders and tech group Bühler has paid tribute to the company’s former owner, Urs Bühler, who died on August 1 aged 82.

The group said his death meant the loss of a figure who significantly shaped the company as an owner, former chairman of the executive board, and who oversaw more than five decades of the firm’s successful development.

Born in 1943 in Uzwil, Urs spent his youth there. He attended the Kantonsschule am Burggraben in St Gallen and later studied mechanical engineering at ETH Zurich.

Joining Bühler in 1970, he held various positions both domestically and internationally, until being appointed CEO in 1986. He became the sole owner of the company in 1990

and also served as chairman from 1994.

Throughout his career, he held a number of executive posts including serving on the board of the Swiss Bank Corporation, Sulzer Group, and Winterthur Insurance. He was also on the board of Swissmem for 30 years, significantly contributing to Swiss industrial history.

In 2001, as part of succession planning, he transferred operational responsibility of the group to Calvin Grieder, who also took over as chairman in 2014.

Also in 2014, Urs ensured the succession of family ownership of the firm by transferring shares to his daughters Karin, Maya, and Jeannine – the fifth generation of owners.

That followed his decision in 2011 to transfer ownership of The Uze company (founded in 1892 to manage the family’s real estate) to his daughters.

MAC Engineering & Equipment has announced two key promotions — with Bret Stern becoming VP of sales operations and program management and Nick Dailey senior marketing and visual communications manager.

The appointments were announced on September 10.

Stern, who started his career as an automotive technician, joined MAC in 2022 as sales director covering the US and Canada. The company said he will continue to act as a bridge between sales, customer support, the marketing team, other departments, and customers.

Additionally, he will manage the portfolio of MAC’s customer projects and be responsible for

developing and implementing program strategies.

Internally, Stern’s focus will be on improving processes that support all MAC team members to improve efficiency and effectiveness.

MAC told Batteries International that Nick Dailey, previously engineering and marketing project coordinator, will drive an expansion of MAC’s brand

During his more than 50 years at Bühler, Urs ensured the continued successful development of the company through a number of initiatives, including global expansion and exploiting new technologies such as extrusion and automation.

In terms of innovation, his legacy includes the Urs Bühler Innovation Fund, which is an innovation advisory board comprising recognized experts.

Urs also championed construction of the Cubic Innovation Campus, and the recently opened Bühler Energy Center.

Under his leadership, the mechanical engineering company evolved into a broadly positioned and global technology group, offering a comprehensive range of solutions for the food and mobility industries.

However, Urs remained a modest, reserved, and empathetic person.

awareness and revenue in his new post.

The company said Dailey, who joined MAC in 2023, had shown his talent in overseeing campaign creation and execution across digital and traditional channels and collaborating with other departments like sales, and monitoring key performance indicators to ensure return on investment.

In addition to technology and business, his great passions included equestrian sports, skiing, and a holistic approach to the health of humans and animals, the latter being reflected in the company Health Balance, which he founded in 2004.

Urs’s daughters said in a personal statement: “We are committed to the legacy of our father and predecessors and will continue to run Bühler as a family business. The strategic focus on innovation, training and development, and sustainability also has our full support.”

The company said Urs had always been forward-thinking and innovative. “With gratitude and the utmost respect, we bid him farewell. He remains an inspiring role model to us as a visionary entrepreneur, innovator, and above all, a remarkable human being.”

US immigration officers have detained more than 470 in a raid on the construction site of a battery cell manufacturing joint venture of Hyundai Motor and LG Energy Solution.

Officers from the federal US Immigration and Customs Enforcement (ICE) department swooped on the HL-GA Battery Company site on September 4.

ICE claimed a number of individuals arrested at the site were working illegally and one green card holder from Mexico was arrested — with a view to the individual being deported, based on alleged multiple criminal convictions.

None of those detained

were thought to be directly employed by Hyundai Motor, the firm said on September 5.

However, the company said its North America chief manufacturing officer, Chris Susock, had “assumed governance of the entire megasite” in Georgia and would conduct an investigation to ensure all suppliers and their subcontractors comply with all laws and regulations.

Steven Schrank, special agent in charge of Homeland Security investigations

in Georgia and Alabama, said: “We welcome all companies who want to invest in the US and if they need to bring workers in for building or other projects, that’s fine — but they need to do it the legal way.”

Hyundai and LGES are investing more than $4 billion in the battery plant, which is scheduled to start production early next year.

HL-GA will supply next-generation battery technology to manufacturing facilities for production of Hyundai, Kia and Genesis EV models.

Hyundai said the facility will help create a stable supply of batteries in the region and allow for a quick response to the global EV demand.

East Penn Manufacturing has been ranked as one of America’s best employers for women in 2025.

The lead battery manufacturer announced the ranking, by Forbes and Statista, on August 5 — the second time the firm has been named to the list, which also acknowledged some 700 other large American companies.

The accolade came just five months after Forbes and Statista ranked East Penn as one of America’s best large employers for the fourth time.

David Rosewater, a research engineer at Sandia National Laboratories, has been inducted into Battcon’s Hall of Fame.

A surprised Rosewater was called to the stage at the annual conference this August, to receive the accolade by Ashton Curtis, part of the technical committee of the Battcon conference in Florida.

Curtis said: “This year’s recipient is relatively young and relatively unknown.”

However, over the last five, six years, Rosewater had single-handedly, along with other inputs: “advanced the state of the battery safety industry by leaps and bounds with benefits to us all”.

Rosewater said: “Many of the folks who are past recipients of this award have been my mentors and to be counted among their number is a deep honour. These are folks who have lifted all of us up. And I feel

unworthy to be counted among these people.”

Rosewater’s story began after taking his bachelor’s and master’s in electrical engineering at the University of Montana.

One of his professors had a friend at Sandia National Laboratories who suggested Rosewater apply for a research position and he joined in 2011. Rosewater was mentored by former Battcon recipient Garth Corey, who suggested he submit a paper at Battcon, which he first did in 2013.

The subject was zinc bromine flow batteries.

Rosewater left Sandia to do his PhD at the University of Texas at Austin in 2016 before returning to the national lab in 2020.

During that period, he became aware that there was little agreement on what constituted an industry-wide safety policy. He ended up creating a battery safety

training class.

Rosewater told Battery International at Battcon “I realized that there was a disconnect between what the people who do their work every day are doing and what the standard for electrical safety says they should be doing.”

That started a long process that culminated in the National Fire Protection Agency adopting his results — a huge safety benefit for the entire industry — and Rosewater hopes they will become a permanent part of the standards.

For the latest ranking, Forbes and Statista conducted an independent survey from a representative sample of more than 140,000 women working for companies employing at least 1,000 people in the US.

The final score was based on personal evaluations, given by employees themselves, in addition to evaluations from friends and family members of employees, or members of the public who work in the same industry.

A much higher weighting is given to personal evaluations and the percentage of women serving in East Penn’s leadership team was also incorporated into the final score.

Christy Weeber, EVP and CFO of East Penn, said: “Women have played an essential role in shaping East Penn’s success, helping to build a strong, values-driven culture and contributing in countless ways that have advanced our company.”

California-based lithium sulfur developer Lyten has put a new management team in place in Sweden and Poland for Northvolt, in the wake of its takeover of the troubled European battery maker.

Batteries International reported last August that Lyten had moved

to acquire Northvolt’s remaining assets in Sweden and Germany, after Northvolt filed for bankruptcy in Sweden.

Lyten has since revealed that it appointed a new executive team on September 4 to support the takeover.

Matthias Arleth has been

Li metal battery company

Pure Lithium said on August 25 it had been honoured by the American Chemical Society for its ‘Brine to Battery’ technology.

Pure received the 2025 Green Chemistry Challenge Award in the society’s chemical and process design for circularity category.

Pure said its technology seamlessly integrates lithium metal extraction

and battery anode production, significantly reducing energy consumption and environmental impact associated with shipping materials.

The company said its Li metal batteries eliminate graphite. Instead, it extracts Li metal from lithium brine, which Pure said is abundant in North America, to create a lithium metal anode that completely replaces today’s graphite anode.

named CEO of Lyten Sweden, based in Stockholm and reporting to Lyten CEO Dan Cook.

Arleth is a senior industrial executive and engineer with more than 25 years of international leadership experience across the automotive, energy, and electronics industries, Lyten said.

He joined Northvolt one year ago as president BU Cells and COO, where he was instrumental in the restructuring process in

Sweden and successfully improving production performance at the firm’s Skellefteå facilities.

Meanwhile, Robert Chryc Gawrychowski will serve as CEO of Lyten Poland, based in Gdansk, also reporting to Cook.

He will lead the Northvolt Dwa BESS operations, including the systems organization responsible for BESS product design, after being with Northvolt Poland since its launch.

Markus Danglemaier will be CEO of Northvolt Ett, in Skellefteå, reporting to Arleth.

According to Pure, its batteries represent a step change in energy storage, with double the energy density of today’s lithium ion batteries. The company said it has achieved unprecedented cycle life in small pouch cells, upwards of 5,000 cycles.

Now the company is shifting from pure research and development to the prototyping phase at its new facilities in Chicago. Pure founder and CEO Emilie Bodoin said: “We have demonstrated that our technology is capable of eliminating some of the most energy intensive steps in anode manufacturing.”

Established by the US Environmental Protection Agency in 1996, the Green Chemistry Challenge Awards recognize chemical technologies that incorporate the principles of green chemistry into chemical design, manufacture, and use.

Sami Haikala was confirmed as CEO of Northvolt Labs, in Västerås, Sweden, also reporting to Arleth. He has headed the plant since 2022 and will be responsible for both lithium ion NMC product enhancements and work with Lyten’s San Jose team to accelerate lithium sulfur development.

Dennis van Schie has been named chief supply chain officer for Lyten Sweden, based in Stockholm and reporting to Arleth. Lyten said he has nearly three decades of experience in the automotive, electronics, and chemical industries.

Lyten said all members of the team had been pivotal in stabilizing operations and delivering to customers over the last year.

Lyten CEO Cook said: “We have the ingredients to be successful in Sweden, Poland, and Germany. This is a team that knows how to execute. They each have a proven track record in industry and collectively drove a step change in manufacturing performance in Skellefteå over the last year.”

Stryten Energy has been named among the best US companies for women to work.

Stryten said on September 25 it had received the honour in the ‘inclusion’ category of the 2025 Women’s Choice Award for Best Companies to Work — a recognition that highlights organizations committed to fostering inclusive and supportive workplaces for women.

Wendy Henderson, senior VP and chief human resource officer, said: “Receiving this recognition is a reflection of the

programs and benefits we offer all employees, with the objective of providing development opportunities, wellness, and a means to financially prepare for the future.”

Stryten said women who work at the company have job satisfaction along with stability, high-earning potential, flexibility and advancement.

The company is also active in the Women in Auto Care Associa-

tion and Women in the Global Battery Industry, which was formed by Battery Council International (BCI) to promote and develop the growth of women in the battery industry.

Last May, Stryten won BCI’s Amplify Award for Product Marketing for the firm’s innovative video campaign promoting Enhanced Flooded Batteries, featuring the Not-SoGrim Reaper.

Ateios Systems has been named as battery manufacturer of the year at The Battery Show North America.

Ateios received the honour on October 7 at the conference in Detroit for its RaiCure electron-curing technology, which the firm said combines solventfree battery manufacturing, near-zero emissions and domestic scalability.

RaiCure delivers the world’s fastest solventfree electrode production, achieving industrial speeds while eliminating harmful PFAS chemicals and dramatically reducing energy use by up to 96%, Ateios claims.

According to Ateios, the manufacturing speed is some 80 meters per minute, which the firm said is nearly 3× faster than the conventional 30m/min process, producing high-energy electrodes — thick cathodes up to >5mAh/cm² with yields exceeding 95%.

All raw materials are sourced from domestic

suppliers that can compete on performance, price, and volume in a global market

The company said the process replaces traditional, solvent-heavy coating methods and is inspired by semiconductor manufacturing.

CEO and founder Rajan Kumar said: “I am proud of how we have validated

performance at scale while uniting production, supply chain, and sustainability in one cohesive solution.”

Founded in 2018, Ateios said it is committed to enabling a Moore’s Law for batteries, developing techniques to be adopted for years to come while doubling production speeds.

A new expert study on growth rates and future trends of lead battery markets has been published by Battery Council International and research consultancy CRU.

BCI said the “first-of-itskind report” is powered by decades of metals market intelligence at CRU and the proprietary data BCI has collected on battery sales and manufacturing.

Key takeaways in the report include automotive lead battery demand grew 3.9% in 2024, with more

modest growth of 2.5% expected in 2025 and 2.8% in 2026.

Forecasts on lead battery sales for stationary storage include a compound annual growth rate of 2.8% through 2027, according to the report.

Meanwhile, global light vehicle production is now expected to increase only 0.4% in 2025 and 0.7% in 2026, dampened by readjustment of supply chains and stock drawdowns.

With more than 80 years of sales statistics and annual market forecasts

provided directly by its member companies, BCI says it is the exclusive provider of real-world data for the North American battery industry.

BCI said its trusted data, partnered with CRU’s best-in-class analysis and insights, offers the most comprehensive and reliable report available on lead battery market trends.. The report is currently available only to BCI member companies. Email info@batterycouncil.org for details

Lead-based battery-electrolyser technology developed by a UK university has received an ‘outstanding international impact’ accolade at the 2025 Hydrogen Awards.

Loughborough University announced on September 19 it had secured the award at a ceremony in Birmingham, marking its second consecutive Hydrogen Awards win.

The honour comes three years after the Consortium for Battery Innovation said it was supporting the university’s proposals to deploy lead battery technology as part of two projects to provide innovative energy storage systems for Africa.

Earlier in September, the

first full-scale containerised battery-electrolyser was shipped to a rural hospital in Malawi. The university said it will provide solar-powered energy storage for lighting and medical equipment, while producing green hydrogen for clean cooking.

This year’s Hydrogen Awards judging panel praised Loughborough’s technology for its potential in both energy storage and green hydrogen production, particularly providing energy access in underserved regions and to off grid communities.

Developed by the Battery-Electrolyser Team at Loughborough University’s Centre for Renewable Energy Systems

India-based Amara Raja group has opened a base in Dubai in a move the battery giant said will boost business in the region.

Harshavardhana Gourineni, executive director of the group’s Amara Raja Energy & Mobility unit, formally opened the new office and announced the event in a LinkedIn post on August 28.

Gourineni said the office will serve as a hub for customers in Europe, the Middle East and Africa while boosting battery sales across the regions.

Meanwhile, the group said it is ramping up work to develop four manufacturing units in India’s Telangana state that will form part of Amara Raja Energy & Mobility’s battery ‘giga corridor’.

Technology, the technology has redesigned the traditional lead acid battery.

The battery-electrolyser cells can store renewable electricity and also produce high-purity hydrogen when overcharged.

Built entirely from widely available, recyclable materials, it provides a low-cost and scalable alternative to standard electrolysers, the university said.

Parallel international projects, including a demonstrator at Loughborough University as part of the East Midlands Zero Carbon Innovation Centre, will also demonstrate the system’s adaptability in various community settings.

Professor Dani Strickland, project lead and director of EnerHy, the EPSRC Engineering Hydrogen Net Zero Centre for Doctoral Training, said: “Our battery-electrolyser shows how rethinking established technologies can unlock new pathways for clean energy access and hydrogen production – especially in communities that are often left behind.”

The chief financial officer of battery developer Microvast, Carl Shultz, has left the company less than four months after his appointment.

Microvast revealed his departure in a US Securities and Exchange Commission (USEC) announcement, saying Schultz had ceased to be employed as of July 29.

The reasons for his departure were not disclosed.

In a separate USEC announcement, on August 7, Microvast said its VP of corporate strategy, Rodney Worthen, had been appointed to serve as interim CFO.

Worthen joined the EV and ESS battery tech company in June 2023.

In May 2023, the US Department of Energy reversed a decision to award Microvast a $200 million grant to build a lithium ion battery separator plant, amid claims the company had links to China.

However, Microvast founder, chairman and CEO Yang Wu, an American citizen, said neither China’s government or the Chinese communist party had any ownership of the firm or influenced operations in any way.

Last January, Microvast said it had reached a significant milestone in development of its ‘liquid electrolyte-free true all-solid-state’ battery (ASSB) tech.

Unlike conventional lithium ion or semi solid-state (SSS) batteries, ASSB utilizes a bipolar stacking architecture that enables internal series connections within a single battery cell, the company said.

Lead has steadied near $2,000/t in the second half of 2025 after the April tariff fallout. A weaker dollar limited price declines, while industry fundamentals offered little support through the summer. The US continues to adjust to new government announcements — the most recent being lead making its way on to the country’s critical raw minerals draft list.

to dispel any market tightness.

stem downside movement.

We anticipate that next year will mark the fifth and final year of decline from the price highs recorded on the LME of 2021.

The European market is undergoing commercial shifts while record-low treatment charges threaten refined supply as margin pressure on primary smelters mounts.

LME lead prices steady, low volatility

The Singapore LME dominates warehouse holdings, with consistent flows in and out. This location accounts for 99% of the global LME stock total. CRU still attributes the inflows to financial players capitalizing on rent-sharing deals rather than positioning the metal for market needs, reinforcing the overhang that has weighed on prices and limited upside momentum.

Lead has steadied near $2,000/t in the second half of 2025 after the April tariff fallout. A weaker dollar limited price declines, while industry fundamentals offered little support through the summer. The US continues to adjust to new government announcements — the most recent being lead making its way on to the country’s critical raw minerals draft list.

Alongside other base metals, lead has been affected by the tariff announcement on April 2 by the US government, known as ‘Liberation Day’. After the announcement, the lead price fell significantly, moving to a low of $1,847/t. Over the past few months, the price has mostly been trading at around $2,000/t, and we forecast that lead will average $2,007/t in 2025.

Lead’s micro-industry picture has been less supportive of pricing as the mature recycling regions navigated the typically slower summer months. High exchange stocks also continue

Investor interest in the LME lead contract has briefly stirred to life. A flurry of activity in early July pushed the net position into positive territory and to a similar position last witnessed in the summer of last year.

Since then, the number of lots has increased to reach record highs but the net position identified by CRU remains in negative territory. We anticipate the price will find further support in the weeks ahead as the EU and US markets enter the autumn battery rebuild season.

While the industry picture has been less supportive, the macro-economic environment has been more so. A persistently weaker dollar has kept commodity prices buoyant, but in the case of lead this has only helped to

The European market is undergoing commercial shifts while record-low treatment charges threaten refined supply as margin pressure on primary smelters mounts.

Over the past few months, the price of lead has mostly been trading at around $2,000/t ... we forecast that lead will average $2,007/t in 2025

Chart 1: Three-month lead price sticks close to $2,000 /t

Chart 1: Three-month lead price sticks close to $2,000 /t

Through the turmoil surrounding the tariffs announced by the US in April, the replacement auto battery sector has taken up its traditionally macro-resilient role to support demand. The OE auto side is struggling on slower vehicle output. Lead’s majority share uses across its industrial, e-bike and, to a lesser extent, autos will continue to face challenges from a rising lithium battery market share.

Asia ex. China will account for over half of the global rise in demand out to 2030 and India will account for a majority of this. Demand growth is expected to be much slower in the more mature markets with the European and US markets accounting for 15% and 16% of the global total respectively.

Chinese demand is forecast to slow and subsequently contract towards the end of the decade as lithium battery technologies take further market shares in OE automotive and BESS.

In China e-bike trade-in policies have helped to offset weaker lead demand through the summer. This support will however diminish as lead’s low-voltage (12V) auto uses is lost to lithium batteries, notably LFP. Indian demand strength will be supported by healthy economic growth estimates, but also by embracing lead batteries to play a role alongside lithium batteries. In e-rickshaws powering India’s FAME revolution and even in BESS, as the renewable energy contribution to the grid starts to grow.

Growth of energy storage is primarily being driven by the economics of power storage, arbitrage, and grid balancing services. In major markets, a third of installations last year were standalone, i.e., not directly connected to renewable power installations. This will continue to be a key market segment this decade as grids deal with a growing share of intermittent supply.

Co-located solar and storage ratios vary by region. The US leads in co-location due to fewer crosscountry grid connections and statespecific storage policies. However, medium-term uptake estimates for the US have been reduced amid market uncertainty from reciprocal tariffs.

In highly interconnected grids like China, standalone storage plays a larger role in grid balancing. Uptake ratios are now expected to be higher in many other regions due to new PV and BESS mandates, funding, and giga-scale project announcements in India, Australia, and the Middle East.

Despite the removal of energy storage mandates and new grid pricing regulations in China earlier

We anticipate that next year will mark the fifth and final year of decline from the price highs recorded on the LME of 2021

this year, our forecast assumes that the significant growth in the solar PV sector will continue to drive utilityscale BESS installations.

Our bottom-up modelling shows that solar module and BESS costs and prices will stay low, driving expansion in regions with strong solar economics. Up to now, lead batteries have gained little from the battery storage boom, which is dominated by utility scale lithium, especially low cost LFP. Lead’s best opportunities

Investments are increasingly driven by geopolitics, electrification and technological developments. China is looking outward, which is changing metal supply chains and the industries they support.

Many other governments are looking to localize production and reduce reliance on China, compounding this change.

The pace of technological development is rapid, creating winners and losers. One only needs to look at the state of flux in automotive markets and energy systems to see how rapidly change is happening.

Yet, the material-intensive technologies of tomorrow will not look exactly like those of today. Material efficiency (thrifting), technological shifts and substitution are all key risks.

Getting the balance right between risks and returns is difficult.

Some investors will conclude other sectors offer higher returns on a risk-adjusted basis. However, commodity value chains are strategically vital — they are the building blocks of much of the economy and enable technological change.

Owning or controlling them brings geopolitical power and supply chain security. Metal market investments will be increasingly viewed through this lens.

China’s dominance in the global metals supply chain is a result of a multi-decade strategic plan and pressing macroeconomic necessities, which drove massive investments both domestically and internationally. If western governments want to catch up, then longterm policy stability is needed, but often this does not survive successive governments.

Metal market investments require long-horizon planning — for producers, consumers and investors, navigating this landscape increasingly requires balancing long-term vision with new policy and technology risks.

led

are in behind the meter applications, but CRU sees limited opportunity for this battery metal within this fastgrowing sector.

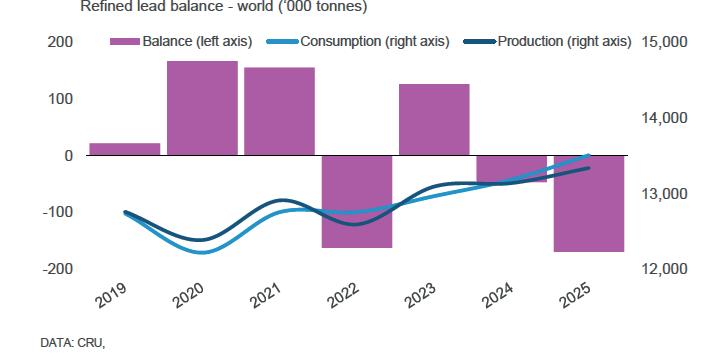

Global lead production is expected to exhibit growth of 1.5% y/y this year. This mostly reflects changes in China as smelters adjust to weaker demand as well as high feed costs. From next year, we expect that secondary production growth will modestly slow while primary will weaken.

The new forces rewriting demand

Governments are reprioritising economic security over efficiency, fundamentally altering investment flows and supply chains, and creating new ones.

This shift extends far beyond the energy transition. While electric vehicles and renewables remain important, technological change now includes robotics, automation, data centres and AI infrastructure, each with distinct material requirements that need to be captured in forecasts.

EMBEDDED IMAGE 3

Geopolitical tensions are redrawing the map of who invests what and where. For example, defence spending is increasing across major economies, and supply chain security is in focus. Climate change will also increasingly alter the nature of economies and investments; spending on both mitigation and adaptation will need to scale massively.

Consequently, industrial production as a share of global GDP is set to rise for the first time in decades.

Source: CRU

Investments are increasingly driven by geopolitics, electri fi cation and technological developments. China is looking outward, which is changing metal supply chains and the industries they support.

Many other governments are looking to localize production and reduce reliance on China,

Tel: 317.290.8485 | Email: sales@eagleoxide.com | www.eagleoxide.com

Primary growth will be constrained by tight concentrate availability until 2027–2030. Smelters, especially in China, are prioritizing silver over lead recoveries and are processing more lower lead content non concentrate feed to improve margins.

Secondary lead growth is likely to decelerate, reflecting smaller gains in lead scrap supply. This is tied to softer post pandemic lead demand and the rising penetration of lithium batteries in applications once dominated by lead batteries. In China lower scrap availability, due to import scrap bans, will limit feed and constrain production at a faster rate in comparison to the rest of the world.

Secondary lead output will be higher next year than this, but the outlook remains challenged by tighter scrap supply and rapid technology shifts.

Lithium battery chemistries, especially low-cost lithium iron phosphate, are displacing lead batteries across multiple segments as major cell producers and global automakers expand lithium-based starter, auxiliary, and industrial battery offerings. Chinese battery exports also mean more scrap arisings outside than inside China, constraining recycling feedstock.

This is already evident, with many major secondary smelters reporting scrap shortages, and in turn cutting production.

Asia will remain the region of higher growth for recycling, but this will be tempered by slower increases in domestic scrap generation, which

Growth of energy storage is primarily being driven by the economics of power storage, arbitrage, and grid balancing services … his will continue to be a key market segment this decade as grids deal with a growing share of intermittent supply

is lagging the pace of underlying lead battery demand.

Primary production in China is expected to decline more noticeably by the end of the decade. Policy will continue to encourage higher recycling, but tightening scrap feed makes this increasingly difficult.

Primary smelter capacity will be needed to bridge the gap and support demand, though not at the previously anticipated volumes. Smelters are likely to maintain a more diversified feed mix, processing complex concentrates alongside scrap and residues.

Resilient outlook for lead

Lead is entering a small global deficit phase on account of struggling Chinese producers facing a slack demand picture and tightness of feed. This is mostly evident on the secondary element of the market, but feed issues remain wholly relevant on the primary side of production too.

The closed-loop recycling has helped and will continue to stabilise nominal lead prices, though inflationadjusted prices have trended lower since 2007. Investor sentiment

Asia ex. China will account for over half of the global rise in lead demand out to 2030 and India will account for a majority of this

IMAGE no 2 here

Chart 2: Deficit deepens on Chinese production cuts Data: CRU

The global energy transition remains underway, although its pace may be slowing due to economic and logistic headwinds. Multiple battery

toward lead batteries within the energy transition remains cautious, which caps near-term price upside, though there are signs it may be improving. Steady demand and wellestablished infrastructure continue to reduce downside price risks for lead.

The global energy transition remains underway, although its pace may be slowing due to economic and logistic headwinds. Multiple battery technologies will likely be required to meet diverse use cases. Lead batteries may continue to play a role given their existing infrastructure, reliability, and established applications. However, growing competition could challenge lead’s market position. Ultimately, the future role of lead will hinge on market dynamics, technological advances, and policy decisions.

James Griffiths is a key member of CRU’s markets and forecast team and a major contributor to the company’s lead market analysis. He is the lead and editor of CRU’s Lead Monitor and Lead Market Outlook, providing in-depth insights into the lead market.

EnerSys has announced a $1 billion increase to its shares buyback program to be completed over the next five years.

The lead and lithium battery giant announced the board’s authorization for the program, along with a quarterly dividend increase of 9%, on August 6.

The move came just days after Batteries International reported EnerSys was cutting 575 non-production jobs as part of a restructuring plan aimed at securing $80 million in annualized savings.

On the new stock buy-back program, EnerSys said repurchases would be made from time to time on either the open market

or through privately negotiated deals.

EnerSys said the timing, volume and nature of share repurchases would be at the sole discretion of its management, dependent on market conditions, applicable securities laws, and other factors, and may be suspended or discontinued at any time.

The company said it could give no assurance that any particular amount of common stock would be repurchased.

In a related August 6 announcement, EnerSys reported increased first-quarter revenue for fiscal 2026, buoyed by the firm’s acquisition of portable power firm Bren-Tron-

ics, strong datacenter demand, and a rebound in the US telecoms market.

Revenue rose 4.7% yearon-year to $893 million. Adjusted diluted earnings per share was $2.08, up 5% from the previous year. However, basic earnings per share, excluding tax credit benefits, fell 6% to $1.11.

Chief financial officer, Andrea Funk, said the first quarter had been hit by tariff-related delays in customer purchasing, such as in the forklift and transportation markets, plus foreign exchange pressures.

EnerSys president and CEO Shawn O’Connell said earnings growth, strong cash flow and a solid

balance sheet enabled the firm to continue investing in long-term growth while returning more capital to shareholders.

He said the stock repurchase authorization reflected the firm’s belief in the value of the company and its growth trajectory.

“At the same time, we are committed to maintaining a competitive dividend that grows with our earnings, excluding the effects of 45X (federal clean energy tax) benefits. During this period of macro uncertainty, we intend to keep our leverage below the low end of our target range, retaining a prudent level of dry powder for future capital allocation optionality.”

Asia-based battery giant Leoch is mulling a possible expansion of production at its Mexico plant even before it opens — plus a potential new factory in the US.

Company chairman Dong Li revealed on August 29 the company had launched feasibility studies on the capacity expansion in Mexico, which is set to start-up in the fourth quarter of this year.

The possible opening of a US plant could underpin the long-term development of business in the American market, but Leoch did not disclose potential battery-making capacities for Mexico or the US.

The studies were announced as Leoch posted interim results for the six months ended June 30 showing a fall in profit of more than 71% compared to the same period last year — which was in line with a profit warning issued earlier this year.

However, Leoch’s network power battery business accounted for nearly 41% of the group’s

total sales during the period, with sales revenue of Rmb3.4 billion, representing a 9.4% year-onyear growth over the same period last year.

The increase was mainly driven by the rising demand for UPS batteries in datacenters as a result of the growth in cloud computing, 5G networks and digital transformation initiatives.

Leoch said it continued to have a solid presence in the datacenter and other

Microporous has marked the formal opening of its new lithium ion battery separator manufacturing line in Tennessee with a ribbon-cutting ceremony.

The company announced the opening in a Facebook post on August 7.

CEO John Reeves said the line was designed to manufacture battery separators for EVs and backup power, in support of green energy and reducing emissions.

Batteries International reported last January that

areas of the network power battery market, offering high-quality lead acid and lithium ion batteries tailored for critical power backup applications.

Looking ahead, the company expects demand for lead-acid batteries in UPS applications to grow as the global dependence on digital infrastructure expands.

Sales revenue of the SLI battery business, the second largest revenue contributor to the group, accounted for

Microporous had been awarded a $100 million US federal grant for its ultra-thin, coated wet-process polyethylene (PE) lithium battery separator facility.

Reeves said the company had started looking into the expansion nearly three years ago, Reeves said. The Microporous board gave the green light to fund the project around a year ago.

“Our long-term investment for green energy is about $1.3 billion, and

37% of overall sales with Rmb3.1 billion, representing a year-on-year growth of 9.6%.

Leoch said the increase was mainly driven by increased vehicle production, especially in emerging markets like India, Southeast Asia, and South America.

The group’s recycled lead business posted sales revenue for the period of Rmb1 billion, which was a yearon-year increase of nearly 47%.

this is the first step in this investment.

“This is a full manufacturing line, representing over $20 million in investment, and when it’s fully up and functional, it will represent about 50 new really good jobs for this area.”

Board member Ray Desrocher said further investment is being made in Danville, Virginia, where the company is building its high-volume coated PE lithium battery separator production in Virginia.

Exide Technologies confirmed in October it is pushing ahead with its closure of a lead battery production plant in France.

A company spokesperson said it was actively seeking unspecified ‘industrial players’ interested in establishing operations at the site in Lille.

The move comes just weeks after Ecobat announced it was halting its battery recycling and speciality lead manufacturing operations in France, followed by the sale of its

lead battery and polypropylene recycling operations in Italy.

Exide had already said in June that it planned to cease operations in Lille following a “thorough review of the economic realities, market attrition, and overcapacity in the industrial traction battery industry”.

But the battery manufacturer said it was committed to the process of finding a buyer under France’s ‘Florange’ law — which requires any firm bidding to take over a site to discuss

their plans with workers’ representatives.

Bidders who refuse to divulge their plans or are later to be found to have withheld their intentions may face prosecution.

Meanwhile, Exide said it is developing a jobs protection plan that includes internal and external redeployment opportunities. This aims to help the 200 or so employees likely to be affected by Exide’s pull-out to receive support in finding new careers.

Laurent Wieczorek,

senior VP for motion and recycling said: “The battery industry is changing significantly and rapidly. The economic challenges have become increasingly difficult to overcome.

“Although this is a difficult announcement, we remain committed to transparency, social responsibility and ongoing dialogue with all relevant stakeholders throughout the information and consultation process. Our intention is to ensure a structured process.”

EnerSys has received a tax refund of around $140 million plus interest thanks to the sale of batteries.

Batteries International reported last year that the US-based firm was in line for an unexpected boost, after the federal government unveiled proposed new guidance on battery components and materials qualifying for tax credits.

Now, in a statement released on August 27, EnerSys confirmed it had received its fiscal 2024 US tax return refund of $137

million, plus accrued interest.

The refund is associated with sales of batteries EnerSys produced in the US which qualified for credits under section 45X of the Advanced Manufacturing Production Credit (AMPC) program — part of the Inflation Reduction Act.

Section 45X provides AMPCs for battery cells and battery modules produced in the US with an energy density of not less than 100 watt-hours per litre. Cred-

European metals recycling and speciality chemicals group Campine has launched a probe into the alleged resale of its products into Russia.

Belgium-based Campine, which is about to acquire Ecobat’s French battery recycling and speciality lead manufacturing operations, revealed the allegations in a statement released on August 15.

Campine, which acquired two lead battery recycling plants from French recycler Recyclex in 2022, said it was committed to ensuring compliance with applicable

laws, including sanctions and export controls laws.

“We are working with external legal counsel to address the issue, including assessing whether it is appropriate to further enhance compliance measures and what the next steps should be,” the firm said.

The company halted all sales to Russia following the outbreak of the RussiaUkraine conflict in March 2022 and said it took allegations that its products have been resold to Russia by third parties “very seriously”.

its are determined based on sales of qualifying products produced in the US from January 1, 2023 until December 31, 2032.

EnerSys had said previously that its analysis of guidance released in December 2023 by the US Treasury and Internal Revenue Service indicated the battery maker could expect annual tax credits recorded as a reduction to the cost of goods sold, and not subject to taxation, to be in the range of around $120 million to $160 million up to 2032.

Earlier in August EnerSys announced it was to cut 575 non-production jobs as part of a restructuring unveiled on July 22 aimed at securing $80 million in annualized savings.

Shawn O’Connell, who succeeded David Shaffer as president and CEO this May, said the “difficult” decision to axe jobs — primarily in corporate and management positions — was a necessary move to stay competitive.

The cuts represent 11% of the US-based battery manufacturing giant’s non-production global workforce.

EnerSys said it expected the shake-up to be

“substantially complete” by the end of the second quarter of fiscal 2026, subject to local law requirements. Combined with other “non-headcount-related actions”, these changes are expected to result in about $80 million in annualized savings starting in fiscal 2026.

EnerSys said the estimate comprises around $70 million in savings, representing a reduction of over 10% of the company’s fiscal 2025 operating expenses, as well as an estimated $10 million reduction in the cost of goods sold.

The firm expects to realize about $30 million-$35 million of savings in fiscal 2026, with material benefits beginning in the third fiscal quarter.

The company revealed this May that its stock lost and regained $900 million in the marketplace over a three-month period amid the recent flurry of US trade tariff announcements.

That came after EnerSys announced the closure of its flooded lead acid battery manufacturing facility in Monterrey, Mexico and a production switch to its existing Kentucky plant, while expanding capacity in the US and Europe.

International press conference on a unique form of alternative energy

Andy Shih, head of the LumiFusion Green Energy research team, will present a talk and proof of concept experiment to demonstrate the potential of Mt Fuji’s volcanic rock to become one of the cleanest, renewable energy sources in the new era.

This revolutionary technology, developed by the LumiFusion Green Energy research team, is ready to bring innovative solutions to the global energy crisis and climate change.

Since 2017, the LumiFusion research team has discovered that the environment in which the Earth’s matter exists is full of diversified energies, and it has actively sought ways in which to effectively use these energies.

Location: Marriott Hotel, Osaka, Japan

Date: December 12, 2025. Time: 14:00

For further information please contact: Amanda Chiu: actwgb@gmail.com

Lead acid batteries will continue to be the mainstay of GS Yuasa’s global business beyond the next decade, the corporation’s president has said.

Takashi Abe, who was appointed president last year, said in a report released on September 30 the Japan-based battery giant expected demand for lead acid to remain strong, “at least through 2040” — continuing to provide a solid foundation for business performance.

The report, which covered the fiscal year ended last March, said demand for automotive lead batteries should remain steady and centered on the replacement market.

Considering current demand trends and advantages in cost and recycling, Abe said Yuasa forecasts that demand for automotive lead batteries will

remain at around 90% of current levels even in 2035.

Similarly, demand for motorcycle lead-acid is expected to continue expanding, particularly in the ASEAN region.

“In Japan, we are actively advancing our business continuity plan to build a system capable of manufacturing products of the same quality at any of our manufacturing sites in eastern, central, or western Japan, so that customer production lines will not be stopped under any circumstances, including disasters.”

Abe revealed that the company is also considering a fresh investment boost in production overseas, “as an option to further strengthen our market position”.

Abe said in fiscal 2024, the second year of its sixth mid-term management plan, operating profit

exceeded both the initial target and the upwardly revised target, marking the firm’s third consecutive year of record-high profits.

Profit before amortization of goodwill, which had remained at the JPY 20 billion ($131 million) level through fiscal 2021, rose to JPY 30 billion the following year, JPY 40 billion in 2023 and JPY 50 billion in fiscal 2024.

“This is evidence of our performance improving steadily, step by step,” Abe said.

However, Abe warned that current US trade tariffs were “shaking the global economy”. But as Yuasa’s business centers on local production for local consumption, he said the impact of tariffs would be limited.

Nevertheless, there is some risk of a fall in exports from Japan and Southeast

InoBat secures €55m loan and grant deal for Spanish gigafactory

The Spanish government said on September 8 it had awarded Slovakian EV batteries developer InoBat a grant of €54 million ($64 million) and a loan of €456,000 to set up a gigafactory in the country’s northwest.

InoBat has indicated previously that the plant, in Valladolid, will need an investment of more than €700 million to produce its lithium-based EV batteries. The gigafactory is

Energy Vault said on August 7 it had entered into an exclusivity agreement for a $300 million preferred equity investment to launch a subsidiary focused on developing, building and operating energy storage systems.

The proprietary battery,

expected to be operating by 2027 with a production capacity of 32GWh and to ramp up further by 2029.

The industry and tourism ministry said it has awarded a total of nearly €2.5 billion to date to 300 companies involved in the rollout of electric and connected vehicles.

Other companies to benefit from support for projects in the country have included PowerCo, Stellantis and Renault.

gravity and green hydrogen ESS company said the new Asset Vault subsidiary would accelerate 1.5GW of energy storage projects globally.

Asset Vault will consolidate Energy Vault’s growing portfolio of contracted and operational storage projects, the firm said.

Asia to the US.

Abe said the worldwide downturn in sales of EVs and a slump in the lithium market had been felt by the corporation.

He said Yuasa was seeing a decline in sales and profits for automotive lithium ion batteries, which meant improving profitability in that sector would be a “challenge” for the foreseeable future — revising forecasts made earlier this year.

ExxonMobil acquires Superior Graphite to enter battery anodes market

Oil and gas major ExxonMobil has acquired privately-owned US-based Superior Graphite for an undisclosed sum.

In September 2023, InoBat formalized a collaboration agreement with Echion Technologies to study how Echion’s niobium-based XNO anode material could boost battery performance.

InoBat said then it was about to start R&D into using XNO, which it claimed could lead to lithium ion batteries that deliver high power across a cycle life of more than 10,000 cycles.

Within the initial $300 million investment, Asset Vault is expected to generate more than $100 million in recurring annual EBITDA in the coming three to four years as a consolidated subsidiary — in addition to Energy Vault’s existing ESS business.

Exxon confirmed on September 9 that it was acquiring key assets and technology of Superior Graphite, ahead of the fossil-fuel giant’s planned entry into the battery anode graphite market.

Synthetic graphite powers EVs and BESS systems and Exxon said the move marked a major milestone in its strategy to build a robust, synthetic graphite supply chain in the US.

Exxon said it believed synthetic graphite can play a critical role in the energy transition and the firm expects the demand for higher performance batteries will continue to grow, increasing demand for higher performance graphite materials.

The company said synthetic graphite was a game-changer because, compared to traditional mining operations, it is less labour-intensive, more consistent in quality, and can be made with carbonrich feedstocks from Exxon’s existing refining streams.

Switzerland’s SUSI Partners is to be acquired by UK-based Gresham House Holdings for an undisclosed sum, in a move aimed at expanding investment in the global BESS and energy infrastructure markets.

The energy sector-focused investment firms said on September 19 SUSI’s investment strategies, products, and portfolio management teams will be combined with Gresham’s UK-focused BESS-led energy transition infrastructure division.

This will more than double the division’s size to around €3.1 billion ($3.8 billion) in assets under management. On completion of the deal, the newly combined division will be led by SUSI’s CEO, Marco van Daele.

SUSI’s portfolio management leads and teams will manage the firm’s existing equity, credit, and Asia

strategies, while Gresham’s UK-focused strategies will continue to be managed by the firm’s team.

Gresham CEO Tony Dalwood said global investment in the energy transition reached a record $2.1 trillion last year and would need to rise to $5 trillion annually by 2035 to achieve net zero emissions by 2050.

“The acquisition of SUSI Partners will strengthen our ability to meet this demand across equity and credit, combining market-leading expertise with deep local knowledge in Europe and Asia.”

Dalwood said the deal will also expand Gresham’s geographic reach and spur a wider range of strategies, such as co-investment opportunities.

“Together, we will be better placed to deliver financial returns by investing in the global themes shaping the future.”

Swiss ‘membrane-free’ RFB tech secures pre-seed finance

Unbound Potential, a Swiss newcomer to the flow battery market, has raised nearly €15 million ($18 million) in a pre-seed financing round.

Unbound said on September 19 the financing, comprising around €8 million in non-dilutive grants and €6.4 million in additional funding, will spur development of its membrane-free, redox flow battery tech as the firm seeks to be a player in the energy storage market. It describes itself as a “platform solution, compatible with different chemical systems”.

The company will demonstrate its system in pilot projects, including a collaboration with Amazon on logistics electrification and discussions with FlexBase for Europe’s largest

Flexgen Power Systems said on August 6 it had been given court approval to acquire a substantial portion of the business of US-based BESS developer Powin.

Batteries International reported in June that Powin had voluntarily filed for Chapter 11 protection under the US Bankruptcy Code in the District of New Jersey.

Powin said the decision was part of moves to tackle financial liabilities and secure its core businesses — which would include spinning off a new business entity to encompass its existing monitoring and energy services operations.

Now BESS tech company Flexgen said it will own all of Powin’s IP, including hardware and software IP and information technology systems, plus a significant spare parts inventory.

Once the acquisition is finalized, FlexGen will support over 25GWh of

redox flow storage project.

A pilot plant is scheduled to start operations in mid-2026.

Unbound said flow battery stacks with increased liquid storage are the ideal foundation for supplying the rapidly growing demand for long-duration energy storage.

Traditional stacks rely on “fragile” 2D membranes, made of hundreds of layers that are costly to produce and difficult to scale, according to Unbound.

The start-up said it has solved this problem by eliminating the membrane entirely, “reducing the stack to just two robust parts. This radically simple design enables fast, cost-effective production using existing industrial processes — no specialized, fragile components required.”

battery energy storage systems and 200 projects across 10 countries in its portfolio.

FlexGen said it would draw on its 15 years of integration experience with over 65 configurations from 22 global vendors to support Powin customers.

FlexGen CEO Kelcy Pegler said: “This is a significant milestone, not just for FlexGen, but for the entire industry, as storage is no longer a nice-tohave, but rather, essential to meeting global energy demand and opportunities.”

In May, Powin unveiled its ‘Pod Max’, which the company said was its most powerful and energy-dense product to date.

Delivering 6.26MWh of capacity in the same 20-foot liquid-cooled container as previous models, the Pod Max offers a 25% increase in energy density over Powin’s standard 5MWh system.

Metair’s Rombat, First National, post mixed H1 results

South Africa’s Metair Investments has announced mixed results for its battery production companies Rombat and First National Battery for the first half of this year ending in June.

First Battery in South Africa posted a slight fall in sales to around 770,000 batteries over the period, compared to 786,000 in the same period last year, Metair said on August 7.

However, sales at Rombat in Romania improved by around 6% to nearly 1.5 million compared to the year-ago period.

Metair said Rombat’s performance was under-

pinned by an improvement in local automotive aftermarket and original equipment manufacturer (OEM) sales.

Meanwhile, the group said the sale last December of its Mutlu Akü Turkish lead acid operation had significantly derisked the balance sheet.

Following that sale, and the acquisition of South African car parts firm AutoZone, Metair restructured its operations into two core units — the OEM direct component manufacturing segment and the aftermarket parts and retail segment, which includes battery manufacturing.

Batteries International flew to Malta to meet a company that continues to prove that focusing on research and development is the clear path to product innovation and profits.

In diversity lies strength. It sounds like a Soviet-era catch phrase from a couple of generations ago. But in an odd way this is the only way to define Abertax, a veritable Maltese powerhouse of energy related ideas and energy storage businesses.

At the heart of Batteries International visit to the firm, there are three figures: Joseph Cilia, chairman since 2019, George Schembri, the president and Malcolm Tabone, the CEO.

The ideas man is Cilia, a university professor-turned-entrepreneur who has been connected to the firm and its founder Werner Schmidt and co-founder Martin Florin since almost the beginning, next is Schembri, now semi-retired who knows the business inside-out and has helped shape the company from 2003 when there were only five employees; and finally is Tabone who brings an extraordinary gift of converting ideas into designs and designs into manufactured products.

The first iteration of Abertax derives from when Werner Schmidt, a German businessman on holiday in the Mediterranean, had an accident and was forced to berth his yacht in the port at Valletta, the capital of Malta. He liked the island. Very much. It was 1985 and in a nod to

sentiment named his new company on his berth number in the port: 14 — sounds like Abertash in the Maltese language (but spelt with an ‘x’ at the end, hence incorrectly Anglicised to Abertax).

He set up various modest businesses there, including a small injection moulding company which started to prosper.

Two things emerged from his quality-oriented attitude and professional advice. The first was Abertax has a quality culture of testing its products that is probably second to none. The second, equally genetic in the firm’s psyche, is an obsession with being self-reliant.

With a quite extraordinary anticipation of the need for manufacturing independence, the founder of the firm Schmidt, who passed away in 2015, saw that the way forward for a small Maltese firm sitting in the middle of the Mediterranean was to be able to design and make its own products and machinery.