Hammond’s innovative signature products, GravityGuard® and Treated SureCure®, are two of more than 150 customized additives that are improving battery performance and lowering manufacturing costs for battery manufacturers around the world.

Hammond has released a comprehensive whitepaper detailing exciting findings of new benefits of the antistratification additive GravityGuard ® New research shows that the BCI Innovation Award winning product also offers significant serendipitous improvements that may provide additional value to battery manufacturers and their products. Specifically, the results show GravityGuard® used

in the PAM and NAM can improve CCA performance, 2C Capacity, and extend PSoC Cycle life. The paper presents notes on evaluation methods, specific comparative data, and more than a Independent GravityGuard ® Testing Reveals Improved CCA & PSoC Cycling

dozen charts and graphs with detailed analysis of a wide variety of test results. A PDF is available online. Just snap the QR code above to go to the publication download page.

Mike Judd says he lives, eats and breathes batteries. But when Shona Sibary delved a bit further she discovered that the CEO of one of America’s largest lead battery manufacturers also has eight women in his life … and a penchant for Route 66.

EDITORIAL 4

Shifting invention to innovation — how to beat first-mover advantage

8

Clarios celebrates 15 years of Meadowbrook LTO production • Fischer succeeds Riske as Sunlight Group chairman • Hoppecke celebrates 40 years of US operations • Nourhan Moustafa joins Hammond in senior EMEA sales position • Shona Sibary takes over as next editor of Batteries International • Pruitt to head East Pennboard in leadership shake-up • Clarios’ Rosenkranz joins BCI board • New energy storage trade body launched in UK • O’Connell takes helm of EnerSys • Walker appointed as Metair’s new CFO

Study highlights concern over EU-China battery investments ‘paradox’ • Landmark US BBA is ‘harbinger' of challenges for ESS investors • EnerSys to cut management jobs in annual savings bid • Leoch profit warning over US tariffs, Mexico start-up delayed • US line Matson suspends EV shipments over battery fire risks • Insurer rolls out BESS cyber-attack protection • EU waste firms ‘refused insurance’ over Li battery fires surge • Insurer’s UK alert over ‘worrying surge’ in Li battery fires • Industry looks to extend US battery expander R&D support • Exide Industries CEO says lead and lithium in line for boost • Clarios plans supercap pairing with AGM batteries • Clarios to open advanced R&D and training center for batteries • Lead batteries can ‘outpace market’ in key areas, says KPMG • China backs $6bn Indonesia EV battery, minerals project • Sumitomo receives more LDES/flow battery orders • UK’s Faraday backs Na-ion battery tech project for Africa • Google invests in LDES with Energy Dome’s ‘CO2 Battery’ tech • Banner hails lead battery tech as sales and revenue grows • CATL in battery tech agreement with BHP • EU accepts battery material supply deals beyond its borders • China tightens rare earths grip • Powin files for Chapter 11 bankruptcy, plans spin off • ‘Grid-forming’ BESS tech ‘needs $1.2tn boost’ to support renewables • Cabot extends Li sector reach with new conductive carbon for ESS •

BATTCON: CBI PICKS UP THE TECHNICAL BATON 14

"We took over the conference because it will advance the future of battery technologies," says CBI's Matt Raiford and Alistair Davidson

Investors beware. There are too many gigafactories chasing not enough money, something has got to crack

From caffeine to cars — blazing a paper trail

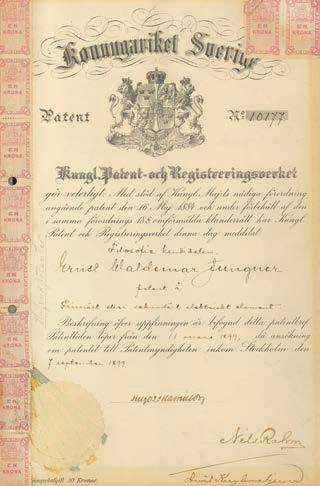

By the time the inventor of the nickel cadmium battery, Jungner, died aged 55 he had provoked a complete rethink of many of the ways we look at battery chemistries

DEVELOPMENT

• Squuezing money from the biggest of the big boys 63

• International and national development banks can nevefrtheless sometimes be a useful tool in financing some of the world’s more challenging energy storage projects

Ecobat follows up French sale with Italian market exit with lead operations sell-off

• New Gopher video showcases lead’s circular economy • Gravita planning new lead recycling plant in India • First eight lead battery certification program peers named • Further rise in refined lead metal supply surplus • Ace Green, Enecell in Australia lead master offtake deal

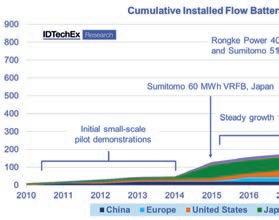

An industry on the cusp — this year’s meeting of flow battery professionals turned out, yet again, to have a whiff of optimistic expectation in the air. It was well worth attending.

Batteries International’s invaluable round up of the exhibitions, conventions and events that are key to connecting and driving the industry forward.

• Roger Winslow, at the heart of the lead battery industry for five decades

• Imre Gyuk, the visionary champion of battery storage who set the agenda for the US DOE.

Publisher Michael Halls

editor@batteriesinternational.com +44 7342 890 592

Editor Shona Sibary shona@batteriesinternational.com +44 7585 280152

Finance administrator

Juanita Anderson

Juanita@batteriesinternational.com

Subscriptions, enquiries

subscriptions@batteriesinternational.com admin@batteriesinternational.com

Production/design

Antony Parselle aparselledesign@me.com

Content researcher Matt Halls Matthew@batteriesinternational.com

Our battery test systems are renowned for their high-speed data acquisition and control, ensuring precise measurements critical for medical device applications.

The Series 6000, our next-generation battery tester, exempli es this with its advanced capabilities designed to meet current and future testing demands

Designed to support a wide range of applications, our battery test systems are chemistry agnostic, making them suitable for testing everything from small coin cells to large EV batteries.

This versatility ensures consistent performance across various testing scenarios, a crucial factor for medical device manufacturers who require dependable equipment.

Our comprehensive software suite, including tools like MacTest and MIMS Server, provides robust data management and traceability features.

These tools enable detailed tracking and analysis of testing processes, ensuring compliance with stringent medical industry standards and facilitating quality assurance.

Our worldwide customer service team is ready to handle upgrades, service, and repairs directly at your location, eliminating the need to ship your equipment. This minimizes downtime and enhances e ciency.

4322 South 49th West Avenue | Tulsa, OK 74107

Phone: (918)446-1874 | sales@maccor.com www.maccor.com

Mike Halls • editor@batteriesinternational.com

Good idea. Perhaps even a great one. But lousy leadership. The man who revolutionised mass transportation with the movable car assembly line — and even gave rise to the troubled dreams of an entire nation — was basically an ignoramus.

Henry Ford, in the words of one historian, was “barely educated and close to functionally illiterate… he did not like bankers, doctors, tobacco, pasteurised milk, liquor, overweight people, JP Morgan & Co, tall buildings, college graduates, Roman Catholics or Jews … he seldom let facts or logic challenge the certainty of his instincts.”

His leadership skills essentially were an opinionated misguided form of bullying. His choice of senior management was flawed at best and mostly catastrophic. Ford wanted to micro-manage everything.

Yet within a decade he had created an empire of more than 50 factories on six continents, employed 200,000 people and produced half of the world’s cars.

The oddest thing about Ford’s success was that his staple product, the Model T, was not even particularly good.

Ill thought-out

Everything about it was rudimentary and, by today’s standards, appallingly ill-thought out. There were no fuel or oil gauges. Why should anyone need a speedometer too? (Though that was added after a while.) The gravity-fed fuel system meant that the car sometimes had to be driven in reverse to climb hills, the headlights were either too dim or blew at speed. There were even two sizes of tyres for back and front.

With the same convoluted logic the preceding series of Model Ts went A, B, C, E, N, R, S and K.

That said, it was the first of its kind giving Ford market leadership … But it was inevitable that it could only be temporary.

If invention is the creation of something new, innovation typically is finding new ways of commercialising that invention — it could be improving the products, the manufacturing processes, even changing markets.

Henry Ford’s huge revolution in car making

— by the late 1920s there would on average be almost one car per family across the US — was quickly copied by other firms.

And then improved upon it. Innovation.

Two firms in particular — General Motors and Chrysler — looked at all the things the Model T lacked and rethought both the final product and the way it was produced.

In the case of GM the process of innovation came with the clear focus on leadership at the very top.

So enter Alfred Sloan, who became CEO in 1923 — and coincidentally had worked as a supplier to Ford — whose management style looked at both markets and technology. In terms of production he surrounded himself with more-or-less autonomous competent managers and gave them leeway to run operations as they saw fit.

Sloan also instituted a sophisticated advertising campaign to make the public aware of what GM had to o er, and instead of stressing cheap prices, Sloan built demand for GM products by stressing style, comfort, and status, capturing his sales philosophy in the slogan “A car for every purse and purpose.”

He also introduced the idea of planned obsolescence — the release of the annual model change. Fashionable cars!

Another genius idea was a pricing structure which he referred to as “the ladder of success”, whereby models would reflect owners’ buying power and preferences changed as they aged. The Chevrolet was the cheapest, the Cadillac the most expensive.

In 1919, he and his corporate deputies created the General Motors Acceptance Corporation, a financing arm that practically invented the auto loan credit system. This allowed car buyers to short-cut the time required to buy a Ford car.

Sloan created a fortune for his shareholders and himself — he went on to become a philanthropic giant — and built an empire that until recently could claim to be the largest industrial enterprise the world had ever known.

Chrysler, founded in 1925 but operating in

various guises before this, took a slightly di erent approach. It looked at Ford’s vehicles and sought ways of improving them. New functionality included a carburettor air filter, high compression engine, full pressure lubrication, and an oil filter, features absent from most autos at the time. It also included the first practical mass-produced four-wheel hydraulic brakes.

The firm’s profits were such that it went on to build the Chrysler building in New York, which for 11 months in 1930 made it the tallest skyscraper in the world.

So how do the history of these firms relate to the present battery and EV industry?

If you look aside from the world of the lead acid battery, the present challenge for the North American and European battery industry is a geographic one and largely a problem of its own making.

Put at its most simple. Chinese firms have taken the high ground and are producing, arguably the best EVs in the world in terms of quality and value for money. They are powered by the most competitively priced and competently produced lithium battery packs. Firms such as BYD and CATL in as little as 15 years have become world class heavyweights.

A lack of foresight

plot when it assumed it would be a natural fit to move into the personal computing space.

Those accolades could have gone to Western firms — as this column has mentioned on various occasions — if they had had the foresight and support that the Chinese government gave the industry.

In 1992, China’s eighth five-year plan talked about the proposed creation of a so-called New Energy Vehicle. While most of the rest of the world was pussy-footing about, China was able to showcase a fleet of 50 lithium battery powered electric buses, with a range of 130km, at the 2008 Olympics.

So where’s the relevance of Henry Ford and Alfred Sloan to the present Western battery impasse?

It’s simply this. All empires come to an end. All technologies succumb to newer and better innovations. Moreover, the pace of progress is faster than ever.

The history of technology, as well as the history of business, shows that business empires rise and fall. IBM, which had become the huge giant for main frame computing in the 1960s lost the

It partnered with Bill Gates — who realised that software would become more important than hardware — and the rest of course is history and the massive success story that is Microsoft. Today’s battery industry needs to foster innovation not hide behind protectionist walls. In the end these barriers will eventually stifle competition and shield businesses from the economic realities that drive change. Where this will come from is uncertain — the most likely route is from a new battery chemistry or technology.

Some of the leadership is here already. Our recent interviews with Stryten CEO Mike Judd (featured in this issue) and that of Varta’s Michael Ostermann (issue 135) show that some of the top battery-people have vision in buckets and see a sense of direction — something Henry Ford stumbled with for many a year.

Last, innovation can be a two-edged sword. Perhaps the most deadly innovation for motorists came in 1928. The first proper cigarette lighter for cars was patented that year by the Connecticut Automotive Specialty Company. Casco went on to invent the modern lighter that bounces out when ready.

Odd that such a small invention would promote the death of millions.

Mike Halls, editor-at-large

East Penn Manufacturing is to separate the roles of president and CEO later this year as the well known and popular Chris Pruitt retires from the posts.

Pruitt, 63, will continue as president and CEO until September 29, when he will become executive chairman of the board, East Penn said on June 13.

E ective from September 29, Pete Stanislawczyk will be promoted to CEO and Christy Weeber will be promoted to president.

Pruitt has worked as president and president/CEO for 11 years and has been

with the company for over 31 years, holding several financial posts including CFO.

Stanislawczyk, currently executive VP and CCO, has been with East Penn for 33 years and is a former senior VP of transportation and diversified sales.

In his new position, he will oversee the operations and commercial areas of the business, which includes manufacturing and distribution, engineering, sales and marketing as well as serve on the East Penn board.

Weeber, who has been with the company for 13

years, is EVP and CFO. She was formerly the senior VP of finance.

In her new position, she will oversee finance, legal, personnel and IT as well as serve on the board.

Pruitt said: “I have high expectations for the future of the company. Pete and Christy will carry on the legacy and mission of East Penn alongside a very accomplished management team and the full support of the founding family.”

Battery Council International president and executive director Roger Miksad said: “Chris has given so

A new trade body has been launched in the UK to champion the energy storage industry.

Energy Storage Association UK said on June 25 it aimed to drive innovation, investment and policy to unlock the full potential of storage solutions including batteries, pumped hydro and hydrogen-based technologies.

Founding members of the body include GivEnergy, Sunsynk, Powervault, Octopus Energy, Keele University and Durham University. The body cited a study

by Imperial College, which found that that e ective energy storage could save the UK between £500 million ($620 million) and £3.5 billion annually.

At present, the cost of energy curtailment added between £400 million and £920 million to energy bills last year, according to the study.

Association interim CEO Jason Howlett said: “Our vision is simple: we see a world where energy storage is allowed to lower consumer costs, stabilize the grid and accelerate the transition to net zero.”

Howlett said energy storage is not just a technical solution but a necessity for delivering dependable, a ordable, clean energy from renewables where and when it’s needed most.

much to the battery industry over 30 years of service, and was duly honoured for this work as a recipient of our Distinguished Service Award in May.

“We look forward to a bright future at East Penn with their newly appointed CEO and president and continued partnership and growth for the energy storage industry.”

Battery Council International has welcomed Clarios senior executive Christian Rosenkranz to the trade organization’s board of directors.

Rosenkranz, VP of industry and corporate a airs EMEA and MD of Clarios Germany, is an industry veteran of 27 years.

BCI announced Rosenkranz’s board role in a LinkedIn post on June 16.

His experience includes posts with VARTA and Johnson Controls and he is also chairman of the Consortium for Battery Innovation, having been appointed in 2021.

Rosenkranz’s background also includes leadership roles in lithium ion system integration, global engineering component development, and sustainability initiatives.

Emma Nehrenheim has been named as managing director of the European Battery Alliance.

The Alliance said on June 6 that Nehrenheim has more than two decades of experience in environmental engineering and battery manufacturing.

Most recently, she was chief environmental o cer and president of Northvolt Materials. She also contributed to the development of the EU’s Battery Regulation.

She succeeds Thore Sekkenes, who has led the industrial stream of the Alliance for more than six years and will continue to remain actively involved

with the organization. Nehrenheim said: “Our mission isn’t just to build a battery industry, but to make it European, shaped by our standards, driven by our innovation, and powered by our industrial strength.” The Alliance was launched in 2017 by InnoEnergy with the backing of the European Commission. The body is now known as EBA250, in recognition of the estimated €250 billion ($290 billion) annual value of Europe’s battery market by 2025.

Shawn O’Connell, formally took over as president and CEO of EnerSys on May 23. He takes over from Dave Sha er who announced his retirement and O’Connell’s appointment in December.

He was previously chief operating o cer from November 2024. Before that he was president, Energy Systems Global from November 2023 and president, Motive Power Global from July 2020.

Earlier work positions include president, Motive Power Americas from April 2019 and vice president — Reserve Power Sales and Service for the Americas from February 2017 and vice president of EnerSys Advanced Systems from December 2015.

He joined EnerSys in March 2011 and has held a variety of leadership roles in sales and marketing across the business. He began his career in the energy storage industry in 1997 and first became involved with EnerSys in

2003 as an outside channel partner.

He is also a director of several EnerSys subsidiaries, is vice chairman of the board of directors of Battery Council International, and is a director of EUROBAT. (the Association of European Automotive and Industrial Battery Manufacturers).

In a recent earnings sstatement for the company he said that

should tari s continue to remain high for Asiabased lithium or incoming lithium cells, this could be a benefit to the firm’s thin plate pure lead (TPPL).

“That gets you most of the way of lithium without some of the downside risk and safety considerations,” he said. “We could actually see an uptick in our TPPL o ering should that tari environment stay robust on lithium.”

Alastair Walker has been appointed as chief financial o cer and an executive director of South Africa’s Metair Investments with e ect from next month.

Metair, which owns battery production firms Rombat in Romania and South Africa’s First National Battery, said on June 10 that Walker’s appointment takes e ect as of July 1.

He succeeds Anesh Jogia, who resigned in April and whose notice period ended on June 30.

Metair said Walker has extensive private equity and corporate finance experience, gained both in South Africa and internation-

ally, and has been investing and partnering with several South African-based entrepreneurs across a range of industries since 2018.

He has worked with companies including Deloitte and Anglo American Corporate Finance.

Batteries International reported in April that Metair had posted an overall 28% EBIT boost from its remaining battery businesses after selling o its troubled Mutlu Akü Turkish lead acid firm last year.

Clarios celebrated the 15th anniversary of its Meadowbrook facility in Michigan on June 10.

The plant has produced more than six million lithium titanate oxide cells to date and has contributed to the recent milestone production of more than

one million lithium ion batteries, the company said.

The anniversary celebrations featured several events at the plant, including a visit by some of Clarios’ worldwide engineers, who joined 11 Meadowbrook employees who have been with the battery manufacturer since

the facility opened.

Federico Morales-Zimmermann, VP and GM for global OEM customers, products, and engineering, said the milestone was a testament to the hard work and dedication of employees, the support of partners and the trust of customers.

In May 2022, Clarios unveiled plans to mass produce sodium ion batteries at Meadowbrook, in partnership with Natron Energy. Natron installed new cell assembly equipment at the plant, with support from the US Department of Energy’s Advanced Research Projects Agency-Energy (ARPA-E).

Last March, Clarios announced a 10-year, $6 billion plan to expand battery manufacturing and help boost US energy and critical minerals independence by increasing production of “low-critical mineral battery chemistries”, such as its most advanced AGM batteries and additional cutting-edge energy storage technologies.

Sunlight Group, the Greece-based lead and lithium battery manufacturer, has appointed Matthias Fischer as its new chairman. Sunlight, part of the Olympia Group, said on July 15 that Fischer succeeds Gordon Riske,

who is stepping down.

Fischer is a former president and CEO of Toyota Material Handling and MD of Jungheinrich, where he was responsible for global sales, service and marketing.

He will also chair

Sunlight’s strategic planning committee and serve as a member of other key committees.

Meanwhile, Eric Alstrom, a former president of Danfoss Power Solutions and General Motors executive, joins the board as an

adviser, while Francis Wang is stepping down as an independent non-executive director.

Lampros Bisalas, who continues as Sunlight’s CEO, executive board member and a member of the strategic planning committee, thanked Riske for his guidance and dedication.

European lead battery giant Hoppecke is marking 40 years of successful operations at its US subsidiary with a pledge to power ahead with innovative technologies and products.

The company praised its workforce and customers on July 2, saying “we’re just getting started”.

Hoppecke founder Carl Zoellner signed the articles of incorporation for a new joint-stock family company in Brilon, Germany in 1927.

The north American operation, Hoppecke

Battery Systems, was founded in 1985. The subsidiary became Hoppecke Batteries in the early 2000’s.

In a US update last year, Hoppecke said lead batteries continued to be the mainstay of operations in the country, revealing its Federal Railroad Administration-compliant lead systems can be used as starter batteries for diesel engines or in auxiliary applications.

The company is also producing NiCd batteries, used in applications

including backup power systems.

Meanwhile, Hoppecke said it was constantly working to increase the local content of its lithium ion battery systems.

HOPPECKE is committed to investing in America, to increase local production capacity and technical expertise.

Hoppecke said: “In an era where sustainability, reliability, and innovation are paramount, the importance of locally manufactured products cannot be overstated.”

“These board updates reflect our bold commitment to top-tier leadership and global insight.”

He said Fischer and Alstrom bring invaluable international expertise and deep sector knowledge that will help propel Sunlight into its next era of innovation and market leadership.

Last January, Sunlight said it expected to boost production e ciency by 40% after a major upgrade of the group’s software systems. The group also announced an expansion of its global business, digital and IT team, including setting up a new IT hub in Germany.

Hammond, the international oxide and specialist additive group, has appointed Nourhan Moustafa as its senior regional sales manager for the EMEA region.

Nourhan will be based in Dubai. “She will play a pivotal role in supporting our expanding global strategy and customer engagement e orts throughout Europe, the Middle East, and Africa,” says Brad Bisaillon, vice president of sales at Hammond.

“As a chemical engineer with hands-on experience in the battery industry, Moustafa brings a strong background in business

development within the Middle Eastern energy sector.”

She was most recently business development manager at Chloride Egypt. She has a degree in Chemical Engineering from Cairo University and is fluent in Arabic and English.

“In my new role, I aim to be much more than just a sales professional; I want to be a trusted consultant and partner to our customers,” she says. “My core objective is to deepen our existing relationships and forge new ones, helping our

clients in the rapidly growing EMEA battery market to truly unlock their full potential.

“I plan to achieve this by collaborating closely with them, understanding their specific challenges, and demonstrating how Hammond Group’s innovative additives and technical solutions can enhance their products and operational e ciency. Ultimately, I’m driven by the desire to see our customers succeed and to further solidify Hammond’s position as the go-to strategic partner in the region.”

Fleet Street journalist, Shona Sibary, took over as editor of Batteries International in the middle of May. Shona has had a career spanning three decades in print and broadcast journalism working for UK national newspapers and mainstream newsstand magazines.

Shona joined Batteries International in April 2024 as deputy editor for the authoritative long-standing journal of record of the energy storage and battery industry.

Mike Halls, who has been editor of the title and owner of the firm, for the past 17 years, takes over as publisher.

“Having never previously worked on a trade publication before, Shona has brought an exceptional, commercial perspective to our editorial, drawing on years of breaking exclu-

sives and interviewing people as diverse as Colin Firth through to John Major whilst he was PM,” Mike said.

“She has fully immersed herself in the battery world and identified some strong strategic directions in which to take our platforms, maximising all the exciting market opportunities out there. In addition to her superb journalistic skills, Shona is, at heart, a people person and loves nothing more than profiling the movers and shakers of the battery industry and really getting to the heart of what makes them tick.”

Shona says: “In my career to date, I have written about everything from botched boob jobs to celebrities behaving badly. Fun years! But never have I, until now, felt so instinctively in the right place at the right time. There is so much scope in the industry

today for brilliant editorial and breaking stories that the world needs to hear.

“I can’t wait to get those stories out there and

continue Batteries International’s unrivalled reputation for being the trailblazing publication it is.

CBI has taken over Battcon — the industry’s most focused event for realworld battery expertise. Being held during the first week of August in Orlando, the conference promises unbiased insight, hands-on learning and direct access to the leaders solving today’s biggest challenges. Here, CBI’s director, Alistair Davidson and senior technical director, Matt Raiford reveal how they came to be running the show.

Batteries International: How did CBI take over the Battcon conference? I’ve heard it’s Matt’s baby — is that true?

Matt: I don’t know if you would call it our baby, but we adopted it. Battcon has a long history in the United States. It was first started by Alber, a telecommunications company. Vertiv acquired Alber — Vertiv is a huge provider of UPS systems and data centers, and Battcon became their forum.

Alistair: It’s a very end user focused conference. Battery companies talking to the end users, and the end users being educated how to use their batteries. We haven’t had that before. ELBC, for example, is a platform focus.

Matt: So Vertiv acquired it, and then they held it for about 20 years. In that time, Vertiv changed and morphed and expanded. And a couple of years ago, their board changed, and they basically said: ‘We don’t want to dedicate time to things that don’t make more than 150% profit.’ So it was decided that they were not going to do conferences anymore and they got rid of all of their events. And it stranded Battcon. That’s when they put it upon the planning committee to find a new home. Vertiv were very kind, and they just said: ‘Whoever you guys pick, whoever you want to adopt it, we’ll give it to them, okay?’

Alistair: Our membership was really supportive of us running it. They felt it was a technical conference, and obviously we had the equity

of running a technical workshop already. So it was a sensible home for us, given our expertise in the field.

BI: Had you made a decision that you wanted to have a bigger platform in terms of conferences and that this was the direction you were looking to go?

Alistair: No, it wasn’t that, but it did meet the overall objective of CBI. One of our big focuses is to showcase lead battery innovation, and this felt very alongside that. It’s multi-technology and a great showpiece for the lead battery industry.

Matt: Also, a lot of our member companies exhibit and give papers at this conference. And I knew most of the technical committee anyway through my work with standards and fire codes on the stationary side. So they were finding a new kind of home to fall back on and they eventually voted for us.

BI: Was there anyone else in the running to take it over?

Matt: I do know that other companies were interested, but I don’t know who.

Alistair: One of the things that we wanted, was to interact more with end users in the industrial energy storage space and we thought Battcon would give us that opportunity and it has.

Matt: That’s what allowed us

to suddenly be able to speak to stationary end users specifically in the US — utility companies, telecommunications firms, data center providers. Companies like Southern Company, Comcast, AT&T — these pretty premier organizations that use a lot of batteries but they’re typically one step back from that part of the supply chain. So, it has allowed us to actually speak to these really large consumers

The technical program is not meant to be commercial, it’s meant to truly be educational. If you submit something that’s too commercial it gets rejected. It needs to be something like, ‘lessons I’ve learnt from my journey’.

— Matt Raiford

in a more demonstrative, intentional way. And, like Alistair said, it’s multitechnology, so lead has a significant presence there, but lithium, sodium and zinc all have their slice of the pie too. Lead will always be our sweetheart. But now we actually get to see how all the batteries play.

Alistair: We’ve had some big names, significant data companies have just signed up to attend which is great news.

Matt: About 40-ish percent of all the world’s data centers are present in the United States, so that’s huge.

BI: Do you have plans to change anything about Battcon?

Matt: We want to keep the fact that it’s a really practical, end-user focused conference. There’s a big training element around how to maintain batteries and also a lot of stu about getting operators and engineers up to date on best practices and standards. We don’t want to change any of that.

But one thing we are doing is bringing in students. Years ago there were mentorship programs associated with the event and we’ll be resurrecting those.

BI: It’s a bit of a departure from what CBI has done previously. What have been the challenges for you in terms of preparing for Battcon?

Matt: We’ve taken a step back to understand what the crowd who comes to Battcon want. We adopted the conference five months before it was due to take place in Miami last year. Vertiv had planned it all and then dropped it, saying “Go find a home for this.” And it was a mad scramble for us before the event date to understand what we had.

Alistair: We inherited a lot of the program as well. And the feedback we had from some of the delegates was that the education is important but the program was getting repetitive. There wasn’t anything new.

So one of the things we’ve done this year is implement some new speakers, slightly di erent directions on the topics, and also made it more

We don’t run events for the financial gain. That isn’t the priority for these events. It’s to help our industry. Running Battcon will help the lead battery industry to showcase their products and interact with end users.

global. We’ve invited our members from CBI who are not just in the US, but from other regions of the world as well.

Matt: The US is avant garde when it comes to very hot topics — no pun intended — such as fire safety for energy storage systems. Partly it’s because of the sheer presence of BESS systems in the US, and then just a lot of di erent stakeholders, standards such as NFPA and international fire codes are housed in the US.

So these best practices — like how do you actually build a safe BESS — we want to translate that to the rest of our membership. And Battcon serves our membership in that way as we now have a forum for best practices. Battcon has always been a leader in that regard, and we want to maintain that.

BI: Is it a commercial project for you? Or an educational one?

Alistair: We don’t run events for financial gain. That isn’t the priority for these events. It’s to help our industry. We’re not here to make huge profits. We believe that running Battcon will help the lead battery industry to showcase their products and interact with end users.

Matt: The other thing about Battcon is that the paper selection process is extremely thorough. So the abstracts, the technical committee approves them. It’s a smaller set of papers. And then you actually write a periodical, like a peer review.

They review every slide. It’s very robust. Therefore the quality of the technical program — it’s not meant to be commercial, it’s meant to truly be educational. If you submit something that’s too commercial it gets rejected. It needs to be something like, ‘lessons I’ve learnt from my journey’.

Also, it’s a forum to understand how new technologies can serve this end user base. What technologies

are actually gaining momentum? It allows us to understand the battery landscape a little bit more widely. There’s an element of, ‘What’s on the horizon?’

Alistair: There’s a lot of potential at Battcon. It should be our showcase. It’s the only conference out there that has this sort of end user industrial focus on all batteries. And there’s so much potential for us to improve it and grow.

Matt: It’s important for us to get the right people in the room. We want the people who fix the problems — the engineers and operators, the technologists. So we’re trying to keep that part very vibrant and alive. But it’s brilliant because Battcon allows us to actually see the entire landscape.

It’s a very end-user focused conference. Battery companies talking to the end users, and the end users being educated how to use their batteries. It’s also multi-technology and a great showpiece for the lead battery industry.

— Alistair Davidson

The EU is poised to introduce new workplace exposure limits for sectors including EV battery production — despite warnings the move cost the industry €20 billion ($24 billion) over 40 years and force plant closures.

The exposure limits recommended by the Commission — in the sixth revision of the EU’s carcinogens, mutagens and reprotoxic substances directive (CMRD) — include cobalt and inorganic cobalt compounds, polycyclic aromatic hydrocarbons and 1,4-dioxane, which can be found in a range of household products. Welding fumes are also added under the scope of the CMRD.

The Commission said on July 18 the move could prevent about 1,700 lung cancer cases and 19,000 other illnesses, including restrictive lung disease and damage to the liver and kidneys, over the next four decades.

However, preliminary figures from the Cobalt Institute indicate the new limits could lead to more than 110,000 job losses out of a total of over 640,000 jobs and lead to the closure of around 20% of some 9,000 sites.

The Commission’s proposal will now be discussed by the European Parliament and European Council. If adopted, EU states will have two years to incorporate the directive into respective national laws.

An impact assessment of the proposal acknowledges industry fears that the new limits could lead to the relocation of production sites to countries and regions outside the EU and “have more far-reaching consequences for the European industry than only the increased protection of workers”.

The Commission said cobalt and inorganic compounds are commonly used in battery production and manufacturing

The European Commission’s proposal to overhaul the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) Regulation is almost certainly the most significant update to REACH since its creation, shaping the future of chemicals regulation in Europe. The changes aim to simplify EU chemical regulation making it more transparent, and fit for purpose.

The revised proposals form part of the broader Chemicals Industry Package. The final package which should be adopted by the end of this year will simplify registration, enhance enforcement, drive digitalisation and modernise risk management.

One important aspect of the revised REACH Regulation is the overhaul of the registration system. Registration validity will now be

processes for magnets and hard metals.

The proposed limit for cobalt and inorganic compounds is 0.01 mg/ m3 for particles that can be breathed in through the nose and mouth, and 0.0025 mg/m3 for finer particles that can reach deeper into the lungs. Transitional limits (0.02 mg/m3 and 0,0042 mg/m3 respectively) will give industries six years to adapt, the Commission said.

Existing limits vary across the EU range from 0.01 mg/m3 (the ‘strictest’ national binding occupational exposure limit) to 0.5 mg/m3 (the ‘least strictest’).

According to the Commission, the proposed measures reflect the latest scientific data and benefits from analysis provided by the Advisory Committee on Safety and Health at Work.

The measures could save in excess of €1 billion ($1.2 billion) in healthcare costs and significantly improve

limited to 10 years, and ECHA will be able to revoke registration for failure to submit updates or incomplete data.

This will be the most significant update to REACH since its creation, shaping the future of chemicals regulation in Europe.

Digitalisation will become important with harmonised electronic formats for SDS (Safety Data Sheets) and the gradual introduction of DPP (Digital Product Passports) for products such as batteries, textiles, and furniture.

the quality of life for workers and their families, the Commission has claimed.

In 2023, in preparation for the Commission’s proposed changes, the Cobalt Institute said it had always supported the introduction of cobalt occupational exposure limit values in the EU.

However, “the values need to protect workers and let industry operate in Europe”.

The institute said then, based on its recently conducted scientific and socio-economic studies, it recommended 0.02 mg/m3 (inhalable) and 0.0025 mg/ m3 (respirable) occupational exposure limits for cobalt and cobalt compounds. These two recommended values would protect workers and allow for industry to continue operating in Europe. In addition, these values are progressive and are considered as still dicult to achieve for certain industries, the institute said.

These will improve traceability, reduce administrative burdens and provide greater transparency on substances of concern.

The Commission proposes the creation of a European Audit Capacity to assess how e ectively member states enforce REACH, ensuring uniformity across the EU. Customs controls will change with mandatory SDS provisions at import and automated verification of registration and authorisation numbers. The European AntiFraud O ce will be empowered to investigate cross-border REACH violations.

A key addition is the “essential use” concept. THis identifies substances critical to society yet pose a significant risk. This ensures that safety measures focus on the most important substances.

Basis weight measuring system for single and double sided coating lines

NO DANGER from radiation due to ultrasonic measuring principle Discover our solutions – WE

Mike Judd says he lives, eats and breathes batteries. But when Shona Sibary delved a bit further she discovered that the CEO of one of America’s largest lead battery manufacturers also has eight women in his life … and a penchant for Route 66.

Steel and winches. Two whopping great industries in Oregon that have no idea what they’ve missed and are, quite probably, more than a little worse o because of it.

The reason? Back in 1991, a young man, with no high school diploma to his name, needed a job. These were the businesses that paid well, had been around for a long time and, in his own words, ‘had a way of promoting people.’

Luckily for the battery industry, Mike Judd, instead, landed his first job with Johnson Controls. Day one on the factory floor saw him putting the top label on the battery. Day two, he was promoted to taking the vent caps o and the finishment caps on. And the rest, as they say, is history.

Today, Judd is the CEO and president of Stryten Energy, one of America’s largest domestic battery manufacturers with over 2,500 employees. The firm builds ‘darn good’ batteries that power everything from submarines to microgrids, distribution centers, cars, trains and trucks.

Headquartered in Alpharetta, Georgia, they are an undisputed industry leader with a huge expertise, delivering energy solutions through technologies including advanced lead, lithium and vanadium redox flow batteries, intelligent chargers and energy performance management software.

Stryten’s history dates back to 1888 and its predecessor, the Electric Storage Battery, which grew over the next century. In 2020, Stryten Energy emerged as a new company and quickly began expanding, acquiring Tulip Richardson Molding in 2021, which added three battery component plants to its footprint. Stryten extended its battery tech into lithium and vanadium flow batteries with acquisitions of Galvion’s power division in 2021 and Storion Energy 2022.

It’s an impressive portfolio that has seen the company constantly diversifying to keep ahead of the game.

But while Judd is immeasurably proud of the fact that Stryten is ‘probably the most diversified battery manufacturer in the US,’ he is also keen to keep their feet firmly on the ground.

“We’re very mindful of how many di erent technologies we get into,” he says. “Today, it would be very easy just to go and invest, to gobble up all

kinds of new technologies. But the core part of our business is domestic battery production and that’s leadbased chemistry. The second would be lithium and then flow batteries after that.

“And the way we run the business is to focus on the core part, making sure we pay the rent, pay our

employees and produce batteries for our customers. That needs to be completely protected.

“The only time we add on new technologies is if we can buy a small business that we think has the opportunity to go big in the market. Vanadium flow is a good example. But we don’t distract our

Judd’s early passion for the technology of batteries and how to make them more e cient in the manufacturing process was learnt on the job — and not at university. It’s something that has inspired him to put programs in place at Stryten to create new electricians through apprenticeships and not look at a new hire for the company solely on the basis of whether they are a graduate.

“My take on this is that if somebody can prove they have the technical ability for the position, then that is first and foremost and the college degree is second. What I tell people is that there’s probably a point in your career, as you progress, that it’s going to become more important to have that degree box checked.

So while I’ll give you this job today, which is a supervisor or manager or engineer — because

you’re so good at what you do, I would be crazy not to give you that — there may be a ceiling you hit at some point where somebody says: ‘You know, you can’t run a plant or be a director of a whole bunch of people without a degree.’ I mean, that’s not how we treat it at Stryten. But if they don’t always work for us, somebody else may still have that requirement.”

“I often think about that manager at the very first plant I worked at who was able to take a risk on somebody who didn’t have a mechanical engineering degree and put them in a position of engineering and designing stuff. You know, it takes a special manager, to do that”

Mike has a surprising coping strategy to decompress from the demands of being a CEO.

“I have a road motorbike, an adventure bike, if you will, that I take on solo trips across the country for four or five days at a time,” he says. ‘And I have just three rules. No hotels, no restaurants, and no freeways. I sleep in a tent, pack all my own food and cook it on my own. The last trip I took was up through Canada from Georgia, all the way up to Labrador and then all the way around and back down.

“Another favourite is riding

sections of the old route 66 in the south, New Mexico, that area. It’s very beautiful because you go through towns that used to be amazing until the freeways went in, and then they kind of died down. But all the history is still there, and there are still folks who live there and are never going to leave.”

Long road trips aren’t Mike’s only obsession. He also talks about a love of ‘anything to do with wheels and hours spent in his workshop building something with engines.

“I have several o -road dirt bikes,” he says. “I was actively competing

two years ago on the Georgia race circuit but then decided last year to take some time o from that. It’s pretty hard on the body. And I have electric motorcycles that I tinker with to try to see how much more energy I can get out of them, what battery packs I can put on.”

He stops and grins. “It’s a running joke around here that I have zero interest in sports. I’m the worst person to have a conversation with about what’s happening in basketball or baseball or football or soccer or anything, because I know absolutely nothing.”

“A subsidy says that the business probably can’t perform on its own”

baseline workforce for that. We would never put that at risk because we realise that in those markets there are no guarantees. You can’t make a workforce feel that those are guarantees because you lose that focus on the baseline business.

Let the market decide

“So, yes. There might be potentially humungous opportunities out there, right now, but we are not going to take a bunch of resources and try to drive that. Instead, we’re going to let the market determine what they want for technology. And when we see the market wanting a technology, we’ll look into it, but we’re not going to invent a technology and try to shove it through.”

It’s a sensibly cautious approach from a man who admits that he lives, eats and sleeps batteries. “Most of the time when I’m thinking about something, it’s batteries,” he grins.

He describes the industry landscape right now as ‘unrelenting.’ But loves how excited that makes him feel.

“There just isn’t a single part of our lives right now that isn’t attached directly to a battery,” he says.”

Will Trump help or hinder Stryten’s strategy?

“I don’t think a government’s decisions on how to drive revenue and things like that really a ect, or change, in any way, the consumer and their requirements,” Judd says. “We need more energy every single day. That’s not going to change based on pricing or tari s. It may change short term, but in the long term it’s all going to settle out. The demand doesn’t change. So filling that demand also won’t.”

Like every other business, Stryten has had to have conversations and come to conclusions in response to the current political situation, but Judd feels they’re not too a ected.

“Obviously we’ve had meetings on how our potential suppliers are going to react,” he concedes.

“A good example would be firms integrating solar fields. They have a di erent business model that they’re going to have to use now. And if you think about the real di erence that’s

Judd is keen to talk about a bigger picture here — one of environmental responsibility. And it’s this that gets him truly fired up.

“Batteries are the future of conservation,” he enthuses. “Regardless of the technology that we use to power the world, there has got to be a point when we all start conserving rather than consuming. The planet is still growing, still consuming, but at some point, that’s got to shift. And what’s going to enable that shift is batteries.

“Take a small island that is powered 100% by a diesel or natural gas generator today and they want to add some renewables and solar panels and wind turbines. None of these resources run eciently unless you can utilize that resource over time.

“So imagine an island with a generator running a percentage of the time. If you put a big battery there, you can now run that generator at 100% e ciency for four hours a day, rather than 24 hours a day at 60% e ciency.

“It’s really about sending all the energy to the battery. The battery is the main place where you can truly conserve energy, because

it can deliver energy exactly when it needs to be delivered. Nothing more, nothing less. So no more heat generated, no more wasted energy.”

Judd is convinced that Stryten is at the forefront of creating this energy ecosystem of the future and he has come up with a concept called ‘The Battery First model,’ which, simply put, is all about putting the battery at the centre, whether it’s a firm energy resource like hydrocarbons, or something more intermittent like solar or wind.

“It’s a conservation model that provides grid stability and drives e cient use of the power generated from renewable and carbon-based sources,” he says. “This approach will enable long-duration energy storage that can be scaled in size and duration to meet the needs of utilities, commercial and industrial, as well as military bases and emergency response applications.”

Judd’s vision — and it’s not an unrealistic one — is that this will take batteries from being a sidekick to playing a central role in energy security in America.

“We have solar fields today that are sitting in the middle of the desert in California doing absolutely nothing”

changed from one administration to the next, it’s this shift between subsidies and incentives.

“A subsidy says that the business probably can’t perform on its own. There should be a view somewhere down the road that either it gets its manufacturing costs down and can

be profitable without a subsidy, or the market price goes up so it can be profitable that way.

“Well, on the solar and wind side, that’s a hard argument to have. Because if the price goes up to the consumer, which makes them profitable, it goes against the whole

“I’m probably one of the few people who has been in every single battery manufacturing plant in the United States”

“At home I don’t win many battles”

Mike describes his family set-up as a little ‘complicated’ although as he goes on to explain, it becomes obviously that, really, it is something quite wonderful.

“My wife and I have three daughters and along the way we adopted four more,” he says. “They happened to be friends of our daughters at the time, and they had a family situation that necessitated them needing a place to stay. They ended up staying with us, and then staying for many, many years. But it’s perfect. They’re all great, and they match up with our daughters.

“And, you know, the beautiful part about these seven girls is that we moved around a lot and because

of my job when they went to new schools they immediately had friends from day one, because they all went together. And even though most of them have left home now — the youngest is graduating this Fall — it’s all still working out. We have two grandchildren now with one of the adopted girls, and so it’s a big, big family.”

And as the sole male in the midst of all these women, one imagines Judd has boundless patience and a whole heap of soft skills that must really benefit him in running a company. “Put it this way,” he says. “I don’t win many battles. In fact, I can’t remember a single one where I’ve come out on top.”

idea of renewables which is to keep the cost of electricity down.

“So that means that the only way for you to really become profitable is to reduce your manufacturing costs. And those are known things that you can model out for years.

“On the incentive side, which is the new administration, they’re saying: ‘We’re going to incentivize folks who can already pay all their bills, who can pay their rent and their employees, but they can only go so fast in development of new technology. So let’s incentivize those companies to go as fast as they can.

“That’s really what has changed. When we partner up with people to do BESS solutions now, those people are probably going to have to be on the incentive side and already profitable, leveraging their position in the market, rather than folks who are saying: ‘Someday I’m going to be profitable, but without these subsidies today, I’m not.”

Does he worry that this push and pull dynamic will slow down solar installations?

“Maybe. Maybe not. I don’t know. I’m not a solar installer. But what I do know is that if there were money to be made in a solar field yesterday and the subsidies don’t exist, then you’re going to have to invest in BESS to make that investment pay.

“It’s going to have to be able to deliver energy 24 hours a day, not just when the sun is shining. We have solar fields today that are sitting in the middle of the desert in California. They’re doing absolutely nothing. But with BESS they absolutely could. So I think it’s going to have people go back and say: ‘You know what? The ones we installed for the last 15 years, there’s now a market that’s saying we need to go as fast as we can to install BESS so that we can serve that market 24 hours a day and actually make money from it.’

“The rest of the market, it will figure itself out. I mean, it’s just a shift between one administration and the next. Is one right or wrong? I couldn’t possibly tell you because the dynamics are so complicated. We need time.”

And best supporting role goes to…

Within Stryten’s optimistic forecast, how large a role does Judd see lead — its core business — playing?

“I don’t think it will play the biggest part — that is going to be

for emerging technologies that have really good energy densities,” he says. “But it is certainly going to play a meaningful role, for sure, especially in places where space is not a constraint, and when you’re looking at something like five to seven hours of duration.

“Lead works very well in that environment. It takes more space, but it’s nearly 100% recyclable, and there can be business cases put in place where you buy it once, and it just gets replenished as you go along. And there is no big ‘pull it all out and start all over again’.

“So there’s certainly a market for lead, especially when you start to think about, not humongous solar fields, but smaller micro grids and backup systems. It fits perfectly in that hundreds of gigawatts space. It’s not a small market at all, just for lead, considering the thousands that will be for the entire market, which would include flow, compressed air, hydroelectric or pumped hydro, lithium, or all of them. They’re all going to fit someplace.”

Stryten’s place in the race It’s going to be a highly driven landscape. How does he feel they set themselves apart from their competition?

“First of all, we strive every day to make sure that we take care of our customers. We’ve created a position for ourselves where we are very nimble. We can react quickly. I think we o er that security to our customers. The other thing is that we are absolutely focused on manufacturing, environmental health and safety.

“All the decisions that we make, we firstly ask the question: ‘Is it going to help our 2500 employees?’ Secondly, is it going to help the environment in or around our plants, the safety of our folks? If we can answer those questions, yes, then most likely it’s going to be a good business decision.

“If you look at the scale of battery manufacturers, we’re certainly not the biggest and we’re certainly not the smallest, but every manufacturer of whatever size has to react di erently to the needs out there. And so I think we have found a way to fit nicely where we are and to make sure that we’ve got a diversified portfolio that when one market is down, the other one most likely is not going to be down. We can shift our focus, our resources and our supply chains over to serve whichever side of the business that we

“BESS is a monster,” Judd says. “It’s very, very large. But it’s not totally developed yet. If you look at something that says, ‘How big could the demand be?’ Then, it’s energy storage. Even if you consider that there could be a slowdown in solar and wind, because, you know, subsidies went away, there’s been a lot of installations over the years that still don’t benefit from energy storage.

“And then there’s also this whole shift in the market that is dictating that if you’re going to put a battery

in any application you want that battery to do something besides just sit there in a standby mode waiting for the power to go out.

“What that means, in real terms, is considering that battery an integral part of an energy plan and then working out how to utilize that plan. A lot of the conversation we have with customers is how to do just that and it starts with an automobile to a fork truck right the way through to government and the military.”

Energy Founders Day: 2023

need to. We’re in a very good spot.”

What does he, personally, feel he contributes to that success?

“I’ve worked in so many di erent technologies and been across the industry,” he replies. “In fact, I’m probably one of the few people who has been in every single battery manufacturing plant in the United States, every one of them.

“I’ve encountered so many great leaders who have all given me little snippets along the way that have helped me to where I am today.

“But the one thing that I live by is that unless I’m forced to make a decision, I wait.

\”I think it benefits my team and it benefits the whole business. People sometimes wrongly feel that if there’s a decision to be made you’ve got to make it immediately because otherwise it might show that you’re not up to speed with the business. But I truly believe that we can discuss and talk about things, that we don’t always need to end the meeting with the decision. We can think about it, come back and find the right path.”

A drive to succeed

It’s a self-deprecating remark from a man who, whilst maybe not winning battles at home, is certainly doing something right in the boardroom.

He attributes this to a long, hard climb from the bottom of the battery business, through the ranks, where he worked as one of the utility people filling in whatever job needed to be done at the plant when someone didn’t show up for their shift. He picked up his GED, then a business degree and then a master’s along the way but has never forgotten those humble beginnings.

It’s a foundation that still keeps him grounded today.

“I often think about that manager at the very first plant I worked at who was able to take a risk on somebody who didn’t have a mechanical engineering degree and put them in a position of engineering and designing stu . You know, it takes a special manager, to do that.

“Back then, I went work to make a living but then something changed along the way. I started wanting to make batteries better and processes better.”

Thirty-four years later, we could all be forgiven for saying, ‘Job well done.’ Except we’d be missing the point. Mike Judd is only just getting started…

“We

can shift our focus, our resources and our supply chains over to serve whichever side of the business that we need to. We’re in a very good spot”

“I have a love of wheels and anything to do with tinkering with engines”

SORCS, Blueberry Hill, Collinsville, Alabama, 2021

Europe’s superficial love-hate relationship with Chinese battery tech and EV investors risks derailing the bloc’s sustainability, economic and security objectives, and potentially harm trade with the US, according to a new study.

Brussels-based thinktank Bruegel said in its analysis, released on July 16, the EU’s current crossroads in EV industrial policy is defined by a paradox.

The bloc must accelerate its green transition while managing rising strategic dependence on foreign — especially Chinese — technologies.

However, the EU lacks a united strategy across all member states to align it with climate, industrial and security aims, the study said.

Despite the EU’s imposition of provisional import tari s on Chinese battery EVs amid concerns over unfair state subsidization, Chinese investment in Europe’s EV sector has moved from the periphery to the core of the continent’s green industrial transition, according to Bruegel.

In 2024, Chinese greenfield investment in the EV sector was around €5 billion ($6 billion) — more than 50% up from 2022, accounting for

half of all completed Chinese greenfield foreign direct investment into Europe that year.

Plant-level investment data shows that China has become the second-largest investor in Europe’s EV supply chain.These investments span nearly the entire value chain, from upstream cathode and anode materials to midstream battery cell and module production, and downstream into EV assembly and battery recycling.

However, while it makes sense to tap Chinese FDI to fill immediate gaps, the ultimate benchmark should be whether this investment complements domestic capacity building and diversification towards partners more aligned with EU norms, Bruegel said.

“But Europe’s reliance on Chinese firms for critical raw materials and battery components is a vulnerability. China control to a significant degree the refining and processing of lithium, nickel, cobalt and rare earths, which are essential inputs for EVs.”

Chinese moves to tighten export controls on rare earths and high-performance magnets in retaliation

against US tari s illustrate Beijing’s readiness to weaponize supply chains as a tool of geopolitical leverage, according to Bruegel.

“For Europe’s automotive sector, this means that abrupt restrictions or price shocks could disrupt production, hinder the scaling-up of production of a ordable EVs and erode industrial resilience.”

China’s involvement in the European EV and battery supply chains could also complicate EU access to major export markets, especially the US.

In terms of security, as EVs are now software-defined products, electronics and technology FDI poses particular risks related to data security and unauthorized access to sensitive information.

“Although locally assembled vehicles must comply with EU technical standards, embedded hardware and proprietary software can remain opaque, creating enduring vulnerabilities that are di cult to monitor and mitigate,” the report warned.

The EU Battery Regulation, adopted in 2023, could be used to restrict market access, ensuring that batteries, and the EVs powered by them, can only be sold in the EU if they meet tough environmental standards.

“However, until core provisions are finalized and enforced, much of the regulation remains toothless and does not tackle economic security concerns,” Bruegel said.

The US energy storage market faces major challenges in the years ahead as investors manage the “political whiplash” impact of the newly enacted ‘One Big Beautiful Bill Act’, say analysts.

The flagship policy of US president Donald Trump, which he signed into law on July 4, was welcomed as decisive action to help preserve advanced manufacturing production credits for battery manufacturing by lead industry trade body Battery Council International.

However, energy analysts at Wood Mackenzie warned on July 10 that the new laws will pile pressure on energy storage supply chains.

And while investment tax credit eligibility is maintained through to 2030, energy storage faces “onerous ‘foreign entity of concern’ restrictions” that likely preclude purchasing

battery cells from competitor nations such as China, Wood Mackenzie said.

According to the firm’s analysis, the risks and costs of supply chain shifts will put downward pressure on storage growth, despite being one of the few resources that can be added quickly to support growing demand.

And with EV incentives eliminated, reducing Wood Mackenzie’s US battery electric vehicle market share forecast for 2030 from 23% to 18%, the firm said most EV growth will now come from companies with established supply chains — or non-domestic players using BEVs to enter premium markets.

David Brown, director, energy transition research for Wood Mackenzie, said: “The policy prescriptions increase the likelihood of Wood Mackenzie’s delayed energy transition

scenario for the US.

“The legislation serves as a harbinger of central challenges facing energy investors — managing political whiplash when investing in assets with 30-year-plus lifespans amid dramatic policy swings every election cycle.”

However, the BCI said the retention of critical manufacturing incentives in the new Act demonstrated a clear understanding that American battery manufacturers are essential to the nation’s economic security, energy independence, and competitive advantage.

BCI president and executive director Roger Miksad said: “This vote sends a powerful message that America is committed to building and maintaining the world’s most advanced battery manufacturing ecosystem.

EnerSys is to cut 575 non-production jobs as part of a restructuring plan unveiled on July 22 aimed at securing $80 million in annualized savings.

Shawn O’Connell, who succeeded David Shaffer as president and CEO this May, said the “dicult” decision to axe jobs — primarily in corporate and management positions — was a necessary move to stay competitive.

The cuts represent 11% of the US-based battery manufacturing giant’s non-production global workforce.

O’Connell said EnerSys had spent the past six months listening, evaluating, and testing how the firm could best serve its customers, deliver stronger returns, and build a more agile organization.

“EnerSys is powered by an incredible team, and this decision in no way reflects the dedication or contributions of the individuals impacted,” he said.

“We are committed to supporting our employees through this transition with care and respect.”

EnerSys expects the shake-up to be “substantially complete” by the end of the second quarter of fiscal 2026, subject to local law requirements.

Combined with other “non-headcount-related actions”, these changes are expected to result in about $80 million in annualized savings starting in fiscal 2026.

EnerSys said the estimate comprises around $70 million in savings, representing a reduction of over 10% of the company’s fiscal

Asia-based lead and lithium major Leoch International has issued a profit warning in the wake of US tari turmoil — and delayed the start-up of its new lead acid plant in Mexico.

Leoch said preliminary analysis indicated profit for the first half of 2025, ended last June, is expected to fall by about 60%-80%, compared to the corresponding period last year, despite an expectation the group will see a 10%-20% year-on-year revenue increase.

The setback is mainly due to additional import tari s imposed by the US on goods in the second quarter of this year, which led to an increase in the costs of unspecified products on which Leoch had already paid taxes and delivered.

However, in a statement to the Stock Exchange of Hong Kong, based on the group’s preliminary review of unaudited consolidated accounts, Leoch chairman Dong Li

2025 operating expenses, as well as an estimated $10 million reduction in the cost of goods sold.

The firm expects to realize about $30 million-$35 million of savings in fiscal 2026, with material benefits beginning in the third fiscal quarter.

Estimated savings exclude one-time charges related to the restructuring, which are anticipated in the range of $15 million-$20 million, with the majority occurring in the second and third quarter of fiscal 2026, primarily for severance and other related costs.

EnerSys said the moves are part of a broader strategic plan that will be discussed during its fiscal first quarter 2026 earnings report, which is scheduled to be published after

said the sales price of a ected products would not be increased until the end of 2025.

Meanwhile, operations in Mexico will now start in the fourth quarter of this year, instead of the planned second quarter. This was blamed on “the impact of the supply chain and construction progress”.

Leoch said it was still in the process of finalizing the results of the group for the first six months of the year. Interim results are set to be released on or before August 31.

Batteries International reported last April that Leoch had posted a near 20% boost in topline growth in annual results for 2024, driven by robust sales of the group’s mainstay lead battery technology across global markets.

Revenue for the year was Rmb16.1 billion ($2.2 billion) compared to Rmb13.5 billion the previous year, according to results posted on March 27, while net

market close on August 6. This will be followed by the firm’s earnings conference call scheduled for August 7.

The company revealed last May that its stock lost and regained $900 million in the marketplace over a three-month period amid the recent flurry of US trade tari announcements.

That came after EnerSys announced the closure of its flooded lead acid battery manufacturing facility in Monterrey, Mexico and a production switch to its existing Kentucky plant, while expanding capacity in the US and Europe.

However, in June, the company formally opened its expanded US Sumter plant, as it expands investment in Thin Plate Pure Lead, flooded lead and lithium ion batteries.

profit stood at Rmb564 million from Rmb568 million in 2023.

In May, Leoch announced it was strengthening ties with Japan-headquartered GS Yuasa and discussing plans to develop and market their respective brands worldwide.

The talks took place less than two years after Leoch signed an agreement to acquire controlling stakes in two China-based lead battery firms owned by Yuasa — Tianjin GS Battery and Yuasa Battery Shunde. Editor’s note: EnerSys confirmed last April that it was closing its flooded lead acid battery manufacturing facility in Monterrey, Mexico and switching production to its existing Kentucky plant while expanding capacity in the US and Europe.

The company’s announcement came just hours before US president Donald Trump was set to unveil a raft of reciprocal tari s on countries that impose duties on US goods.

US shipping line Matson has confirmed its suspension of shipments of EVs amid rising concerns about fires sparked by lithium ion batteries.

Matson told Batteries International on July 23 it had written to customers on July 14 saying, e ective immediately, it had ceased accepting new bookings for shipments of EVs and plug-in hybrid vehicles.

The company, a US owned and operated transportation services firm headquartered in Hawaii, said it would continue to support industry e orts to develop compre-

hensive standards and procedures to address fire risks posed by lithium batteries at sea.

Matson said it does not plan to resume shipping services for EVs until “appropriate safety solutions” that meet its requirements can be implemented.

The company said it provides a vital lifeline to the economies of Hawaii, Alaska, Guam, Micronesia, and the South Pacific and o ers a “premium, expedited service” from China to Southern California. The company’s fleet of vessels

includes container ships, combination containers, and roll-on/roll-o ships and barges.

Matson’s suspension announcement follows a string of global incidents in which fires broke out on vessels carrying EVs.

In 2022, a vessel carrying 4,000 vehicles sank in the Atlantic after a suspected EV battery fire and the ship’s owner said a year later it was likely never be recovered and the cause of the disaster would remain a mystery.

In March 2022, China called on the International

Maritime Organization to consider a shake-up of maritime safety rules for EVs being shipped by sea, amid a rising tide of fires involving lithium ion batteries.

The following year, Norwegian shipping company, Havila Kystruten, announced it was banning electric cars, hybrids and hydrogen vehicles on its ferries because of potential fire hazards. This followed a risk analysis conducted by Proactima, a Norwegian risk management advisory consultancy, according to chief executive Bent Martini..

McGill and Partners has launched a cybersecurity insurance policy tailor-made for challenges faced by the BESS market.

The UK-based international company said battery storage installations are becoming an increasing target for cyber threats as reliance on interconnected power systems grows.

The new insurance policy, with cover provided by certain Lloyd’s underwriters, o ers physical damage

protection as well as cover for business interruptions resulting from cyber incidents or technical failures.

McGill said the cover is flexible, sector-specific, and o ers robust protection to safeguard operations.

The policy also extends to cover increased regulatory costs as a result of the compliance required to meet evolving cybersecurity and resiliency standards.

McGill partner for cyber, Tom Dryden, said the company was seeing greater

demand from clients for industry-specific coverage.

“Cyber incidents and technical issues at battery energy storage systems are

becoming increasingly relevant as these systems become more integrated into global critical infrastructure and smart grids.”

UK firefighters are tackling at least three lithium ion battery fires a day, following a 93% surge between 2022 and 2024, according to research published by business insurer QBE in May.

E-bikes are a major

contributor, being linked to nearly 30% of all recorded lithium ion battery fires in 2024, according to analysis of data acquired by QBE under Freedom of Information requests to UK fire services in March 2025.

Insurance companies are increasingly refusing to cover waste management facilities, or hiking the cost of premiums, amid a surge in fires caused by discarded lithium batteries, an alliance of European firms has warned.

In Germany alone, waste collection trucks are being hit by up to 30 fires a day, while it is estimated that lithium batteries are the root cause of 180-240 fires annually in Austrian waste plants, according to eight groups including the

European Waste Management Association.

The group has issued a statement urging EU leaders to take “decisive regulatory action” to protect waste management infrastructure and employees.

The group has called on the European Commission to establish a Battery Fire Prevention and Recovery Fund and a Deposit Return System to meet collection targets set out in the EU’s Battery Regulation.

Battery fires in the waste management sector result

in significant economic losses and an increasing health and safety risk to workers and citizens, as well as a reputational issue for the a ected companies and the entire sector due to negative media coverage, the group said.

For many medium-sized waste management companies, it is no longer a ordable to insure their facilities, while some facilities in Belgium are expected to lose insurance coverage altogether by 2025 due to the risk of fire, the group said.