What the TechMed Revolution Means for Healthcare

Alan Cohen of DCVC forecasts agile, data-driven innovation

Venture Report, Power Moves, Alumni Milestones, and more...

Alan Cohen of DCVC forecasts agile, data-driven innovation

Venture Report, Power Moves, Alumni Milestones, and more...

January 2025

Scott Pantel

Chief Executive Officer, LSI Editor-in-Chief

Rebekah Murietta Vice President of Media, LSI Contributing Author

Kelly Williams Subscriptions & Enterprise Sales, LSI

Henry Peck

Chief Business Officer, LSI Editor-in-Chief

Brenna Hopkins Sr. Content Manager, LSI Contributing Author

Benny Tomlin Contributing Photographer

Tracy Schaaf Managing Editor and Content Strategist, LSI Lead Author

Blake Matrone Sr. Marketing Manager, LSI Contributing Author

Nicholas Talamantes Sr. Director of Market Intelligence, LSI Contributing Author

Maricela Almonte Customer Service & Fulfillment, LSI

(LSI)

714 847 3540 tel/fax email: info@ls-intel.com Vol 2. No. 1 January 2025

Created by LSI, The Lens leverages LSI’s deep industry relationships and proprietary market intelligence to help executives like you build lasting medtech companies. Start your Individual, Group or Enterprise-Wide subscription today!

Scan QR Code to activate your subscription.

The Lens is published monthly and available in print and electronic formats. Copyright by Life Science Intelligence, Inc. All rights reserved. Editor takes care to report information from reliable sources and does not assume liability for information published.

Interested in subscribing? email to: info@ls-intel.com

Interested in advertising? email to: kelly@ls-intel.com

Dear Readers,

As we step into 2025, we are thrilled to share the latest edition of The Lens. The new year has been off to a fast start for many, and the medtech industry continues to lead the way as a hub of innovation, resilience, and collaboration. It is an extraordinary time to be part of this ecosystem (perhaps the most exciting time in the industry’s history) where today’s transformative breakthroughs will shape the trajectory and future of healthcare for generations to come.

Medtech mergers and acquisitions (M&A) have set a positive tone for the year, with Stryker’s $4.9 billion acquisition of Inari Medical reinforcing their strategic expansion into neurovascular care. Similarly, the broader healthcare sector is making waves with Johnson & Johnson’s $14.6 billion acquisition of Intra-Cellular Therapies, reflecting a robust appetite for strategic expansion into new indications beyond value-accretive M&A supporting core product portfolios. While these deals promise immediate gains, we are also closely observing the long-term implications of a more consolidated set of strategic acquirers. What does this mean for innovation and competition? It’s a question that will shape the trajectory of our industry in the years to come.

Adding to the dynamism, a new U.S. administration brings both opportunity and uncertainty to stakeholders across medtech, from clinicians to startups to multinational corporations. As the administration sets its priorities, our industry is uniquely positioned to adapt, respond, and innovate in the face of evolving policy landscapes.

This edition of The Lens captures the unprecedented moment medtech finds itself in—one defined by both challenges and boundless possibilities. Few advancements are as electrifying as the integration of artificial intelligence into healthcare. We are thrilled to feature insights from Alan Cohen, General Partner at DCVC, whose TechMed thesis explores the revolutionary impact of AI and healthcare data on the industry’s future.

We also take a moment to reflect on 2024, with original analysis from Jon Norris and the team at HSBC, presented in their HSBC Innovation Banking Venture Healthcare Report. Their findings highlight sector-specific growth in areas like neurology and neuromodulation, increased funding for urological and gynecological innovations, and the leadership role cardiovascular M&A continues to play in delivering life-changing technologies to patients.

As we embark on this journey into 2025, we remain steadfast in our commitment to equipping you with the insights, connections, and tools needed to thrive in this vibrant and ever-evolving industry. On behalf of our entire team, we are honored to be part of your journey and your success.

Here’s to a year filled with progress, purpose, and shared triumphs.

All the best,

Scott Pantel and Henry Peck

Scott Pantel Chief Executive Officer, LSI Editor-in-Chief

Henry Peck Chief Business Officer, LSI Editor-in-Chief

De-risk your biggest strategic decisions with our most comprehensive market data and projections (worldwide sales, share by supplier, CAGRs) on 27 major market segments and 200+ sub-segments, prepared with consistent methodologies and forecast periods.

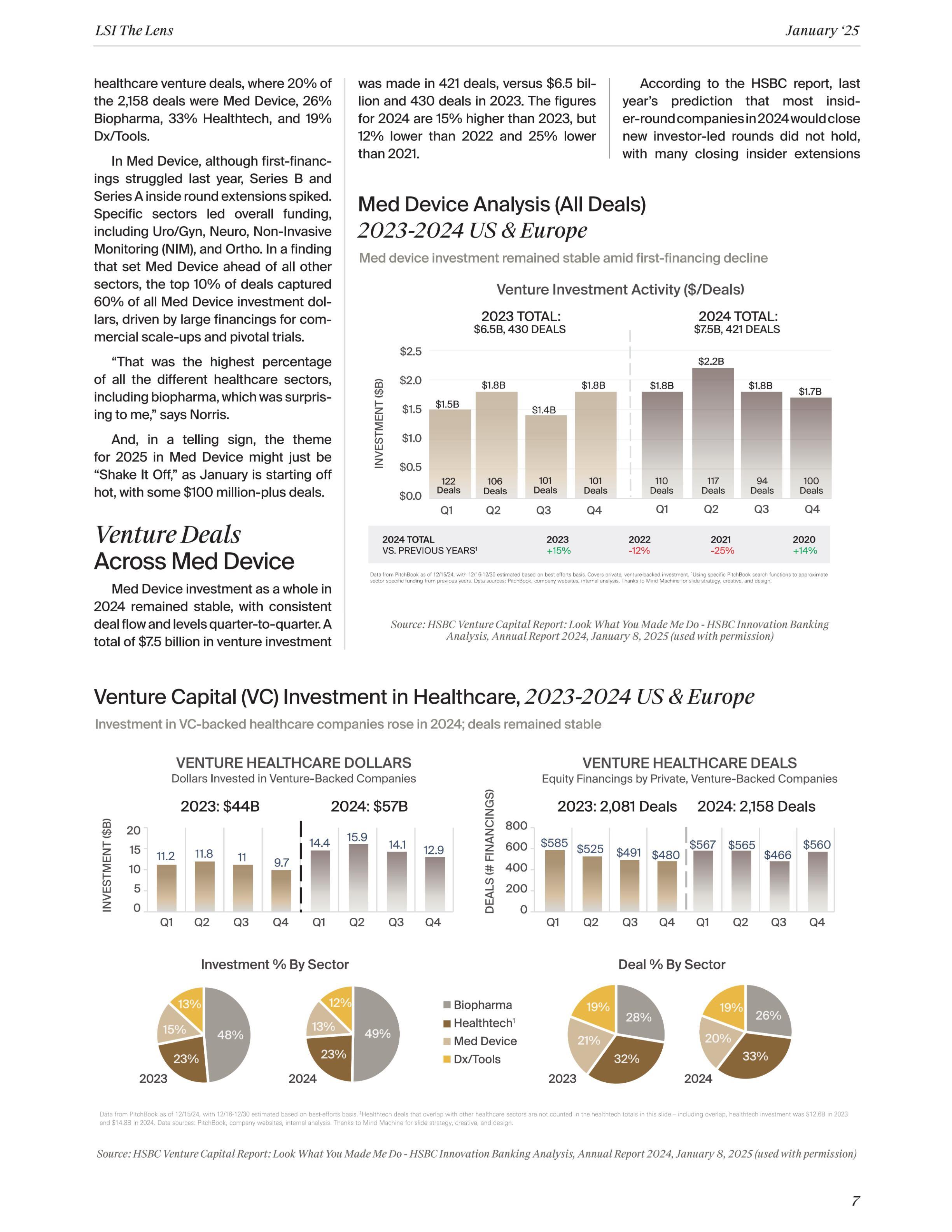

HSBC’s Annual Venture Healthcare Report reveals a resilient VC-backed healthcare space in 2024, dominated by mega early rounds or derisked, later-stage deals. Med Device stood out with the top 10% of deals capturing 60% of all investment dollars. In 2025— which is starting off strong—a diversified investor pool will balance bold new bets with strategic portfolio support, saving dry powder for the kind of company everyone wants to have: high potential.

For HSBC Innovation Banking’s Managing Director, Jonathan Norris, the theme of his 2024 Venture Healthcare Annual Report, “Look What You Made Me Do,” is not only in homage to Taylor Swift’s hit song but it references the altered state of healthcare investing in 2023 to 2024, after the turbulent, record investment and aggressive valuations experienced from 2020 through the first half of 2022. That phase of furious market activity began counter-balancing in 2023, as public market struggles and the lack of significant private M&A activity led venture firms to prioritize portfolio triage, deciding which of their companies they need to support because they do not have enough dry-powder capital to support them all, Norris describes. Inside rounds prevailed in 2023. Then, in 2024, driven by large therapeutic deals, novel technologies like AI-powered diagnostics, minimally invasive therapies, and precision health tools, new deal activity resumed, with a 30% rebound in dollars being invested—albeit with a clear shift and investor focus.

“At some point investors have to be strategic with the dry powder they have left in their funds, which companies are they going to support or not? And that’s what I mean by, ‘look what you made me

do,’” Norris said in a recent conversation with The Lens. “There hasn’t been a ton of distributions for venture firms back to their limited partners (LPs), and so they’re very hesitant about going out and fundraising until they have those distributions. And how do they get them? By supporting their best companies, at the expense of companies they have questions about or are not doing as well,” he continues.

As detailed in the HSBC report, across healthcare as a whole—including the sectors of Biopharma, Med Device, Healthtech and Dx/Tools—the challenges of securing follow-on financing, particularly Series B rounds, dampened some early-stage activity in 2024, resulting in fewer Seed and Series A deals. Investors have instead leaned toward a “strength in numbers” play for Series A: larger syndications raising large early-stage rounds, including $100 million or larger mega rounds—which is much different from what we’ve seen in the past—or else investors have shifted their focus to later-stage, derisked opportunities. (Also see the LSI Market Intelligence Deals table on page 24 of this issue, and “Long Game Legends: Makower and Papiernik’s Playbook for Success,” The Lens, Dec. 2024.)

The pressure is on in 2025 for both companies and investors, says Norris. Many companies that raised add-on or inside rounds in 2023 are now “on the clock,” he says, as they are facing pressure to secure new investor-led financing or risk consolidation or shutdown. And, the increase in investment in 2024 comes as investors face pressure from LPs to demonstrate returns before raising their next fund. Distributions from exits have been challenging in recent years, and this casts uncertainty on the timing of future fundraising, according to the report.

All of this is not to say that healthcare investment is in a negative place—it definitely is not. A total of $57 billion was invested in venture-backed healthcare companies in 2024, up from $44 billion in 2023, though with only 77 more deals in 2024 (2,158 vs. 2,081 in 2023), according to the HSBC report. In fact, the top 10% of these healthcare deals (216 deals) accounted for $30.2 billion in investment, representing 53% of all venture healthcare dollars.

By sector, 13% of the venture capital healthcare dollars last year were in Med Device, compared to 49% Biopharma, 23% Healthtech, and 12% Dx/ Tools. This compares to the number of

instead. However, the unexpected surge in new investor-led, later-stage financings highlighted the ongoing disparity between “haves” and “have nots.” Incredibly, the top 10% of Med Device financing attracted 60% of all investment dollars, the highest percentage among all sectors covered in the HSBC report.

A strong mix of capital sources drove later-stage financing last year, including traditional VC, growth, private equity, and crossover investors. Additionally, corporates from pharma, diagnostics, and medtech returned to the Med Device market, funding both larger and smaller deals. This diversity represents the most varied funding sources for Med Device in a decade, which is a positive sign for the sector, says the HSBC report.

The 20 largest financings in 2024 supported both commercial and development-stage projects. Eleven deals focused on commercial 510(k) products, two funded commercial PMA/De Novo deals, and seven were pre-commercial financings, including three development-stage PMA and four PMA pivotal trials, notes the report.

Typically challenging Series B venture deals stood out in 2024, with 47 new financings closed during the year. Among the 27 deals with valuation data,

15 were up rounds, seven were flat, and only four were down rounds.

“For the companies that are doing really well, there is capital out there in the Series B,” says Norris. “When we say there were 47 deals, you have to put that into perspective because that comprised just 11% of all deals in 2024, which means there’s still a lot of Series A companies out there that are on insider rounds that have no ability to raise that Series B. They’re still hoping to hit some sort of value inflection point to get a new investor to come in.”

Looking at all Med Device investment by indication in 2024, NIM, Orthopedic, and Vascular attracted investment, while Neuro and Cardio remained stable. Neuro maintained its leadership in Med Device investment, with brain/computer interface technologies (Blackrock, Precision, and INBRAIN) securing three of the top eight largest neuro financings. Neurostim technologies dominated, featuring in 21 of 46 deals in this area, led by Nalu, SPR, ShiraTronics, and Cala Health. The HSBC report points out that despite strong investment, neurology saw more flat and down rounds, 11 combined, than up rounds (five).

NIM, sensor-based technology that captures important patient data, rebounded strongly, surpassing $1 billion investment in 2024, says the report. Cardiovascular and metabolic secured 11 NIM deals each, followed by six deals in vital sign monitoring and uro/gyn.

$48M/8Deals

$88M/13 Deals

$131M/21 Deals

$85M/10 Deals

$48M/8Deals

$46M/6 Deals

$88M/13 Deals

$154M/7 Deals

“Urology/gynecology is a really interesting area, and I feel like we’re seeing a lot more activity there. Not only in interventional technologies but also in imaging, and in noninvasive monitoring and pelvic floor training,” adds Norris.

$131M/21 Deals

$97M/11 Deals

$85M/10 Deals

$103M/14 Deals

$46M/6 Deals

$154M/7 Deals

$40M/11 Deals $126M/12 Deals

$97M/11 Deals

$103M/14 Deals

$36M/5 Deals $15M/1 Deal

$40M/11 Deals

$126M/12 Deals

$53M/6 Deals $27M/6 Deals

$36M/5 Deals $15M/1 Deal

$33M/8 Deals $13M/1 Deal

$53M/6 Deals $27M/6 Deals

$33M/8 Deals $13M/1 Deal

$48M/8Deals

$131M/21

$48M/8Deals

$88M/13 Deals

$46M/6 Deals $154M/7 Deals $97M/11 Deals

$36M/5

Deal

Vascular and orthopedics investment also grew in 2024, according to the report. Ortho deals focused on both implant technologies (19 deals) and surgical robotics (seven deals; for more details see the Orthopedic Surgery Market Dive, The Lens, December 2024), while vascular financing included five $50-million-plus deals: two for commercial 510(k) products and three in clinical stages.

/ 8 Deals

$36M/5 Deals $15M/1 Deal

$53M/6 Deals $27M/6 Deals #33M/8 Deals $13M/1 Deal

Looking at imaging, investment has experienced significant annual fluctuations ranging between $500 million and $1 billion a year since 2020, according to the HSBC report. With a crowded market and limited acquirers, the focus in imaging has shifted to technologies that enhance therapy planning and guidance. In 2024, oncology and cardiovascular were the leading areas for imaging investments. A few examples include CapsoVision, a company with an innovative endoscopic capsule technology that raised $65 million, wearable MRI company Openwater that raised $54 million, and cardiovascular imaging company SpectraWave that brought in $50 million.

Cardiovascular investment in 2024 remained steady compared to 2023, but was down 15-20% from 2020-2022 levels. There were seven deals exceeding $40 million, including four in development or feasibility trials, two in pivotal trials, and one commercial-stage deal, according to the HSBC report.

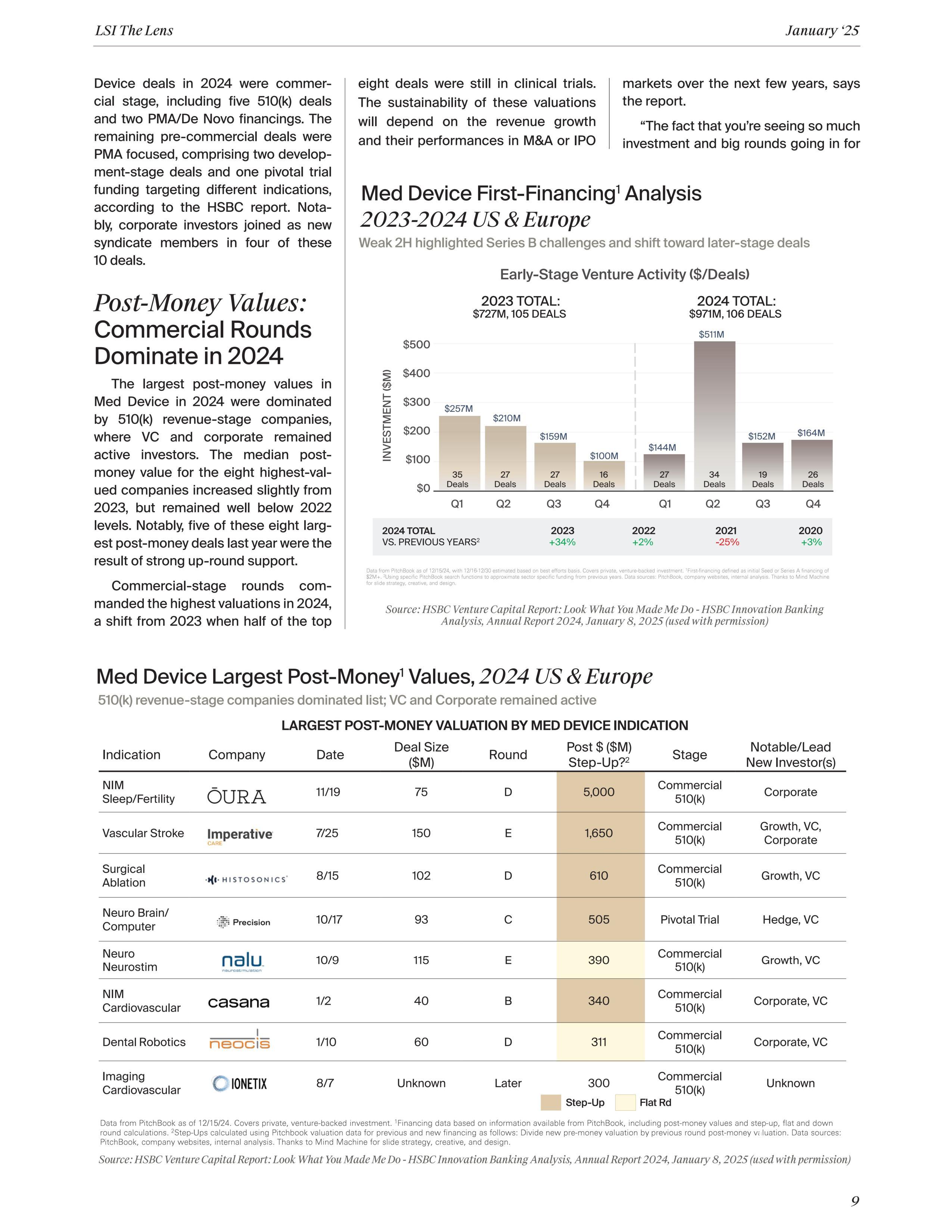

Speaking of commercial stage, these types of revenue-generating deals dominated larger Med Device venture investment in 2024, says the HSBC report. Seven of the 10 largest Med

Founded: 2021, as a spinout from the University of Oxford

Headquartered: London, UK

Technology: Fully implantable, adaptive neuromodulation therapy to treat mixed urinary incontinence

Financing: Series A

Amount: $100 million—one of the largest Series A rounds ever in Europe for a medical technology company

Deal Announced: June 10, 2024

Investors: The round was led by New Enterprise Associates (NEA) as part of a syndicate of new investors F-Prime Capital, Lightstone Ventures, and Intuitive Ventures, alongside existing investors Oxford Science Enterprises and 8VC

Founded: 2021

Headquartered: Amsterdam, The Netherlands Technology: Platform for AI-powered protein engineering; company reports that its technology has significantly sped up R&D projects between 1.2 and 12x, with cost reductions of up to 90%

Financing: Series B

Amount: $73 million

Deal Announced: November 26, 2024

Investors: Led by IVP with participation from previous investors Index Ventures and Kindred Capital

Founded: 2021, as a spin-out from UCLA

Headquartered: Malibu, CA

Technology: Microsurgical robotics; its flagship product, Polaris, combines state-of-the-art robotics, advanced medical imaging, and AI to push the boundaries of surgical precision, empowering surgeons to exceed current limitations

Financing: Series A

Amount: $30 million

Deal Announced: October 16, 2024

Investors: Led by ExSight Ventures and an undisclosed major corporate investor, with participation from Main Street Advisors and University of California (UC Investments), among others.

Sources: HSBC Venture Capital Report: Look What You Made Me DoHSBC Innovation Banking Analysis, Annual Report 2024, January 8, 2025; LSI Market Intelligence

these late-stage companies, I think it represents real optimism from folks who understand the market, that they believe that the IPO market will open up again. And I feel it’ll open again fairly soon for a small group of high performers,” says Norris.

Corporate investors participated in half of the top-valued deals in 2024, reflecting strong interest in supporting commercial growth. However, corporates are more willing to assume the dual risk of clinical and reimbursement challenges when the product aligns with their domain expertise, notes the HSBC report. Also, corporate syndicate members are more likely to acquire their device investment. In Med Device since 2018, M&A by a corporate that was also an equity investor yielded the highest percentage (15%), among healthcare sectors.

In 2024, a total of $971 million of private, venture money was invested in 106 total Seed or Series A Med Device deals of $2 million or more, according to the HSBC report. On the bright side, this dollar total was 34% higher than 2023, which saw $727 million invested in 105 first-financing deals. Looking back in time, however, the total invested in 2024 was just 2% above 2022, 25% less than 2021, and 3% higher than 2020.

What’s more, as noted in the figure, although investment levels stabilized in 2024, as compared to the decline in 2023, quarterly activity was inconsistent. The third and fourth quarters only saw 19 and 26 deals, respectively, for a total of $316 million, versus the anomaly that occurred in Q2, with $511 million invested in 34 deals (the three largest early-stage first financings of 2024, announced in Q2 and Q4, are detailed in the sidebar).

Annualized 2H 2024 investment shows total funding below 2023, trailing the prior three years by more than 40%, according to the HSBC report.

“The second half of 2024 was not very strong for early-stage Med Device,” says Norris. “And if you put that into context, it’s way behind previous years. The question is, is that a blip or is that the trend line? Will we see a billion-dollar investment year in 2025?”

New investors, drawn to the lower financing risk, attractive valuations, and potential for faster exits, showed a preference for later-stage investments last year, leading to an uptick in Series B investments in 2024, offering some relief to Series A early-stage companies funded in the previous few years. However, new Seed and Series A deals struggled to attract attention under these dynamics.

In a positive sign for 2025 and beyond, Norris notes that a lot of VCs have raised new funds, but they each tend to invest in just a few Med Device deals a year, he says. This includes investors like F-Prime Capital, NEA, Lightstone Ventures, Deerfield Management, and Vensana Capital. Vensana just announced in January the closing of Vensana Capital III, with $425 million in committed capital. The fund was oversubscribed at its hard cap with the support of the firm’s existing limited partners alongside select new institutional investors, and it brings Vensana’s total capital under management to approximately $1 billion.

“You’re seeing a lot of really good brand name VCs. You just don’t see them doing more than two or three deals,” says Norris. The problem for entrepreneurs is how do you thread the needle of

which VC firm still has an open slot looking for a company in your area, at your stage. It’s difficult. I think that we will see an uptick in large Series A syndicated investment in 2025, as investors band together to lead larger Series A deals with multiple investors. This will provide ample dry powder to help mitigate Series B financing risk.”

The rapid pace of medical device innovation is being powered by emerging technologies like AI and ML, to enhance early disease detection, improve diagnostic accuracy, and reduce the need for invasive procedures, among other game-changing benefits (also see the TechMed cover story featuring perspective from Alan Cohen of DCVC, and the BPH Market Dive in this issue). These advanced technologies are being supported by regulatory bodies such as CMS and FDA, with the FDA having approved approximately 1,000 medical devices driven by AI and ML to date for potential use in clinical settings. These and many other early-stage tech-enabled devices will be in high demand across the diagnostic and therapeutic landscape in the coming years, as illustrated by venture investment in 2024, and two of the three biggest early-stage deals, detailed previously.

According to the HSBC report, by Med Device indication, urology/gynecology, NIM, and neuro exceeded 2023 first-financing investment in 2024: uro/ gyn with $154 million in seven deals, up from $46 million in six deals in 2023; NIM saw a significant resurgence and reached $126 million in 2024, up from $40 million in 11 deals in 2023; and neuro deals totaled $88 million in 13 deals, compared to $48 million in 8 deals in 2023. Neurology reversed a four-year decline in early-stage funding, with half of the deals leveraging neurostim or brain/computer interface technologies.

In terms of valuation in Med Device in 2024, smaller Seed and Series A deals, particularly Software as a Service (SaaS) companies, commanded higher premoney valuations with four of the top five in NIM and imaging solutions, says

“I think that we will see an uptick in large Series A syndicated investment in 2025, as investors band together to lead larger Series A deals.”

– Jonathan Norris

the HSBC report. These include Dynocardia, BrainTemp, CairnSurgical, and Sonavex, all with pre-money valuations higher than $30 million.

Notably, four of the top six pre-money valuations in smaller Series A deals ($15M and smaller) were Series A extensions, underscoring the challenge of finding new Series B lead investors.

Neurostim and brain/computer interface technologies continue to attract substantial pre-money valuations for Series A deals, including Paradromics ($250 million pre-money), Invicta ($50 million pre-money), and Otolith ($46 million pre-money), all of which were Series A extensions, according to the report.

Orthopedic and NIM technologies both saw multiple financings with $70 million-plus pre-money valuations, including orthopedic deals Icotec and Cionic, and NIM deals Allez Health and Dynocardia. Two of these four deals were Series A extensions.

“What I’m finding is a lot of these higher pre-money valuation deals are Series A extensions. These companies should have raised their Series B and didn’t, but instead they raised an extension with their existing investors,” adds Norris. “These companies hope to use the additional capital to hit crucial value creation milestones to enable Series B investment by a new lead investor.”

Uro/Gyn interest continued to grow; neuro and NIM exceeded 2023 investment

Uro/Gyn

After a weak first half of last year for exits, Edwards Lifesciences and Stryker spurred a Q3 M&A rally, and the Ceribell IPO shined.

According to HSBC’s analysis, exits in the first half of 2024 were slow, with only three exits. In Q3, there was a significant uptick in M&A, with nine deals, including three led by Edwards. There were 14 venture-backed M&A deals in 2024, the highest since 2021.

Six deals in 2025 have already surpassed the $100 million mark, setting a positive tone for the year.

financing increased to 11.9 years in 2024, more than double 2021’s 5.8-year median. This extended timeline may be contributing to the decline in first financing, notes HSBC.

Edwards and Stryker drove M&A momentum in 2024 with three deals each, while Hologic completed two. (56)

While Q4 ‘24 saw limited private M&A activity with only two deals, it marked the year’s first Med Device IPO. Sunnyvale, CA-based Ceribell, in the NIM and Neuro categories with its AI-powered, rapidly deployable, point-of-care electroencephalography platform designed to address the unmet needs of patients in the acute care setting, priced its IPO on October 10, 2024. It

raised $180 million in IPO proceeds at a pre-money step-up from its last private round and has since traded to nearly two times its IPO post-money value, generating public market excitement for 2025. Ceribell’s IPO marked the first growth medtech IPO since October 2021. However, revenue predictability, and achieving profitability on IPO proceeds remain critical factors for future IPO candidates, says the HSBC report.

The report also points out that the median time to M&A exit from first

The new year is off to a brisk start in the Med Device fundraising space, with nearly $1 billion raised between January 1st and 15th, spanning a variety of market sectors. Incredibly, six deals in 2025 have already surpassed the $100 million mark, setting a positive tone for the year. What’s more, the new year already features a number of venture syndicates in action, that collectively are boosting many promising cutting-edge medical technologies over their clinical and regulatory hurdles.

After a weak 1H 2024, Edwards, Stryker spurred Q3 M&A rally; Ceribell IPO shined

Multiple acquisitions have already been announced in 2025, including Stryker’s planned acquisition of venous thromboembolism device company

Inari Medical for $4.9 billion, Boston Scientific’s $664 million purchase of Bolt Medical, and the completion of Hologic’s $350 million acquisition of Gynesonics. FIRE1, developer of the Norm heart failure management system, completed a $120 million financing round, led by Polaris Partners and Elevage Medical Technologies, joined by new investors Sands Capital and Longitude Capital, and existing investors Andera Partners, Gilde Healthcare, Gimv, the Ireland Strategic Investment Fund, Lightstone Ventures, Medtronic, NEA, Novo Holdings, and Seventure Partners (FIRE1 also received FDA Breakthrough Device Designation and has been accepted into the agency’s Total Product Lifecycle Advisory Program (TAP)).

Along with these deals, in January, Saluda Medical closed a $100 million financing to support its novel closedloop, dose-control neuromodulation platform for treating chronic pain. Existing investor Redmile Group led the round, with other existing investors Wellington Management, TPG Life Sciences Innovation, Fidelity Management & Research Company, Action Potential Venture Capital participating, and new investor Piper Heartland Healthcare Capital.

Wearable insulin delivery device company CeQur closed a $120 million financing round, investors undisclosed, to support its four-day wearable insulin patch technology.

In another hefty deal, Aspect Biosystems, a biotech company pioneering the development of bioprinted tissue therapeutics as a new category in regenerative medicine, closed a $115 million Series B financing round. The financing was led by Dimension, with participation from existing and new investors including Novo Nordisk, Radical Ventures, an undisclosed leading global investment firm, InBC, Pallasite Ventures, Pangaea Ventures, Rhino Ventures, and T1D Fund: A Breakthrough T1D Venture.

Also in January, Alleviant Medical, a privately held medical device company developing a no-implant atrial shunt for heart failure, announced a $90 million

financing to fund its second pivotal trial. Led by Gilde Healthcare, the round also adds Omega Funds and includes participation from existing shareholders S3 Ventures, RiverVest Venture Partners, Vensana Capital, Longview Ventures, Gilmartin Capital, TMC Venture Fund, and undisclosed strategic investors.

The new year already features a number of venture syndicates in action, that collectively are boosting many promising cuttingedge medical technologies over their clinical and regulatory hurdles.

Francis Medical, a privately held developer of an innovative and proprietary water vapor ablation therapy for the treatment of prostate, kidney, and bladder cancer, announced the completion of an oversubscribed $80 million Series C equity financing, the largest fundraising round to date for the company. Arboretum Ventures and Solas BioVentures co-led the Series C round. New investors Orlando Health Ventures and two additional strategics joined this round, along with previous investors Coloplast A/S and Tonkawa

The Series C proceeds will continue to fund the VAPOR 2 pivotal clinical study for the management of prostate cancer and the development and U.S. commercialization of its Vanquish Water Vapor Ablation proprietary prostate cancer treatment, expected by the end of 2025.

In another large deal announced in January, Cornerstone Robotics, a surgical robotics company, announced it raised more than $70 million in Series C funding. EQT led the round, with participation from Qiming Venture Partners, Alpha JWC Ventures, the Innovation and Technology Venture Fund, eGarden Ventures, CTS Funds, K2VC, and Long-Z Capital.

Also in the robotics space, Chinese robotics firm Fourier booked nearly $109 million in a Series E round, backed by Saudi oil giant Aramco's Prosperity7 Ventures. The Chinese asset management firm Peakvest and multiple investment companies from Shanghai, including the state-backed Guoxin Investment and Zhangjiang Science and Technology Venture Capital also participated. The company designs and produces exoskeleton and robotic rehabilitation products that are innovating the rehabilitation process. The company has developed upper body (arm) and lower-limb solutions, and it also has a humanoid robot.

Adding to the deals announced in January, Zeto, a medical technology company revolutionizing electroencephalogram (EEG) diagnostics with its cutting-edge devices and AI-driven cloud platform, announced the recent successful closing of a $31 million funding round. The round was led by MindWorks Global, a Michigan-based investment entity.

GT Medical Technologies, a medical device company focused on improving the lives of patients with brain tumors, completed a $37 million first close of a Series D financing round. The financing was led by Evidity Health Capital, alongside new investor Accelmed Partners. Also participating were existing investors MVM Partners, Gilde Healthcare, and Medtech Venture Partners. The funds will accelerate the completion of the ROADS clinical study that is focused on GammaTile for newly diagnosed brain metastases, and the GESTALT clinical trial for patients with newly diagnosed glioblastomas. In addition, the funds will support the continued commercialization of GammaTile, the company's FDA-cleared bioresorbable radiotherapy implant for the treatment of brain tumors.

LSI’s Market Intelligence Software Platform is your one-stop-shop for global market sizing and analysis, procedure volume data, startup company and deal tracking, curated insights, and more.

Scan the QR code to learn more!

Celebrating recent leadership shifts and other announcements and accolades impacting our global medtech community.

Adagio Medical, a leading innovator in catheter ablation technologies for treatment of cardiac arrhythmias, announced that founder Olav Bergheim departed as CEO and Chairperson of the Board of Directors of the company, effective December 13, 2024. Concurrently, the company announced the

appointment of LSI alumni Todd Usen as CEO and Director of the company, and Orly Mishan as Chairperson of the Board of Directors, effective December 13, 2024. Before joining Adagio, Todd served as President and CEO of uterine health company and LSI alumni Minerva Surgical, where he successfully restructured the organization, completed successful financings, and drove significant top-line growth. Prior to that, he was CEO of Activ Surgical, also an LSI alumni company, overseeing FDA/CE clearance of advanced surgical imaging technology and leading four fundraising rounds totaling over $92 million.

Augmedics, a pioneer in augmented reality surgical navigation, has named Paul Ziegler as its president

and CEO, filling the vacancy created when Kevin Hykes left for neuromodulation company CVRx. With the appointment, LSI alumni Gwen Watanabe will

transition from interim CEO and serve as Vice Chair of the Board. Ziegler, a 20-year med device veteran, assumes leadership as the company enters a new phase of commercial growth. In November, Augmedics announced a new milestone of 100 patients treated in a single week, as well as FDA clearance for a new CT-Fluoro registration method for the xvision Spine System that greatly expands navigation access for spine surgeons.

Freyja Healthcare, founded in 2017, is focused on improving the standard of women’s health in surgical and in-office procedures to enable physicians to provide safe, effective care. The company recently appointed LSI alumni Kurt Azarbarzin, former CEO of EndoQuest Robotics and Verb Surgical, and founder of SurgiQuest, to its Board of Directors. Azarbarzin has also held senior roles at CONMED Corporation, U.S. Surgical, and Tyco Healthcare.

Hyperfine, an LSI alumni company that has redefined brain imaging with the first FDA-cleared, AI-powered, portable magnetic resonance (MR) brain imaging system, the Swoop system, announced the appointment of Chi Nguyen as Vice President of Office Strategy and Partnerships, and Rafael Donnay as Vice President of Hospital Strategy and Health Economics, to provide leadership in key growth areas. These strategic leadership appointments bolster the capability of Hyperfine to drive commercial adoption in hospital inpatient and outpatient settings and expand to neurology office settings.

Integra LifeSciences President and CEO Jan De Witte retired on January 6, 2025, with former 3M Health Care President Mojdeh Poul replacing him

at the LSI alumni tissue regeneration and neurological treatment technology company. De Witte joined Integra in December 2021. Before joining 3M, Ms. Poul held global business leadership positions of increasing responsibility at Medtronic and Boston Scientific. In these roles, she accelerated penetration of neuromodulation and emerging cardiovascular technologies and therapies through the deployment of multifaceted market development strategies.

Intuitive Surgical has announced three executive promotions to strengthen the surgical robotics market leader’s leadership team and position the company for continued growth. Henry Charlton, a 21-year Intuitive veteran

who took on the CCO role in 2022, is moving up to the role of EVP and chief commercial and marketing officer, after having served in key leadership roles across multiple geographies (U.S., Europe and APAC) and global distribution and commercial organizations, regional marketing, global customer

services and commercial enablement functions. Gary Loeb, who joined Intuitive in 2022 as SVP and general counsel, now shifts to the role of EVP and chief legal and compliance officer. In the post, he oversees legal and governance functions and ESG reporting while serving as chief compliance officer. Jamie Samath is taking on the position of EVP, CFO and enterprise technology leader. Having originally joined the company in 2013, Samath became CFO in 2022 and enterprise technology leader in 2024.

LSI alumni Lazurite, developers of the first wireless arthroscopic surgical camera system, ArthroFree, (powered with aerospace-grade batteries used in spacesuits, on the International Space Station, and in satellites, following early support from NASA), announced that Mark Froimson, MD, has been appointed as the new CEO, after joining the company in 2018 as Chairman of the Board. During this transition, Lazurite’s founder and former CEO, as well as inventor of ArthroFree, Eugene Malinskiy, will take on the role of Chief Product and Technology Officer, to advance the next generation of ArthroFree products, including ArthroFree S4k and T4K. Dr. Froimson is also principal of Riverside Health Advisors, specializing in financing and accelerating healthcare innovation. He serves as chief medical officer for AngelMD, chairs the boards of Lazurite and Thrive, and is a board member for Pacira Biosciences, Sintx Technologies, and several nonprofits including the Arthritis Foundation.

Moon Surgical, a pioneer in laparoscopic surgical innovation, announced the appointment of Chris Toth as an

independent member of its Board of Directors. With over 20 years of experience in scaling and managing commercial operations, Toth brings extensive expertise in commercial acceleration. He is currently Executive Vice President and Group President of Baxter

International’s Kidney Care segment, which will be named Vantive upon completion of its pending sale to Carlyle by Baxter. Toth is the named CEO of Vantive. Prior to his current role, Toth was the CEO of Varian, a Siemens Healthineers company (and LSI alumni), where he spent 20 years in a variety of leadership roles, including President of Global Commercial and Field Operations.

LSI alumni Moon Surgical’s Maestro System is pioneering a new category in soft tissue surgery, addressing the critical need for efficiency in smaller operating rooms and outpatient settings. With its ability to support high-volume procedures while maintaining surgeon control and operational consistency, Maestro is uniquely positioned to transform the care of the 20 million soft tissue procedures performed annually worldwide.

NeoPredics AG Switzerland, a leader in predictive analytics and clinical decision support for maternal and neonatal health and LSI alumni, announced that Stefan Verlohren, MD, PhD, will

join the company as Chairman of the Medical and Scientific Advisory Board, effective January 1, 2025. Prof. Verlohren is a Professor of Obstetrics and the Chairman and Director of the Department of Obstetrics and Fetal Medicine at University Medical Center Hamburg-Eppendorf, Germany, with over two decades of experience in maternal-fetal medicine and an extensive background in clinical innovation.

NeoPredics also announced the appointment of medtech industry vet and LSI alumni Todd Usen as Chairman of the Board. With career highlights that include leading Minerva Surgical through an organizational transformation, spearheading the commercialization of Activ Surgical’s groundbreaking AI-powered technology, and driving global growth initiatives at Olympus Medical, Usen’s influence on the healthcare industry is both broad and profound. His passion for advancing

women’s health aligns perfectly with NeoPredics’ mission to deliver innovative solutions that improve outcomes for mothers and children.

Mike Karim, a seasoned life sciences entrepreneur, has joined Singaporebased Synapto Ventures as Venture

Partner, where he will lead business development activities in the United Kingdom, Europe and the U.S., including client relationship management and fundraising execution. Karim is currently mentoring start-ups and entrepreneurs, and providing support to life science companies through his company Mike Karim Consulting. He also contributes to the healthcare and medical industry through leadership roles in NHS governance and industry associations. Previously he was the CEO and co-founder of Oxford Endovascular Ltd., a spinout from the University of Oxford, developing a next-generation brain aneurysm flow diverter treatment (Karim presented Oxford Endovascular at LSI USA ‘24).

Gal Noyman-Veksler, PhD, a Partner at Tel Aviv, Israel-based VC firm Lionbird and a behavioral researcher, investor, and entrepreneur focusing on innovation in tech and healthcare, has been recognized on the “40 Under 40” list for 2025 by TheMarker, a Hebrew-language daily business newspaper.

At LionBird, Dr. Noyman-Veksler invests in U.S.-focused early-stage tech and scientific-driven startups looking to reset healthcare’s relationship with technology. She is passionate about using AI and big data to understand human behaviors and finding digital solutions to help users lead a better, healthier, and happier life, manage chronic conditions and improve general well-being, as described on her LinkedIn profile.

As an LSI alumni, Dr. Noyman-Veksler participated on two panels at LSI Europe ‘24 in Portugal: AgeTech Headwinds and Training & Supporting the Next Wave of Entrepreneurs.

March 17th - 21st, 2025

Waldorf Astoria, Monarch Beach, Dana Point, CA

In 2024, LSI USA convened 1,500 executives from emerging companies, venture capital and private equity firms, family offices, global strategics, professional service providers, ecosystem partners and more.

Registration and applications to present are now open for LSI USA ‘25. Get in touch to learn more about the event.

Highlights: Novel AI and implantable brain-computer interface technologies gain traction, migraine neuromodulation implant moves to pivotal stage, and wearable robotics company makes a public offering.

Anteris Technologies Global Corp., founded in Australia with offices in Minneapolis, MN, is developing the balloon-expandable DurAVR transcatheter heart valve for the treatment of severe aortic stenosis. The DurAVR device is the first biomimetic valve, which is shaped to mimic the performance of a healthy human aortic valve and aims to replicate normal aortic blood flow.

The company recently announced the closing of its initial public offering (IPO) of 14.8 million shares of its common stock in the U.S., at a price of $6.00 per share, resulting in aggregate gross proceeds of approximately $88.8 million. An additional 2.2 million shares of common stock are issuable pursuant to the underwriters’ option to purchase additional shares, if exercised in full. ATGC’s common stock is listed on NASDAQ under the ticker symbol AVR.

The DurAVR device, developed in partnership with the world’s leading interventional cardiologists and cardiac surgeons, is made using a single piece of molded ADAPT tissue, Anteris’ patented anti-calcification tissue technology. ADAPT tissue, which is FDA-cleared, has been used clinically for over 10 years and distributed for use in over 55,000 patients worldwide. The DurAVR transcatheter heart valve (DurAVR THV) System consists of the DurAVR valve, the ADAPT tissue, and the balloon-expandable ComASUR Delivery System.

Anteris currently intends to use the net proceeds from its IPO, together with its existing cash and cash equivalents, primarily for the ongoing development of its DurAVR THV and the preparation and enrollment of a randomized global pivotal study of DurAVR THV for treating severe aortic stenosis, with the remaining for working capital and other general corporate purposes, including the repayment of amounts owed under its convertible note facility.

Cleerly has developed an artificial intelligence-driven tool that uses coronary computed tomography angiography (CCTA) to generate a 3D model of patients’ coronary arteries and noninvasively measure plaque, vessel narrowing and the likelihood of insufficient blood flow. The company has generated evidence that shows its system is better than experts at assessing vessel narrowing, plaque volume and composition, helping it to recently secure Medicare coverage for the technology. It has also received a CPT Category I code for advanced plaque analysis.

Cleerly recently raised $106 million in a Series C extension funding round, led by global software investor Insight Partners and joined by Battery Ventures, with participation from pre-existing investors. With this new funding, Cleerly will continue to scale its commercial growth and clinical evidence generation, helping healthcare professionals improve outcomes for patients across the coronary care pathway.

In October, five Medicare Administrative Contractors (MACs) officially approved Cleerly’s AI-Quantitative Coronary CT (AI-QCT) scans for Medicare recipients exhibiting stable and acute symptoms suspicious of coronary artery disease. The new coverage took effect on November 24, 2024, for Palmetto GBA, CGS Administrators, National Government Services, and WPS administrative groups, and took effect for Noridian on December 8, 2024, impacting approximately 67 million Medicare beneficiaries. The new Medicare coverage will include Cleerly Labs Plaque Analysis for patients with acute or stable chest pain and no known CAD, as well as CAD-RADS 1-3. Additionally, the American Medical Association recently approved a permanent CPT Category I code for Cleerly’s AI-QCT advanced plaque analyses, effective January 1, 2026.

Cleerly’s AI-QCT technology, in several studies comparing it with invasive gold standards, has been demonstrated to be highly accurate in the assessment of the presence, extent, and composition of coronary atherosclerotic plaque and similar to consensus readings of Level 3 Expert Physician Readers. Cleerly ISCHEMIA, an additional AI-enabled product, has also been proven to demonstrate high diagnostic performance compared to invasive fractional flow reserve (FFR) and higher performance than such legacy tests as nuclear SPECT imaging and FFRCT.

Tempus AI, a technology company advancing precision medicine through the practical application of artificial intelligence in healthcare, recently announced a new decision by CMS that will allow reimbursement for assessments of cardiac dysfunction using the Tempus ECG-AF algorithm. ECG-AF is one of just a few FDA-authorized medical technologies in the country to be impacted by the new CMS decision, and this milestone allows Tempus to more broadly support clinicians in identifying patients at increased risk of atrial fibrillation/flutter.

Per the CMS policy to allow payment for certain Software as a Service (SaaS) devices in the hospital outpatient setting, CMS has assigned associated procedure codes for assessments with assistive algorithms like Tempus’ ECG-AF (CPT 0764T and CPT 0765T) to APC 5734, which has a Medicare rate of $128.90, effective January 1, 2025. This ruling is expected to allow hospitals to receive reimbursement for using Tempus’ ECG-AF to help identify patients at increased risk of AF.

Earlier this year, Tempus received 510(k) clearance from the FDA for the Tempus ECG-AF device, which was the first FDA clearance for an AF indication in the category known as “cardiovascular machine learning-based notification software,” and paved the way for clinicians to use this innovative algorithm in the care of their patients.

In other cardiac AI news, Philips and Mayo Clinic have entered a collboration aimed at advancing MRI for cardiac applications through AI. Under the collaboration, Philips aims to leverage Mayo Clinic’s proprietary AI technology in combination with its own. This combination could help reduce MRI scan times and improve the efficiency needed to relieve the burden on healthcare professionals. With AI, the two organizations say less experienced radiographers could potentially perform complex cardiac MRI exams. In addition to CT scans, MRI can prove useful when treating congenital heart disease or disease affecting the heart muscle. However, high costs and limited availability often hinder access to high-quality MRI, according to Philips.

Additionally, the research partnership intends to look at the potential of lower-field-strength MRI solutions, developed by Philips, to enable MRI installations in a broader range of applications. They also provide safer scanning options for individuals with implants sensitive to high magnetic fields.

Axoft, a Cambridge, MA-based neurotechnology company, is on a mission to unlock new treatments for patients suffering from neurological disorders by producing implantable

brain-computer interfaces (iBCIs) that answer critical unmet needs. The company recently announced the approval of its first-in-human clinical study, which will take place early this year at The Panama Clinic. The study will demonstrate the usability of Axoft’s novel soft materials that mimic the mechanical properties of brain tissue and are tailored to improve the stability of the tissue-electronics interface for iBCIs. Axoft’s study marks the first time this type of bio-inspired material is authorized for human use. The study will include up to five patients undergoing existing brain resection surgery. Study participants will be awake during the testing of Axoft’s iBCI, allowing for the decoding of volitional brain activity.

Axoft grew out of research from Dr. Jia Liu’s Lab of Bioelectronics at Harvard University, and the company has secured a licensing contract with the institution. In 2024, Axoft published papers outlining the capabilities of its novel brain implant technology in Nature Nanotechnology and Nature Neuroscience

Minneapolis, MN-based ShiraTronics has designed a minimally invasive implantable neuromodulation system, the ShiraTronics System, that offers a new and potentially more effective treatment option to address the symptoms of migraines. The fully implantable, programmable device goes just beneath the skin in the head, where it delivers precise electrical pulses tailored to disrupt migraine pain signals. The device offers precise, 24/7 electrical neuromodulation to reduce the frequency and intensity of migraine attacks, and could allow patients to maintain their daily activities with fewer disruptions, according to the company.

The company recently initiated an FDA investigational device exemption (IDE) pivotal trial to evaluate the company’s neuromodulation therapy for chronic migraine. The RELIEV-CM2 Clinical Study will implant up to 148 patients across the U.S. and Australia to assess the long-term safety and potential efficacy of ShiraTronics implantable neuromodulation therapy. Unlike other approaches that primarily manage migraine symptoms, the ShiraTronics System is designed to provide preventive, sustained relief for those who experience 15 or more headache days per month and have not achieved success with other treatments. For many of the millions who live with the challenging effects of chronic migraine, this novel approach could represent a potential new therapy option.

The device won FDA breakthrough device designation in 2021. ShiraTronics completed enrollment for its RELIEV-CM pilot study for the device in February 2024. In October 2024, the company raised $66 million to support the launch of its trial.

Inotec AMD, based in Cambridge, United Kingdom, has developed continuous topical oxygen therapy (cTOT) solutions that enhance healing and improve patients’ quality of life The company recently closed a $33 million Series C financing round, led by existing investors Amadeus Capital Partners, Meltwind, Puhua Capital, and the Wealth Club. The

financing marks a major milestone in the company’s mission to heal every chronic wound and improve patients’ lives on a global scale.

The proceeds from this round will be strategically used to secure national reimbursement in the U.S. for the company’s flagship cTOT product, NATROX O₂, ensuring broader accessibility for patients across the US. Additionally, the funds will support the expansion of the company’s leadership team, strengthening its global capabilities to drive future growth and innovation.

NATROX O₂ delivers a continuous flow of oxygen directly to the wound, creating an optimal environment for healing. NATROX O₂ has set new standards in wound care, providing a non-invasive, wearable solution that enables providers to offer a simple, user-friendly therapy designed to accelerate healing, even in wounds that have persisted for years such as diabetic foot ulcers, venous leg ulcers, pressure injuries, and non-healing surgical or traumatic wounds.

More than 100 million people in the world suffer from wounds that will not heal. In the U.S., wound care costs the health system an estimated $97 billion annually, with chronic wounds making up $50 billion of that expense.

FastWave Medical is a clinical-stage device company developing a portfolio of highly deliverable intravascular lithotripsy (IVL) catheters to treat artery calcification. The company, founded in 2021 and headquartered in Minneapolis, MN, recently announced the close of a $19 million funding round, increasing the total capital invested into the company to over $40 million. The latest investment was led by Epic Venture Partners, with participation from M&L Healthcare Investments and the company’s existing investors. The funds will fuel FastWave’s development momentum and provide support for ongoing regulatory and clinical initiatives for its product portfolio.

In May, the company announced successful 30-day results from the first-in-human study of its intravascular lithotripsy (IVL) technology. The prospective, single-arm study aimed to assess the IVL system’s safety and feasibility in patients with peripheral arterial disease (PAD) affecting the superficial femoral artery (SFA) and popliteal artery with moderate to severe calcium.

According to a news release, investigators successfully treated eight patients with moderate to severe calcified occlusions in the SFA and popliteal arteries. Evidence supported early safety and feasibility of the IVL system. Findings included 100% procedural success and 0% peri-procedural adverse events. FastWave reported 5.9% mean residual diameter stenosis post-therapy. At 30 days, the company also reported zero major adverse events, 100% patency and 0% revascularization.

Calcific plaque, which is prevalent in about 30% of CAD patients, resists vessel expansion, making it difficult to treat with traditional interventional modalities. FastWave Medical states on its website that it is elevating IVL delivery with a reduced crossing profile, optimized shaft for better trackability, a sleek, rupture-resistant design, and hands-free energy delivery with an improved generator UI that offers real-time procedural feedback.

LaNua Medical, a start-up spun out of University College Dublin (UCD), is developing an innovative technology that makes it easy, safe, and cheaper for doctors to treat internal bleeding, vascular malformations and many benign and malignant tumours.

The company has raised $6.3 million in seed funding to develop Ecore, a device that targets embolization procedures and aims to help improve patient outcomes, lower hospital costs, minimize duration of hospital stays, and reduce stress and procedure times for practitioners.

The funding will accelerate product development and market access, with a focus on the U.S. The funding round was co-led by Elkstone and Atlantic Bridge, with participation from Enterprise Ireland and Furthr VC. The funding will be used to accelerate product development and market access.

LaNua’s pioneering Ecore device allows doctors to restrict blood flow in a targeted segment of veins or arteries while still allowing ancillary medical tools such as guidewires and catheters to pass through it. The innovative device design will safely complement liquid and microparticle embolization, including localized intravascular radiation procedures performed by interventional radiologists worldwide. Exposure to x-ray radiation is also reduced for both patient and practitioner, and lowers the risk of human errors like inadvertently blocking blood flow to healthy adjacent organs. The company says the device will be adaptable for use in many areas of the human body to treat multiple disease states.

LaNua was founded in 2024 by interventional radiologist Dr. Cormac Farrelly, Tom Fitzmaurice (ex-Medtronic VP) and UCD biomedical engineers Dr. Eoin O'Cearbhaill and Dr. Sajjad Amiri.

Myomo, a Boston, MA-based wearable medical robotics company that offers increased functionality for those suffering from neurological disorders and upper limb paralysis, announced that it has priced an underwritten public offering of 3,000,000 shares of its common stock at a public offering price of $5.00 per share. Myomo expects the gross proceeds from this offering to be approximately $15 million, before deducting the underwriting discount and other offering expenses.

Myomo has developed and is marketing the MyoPro product line. MyoPro is a powered upper-limb orthosis designed to support the arm and restore function to the weakened or paralyzed arms of certain patients suffering from cerebrovascular accident (CVA) stroke, brachial plexus injury, traumatic brain or spinal cord injury or other neuromuscular disease or injury. It is currently the only marketed device in the U.S. that, sensing a patient’s own EMG signals through non-invasive sensors on the arm, can restore an individual’s ability to perform activities of daily living, including feeding themselves, carrying objects and doing household tasks. Many are able to return to work, live independently, and reduce their cost of care.

Sotelix Endoscopy is a Baltimore, MD-based startup developing next-generation therapeutic endoscopy devices for minimally invasive procedures dependent on the closure of gastrointestinal (GI) tract tissue, without the need for incisions.

The company recently announced the closing of a $1.7 million seed round financing, from individual investors, among them some of the world’s leading endoscopists, experienced medical device entrepreneurs, and other investors with clinical, technical, and business expertise. The investment will fund

the company’s research and development efforts, including in vivo testing of its innovative device.

Sotelix Endoscopy was founded by Dr. Mouen Khashab, a Professor of Medicine at Johns Hopkins University School of Medicine and one of the world’s leading endoscopists. The leadership team includes co-founder Dr. Venkata Akshintala, an associate professor at Johns Hopkins University School of Medicine and pioneer in gastrointestinal medical device development; chairman Mohamad Khachab, a successful entrepreneur and investor; and CEO John Schellhorn.

Marlborough, MA-based CardioFocus, a device company dedicated to advancing ablation treatment for cardiac arrhythmias, recently announced the first series of patients treated with the investigational OptiShot Pulsed Field Ablation (PFA) System for the treatment of paroxysmal atrial fibrillation, as part of the VISION AF clinical trial. The first-in-human trial will treat up to 50 patients in the coming months with 12-month follow-up planned, including critical remapping procedures to validate the efficacy of this novel technology.

The OptiShot balloon catheter is unique among the advanced generation of PFA catheters, with its ability to deliver circumferential lesions to the pulmonary veins with endoscopic visual confirmation of electrode-tissue contact, according to study researchers.

CardioFocus is taking a portfolio approach to PFA. In addition to OptiShot, CardioFocus will continue clinical trials evaluating the investigational QuickShot PFA System, a large area focal ablation catheter that integrates with various navigation technologies. In the EU, CardioFocus has treated over 6,000 patients with the Centauri PFA System, which uses a proprietary monopolar waveform with marketed contact-force sensing focal ablation catheters and mapping systems.

NanoVibronix, a device company that produces the UroShield, PainShield and WoundShield Surface Acoustic Wave (SAW) Portable Ultrasonic Therapeutic Devices, today announced it has renewed its exclusive distribution agreement with Ultra Pain Products, Inc. (UPPI) for the distribution of the company’s PainShield for another five years, with a minimum purchase commitment of $12 million. The company’s

decision to renew the distribution agreement comes in recognition of UPPI’s growth over the past four years and its evolution into a leading force in the non-opioid pain management and injury recovery industry.

NanoVibonix’s proprietary technology allows for the creation of low-frequency ultrasound waves that can be utilized for a variety of medical applications, including for disruption of biofilms and bacterial colonization, as well as for pain relief. The devices can be administered at home or in any care setting, without the continuous assistance of medical professionals.

MeMed, a developer in the emerging field of advanced host response technologies, recently announced that the FDA has granted Breakthrough Device Designation to its innovative MeMed Severity test, used to help manage patients with suspected acute infections and suspected sepsis by empowering clinicians with timely, data-driven, clinical insights.

Building on the scaling adoption of the FDA-cleared MeMed BV test, which redefines how clinicians differentiate between bacterial and viral infections, MeMed Severity aims to aid clinicians in rapid risk stratification and predicting disease progression, in conjunction with clinical assessments and other laboratory findings.

The test is based on advanced host-response technology that measures multiple proteins from a blood sample and uses machine learning to stratify the risk of a patient with a suspected acute infection deteriorating to severe outcomes within 72 hours or death within 14 days. Designed for emergency department settings, it has the potential to support critical decisions on triage, treatment, and optimized patient disposition.

With easy-to-interpret results in under 15 minutes, compatibility with high-throughput analyzers and minimal blood volume requirements, MeMed Severity will integrate into clinical workflows, driving value for both care providers and patients. The Breakthrough Device Designation will accelerate MeMed Severity's path to market, supporting reimbursement strategies, and ensuring that this critical tool reaches healthcare providers as quickly as possible.

Irish maternal health company NUA Surgical has secured €6.5M ($6.6 million) in Series A funding, led by EQT Life Sciences. The round was also supported by new investors Kidron Capital and the Texas Medical Center Venture Fund, and existing investors including Enterprise Ireland and business veterans from Ireland and the US. The proceeds will be used to drive the regulatory clearance and early commercialization of the company’s product, the SteriCISION C-Section Retractor, specifically designed to address the unique challenges of Caesarean-section (C-section) surgery.

With this new investment, the Nua Surgical Board will be strengthened with several experienced female board members. Anne Portwich, Partner at EQT, and Anula Jayasuriya, Co-Founder of Kidron Capital, will join as Board Directors, while Gabrielle Guttman of TMC Venture Fund and Prashanthi Ramesh of EQT will serve as Board Observers.

C-sections are the most common major surgical procedure globally, with over 30 million performed each year. The SteriCISION C-Section Retractor is ergonomically designed to provide fast, adjustable, and safe retraction, enabling clinicians to deliver the baby, repair tissue, and crucially, identify bleeds. As a single-use sterile device, it aims to reduce the risk factors that lead to surgical complications, benefiting the patient, clinician, and the healthcare system. The new investment will support Nua Surgical's next phase of development and the early commercialization of SteriCISION.

“This is a meeting where we find the best quality—size of the meeting, the venue—it’s conducive to proper one-on-one meetings and multiple interactions with entrepreneurs. The entire ecosystem shows up at the LSI conference."

Dr. Luc Marengère

Managing Partner,

TVM Capital Life Science

The industry’s most comprehensive and trusted global procedure database, with coverage of 300+ diagnostic and therapeutic procedures across 37 countries.

Fred Alger Management, T. Rowe Price Associates, Mumtalakat, Parkway Venture Capital, Breyer Capital, Tizvi Traverse, S32, US Innovative Technology Fund, Ava Investors, Eric Schmidt, Marc Benioff, Yann LeCun, and others

Your one-stop-shop for global market sizing and analysis, procedure volume data, startup company and deal tracking, curated insights, and more. Scan QR code for details.

Fund (led), Nexus NeuroTech Ventures (led), Action Potential, Johnson & Johnson, Lightstone, Lux, Google Ventures (GV), OSF Ventures, Ascension Ventures, TriVentures, Reimagined Ventures, Peak6,

The integration of advanced AI, machine learning, and computer vision tech with medical devices, dubbed the TechMed revolution, is a bold, empowering new chapter happening now in healthcare, and differentiated from MedTech, describes Alan Cohen, General Partner at DCVC. This data-driven new era is poised to improve patient outcomes worldwide.

Not all that long ago, groundbreaking medical technology began to change healthcare as we know it. Advanced, hardware-centric devices impacting the lives of patients during the MedTech Revolution, ranging from transcatheter heart valves to knee replacement implants, have improved patient outcomes and quality of life for problematic and prevalent health conditions. Today, the traditional, $500-billion-a-year

Source: LSI Europe ‘24

medtech industry is being overshadowed by the transformational power of data, in a bold new era in patient-centered healthcare, coined by Alan Cohen, General Partner at deep tech venture capital firm, DCVC as TechMed.

Cohen, whose keynote address at LSI Europe ‘24 in Sintra, Portugal in September 2024, “The TechMed Movement Has Arrived,” offers a thought-provoking

view on the emerging but current impact of data and deep tech in healthcare. This tech-enabled movement represents a shift from traditional medical technology, to a data-first, innovation-driven approach aimed at empowering healthcare professionals and transforming patient outcomes, describes Cohen.

"TechMed is a speciation event—a new species emerging from medtech,

driven by a technology-first approach," he told the audience.

Cohen’s tech background and role at DCVC parallels his futuristic, but realistic view. He been a successful entrepreneur, technology executive, and board member for over 25 years for a range of companies including DCVC-backed Illumio, Nicira (acquired by VMware), Airespace (acquired by Cisco), Cisco (where he led the $25 billion enterprise marketing and solutions organization), General Growth Properties, and IBM

The TechMed paradigm represents the evolution of traditional medtech by integrating advanced technologies such as sensors, machine learning (ML), and proprietary datasets, says Cohen. This approach prioritizes technology as the foundation for medical applications, rather than retrofitting existing medical disciplines. By blending advanced artificial intelligence (AI), ML, and computer vision with hardware, TechMed companies—differentiated from their MedTech brethren—are poised to tackle some of the healthcare industry’s most difficult and long-standing challenges.

Advancements in the use of AI/ML are enabling the identification of population trends and the ability to forecast health outcomes by evaluating enormous amounts of medical data, including images, test results, and patient records. These powerful, novel capabilities promise to offer healthcare professionals a whole new level of diagnostic accuracy, individualized treatment strategies, and effective patient monitoring, that hold the potential of democratizing access to high-quality care, reducing costs, and improving patient quality of life worldwide.

And, the term TechMed is catching on big time within industry. NVIDIA, a leader in AI hardware and software, promoted the term at the recent annual J.P. Morgan Healthcare Conference in San Francisco. Tom Oxley, CEO of Synchron, described in a LinkedIn post and in presentations that there is a new, fast-growing and high-potential sector that is data-first in healthcare, TechMed, that they are calling Digital Devices, that is comprised of robotics and Brain Computer Interfaces (BCI). This is akin to the “'TechBio” subset of Biotech that is data-first, according to Oxley. To the Medtech analysts and VCs, he says this is real, it is coming, and it is big.

Here we take a look at the main takeaways from Cohen’s keynote and his vision of TechMed, which he presented to the LSI Europe ‘24 audience as offering unprecedented opportunity for the MedTech and healthcare ecosystem.

The seamless integration of hardware and software is a driving force behind transformative medical technologies, enabling more accurate diagnostics, streamlined workflows, and improved treatment outcomes, notes Cohen. As a powerful example, innovative medical devices are combining AI with imaging tools to identify anomalies with a level of precision that was once considered impossible. Robotic-assisted surgery platforms use 3D imaging and haptic feedback to allow surgeons to perform minimally invasive procedures with enhanced precision. This fusion is also being used to improve workflow efficiency, such as automating data collection and analysis in hospitals to reduce the burden on clinicians and increase operational efficiency.

"Hardware and software are fusing in transformative ways, changing how we approach healthcare," he says.

A central theme of the TechMed revolution is its ability to empower rather than replace healthcare professionals, says Cohen. Tools like AI-assisted imaging systems enable radiologists to interpret scans faster and more accurately, while wearable technologies provide nurses with real-time patient vitals, allowing for timely interventions.

TechMed innovation focuses on providing tools that enhance the capabilities of medical practitioners, ranging from sonographers to surgeons. For instance, AI-powered guidance systems allow non-specialists to perform tasks like capturing diagnostic-quality images, helping to alleviate workforce shortages. This democratization of expertise means that care can reach more patients, particularly in underserved areas.

“The goal is to give superpowers to people to do their job better, to be more effective,” emphasized Cohen.

AI and machine learning are unlocking new possibilities across the healthcare continuum. Examples include Caption Health’s use of AI to guide imaging and diagnostic tools (more about Caption Health on the next page), as well as semantic AI, which creates hyper-detailed anatomical models. These innovations are revolutionizing areas like personalized medicine, where algorithms analyze a patient’s unique characteristics to tailor treatments.

• More actionable, precise, and accurate care

• Reduced costs through scalable technology

• Broader global accessibility

• Integration of care into everyday life

"Machine learning and neural networks collect information from the periphery and bring it back—just like what we do in medicine," notes Cohen.

Despite AI's transformative potential, its adoption in healthcare lags behind other industries, he says. Cohen emphasized the urgency for the medical device sector to harness AI for diagnostics, digital therapeutics, and clinical insights.

He also introduced the concept of "Semantic AI," focusing on using AI to create highly detailed anatomical models and improve the understanding of the body's interactions with drugs, devices, and procedures. Semantic AI is poised to revolutionize healthcare by integrating and visualizing diverse health data streams, including lifestyle,

medical interventions, and environmental factors.

"Semantic AI will enhance our ability to understand human anatomy and its interactions with medical interventions down to the millimeter," he describes.

Data is the backbone of the TechMed revolution. And, the transition from static, point-in-time measurements to continuous, real-time data flows is enabling more proactive and personalized care, says Cohen. Wearables, implants, and monitoring devices are now capable of generating dynamic datasets that allow clinicians to detect issues early and intervene proactively. For instance, platforms like Sickbay aggregate data from multiple devices to monitor for conditions such as sepsis or heart failure, enabling faster and more informed clinical decisions, he notes.

"Using AI to enhance healthcare outcomes is dramatically more important than building models to write marketing copy," says Cohen.

In effect, Cohen notes, both in his keynote address and in his thesis entitled “The TechMed movement has arrived,” that TechMed companies cultivate a “data river” rather than a data moat, a continuous and dynamic flow of data that spans the entire patient lifecycle, from diagnostics to intra-procedures, and post-procedure phases. The depth, breadth, and constant updating of these datasets ensure they remain comprehensive and relevant, with each new data input enhancing the model’s capabilities. This contrasts with traditionally “siloed” institutional data stores that are fragmented, narrow in scope, and quickly become stale, Cohen notes.

This concept aligns with the growing trend of real-time health monitoring and adaptive care models. For the medical device industry to thrive, leveraging continuous, real-time data from implants, wearables, and other devices is crucial, Cohen continues. "To fulfill the promise of TechMed, we must move from static snapshots to dynamic, real-time insights."

TechMed is as much about purpose as it is about innovation. Many TechMed pioneers are inspired by deeply personal experiences, driving them to create solutions with lasting societal impact. For Cohen, when his father, a Navy corpsman providing medical care during the Korean War, was diagnosed with glioblastoma in 2016, he talked Cohen into leaving the tech industry and doing something that would have a more long-lasting impact on society. Based on his father’s impact on troops during the war, he chose the field of medicine.

“To fulfill the promise of TechMed, we must move from static snapshots to dynamic, real-time insights.”

– Alan Cohen

This mission-driven mindset fosters TechMed innovations that prioritize accessibility, affordability, and meaningful change. For instance, autonomous robotics, like those being developed by Remedy Robotics, leverage advanced robotics inspired by self-driving cars, and aim to provide precision care in remote settings. The implications of this advancement can also help address long-standing concerns with global disparities in healthcare access, says Cohen.

Drawing from his work with AI pioneers, Cohen underscores the role of neural networks and machine learning in advancing medical technologies. Two DCVC-backed companies exemplify the TechMed thesis: Proprio and Caption Health, he describes.

Proprio is a surgical navigation and intelligence company focused initially

on spine procedures like posterior spinal fusions to correct curvature of the spine. The company’s flagship product, the Proprio Paradigm platform, revolutionizes the surgical process by providing AI-guided visualization and data-driven insights that improve precision, efficiency, and patient outcomes. It relies on an advanced array of sensor technologies including lightfield imaging, which captures visuals with far more depth and dimensionality than traditional cameras. The company’s system gives surgeons real-time 3D guidance akin to “surgical GPS,” continuously mapping and adjusting the operative field to ensure optimal implant placement and spinal alignment. It leverages computer-vision AI models built from analyzing hundreds of prior procedures by world-class surgeons across 250+ gigabytes of multi-modal operating room data per procedure. This proprietary data pipeline allows Proprio’s system to improve with every surgery, learning new techniques and adjusting for any intraoperative changes.

In 2023, Proprio secured landmark FDA 510(k) clearance as the first such AI-guided surgical navigation system for spine surgery. With a robust pipeline of further FDA submissions across other spine procedure types and ultimate ambitions to expand into orthopedics, neurosurgery, and more, Proprio is looking to become the default “co-pilot” platform, augmenting surgeons across myriad therapeutic areas.

Companies like Proprio demonstrate the strength of diverse expertise, blending machine learning, medical device engineering, and clinical knowledge to advance surgical technology. "The fusion of disciplines at Proprio shows how collaboration builds entirely new platforms for the industry," describes Cohen.

Caption Health, acquired by GE Healthcare in 2023, took a similar datadriven AI approach but for the imaging diagnostic realm. Its breakthrough product was an AI guide that enabled minimally trained operators to capture diagnostic-quality ultrasound image sequences on par with expert sonographers or cardiologists. By studying tens of thousands of prior exams, Caption’s AI learned to identify standard views and provide real-time instructions on properly manipulating the ultrasound wand.

For conditions like heart disease, which require assessing the heart’s ejection fraction, Caption’s “virtual instructor” democratized the ability to administer these studies at the point of care, rather than having to rely on scarce, trained staff constantly shuttling between imaging rooms and offices. Caption subsequently expanded its product into other use cases like lung imaging and maternal health, creating AI-guided imaging protocols for a variety of acute and chronic conditions, describes Cohen.

The human and economic impact of the TechMed movement is multifaceted and transformative, says Cohen. Unlike the slower innovation cycles of traditional MedTech companies, TechMed players like Proprio and Caption more resemble agile tech industry disruptors, he notes.

This new revolution is not just a technological shift but a profound transformation of how healthcare is delivered. By harnessing the power of data and deep tech, this movement holds the promise of democratizing access to high-quality care, reducing costs, and improving lives worldwide. And, it's already happening.

Ultimately, TechMed stands at the forefront of a healthcare transformation, promising better patient care, more efficient medical practices, and a more economically sustainable healthcare system, says Cohen. It also means that the traditional medical device business model faces disruption. Startups and incumbents alike must rethink how they deliver value, says Cohen. Subscription-based and value-driven pricing are emerging as sustainable models, aligning costs with benefits for providers and patients.

"If you provide a compelling solution for users, they will help pull you through on the business model," he describes. Cohen concludes his address with a call to action for MedTech innovators: the time to lead this change is now, and to work with tech-forward companies to not only innovate but to profoundly enhance human health. For those ready to embrace the TechMed vision, the possibilities for impact are immense.