A Page from Ray Cohen’s Playbook: Scaling, Exiting, and Winning in Medtech

Alumni Innovator Spotlights, Medtech Pulse Check, Electrosurgical Devices, and much more...

A Page from Ray Cohen’s Playbook: Scaling, Exiting, and Winning in Medtech

Alumni Innovator Spotlights, Medtech Pulse Check, Electrosurgical Devices, and much more...

February 2025

June 2025

September 7th - 11th, 2025

JW Marriott Grosvenor House, London

Now in its fourth year, LSI Europe has become a staple of the global Medtech and Healthtech community. The 2025 event in London will convene industry-leading startups, venture capital and private equity investors, strategics, and more.

Registration and applications to present are now open for LSI Europe ‘25. Get in touch to learn more about the event.

Scott Pantel

Chief Executive Officer, Editor-in-Chief

Rebekah Murrietta

Vice President of Media, Contributing Author

Benny Tomlin Contributing Photographer

Henry Peck

Chief Business Officer, Editor-in-Chief

Blake Matrone Sr. Marketing Manager, Contributing Author

Kristin Karkoska Contributing Photographer

Tracy Schaaf

Managing Editor and Content Strategist, Lead Author

Gavin Kennedy Business Development, Contributing Author

Paul Streeto Graphic Designer

Brenna Hopkins Sr. Manager of Content Programs, Lead Author

Almonte Customer Service & Fulfillment

Nicholas Talamantes

Sr. Director of Market Intelligence, Contributing Author

Kelly Williams

Subscriptions & Enterprise Sales

Vol. 2, No. 6 June 2025

Created by LSI, The Lens leverages LSI’s deep industry relationships and proprietary market intelligence to help executives like you build lasting medtech companies. Start your Individual, Group or Enterprise-Wide subscription today!

Scan QR Code to activate your subscription.

The Lens is published monthly and available in print and electronic formats. Copyright 2025 by Life Science Intelligence, Inc. All rights reserved. Editor takes care to report information from reliable sources and does not assume liability for information published.

Interested in subscribing? email to: info@ls-intel.com

Interested in advertising? email to: kelly@ls-intel.com

Dear Readers,

We are fresh off of LSI Asia ’25, our first-ever summit in the Asia-Pacific region and our tenth event since reimagining what a medtech summit could be. The format we built was made to match the pace and ambition of the executives driving this industry forward. And in Singapore, the pace and ambition were on full display.

Nearly 75 early and growth-stage companies took the stage, representing breakthroughs from across the globe. Their presentations were compelling not just for what they pitched but for what they proved: medtech’s center of gravity is global, and its next era will be shaped by operators who know how to move fast, stay lean, and execute with clarity.

You’ll see more coverage of these companies in upcoming editions of The Lens.

That spirit of clear-headed execution is exactly what Ray Cohen brought to the cover story of this issue. Cohen has led some of the most successful exits in medtech history, including Axonics and SoniVie (both acquired by Boston Scientific). But what sets him apart isn’t just the dollar amounts. It’s his no-nonsense, all-in leadership style that blends bold strategy with brutal transparency.

Cohen doesn’t sugarcoat. “If I build it, they will come” is a myth. Commercialization is war. Winning requires the right people, trained hard and treated well, with a plan that starts at the exit and works backward.

This issue also zooms in on a market entering a new chapter: electrosurgical devices. Fueled by the rise of robotic surgery and platform integration, our analysts project this space to grow from $10.2 billion in 2024 to $14.7 billion by 2029.

The implications go far beyond energy tools. What’s emerging is a competitive race to own the full surgical workflow, where hardware, software, and data converge inside the OR. From established giants like Intuitive and J&J to category-challenging players like Creo Medical and Novuson, the next wave of surgical innovation won’t just cut. It will connect.

Across this edition, you’ll find a common thread: the value of momentum—not hype, not noise, but real momentum. Built by teams who know what problem they’re solving, where their market is headed, and how to lead with impact.

Thanks for being a part of this growing community.

Let’s keep raising the bar.

All the best,

Scott Pantel Chief Executive Officer, LSI Editor-in-Chief

Henry Peck Chief Business Officer, LSI Editor-in-Chief

Need fresh inspiration for your medtech company as we navigate Q325? We’ve gathered insights from some of our LSI alumni thought leaders to help you stay ahead.

“If you have a Chief Medical Officer who’s like, ‘No, we’re staying in this space. I know it, I know it.’ Trust me, not all physicians understand the business side of this world.”

— Anita Watkins, Managing Director, Rex Health Ventures

LSI Europe ‘24 Panel: Light at the End of the Tunnel in Medtech Financing

“There’s no ‘fun’ in fundraising. It’s certainly not a character builder, but it sure reveals it.”

Dr. Luc Marengère, Managing Partner & Co-Owner, TVM Capital Life Science

LSI USA ‘25 Panel: Investors — Do The Best Operators Really Need You?

“Too many people are looking for win-lose deals … There is a middle ground where both parties feel like ‘I gave up a little more than I wanted to,’ ‘I paid a little more than I wanted to.’ When you get to that point, you know you got a good deal.”

— Ray Cohen, Chairman of the Board, SoniVie, Former CEO, Axonics

LSI USA ‘25 Signature Series: Building and Exiting Companies in Medtech’s New Post-COVID Financial Era

“Time kills all deals, kills all opportunities. You’ve got to move fast. The fuel for moving fast is capital.”

“Overcoming fear is the number one hurdle. Patients are now expected to do things like self-cannulation. We need to give them the confidence and tools to succeed.”

— Tim Fitzpatrick, Founder, Signals Group

LSI Europe ‘24 Panel: Alternate Sites of Service: Migration of Renal, Cardiac, and Surgical Care

— Christopher Shen, Partner, Novo Holdings

LSI USA ‘25 Signature Series: Current Market Perspectives from Shifamed and Novo Holdings

“When you take on investors, it’s not your company anymore.”

Dan Sands, Managing Director, Factor 7 Medical

USA ‘25 Panel: Founder ≠ CEO

“Relationships are more important than money. In the face of uncertainties, strong collaboration between investors and founders builds trust and enables success, even in the toughest challenges.”

— Marta Zanchi, Founder & Managing Partner, Nina Capital

LSI Europe ‘24 Fireside Chat: “Value-Add” is a Two-Way Street: Success Through Investor-Founder Partnerships

Health (led), Wellington Partners (led), Kfund, naturalX Health Ventures, redalpine, Khosla Ventures, Molten Ventures, Translink Capital, Verve Ventures

Your one-stop-shop for global market sizing and analysis, procedure volume data, startup company and deal tracking, curated insights, and more.

Ensweet Seed Telehealth for cardiac rehabilitation

Mutuelles Impact (led), AG2R La Mondiale, Angels Santé, Nord France Amorçage, 50 Partners, Finovam 2, MakeSense, several business angels

Tech Grant Assistive glasses frames for vision impairment

Zeiss Ventures (led), European Innovation Council Fund, Lednil,

Source: LSI USA ‘25

With four decades of company-building, IPOs, boardroom leadership, and monumental exits behind him, Raymond W. Cohen has become one of medtech’s most successful operators. But behind the financial wins—including the recent back-to-back $3.7 billion Axonics and $600 million SoniVie acquisitions by Boston Scientific—is a deeper story of Cohen’s contrarian, full-transparency, people-centered, no-BS approach to leadership and strategy.

“People crave inspired, authentic, and transparent leadership that thinks big and acts boldly. They want to be enrolled in a vision of what is possible, and be recognized and compensated for creating measurable results, not be fed a bunch of platitudes.”

A quote that is classic Ray Cohen blunt, unapologetic, no-nonsense, and grounded in hard-won experience. With more than four decades in medtech, Cohen has done what many aspire to— build, lead, scale, and sell high-stakes, successful ventures with precision and zero fluff. Known for his no-BS, direct approach, Cohen has turned startups into gritty, focused, execution-driven teams that deliver real results—and big exits—by staying lean, investing in sales and marketing, moving fast, and operating with a ruthless clarity of purpose.

On the LSI USA ‘25 stage in Dana Point this past March, in a discussion entitled “Building and Exiting Companies in Medtech’s New Post-Covid Financial Era,” with State of MedTech podcast host Omar Khateeb, and in a recent interview with The Lens, Cohen offered a glimpse into his personal playbook of successful strategies, best practices, and lessons learned. From growing up in a working-class immigrant household in Queens, NY, to leading back-to-back exits, including his crowning achievement, Axonics, sold to Boston Scientific for $3.7 billion (closed Nov. 2024), and SoniVie ($600 million, closed in May 2025 also to Boston Scientific), Cohen described that his approach, although at times boldly contrarian, has been simple: show up, go all in, execute relentlessly, share the wealth, and build something that actually helps improve patient’s quality of life.

Cohen served as the chief executive officer and member of the board of directors of Nasdaq-listed Axonics, an Irvine, CA-based medtech company developing best-in-class solutions for people with incontinence that he co-founded in 2013 and took public in late October 2018. Axonics ranked #1 on

the Deloitte Technology Fast 500 and the Financial Times ranking of the fastest-growing companies in the Americas in 2021 and 2022.

Cohen retired from the company following the closing of the acquisition. He led the epic deal and got it over the finish line, leveraging the deep relationships and trust he had earned with the Boston Scientific leadership team, going back to his days as CEO of the renal denervation company Vessix Vascular, that he sold to Boston Scientific in late 2012 (prior to the failed pivotal SYMPLICITY HTN-3 trial debacle in 2014).

Axonics’ success can be traced back to brash, “Cohen-esque” choices made along the way. For one, following Axonics’ IPO in 2018, Cohen threw out the standard commercialization playbook. Instead of hiring a small team and scaling slowly, Axonics went all in.

“People asked me during the IPO roadshow, how are you going to deploy the funds? I told them, despite the fact that we are perhaps as much as a year away from FDA approval, I’m hiring 100 salespeople for the launch, I’m going to guarantee them $20,000 a month, and I’m going to train the hell out of them. After all, we are competing with Medtronic, the largest medtech company on the planet that has enjoyed a monopoly and a 20-year head start on us,” he says.

“We hired 30 or 40 clinical specialists as well. The team trained intensely for an average of six months, so much so that you could wake them up at three in the morning, and they could jump out of bed and sing the company song. A silly expression but it got the point across.”

A lot of people told Cohen that he’s crazy and that’s not the way it’s done.

“I said, ‘well, that’s a common theme that I hear, but that’s what we’re going to do. And when the bell rings after we secure FDA approval, we’re going to hit the ground running on day one.’ And that’s what happened. When we got the green light, we launched like a rocket.”

Axonics’ sacral neuromodulation (SNM) system for the treatment of urinary and bowel dysfunction, the r-SNM System, a rechargeable, full-body MRI-compatible device, received FDA approval in late 2019. Subsequently, in March 2021, Axonics acquired Contura

and its flagship Bulkamid product for $225 million, a unique hydrogel to treat women with stress urinary incontinence. Bulkamid had no sales in the U.S. at the time of acquisition, but by 2024, annual revenue was ramping towards $100 million. In addition, a second embodiment of the Axonics system (the F15 recharge-free SNM system) was FDAcleared in March 2022.

The result of Cohen’s high-risk strategy? Twenty straight quarters of beating revenue targets. Axonics stock moved from an IPO price of $15 per share to $71, and then the $3.7 billion acquisition by Boston Scientific, closing a few days before Thanksgiving 2024.

“The strategy paid huge dividends for us, and we never looked back,” Cohen continues. “We just kept adding more high-quality, field-based commercial folks. In the end, of the 900 people in the company, about 500 were in sales or clinical support roles, 95% in the U.S. In my opinion, you need more salespeople and clinical specialists than any other roles in your company.”

When building a company, Cohen is deliberate about who he hires and why.

“An effective team shapes up like a pizza pie,” he says. “The perfect pie, in terms of a team, is that you have all these pointy people, meaning they each have a very specific expertise. What I’ve always tried to do is gather a group of highly specific experts and then fit them together. Now you’ve got the perfect circle of individuals who all have expertise in different areas. Then the key is to get them to work collaboratively as a team. I don’t want to hire a bunch of generalists because you won’t have the expertise that is needed.”

Cohen also believes in treating team members with respect, compensating them well, and providing them with a meaningful equity stake. This not only fosters loyalty but also drives performance.

“When I find great people, I’ve made it a point to stay close to them, treat them with respect, pay them well, provide equity and excellent

Omar

Khateeb and Ray Cohen onstage at LSI USA’ 25 -

“Signature Series: Building and Exiting Companies in Medtech’s New Post-Covid Financial Era”

company-sponsored health benefits. Bottom line, make sure they have a good experience. To the extent that their expertise is needed again, I will invite them to join the next venture. It’s ideal to bring people together with mutual trust and respect. You can’t accomplish anything by yourself. It’s all about people. High-performing people have been the key to success in all my ventures.”

Cohen describes that at first at Axonics, it was all about feet on the street: well-trained people with a great product who are aggressively going after the business. But commercialization success doesn’t just happen.

“Having a product that’s safe and effective, and perhaps better than your competition, is just the start of it all. There’s no such thing as ‘if I build it, they

“You can’t accomplish anything by yourself. It’s all about people. High-performing people have been the key to success in all my ventures.”

will come.’ To this day, some entrepreneurs still believe that. And it’s ridiculous,” he says.

Based on his wide and varied experience, Cohen offers his philosophy and advice to startups on device commercialization.

“The skill sets of people that are required to commercialize are very different than they are to develop a product, to run clinical studies, etcetera,” he says. “The question for early-stage

companies is, do you want to take this project all the way to commercialization? I think it might be a mistake. However, if you want to do that, you’d better hire people who have the right experience—and be prepared to pay them. It’s really hard if you’re a single-product company and now you’re going to try to commercialize your product. It’s very challenging when you are the new kid on the block. Physicians and hospitals are often reluctant to change the status quo.”

After Axonics, Cohen shifted gears— but not his pace.

On the very night that the Axonics deal closed in November 2024, and to cure Cohen’s concern about not being busy enough, he became chairman of

privately held SoniVie, an Israeli developer of a renal denervation system to treat hypertension. In March 2025, he joined PE-backed Spectrum Vascular, which markets vascular access products, as an independent board member. In addition, as an independent board member, he supported Kestra Medical Technologies’ March 2025 $232 million oversubscribed IPO. In April 2025, Cohen joined peripheral nerve neurostimulation company, Nalu Medical, as chairman.

Then, as this issue of The Lens approached publication time, Cohen agreed to become vice chairman of privately held hydrogel maker, Tulavi. Cohen is also now chairman of Archimedes, a startup that just got funded by Sherpa Healthcare Partners, where Cohen serves as a venture partner.

Cohen’s style remains bold but boundary-respecting.

“As chairman, your job is to support and guide strategy, not to run the company. You influence through the CEO,” he says.

“As chairman, your job is to support and guide strategy, not to run the company. You influence through the CEO.”

Cohen’s philosophy on exits is clear, but somewhat controversial: “The best time to sell a company is before you ship the first commercial product,” he advises.

This strategy hinges on presenting a fully developed, regulatory-approved, commercially ready product that hasn’t yet faced the challenges of commercialization. By doing so, companies can maximize valuation while minimizing operational and adoption risks, he advises.

A prime example is the sale of SoniVie to Boston Scientific, announced this March, as Cohen described for the LSI

USA ‘25 audience. SoniVie developed the TIVUS Intravascular Ultrasound RDN System, designed to denervate nerves surrounding the renal artery to treat hypertension. Boston Scientific held an equity stake of approximately 10% in SoniVie. The transaction consists of an upfront payment of $400 million and up to $200 million upon achievement of FDA approval.

As chairman, Cohen describes that he negotiated the deal directly with Boston Scientific’s leadership, bypassing traditional investment banking channels.

“Why incur a cost of banking fees when we had the buyer at the table?” he quipped, emphasizing the value of trust and direct communication in deal-making. “I was able to save the company money and get the deal done in record time. Of course, it was a heck of a lot of work, however, the juice was worth the squeeze.”

Beyond exits, Cohen has a keen eye for identifying when to pivot and when to pursue public offerings. His approach involves assessing the total addressable market, and ensuring a robust reimbursement path. Cohen’s ability to craft and communicate a compelling vision has been instrumental in attracting investors and strategic partners alike.

Kestra Medical is a prime example. “In order to execute a successful IPO, you need a big story, i.e., a big TAM, and a good storyteller,” Cohen told the LSI USA ‘25 audience.

Cohen preaches and practices straight talk with investors, and offers innovators his blunt advice.

“Don’t get hung up on dilution … 100% of nothing is nothing, but 1% of a billion dollars can change your life.”

hundred percent of nothing is nothing, but 1% of a billion dollars can change your life.”

“If you’ve never raised capital, not only do you need a large, underserved market and a compelling, differentiated product, you need to find someone with some gray hair, scars on their back, the right relationships and proven results. You need someone who can speak the investors’ language and help them believe,” he says.

When it comes to communication, he also emphasizes full transparency.

“Keeping investors or board members engaged is really important. If you get the question ‘how’s it going?’ from someone who’s been funding your company, you are screwing up. You need to keep folks upline and downline informed.”

His advice? Push updates to the team. The good, the bad, and the scary stuff. Be real.

“One of the things I would do every weekend morning is sit down and provide an update to the board and copy the executive management team. Here’s what’s going on, folks. These are the initiatives we agreed to, this is the progress we’re making. Here’s what we sold last week, last month, those kinds of details. Flat out push the data to the board members. Because once again, if you’re at an early stage, these are your shareholders,” Cohen says. “The absence of information is the worst possible thing, given that people typically will come up with a story that is worse than the actual facts.”

His mantra is to always share facts, set direction, and enroll stakeholders in the solution.

Cohen’s nuggets of wisdom offer valuable lessons for medtech entrepreneurs:

• Think Exit Early: Identify potential acquirers from the outset and tailor your strategy accordingly.

“Don’t get hung up on dilution,” he says. “You are going to need capital, so don’t be worried about dilution. One

• Prioritize People: Invest in building a strong, cohesive team that can execute flawlessly.

Raymond W. Cohen is an accredited public company director with over 40 years of experience in the life sciences industry. He co-founded Axonics, leading it to a successful IPO and subsequent $3.7 billion acquisition by Boston Scientific.

From 2010 to 2012, he served as CEO of Vessix Vascular, a venture capital-backed renal denervation company that was acquired by Boston Scientific. Previously, he spent nearly a decade as chairman and CEO of Nasdaq-listed Cardiac Science, which was ranked as the fourth-fastest growing company in the U.S. in 2004. From 2006 to 2021, Mr. Cohen served as chair of the board of directors at BioLife Solutions, a developer and manufacturer of preservation media for regenerative medicine. From 2013 to 2020, Cohen served as an independent director, chair of the compensation committee, and member of the audit and nominating committees of Spectrum Pharmaceuticals. Cohen also previously served on the boards of two companies that were successfully sold in 2017: Zurich-based LifeWatch, sold to Biotelemetry; and Colorado-based Syncroness, a privately held contract engineering firm, sold to ALTEN Group, a multibillion-dollar French engineering services company.

Cohen has earned accolades such as Cambridge Healthtech Institute’s 2024 MedTech MVP Award and the Orange County Business Journal’s Businessperson of the Year. In 2021, Cohen received a lifetime achievement award from SoCalBio for his four decades of work in medical technology. In 2020, Cohen was named Entrepreneur of the Year by Ernst & Young for the Pacific Southwest United States.

• Raise More Capital: Raise more money than you think you’ll need, given things always take longer and cost more than you think. Don’t fear dilution.

• Maintain Transparency: Keep communication open with your team and stakeholders to build trust and align goals.

Even after numerous successes, Cohen isn’t ready to slow down. He remains deeply committed to the medtech ecosystem, serving on multiple boards and actively mentoring emerging entrepreneurs. “I want to stay in the game, be relevant, and share my experiences,” he says.

His passion for improving patient’s lives continues to drive his endeavors. “It’s a privilege to be in an industry whereby we are helping people solve their medical problems,” Cohen affirmed, highlighting the profound impact medtech innovation can have on quality of life.

Cohen takes time to speak to MBA students at UCLA and UC Irvine, and his family has also launched a non-profit foundation focused on helping the less privileged in his local area of Orange County, CA.

“If you can do good for people and do well for your family, that’s what it’s all about. I sleep well at night knowing that hundreds of thousands of people live better lives because of the work done by myself and my colleagues.”

• Signature Series: Building and Exiting Companies in Medtech’s New Post-Covid Financial Era - featuring Ray Cohen and moderator Omar Khateeb of Khateeb & Co. Visit the LSI website (Resources > Video Library) to access the presentation from LSI USA ‘25, March 20, 2025.

• Omar Khateeb’s “The State of Medtech” Podcast Episode 279: Ray Cohen on Building & Selling Billion-Dollar MedTech Startups Without Bankers (khateebandco.com/state-of-medtech)

Driven by the rise of robotic surgery and increased application across high-volume procedures, the global electrosurgical devices market is set to expand from ~$10.2 billion in 2024 to ~$14.7 billion by 2029. This Market Dive examines the driving forces behind this growth, competitive dynamics, and recent innovations that are reshaping the future of surgical energy.

Electrosurgical devices have been an operating room mainstay for over a century. Today, they are at the forefront of a new wave of innovation, propelled by the growing use of surgical robotics. As robotic-assisted procedures expand in scope and frequency, electrosurgical technologies—especially robotic-compatible generators and instruments— are seeing accelerated demand.

Market growth is being fueled by higher device pricing and a shift in procedure mix. While conventional

electrosurgical forceps remain in wide use, robotic electrosurgical devices can cost up to 10 times more per unit. Moreover, even though many of these instruments are reusable, their lifespan is strictly limited by robotic system protocols, resulting in high cost per use and sustained demand for replacements.

Soft tissue robotic procedures are a major growth engine. According to LSI’s Global Surgical Procedure Volumes database, soft tissue surgeries are expected to grow from 151.7 million in 2024 to 174.9 million by 2029. Electrosurgery plays a crucial role in many of these procedures across general surgery, OB/ GYN, urology, and beyond.

While Ethicon, a subsidiary of Johnson & Johnson MedTech, maintained the largest market share in 2023, Intuitive Surgical is quickly closing the gap. In 2020, Intuitive held roughly 16% of the electrosurgical device market. By 2024, that figure rose to 25%. With the FDA clearance of its da Vinci 5 system in early 2024, Intuitive is poised to overtake legacy leaders.

Medtronic and J&J are responding with major investments. Medtronic

recently submitted its Hugo roboticassisted system for FDA clearance in the U.S. after successful IDE trials and continues to expand the platform’s indications. J&J's OTTAVA system also reached a clinical milestone in 2025, with initial surgeries completed under IDE.

These efforts represent more than a push for platform parity. Both companies are integrating energy tools with their robotic systems, aiming to control the full surgical workflow—from instrumentation to data.

• Medtronic submitted its Hugo system to the FDA in Q1 2025 after meeting safety and effectiveness endpoints in the Expand URO IDE study.

• Johnson & Johnson MedTech completed the first clinical trial cases using the OTTAVA system in Q2 2025.

• In April 2025, Erbe launched its next-generation VIO 3n and VIO seal generators, offering tailored energy modes and streamlined workflows across surgical specialties.

• In October 2024, Hologic announced its upcoming $350 million acquisition of Gynesonics, expanding its presence in women’s health and radiofrequency ablation technologies.

Notes: The “Other” category includes Boston Scientific, Cooper Surgical, Minerva, and Stryker, among others.

Source: Annual company reports, SEC filings, investor relations materials, and LSI Market Intelligence

Source: LSI Market Intelligence

Craig Gulliford, CEO of Creo Medical, is leading the charge in minimally invasive surgery with the company’s CROMA Advanced Energy Platform. Powered by proprietary Kamaptive technology, the platform combines adaptive bipolar radiofrequency and high-frequency microwave energy for precise dissection, ablation, and coagulation. Already FDA-cleared and CE-marked, Creo’s devices—including Speedboat and MicroBlate—are helping clinicians treat cancer and other conditions in hard-to-reach areas like the lung and pancreas with greater accuracy and fewer complications.

Led by Founder and CEO Dr. Stuart

Mitchell, Novuson Surgical is pioneering a new class of surgical instruments powered by direct therapeutic ultrasound (DTU). Unlike traditional electrosurgical tools, Novuson’s technology minimizes thermal damage and eliminates surgical smoke, enabling safer, cleaner procedures. With regulatory clearance on the horizon and commercialization plans underway, Novuson is poised to replace outdated energy modalities with a more precise, scalable solution.

Led by CEO and surgical oncologist Dr. Jerome Canady, US Medical Innovations is transforming surgical oncology with the Canady Helios Cold Plasma (CHCP) Ablation System. This non-thermal plasma technology targets residual cancer cells at the surgical margins without harming surrounding

tissue. Following its FDA 510(k) clearance in May 2024, the CHCP system offers a novel approach to cancer recurrence prevention and potential immunotherapeutic synergy.

The electrosurgical devices market is undergoing a fundamental transformation. As surgical robotics moves from cutting-edge to standard of care, companies that successfully integrate electrosurgical tools into robotic platforms will define the next decade of surgical innovation.

Surgeons and hospitals alike are gravitating toward comprehensive ecosystems where tools, platforms, and data operate in harmony. The companies that can deliver this seamless integration while also maintaining performance, safety, and cost-effectiveness will be best positioned to lead.

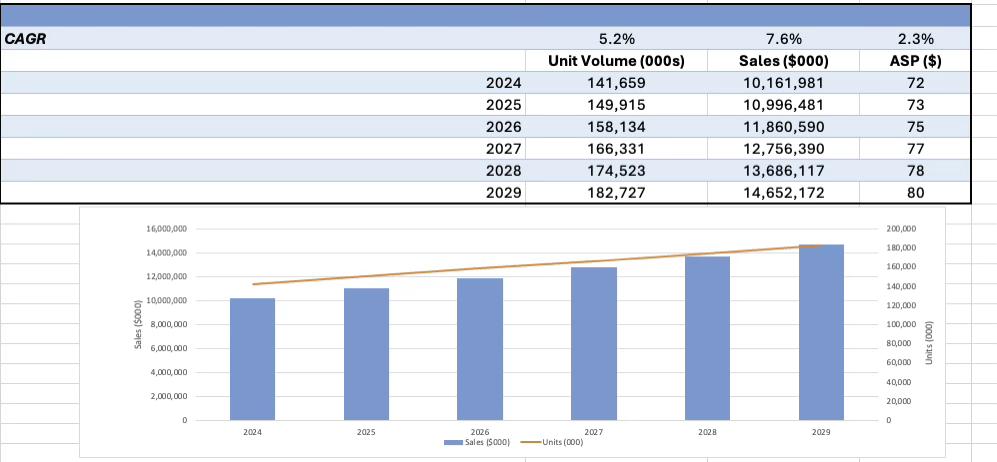

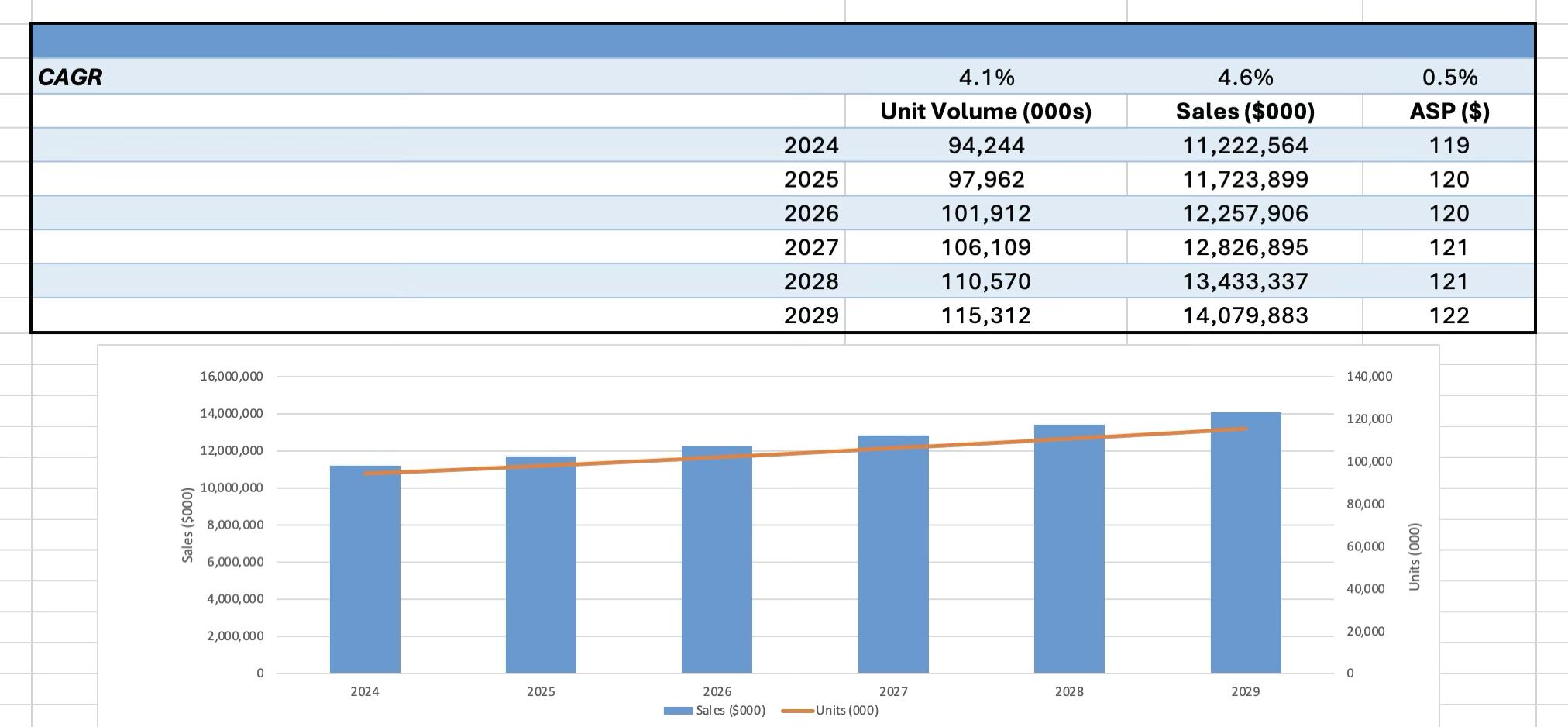

Fueled by rising procedure volumes, steady demand for minimally invasive cardiovascular treatments, and global access expansion, the global interventional cardiology device market is projected to grow from $11.2 billion in 2024 to $14.1 billion by 2029. Despite persistent pricing pressures, innovation and procedural growth continue to push the market forward.

Interventional cardiology devices— which include balloon catheters, stents, interventional guidewires, and intravascular guidance devices such as intravascular ultrasound (IVUS) catheters and flow wires—are used to diagnose and treat cardiovascular diseases through minimally invasive procedures. According to LSI’s Market Intelligence team, the global market for interventional cardiology devices is projected to grow at a compound annual growth rate (CAGR) of 4.6% from 2024 to 2029. This upward revision from last year’s 4.3% CAGR forecast reflects updated data on inflation and unit volume trends

despite continued pricing pressures for high-cost items.

Worldwide interventional cardiology procedure volumes are expected to grow at a healthy 3.9% CAGR during this period, driving a 4.1% increase in unit volumes according to LSI.. However, prices for many devices remain under pressure due to reimbursement dynamics and global cost containment initiatives. Drug-eluting stents (DES), for example, have seen dramatic pricing erosion, dropping from approximately $3,000 at launch to as low as $1,150 in the U.S. Similarly, in China, DES prices dropped from roughly $2,000 to $100. While current pricing has made DES cost-effective in mature markets like the U.S. and Europe, emerging markets

continue to face margin pressures amid accelerating procedure growth.

The price environment for interventional cardiology is unlikely to improve meaningfully in the near term. While inflation has led to slight price increases in some categories, global price growth is expected to lag overall medical device inflation. As a result, market expansion will remain volume-driven rather than price-driven.

Nevertheless, underlying demand remains strong. Heart disease is still the world’s leading cause of death, with

over 200 million people living with coronary artery disease. Minimally invasive coronary interventions are now the standard of care, and innovation in drug-coated balloons, bifurcation lesion treatment, and imaging guidance is expanding the market’s addressable scope.

Recent activity from major players and new entrants underscores the market’s dynamism. In early 2025, Teleflex announced a nearly €760 million acquisition of BIOTRONIK’s Vascular Intervention business, dramatically expanding its coronary and peripheral vascular portfolios. The deal adds a broad suite of devices, including drugcoated balloons, covered stents, balloon- and self-expanding bare metal stents, and balloon catheters.

Meanwhile, Medtronic received expanded CE Mark indications for its Prevail drug-coated balloon, including bifurcation lesions and multivessel disease— a signal that drug-coated balloons are gaining traction in complex percutaneous coronary intervention (PCI) settings.

On the early-stage front, Advanced Bifurcation Systems closed a $20.8 million SAFE financing round in January 2025. The company is developing a stent delivery system designed to treat all coronary bifurcation lesions in coronary angioplasties, a challenging subset of cases in interventional cardiology. With FDA Breakthrough Device designation and an expanded board, the company is ramping up for clinical and regulatory progress.

Boston Scientific, still the category leader, has continued advancing clinical evidence for its DES platforms. The company recently completed enrollment in the SYNTAX trial—a landmark study comparing DES to bypass surgery in complex, multivessel disease.

Tyler Melton, Co-Founder and CEO of Corveus Medical, is leading the development of a minimally invasive, catheter-based therapy designed to improve quality of life for patients with chronic heart failure. The company’s novel approach targets a sympathetic nerve branch in the thoracic cavity—an overactive driver of fluid retention and disease progression. By locating and ablating this nerve through a transvascular, extracardiac procedure, Corveus

Source: LSI Market Intelligence

offers the potential for outpatient treatment with immediate symptom relief. In 2024, Corveus joined Fogarty Innovation’s accelerator program, further advancing its mission to reduce the clinical burden of heart failure. With strong preclinical data, FDA engagement, and a first-in-human study on the horizon, Corveus is aiming to fill a critical gap for patients unresponsive to existing therapies.

Elixir Medical, led by CEO Motasim Sirhan, is redefining the treatment of coronary artery disease with a bold vision for long-term vessel restoration. The company’s flagship innovation, the DynamX Coronary Bioadaptor System, is engineered to support the vessel during healing and then unlock

over time—restoring natural motion, enhancing blood flow, and enabling plaque regression in synergy with statin therapy. This dynamic platform has shown superiority in clinical trials over traditional drug-eluting stents, delivering improved pulsatility and a 20% absolute difference in plaque volume change at one year. With a robust IP portfolio, expanded reimbursement

coverage, and multiple large-scale trials underway, Elixir is aiming to establish a new standard of care for millions of patients worldwide living with coronary artery disease.

The interventional cardiology market is both mature and in motion. As pricing pressures persist, success will hinge on differentiated technology, expanded indications, and strategic global growth. While established players consolidate and expand, emerging companies are pushing the field forward with precision tools, novel delivery systems, and data-driven platforms. With more than 200 million people worldwide affected by coronary heart disease, the need for effective, scalable interventions has never been greater.

Notes: The “Other” category includes B Braun, BD, Cook, Lemaitre Vascular, Merit Medical, Teleflex and Terumo, among others.

Source: Annual company reports, SEC filings, investor relations materials, and LSI Market Intelligence

Every week, LSI’s Market Intelligence team tracks the shifts, signals, and standout stories shaping the global medtech landscape. From financial performance and product divestitures to shifting patient behavior and overlooked clinical needs, The Numbers newsletter offers a data-driven lens on what matters most. Here’s what the LSI Market Intelligence team tracked this past month across public company earnings, kidney health, sleep therapy, and diabetes devices.

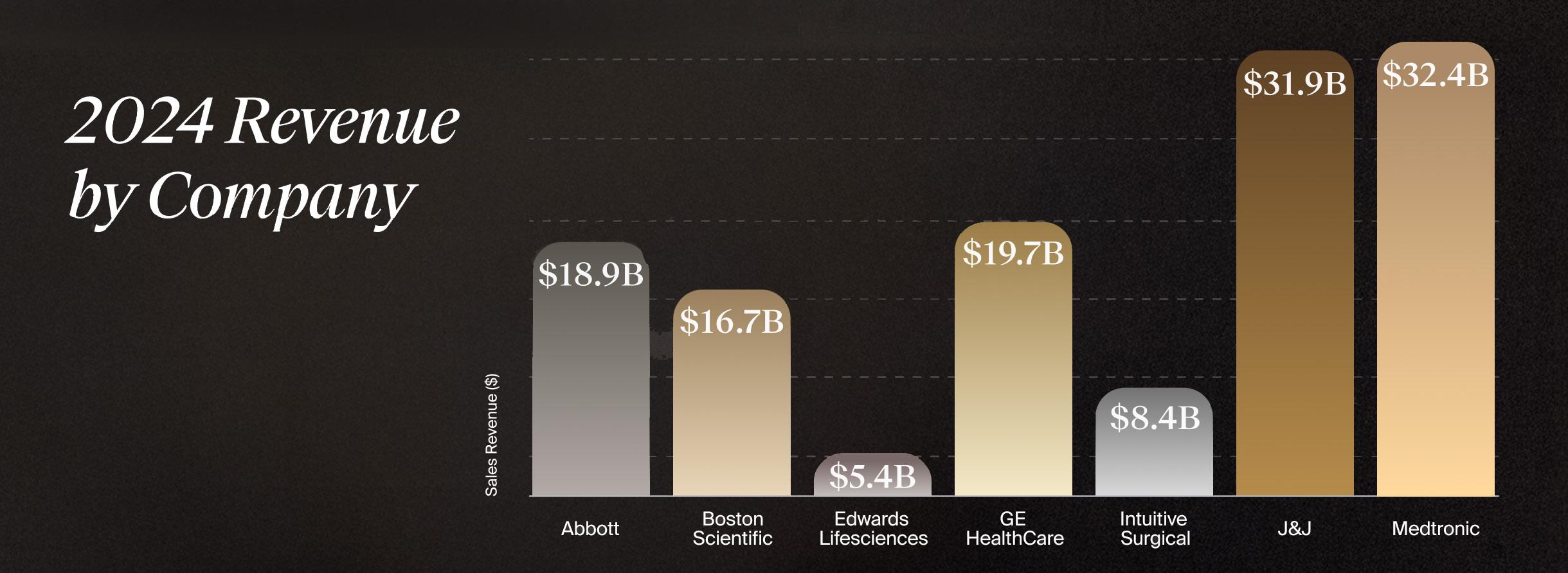

The first quarter of 2025 is in the books, and 2024 earnings reports from top medtech companies offer an early barometer of where the industry is heading. While macroeconomic pressures and regulatory headwinds persist, many strategics posted strong growth, particularly in cardiovascular, diabetes, and structural heart segments.

Abbott

• 2024 Medtech Revenue: $18.9B

• Q1 2025 growth: +12.5%

• Notable drivers: structural heart, diabetes care

• 2024 Revenue: $16.7B

• Q1 2025 growth: +22.0% (Cardiovascular up 26.2%)

• Momentum: Exceeded guidance; some deceleration expected for the rest of 2025

• 2024 Revenue: $5.4B

• Q1 growth: +8.0% to $1.4B

• Updated full-year revenue guidance: Raised from 8% to 10%

• Challenges: Slower-than-expected mitral system launch; competitive pressure

• 2024 Revenue: $19.7B

• Q1 growth: +4.0% to $4.8B

• Notes: U.S. strength offset by weaker performance in China

• 2024 Revenue: $8.4B

• Q1 2025 growth: +19% YoY to $2.3B

• Drivers: Procedure volume growth both domestically and internationally

• 2024 Medtech Revenue: $31.9B

• Q1 growth: +4.1%

• Positives: Cardiovascular, surgical vision, and wound closure acquisitions driving growth

• Headwinds: Competitive pressures in energy and endocutter segments; volume-based procurement (VBP) in China

• 2024 Revenue: $32.4B

• Q3 (Feb 2025) growth: +4.1% to $8.1B

• Strength: Pulsed-field ablation, valves, pacing, diabetes, neuromodulation

• Risks: Trade/tariff concerns, surgical stapling competition

Within the LSI ecosystem, alumni of our summits in the USA and Europe raised $1.37 billion in the first quarter alone. For context, total alumni fundraising in 2024 was $2.67 billion.

Emerging strategies include more silent strategic participation, contract development and manufacturing organizations (CDMOs), and hybrid deal structures that align risk across stakeholders. Startups are adapting to macro shifts while capital remains active—just quieter.

Dialysis remains the default treatment for end-stage kidney disease (ESKD), with over 500 million dialysis treatments

performed annually across the globe. Yet, despite its critical role, dialysis care is often outdated, expensive, and logistically burdensome—especially in lower-income countries.

• 2024 global market value: $14.0B

• 2029 projected value: $17.05B

• Projected CAGR (2024–2029): 4.0%

• U.S. treatments/year: ~85–90M

• Global patient population growth: 3%–5% annually

Today, hemodialysis dominates with 87% of product sales, largely due to reliance on consumables like cannulas, catheters, and dialyzers—which make up ~86% of product revenue. Meanwhile, peritoneal dialysis (PD) remain underutilized despite being more portable and home-friendly.

• Fresenius: ~35% global market share

• Other major players: Baxter, DaVita Kidney Care, NIPRO

• Barrier to entry: High due to infrastructure, networks, and regulatory complexity

But change is brewing—not by reinventing the machine, but by rethinking how and where dialysis is delivered. Key areas gaining traction include:

• Vascular access technologies

• Fluid sensors

• Remote monitoring platforms

• Devices supporting acute kidney injury and fluid overload management in cardiology and respiratory care

At the same time, companies like Quanta Dialysis Technologies, Diality, Roivios, CloudCath, Xeltis, and Relavo Medical are pushing new frontiers and formats toward the market.

The dialysis market is ripe for disruption—but real transformation will require updated reimbursement, new care models, and workforce support. Until then, it remains a high-need, under-innovated segment demanding attention.

Source: LSI Market Intelligence

Sleep health is no longer a niche category. With over 1 billion people affected by obstructive sleep apnea (OSA) and another 500–750 million suffering from chronic insomnia, the market is expanding—and diversifying fast.

• 2024 Market Value: $6.2B

• 2029 Projected Value: $8.9B

• CAGR (2024–2029): 7.4%

• Growth outpaces the broader medtech market CAGR of 6.6%

While continuous positive airway pressure (CPAP) remains the dominant therapy, home sleep diagnostics, wearables, and SaMD platforms are gaining ground.

Resmed’s acquisition of VirtuOx—an independent diagnostic testing facility that serves sleep, cardiac, and respiratory markets—strengthens its end-to-end sleep ecosystem. Though small financially, with an estimated value of $125 million, the acquisition reflects a clear strategic direction: become the operating system for sleep care.

Together, Resmed and Philips control over 80% of the global sleep therapy market, with Resmed estimated to hold a 50–60% share.

ACCELStars

• CEO: Yoshi Miyahara

• Total Amount Raised: ~$7.55M

• Solution: Advanced sleep measurement technology

• CEO: Hamed Hanafi

• Total Amount Raised: $5M

• Solution: Predictive AI tools for PAP therapy

• CEO: Ruben de Francisco

• Total Amount Raised: $60M

• Solution: At-home polysomnography systems for gold-standard diagnostics

• CEO: Rick O’Connor

• Total Amount Raised: $29.5M

• Solution: Injectable outpatient therapy for OSA

Sleep medicine is being reshaped by technology, patient preference, and payor incentives. Companies that can simplify diagnostics and drive long-term adherence will own the next chapter in this evolving market.

In one of the most talked-about moves of the quarter, Medtronic announced it will spin off its $2.5 billion diabetes business into a standalone public company. On 6/12 they announced it’s being called MiniMed. The move underscores the growing divergence between traditional B2B medtech and consumer-facing digital health.

• 2024 Value: $20.8B

• 2029 Projected Value: $30.0B+

• CAGR: 7.6%—a full percentage point above the broader medtech market

• Glucose Monitoring Devices: Majority of global sales (driven by consumables)

• Insulin Management Devices: ~23% of sales

So, why spin out? Medtronic’s diabetes segment:

• Operates in a consumer-centric model

• Requires direct patient engagement, unlike Medtronic’s core B2B units

• Competes with both device and pharma players (e.g., Insulet, Tandem Diabetes Care, Novo Nordisk, and Eli Lilly and Company)

Insulin Pumps and Sets

Source: LSI Market Intelligence

CEO Geoff Martha has emphasized that the spinout will allow each company to focus operationally, technologically, and commercially in their respective spaces.

• CEO: Sean Saint

• Total Amount Raised: $553M Technology: iLet Bionic Pancreas, an automated insulin delivery system

• CEO: Bradley Paddock

• Total Amount Raised: $391.6M

• Technology: Simplicity insulin patch for mealtime dosing

• CEO: Tim Goodnow

• Total Amount Raised: $226M

• Technology: Implantable CGM with external transmitter and mobile alerts

Meanwhile, partnerships like Dexcom + ŌURA are redefining the consumer-metabolic interface, integrating CGM with lifestyle data (sleep, stress, activity) to personalize care.

With diabetes prevalence rising (from 8.5% in 2014 to 11.1% in 2025), consumer-first approaches and real-time feedback loops are the future. Medtronic’s divestiture may position both

MiniMed and core Medtronic to focus—and win—within their respective lanes.

Across these different sectors, one theme is constant: medtech is in motion.

• Strategics are growing, but cautiously optimistic

• Kidney care is overdue for disruption

• Sleep is being re-platformed

• Diabetes is becoming deeply personalized

Behind each market trend is a deeper operational evolution—toward consumerization, platform integration, and value-based delivery.

The next few quarters will test the resilience of these shifts, especially as macroeconomic pressures and policy changes continue. But for now, the numbers speak volumes—and we’ll be here to track every signal.

Until next time, keep your eye on the pulse.

All data in this article is sourced from LSI’s Market Intelligence Platform, and recent additions of LSI’s The Numbers on LinkedIn and on the LSI website.

Access LSI’s continuously updated Market Intelligence Platform.

Scan QR code for details and to request a demo.

This month, to accompany our Innovator Spotlight on Fluid Biomed, we detail the latest LSI Market Intelligence data on the global, Asian, European, and U.S. forecast volume for select neurovascular stroke procedures.

Extracranial Procedures

Extracranial

by Type

LSI’s Global Surgical Procedure Volumes (SPV) Tracker provides trusted coverage of 300+ diagnostic and therapeutic procedures across 37 countries. Scan QR code to request a demo:

LSI’s SPV Tracker includes these geographies: Argentina, Australia, Belgium, Brazil, Canada, Caribbean, Chile, China, Colombia, Costa Rica, Denmark, Dominican Republic, Finland, France, Germany, Guatemala, India, Italy, Japan, Malaysia, Mexico, Netherlands, New Zealand, Norway, Panama, Poland, Russia, Singapore, South Africa, South Korea, Spain, Sweden, Switzerland, Thailand, Turkey, United Kingdom, and the United States.

This month, to accompany our Innovator Spotlight on Solenic Medical, we detail the latest LSI Market Intelligence data on the global, Asian, European, and U.S. forecast volume for knee replacement procedures.

LSI’s Global Surgical Procedure Volumes (SPV) Tracker provides trusted coverage of 300+ diagnostic and therapeutic procedures across 37 countries. Scan QR code to request a demo:

LSI’s SPV Tracker includes these geographies: Argentina, Australia, Belgium, Brazil, Canada, Caribbean, Chile, China, Colombia, Costa Rica, Denmark, Dominican Republic, Finland, France, Germany, Guatemala, India, Italy, Japan, Malaysia, Mexico, Netherlands, New Zealand, Norway, Panama, Poland, Russia, Singapore, South Africa, South Korea, Spain, Sweden, Switzerland, Thailand, Turkey, United Kingdom, and the United States.

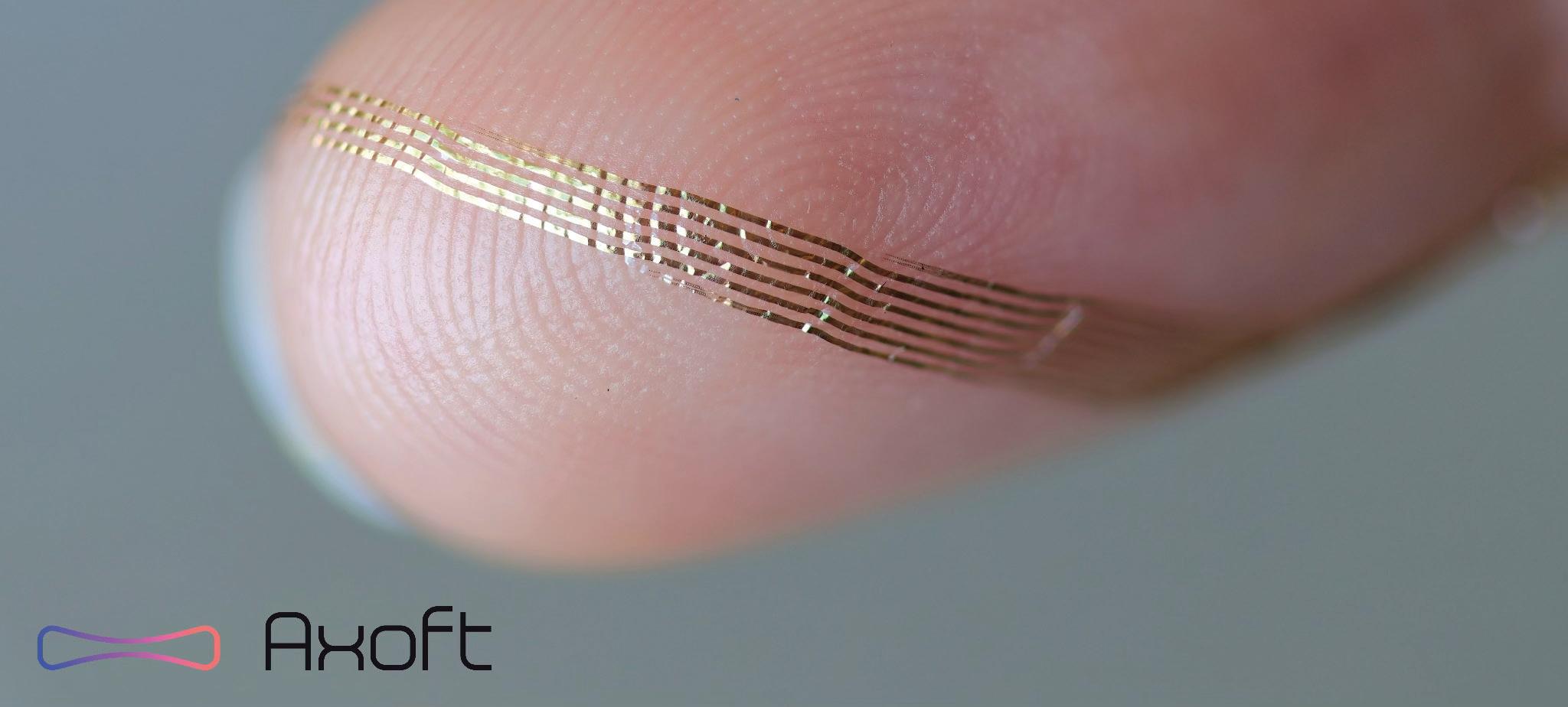

Armed with a brain-computer interface built from a novel ultra-soft material and bolstered by FDA Breakthrough Device Designation, Axoft is taking on neurological disorders, starting with disorders of consciousness as its first clinical indication. With first-in-human cases now complete, CEO and Co-Founder Paul Le Floch shares how Fleuron, their proprietary implant material, is unlocking clinical potential—and a new frontier in neurotechnology.

Neurological disorders affect nearly one in three people worldwide. Yet, for many, there is no drug, therapy, or even a reliable diagnosis. Enter Axoft, a neurotechnology company led by Paul Le Floch, who is on a mission to change that. The Harvard University-trained materials scientist and Forbes 30 Under 30 honoree is reengineering how the brain and technology communicate— starting with a radically soft implant and a bold plan to decode the natural language of the brain.

“Our goal is to unlock the natural language of the brain by capturing the activity of single neurons,” said Le

Floch. “To do that, we had to build a new class of brain-computer interface from the ground up.”

That innovation is Fleuron—Axoft’s proprietary implant material that mimics the mechanics of brain tissue. It’s up to 10,000 times softer than polyimide—which is used in state-of-the-art BCIs—and 1,000,000 times softer than silicon. “Rigid implants damage and move in the brain,” Le Floch explained. “That causes scarring and makes it impossible to get stable, high-density data long-term.”

Fleuron changes that. Designed for seamless integration with neural tissue, the material minimizes glial encapsulation around the implant and moves

with its natural pulsations—rather than resisting them. “They are so soft you can see how they bend around my fingerprints in this image,” said Le Floch. (See image on next page.)

“Rigid implants damage and move in the brain. That causes scarring and makes it impossible to get stable data long-term.”

By minimizing glial encapsulation and micromotion, Fleuron enables Axoft’s 1,024-sensor interface to maintain high-fidelity signal quality across

time and brain regions previously considered inaccessible.

This scalable access to brain activity is central to Axoft’s long-term goal: training foundation AI models on rich neural datasets. “The brain is a data organ,” Le Floch said. “And now, we finally have a way to capture the information needed to decode it.”

Earlier this year, Axoft completed its first-in-human clinical study at The Panama Clinic. The implants were tested during brain tumor surgeries, allowing researchers to evaluate the safety and neural recording in tissue already scheduled for removal.

“We planned for everything to go well—but it’s still a new technology,” said Le Floch. “What’s most exciting is that it all worked exactly as expected.”

The team demonstrated successful signal capture from patients under anesthesia and while awake, setting the stage for Axoft’s first indication: building a reliable prognostic for disorders of consciousness.

Disorders of consciousness, like vegetative or minimally conscious states, affect more than 500,000 patients each year in the U.S. and Europe. These patients are often caught in diagnostic limbo, with over 40% misdiagnosed due to reliance on behavioral exams that can miss signs of awareness. A recent study shows that more than 25% of patients may have cognitive-motor dissociation following a coma—conscious but unable to respond. “In these situations, the standard of care [to determine the condition of the patient and predict their recovery] is almost like flipping a coin to make life-altering decisions,” Le Floch said. “We want to bring more clarity and precision to that process.”

The need isn’t just clinical—it’s financial. Neuro-ICU stays cost $3,000 to $10,000 per day, and long-term care for patients in a vegetative state can exceed $100,000 per year. For those with severe traumatic brain injuries, lifetime care costs often surpass $2 million per patient.

“In these situations, the standard of care is almost like flipping a coin to make lifealtering decisions.”

Axoft’s BCI platform offers a fundamentally new approach: a continuous bedside monitoring system capable of identifying brain states in real time— opening the door for more accurate diagnosis, prognosis, and communication.

The company’s first indication represents a $15 billion market opportunity, with long-term plans to expand into therapeutic applications, first for disorders of consciousness, but also to broader neuropsychiatric indications like dementia and TBI/stroke rehabilitation, part of a broader $400 billion total addressable market.

Axoft has raised over $18 million, including a $10.1 million pre-Series A round and an undisclosed grant from the state of Massachusetts to build out its manufacturing line. The company also holds exclusive licenses from Harvard University and Stanford University, protecting the foundational IP behind Fleuron.

This spring, Axoft made Fleuron available to external partners, marking its commercial debut as a next-generation material platform for research and industrial use.

“Fleuron is not just for Axoft,” said Le Floch. “It’s already being used by

academic and industrial teams around the world.”

With its first clinical milestone achieved and regulatory pathways advancing, Axoft is preparing to raise a $40 million Series A to support its IDE application and premarket submission with the FDA.

“Our product roadmap starts with disorders of consciousness and scales toward treating complex neurological conditions,” Le Floch shared. This includes two FDA-classified devices: a Class II “read” system for disorders of consciousness, expected to enter the market in 2028, and a Class III “read and write” platform, projected for 2032, targeting broader indications such as dementia and TBI/stroke rehabilitation.

“We’ve moved out of the research phase,” Le Floch added. “Now it’s about bringing this into the clinic.”

Axoft made its debut at LSI USA ‘25, where Le Floch presented the company’s first human data just weeks after completing the study.

“It truly felt like the place to be for medical devices,” he said. “I met investors I’d been trying to reach for months— all in one place.”

The team also made valuable connections with other founders, advisors, and strategics. “Startups should try the hard things,” Le Floch reflected. “And when you meet others doing the same, it pushes you forward.”

Source: Axoft’s LSI USA ‘25

Presentation Slide Deck

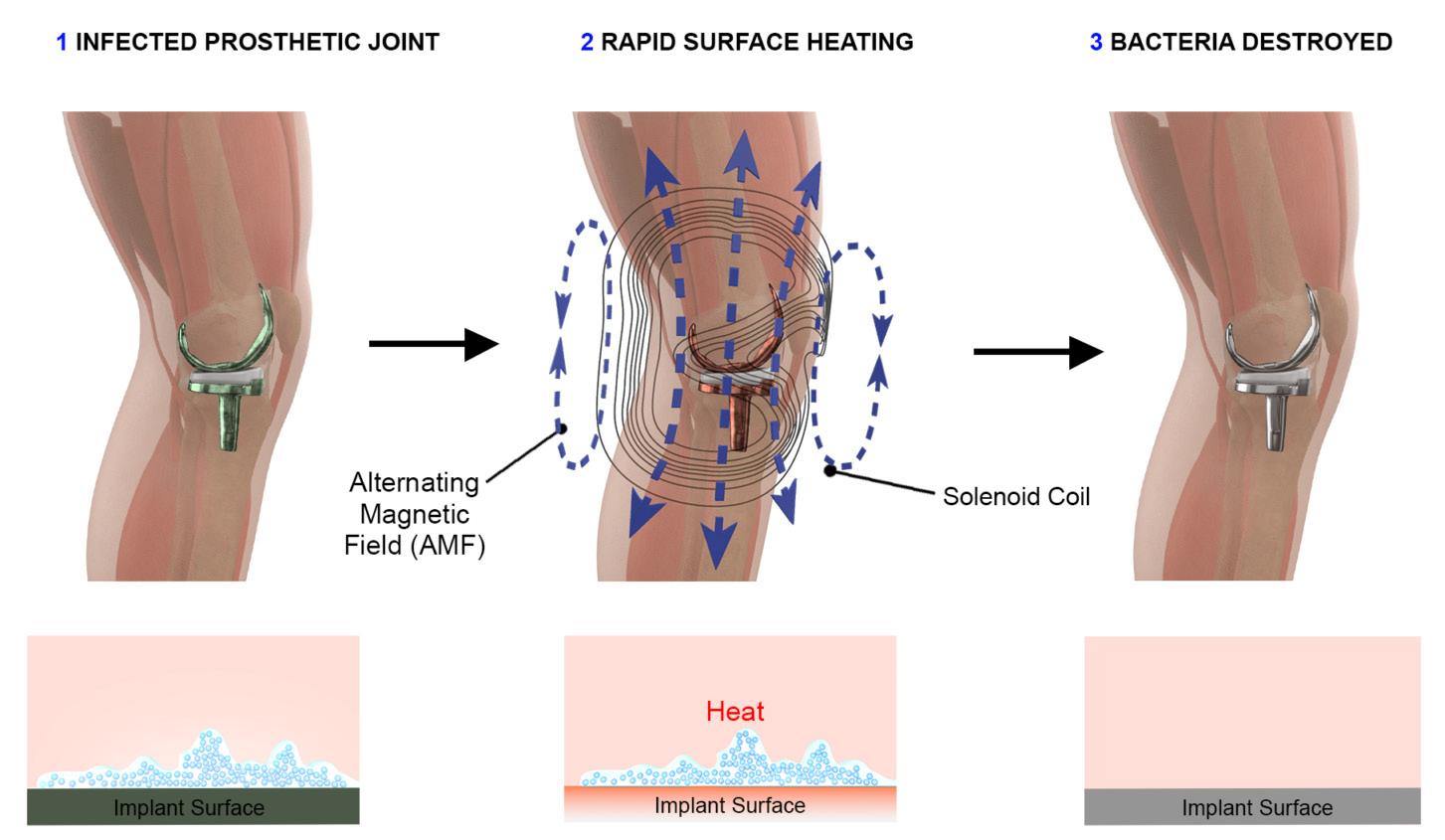

James Lancaster, COO of Solenic Medical, is leading the charge against one of the most devastating complications in orthopedic surgery: periprosthetic joint infections (PJIs). Backed by FDA Breakthrough Device Designation, recent firstin-human clinical milestones, and a growing network of strategic partners, Solenic’s non-invasive platform harnesses alternating magnetic fields (AMFs) to eradicate biofilms on infected implants—without surgery. With early feasibility trials underway and expansion into global markets in motion, Lancaster is shaping a new frontier in infection control.

The origin story of Solenic Medical began at UT Southwestern Medical Center, where infectious disease physician Dr. David Greenberg and physicist Dr. Rajiv Chopra envisioned a novel way to treat one of healthcare’s most challenging problems. They set out to solve the problem of biofilm—the sticky layer of bacteria that forms on implant surfaces and shields infections from antibiotics and the immune system. Their answer: AMFs to induce heat directly on the surface of metal implants and disrupt biofilms noninvasively.

“You can gargle with mouthwash all you want, but if you don’t brush and floss, [the biofilm] stays there. That’s exactly what happens on implants— it has to be physically disrupted.”

“Everyone’s familiar with biofilm,” James Lancaster said. “It’s the stuff you brush off your teeth every morning. You can gargle with mouthwash all you want, but if you don’t brush and floss, it stays there. That’s exactly what happens on implants—it has to be physically disrupted.”

Lancaster joined the founding team in 2018 to commercialize the concept, and Solenic Medical was officially incorporated in 2019.

With more than 1.3 million knee replacements performed each year in the U.S. alone, even conservative estimates of a 2% PJI rate suggest over 26,000 infections annually. Lancaster believes that real-world rates are closer to 4–5%, which would push that number above 60,000.

“Once you have a prosthetic joint infection, it’s a cascade of interventions.”

“Once you have a prosthetic joint infection, it’s a cascade of interventions,” he said. “Weeks of antibiotics, surgeries to open up the site, scraping infected tissue, removing and replacing implants. The failure rate is high, and the consequences are dire.”

According to data presented at LSI USA ’25, 26% of patients with an indicated infection will undergo aboveknee amputation within five years.

Mortality rates are comparable to those for breast and prostate cancer. (Also see Market Dive: Orthopedic Surgery, The Lens, December 2024.)

In March 2025, Solenic treated its first patient in an early feasibility clinical trial focused on knee PJIs. That milestone was followed by the treatment of a second patient in May 2025 and two more patients in June 2025, confirming early proof of concept and validating the team’s careful system development.

“It was a major step for our entire team,” Lancaster said in a recent chat with The Lens. “Seeing our technology used in the clinical setting—and seeing patients benefit from it—was powerful.”

In July 2020, Solenic earned FDA Breakthrough Device Designation, and in June 2023, it raised $5.1 million Series A led by Johnson & Johnson Innovation and joined by other major medical device investors such as ShangBay Capital. The company is now raising a Series B to support pivotal trials and additional indications.

“This is a global problem, and the demand we’re seeing reflects how badly a non-surgical option is needed.”

Interest in Solenic’s technology has come from around the world. Patients from Africa, Israel, and Australia have reached out asking to participate in trials.

“This is a global problem,” Lancaster said. “And the demand we’re seeing reflects how badly a non-surgical option is needed.”

The company is already building clinical and manufacturing infrastructure in Asia and is seeing strong investor and clinical interest in Singapore, Japan, and South Korea. In the U.S., Solenic is targeting 300 hospitals where the majority of revision procedures are

Source: Solenic Medical’s website

performed by fellowship-trained revision specialists.

According to LSI’s Global Surgical Procedure Volumes Database, global knee replacement volumes are projected to grow from 4.3 million in 2024 to 6.4 million in 2029, with a CAGR of 7.9% (see table below).

Even assuming a conservative 2% infection rate, over 86,000 PJIs are expected in 2024 globally. The economic burden is significant: a two-stage revision procedure for a knee implant can cost ~$38,000. That places the annual direct cost of PJIs at over $3.3 billion. And that’s without accounting for lost productivity, rehospitalizations, or long-term disability.

In the U.S., Solenic estimates that 130,000 annual procedures could be addressable with its AMF technology across knees, hips, shoulders, tibial nails, and other metallic implants. At a projected cost of $7,500 per treatment, the total addressable market is substantial.

Solenic is now preparing for its pivotal trial in knees, aiming to begin en-

rollment before the end of 2025. The team is also developing new transducers for hips, tibial nails, and other indications.

The company recently expanded its medical and business advisory boards with orthopedic thought leaders like Dr. Michael Mont and Dr. Antonia Chen, along with James Mapes and commercialization expert Tamara Rook These additions reflect Solenic’s commitment to both clinical rigor and market readiness.

“What we’re doing is delivering a therapeutic dose—measured by time and temperature—without cutting the patient open,” Lancaster said. “It’s thermal medicine, and it works in harmony

with antibiotics to disrupt the infection at its source.”

In a follow-up interview with The Lens, Lancaster shared, “Solenic Medical is pleased to announce the appointment of Bart Bandy as its new Chief Executive Officer. With a distinguished track record of leadership across both private and public healthcare companies, he brings decades of experience in launching groundbreaking technologies, scaling high-performance teams, and creating new markets. This strategic hire marks a bold step forward in Solenic’s mission of delivering transformative and safer healthcare solutions worldwide.”

The industry’s most comprehensive and trusted global procedure database, with coverage of 300+ diagnostic and therapeutic procedures across 37 countries.

Celebrating the accomplishments of a few of the many bright stars in our LSI presenting company and speaker alumni community.

Be sure to check out presentations from these and many other innovative companies from recent LSI events on our website at Resources > Video Library.

UK-based Adtec Healthcare has received MDR certification for its SteriPlas cold plasma device, paving the way for expanded clinical use in Europe. The certification under the EU Medical Device Regulation recognizes Adtec’s years-long investment in safety testing, post-market surveillance, and quality system enhancements.

SteriPlas is a noninvasive treatment platform that delivers cold atmospheric plasma to accelerate healing in complex wounds—such as diabetic foot ulcers—by reducing bacterial load and

disrupting biofilms. The therapy has also shown promise in dermatological applications like actinic keratoses without side effects.

This milestone supports Adtec’s continued international expansion and opens the door to new indications, distribution partnerships, and clinical collaborations in chronic wound care and beyond.

Singapore-based Aevice Health has received FDA 510(k) clearance for pediatric use of its AeviceMD device, a

smart wearable stethoscope designed to remotely monitor lung sounds in children aged three and above. The clearance marks a major milestone in the company’s efforts to support early intervention and home-based care for chronic respiratory conditions like asthma and COPD.

AeviceMD combines continuous auscultation with AI-powered analytics to detect abnormal respiratory sounds and track disease progression from home. The device aims to help clinicians reduce readmissions and manage care more effectively in pediatric populations.

The regulatory milestone follows Aevice Health’s Seed Plus funding round led by Coronet Ventures, with participation from SEEDS Capital, East Ventures, Denka, A&D, and Elev8 VC With FDA clearance in hand, the company is ramping up commercialization and expanding deployment across hospitals and home care programs in the U.S. and Singapore.

Mountain View, CA-based AliveCor has launched KardiaMobile 6L Max, its most advanced AI-powered personal ECG device, alongside KardiaAlert, a first-of-its-kind ECG monitoring feature for KardiaCare subscribers. KardiaMobile 6L Max identifies up to 20 arrhythmias with remote review by board-certified cardiologists, offering users clinically validated, real-time insights without requiring in-person appointments.

KardiaAlert expands this offering by analyzing changes over time across a user’s ECG history, flagging patterns that could signal more serious conditions. This dual release positions AliveCor’s new platform as one of the most comprehensive over-the-counter cardiac monitoring systems available today, supporting proactive care for an aging population at increasing risk of heart disease.

Campbell, CA-based Atia Vision has received FDA Investigational Device Exemption (IDE) approval to begin a U.S. clinical trial of its OmniVu Lens System, a novel dual-optic intraocular lens developed to restore dynamic, natural vision after cataract surgery. The lens features a shape-changing, fluid-filled base and a front optic component that work together to mimic the eye’s native

focusing ability while preserving anatomical integrity.

International trials across 75+ eyes show promising results, with 100% of patients achieving 20/20 or better uncorrected distance vision and sustained performance up to three years post-implantation. With only 6.2% global adoption of presbyopia-correcting lenses, OmniVu aims to reshape the standard of care for the 94 million people affected by visual impairment due to cataracts worldwide.

Cambridge, MA-based Axoft has announced the commercial launch of Fleuron, a next-generation material designed to improve the long-term performance of implantable brain-computer interfaces (iBCIs) and other bioelectronic devices. Up to 10,000 times softer than conventional polyimide and optimized for tissue compatibility, Fleuron was recently used in Axoft’s first-in-human study at The Panama Clinic and is now available to research and industrial partners for R&D applications.

Developed through a collaboration between Stanford University and Harvard University researchers, Fleuron minimizes tissue scarring and implant migration while maintaining high signal fidelity over time. Axoft has secured exclusive licenses from Stanford and Harvard for the core technology and plans to expand its material offerings by the end of 2025, supporting broader applications in neural interfaces, bioMEMS, and organ-on-a-chip systems. (Also see LSI Alumni Innovator Spotlight: Axoft’s Paul Le Floch, this edition.)

Huntington Beach, CA-based BiVACOR has received FDA Breakthrough

Device Designation for its BiVACOR Total Artificial Heart (TAH), a fully implantable system designed as a bridge to transplant for patients with severe biventricular or univentricular heart failure. The designation accelerates the path to market for a technology aiming to fill a critical gap left by existing options like left ventricular assist devices (LVADs).

Compact and magnetically levitated, BiVACOR’s TAH is engineered to deliver pulsatile outflow without valves or flexing ventricular chambers. Following five successful first-in-human implants, the company secured FDA approval to expand its clinical study. The device is currently under evaluation as a next-generation alternative for patients with limited options, offering a smaller, more durable solution that mimics native heart performance with reduced risk of complications.

Paris, France-based BrightHeart has secured a third 510(k) clearance from the FDA—this time for its new B-Right Views software—becoming the first company to offer an integrated AI solution for both real-time fetal heart documentation and detection of structural markers suggestive of severe congenital heart defects (CHDs). B-Right Views automatically confirms whether all required views have been captured

during anatomy scans, helping sonographers improve exam completeness and reduce repeat imaging.

The clearance builds on BrightHeart’s momentum, including prior FDA nods for its B-Right Screen software and cart-side tablet. With Predetermined Change Control Plan (PCCP) approval now in place, BrightHeart is positioned to rapidly iterate its AI platform and expand clinical value across care settings. A limited market release is planned following early pilot success.

Lausanne, Switzerland-based Distalmotion has received FDA 510(k) clearance for its DEXTER Robotic Surgery System in adult cholecystectomy, expanding its U.S. indications beyond inguinal hernia repair. Cholecystectomy is one of the most common general surgeries in the U.S., with 60% performed in outpatient settings. With a compact footprint, sterile console, and compatibility with standard OR infrastructure, DEXTER is purpose-built for hospital outpatient departments and ambulatory surgery centers.

This clearance supports Distalmotion’s mission to broaden access to robotic surgery through streamlined technology designed for high-volume soft tissue procedures. DEXTER has now been used in 2,000+ procedures across 30+ procedure types in general, gynecological, colorectal, and urological surgery.

Eden Prairie, MN-based Elucent Medical has received FDA Breakthrough Device Designation for its EnVisio X1 In-Body Spatial Intelligence System, a next-generation surgical guidance platform. Building on the company’s existing EnVisio platform, EnVisio

X1 enables real-time 3D localization of SmartClip markers and tracked surgical instruments during soft-tissue resections—supporting enhanced precision, margin control, and integration into robotic or video-assisted workflows.

The designation marks a major milestone in Elucent’s mission to redefine the standard of care in minimally invasive oncology. By combining implantable fiducials with wireless surgical navigation, the system aims to reduce positive margins and the need for re-excisions in complex procedures involving thoracic and abdominal soft tissues. EnVisio X1 remains under development, with the FDA Breakthrough pathway expected to accelerate its clinical and regulatory trajectory.

Brisbane, Australia-based Field Orthopaedics has received Therapeutic Goods Administration (TGA) authorization for its Extremity All Suture System (EASS) Griplasty systems, securing Australian Register of Therapeutic Goods (ARTG) inclusion. The Griplasty Base of Thumb System is a single-incision, all-suture implant designed to treat advanced-stage thumb carpometacarpal osteoarthritis (CMC OA)—a condition affecting an estimated 33% of postmenopausal women.

The system features a ‘V-Sling’ implant that stabilizes the thumb by

providing broad, multi-axis suspension and can be deployed dorsally or volarly. With more than 250 patients treated in the U.S. during limited release, the Griplasty platform is gaining recognition as a versatile option compatible with trapeziectomy and tendon transfer procedures. The ARTG listing supports expanded clinical adoption across Australia.

Kirkland, WA-based Freespira has received FDA 510(k) clearance to treat adolescents aged 13-17 with its athome treatment for panic disorder and PTSD, expanding access to a population facing rising anxiety rates and limited provider availability. Freespira’s 28-day, medication-free protocol uses capnometry-guided respiratory intervention (CGRI) combined with real-time software feedback and one-on-one video coaching to correct dysfunctional breathing patterns underlying panic and PTSD symptoms.

Clinical data from adolescent studies showed a 54% reduction in panic disorder symptom severity, with nearly half of the patients reaching remission, and a 44% reduction in PTSD symptoms, with 75% no longer meeting the diagnostic threshold after treatment. With CMS reimbursement codes for digital mental health treatments now in effect, the expanded indication strengthens Freespira’s position as a scalable, cost-effective solution for payors and families alike.

Paris, France-based GLEAMER has received CE Mark approval for BoneCT, the company’s first CT-based AI application and the debut product in its OncoView suite. BoneCT delivers sliceby-slice AI detection of small secondary

bone lesions with instant Picture Archiving and Communication System (PACS) overlays, enabling radiologists to detect metastases earlier and with greater confidence—an area where up to 26% of small lesions are typically missed during manual reads.

This milestone adds to the company’s CE-cleared solutions across X-ray, MRI, and mammography and its FDAcleared X-ray solutions. With BoneCT now CE-cleared, the company is poised to accelerate its rollout of additional oncology-focused tools within OncoView, driving earlier interventions and improving cancer care outcomes.

Paris, France-based Gradient Denervation Technologies has received FDA Breakthrough Device Designation for its catheter-based system targeting pulmonary hypertension due to leftsided heart disease. The company’s platform uses therapeutic ultrasound to ablate nerves around the pulmonary artery in a percutaneous procedure designed to reduce pulmonary vascular resistance by modulating sympathetic activity. Gradient is currently enrolling patients in its PreVail-PH2 early feasibility study, which received FDA approval to proceed in March 2024.

The designation demonstrates growing interest in nerve-targeting therapies

beyond renal denervation, an area that’s seen multiple recent approvals. Gradient’s focused approach to pulmonary artery anatomy builds on familiar interventional techniques and offers a novel path forward for underserved heart failure populations. The company previously raised $15M in Series A funding to support its clinical and regulatory programs.

Lexington, MA-based Hyalex Orthopaedics has received FDA approval for a supplemental IDE, allowing its early feasibility study of the Freestyle Knee Implant to advance into a pivotal clinical trial. The company is developing joint preservation solutions based on its HYALEX HYDROSURF materials platform, designed to replicate natural joint mechanics. The Freestyle Knee Implant specifically targets patients with cartilage damage and early osteoarthritis of the femoral condyle(s)—an underserved population estimated to represent a $2 billion U.S. market.

The upcoming pivotal trial will be conducted across leading orthopedic centers in the U.S. and Europe, enrolling a diverse group of patients with limited current treatment options. The decision follows promising early feasibility results and underscores the implant’s potential to restore mobility and improve longterm outcomes. According to Hyalex, the Freestyle Knee Implant could redefine treatment strategies for focal chondral and osteochondral defects by enabling patients to maintain active lifestyles without requiring total knee replacement.

Caesarea, Israel-based Nitinotes has announced promising interim clinical results for its fully automated endoscopic suturing system, EndoZip,

presented at the IFSO-EC 2025 Congress in Venice. The data—drawn from one site in a larger multicenter trial— demonstrated an average total body weight loss of 11.4% at 12 months in patients with class I and II obesity (BMI 30–42 kg/m²), all of whom also had hypertension and/or type 2 diabetes. Over half of hypertensive participants showed improved blood pressure, and 62.5% of patients with type 2 diabetes saw improvements in their diabetes health condition.

EndoZip is designed to reduce operator dependency and procedural complexity in endoscopic gastroplasty procedures, offering a minimally invasive and potentially scalable solution for patients who have been unsuccessful with noninvasive weight loss therapies. While the device is still investigational and not yet approved for commercial use, the company anticipates CE mark approval soon and is in active discussions with the FDA.

Eindhoven, Netherlands-based Onera Health has been named the winner of the 2025 MedTech Breakthrough Award for ‘Medical Device – Best New Technology Solution – Diagnostic,’ a recognition that underscores the company’s leadership in sleep diagnostics innovation. The award celebrates Onera’s commitment to transforming the sleep testing landscape with its patient-centric, clinically robust technologies.

At the heart of this transformation is the Onera Polysomnography-as-aService platform, which enables hospitals and clinics to offer full-scale sleep diagnostics in the comfort of a patient’s home. Powered by the Onera Sleep Test Study (STS), a patch-based sensor system that collects all signals required for a traditional PSG, the solution eliminates the need for in-lab studies, minimizes setup time, and expands access for underserved populations. With no wires, no upfront investment, and minimal clinical workload, Onera is reshaping how sleep disorders are diagnosed.

Kirkland, WA-based Prevencio has received Breakthrough Device Designation from the FDA for HART CADhs, its artificial intelligence-powered blood test for the detection of obstructive coronary artery disease (CAD). As the only multi-protein, AI-based blood test of its kind, HART CADhs uses machine learning to combine biomarkers into a single diagnostic tool capable of identifying arterial blockages with high accuracy from a simple blood draw.

Currently available as a Lab-Developed Test with results in two to 10 days, the company is now working toward a rapid FDA-cleared version for emergency room use. In studies conducted in partnership with Massachusetts General Hospital, HART CADhs

significantly outperformed standard-ofcare tests like stress echo and nuclear imaging. The designation supports Prevencio’s mission to deliver faster, more accessible diagnostics in both outpatient and acute care settings—an important step toward improving outcomes for patients in underserved communities and reducing overall cardiovascular care costs.

Baltimore, MD-based ReGelTec has received CE Mark under EU MDR for its HYDRAFIL system, a percutaneous hydrogel implant designed to relieve chronic low back pain caused by degenerative disc disease (DDD). In a study of 75 patients, the outpatient disc augmentation procedure demonstrated over 80% improvement in Oswestry Disability Index scores and a 70%+ reduction in pain scores—benefits sustained at the two-year mark for patients completing follow-up. The system offers a minimally invasive alternative for patients who fall between conservative therapies and spinal surgery.

The CE Mark supports commercial expansion in Europe and follows FDA approval of an IDE for the U.S. pivotal trial, HYDRAFIL-D, now enrolling across eight U.S. sites. With over 10 million Americans affected by DDD, HYDRAFIL addresses a critical treatment gap by restoring disc biomechanics and redistributing spinal load via hydrogel

injection, potentially transforming care for millions seeking relief from chronic back pain without invasive intervention.

Massy, Ile-de-France-based Sensome has completed enrollment in the INSPECT study, a first-in-human clinical trial evaluating its novel tumor detection technology for real-time tissue characterization during transbronchial lung biopsies. The investigational device uses miniaturized impedance-based microsensors to differentiate cancerous from healthy tissue in situ—without relying on additional imaging modalities. By confirming whether a biopsy needle is accurately positioned within a lesion, the technology aims to streamline procedures and reduce delays in diagnosing lung cancer, the world’s leading cause of cancer-related death.

The study enrolled 27 patients across two leading centers: Hôpitaux SaintJoseph & Marie-Lannelongue in France and Royal Brisbane and Women’s Hospital in Australia. Early feedback from investigators emphasizes the tool’s ease of integration into standard bronchoscopy workflows and its potential to improve diagnostic precision. This lung cancer study is part of Sensome’s broader strategy to bring its proprietary microsensor platform to clinical practice across lung cancer, stroke care, and peripheral vascular disease.

March 16th - 20th, 2026

Waldorf Astoria, Monarch Beach, Dana Point, CA