The Lens is published monthly and available in print and electronic formats. Copyright by Life Science Intelligence, Inc. All rights reserved. Editor takes care to report information from reliable sources and does not assume liability for information published.

Scott Pantel Chief Executive Officer, LSI Lead Author

Henry Peck Chief Business Officer, LSI Lead Author

Tracy Schaff Sr. Writer and Editor, LSI Contributing Author

Letter from the editors

In an era dominated by the endless scroll of social media and the rapid evolution of artificial intelligence, we know what you are thinking: Why print a magazine? Why invest in a medium that, to some, might seem outdated?

The answer is simple: We believe in the power of the tangible. There is something profoundly gratifying about holding a magazine in your hands, feeling the weight of the pages, and turning them one by one. It's an experience that is both tactile and immersive — a deliberate choice to slow down in a fast-paced world.

In today's digital landscape, information is more accessible than ever. Yet, finding the trusted insights you need often feels like searching for a needle in a haystack. Digital platforms, while undeniably important, are constantly bombarded with ads and attention-grabbing headlines. Content changes rapidly, and what is true one minute may be buried under layers of new information the next. In contrast, print is static and immortalized. It doesn't get lost in the noise. Editions of well-curated print media become a library of knowledge — a reference you can return to time and time again. It is a repository of carefully chosen words and thoughtfully selected graphics, free from the distractions of pop-ups and clickbait.

Trust has never been more critical, and that's where our magazine comes in. In this first edition, we were fortunate to collaborate with some of the most intelligent and boundary-pushing analysts and industry insiders. These are individuals who not only understand the complexities of medtech, but also have a knack for distilling “the intricate” into “the actionable.” Their contributions ensure that every written column is a treasure trove of valuable information, a reflection of their deep expertise and forward-thinking perspectives. And, of course, we included some columns for entertainment and levity —

a well-earned respite from the pressures of innovating in healthcare.

We are incredibly proud of this first issue, and it is indicative of issues to come. Inside, you will find original commentary on the financing and M&A activity from the first half of 2024 — a crucial period that sets the tone for the rest of the year and beyond. We also dive deep into some of medtech’s hottest market segments, including neuromodulation, mitral and tricuspid valve repair, and urology and renal devices, to give you a comprehensive understanding of where the industry is heading and the forces driving it forward.

We also have exclusive reflections from industry titans like Alex Gorsky and Thomas Oxley, who share their insights on the current state of medtech and AI. Their perspectives are not just opinions, but are grounded in years of experience and leadership. This edition also highlights relevant LSI alumni milestones, calling attention to innovators making waves in the industry. Taken together, these stories capture the spirit of innovation and the relentless pursuit of excellence that defines medtech in 2024.

As you read through, we hope you find the content both informative and entertaining. Whether you’re making major strategic decisions for your company or simply enjoying a moment of quiet reflection, this magazine is designed to be a valuable executive resource and a conversation starter. Keep it on your desk, and let it be a bridge to new ideas and discussions with fellow medtech leaders.

In a world where everything seems to be moving at breakneck speed, we invite you to pause, reflect, and enjoy the timeless pleasure of reading in print. Here’s to thoughtful analysis, trusted insights, and the joy of discovery on every page.

We welcome your feedback and suggestions for future coverage; email us at hpeck@ls-intel.com and spantel@ls-intel.com.

Warm regards,

Scott Pantel and Henry Peck

Scott Pantel Chief Executive Officer, LSI Lead Author

Henry Peck Chief Business Officer, LSI Lead Author

Financing Outlook 1H 2024: Show Me the Money

After a difficult couple of years, healthcare venture funding appears to be on the mend, with positive signs in the first half of 2024 quelling fears of a more extended downturn and fostering an environment of cautious optimism.

There was “increased investment across every sector” in 1H 2024, including Healthtech, Med Device, Biopharma, and Diagnostics, and “numerous” new investor-led

rounds, according to Jonathan Norris, managing director of HSBC Innovation Banking, writing in the latest HSBC US and Europe Venture Healthcare Report, released in July.

That optimism was echoed by Silicon Valley Bank (SVB) in its Mid-Year 2024 Report on Healthcare Investments and Exits, released in August, which also found “signs of recovery” across all sectors. Median Series A valuations in the device sector were

at an “all time high” in 1H 2024, the report noted, and VC fundraising was “impressive” despite the highest federal funds rate in decades. Although fundraising cycles have lengthened since 2021, healthcare VCs in the US and Europe closed on more than $9 billion in capital in the first half of 2024, with $6 billion more in process, according to SVB.

Cautious Optimism

Despite the good news, there are some lingering challenges that could weigh on performance going forward, including a weak exit environment, the continuing impact of insider rounds (a common tool used to bridge the funding gap in 2023), and overaggressive valuations leftover from 2021’s frothy, pandemic-driven investment frenzy.

Although the industry appears to have “largely shaken off 2023’s malaise,” writes Norris, those companies still relying on “dwindling” insider cash “will need to find a new lead investor or else face consolidation or shutdown.” Moreover, since only about half of the unicorns formed during the pandemic investment bubble in 2020 and 2021 have come back to raise another round, valuations are still in the crosshairs and “the markdown hammer has yet to fully drop,” cautions SVB.

Although funding was up, investments in the first half split the start-up field clearly into two baskets: “the haves and the have nots,” according to SVB, with VCs “increasingly focused on quality over quantity.” Moreover, deals may take longer to put together, with

many investors waiting to form solid syndicates before pulling the trigger, and checks may be smaller than anticipated. Although down rounds are not as common as in 2023, down or flat rounds are still sitting at “the highest level in recent decades,” the SVB report states.

Turning the Corner?

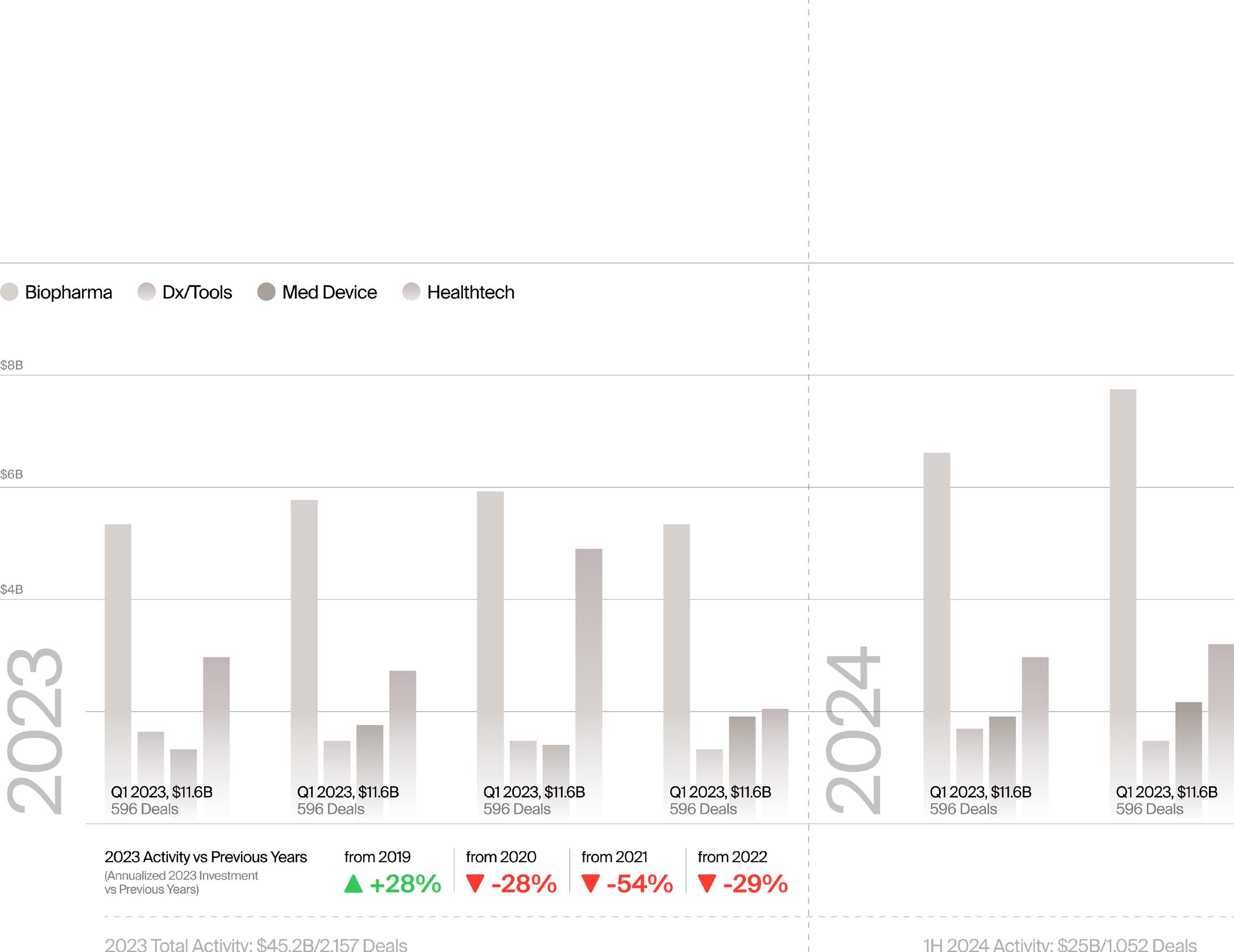

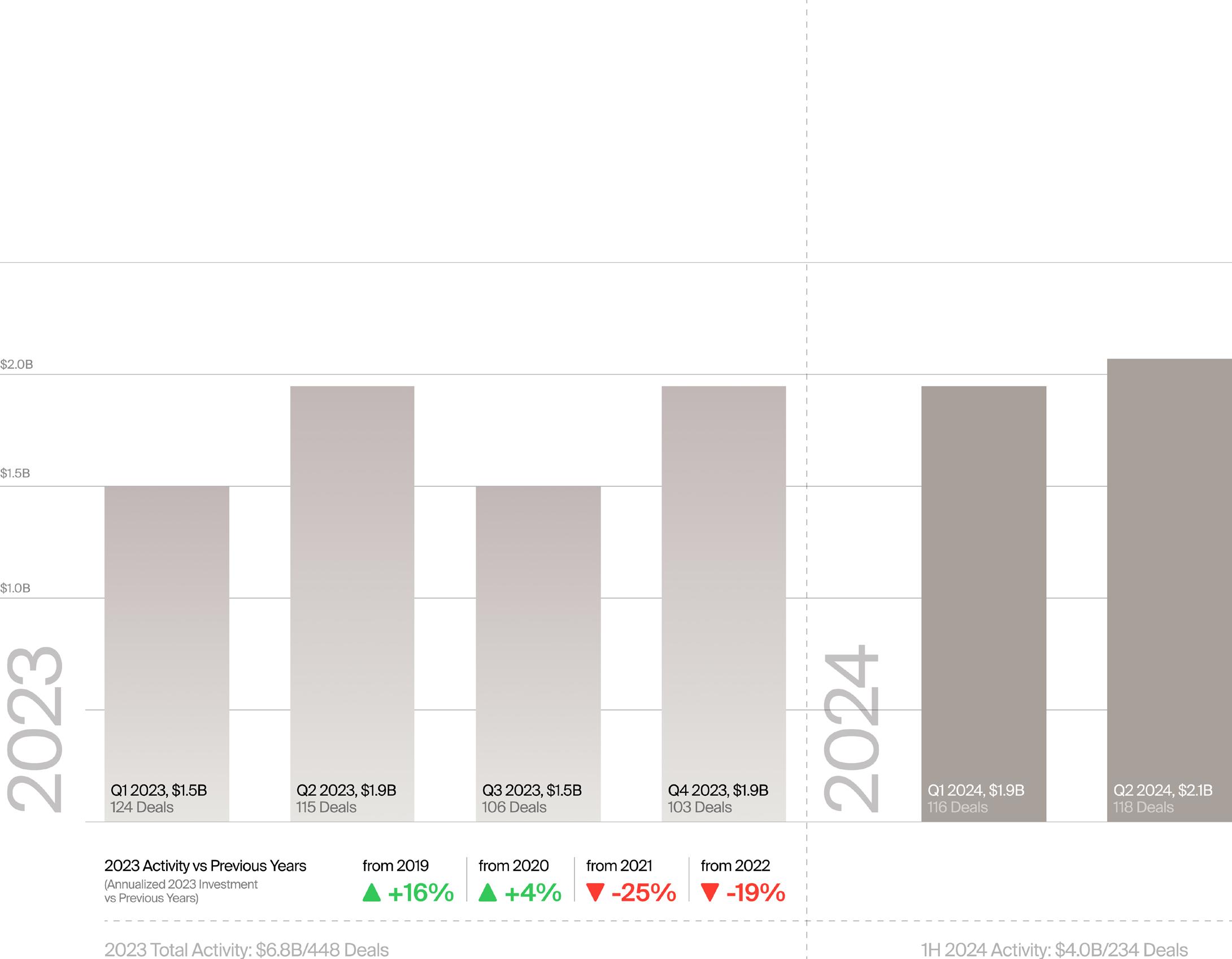

Still, the data thus far are encouraging. Healthcare investment in the first half totaled $25 billion, $4 billion of which went to the medical device sector, according to Norris. That puts Med Device on track to surpass 2023 investment levels and come close to 2022’s funding total. And that is very welcome news for an industry that has endured two years of tumult and uncertainty. Ironically, the difficulties began in 2021, at the height of the pandemic, when an unprecedented amount of investor money flowed into healthcare. Much of that money was aimed at technologies that could enable remote care, and a good deal came from investors who were new to medtech and unfamiliar with its typical valuations and returns. The influx drove up company valua-

Venture Capital Investment in Healthcare

tions to unrealistic levels, particularly in the digital health sector, and in the second half of 2022, when pandemic concerns waned and economic conditions worsened, the industry faced a reckoning.

Early-stage medtech financing was hit particularly hard as investors stepped back and focused on supporting their existing portfolios. In 2023, first-financing investment in medical devices (defined as initial seed or Series A funding of $2M+) declined by 18% compared with the previous year, according to Norris, driving down the number of overall deals in the medical device sector by 20%. Total dollars invested remained steady due to the strength of later-stage deals, but many companies relied on insider rounds and nearly one in three Series B and later deals led by a new investor were down rounds.

Encouraging 1H Trends

With medtech clearly in a period of transition in 2023 and investment dollars harder to come by, many observers predicted more pain to come in 2024. However, the investment picture this year thus far is much

rosier than anticipated, an indication of the healthcare sector’s resilience and of continued confidence among seasoned investors. Even Healthtech, which experienced a particularly acute investment decline in 2023, was able to reverse course in 1H 2024, with fewer later-stage companies reliant on insider rounds and a surge in early-stage financing (led by AI-based technologies).

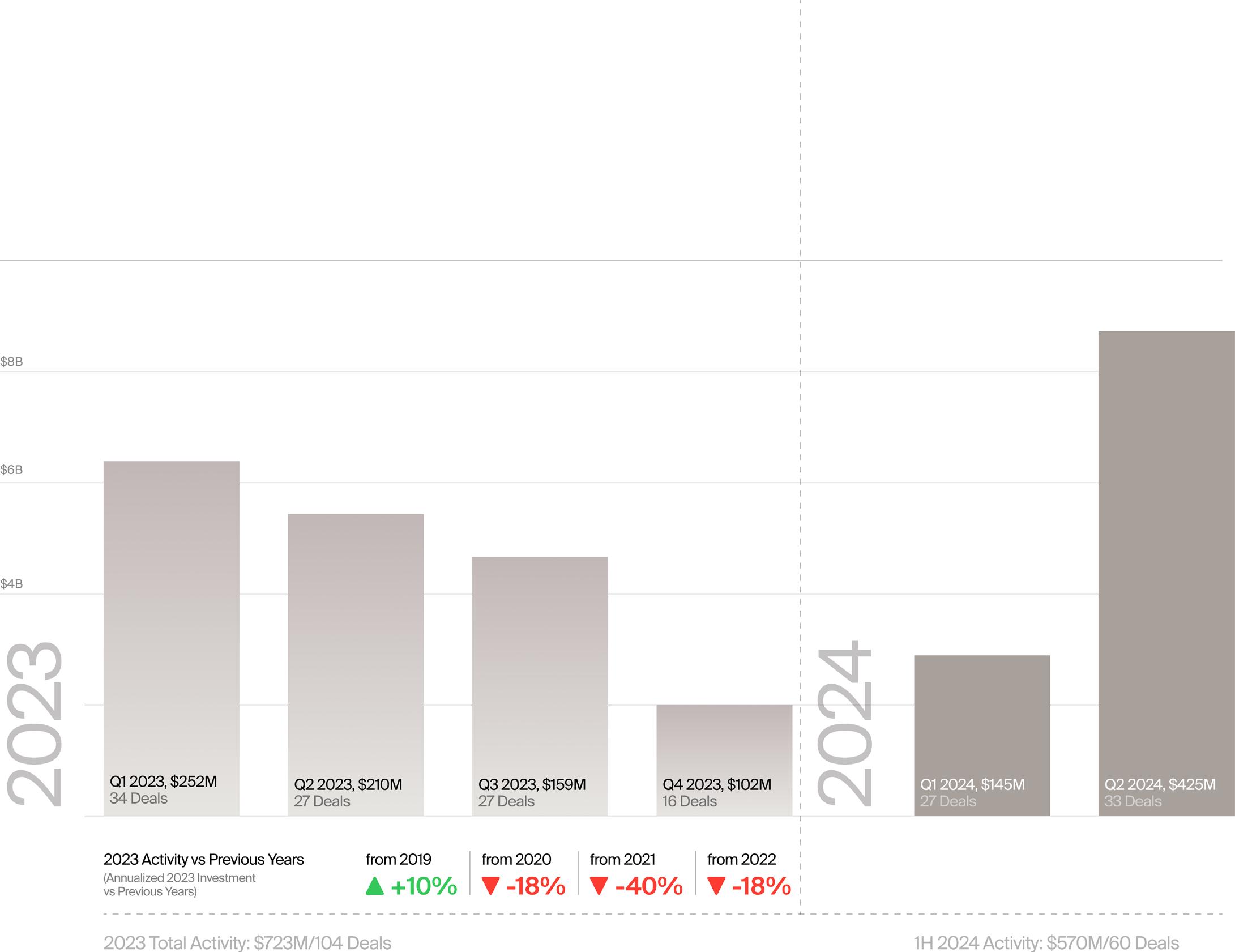

The Med Device sector also saw a substantial increase in first-financing deals in 1H 2024, with $570 million invested in 60 deals, according to Norris. The bulk of that dealmaking occurred in the second quarter, with $425 million invested in 33 deals, a rapid upswing that set a four-year quarterly investment record. Many of those deals involved syndicates that included both VCs and corporate investors.

New investors also led a substantial number of Med Device Series B rounds, and there were fewer down rounds overall. The percentage of down rounds led by new investors in Series B and later deals fell from 33% in 2023 to 20% in 1H 2024, with an increase in median pre-money valuations.

Some clinical areas benefited more than others. Investors seeking new opportuni-

ties were drawn to high-growth areas such as neuro, which garnered the largest share of Med Device first-financing money in 1H 2024. And they were much more willing than they were a year ago to fund device startups requiring extensive clinical trials, such as those pursuing the cash-intensive PMA regulatory pathway. In fact, larger pivotal trial fundings and 510(k)-cleared commercialization rounds accounted for much of the early-stage funding growth that occurred during the first half, according to Norris.

Investors Confident, but Careful

All of this suggests that investor confidence is on the rise. As SVP notes in its recent report, “the combination of improving numbers and investor sentiment in the [device] space makes us cautiously optimistic that investment in devices is turning the corner.”

But while the picture is brighter than it was a year ago, the industry hasn’t completely shaken off the angst of the past couple of years. Traditional medtech investors

Medical Device First-Financing Analysis

have been very successful at raising cash, so there is money to be spent. But as they pick up the pieces left after the pandemic rush, and with exits currently constrained, they are pickier than they were in the past and somewhat more risk averse.

In this back-to-basics environment, investors are looking for start-ups that check all the boxes. That includes companies targeting significant unmet needs with solutions that fit well into existing workflows, a clear path to reimbursement/profitability, preferably with some clinical data to back up their claims, a seasoned management team, and low cash burn. In addition, they are more inclined to share the risk by pulling together multifaceted syndicates that include VCs along with other stakeholders such as corporate investors and large provider systems.

Finding an Exit

The wild card for investors is the exit environment, which was disappointing in the first half of 2024, with fewer M&A deals than anticipated and a dearth of IPOs. Some po-

Investment and Deal Activity ($s/Deals)

2023-1H

Medical Device All Deals Analysis

Investment stable, driven by pivotal trial and commercialization deals

tential buyers may still be waiting for further valuation adjustments, and with the IPO window essentially closed at the moment, corporate acquirers can afford to wait and shop around for the best deal.

Although some analysts are predicting an uptick in exits by the end of this year or early next, a scenario that SVB notes could “spark a wave of new private investments,” there are still unpredictable economic and geopolitical factors at play that could slow the exit recovery.

IPOs have been particularly sparse so far this year. The one medtech company that did go public during 1H 2024—Fractyl Health—has not performed well in the aftermarket (Fractyl, which went public in February, is developing endoscopic hydrothermal ablation devices designed to treat metabolic diseases, including diabetes and obesity. The company’s stock was initially priced at $15 per share but is now hovering around $2 per share).

However, there have been several successful M&A deals completed or announced during the first half, which adds to the positive momentum. Perhaps most notable is Boston Scientific’s planned $1.26

Venture Investment and Deal Activity ($s/Deals)

Source: HSBC Healthcare Annual Report 1H 2024

billion acquisition of carotid intervention company Silk Road Medical, announced in June. Silk Road nicely complements Boston Scientific’s peripheral interventions unit and bolsters the company’s presence in the potentially multi-billion-dollar global carotid disease market.

Silk Road is the second large M&A deal announced by Boston Scientific this year. In January, the company inked a $3.7 billion agreement to acquire Axonics, a company with neuromodulation devices for incontinence. Both the Axonics and the Silk Road deals are currently under FTC review, which will delay the anticipated closing dates.

Despite the current challenging environment, Boston Scientific remains one of the most active medtech strategic acquirers, typically completing a “good handful” of acquisitions every year, according to Michael Ryan, Boston Scientific’s VP Venture Capital & Business Development, speaking at LSI’s 2024 USA conference during a panel entitled “Corporate VCs: What They Want and How They Align with M&A and Business Development.”

But even Boston Scientific has been looking to de-risk its investments. Although

Ryan noted that the company does occasionally acquire pre-commercial entities, its most recent deals have focused on companies that are already generating significant revenue. “Most of our acquisition dollars and activity goes towards companies that have been further de-risked, have demonstrated that there’s market demand and reimbursement, and already have a revenue trajectory,” he said.

That desire to de-risk is much more prevalent than it was a few years ago, according to Bennet Blau, a managing director with Goldman Sachs, who spoke at the same meeting during a panel session entitled “Medtech M&A 2024: Looking Onward and Upward.” The amount of capital available for M&A remains “exceptionally high,” Blau noted, but the bar is now much higher. “The criteria have increased substantially in terms of de-risking, of checking the box not only on growth, but quality growth, recurring revenue, and good business models.”

Chris Eso, Medtronic’s VP, Global Head of Corporate and Business Development M&A and Ventures, agreed, noting during the same panel session that right now, the overall aim of M&A for Medtronic is to “im-

prove our earnings power” and “get our margins back to where they were pre-pandemic.” That said, he pointed to some macro headwinds that are impacting M&A activity in 2024, including inflation, high interest rates, and low stock prices. In that environment, it’s difficult to find M&A offering a nearterm growth opportunity at a reasonable valuation, he said. That could improve over the next several months, but in the meantime, Medtronic is “still looking and active, we just haven’t pulled the trigger on a lot of things.”

Medtronic is unique because it was one of the first large strategics to align itself with a private equity firm—Blackstone—which has invested “well over a billion dollars” to help fund some of Medtronic’s growth objectives, according to Eso.

And, Eso noted that de-risking those investments is a big part of the appeal of working with partners such as private equity firms. “We need some more later-stage dollars like Blackstone to take the clinical and reimbursement risk so that we’re taking the commercial risk,” stated Eso. “That’s what we’re good at—taking a technology and driving it to standard of care. But everybody has their piece that they do really well, and we as an ecosystem have to work together across the board.”

Even though strategics are being more cautious, they are doing deals. In addition to the large acquisitions announced by Boston Scientific, Stryker closed on several tuck-in acquisitions this year, and plans to add more as the year progresses. And Edwards Lifesciences has also been on something of a buying spree lately.

In March, Stryker acquired French ortho implant company Serf, followed in July by two more tuck-ins: soft tissue fixation com-

pany Artelon and Molli Surgical, which has a breast cancer surgical marker.

Stryker’s latest deal, announced in August, is a definitive agreement to acquire care.ai, which provides AI-assisted virtual care solutions, including smart sensors and other smart room monitoring systems, to hospitals and other care providers. According to care.ai, the technology will assist Stryker’s customers, who continue to face nursing shortages, employee retention challenges, overworked staff, and workplace safety concerns, and will fit “seamlessly” into Stryker’s Vocera communication platform.

Edwards Lifesciences announced three acquisitions this summer involving both early- and late-stage companies, all of which fit well into Edwards’ existing structural heart business. In mid-July, Edwards announced that it had exercised its right to acquire early-stage transcatheter mitral valve replacement company Innovalve for an undisclosed amount. Edwards has been an investor in the company since 2017 and noted in the announcement that Innovalve had demonstrated “promising early clinical experience.”

This was followed about a week later by agreements to acquire JenaValve Technology and Endotronix. JenaValve brings the Trilogy Heart Valve System for aortic regurgitation, which is expected to be FDA approved in late 2025, and Endotronix recently received FDA approval for Cordella, an implantable pulmonary artery pressure sensor for people with heart failure. Edwards had been an investor in Endotronix since 2016 and held an option to acquire the company. Individual purchase prices were not disclosed, but Edwards said the aggregate up-

front purchase price for JenaValve and Endotronix was about $1.2 billion. The company expects all three acquisitions to strengthen its leadership position in structural heart and offer long-term growth opportunities.

Will the Momentum Continue?

With healthcare investment showing positive momentum in the first half of the year, the question now is whether that momentum will continue through the end of 2024 and beyond. Although the early signs are hopeful, with US election uncertainty and continuing economic concerns potentially casting a shadow well into the fall, it could be early 2025 before things are truly back on a more normal course.

And for some companies, this uncertainty is creating an existential moment. Surgical robotics company Asensus Surgical, for example, recently told its shareholders that if they did not approve a pending 35-cents per share merger with Karl Storz, Asensus would be forced to file for bankruptcy.

Although analysts such as Norris do anticipate more industry consolidation and company shutdowns in the second half of the year, particularly as insider cash runs out, the outlook for the most part is optimistic. As HSBC notes in its 1H 2024 report, 2024 activity has demonstrated the healthcare investment community’s ability to find a path forward despite headwinds. “We are now seeing healthy and sustainable investment revitalize optimism for a solid, albeit bumpy, second half of the year.”

Emily West (Managing Director, Goldman Sachs), Siddarth Satish (Vice President AI, Stryker), Adam Wollowick (Sr. Director Business Development, Stryker) and Bryant Zanko (Vice President Corporate Business Development, Stryker) discuss the role of M&A in Stryker’s

‘24

Around the Industry — Notable Medtech Investments in 2024

With today’s more stringent investor requirements in mind, it’s worth taking a look at a few of the stand-out medtech investment deals completed thus far in 2024 to help identify common threads attracting investor interest.

Women’s Health, Neurostim, and Incontinence Gain Early-Stage Dollars

Of the early-stage medtech rounds completed in the first half of the year, UKbased Amber Therapeutics’ huge $100 million Series A haul, which closed in June, tops the list. The company—a presenter at LSI’s 2024 Europe conference—garnered one of the largest Series A rounds ever for a European medtech.

Although the deal seems massive for a little-known company founded only three years ago, it should not be surprising given Amber’s focus on neuromodulation (one of the hottest growth areas) and women’s health (one of the most underserved), as well as its quick, cash-sparing path to the clinic (the company was founded in 2021,

began its first human study in late 2022, and by early 2024 had preliminary results confirming the safety and feasibility of its technology).

The Series A raise was financed by a syndicate of US and UK investors, led by New Enterprise Associates, and including new investors F-Prime Capital, Lightstone Ventures, and corporate VC participant Intuitive Ventures, along with existing investors Oxford Science Enterprises (which operates in partnership with the University of Oxford), and 8VC.

Amber Therapeutics intends to use the proceeds to fund pilot and pivotal studies aimed at US regulatory approval for its Amber-UI device, a unique, fully implantable adaptive neuromodulation therapy for women with mixed urinary incontinence (a combination of both urge and stress incontinence).

Amber-UI targets the pudendal nerve

originating from the sacral plexis in the pelvic region, and the device is implanted using a minimally invasive procedure. It is the first device of its kind aimed at urinary incontinence, a common condition that the company says impacts 40 million women in the US.

The need is clear, the firm says, since less than half of those women are being treated, and no single therapy option is currently available that can treat mixed incontinence. LSI’s Market Intelligence analysts value the global sacral stimulation market at $1.5 billion in 2023, increasing at a CAGR of 7% to $2.2 billion by 2028.

Amber Therapeutics wasn’t the only women’s health start-up that pulled in a sizeable round in the first half, nor was it the only venture funded company targeting unmet needs for people with urinary incontinence. Women’s health diagnostics company PinkDx, cofounded in 2022 by

Veracyte cofounder Bonnie Anderson and based in Daly City, CA, launched in April with a $40 million Series A. The round was led by Catalio Capital Management, LP, and The Production Board, with several other investors participating, including Mountain Group Partners, Byers Capital, and Mayo Clinic.

PinkDx is developing tests aimed at unmet medical needs unique to women, with an initial focus on difficult-to-diagnose gynecological cancers. It aims to “develop solutions to replace invasive and painful diagnostic procedures and mitigate the significant delays women and their doctors often face in obtaining answers.”

In addition, iO Urology, a start-up offering the first digital diagnostic/monitoring platform for home-based urologic care, including incontinence, completed a $19.4 million Series A round in March. iO Urology’s CarePath system consists of an easyto-use, connected hand-held device that patients can use in the privacy of their own home. The device captures data on urine flow rate, volume, time, and duration and a cloud-based analytics platform produces patient reports that the healthcare provider can view on any connected device.

The company’s aim is to improve care for both men and women with lower urinary tract issues, including overactive bladder (urge incontinence), which affects 36% of women and 16% of men in the US, and benign prostatic hyperplasia, which affects 38 million US men, and to provide better tools for clinical trials in the urology/urogynecology area. iO Urology believes CarePath can improve patient compliance, data accuracy, appropriate diagnoses, and patient satisfaction, and decrease healthcare costs.

The Series A round was led by Solas BioVentures and included Launch Tennessee and Jumpstart Capital. It also included two urologic strategics, one of which is Laborie Medical Technologies Corp. (LMT) of Portsmouth, NH, a leading diagnostic and therapeutic medical technology company focused on urology, urogynecology, gastroenterology, OB Gyn, and neonatal health. Based in Knoxville, TN, iO Urology intends to use the proceeds to expand its team and build inventory and distribution capability for CarePath, which is FDA-approved and already in use by urology clinics in the US, according to LMT.

Remote Patient Monitoring Bounces Back

iO Urology also falls into

of remote patient monitoring (RPM), which surprisingly saw a resurgence in funding in the first half of this year, after a dismal performance in 2023 coming off pandemic-driven highs. And, given RPM’s high growth potential, there’s good reason for that. According to LSI’s Market Intelligence analysts, the global RPM market was valued at $23.7B in 2023 and is projected to reach $40.7B by 2028, a CAGR of 11.4%.

Two other RPM companies that garnered substantial venture rounds in the first half were San Diego-based biosensor developer Allez Health, which closed on a $60 million Series A+ round in May, led by a strategic—Korean in-vitro diagnostics company Osang Healthcare—with participation from existing investors; and LSI alum, San Diego-based Biolinq. Biolinq completed a $58 million Series D round in April, led by Alpha Wave Ventures, with participation from Niterra’s corporate VC fund, jointly operated with Pegasus Tech ventures, and several existing investors, including Taisho Pharmaceutical. Both Allez and Biolinq operate in the diabetes space and are developing next-generation continuous glucose monitoring (CGM) technologies, and both are moving toward regulatory submissions. Biolinq expects to complete a US pivotal trial this year for its wearable patch-based intradermal glucose sensor.

Although CGM devices were originally developed to help people with diabetes, it’s worth noting that the two commercial leaders in the CGM space—Dexcom and Abbott—will soon introduce over-the-counter CGM devices that can be purchased without a prescription, opening up the market to a much wider range of potential users, including health-conscious people without diabetes or prediabetes looking for a wearable to track their metabolic health. The potential upside for the CGM market from OTC sales could be huge and is likely a big consideration for investors interested in next-gen CGM technology.

Later-Stage Deals Bolster Cardio, Robotics, and More

Later-stage funding (Series B and above) in 2024 has focused largely on precommercial and pivotal trial rounds, and investors now appear to be much more willing to fund technologies with high-growth potential that require large clinical trials (e.g., PMA devices). As a result, recent investments have aided companies targeting a variety of highrisk/high-reward clinical areas, ranging from

cardiovascular to robotics and beyond.

Making the leap from early-stage/Series A funding to Series B has been particularly difficult for medtech companies over the past two years, but this hurdle seems to have eased somewhat over the past six months, with a handful of medical device start-ups recently completing noteworthy Series B rounds.

One of those is cardiovascular company CroiValve, an LSI alum that closed on a $16 million Series B in August. The round was led by MedTech & Irrus Syndicates and included new investor IAG Capital Partners as well as existing investors Ascentifi, Atlantic Bridge University Fund, Broadview Ventures, Elkstone, Enterprise Ireland, Furthr, and SOSV.

Although venture funding for cardiovascular (CV) technologies was down overall in the first half of 2024, according to Jonathan Norris, managing director of HSBC Innovation Banking, CroiValve was able to buck that trend by leveraging its unique technology, designed to address a significant unmet need, and the fact that it already has promising human clinical trial data.

Headquartered in Dublin, Ireland, CroiValve is developing a novel transcatheter treatment called DUO for tricuspid heart valve regurgitation (TR) that combines the attributes of valve repair and replacement into one device. DUO consists of a coaptation valve, which fills the valve orifice and works in conjunction with the native valve, along with an anchor system—anchored within the superior vena cava with a stent— that connects to the coaptation valve, locking it in place while allowing normal respiratory and cardiac motion.

According to CroiValve, the system is designed to address the unique challenges inherent in the tricuspid valve, including tissue frailty, the presence of nearby critical structures, and the progressive nature of TR, which causes significant annular dilation and massive regurgitation by the time patients are symptomatic. DUO leaves the frail right heart tissue untouched, so it is safe, the company says. It is also effective for a wide range of anatomies and easy to use, according to CroiValve.

At the New York Valves 2024 conference in June, researchers presented positive sixmonth results from CroiValve’s 10-patient TANDEM I first-in-human study. According to the company, the trial showed that the DUO System could significantly reduce TR, had stable positioning and functionality, and that the procedure was simple and safe, with no incidences of arrhythmia or requirements for permanent pacing. CroiValve is working to bring DUO to the US market and

John

began an FDA IDE feasibility study, TANDEM II, in January.

Another recent Series B comes from Shanghai-based Ronovo Surgical, a surgical robotics company that presented at LSI’s 2023 USA conference. Ronovo closed on a $44 million Series B financing in June, co-led by Guolian Capital and INCE Capital, with participation from King Star Med LP and existing shareholder, LongRiver Investments.

Founded in 2021, Ronovo is developing the Carina Platform, the first modular laparoscopic robotic platform developed in China, but “made for the world,” according to company Founder, Chairman, and CEO, John Ma.

Carina is a flexible and cost-effective robotic surgery platform that allows physicians to choose from multiple docking and set-up configurations. The initial system enables three- and four-arm configurations, with 5mm (straight) and 8mm (articulated) instruments, and it is compatible with Storz or Olympus 3DHD vision systems or with a proprietary Ronovo 3DHD system. Eventually, the company plans to offer more modular configurations, additional diversified instruments, and additional vision capabilities, including integrated preoperative imaging.

The company has more than 100 patent applications and is initially targeting gynecology and urology procedures, with plans to expand to general and thoracic surgery in the future. Its most immediate commercial goal is to increase robotic surgery penetration in the Chinese market, where robotic procedures account for less than 1% of the total minimally invasive surgical volume in the country. Ronovo expects to receive reg-

Ma, CEO at Ronovo Surgical, presenting the company’s vision for robot-assisted soft tissue surgery at LSI USA ‘23

ulatory approval in China and begin commercialization in early 2025. But the company hopes eventually to market the system internationally as well, including in the US, where Ronovo recently launched its first international facility—the Ronovo Institute of Surgical Excellence in Orlando, FL—aimed at “deepening clinical collaboration with top international surgical experts and medical societies.”

A few post-B rounds targeting women’s health and robotics also deserve a closer look.

The largest occurred in February, when robotics company Medical Microinstruments (MMI) closed on a $110 million Series C, which it called “the largest ever investment in microsurgery innovation.” The round was led by Fidelity Management & Research Company and included all of the firm’s existing investors. It follows a $77 million Series B the company raised in 2022, bringing the company’s total funding to date to over $200 million.

Founded in 2015 near Pisa, Italy, with US offices in Jacksonville, FL, MMI intends to use the Series C proceeds to support commercialization of its Symani Surgical System and to invest in additional clinical studies aimed at indication expansion.

Symani, with its NanoWrist instruments, is a first-of-its-kind robotic surgery system designed specifically for microsurgery and supermicrosurgery procedures, replicating the natural movements of the human hand at the micro scale and enabling physicians to safely access and suture vessels as small as 0.3 mm diameter.

The system is CE marked in Europe and received US de novo FDA clearance in April

for soft tissue manipulation during microsurgery, making it the only commercially available robotic platform in the US for reconstructive microsurgery, the firm says. The first US clinical cases with the system— for reconstructive extremity microsurgery— were performed in May at Penn Presbyterian Medical Center, and in August, the company performed the first preclinical study of Symani in neurosurgery, demonstrating the feasibility of the system for robotic-assisted microsurgery in an animal brain model.

In June, another company operating in the robotic surgery realm, Oakland, CAbased Promaxo, founded in 2016, garnered $32 million in a Series B3 round, with investment from Zynext Ventures USA, the VC arm of global pharmaceutical company Zydus Lifesciences. In a statement, Jay Kothari, director of Zynext Ventures noted that Promaxo’s “innovative technology aligns perfectly with Zynext’s mission of investing in disruptive new-age healthcare solutions that elevate patient outcomes.”

A presenter at LSI’s USA 2024 conference, Promaxo has developed a portable, low-field MRI system that is open and compact, can be placed in a clinic or operating room, and is designed to be compatible with robotic procedures.

Promaxo’s single-sided MRI with AI based imaging system was the first of its kind in the US to receive FDA 510(k) clearance (in 2021) for use in MR-guided manual and robotic prostate biopsy and targeted therapy. And it has resonated with physicians and patients, with more than 100 sold to date, according to company COO Dinesh Kumar, who told attendees at the LSI conference that Promaxo is “well on the way” to

profitability in the next 12-18 months, with a clear path to up to 70% growth margin.

Promaxo is currently working to obtain FDA clearance for its own robot for guided prostate interventions, including targeted and whole gland procedures, and hopes to receive clearance by the end of 2024 or early 2025. It plans to eventually expand to other indications, including female pelvic floor, OB/gyn, kidney, and breast procedures. The company is also expanding into international markets, with EU as the next geography, and has established a subsidiary in Brussels, Belgium.

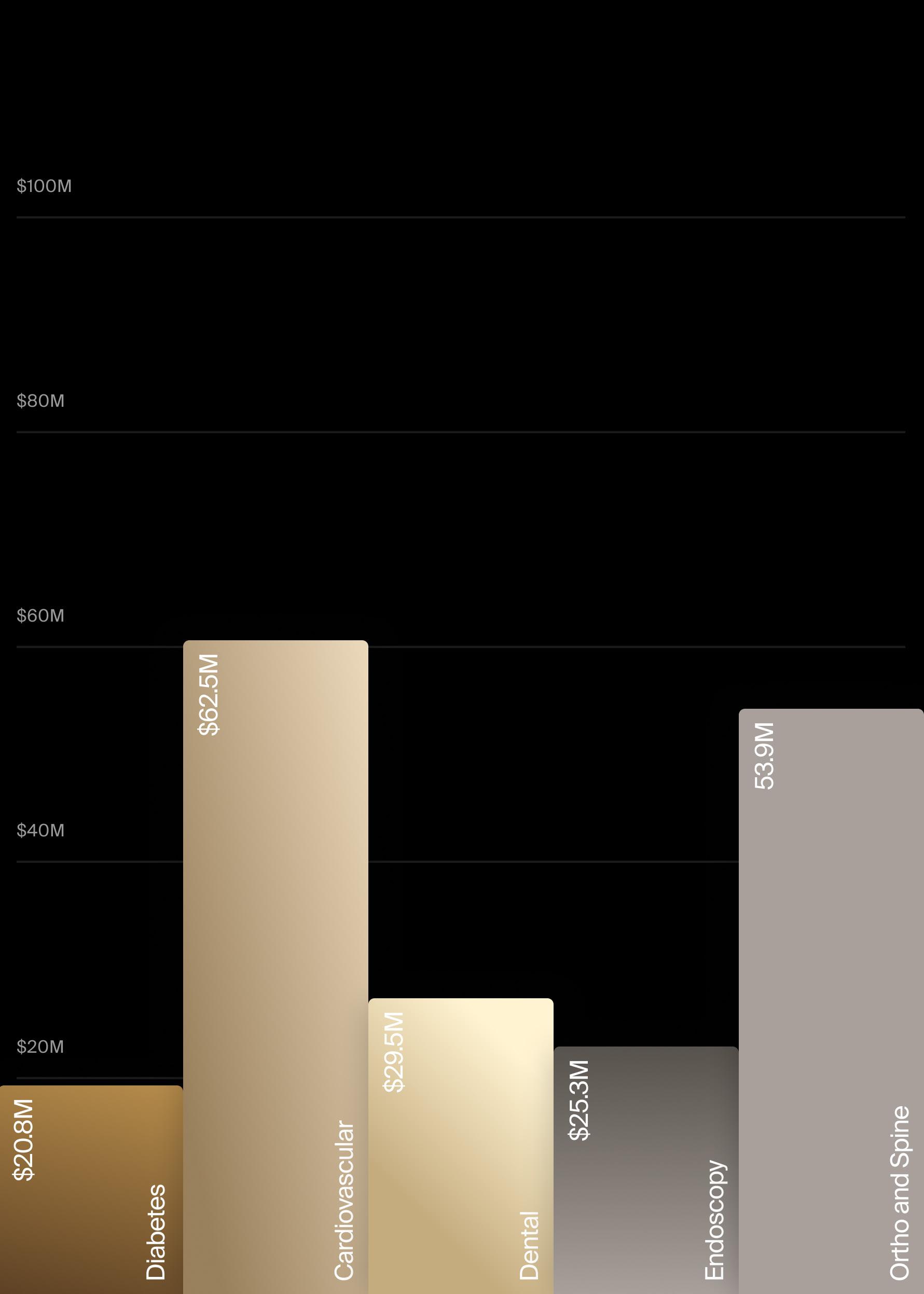

Another later-stage round of note this year was a $77 million Series C (the last $5 million tranche of which closed in May), that went to women’s health company Meditrina. Meditrina received 510(k) clearance in May for its Gen 2 bipolar RF hysteroscopy system, designed to improve minimally invasive gynecologic procedures by offering faster procedure times, enhanced versatility, and the ability to address difficult-to-treat fibroids. The Series C was led by Deerfield Management Company, ShangBay Capital, and other insiders, and was combined with an additional $5 million debt financing by SLR Capital Partners. Meditrina is “approaching cash-flow positive,” the company said in a statement, and will use the proceeds to accelerate new product introduction and expand its sales force.

Meanwhile, several large Series D medtech rounds also closed this year, including an oversubscribed $102 million round completed in August that went to focused ultrasound company HistoSonics; a $96 million round completed by Nectero Medical, which has a novel drug-device combination technology for stabilizing small abdominal aortic

aneurysms (AAAs); and $91 million for knee osteoarthritis device company Moximed (including $61 million up front and an option to close on up to $30 million additional).

HistoSonics plans to use its Series D funds to scale the launch of its noninvasive Edison histotripsy platform, FDA de novo cleared in October 2023, which uses focused ultrasound to destroy and liquefy targeted liver tumors. The company also plans to initiate a clinical study investigating the system for the treatment of liver tumors across multidisciplinary users. The funding round was led by Alpha Wave Ventures, with participation from new investors Amzak Health and HealthQuest Capital, and existing investors Johnson & Johnson Innovation, Lumira Ventures, Yonjin Venture, and others.

Nectero’s $96 million Series D, which closed in April, was led by Norwest Venture Partners, with “large investments” from Boston Scientific Corp., BioStar Capital, Cadence Healthcare Ventures, Aphelion Capital, and others.

The company will use the proceeds to accelerate a Phase II/III trial and support submission of an FDA New Drug Application for its novel Nectero Endovascular Aneurysm Stabilization Treatment (Nectero EAST) System. Nectero EAST uses a single-use dual-balloon catheter to deliver pentagalloyl glucose locally into the aneurysm wall where it binds to elastin and collagen to strengthen the wall and potentially reduce further degradation and growth of the aneurysm. The Phase II/III trial, initiated in January, is investigating Nectero EAST in patients with infrarenal AAAs 3.5-5.5 cm in diameter. There is currently no standard treatment option for people with these

smaller AAAs; endovascular treatments are primarily reserved for AAAs larger than 5-5.5 cm, people who are symptomatic, or those with rapidly expanding aneurysms. Smaller aneurysms are typically monitored over time to see if they are enlarging, but they carry a 0.5-5% annual risk of rupture, according to the company, and rupture can be fatal, so there is an unmet need for a safe and effective intervention for these patients. FDA granted Nectero EAST Fast Track and Breakthrough Therapy designations.

Moximed closed its Series D in August and will use the proceeds to accelerate US commercialization of its FDA-cleared MISHA Knee System, the first “implantable shock absorber” for knee osteoarthritis (OA). The MISHA device is implanted during an outpatient procedure and has been shown to alleviate pain, improve function, and delay the need for knee replacement in certain patients with mild-to-moderate OA, the company says. The Series D was led by Elevage Medical Technologies, a platform established by Patient Square Capital. Elevage provides companies in the advanced clinical or commercialization stage with capital as well as technical, regulatory, and operational expertise, and is “dedicated to supporting medical technology companies that can meaningfully improve health outcomes and quality of life for patients.”

Others who participated were new investors Cormorant Asset Management and Warren Point Capital and existing investors New Enterprise Associates, Future Fund, Advent Life Sciences, Gilde Healthcare, Vertex Ventures, GBS Venture Partners, and Morgenthaler.

Dinesh Kumar, Chief Operations Officer at Promaxo, presenting on “Modular MRI and MRI Based Technologies” at LSI USA ‘24

Market Dive Neuromodulation Devices

Source: LSI Market Intelligence

Therapeutic neuromodulation refers to the alternation of nerve activity through the targeted delivery of a stimulus to specific neurological sites in the body to “modulate” its activity. Just as a cardiac

pacemaker is used to correct abnormal heart rhythms, neuromodulation aims to restore normal nervous system function. With a wide range of potential therapeutic applications, including chronic pain, epilep-

Neuromodulation

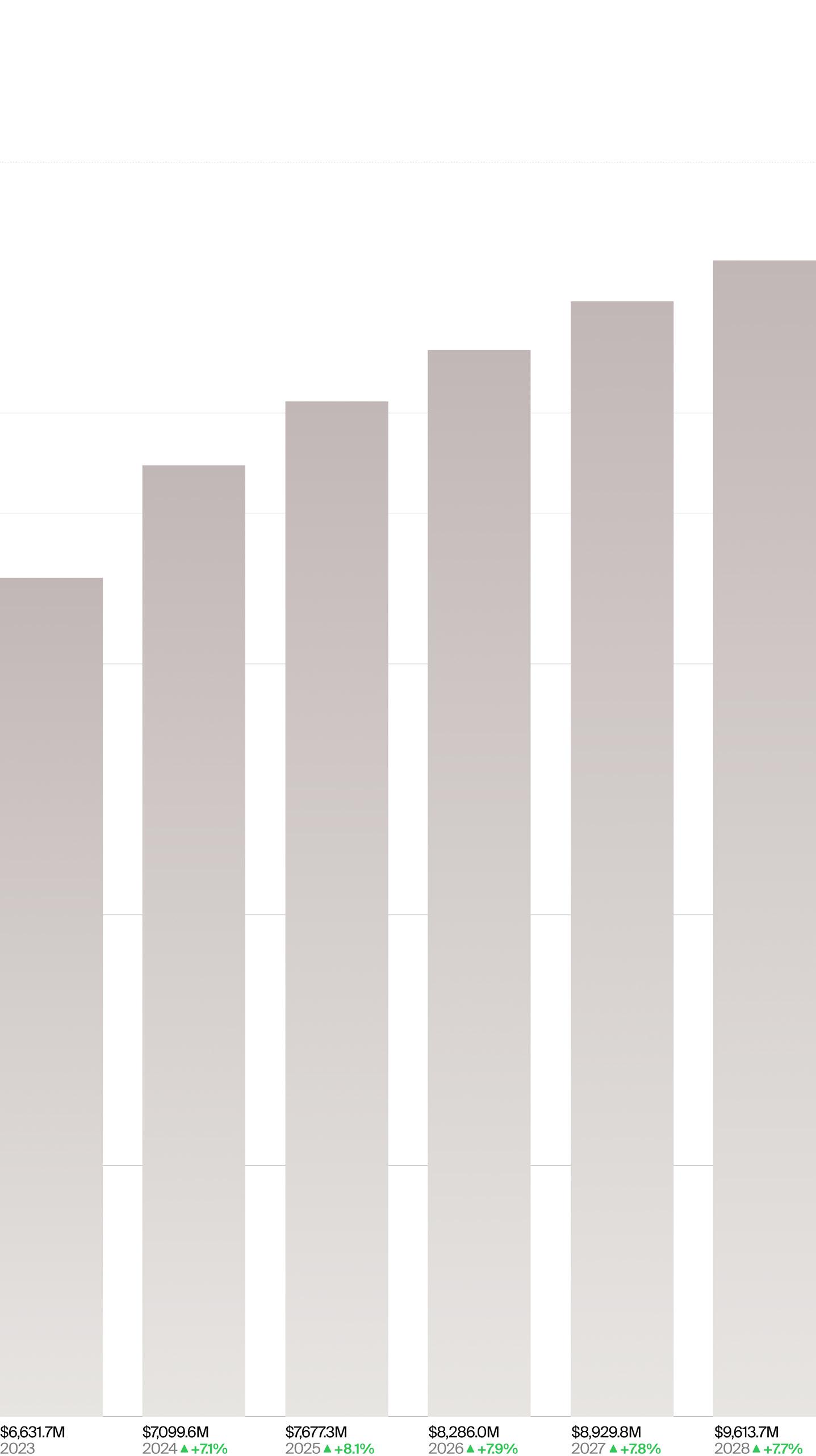

Devices Market Size

Valued at nearly $6.6 billion in 2023, the market is projected to increase at a CAGR of 7.7% from 2023 to 2028.

199,100 Total Procedures Worldwide ~$6.6Bn Market Value

7.7% Growth Rate CAGR (2023- 2028):

sy, movement disorders, and mental health disorders, the global neuromodulation device market continues to see significant growth, attracting new entrants.

Neuromodulation Devices Market Forecast

The neuromodulation devices market remains highly competitive, with leading medical device companies and innovative new medtech firms continually battling for market share. Valued at nearly $6.6 billion in 2023, the market is projected to increase at a CAGR of 7.7% from 2023 to 2028. Approximately three-fourths of the market is attributable to implantable devices, and the high selling price of such devices contributes to a large dollar volume market.

In 2023, an estimated 199,100 procedures involving neuromodulation devices were performed worldwide. Of these, peripheral-based procedures (phrenic nerve stimulation, sacral nerve stimulation, and spinal cord stimulation) accounted for 55% of all procedures performed, while intracranial procedures (deep brain stimulation, vagus nerve stimulation, and responsive neurostimulation device implants) accounted for 45%. Those involving spinal cord stimulation are the most common of all procedures performed.

Over the 2023 to 2028 forecast period, procedure volumes are expected to increase slowly at a 2.9% annual rate, up from 1.4% in the prior year’s analysis. Additionally, a re-analysis of sales in the sacral nerve modulation segment resulted in an increase

of approximately $1 billion, equating to a 20% increase in the total market value. This makes the sacral nerve modulation product segment the fastest-growing product segment in the neuromodulation device market.

Other neuromodulation devices, such as the Inspire hypoglossal nerve stimulator from Inspire Medical, have demonstrated significant market acceptance, with revenues increasing 142% from 2021 to 2023 to $565 million.

Analyst Insights: Key Driving Factors

Historically, neuromodulation devices have been used primarily for the treatment of chronic pain and movement disorders, such as Parkinson’s disease. However, there has been increased adoption of vagus nerve stimulation, deep brain, transcutaneous magnetic stimulation, hypoglossal nerve stimulation, and sacral nerve modulation in an increasing number of indications. The expansion into new indications that have long lacked effective therapies, such as Alzheimer’s disease and depression, is a significant factor driving the high, single-digit market growth. These chronic conditions have historically been challenging to treat and manage via conventional pharmacological treatments. This has

Relevant Global Procedure Volumes (000s)

fueled an urgent need for more advanced solutions—particularly for conditions with high and increasing prevalence, such as Alzheimer’s disease and depression. Improvements in technology have helped decrease the costs associated with certain neuromodulation procedures, increasing the adoption of such devices and, therefore, the neuromodulation device market value. Take sacral nerve modulation, for example. Historically, the adoption of sacral nerve modulation has been relatively limited due to the high costs associated with the procedure. However, improvements in battery technology have reduced the cost of obtaining and maintaining these devices.

Expansion Into New Indicators

As previously mentioned, many companies are looking to utilize neuromodulation to tackle historically hard-to-treat conditions, such as Alzheimer’s disease and depression. People living with Alzheimer’s disease and those with severe or treatment-resistant depression represent two highly underserved patient populations. However, a breadth of exciting medical device development and clinical research shows great promise for these patient populations. Cognito Therapeutics is developing a novel therapy designed to evoke gamma oscillation in the brain via non-invasive visual and auditory stimulation. The company’s Phase 2 OVERTURE trial has shown promising results, with patients experiencing significant slowing of disease progression and preservation of cognition, daily function, and whole brain volume. Also progressing to market is Sinaptica Therapeutics™, which is developing a breakthrough personalized closed-loop neuromodulation therapy for Alzheimer’s disease that aims to enhance neuroplasticity via neurostimulation of key brain networks involved in memory. The company published promising Phase 2 placebo-controlled results demonstrating a slowing of disease progression by more than 80% at six months. The use of neuromodulation devices in the mental health space is also gaining traction, with new and existing players working on transcranial and implantable solutions. Inner Cosmos, for example, created a digital pill that is a subcutaneously implanted brain-computer interface that aims to rebalance networks within the brain by delivering precision micro-stimulations to focused networks within the brain. With an initial focus on treating depression, Inner Cosmos announced promising findings from the initial phase of its human trials in April of 2024.

Market Events: Additional Driving Factors

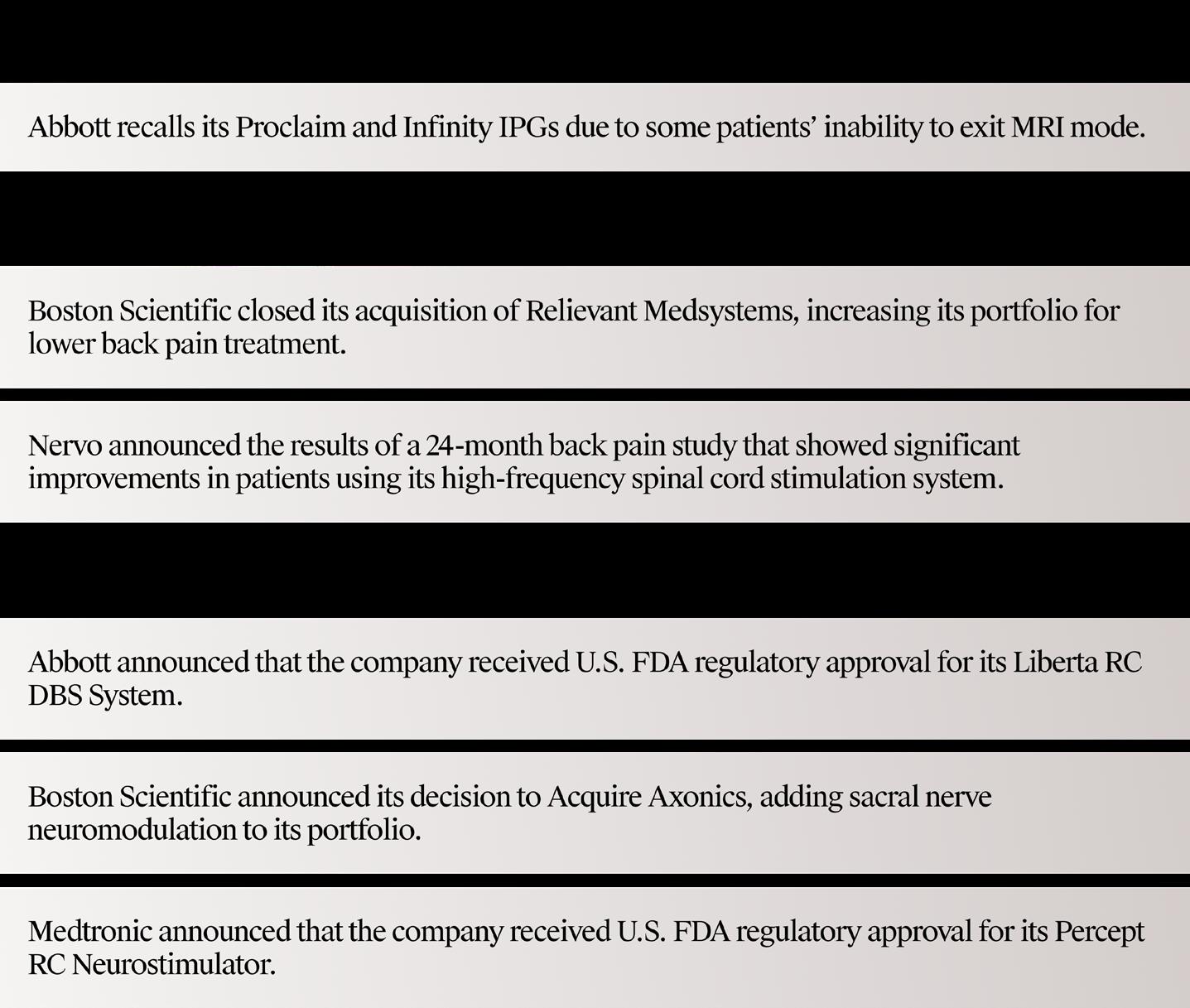

Market events, such as regulatory approvals, M&As, clinical research studies, and recalls, significantly influence the competitive and growing neuromodulation device market. Below is a brief timeline of notable market events:

Axonics is an excellent example of the influence market events can have on the growth of the neuromodulation device market. The rapid scaling of Axonics’ commercial team, combined with strong clinical data across multiple indications, greatly contributed to Axonics’ success. Their aggressive entrance into the sacral nerve modulation market likely prompted market leader Medtronic to innovate to defend its market share. Axonic’s growth, paired

with a product portfolio complementary to Boston Scientific’s Urology business, likely prompted the decision to acquire Axonics. With new technologies, high competition amongst existing players, and the emergence of new players entering the market, the neuromodulation device market is well-positioned for significant growth and expansion. As the market continues to grow, new products continue to gain regulatory approval. Meanwhile, many companies are working to pioneer this type of technology for new indications, such as Autism Spectrum Disorder, heart failure, and autoimmune and inflammatory diseases, further driving growth of the market.

Looking for more Neuromodulation market intelligence and insights?

Access LSI’s full Neuromodulation Devices Market Snapshot today.

Market Intelligence Platform

Global Surgical Procedure Volumes Database

The industry’s most comprehensive and trusted global procedure database, with coverage of 200+ diagnostic and therapeutic procedures in 12 major categories across 37 countries.

Market Dive Urology and Renal Devices

The global urology and renal device market is a rapidly growing segment encompassing a wide range of devices used to diagnose, treat, and manage kidney and urinary system conditions. These include end-stage renal disease (ESRD),

Urology and renal devices have broad applications in dialysis centers, hospitals, and home care settings and are essential in improving quality of life and patient outcomes. Several key factors, such as the aging population and increases in incidence and prevalence, contribute to a competitive and growing market.

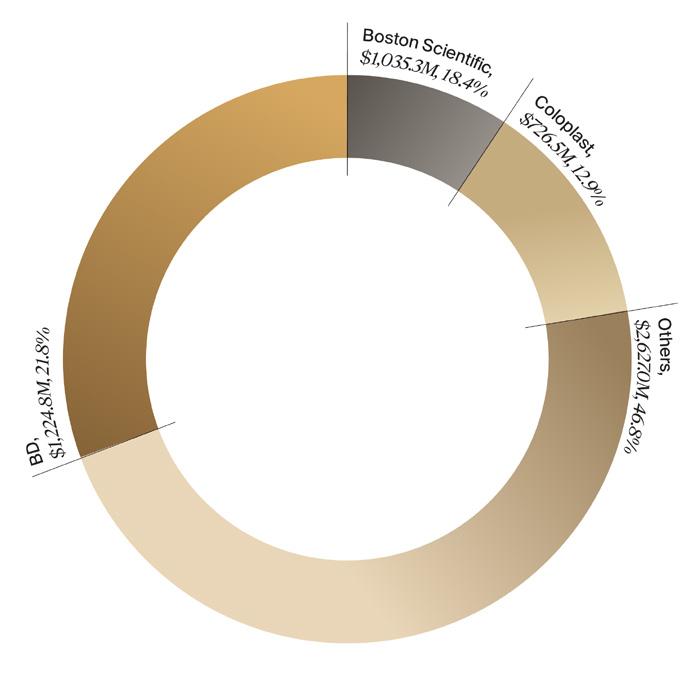

Source: LSI Market Intelligence

Key players such as BD, Boston Scientific, and Coloplast continue to dominate the urology and renal device market, accounting for more than 53% of the market share. BD is leading the charge after its 2017 acquisition of C.R. Bard. With only two of the top ten medtech companies active in the urology and renal device space, there is a significant market opportunity for both new and existing players.

Valued at $5.6 billion in 2023, the urology and renal device market is projected to increase at a CAGR of 8.4% from 2023 to 2028. Dollar-volume market growth is predominantly driven by the adoption of more advanced technologies, like ablation and lithotripsy devices, that command higher average selling prices compared to more commoditized devices, like Foley catheters and urine bags.

Unit volumes are projected to increase at a CAGR of 5.8% from 2023 to 2028. Considering the number of conditions being treated by urology and renal devices and their strong association with advanced age, the primary driver of market growth is the aging population at risk of developing acute or chronic conditions.

Analyst Insights: Key Driving Factors

The market for urology and renal devices is largely driven by increases in the incidence and prevalence of urological diseas-

es, including ESRD, urinary incontinence, BPH, prostatitis, and ED. Price increases for urology and renal devices represent another key factor driving market growth. The global trend in prevalence, in conjunction with the increased use of device-based therapies, will likely contribute to unit volume growth.

A very small percentage of males with prostatitis and ED are treated with device-based therapy. Therefore, it is fair to assume that trends in ESRD, urinary incontinence, renal calculi, and BPH are the primary drivers of the market.

Furthermore, there aren’t many timely, effective, and safe drug-based approach-

Market Events: Additional Driving Factors

es available for many urological conditions. Even for conditions where effective drugs are available, like BPH, there are still issues surrounding side effects and adherence. Many patients would prefer a quick, office-based procedure over taking a pill a day for the rest of their lives.

Similarly, there is a lack of effective drugbased therapies for urinary incontinence, especially stress incontinence, resulting in a high demand for better, non-drugbased solutions. The greater interest in device-based therapies among the patient population will likely contribute to market growth.

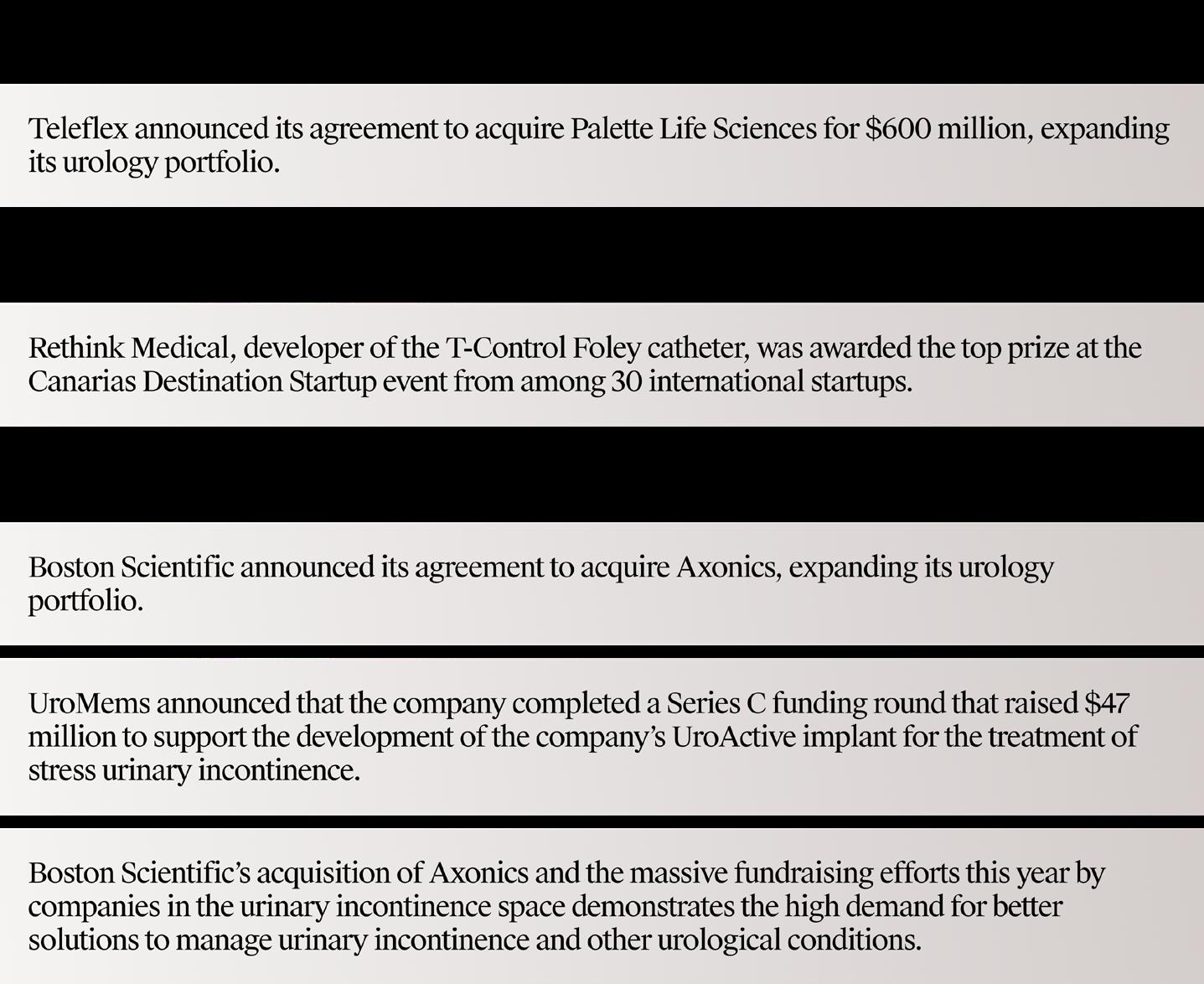

Market events like M&As and fundraising also influence the competitive and growing urology and renal device market. Below is a brief timeline of notable market events:

Source: LSI Market Intelligence

Looking for more Urology and Renal market intelligence and insights?

CAGR (2023 - 2028)

Market Dive Transcatheter Mitral Valve and

Tricuspid Valve Repair and Replacement Devices

Looking for more Transcatheter Mitral Valve Repair devices intelligence and insights?

Looking for more Tricuspid Valve Repair devices intelligence and insights?

Access LSI’s full Tricuspid Valve Repair Devices Market Snapshot today.

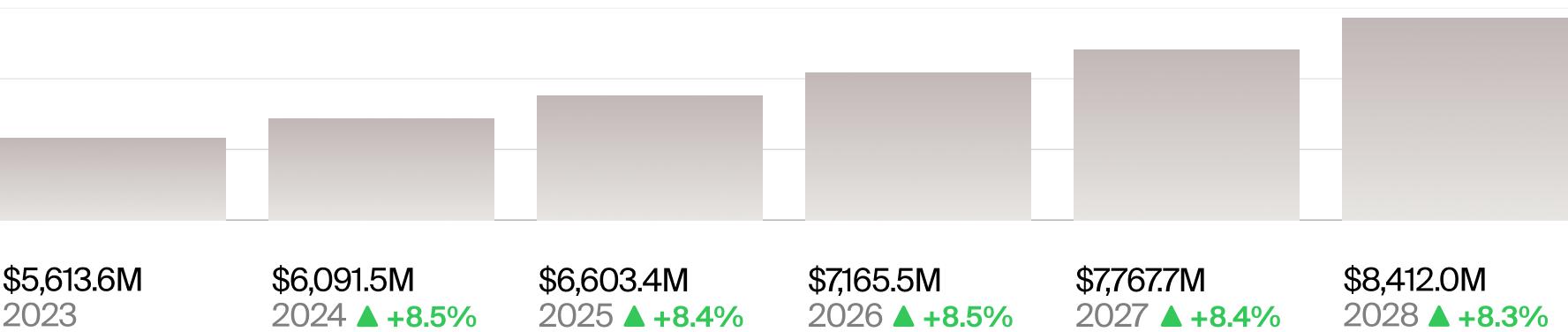

The cardiovascular devices market is a dynamic and rapidly evolving sector within the broader medical technology field. In 2023, the global cardiovascular device market was valued at $58.8 billion, with transcatheter technologies leading the charge.

While the transcatheter aortic valve space is beginning to show signs of maturity, the next major objective within the structural heart market is treating valvular disease of the tricuspid and mitral valves.

These respective markets are beginning to see a steady influx of new transcatheter solutions, which will make less invasive treatment options available to patients contraindicated for open surgical valve repair and replacement.

Tricuspid and Mitral Valve Repair and Replacement Devices Markets

Tricuspid regurgitation is estimated to affect more than 70 million people worldwide and 3 million people in Europe. Currently, only a small fraction of people with tricuspid valve disease disorders receive treatment, with only 9,000 of 3 million patients in Europe estimated to undergo tricuspid valve repair or replacement due to high operative risk.

Mitral regurgitation, one of the most common valvular heart diseases, is estimated to affect more than 175 million people worldwide, a figure considerably larger than that of calcific aortic valve disease. Despite its high prevalence, mitral regurgitation is also regarded as a severely undertreated condition in terms of repairs and replacements.

Tricuspid and Mitral Valve Repair and Replacement Devices Market Forecast

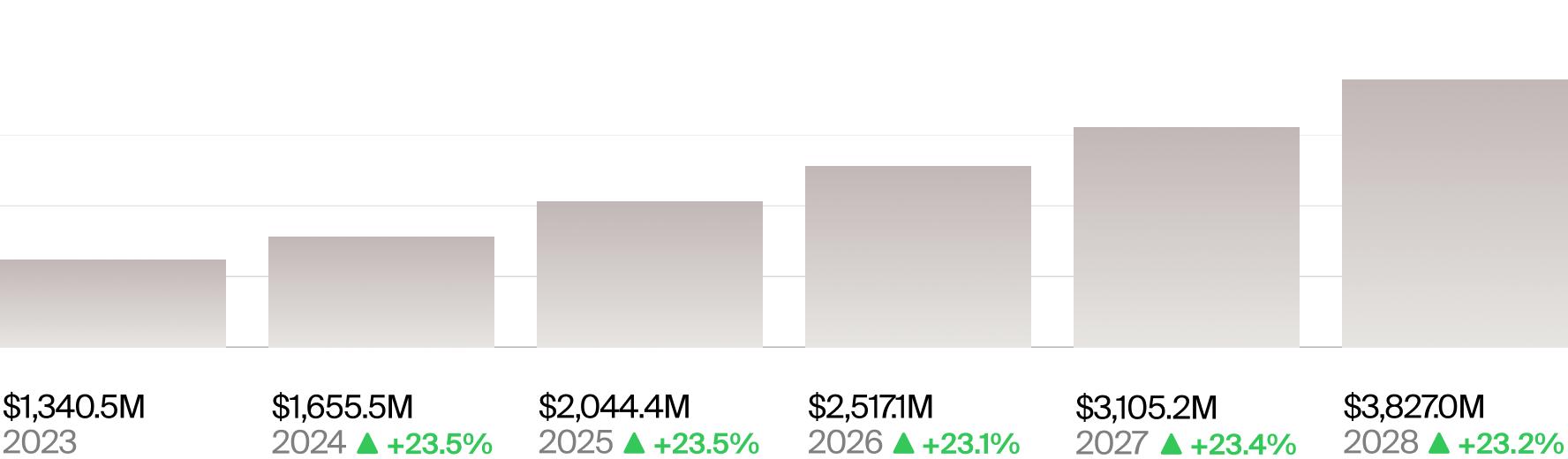

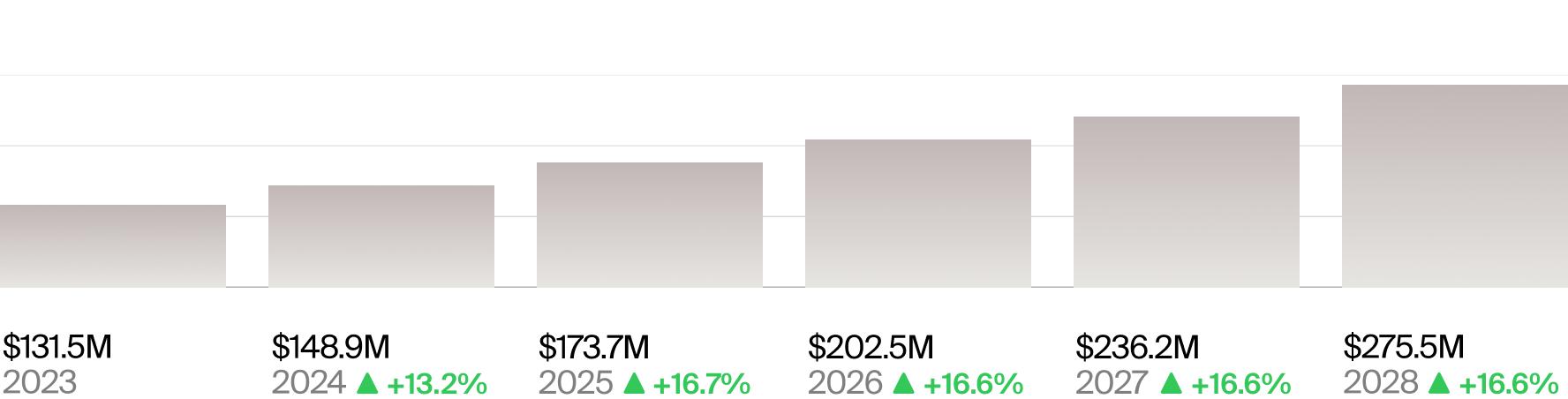

The tricuspid valve repair device market, valued at nearly $132 million in 2023, is projected to increase at a CAGR of 15.9% from 2023 to 2028. The transcatheter mitral valve device market, valued at $1.3 billion in 2023, is projected to increase at a CAGR of 23.3% during the same forecast period.

ties, they exhibit differing characteristics regarding market size, potential for growth, and technological advancements. The transcatheter mitral valve market is more mature and substantially larger than the tricuspid valve repair device market, though both are expected to experience double-digit market growth. The transcatheter mitral valve device market’s growth is primarily driven by the large patient population living with mitral valve disease and the robust pipeline of new devices. On the other hand, the tricuspid valve device repair market’s growth is primarily driven by the emerging focus on treating tricuspid regurgitation and the recent approval of new transcatheter devices (and the premiumprices these devices will command).

Analyst Insights

Currently, in the U.S., the only approved devices on the market for transcatheter mitral valve surgery are Abbott’s MitraClip (a mitral valve repair device), Edwards’ Sapient 3 for mitral valve-in-valve procedures, and Edwards’ PASCAL TMVr system. Worldwide, however, several other TMVr and TMVR devices are on the market, primarily in Europe. This includes Cardiac Dimensions’ Carillon, Edwards’ Cardioband, Mitralign’ MPAS, Abbott’s Tendyne, NeoChord’s mitral valve repair device, and the Venus MedTech/OPUS system.

As new transcatheter mitral valve devices enter the market, growth is expected to continue at double-digit rates. CMS approval of reimbursement for transcatheter mitral valve repair in patients with secondary mitral

regurgitation could potentially double or triple the number of patients who are able to undergo TMVR, proportionally increasing market opportunity.

As previously mentioned, the tricuspid valve repair device market is far less developed than the mitral valve device market. In April 2020, the Abbott TriClip device received the CE mark, becoming the first device of its kind to receive a CE mark for minimally invasive tricuspid valve repair. Subsequently, the OrbusNeich TricValve received a CE mark in May 2021.

At least nine additional transcatheter devices are in development for tricuspid valve repair, including the PASCAL and Cardioband tricuspid devices from Edwards, the Boston Scientific Cardiovalve, the Medtronic Intrepid, the TriSol Medical TriSol device, the Mitralix Mistral, the CroíValve system, the NaviGate valve, and the Tricento device from New Valve Technology.

In February 2024, Edwards received U.S. FDA Approval for its EVOQUE tricuspid valve replacement system, the first system to receive approval for the replacement of the tricuspid valve without the need for openheart surgery.

Although the market introduction of such products is in the early stages, the reduced operative risk associated with introducing these new percutaneous devices will likely drive increased growth in the tricuspid valve repair market. When these devices enter the market, prices are expected to increase at a substantially faster rate, as the average selling price is estimated to be 10-fold higher than for existing annuloplasty rings.

Tricuspid Valve Repair Devices Market Forecast

(2023 - 2028)

(2023 - 2028)

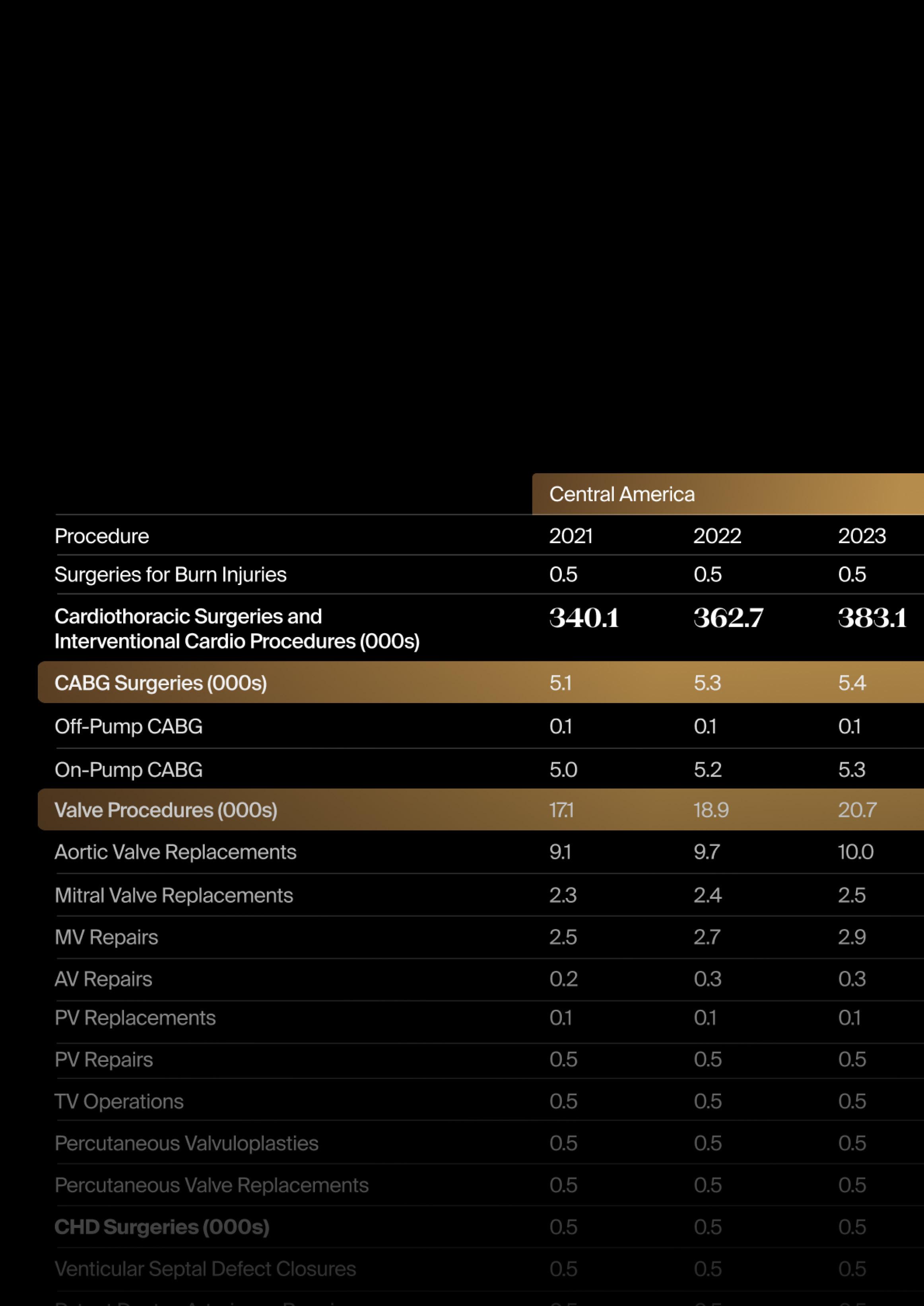

Global Procedure Volumes Cardiothoracic Surgeries and Interventional Cardiology

Data sourced from LSI’s Global Procedure Volumes Database, which provides trusted coverage of 200+ diagnostic and therapeutic procedures in 12 major categories across 37 countries.

LSI Alumni Milestones: June and July 2024

Source: LSI USA ‘24

FibriCheck, founded in 2014, is an innova-

tive digital cardiovascular health company with an initial focus on early detection and monitoring of irregular heart rhythms, such as atrial fibrillation (AF). The company’s goal is to transform the way cardiac care is delivered to provide a highly accessible, user-friendly approach for people to take control of their heart health.

AF is highly prevalent, with an estimated one in four adults over 40 developing AF at some point in their lives. AF is traditionally detected using specialized medical electrocardiogram (ECG) equipment. While there have been improvements in form factor and ease of use, such as wearable ECG and photoplethysmography (PPG) devices, these solutions are often inaccessible to patients due

to their device-dependent nature. By utilizing a “bring-your-own-device” strategy, FibriCheck provides a software-only, device-agnostic PPG solution. Users can measure their heart rhythm in 60 seconds using their smartphone’s camera without additional hardware. The data is then sent to a medical AI platform that performs a heart rhythm analysis.

In July, FibriCheck received FDA clearance for the entire FibriCheck ecosystem, which includes its patient-facing smartphone application, AI platform, and healthcare provider portal. Independent external validation studies showed that FibriCheck’s accuracy for detecting AF is excellent, with a sensitivity of 98.3% and a specificity of 99.9%.

Bone Health Technologies Acquires Wellen

Bone Health Technologies was founded in 2018 and is focused on providing effective, safe therapies for improving bone strength and density to the millions of individuals looking for alternatives or additions to their current treatment options. While initially focused on the broad osteopenia (low bone density) market, Bone Health’s vision is to start with early prevention and treat patients along the disease continuum.

An estimated 64 million and 10 million Americans suffer from osteopenia and osteoporosis, respectively. These numbers continue to persist despite the fact that there have been osteoporosis medications for over 20 years. Fewer than 10% of patients who qualify for osteoporosis medications, even if fractured, will take these medications due to the poor side effect profiles. Although other treatment approaches like high-impact exercise have been shown to be effective in improving bone density, many, if not most, people with osteoporosis are unable to do so.

Thanks to NASA’s recent research surrounding regaining bone density in astronauts, vibration therapy has emerged as an extremely promising therapy for improving bone density. Developed from NASA’s proven vibration platform technology, Bone Health Technologies created a vibration therapy belt. This provides a convenient form factor while delivering precise mechanical stimulation targeted at the hips and lumbar spine, areas known for more frequent and serious fractures.

Following the company’s FDA clearance of Osteoboost™, Bone Health Technologies announced in July that it had acquired Wellen, a Brooklyn-based health technology company reinventing exercise-based osteoporosis care. This acquisition is a significant step toward achieving its vision of a comprehensive, multimodal bone health solution.

Trukera Medical Acquired by Bausch + Lomb

TearLab introduced tear osmolarity testing to eye care with its flagship device, the TearLab Osmolarity System, which has been used to perform more than 24 million tests worldwide. In 2022, TearLab announced a corporate name change to Trukera Medical to reflect its further expansion in the corneal health space. The company’s expanding portfolio continues to focus on improving corneal health, whether as a primary goal or in preparation for surgery.

Unlike many specialties, ophthalmologists are not able to base their decisions on laboratory results, as there is little insight into diseases of the eye from blood, saliva, and urine. This led TearLab to pioneer a concept to precisely measure osmolarity, the salt content of a person’s tears. When exposed to elevated levels of salt, cell stress and death can occur. Hyperosmolarity, a condition not detectable by slit lamp examination, is a leading indicator of asymptomatic dry eye disease and ocular surface disease, both of which can negatively affect corneal, cataract, and refractive surgery outcomes if not effectively treated before surgery. Trukera’s newest device, the ScoutPro, was created to go a step beyond its predecessor and provide a scalable, portable option to keep up with high-volume demands. It offers the same trusted lab precision as the TearLab Osmolarity System but integrates both devices (specimen collection and analysis) into a single handheld device.

In July of 2024, Bausch + Long Corporation, a leading global eye health company, announced an affiliate has acquired Trukera Medical from its previous equity owner, AccelMed Partners, and other shareholders. This tuck-in acquisition will aid in expanding Bausch + Lomb’s surgical presence in the United States and contribut contribute to its leading position in the dry eye space.

SamanTree Medical Closes $14M Series B Funding Round

SamanTree Medical, founded in 2014, specializes in innovative imaging solutions to improve surgical outcomes in cancer treatment. Their goal is to bring microscopy and decision-making to the operating room by providing surgeons with real-time, extremely high-resolution imaging tools to ensure complete tumor removal. Tissue assessment is an essential component of efficient cancer treatment. The challenge is obtaining high-resolution results in a timely manner. Standard histopathologies can take days to weeks, if not a month. Frozen section analysis can be performed by pathologists intraoperatively; however, this process can take anywhere from 40 to 60 minutes.

SamanTree’s Histolog® Scanner essentially replaces histopathology and frozen section analysis, bringing cancer cells to the fingertips of clinicians. The Histolog® Scanner is a confocal microscopy device intended for rapid, high-resolution imaging of the surface of excised human tissue specimens to visualize morphological microstructures, allowing for real-time decision-making. Once a specimen is resected, it is dipped into a fluorescent dye for ten seconds, rinsed, dried, and placed on the scanner. Scanning specimens up to ~17 cm2 takes less than a minute. This technology has to potential to improve patient outcomes, reduce the need for reoperations, and improve staff efficiency and OR bookings. The scanner demonstrated clinical benefit in various use cases, including breast, prostate, and skin cancer. Emerging applications include brain, kidney, lung, GI, and ENT cancer. In July of 2024, SamanTree Medical announced the closing of $14M as part of a Series B funding round led by Relyens Innovation Santé. SamanTree pans to use the new funds to further develop and commercialize the Histolog® Scanner, expanding its reach in Europe and the United States.

Source: LSI USA ‘24

Source: LSI USA ‘24

Source: LSI Europe ‘23

Magenta Medical, founded in 2012, is a company specializing in the development of novel cardiovascular device solutions. The company is working to develop improved, less invasive temporary mechanical circulatory support (MCS) which currently done with intraaortic balloon pumps, Impellas, and ECHMOs. The company is currently pursuing several indications, starting with high-risk percutaneous coronary interventions (HR-PCIs).

During HR-PCIs, as well as in patients hospitalized with cardiogenic shock, the left ventricle may require temporary support in pumping oxygenated blood from the ventricle into the aorta to maintain adequate cardiac output, arterial blood pressure, and coronary and end-organ perfusion. Magenta Medical’s Elevate™ percutaneous Left Ventricle Assist Device (pLVAD) is a self-expanding percutaneous heart pump intended to provide temporary mechanical circulatory support for the left ventricle.

The self-expanding impeller is comprised of a thin, memory-shaped metallic frame and a soft, elastic material that forms the body of the blades. During the crimping process, the impeller is

elongated and its diameter is reduced, allowing for a 3.5x diameter expansion between the crimped profile during insertion into the patient’s blood vessel and the expanded operating profile when deployed in the left ventricle. The Elevate™ System has been successfully evaluated in a First-in-Human study and a U.S. Early Feasibility Study of HR-PCI patients.

In July of 2024, Magenta Medical closed a $105M financing round led by global healthcare investment firm, Novo Holdings. The financing will be used to advance the company’s U.S. clinical programs in several MCS indications and help secure the first FDA approval for the Elevate™ System in patients undergoing HR-PCIs.

Endoron Medical Raises $10M for AAA Stapler

Endoron Medical, founded in 2019, is dedicated to developing innovative solutions for the treatment of vascular diseases, with a heavy focus on minimally invasive solutions for abdominal aortic aneurysm (AAA) patients undergoing Endovascular Aneurysm Repair (EVAR).

A successful EVAR procedure depends strongly on the anatomy of the aorta, which often varies significantly from person to person. Short aortic necks or angulated aortas, which are present in 3040% of patients, result in poor apposition of the stent graft to the aortic wall. Poor apposition leads to graft migration and leakage, which increases intrasaccular pressure and risks rupture of the aneurysm.

Endoron’s Aortoseal is a long-lasting fixation and sealing device that securely holds the stent graft in place. It utilizes a smart stapling

mechanism that enables multiple staples to penetrate the stent graft and the aortic wall simultaneously, resulting in a suturing effect similar to that of manual open surgery.

In July, Endoron Medical announced that it closed a $10M Series A funding round to support its flagship catheter-based stapling solution. Sofinnova Partners led the round with matching contributions from the European Innovation Council Fund. Tel Aviv, Israel-based Endoron plans to use the funds to accelerate clinical validation of its Aortoseal endostapling solution.

MIMOSA Diagnostics is a medical technology company that focuses on developing non-invasive solutions for tissue assessment and wound care. Applications in skin health monitoring include diabetic foot, peripheral vascular disease, pressure injuries, burns, post-operative surgical management, pediatric intensive care, and in-field military operations.

Skin injuries happen every day in healthcare. Early detection and monitoring of skin injuries are essential to avoiding detrimental complications, such as amputation. Although visual inspection of the skin is the current standard of care, skin injuries aren’t visible to the naked eye.

MIMOSA Diagnostics seeks to set a new standard for assessing skin health by looking below the skin’s surface to measure skin vitals. The company’s US FDA 510(k)-cleared and Health Canada-approved product, the MIMOSA Pro, is a pocket-sized tissue image device that captures tissue oximetry, temperature, and a digital image in less than one second. The images are relayed to a HIPAA-compliant

web portal where clinicians can identify early opportunities for intervention, track patient progress, and collaborate with other clinicians to improve patient outcomes. The company is currently developing melanin algorithms to ensure every patient has access to accurate tissue health assessments.

In June, MIMOSA Diagnostics announced the successful closing of its latest round of financing led by Kern Venture Group, Kindling Investment Partners, Spring Impact Capital, Raspberry Investments Corporation, and Mimosa Partners, along with returning investors, Archerwill Investments and the XDL Group. The funds will help fuel MIMOSA’s commercial expansion and organizational growth.

Osteal Therapeutics, founded in 2013, is a privately held, clinical-stage pharmaceutical company developing a new category of drug/device combination therapies to treat orthopedic infections and their consequences. The company aims to develop targeted infection therapies to significantly reduce the mortality, morbidity, and cost of care associated with musculoskeletal infections.

Today, outcomes for musculoskeletal infection patients are often poor and unpredictable. More than 100,000 deep musculoskeletal infections occur every year in the United States. In major joints, the 16-week standard of care fails in 50% of patients at one year. Many infections of the musculoskeletal system are biofilm infections that develop on non-living surfaces, such as implants. Bacteria can effectively “hide” themselves under the complex matrices of biofilms, isolating themselves from the immune system and systemic antibiotics. Minimum inhibitory concentrations (MICs) of antibiotics are insufficient to treat these infections. Therapeutic agents, therefore, must exceed the minimum biofilm eradication concentration (MBEC) to eradicate biofilm infections effectively.

The current gold standard therapy, two-stage exchange arthroplasty, is a long, painful, and unreliable treatment approach. The standard of care is largely ineffective because it relies primarily on systemic antibiotics that reach MICs but not MBEC. Standard-ofcare antibiotics simply can’t achieve and maintain MBEC at the infection site while maintaining safe serum levels.

Osteal Therapeutics is developing a novel route of administration called cyclic local antibiotic irrigation. This approach allows

high concentrations of antibiotics to be delivered directly to the infected area. Cycling antibiotics in and out regularly provides fresh, high-concentration antibiotics while preventing systemic absorption and protecting the patient’s kidney and hearing. The company’s lead product, VT-X7, is a drug/device combination that utilizes high concentrations of vancomycin and tobramycin in conjunction with a drug delivery system to irrigate infected joint spaces as a result of periprosthetic joint infection in joint replacement patients. This therapy is completed in just seven days with 150+ cycles of local antibiotic therapy.

In June of 2024, Osteal Therapeutics announced the completion of an oversubscribed $50M Series D preferred stock equity financing. Zimmer Biomet led the round, joined by returning investors Johnson & Johnson Innovation – JJDC, Inc., Gideon Strategic Partners, and HM Capital. The funds will be used to advance the development of Osteal’s portfolio of therapies, including the submission of a new drug application for—and accelerated commercial launch of—VT-X7 for treating periprosthetic joint infection of the hip and knee.

Zeto Obtains FDA 510(k) Clearance for EEG Product, ONE

Zeto, founded in 2014, is a privately owned medical technology company dedicated to increasing accessibility to medical-grade EEG products that are quick, comfortable, and easy to use in both inpatient and outpatient settings.

EEG is the gold standard diagnostic tool for neurological conditions, such as seizures, epilepsy, sleep disorders, acute care monitoring, depression, TBI assessment, autism, and more. The big problem with EEG isn’t the technology; it’s the lack of availability in most healthcare facilities. This is because it’s a time-consuming process that requires a trained EEG technician to apply the wires and a neurologist to be on-site to read the EEG. It’s estimated that nearly 40,000 EEG technicians are needed in the United States alone today, but less than 3,000 remain in the profession.

Zeto’s goal is to create a complete EEG solution to address unmet needs and take “EEG from the room to anywhere.” Zeto’s EEG device, ONE, is a wearable, dry, wireless EEG headset. The device

is equipped with 21 comfortable, soft-tip electrodes positioned according to the 10-20 standard with EEG video and auxiliary inputs streaming live to the cloud. Zeto’s patented technology eliminates the need for a qualified EEG professional. The EEG can be viewed live on any computer or smart device, allowing for remote live reading and monitoring. ONE also features an AI-powered seizure detection tool that combines high sensitivity with low false alarm rates, offering near real-time notifications to medical staff of ongoing clinical seizures.

In June of 2024, Zeto announced that its innovative next-generation product, ONE, has received FDA 510(k) clearance.

restor3d Closes $55M Series A Funding Round

restor3d, founded in 2017, is an innovative medical device company and 3D printing manufacturer. The company’s mission is to expand the reach of personalized musculoskeletal surgery with additive manufacturing. The company

printing with

surgeons

combines its expertise in 3D

advanced biomaterials and AI to provide

with patient-specific implants that improve surgical precision and patient outcomes.

Off-the-shelf implants have been the standard of care in orthopedics for decades, but every patient’s anatomy is unique. Take the typical total knee joint replacement, for example. All knee implant patients must fit one of four options regardless of weight and height.

3D-printed orthopedic implants can help surgeons move away from this brute-force solution to a patient-centric solution. Advanced 3D-printing technologies open the door to not only improving the fit, simplifying the operation, and improving the range of motion but also allowing for better osseointegration. Traditional implants are made of solid metal, whereas 3D printing can allow for an intricate lattice structure to promote osseointegration and improve bone strength.

restor3d combines the benefits of 3D printing, AI, biomaterials, and biomechanics to craft a wide range of custom orthopedic solutions, including total and partial joint replacement and spinal surgery. The company’s in-house capabilities, paired with its AI-powered design of personalized implants, enable ease of scaling into other procedures.

In June of 2024, restor3d announced the successful closing of a $55M Series A funding round led by private investors, including Summers Value Partners and existing investors, plus an additional $15M in debt financing led by Trinity Capital. These funds will help grow the company’s product lines, in-house production, and AIbased automation capabilities.

Neuspera Medical Closes $23M Series D Funding Round

Neuspera Medical is an implantable neuromodulation medical device company dedicated to improving the lives of patients battling chronic illness. With an initial focus on Urinary Urgent Incontinence (UUI), a symptom of Overactive Bladder (OAB), the company’s mission is to empower patients to change their lives. They take a patient-first approach to deliver a modern, micro-invasive solution to patients looking to improve their bladder control.

30 to 40 million Americans suffer from varying degrees of overactive bladder, yet there has been very little innovation, and current solutions only penetrate 5% of the patient population. Current options on the market require a relatively large incision, a big bulk on the back, and an implant in the sacrum.

The Neuspera Implantable Sacral Neuromodulation (SNM) System is a micro-invasive, battery-free, wire-free solution. The microimplant is just 0.03 cc, making it the smallest in the SNM space. Neuspera’s patented Mid-Field Powering technology uses evanescent and propagating electromagnetic waves to power implanted medical devices to depths of 10 cm and beyond. Patients interact with the system for just two hours a day. They simply take the wireless transmitter, put it in the belt over the implant, and receive the stimulation while going about their normal daily lives. The implant cannot be felt or observed by the patient. Neuspera’s solution eliminates pocket creation and tunneling and minimizes the risk of reoperations and infections.

The 2021 feasibility study (stage I of pivotal) showed that 52% of subjects were 100% dry at the 12-month follow-up visit. At the end of 2023, Neuspera completed the last implant in its pivotal trial, putting it on track for PMA submission in Q3 of 2024.

In July 2024, Neuspera Medical announced the closing of its Series D funding round, which raised $23M and was led by Vertex Ventures HC and Treo Ventures,

with participation from several other investors. This round will support the company through the expected FDA PMA of the Neuspera System.

Affluent Medical Enters Agreements with Edwards Lifesciences

Affluent Medical, founded in 2011, is a structural heart and urological device company focusing on minimally invasive implants to restore essential physiological function in several key areas. The company strives to meet unmet patient needs and improve patient outcomes through advanced technological solutions.

About 160 million people worldwide suffer from mitral insufficiency, and only 4% of these patients are receiving treatment. 420 million people suffer from urinary incontinence, with 80% being women. Affluent currently has three products in clinical development, two in the structural heart space and one in the urology space.