MEET THE EXPERTS IN LONDON ON 24TH MARCH TO GET THE ANSWERS YOU NEED....

+ WHAT DOES THE LONDON PROPERTY MARKET HOLD FOR 2026?

+ EDUCATION: THE LANDLORD'S SUPERPOWER IN 2026

+ WHAT’S HAPPENING TO PRIVATE RENTS ACROSS THE UK? INSIDE THIS ISSUE

+ 2026 LETTINGS MARKET PREDICTIONS

+ STILL STANDING: THE RESILIENT BUY-TO-LET MARKET

+ MAKING TAX DIGITAL: ONLY A COUPLE OF WEEKS TO GO

Welcome to Issue 82 of Landlord Investor Magazine. As we step into 2026, it’s already shaping up to be a pivotal year for the Private Rented Sector, with two major changes set to impact landlords across the UK. From 6 April, the government’s Making Tax Digital requirements will begin to affect more landlords, marking another step towards the full digitalisation of tax reporting. As we’re all well aware, 1 May will see the beginning of the long-anticipated Renters’ Rights Act, introducing significant reforms that will reshape the way the rental market operates. With such substantial changes on the horizon, staying informed has never been more important. Thankfully, support and guidance are always close at hand. Here at Landlord Investor Magazine, we continue to bring together insight and expertise from across the property sector, while the National Landlord Investment Show provides landlords and property professionals with the opportunity to learn directly from industry specialists. Following the successful introduction of training sessions at our events last year, we’re expanding the programme even further in 2026 with a full calendar of eight live shows across the country. Our first event of the year takes place on 24 March at Old Billingsgate in London, bringing together leading exhibitors, expert speakers, and thousands of landlords, investors, and property professionals under one roof. From there, the tour continues across the UK throughout the year, with additional events planned in key locations nationwide. You can find the full 2026 schedule and register for your free show tickets at www.landlordinvestmentshow.co.uk/2026

Show Update | Tracey Hanbury

Education: The Landlord’s Superpower in 2026

What we predict for the lettings market in 2026. 06 10 15 18 16 24 28 30 34 36 42 38

RISE Conversations | Nicole Bonner

Introducing RISE Conversations with Women in Property.

Outlook | Kate Faulkner OBE

What’s Happening to Private Rents Across the UK?

Outlook | Kate Faulkner OBE

What does the London Property Market hold for landlords in 2026?

Outlook | LIS Media

What’s the Outlook for the UK Property Development Market in 2026?

Outlook | Allison Thompson

Investment | Joe Aston Why 2026 Could Be a Turning Point for Prime Property Investors.

Investment | LIS Media Securing Your First Buy-to-Let Mortgage.

Investment | Cat Westerling Still Standing: The Resilient Buy-to-Let Market.

Investment | Reece Mennie Housebuilding falls - but still no Spring Statement support for property sector.

Renters' Rights Act | Nicole Bonner Introducing RISE Conversations with Women in Property.

Taxation | HMRC

864,000 sole traders and landlords face new tax rules in LESS THAN A month.

Editor

Tracey Hanbury

Design

Marc Riley

Social Media

Charlotte Dye

Printing

IOP Marketing

PLEASE NOTE: The National Landlord Investment Show, LIS Media and Landlord Investor Magazine are content aggregators only. Views, statements and opinions expressed in articles, reviews and other materials herein are those of the authors, exhibitors and third-party contributors and not the editors and publishers of LI Magazine. Under no circumstances does the content of this publication constitute investment or legal advice. We do not undertake to advise individuals or organisations upon investment strategy. All investments should be approached with caution under professional guidance. While every care has been taken in the compilation of this publication and every attempt made to present up-to-date and accurate information, we cannot guarantee that inaccuracies will not occur. LIS Media Limited and our contributors will not be held responsible for any claim, loss, damage or inconvenience caused as a result of any information within these pages or any information accessed through the promoted links. Published by LIS Media, Registered address: Foresters Hall, 25-27 Westow Street, London SE19 3RY. © 2024 LIS Media Ltd.

Kate Faulkner OBE

Leading UK Property Analyst.

Nicole Bonner

Content, Community & PR Lead National Landlord Investment Show.

Cat Westerling

Executive Head of Lettings UK Hamptons

Staff Editorial Team

In-house Content by LIS Media

Tracey Hanbury

Co-Founder & Director, National Landlord Investment Show.

Allison Thompson

Chief Lettings Officer LRG

Joe Aston

Sales & Commercial Director Aria Finance

Reece Mennie CEO & Founder HJ Collection

TRACEY HANBURY CO-FOUNDER / DIRECTOR

Team: Donegal GAA

Song: Galway Girl, Steve Earle

Film: Dirty Dancing

Food: Indian

Likes: A busy show - can’t beat it

Dislikes: Rudeness

Fave thing about LIS: Building client relationships

KIERAN MCCORMACK SALES DIRECTOR

Team: Manchester United

Song: Bonkers, Dizze Rascal

Film: American Gangster

Food: Indian

Likes: Family time, Man Utd, golf

(not necessarily in that order)

Dislikes: Tinned sweetcorn

Fave thing about LIS: No day is the same (hence the song choice)

CHARLOTTE DYE OPERATIONS DIRECTOR

Team: Spurs

Song: The view from the afternoon, Arctic Monkeys

Film: E.T

Food: Chinese

Likes: Anything four legged and furry

Dislikes: Clowns and Spiders

Fave thing about LIS: Office cuddles with Ollie

NICOLE BONNER CONTENT, COMMUNITY & PR LEAD

Team: Crystal Palace

Song: Take It Easy by the Eagles

Film: The Devil Wears Prada

Food: Indian

Likes: Travel, photography & cooking

Dislikes: Tinned tuna & snakes

Fave thing about LIS: The innovative and fast-paced nature of the business.

ALICIA CELA HEAD OF ACCOUNTS

Team: Barcelona FC

Song: Hotel California, The Eagles

Film: Shawshank Redemption

Food: Anything Spanish (I'm very biased lol)

Likes: Cooking great food

Dislikes: Liars. Oh, and liver (can't stand it)

Fave thing about LIS: Socialising with the whole team

STEVE HANBURY CO-FOUNDER / DIRECTOR

Team: Crystal Palace

Song: Plastic Dreams, Jaydee (Original)

Film: Goodfellas

Food: Indian

Likes: Team meetings in the pub

Dislikes: Bad manners

Fave thing about LIS:

Show day (as anything can happen)

MARC RILEY CREATIVE DIRECTOR

Team: Letterkenny Shamrocks

Song: What’s going on? Marvin Gaye

Film: On The Waterfront

Food: Sea

Likes: Clean typography

Dislikes: Last minute edits

Fave thing about LIS: The website

JACOB HANBURY BUSINESS DEVELOPMENT MANAGER

Team: Crystal Palace

Song: Michael Bibi - Got the Fire

Film: Step Brothers

Food: Sunday roast

Likes: Skiing, Gym, Crystal Palace

Dislikes: Dirty finger nails

Fave thing about LIS: Great atmosphere at the shows

OLLIE HANBURY ENTERTAINMENT & SECURITY MANAGER

Team: Crystal Palace

Song: Who let the dogs out

Film: 101 Dalmatians

Food: Roast Dinners

Likes: Walkies

Dislikes: Poo in bags left on branches

Fave thing about LIS: Getting all the attention

KATE FAULKNER OBE LEADING UK PROPERTY ANALYST

TRACEY HANBURY CO-FOUNDER & DIRECTOR

NATIONAL LANDLORD INVESTMENT SHOW

2026 is the ultimate year of change for UK landlords, property investors and developers. The Renters’ Rights Act, Making Tax Digital, and EPC Changes, to name a few, are transforming compliance within the private rented sector. Couple this with an ongoing UK housing crisis and ambitious new, affordable housing targets from the UK Labour government, and there’s never a dull day when you work in the property sector.

Now more than ever, UK landlords, investors and developers need the right education and expert guidance. Knowledge is the superpower that will help you continue providing high-quality homes while operating professionally. At the National Landlord Investment Show, we’re here to support you every step of the way.

The Renters’ Rights Act is changing how landlords operate within the sector, and there is now some certainty about what is changing, when and how it is being implemented, with some stages more imminent than others. Whilst many in the industry have been focused on the negative aspects of the change, I strongly believe that the implementation of the Act will set out what it intends to achieve in levelling up and professionalising the sector, and ultimately providing good-quality housing for tenants. Whilst changes will need to happen and we need to operate within a new normal, in the long term, the Act will bring about positive changes to the sector.

The media and property professionals alike have focused on the potential unintended negative consequences of the introduction of the Renters’ Rights Act, in creating, as some might say, a ‘mass exodus of landlords’ from the sector. And whilst this may ring true for some landlords, as a recent article headline, ‘London landlord begins evictions ahead of new renters’ rights law’ (Financial Times), quite rightly highlights, I’m here to tell you why and how the professional landlords and investors who want to stay in the sector and provide housing can navigate the biggest change in over 30 years by connecting with the experts and always developing through the right education.

Let’s turn to Frank Callaghan (UK Student Landlord) as a prime example of how, through the expert-led education and guidance at the October 2025 National Landlord Investment Show, he changed his mind about leaving the sector. He left the show feeling ‘confident and reassured he could navigate the changes ahead’. He, with everyone in the training audience, felt the same, and when asked by the trainer Susie Crolla, ‘Who is still thinking about selling up after my training?’, only one person out of 300 put up their hand.

It was through our show that everyone in the audience of Susie’s training segment felt confident they could help provide good-quality homes and comply with the Renters’ Rights Act. Our mission this year is to ensure every member of our community of landlords, property investors and developers feels just like Frank, so let’s turn to how we can support you in navigating the changes ahead in 2026.

How can we support you?

Face-to-face at our 2026 National Landlord Investment shows

Our shows across the UK are the heartbeat of everything we do, and the buzz of an exhibition floor or a lively panel discussion is unbeatable for us. If you’ve attended our shows before, you’ll understand the positive atmosphere through watching live panel discussions, in-depth expertled seminars, connecting with other landlords like you, and speaking with the expert exhibitors to find efficient solutions for running your property portfolio. Not only will we always support you through this, but at our upcoming London show on 24th March, we will be featuring expertled free Renters’ Rights Act training segments, helping you to prepare now and avoid costly mistakes later.

We’re also pleased to make Landlord Advice Clinics, ‘Property, Politics and Economics' seminars, Property Developer Live and New Investor Masterclasses core to our 2026 shows. So if you’re an existing landlord just looking for support to maintain your portfolio, looking to diversify or expand, or someone completely new to property, our national and regional shows are the property events you need to attend this year. Find out the locations and dates of all the shows here, and most importantly, get your free tickets

Digitally through our LIS Community Hub

You may already attend our shows, but our online digital LIS Community Hub helps UK landlords, investors, and developers stay connected to expert guidance and resources 365 days a year, 7 days a week, and 24 hours a day. Whether you're managing an established portfolio or just starting, we provide the expert insights,

events, property news, training, tools, resources, and expertise you need to succeed on your property investment journey. Helping you thrive in a community-led environment. Join our free community today or sign in here

By bringing you the latest UK Property News

Anyone who provides housing or, in fact, works in the UK property sector knows just how quickly the news changes, and if you’re not careful, you can very quickly fall behind in understanding the changes. Stay on top of the latest UK Property News, plus hear how the experts break down what it means for you, your property portfolio and your tenants, including breaking down the expert property market data over time and by location.

You can read the latest UK Property News on our news portal Property Notify, watch the experts break down property news on our UK Property News channel, plus access expert knowledge written and produced specifically for landlords in this dedicated publicationthe Landlord Investor Magazine.

2026 is a year of change, but we’re here to help you and make sure you feel confident to navigate the changes ahead, so you can continue being professional providers of housing that the UK so desperately needs right now. Through our live shows in person, our digital LIS Community Hub and our channels for understanding and digesting the latest UK property news, our all-around platform will help you stay informed and ahead on your property investment journey. Education at the National Landlord Investment Show will be your superpower as a landlord, property investor and developer in 2026 and beyond.

2026 is a year of change, but we’re here to help you and make sure you feel confident to navigate the changes ahead.

the 31st May 2026

You must give this Information Sheet if the tenancy:

• is an assured or assured shorthold tenancy

• was created before 1 May 2026

• has a wholly or partly written record of terms (including a written tenancy agreement)

If you are a landlord and have a letting agent who manages the property on your behalf, then the agent must provide the Information Sheet to the tenant, even if you have also provided it.

Download the information sheet from the Gov. uk website here with a QR code: www.gov.uk/ government/publications/the-renters-rights-actinformation-sheet-2026

You must give this Information Sheet by 31 May 2026, or you could be fined up to £7,000.

Unlock your access to exclusive content from the cream of the UK property sector with the National Landlord Investment Show’s FREE Community Hub. Access expert knowledge, curated investor insights, and practical strategies designed to manage and grow your property portfolio. No fees. No fuss. Just smarter landlording.

Expert Reports by Kate

Faulkner OBE

Stay ahead of the curve with analysis on key trends and challenges in the Private Rented Sector and wider property market.

Renters’ Rights Education Hub

Navigate the biggest reforms in 30 years with the latest updates, guidance, and expert tips from our network of experts.

Live Webinar Recordings

Access exclusive recent webinars by leading voices in the property sector on topics such as the Autumn 2025 Budget and Renters' Rights Act changes.

Join now to unlock your advantage today.

NICOLE BONNER

To celebrate International Women’s Day 2026, our Co-Founder and Director, Tracey Hanbury, had the pleasure of speaking with the incredible women we work alongside at the National Landlord Investment Show. These conversations were an opportunity to highlight their voices, share their journeys, and celebrate the growing impact of women across the property industry.

From female landlords & investors, financial and legal advisors, and expert property data analysts, the women featured are transforming the property landscape as we know it today in very different ways. In each conversation, we had the chance to showcase each woman’s journey in property, successes, challenges, motivations, as well as their advice to other women rising within the UK property sector. Through conversations, we’ve created a new content series called RISE: Women in property, celebrating the stories and impact of the incredible women shaping the sector today, whilst inspiring the next generation of women to RISE in property and giving back in line with the IWD theme, ‘Give to gain’.

From restriction to representation

If we look back at the history of women in property, for the majority of history up until recent times, the right to own property was very restrictive for women due to legal and societal barriers. It wasn’t until 1975 when the Sex Discrimination Act in the UK was passed that a woman could open a bank account in the UK and thereby apply for a mortgage to own a property without the need for a male guarantor. Just over 150 years ago, women were not allowed to even own property. Severe restrictions on property ownership were one thing, so it was inevitable that female representation across the UK property industry didn’t get off to a balanced start. Fast forward to 2026, the recent English Private Landlord Survey (2024) showed “50% of females are landlords” (Gov. UK ), and “52% of females comprise all roles in real estate” ( We Are Unchained, 2025).

Whilst there's still progress to be made regarding gender equality and equal footing within the sector, particularly when it comes to senior board management, there’s much to celebrate when it comes to women’s representation, but more so, the impact women make within the sector. The conversations from the RISE Women in Property series help us unpack this impact through personal stories of success, and we explore this below:

Different journeys but same passion

Every conversation revealed that each woman had a very different start to her journey in property. For some, like Alvarine Coulton (UK landlord) and Carly Jermyn (CEO from Woodstock Legal Services), family connections sparked their interest and inspired them to follow in familiar footsteps. Others accidentally stumbled upon the sector by chance and quickly discovered a passion for it. Lucy Waters (Managing Director and Founder of Aria Finance) stated, “I was very fortunate to fall into a role which opened my eyes to the sector and gave me the bug for it, and I quickly fell in love with the diversity and challenges of the sector”.

Anna Hughes (Director and Head of Landlord & Tenant at Woodstock Legal Services), for example, trained in law before gravitating toward landlord and tenant law, where she developed a genuine enthusiasm for property as a ‘niche, complex area of law’. Scarlett Douglas (TV Property Expert & Presenter) made a dramatic career shift from performing in musical theatre on the West End to property investment, eventually co-presenting

a property television show alongside her brother. Allison Thompson MARLA began her career as an administrator at the very letting agency she now leads as National Lettings Managing Director of LRG, illustrating her growth as the company grew and evolved. Meanwhile, Kate Faulkner OBE shared that although she didn’t come from a property background, her longstanding love of property led her to transform an MBE project from a property portal into a business, which was her gateway into the sector.

Despite their different paths, each woman brought her own perspective, skills, and energy to the property. Whether inspired by family, chance, or a personal calling, their stories show the diversity of routes into the industry and also roles within the sector that are open to women today.

When speaking of the barriers faced, again, the varied conversations brought up a range of challenges, but also the conversations revealed how all women approached the challenges with optimism and resilience. Scarlette spoke of the role of intersectionality of barriers, stating, “Being a woman in a predominantly male-dominated industry is very difficult; being a black woman is also very difficult”. Adding to this was the fact that she looked young; she felt that at times, people didn’t take her seriously as a property expert. Lucy Waters felt that in a male-dominated room, she always felt that she had to work that little bit harder to prove her credibility, stating, “it wasn’t just because I was female, I was also young, it was unusual to have people in senior roles when I first started out”.

Kate Faulkner OBE touched upon the importance of building connections and opening doors when overcoming the challenge of feeling like an outsider and thanked another female, Anne Maurice, the House Doctor, for opening that door for her and trusting her to help her write a book, which then led to her writing for Which? Trusted Traders. The theme of letting go also came up for Alvarine, and she faced a challenge of handing out responsibilities while balancing work commitments and managing a portfolio from afar. Both Anna and Carly talked about barriers in a positive sense and building up a resilience attitude to face barriers, and used that as a superpower in the sense that when coming up against challenges, as Carly summarised, “resilience allows you to look for new innovative ways to tackle challenges”. Allison’s experience of leading two teams through a merger also showed how she turned a challenge into a very proud achievement as she used her collaboration skills to navigate a challenging time.

Why should women enter the UK property sector?

All the conversations around why women should enter the property sector, either as a landlord or within the property service provider business, were strongly advocated for and supported. The theme around flexibility came out as a core reason why, and even the foundations of Woodstock Legal Services were founded on the need for flexibility, allowing women to have flexibility that a 9-5 job at times can’t accommodate. Most of the women advocated that the property sector give women greater flexibility when it comes to raising a family or carrying out other care commitments with parents and grandparents.

Even in the case of Woodstock, the flexibility element was important for men who also joined the firm as consultants, allowing their female partners to follow their career ambitions. The positive opportunities and work culture within the property sector for women were also talked about, as Allison Thompson MARLA demonstrated how LRG have been

“We need to be proud of the fact that we put roofs over people’s heads”.

Alvarine Coulton, in her role as a landlord of both private and social housing, also shows how being a landlord, you can “provide homes and do good”.

Kate Faulkner OBE

supporting and helping women rise through the ‘Empower Her programme’. Kate Faulkner OBE also talked about the diverse range of roles available to women at a higher pay range, open to many skills and talent from accounting, to writing, media and filming, which many people may not think about when they think about jobs across the UK property sector.

The theme of doing good and providing a good quality service was also mentioned as a key reason why women should enter the sector, as Kate Faulkner OBE, finely put it, “We need to be proud of the fact that we put roofs over people’s heads”. Alvarine Coulton, in her role as a landlord of both private and social housing, also shows how being a landlord, you can “provide homes and do good”.

The RISE Women in Property series allowed us to showcase the voices of incredible women working across the UK property sector in a diverse range

of roles, making a positive impact. You can watch the full content series on our Landlord Investor TV channel. We want to share a big thank you to the incredible women we spoke with that is Carly Jermyn (CEO of Woodstock Legal Services, Alvarine Coulton (UK Landlord), Anna Hughes (Director and Head of Landlord & Tenant at Woodstock Legal Services, Lucy Waters (Managing Director and Founder of Aria Finance), Scarlette Douglas (Property expert & Presenter), Allison Thompson (National Lettings Managing Director from LRG) and Kate Faulkner OBE (UK Property Analyst). Here at the National Landlord Investment Show, we’re committed to keeping the conversation going well beyond International Women’s Day. We look forward to continuing to showcase the valuable stories of the women we work with, while also seeking to highlight more female landlords and property investors who are making an impact through their professionalism, expertise, and contributions to the sector.

If you’re a woman in property and would like to share your story, we would love to hear from you!

I would like to give a special honourable mention to the incredible host of the series, Tracey Hanbury, who is our Co-Founder and Director and a personal inspiration of mine. Despite her not being interviewed, I want to give her a special mention this International Women's Day for making an outstanding contribution to the UK property sector and always leading through innovation, resilience and compassion. Tracey, through her work, role and values, has consistently demonstrated the importance of collaboration and bringing everyone together to deliver practical solutions within the private rented sector. The upcoming show in London on 24th March is a testament to this, as the first panel discussion talking about the biggest landlord challenges in 2026 is led by a true powerhouse of women. Tracey, thank you for your immense contribution and for continuing to make a true difference to the sector. It’s not going unnoticed, and I can't wait to interview you next in the series!

At Woodstock Legal Services, our award-winning Landlord & Tenant team helps landlords and investors across England and Wales stay protected, compliant and commercially strong.

We combine technical excellence with real-world property experience to deliver advice that works in practice — not just on paper. Exceptional service, tailored to you.

Need advice? Email hello@woodstocklegalservices.co.uk to speak with a member of our team.

Talk with an expert today:

Managing Director & Solicitor

Anna Hughes

Jermyn Director & Head of Landlord & Tenant

KATE FAULKNER OBE LEADING UK PROPERTY ANALYST

As the charts from the Office for National Statistics (ONS) show, before governments began interfering in the private rented sector (PRS) with increasingly harsh rental conditions for landlords, rents typically rose by around 2% per year, compared with general inflation running at closer to 3%.

However, once we were over the pandemic and the interventions had bedded in, the fact that they had curbed the growth of the PRS across Scotland, Wales and England, while the existing population, and particularly migration, had increased, meant we have seen much higher annual rental rises. This upward pressure on rents is likely to continue over the next few years.

One comparison rarely made, which in my view should be, is that rental inflation in the PRS is often on a par or indeed lower than increases in the social housing sector. This is because social rents have traditionally risen by general inflation each year, plus an additional 0.5% to 1% annually, whereas PRS rents tend to move in line with wages, which historically haven’t kept up with inflation, especially in London.

Latest data from the government’s own English Housing Survey (2024-25) shows that year on year, PRS rents have risen less than social rents:

Increases (2023–24 to 2024–25)

Private Rented Sector

Sector

Private Rented Sector

Social

Although private rents rose by slightly more in cash terms (£13 vs £11), social rents increased faster in percentage terms (9.3% vs 5.5%).

Over time, however, looking at a five-year change (2019–20 to 2024–25), the increase is pretty similar:

Looking at data over a 5-year period

Over the past five years

Sector

Private Rented Sector

Social Rented Sector

This, for me, is conclusive evidence that the reality is that the PRS sector actually naturally achieves fair rent increases. This is due to the fact that PRS rents aren’t rentcontrolled and typically rise in line with wages, not general inflation.

And, if governments hadn’t intervened in the PRS in the way they have, it’s likely that this upward pressure on private rents wouldn’t have happened, and tenants could have been paying less for their rents than they are now.

Another trend which has emerged in recent years is that rents are now rising faster than property prices. Another shift has emerged in recent years: rents are now rising faster than house prices, whereas historically, property values outpaced rents. This is partly due to the environment of the sector post-pandemic, as wages rose and the balance between demand and available rental stock changed dramatically. This is a significant change in market dynamics, and current forecasts suggest this trend is set to continue.

As with property prices, rental performance varies considerably depending on what you measure and where. Whether you look at year-on-year rental changes by country, region or even individual London boroughs, the variation in average rental growth is substantial. The latest private rent and house prices from ONS are a good way to review the variation.

Will the Renters’ Rights Act result in higher rents for tenants in England?

Much of the fear of the Renter’s Rights Act will be around rising rents. If we look at Wales, Northern Ireland and Scotland, which have all introduced stricter PRS regulations than England, it does show that these regions have seen higher rental inflation as a result. With the Renters’ Rights Act due to come into force in England in May 2026, it is possible that rental inflation in England could begin to rise faster, even though some of the new policies will restrict limits on landlords accepting rental bids when advertising and the rule that only one rental increase can be implemented each year.

The latest ONS data shows that Scotland is currently experiencing the lowest year-on-year rental growth. However, in the past – primarily following the introduction of rent controls – Scotland saw some of the highest increases, with rents rising by as much as 11.7% in August 2023. England, by contrast, has recently recorded the lowest rental growth.

What rental data do you find the most useful as an existing or new landlord? How can we help you better analyse the performance of your properties versus the wider market?

Join the UK’s fastest-growing community of UK landlords, investors and developers for the latest property data analysis for free today. Join or sign up here.

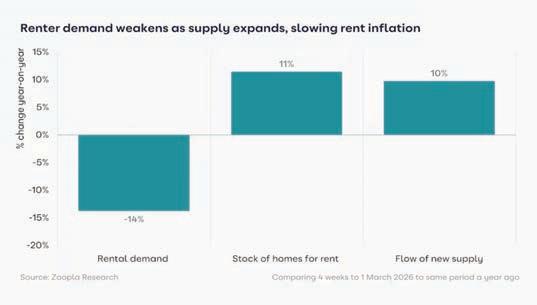

According to the latest Zoopla UK Rental Market Report (March 2026), the UK rental market is beginning to rebalance. Demand for rental homes is now 14% lower year-on-year and at a six-year low, helping slow rental growth to around 1.9% annually. However, rents are still rising faster in more affordable markets in the north of England, where cities such as Liverpool, Newcastle and Glasgow are still recording a stronger increase of 3% to 4.6%’.

Demand for rented homes is falling

Two key factors identified for a fall in demand over the last few years are:-

1. A decline in net migration, which according to ONS estimates shows a 78% decline in net migration over two years and this drop in migration is having a direct impact on the level of rental demand across the country, which is the main tenure those moving to the UK would enter.

2. Improved affordability over the last few years for firsttime buyers to buy, with “a 20% increase in the number of first-time buyer mortgages in the 9 months to September 2025” (UK Finance).

Rent is becoming more affordable

The report also shows that despite ongoing criticism of the private rented sector in terms of high rents, the latest data suggests rental growth is now moderating as earnings are rising 2x faster. The reports show “rent growth has slowed to 1.9%, down from 2.8% last year” whilst affordability is still worse in London. The “annual rent for a typical residential property outside London is 33.5% of gross annual earnings for a single person”, which is expected to continue in 2026.

Competition pressures are easing for rented homes

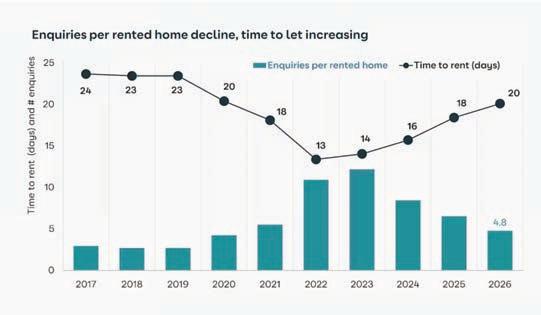

Zoopla data shows that there are “11% more homes for rent than a year ago” and the number of enquiries per property has fallen to “4.8, down from 6.5 per year”. Whilst this is positive news in that supply and demand are starting to rebalance, ‘rental supply still remains 23% below pre-pandemic levels’. This means “Scarcity remains, which will see rents continuing to rise over 2026.”

Source: Zoopla UK Rental Market Report- March 2026

Finally, for landlords looking to let this year, as there's been a reduction in competition, it means that it takes longer to rent as renters can look at a larger pool of rental properties on the market, with the “average time to find a tenant is now 20 days, compared to 13 days back in 2022 when competition was high”.

As Richard Donnell, Executive Director of Zoopla, quotes, the outlook is summarised as “ The rental market is moving back towards balance as supply improves and demand eases. Renters can expect more choice of homes and slower rent increases than in recent years”.

KATE FAULKNER OBE LEADING UK PROPERTY ANALYST

Ahead of the upcoming National Landlord Investment Show on 24th March in London, Old Billingsgate, it’s only right we take a look at the London Property Market in 2026 through the lens of a UK landlord and property investor. Beyond this article, you can also come to the show to attend my ‘Property, Politics and Economics’ seminar, and it will be here that I can go into the details and where you can ask me the questions you want answered.

Whilst headlines often focus on the “London average” property price being around £550k and skyrocketing rents, averaging £2,253, the narrative is often centred on how anyone could afford to live and buy in London. Yet, the reality for landlords is far more nuanced.

So how has the London market really performed, and what can landlords expect between 2026 and 2030?

During 2025, property prices in London fell by around 1% for houses and 3.6% for flats. With inflation running at approximately 3%, this represents a more significant realterm decline. However, performance varies dramatically depending on when landlords entered the market and, most importantly, which borough they invested in, as when and where property investment happens is important. We need to look at the full overview.

There is not ‘one’ London property market; there are 32 boroughs.

When we drill down into the property data, reporting on “London average property price ” is misleading. Looking at the 2025 data, the highest growth in property house price was +6.8% from 2024; in comparison, the biggest fall was recorded in Camden at 11.1% and Kensington and Chelsea at -11.5%.

Average year-on-year growth isn’t enough to get a full picture of property data performance

Another key factor which is important to consider is that year-on-year average property data isn’t enough; what’s more important is to go back over time, back to 2005 and then look to see whether a market is performing more or less than average.

Since 2005, property price growth across London has varied significantly by borough. Areas with a prime location, such as Camden, have seen the strongest average annual increase since 2005 at 6.58%, followed by Richmond upon Thames (6.35%), Barnet (5.92%), and Southwark (5.79%). In contrast, several boroughs have experienced far more subdued price increases over the same period. Croydon has recorded the lowest average annual growth at 0.77%, followed by Hackney (1.26%), Hillingdon (2.81%), and Merton (2.94%).

Overall, there are some fascinating long-term trends landlords need to understand. Flat prices in parts of the Capital are at similar levels to eight years ago, while prime values in some areas remain close to where they were in 2014. Without looking at boroughlevel data and comparing it to your own property’s performance, it’s impossible to know whether your investment is outperforming or underperforming.

For new and existing landlords alike, understanding the details behind the data may be the difference between reacting to headlines versus making confident long-term investment decisions. I’ll be delivering my ‘Property, Politics and Economics’ seminar at the upcoming National Landlord Investment Show and all shows in 2026 to help you break down and understand the property data in practical terms, so get your free tickets today across the UK to attend!

Since 2005, property price growth across London has varied significantly by borough. Areas with a prime location, such as Camden, have seen the strongest average annual increase since 2005 at 6.58%.

What are the challenges and opportunities for developers bridging the gap between supply and demand across the UK’s housing market?

As we enter 2026, the gap between the demand and supply of new housing across the UK is widening at a rapid pace. While the need for newbuild projects has never been clearer, developers are caught between a rock and a hard place.

Rising costs and evolving regulations are creating an environment where government-backed hurdles and bureaucratic "red tape" are increasingly making governmentled housing targets appear more aspirational than achievable.

In this feature, we will look at what’s in store for UK property developers in 2026 and explore how many new properties are actually needed to meet demand.

Before we dive into the stats, sign up for your free ticket to the National Landlord Investment Show in London on 24th March to gain expert insights through the Property Developer Live masterclasses. This segment is designed for experienced landlords transitioning or diversifying through property development to small- to medium-scale developers looking to expand their existing portfolios. Book your free ticket today

How Many New Homes are Needed?

According to the Centre for Cities, the UK is currently grappling with a housing deficit estimated at 4.3 million homes.

To address this backlog within the next 25 years, England alone would need to build 442,000 homes per year. To clear it within a decade, that figure rises to a staggering 654,000 per year.

When compared to a current track record of around 200,000 new homes per year, the scale of the challenge (and the potential opportunity) is unprecedented.

The government’s ambitions pledge to deliver 1.5 million new homes by 2029 is at the heart of their strategy to address the UK’s housing crisis; however, the latest estimates from the Office for Budget Responsibility (OBR) suggest the target is already out of reach.

When faced with the reality on the ground, the numbers are sobering, particularly in the capital. In London, where the housing crisis is most apparent, only 4,170 new homes were started recently, marking a 72% drop compared to 2023/24.

While London has historically built over 10,000 homes annually since 1946, consultancy Molior predicts that low housing starts will result in only 4,550 completions in both 2027 and 2028. The capital is currently facing its most significant housebuilding hurdles since the Second World War.

Nationally, the picture is similarly strained. Across England, just 115,700 homes were started in the government’s first year, only 39% of the 300,000 annual starts required to hit the 2029 target.

This slowdown is reflected in a notable dip in raw material production; cement production decreased by 5.3% to 7.3 million tonnes in 2024, while deliveries of bricks and blocks fell by 6.1% and 11.5%, respectively, in late 2025, according to government data

Echoing this sentiment, the Mineral Products Association (MPA) has highlighted a significant downturn in the sector, reporting that ready-mixed concrete volumes fell by 11.5% to 2.7 million cubic metres in Q2 2025. This marks a historical low with the MPA noting that " the last time Britain’s annual concrete volume was this low was 1963.”

While

London has historically built over 10,000 homes annually since 1946, consultancy Molior predicts that low housing starts will result in only 4,550 completions in both 2027 and 2028. The capital is currently facing its most significant housebuilding hurdles since the Second World War.

Despite the systemic challenges, 2026 is emerging as the year of the reset. Several indicators suggest the decline in housebuilding volumes may have finally reached its floor.

For the UK to have any chance of seeing more housing stock added to the market, small- and medium-sized (SME) developers are essential for regional growth, yet they have been disproportionately squeezed.

Data from the Home Builders Federation (HBF) reveals that in 2024, only 17,000 homes were approved on small sites, far below the historic average of 35,000. Planning permissions for sites of 150 units or fewer have plummeted from 20% of total permissions in 2008 to just 6% to 8% today.

Smaller developers are uniquely positioned to unlock development opportunities across the UK, exploring locations and pockets of land or redevelopment opportunities that larger housebuilders overlook.

Despite their vital role in delivering local housing, SME developers face mounting pressures from rising costs, evolving regulations, and systemic planning hurdles. These external factors are stifling development and significantly reducing the supply of new-build housing entering the market.

The demand for quality housing is not just a dream for homeowners; it is a requirement for the rental sector. In 2024, 35.2% of the UK population opted for rented accommodation (Statista), with the English Housing Survey noting that 19.5% of all households are private renters.

With the ONS projecting a population increase of 4.9 million (7.3%) by mid-

2032, the supply-demand gap is set to widen further. Savills reports that the UK requires 1 million new private rental properties by 2031 to meet this rising need. Currently, the pressure is immense: Zoopla reports an average of 12 renters vying for every single available property.

This scarcity has seen private renters face the steepest increase in living costs, with a 24% surge in new rental prices over the last three years.

When looking at new housing supply, there must be a balance of affordable homes for buyers alongside the delivery of high-quality rental housing. The role of Build to Rent developments is more important than ever to address the rising cost of renting.

2026: Signs of a Measured Recovery

Despite the systemic challenges, 2026 is emerging as the year of the reset. Several indicators suggest the decline in housebuilding volumes may have finally reached its floor.

EPC data shows that over 200,000 new homes were built in the 12 months to September 2025. This has remained steady for three consecutive quarters, suggesting the two-year decline is bottoming out.

The NHBC reported 30,643 new home registrations in Q3 2025, an 8% increase year-on-year. This marked the third consecutive quarterly uplift.

According to the Savills Development Land Index, the price of land, labour, and materials has remained subdued compared to the 2022-23 peak, offering a small window for developers to improve margins.

As we look to the future, the Construction Products Association (CPA) projects total construction output to rise by 2.8% in 2026; however, infrastructure projects make up the lion’s share of this growth, with only a 4.0% rise in private housing construction expected.

While there is no denying that the demand for residential property is high, developers will likely move forward with cautious optimism. While the big builders will continue to struggle with the sheer scale of national targets against a backdrop of industry challenges, the opportunity for agile, quality-focused developers has never been greater.

The planning decline is slowing, and while the material price index for all work increased by 3.0% in late 2025, the overall volatility of the previous years is showing signs of stabilising. Interest rates are beginning to normalise, and with wage growth improving affordability, first-time buyers and professional investors are returning to the market.

The UK housing shortage remains a defining challenge in 2026; however, help is available. Sign up today for Property Developer Live Masterclassesat the London National Landlord Show in London on 24th March to gain expert insights on Securing specialised Development Finance, Tax Planning with Development Projects, navigating complex planning & legal challenges, acquiring Land and Site opportunities and Sourcing Professional Project Management and QS services: Book your free ticket today. LIS Media

Turn unused land or building space into reliable income with Wildstone.

Wildstone partners with corporate landlords, property agents and asset owners to unlock new revenue from outdoor advertising opportunities.

Wildstone funds, owns and manages the high-quality digital advertising assets, allowing landlords to benefit from long-term income without any capital investment.

Our partnership approach includes:

We review your existing portfolio to identify suitable roadside locations and provide a free valuation.

Landlords receive either secure, ongoing rental income or a single upfront capital payment in exchange for the advertising site.

Our in-house planning, construction and legal specialists oversees planning applications, installation and ongoing maintenance, ensuring a streamlined process from assessment to operation

Partnering with Wildstone supports improved portfolio performance and additional income from underused property assets across diverse locations.

ALLISON THOMPSON CHIEF LETTINGS OFFICER LRG

After several years of imbalance, the lettings market began to stabilise in 2025. While the gap between supply and demand narrowed significantly, it remained well above pre-pandemic levels. This ongoing shortage of rental stock, combined with real-terms wage growth still slightly outpacing inflation, meant rents continued to rise.

Latest figures from the Office for National Statistics show that in the year to October 2025, annual rent growth saw rents up 5% in England, 6.7% in Wales, and 3.4% in Scotland, while Northern Ireland recorded a 6.6% increase in the year to August.

Yields held up well too. Rightmove data shows that by mid-2025, the average UK gross yield was 6.3%, ranging from 5.7% in London to 8.1% in the North East. All English regions recorded a modest annual increase, underlining the continued appeal of buy-to-let for income-focused investors.

Rental pricing is shaped by competition, but affordability continues to be the decisive constraint. While an undersupply of rental homes persists across much of the UK, slowing wage growth is likely to put a ceiling on further rent rises.

In real terms, earnings only just kept pace with inflation in 2025. Annual pay growth is expected to drop below 3% in 2026 and ease to around 2.5% in 2027. This softer income outlook will limit how far landlords can increase rents, particularly given the heightened risk of arrears if affordability is pushed too far.

Tenant demand has also cooled. Compared with a year ago, demand is around 20% lower and, outside London, is at its weakest level in six years. This reflects two main factors: a sharp slowdown in net migration, down 78% in the two years to June 2025, and

improving mortgage affordability for first-time buyers. In the nine months to September 2025 alone, first-time buyer mortgage volumes increased by 20%.

As more renters transition into home ownership, additional rental stock has come back onto the market, helping to ease the long-standing imbalance between supply and demand.

Against this backdrop, Zoopla expects annual rent growth to slow to around 2.5%.

The Renters’ Rights Act is expected to be the defining influence on the English lettings market in 2026. From 1 May, the new assured tenancy will be introduced, bringing an end to fixed terms, abolishing Section 21, and tightening the rules around possession, rent in advance and pets.

Landlords will also be capped at a single annual rent increase, only where it reflects local market conditions, and there will be bans on rental bidding above the advertised price.

A potential unintended consequence is that landlords may advertise rents higher initially so that this overcomes the bidding war situation and they can then negotiate lower offer. This could have the opposite effect of driving advertised rents up.

Ultimately, 2026 will be a year of implementation. The landlords who perform best will be those that prepare early, seek the right advice, and take a proactive approach to navigating the Renters’ Rights Act.

The Renters’ Rights Act is expected to be the defining influence on the English lettings market in 2026. From 1 May, the new assured tenancy will be introduced, bringing an end to fixed terms, abolishing Section 21, and tightening the rules around possession, rent in advance and pets.

After more than a decade of correction, London’s prime property market may finally be nearing an inflection point. Values in Prime Central London remain around 24.5% below their 2014 peak, one of the deepest downturns in recent history. Forecasts suggest a modest fall of around 2% in 2026, with flat performance in 2027. Yet this weakness may in fact mark the formation of a new base for recovery through the rest of the decade.

Research from Savills indicates that prime regional markets outside London are expected to deliver steady capital growth over the next five years. In London itself, the investment story is increasingly being driven by income rather than short-term price appreciation.

For much of the past decade, prime property has offered limited capital upside. Transaction volumes slowed, stock levels rose and sellers often discounted. Investors focused purely on price growth had little incentive to enter the market.

The rental market, however, tells a different story.

By mid-2025, rental agreements for properties commanding at least £1,000 per week had risen sharply year-onyear, generating £82.8 million across 1,588 high-value tenancies. While overall volumes were marginally down on 2024, the super-prime segment remained resilient.

Several structural factors are driving demand. Stamp Duty changes and the abolition of non-domicile tax status have prompted some high-net-worth individuals to sell UK homes and relocate overseas, while renting when in the UK. This has intensified demand for quality rental property in prime locations.

For investors, the result is a rare alignment: compressed capital values alongside strengthened yields. Assets that once appeared fully priced are now delivering attractive income returns at what may prove to be cyclical lows.

Broader economic trends are also supportive. Interest rates have fallen, improving borrowing costs and leveraged returns. Inflation is expected to stabilise, bringing greater certainty to financial planning.

Meanwhile, structural undersupply in the UK housing market remains unresolved. Ambitious housebuilding targets face delivery constraints, suggesting shortages, and rental growth, are likely to persist.

International demand adds further support. Sterling’s relative weakness against several major currencies has made UK property more attractive to overseas buyers, effectively creating a currency discount on already-adjusted prices.

Sentiment is also improving. Landlord confidence in 2026 has strengthened compared with 2025. Professional investors are increasingly viewing current pricing as the foundation for the next growth cycle rather than a market to avoid.

The opportunity lies in timing. Purchasing at compressed valuations, securing finance at lower rates and generating immediate income from stronger yields offers a compelling combination.

Prime residential yields of around 5%, common for one- and twobedroom flats in outer prime London, can translate into returns of roughly 8–10% when financed at 70% loan-to-

value under current conditions. Prime commercial assets with strong tenant covenants may offer higher income returns.

Importantly, investors are not reliant on rapid capital growth. Income provides resilience, even if recovery is gradual. However, if values strengthen from 2027 onwards as forecast, early entrants could benefit from both yield and capital uplift.

For long-term investors, 2026 may represent a rare window, securing highquality prime assets at cyclical lows, supported by robust rental demand and improving fundamentals, before confidence and competition return.

The opportunity lies in timing. Purchasing at compressed valuations, securing finance at lower rates and generating immediate income from stronger yields offers a compelling combination.

What first-time landlords need to know about sourcing the right Buy-to-Let mortgage deal for their rental property investment.

Securing your first Buy-to-Let (BTL) mortgage is a key step to determining the budget you will have to buy a rental property.

If you’re looking to invest in your first investment property in 2026, it’s important to understand that Buy-toLet mortgages differ from traditional homeowner mortgages. It’s not just about finding the lowest interest rate; it’s about securing the most suitable Buy-to-Let mortgage product to get you started on your property investment journey. For anyone new to property investment, the National Landlord Investment Show on 24th March in London offers an in-depth New Investor Masterclass led by a panel of experienced investors and industry experts who will guide you on how to build a profitable portfolio, leverage finance and avoid costly mistakes. Get your free show ticket here

In this article, we highlight the key considerations and focus on the financing of property investment for first-time and accidental landlords seeking a Buy-to-Let mortgage.

Differences Between BTL and Homeowner Mortgages

The majority of new landlords are already homeowners and have, at some point, secured a mortgage to buy their property; however, moving from a residential homeowner to a property investor requires a change in mindset.

Lenders view rental properties through a different lens, weighing commercial

risk rather than personal affordability, which means there are key differences in the application process and approval criteria.

Seeking professional advice from a trusted mortgage broker who specialises in the Buy-to-Let market will help you to navigate the application process and could help you to secure a mortgage deal you may not find through your personal searches.

There are a few key primary areas where BTL mortgage products differ from standard mortgages.

Most lenders view Buy-to-Let mortgages as higher risk, which is reflected in the deposit requirements. Generally speaking, lenders require a minimum of 25% deposit; however, some specialist products offer 20% deposits.

For a first-time investor, having a larger deposit (35-40%) could unlock better interest rates; however, it’s best to seek advice from a BTL mortgage specialist to determine the most suitable options for your budget and long-term investment goals.

Unlike standard mortgages, Buy-to-Let mortgages are typically interest-only, with only the interest paid monthly and a single lump-sum repayment required at the end of the mortgage term.

Whilst it is possible to secure a repayment mortgage on an investment property, it isn’t the industry ‘norm’.

Most lenders view Buy-toLet mortgages as higher risk, which is reflected in the deposit requirements. Generally speaking, lenders require a minimum of 25% deposit; however, some specialist products offer 20% deposits.

By using the services of a trusted and professional BTL mortgage advisor, you may even gain access to mortgage products that you’d be unable to secure yourself.

Interest Cover Ratio

To assess the affordability of a BTL mortgage, lenders use an Interest Cover Ratio (ICR) to ensure the rent can cover the mortgage.

Typically, lenders require the rental income to be 125% to 145% of the mortgage payment, often calculated at a hypothetical "stressed" interest rate (e.g., 5.5% or higher).

The Bank of England explains, “A stressed ICR of 125% reflects the amount of gross rental income required for landlords to break even, factoring in the costs of mortgage repayments (including a potential increase in interest rates), tax and property maintenance.”

Alongside stress-testing the numbers, most lenders still require you to have a separate personal income (typically a minimum of £25,000) to ensure you can cover any potential void periods, if the property is unoccupied.

In some cases, people find themselves becoming landlords by accident. This can happen through inheriting property and changes in living situations, for example, moving in with a partner.

Accidental landlords should contact their current lender if they plan to let out a property with an existing owneroccupier mortgage in place. If you fail to do so, you could invalidate your current mortgage.

In some cases, lenders may grant you ‘consent to let’ based on your current mortgage, or they may require you to switch to a Buy-to-Let mortgage.

If your current lender does not provide ‘consent to let’ and you cannot switch to a Buy-to-Let mortgage with them, you will likely need to remortgage elsewhere, which may incur early repayment charges depending on your current mortgage term.

It’s best to speak to your current lender to get advice based on your current circumstances and long-term goals for the property.

If you are considering buying your first BTL property, seek independent mortgage advice from a provider who specialises in Buy-to-Let property. They will be able to provide you with advice based on your personal circumstances and your future plans for the property, plus they will help you navigate the paperwork and application process.

By using the services of a trusted and professional BTL mortgage advisor, you may even gain access to mortgage products that you’d be unable to secure yourself.

Don’t Forget Stamp Duty and Additional Fees

Alongside the money required to buy an investment property, new landlords must account for the amount of Stamp Duty Land Tax (SDLT) payable upon completion. Solicitor fees, landlord insurance, maintenance and management fees should also be budgeted for to ensure you understand the total cost required to invest in your BTL asset.

The 2026 rental market remains a land of opportunity for those who are well-prepared. With rental demand still outstripping supply in major UK hubs, Buy-to-Let property has the potential to help you build wealth long-term. If you’re looking to invest in your first Buy-to-Let property in 2026 or are an accidental landlord unsure how to manage your new responsibilities, sign up to attend the National Landlord Investment Shows in 2026 and attend the New Investor Masterclasses

LIS Media

CAT WESTERLING EXECUTIVE HEAD OF LETTINGS UK HAMPTONS

For years now, it’s felt fashionable to predict the death of buyto-let. A tougher tax regime, higher borrowing costs and shifting legislation have all contributed to a sense that private landlords are heading for the exit. Yet look beneath the surface, and things look a bit less gloomy. Rather than disappearing, landlords are adapting and finding new ways to make the sums stack up.

The numbers tell a story of resilience rather than retreat.

Last year, 10.9% of homes in Great Britain were bought by a landlord – slightly down on 2024, reflecting the first full year of the higher 5% stamp duty surcharge, but still marking a market that’s functioning, not folding. Meanwhile, 13.6% of homes sold in 2025 were sold by a landlord, broadly in line with the year before and notably below the 2022 high of 16.5% when many took advantage of buoyant conditions mortgage interest relief finally vanished.

Rising interest rates and higher entry costs widened the divide between places where new buy-to-let purchases worked and those where they didn’t. Investors gravitated towards higheryielding pockets of the Midlands and North, which continue to offer some of the strongest returns – an essential buffer in a world where costs from mortgages to maintenance have climbed. And yields matter more than ever: rents are up 48% over the last decade, outpacing inflation at 38%. That long-run rental growth continues to do the heavy lifting for long-term landlords’ margins, even if they have faced more pressure.

But 2025 saw somewhat of a reversal. After several years of softer prices in London and parts of the South, we’ve begun to see opportunistic investors buy back in. Even in the capital, 9.9% of homes sold last year went to a landlord – evidence that landlords aren’t totally overlooking London. While yields may still trail those achieved in the North, recent growth has been enough to

tempt some landlords south again, particularly as falling mortgage rates improve the arithmetic.

Perhaps the clearest sign that buy-tolet isn’t on its knees comes from the corporate side. 2025 was a record year for new buy-to-let limited company incorporations, which rose 8% from the previous high watermark set in 2024. Landlords aren’t just holding on; many are professionalising and restructuring. Incorporation has long been a way to offset tax changes, but the scale of last year’s growth suggests something more: landlords preparing for a future in which portfolios are run more like small businesses.

These changes are happening against a backdrop of an undersupplied rental market. Even though rents dipped slightly in 2025 – the first calendaryear fall on record – that softness was driven more by a temporary cooling in demand than by any real increase in supply. Stock levels remain 38% below 2016. The country still needs more rental homes, and private landlords remain central to delivering them.

None of this suggests that buy-to-let is easy. Margins are tighter, regulation is heavier, and the operating environment is more complex than it once was. And with the Renters’ Rights Act coming into force in May, some investors are bracing for additional procedural friction.

The new rules will, amongst other things, prevent landlords from accepting offers above the asking price. While the immediate impact on achieved rents is likely to be limited,

the longer-term effect may be to squeeze choice and nudge some marginal homes out of the sector. Yet despite these headwinds, the landlords who remain are choosing to stay – and in many cases, to grow. They’re buying smarter, structuring carefully, and seeking returns in places that would have made them raise an eyebrow ten years ago.

Buy-to-let hasn’t died, and today’s landlords aren’t speculators riding a wave of capital appreciation. Rather, they’re yield-focused operators navigating a tougher landscape with more discipline and a long-term view. And as the market stabilises and borrowing costs ease, it’s increasingly clear that a leaner, more professionalised version of the sector is here to stay.

Even in the capital, 9.9% of homes sold last year went to a landlord – evidence that landlords aren’t totally overlooking London.

REECE MENNIE CEO & FOUNDER

With housebuilding plummeting well below target levels, continually rising mortgage rates, and a backdrop of landlords selling up in droves, the Spring Statement provided a further opportunity to provide additional support to the UK’s property sector.

Yet it was a missed one, with Chancellor Rachel Reeves providing no substantive announcements for the industry – or around wider concerns such as taxation. Instead, the statement simply dashed any remaining hope that Labour could achieve its highly ambitious target of building 1.5 million new homes during its first term in power.

This aim looks less achievable than ever, with around 220,000 homes set to be developed in 2026/27. This is not only well below the average of 260,000 a year we were seeing in the early 2020s, but also far less than the 300,000 needed annually to hit that 1.5m target. It is now expected that 2030/31 will be the first year that we see more than 300,000 built.

All of which backs up the sentiment that the British housing crisis is not going to be solved through new builds alone – something which savvy investors and developers had realised some time ago. These individuals and organisations have already turned their attention to alternative ways to narrow the gap between demand and supply, by focusing on the rejuvenation of existing empty sites. By renovating unused residential and commercial buildings and bringing them back to life, more people will have the chance to live in a quality home in a desirable location. There are a wealth of these sites currently lying empty in town and city centres, near to amenities and transport links – ideal for commuters, families, and downsizers alike.

Recent years have been extremely challenging for landlords. Tax increases, regulatory pressure and higher borrowing costs have all

squeezed returns, and a further 2% rise in tax on property income is due to come into force in April 2027. So, it is little wonder that Government figures show a record 26% selling at least one property in 2024, and (while official numbers have not yet been released) a further 93,000 landlords were expected to get rid of their entire portfolio in 2025.

Aside from the effects on the shrinking number of landlords, we must also consider the impact on tenants too: reduced rental stock, rising rents, and fewer options in an already strained market. It is simply not good news for anyone, and the situation shows no sign of being brought under control by those in power.

Among those still concentrating on traditional buy-to-let and build-to-let options, those thriving are few and far between. With yet another missed opportunity to act, the Chancellor’s lack of intervention reinforces the need for those seeking strong, predictable returns to look at other options instead. More than a quarter of a million residential properties are vacant and a further 170,000 commercial properties empty. Through leveraging permitted development rights, reusing as many materials as feasible, and retaining the original structure of the building where possible, these can be transformed into modern homes in a fraction of the time a new development takes to plan and construct.

There is a real opportunity for the property sector to help address the housing crisis by focusing on underused buildings and existing urban space, which is something government policy continues to overlook.

More than a quarter of a million residential properties are vacant and a further 170,000 commercial properties empty. Through leveraging permitted development rights, reusing as many materials as feasible, and retaining the original structure of the building where possible, these can be transformed into modern homes.

NICOLE BONNER

CONTENT, COMMUNITY & PR LEAD

NATIONAL LANDLORD INVESTMENT SHOW

On 19th January 2026, the government published the wording for a new written statement and information required before a tenancy agreement is signed on or after 1st May 2026.

What is the Written Statement of Terms?

The Written Statement of Terms is a statement of terms of information issued by a landlord to a tenant before entering an assured period tenancy agreement on or after 1st May 2026. This change is a key legislation update as part of Section 12 of the Renters’ Rights Act.

The draft statutory instrument of the written statement can be found here It is important to note that it is still a draft and it may change before it is likely to be passed in March 2026.

What needs to be in the Written Statement of Terms?

Contact details of parties

• Landlord name

• Tenant name

• An address in England or Wales where notices can be served on the landlord by the tenant.

Property details & tenancy start date

• Address of the property being let

• Start date of the tenancy

Financial terms

• Amount of rent payable by the tenant to the landlord

• Date the rent is due

• A statement explaining that if the landlord makes a new proposal to increase the rent under the tenancy, the landlord must serve a notice on the tenant in accordance with section 13 of the 1988 Act (increases of rent under assured tenancies other than relevant low-cost tenancies).

• Relevant bills & utilities – in the case where a landlord charges a tenant for bills. The written statement should clearly outline whether these costs are included, and, if not, how and when the tenant should be notified of additional payments if the costs are in addition to the monthly rent payment.

• Tenancy deposit amount

Notice

• The minimum notice a tenant must provide when giving a notice to quit the property.

• Possession by a landlord: In most circumstances, the landlord can only bring an end to the tenancy by obtaining an order of the court for possession of the property and the execution of the order

& compliance

• Fitness & habitation statement explaining that the landlord is under an obligation to ensure the property is fit for human habitation, to the extent required by that section.

• Repair statement explaining the landlord’s duties for structure, exterior and installations in the property

• Electrical safety statement explaining that the landlord is under an obligation to ensure that relevant electrical safety standards are met during any period when the property is occupied under the tenancy, and that electrical installations in the property are inspected and tested by a qualified person (within the meaning of that regulation) at least every five years. The full report and inspection schedule should be provided to the tenant.

• Gas Safety statement explaining that the landlord is under an obligation to maintain in a safe condition any relevant gas fitting and any relevant flue which serves a relevant gas fitting, and maintain an annual gas safety and testing inspection

Information

• Pet consent rights, including that consent must not be unreasonably withheld if the tenant requests to keep a pet.

• Disability adaptations.

• Supported accommodation status, where relevant.

When will it need to be issued, and how can it be issued?

The Written Statement of Terms must be provided when a new tenancy is created, on or after 1 May 2026. This will need to be done before a tenancy agreement is signed or a tenancy is otherwise agreed. The information can be provided within a written tenancy agreement or given separately.

The information can be provided in hard copy format or electronically.

Why is this important?

Failure to comply with this new requirement and responsibility as a landlord may result in civil penalties being issued by local authority powers, so it’s important to comply. This also applies to letting agents acting on behalf of the landlord.

Will this apply to existing tenancies?

If you have signed tenancies in place before 1st May 2026, you will not need to provide a new assured tenancy agreement or a written statement.

Instead, landlords with existing tenancies will need to provide tenants with a copy of the UK Government published ‘Information Sheet’ on or before 31 May 2026. The information sheet will be published in March 2026. The information sheet must be given to all tenants named on a tenancy agreement. It can be provided electronically or in hard copy.

In the situation where your current tenancy is based entirely on a verbal agreement, you’ll need to give your tenant a written record of the specific terms of the agreement. You will have to do this instead of providing the information sheet.

How can you get support?

Staying up to date with the progress of the Renters’ Rights Act is crucial to ensure you stay professional and compliant as a landlord. Attending live events in 2026, such as the National Landlord Investment Show with the upcoming show on 24th March, with free Renters' Rights training led by Susie Crolla, Managing Director of the Guild of Lettings & Management and other expert-led segments on the changes ahead from LRG and Hamptons.

Prepare now and avoid costs later to stay ahead. You can now get your free tickets to all live 2026 shows across the UK, and attend the first show of the year in London, Old Billingsgate on 24th March

Landlords are losing millions of pounds worth of equity simply because they do not know how to title split their properties.

They are either unaware they can Title Split, or they have been advised to leave it until they sell. Landlords own multi-unit freehold properties (multiple properties on one freehold). Where multiple addresses exist on one freehold and a landlord attempts to sell their property as a multi-unit freehold, it is valued at wholesale price. Unfortunately, many landlords believe these properties can be sold to another landlord, with tenants in situ at the retail price. This is simply not true and regularly leads to disappointment for exiting landlords.

Today, as I write this article, there are 760,325 unsplit freeholds in England and Wales with between 2 and 20 addresses on a single freehold. This data sits on the land registry. These landlords own the multi-unit freeholds (MUF) or multi-unit freehold Blocks (MUFB) in their own names. A further 84, 254 are owned by private companies. Total unsplit freeholds 844,579. The benefit of Title Splitting MUF’s or MUFB’s is that individual units will grow in line with UK capital growth.

Retail Price = Comparable, the price for a similar property recently sold nearby with a similar standard of refurbishment. A RICS surveyor will look for the nearest comparable sold prices. This price is for individually sold, vacant properties.

Wholesale price= Investment valuation (You may know this as a commercial valuation). Investment valuations are calculated by a RICS surveyor based upon a local yield calculation multiplier and the rent on the property. In many

instances, this price is substantially lower. This price is for multiple tenanted units. Unfortunately, landlords selling these properties en masse, expect to receive the individual comparable prices based on similar properties sold locally, when selling multi-unit freehold units to another landlord. The banks then give a lower-than-expected valuation and the landlords’ sale falls through. This can be disruptive for tenants (renting in the property) and landlords who are looking to exit the market.

How can this problem be fixed for exiting or holding landlords?

Landlords looking to release equity, have a few options, depending on whether they are planning to continue as a landlord or sell their properties:

1. Remove tenants and sell the property vacant, one at a time (title split on sale) to owner buyers. This can be problematic, as you would need permission from your mortgage lender to reduce their security one flat at a time. Most lenders would not allow it. Bridging lenders are more likely to allow this, so you could move onto a bridging loan to sell.

2. Sell the entire MUF or MUFB to another Landlord for the wholesale value. If you are looking to exit sooner rather than later, then this is probably the best option.

3. Arrange to Title Split the MUF or MUFB to release capital and access capital growth. Remember this valuation is based on a bank valuation carried out by a RICS surveyor. In most parts

of the UK, this will give you access to around 25% to 35% capital uplift on the block. Once you have each unit on an individual title and an individual Buy-ToLet mortgage, this gives you the option to give notice and sell one retail unit at a time in the future.

The Opportunity for Developers and Landlords who are buying MUFs and MUFBs

Title Splitting is a huge opportunity for those looking to acquire property and grow their buy-to-let, commercial property or commercial to residential portfolios. It enables you to buy one property and create multiple pots of income and capital growth in your property portfolio. In addition, it is absolutely perfect for developers wanting to flip properties. MUFBs and MUFs very rarely require planning or permitted development as the units exist already. Having access to the right team and the right knowledge is crucial to making this happen. TitleSplit.com can help both buyers and sellers of blocks access the massive equity sitting in these unsplit freeholds (over £115 Billion).

Also, we have secured a limitedtime, exclusive offer for LIS Leaders: a 2-day LIVE Title Split Unleashed Bootcamp programme. This offer is not available publicly.

Scan the QR code to find out more.