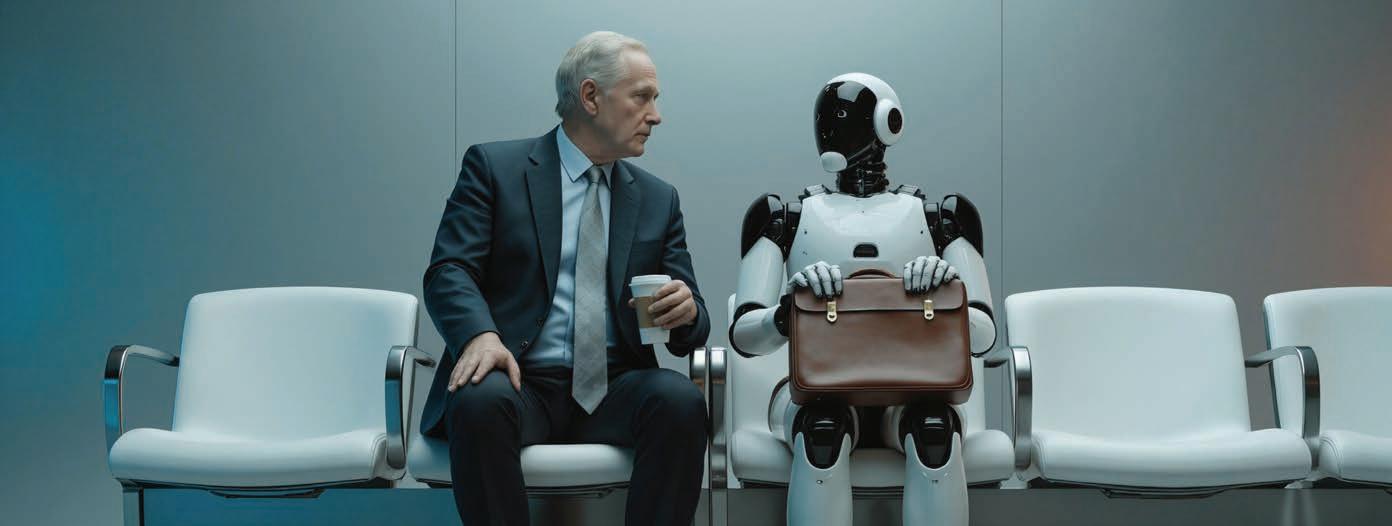

Wealth managers move toward an AI future

Amid uncertainty, advisors are connecting AI across systems

24 Orion doubles down on AI CEO Natalie Wolfsen forecasts an exponential productivity boost

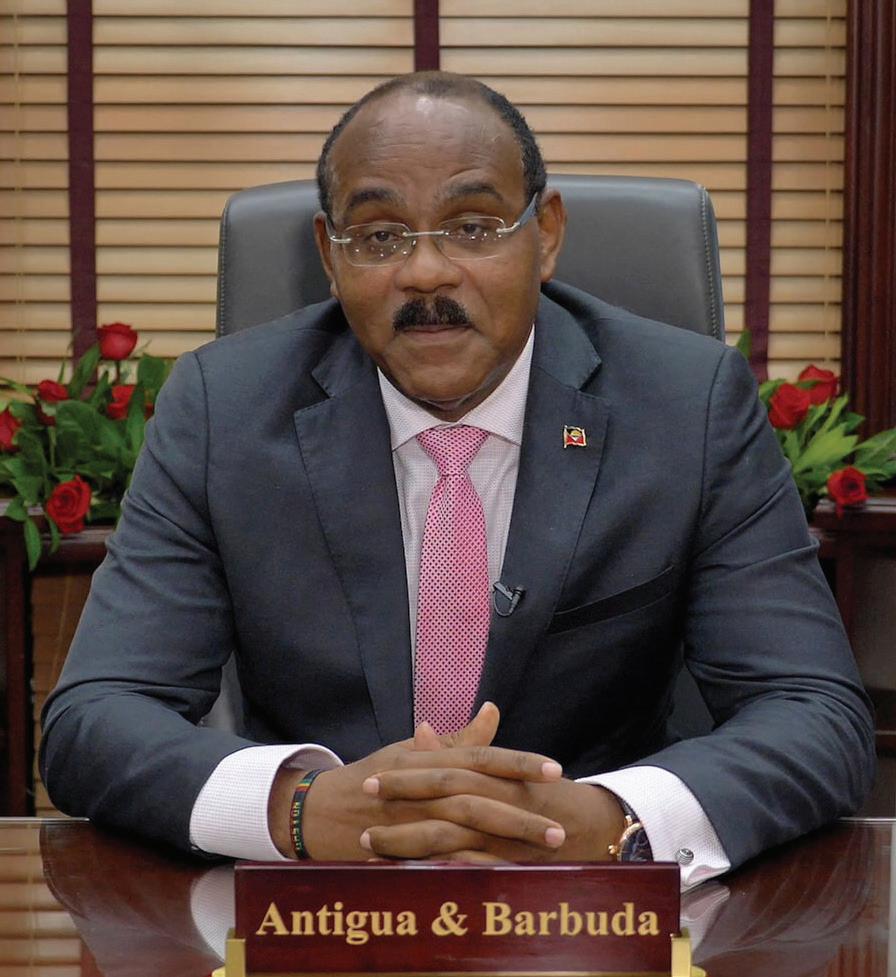

26 Renaissance in Caribbean nation as Americans invest Gaston Browne, prime minister of Antigua and Barbuda, welcomes the global elite

28 A future for AI notetaking tools? ‘Advisor operating systems’ may top CRMs

BY JAMES ROGERS

Afew years ago, if I’d used AI to help in the production of a story, I would have been marched out of the newsroom. Today, like many of my colleagues, I’m leaning on it more and more – for research, sharpening angles, and speeding up routine work. The job hasn’t disappeared; it has changed. The same dynamic is now bearing down on financial advisors, broker-dealers, and RIAs.

Orion’s annual Advisor Wealthtech Survey underscored just how central AI is becoming: more than half of respondents said AI and automation will have the biggest impact on firm success in 2026 and beyond.

Yet the survey also highlighted friction points most firms will recognize: uncertainty around compliance and regulation, anxiety about accuracy and client trust, and a shortage of internal AI expertise or training. The wealth industry is convinced AI matters, but it’s far less certain about how to adopt it safely and intelligently.

For many firms, AI conversations start – and potentially stall – in the compliance department. At the recent Exchange ETF conference in Las Vegas, SEC Commissioner Hester Peirce described getting “an earful” during meetings with compliance officers. They “want to use AI,” she said, but they feel like they’re “walking into some landmines on the regulatory side.”

Her response should be carefully noted by anyone leading an RIA or broker-dealer: “My view is that we don’t need a rule that is specifically for AI unless we see problems that are specifically tied to AI.”

As for the technology itself, advisors have every right to be skeptical of something that sometimes “hallucinates.” While that’s an annoyance for consumers, it’s a risk in a regulated environment.

But it is getting better by the day. The building blocks of AI are being constantly fine-tuned, boosting accuracy and precision.

Building client trust is a mountain advisors should be able to climb – trust, after all, is the cornerstone of the advice industry. Openness is key, and advisors should spell out both the benefits and limits of AI. Make it crystal clear where AI ends and human oversight begins; the human-in-the-loop is key.

Yes, this is a training challenge, particularly for smaller firms, but it’s also an opportunity − early, disciplined adopters can quickly build a lead over their rivals. Now is the time to identify the “AI champions” in your business and let them lead.

“Building client trust around AI is a mountain that advisors should be able to climb – trust, after all, is the cornerstone of the financial advice industry”

If you feel behind on AI, you’re not alone. A recent survey of 5,000 knowledge workers in large companies across the US, Canada, and the UK found that, three years after the release of ChatGPT, most people are still AI beginners. Less than 3 percent of the workforce currently qualifies as AI practitioners or experts, according to the research by AI workforce transformation firm Section.

Quite simply, your career could hinge on how quickly you get to grips with AI. Half of the CEOs recently surveyed by Boston Consulting Group said that their job is on the line if AI doesn’t pay off. In virtually every industry, AI may be the biggest wave that any of us have seen. But, whether you’re a journalist or an RIA, we all have to ride it.

EDITORIAL

VP - Editorial: James Burton

Managing Editor: James Rogers

Senior Columnist: Bruce Kelly

Retirement & Planning Editor, Multimedia Anchor: Gregg Greenberg

Journalists: Andrew Cohen, Leo Almazora

Senior Sponsored Content Writer: Manal Ali

SALES

Chief Revenue Officer: Dane Taylor dane.taylor@keymedia.com

Business Development Managers: Catherine Reale catherine.reale@keymedia.com; Victoria Hamilton victoria.hamilton@keymedia.com; Barry Echavarria barry.echavarria@keymedia.com

Lead - Fulfillment Team: Cole Dizon Fulfillment Coordinators: Cyrus Arroyo, Pauline Talosig

PRODUCTION

VP – Production: Monica Lalisan

Lead Production Editor: Roslyn Meredith Production Editors: Tara Tovell, Karen Atienza, Allison Ingusan

Production Coordinator: Kat Guzman Designers: Joenel Salvador, JP Dizon, Juan Ramos Design Manager: Sheila San Miguel Creative Director: Marla Morelos

EVENTS VP – Events: Katie Jones Head of Event Marketing: Oliver McCourt Awards Director: Jessica Duce Head of Event Production: Jesse Friedl

MARKETING & RESEARCH

Global Director: Claire Preen Marketing and Operations Director: Danica Mendoza Managing Editor – Special Reports: Chris Sweeney

VP – Marketing Services: Lauren Counce

Marketing Activation Manager: Rissa De Leon

Project Manager: Kristyn Dougall

CORPORATE

President: Tim Duce

Director, People and Culture: Julia Bookallil CIO: Terry Szames

CEO: Mike Shipley

COO: George Walmsley

INSURANCE BUSINESS AMERICA cathy.masek@keymedia.com

INSURANCE BUSINESS AUSTRALIA sophie.knight@keymedia.com

INSURANCE BUSINESS CANADA chad.beck@keymedia.com

INSURANCE BUSINESS UK gemma.powell@keymedia.com

BENEFITS & PENSIONS MONITOR WEALTH PROFESSIONAL CANADA abhiram.prabhu@keymedia.com

Allianz Life has found more than half of women taking responsibility of their household’s finances, though just two thirds say they’re on sound financial footing.

In Cerulli’s survey research of advisors, an overwhelming majority agreed their firms’ tech is somewhat or very effective at supporting a wide range of key business objectives, including but not limited to regulatory compliance, creating quality experiences for clients, and enabling delivery of investment management services.

The most recent analysis by the Tax Foundation found that for 2026, New York, New Jersey, California, District of Columbia, and Connecticut were the least tax-competitive jurisdictions, based on five major areas of taxation, including individual income taxes. EASTERN STATES

Source: Allianz Center for the Future of Retirement, March 2026

Based on survey data from Greenwald Research, the Center for Retirement Research at Boston College in partnership with Jackson Financial determined that since the start of 2025, nearly one in two advisors thought the US economy has gotten stronger, while just over half of near-retiree and retired investors think it’s taken a turn for the worse.

Source:

While most college students see planners as a trusted source of financial advice, two thirds say they don’t know where to find the right one, and just over half don’t know what questions to ask.

With $11 billion in assets across 20 deal announcements, Wealth Enhancement Group was the most prolific acquirer last year, though Mariner got the most new assets, according to Echelon Partners’ 2025 RIA M&A deal report.

Congressional hearings in March laid bare the severe doubts some lawmakers in Washington have about FINRA, the giant self-regulatory organization that oversees the securities industry

BY BRUCE KELLY

After a year when it fended off questions about its legitimacy raised by a lawsuit by brokerdealer, FINRA started 2026 in the hot seat before Congress.

At hearings in March, some lawmakers questioned whether the self-regulatory organization, which acts at the behest of the Securities and Exchange Commission, even has a right to exist.

Meanwhile, as it remains under attack in the highly anti-regulatory environment in Washington, FINRA is also working to have a friendlier relationship with the securities industry.

For example, recent changes make the enforcement process a little easier for broker-dealers.

Plus, FINRA recently said it was giving a rebate of $100 million to the broker-dealers it oversees, dismissing howls from the plaintiff’s bar that such money should go to investors who won arbitration awards against firms but never received a dollar in payment.

FINRA’s current dilemma is due, in part, to its role as a regulator during a Republican administration that staunchly believes in cutting regulations and rules, many of which are costly to implement.

The Trump administration’s recent push to allow advisors to sell more alternative investments in retirement plans will only put more pressure on regulators.

“I don’t think FINRA is being picked on, but the organization is being looked at to see its effectiveness versus its cost,” says Sander Ressler, managing director of Essential Edge Compliance Outsourcing Services. “Lawmakers are concerned that a membership organization that regulates the industry will have buy-in.”

“The biggest firms contribute the most cash,” he notes. “Will FINRA regulate those firms as tough as smaller firms? It’s a legitimate concern.”

“Congress is looking to reduce regulation, and as long as there is a Republican majority, it will continue to seek a reason to cut regulations for the securities industry,” Ressler says. “That also means tarnishing FINRA in public and questioning its constitutional authority.”

FINRA right now is no darling of some in Congress. On March 6, the Capital Markets Subcommittee took its time criticizing the selfregulatory organization in a hearing devoted to SROs.

“Today, FINRA staff, not industry members, writes binding rules, investigates people, brings enforcement cases, holds hearings, issues large fines, and can permanently end someone’s career,” says Republican Congresswoman Lisa McClain of Michigan.

“Yet, FINRA is not subject to the same transparency laws as federal agencies,” McClain says. “Its meetings are not fully open. Its records are not fully public. Now, if an organization exercises government-level power, it should have governmentlevel accountability.”

“The biggest firms contribute the most cash. Will

FINRA regulate those firms as tough as smaller firms?”

SANDER RESSLER, ESSENTIAL EDGE COMPLIANCE OUTSOURCING SERVICES

“FINRA exercises regulatory authority over thousands of firms, yet it is not subject to the Administrative Procedures Act, FOIA, or direct congressional appropriations,” says Republican Congressman Warren Davidson of Ohio. “So members of this committee have had similar concerns about the structure of the Federal Reserve, for example.”

When asked about the Congressional hearing and such comments, a FINRA spokesperson replied: “As a self-regulatory organization, FINRA protects investors and safeguards market integrity at zero cost to the American taxpayer.”

At the end of 2024, Finra reported

“FINRA is not subject to the same transparency laws as federal agencies. Its meetings are not fully open. Its records are not fully public”

LISA MCCLAIN, REPUBLICAN CONGRESSWOMAN, MICHIGAN

FINRA has faced criticism from the securities industry it regulates ever since it was formed in 2007 by the merging of NASD and NYSE Regulation, Enforcement, and Arbitration.

At the end of 2024, FINRA oversaw and regulated 3,249 firms and 634,508 registered reps, or financial advisors. Although it is not a governmental agency, it operates under the aegis of the SEC. It charges broker-dealers fees, which make up its budget.

Once Donald Trump was re-elected president in 2024, FINRA staff was likely preparing to face such public criticism. After all, Project 2025, published by long-running FINRA foe the Heritage Foundation, and a blueprint for the Trump presidency, calls for the self-regulator to be eliminated.

Despite the attacks, FINRA is still the central regulator of the securities industry.

And the organization had its defenders in the March hearings in Congress.

“The Exchange Act’s model of securities industry self-regulation is grounded in certain core principles, which continue to resonate today,” said Onnig Dombalagian, professor of law at Tulane University, in written testimony.

“These include the industry’s familiarity with securities market operations, its reputational interest in upholding mutual and reciprocal principles of trade, and the ability to shift the financial burden of regulation to the industry through membership fees and other revenue sources,” Dombalagian notes.

“As markets have evolved, SROs including FINRA also maintain critical infrastructures for advancing the goals of the national market system, such as information processing and dissemination services, market and member surveillance systems, and other utilities,” he adds.

FINRA’s been in the hot seat before.

It spent 2024 and 2025 fighting a lawsuit that in part alleged the organization didn’t have a constitutional reason to exist. It ultimately prevailed when the Supreme Court last June declined to hear the appeal of Alpine Securities, the firm suing FINRA. That left in place a lower court’s ruling that gives FINRA the authority for enforcement action but required it to check with the SEC before expelling a firm.

“We’ve seen more attacks on FINRA the last couple years than in decades before,” Ressler says. “From the Alpine lawsuit to hearings in Congress, FINRA is being questioned for its reason to exist.”

Alternative investment platforms like SEI Access now let financial advisors explore litigation finance, a high-return but high-risk alternative

BY ANDREW COHEN

Alternative investment platforms are adding litigation finance opportunities for financial advisors, but many RIAs remain cautious about allocating client capital to a strategy whose returns hinge on courtroom outcomes rather than market performance.

SEI announced earlier this year that it expanded its alternatives marketplace, SEI Access, to include a litigation finance offering from Pravati Capital, an Arizona-based firm that’s funded more than $248 million to law firms and litigants since its founding in 2013. The global litigation funding investment market was valued at more than $20 billion in 2025 and is projected to grow to more than $50 billion by 2036, according to a report from consulting firm Research Nester.

“Oftentimes litigation finance for the United States isn’t nearly as adopted as it is outside the United States, in Europe specifically, and historically it has been institutional in terms of who would be allocating to it,” Pravati Capital managing director Kris Kjolberg tells InvestmentNews “But now advisors are looking at asset classes like litigation finance, which leads us to platforms like SEI’s Access, like CAIS, like iCapital. They provide compliance workflow, due diligence, and operational controls that wealth managers, RIAs really require.”

Litigation financing remains a niche corner under the broader private credit asset class. “Advisor demand is real, but the category is education

driven,” says Kjolberg. Pravati Capital primarily makes senior-secured loans to middle-market law firms, using portfolios of legal claims as collateral instead of financing individual cases. Loans typically originate at annualized interest rates between 19 and 27 percent, with an average investment duration of roughly two to two-and-a-half years, according to company materials.

“It’s an interesting alternative class, because the returns could be pretty high. From what I know,

“Large-scale commercial disputes illustrate why advisors are seeking exposures that are driven by legal processes and not economic cycles”

KRIS KJOLBERG, PRAVATI CAPITAL

returns on successful funds are 20 to 40 percent,” says attorney Corey Kupfer, whose Kupfer Law firm specializes in M&A for RIAs. “They’re totally unrelated to economic conditions. In fact, sometimes when there are bad economic conditions, there’s more litigation.”

Public disclosures from Burford Capital, the largest litigation financing firm in the US, show the economics driving litigation finance. Across concluded investments, the firm reports a roughly

26 percent internal rate of return (IRR) and 83 percent return on invested capital. Most cases − roughly 78 percent − settle before trial, generating around 22 percent IRR, while cases that proceed to trial and win can produce returns exceeding 200 percent on invested capital.

According to Burford’s latest investor presentation, approximately 8 percent of funded cases lose at trial, resulting in an average negative 87 percent return on invested capital.

“Because of the nature of the risk level, this is less applicable for firms that are doing massive affluent type clients as opposed to more ultra-high worth,” adds Kupfer. “Obviously, this is something you see in the family office model, the multi-family office model much more often.”

Count Mercer Advisors among the large national RIA firms not buying the return-to-risk profile of litigation financing. The mega-RIA manages nearly $100 billion in client assets, including its Regis Group division covering ultra-high-net-worth clients with $25 million or more in investible assets. Litigation financing was described as a “highly speculative investment” by advisor David Krakauer, VP of portfolio management at Mercer Advisors.

“There’s a high risk of loss, very unpredictable outcomes. And then when we think about who’s bringing the lawsuits and who’s actually running the proceedings, there’s actually a high potential for conflicts of interest as well when we think about

the outcomes and who’s influencing the outcomes of some of these cases,” says Krakauer.

“With something like litigation finance, the outcomes are so widespread. It’s very hard to peg this asset class as something that’s going to deliver X returns for our clients over a certain period of time,” he adds.

Current broader market developments could affect demand for litigation finance. A U.S. Supreme Court decision in February to strike down many of President Trump’s tariffs imposed under the International Emergency Economic Powers Act has spurred a wave of litigation seeking refunds to recover tariff payments totaling over $130 billion in the 10 months they were in effect.

The Wall Street Journal reported in March that more than 2,000 lawsuits have been filed by companies seeking tariff refunds, including well-known names like FedEx, Costco Wholesale, Goodyear Tire & Rubber, and Barnes & Noble Purchasing.

GLOBAL LITIGATION FUNDING MARKET

2025 market value: $20B

Projected 2036 value: $50B

Growth driven by US commercial disputes and global adoption

“Companies that paid tariffs are pursuing refund litigation. The analysts that I read estimated $130 to $175 billion in refund claims, which is very large,” says Kjolberg. “Large-scale commercial disputes illustrate why advisors are seeking exposures that are driven by legal processes and not economic cycles.”

Pravati Capital mainly finances contingency-fee personal-injury law firms, and to a lesser extent backs mass-tort, commercial, intellectual property, and whistleblower cases. Pravati Capital has participated in government litigation, funding a law firm that represented individuals in the Camp Lejeune toxic-water cases stemming from water contamination at the North Carolina Marine Corps base between the 1950s and 1980s. Settlements and awards since 2023 have totaled hundreds of millions of dollars.

New York has taken the lead on regulating litigation finance, passing one of the first substantive state laws aimed at increasing transparency and consumer protections in third-party funding arrangements. The New York Consumer Litigation Funding Act, signed by Governor Kathy Hochul in December 2025, requires funders to disclose key terms of their financing agreements to plaintiffs and courts and prohibits funders from interfering with litigation strategy.

“New York has moved litigation financing from the shadows to a supervised, disclosure-heavy regime, while empowering courts to probe funding when it bears on motive or misconduct,” wrote Maryan Alexander, partner at New York-based law firm Wilson Elser. “Stakeholders should prepare for regulatory compliance and more nuanced discovery practice as these changes take hold.”

“With something like litigation finance, the outcomes are so widespread. It’s very hard to peg this asset class as something that’s going to deliver X returns for our clients over a certain period of time”

DAVID KRAKAUER, MERCER ADVISORS

SEI Access reports having over 250 wealth management firms using its alternatives platform, which is distinguished in its litigation finance offering compared to competing alts marketplaces like CAIS and iCapital that have not made any announcements around litigation finance offers. New York’s legislation to bring transparency to litigation financing is a step toward filling the transparency gap for RIAs currently avoiding the asset class.

“There’s so much non-transparency and expertise that’s involved in this, it makes it highly

difficult to say [litigation financing] is a good, investable asset class for our clients,” says Krakauer. “If we did hear demand for it, I think the question would be, how do we put a valuation on that? How do we know if the price we’re getting is a good price or a bad price − if we’re investing into that space, what’s the yield, or what’s the multiple we should be requiring to take that risk?”

AMID MARKET VOLATILITY, persistent in ation, and an aging population that increasingly must shoulder retirement security, the work of the best nancial planners in the US has never been more consequential.

It’s estimated by Northwestern Mutual that Americans will need $1.26 million to retire comfortably. At the same time, surveys show nearly half of Americans expect to retire with less than $500,000, underscoring a widening advice gap and the need for high-quality planning.

Against this backdrop, the profession continues to expand in both scale and in uence. As of December 31, 2025, the number of CFP® professionals reached an all-time high of 107,529, an increase of 4.3 percent over 2024. Last year also marked the largest number of exam candidates in CFP Board history, with 11,037 people sitting for the exam, a 5.7 percent increase over 2024. Revenues from

INVESTMENTNEWS’ 5-STAR FINANCIAL PLANNERS: BY THE NUMBERS

Total AUM: $37,197,405,093

Average AUM: $470,853,229

Total clients: 26,844

Average number of clients: 340

fee-based advisory relationships climbed from an estimated $150 billion in 2015 to $260 billion in 2024, re ecting robust demand for human advice that has grown several times faster than the overall population. McKinsey estimates advised relationships will expand at least 28 percent over the next decade, from 53 million to 67–71 million by 2034.

Yet the value of the best nancial planners cannot be measured by growth statistics alone. In 2025, CFP® professionals in the US delivered more than 433,390 hours of pro bono nancial planning – an 11 percent increase over the prior year –providing an estimated $130 million in services to households that might otherwise go without advice. This combination of technical rigor and publicspirited service re ects the profession at its best.

This report is where InvestmentNews recognizes those nancial professionals who stand out within that landscape – planners who, over the past 12 months, have demonstrated not only strong performance but also integrity, client-centric innovation, and a clear commitment to helping individuals and families reach their nancial goals. These nancial planners are setting the standard for what modern planning can and should be: goals based, evidence driven, and rmly anchored in the best interests of the client.

about what his rm is really selling: service. As a CFP® professional and CFF®, he has built his practice around a high-touch, highly responsive client experience that he insists is still the exception rather than the rule.

“We believe that the product that we deliver is service,” he says. “Nowadays, technology is amazing at what it can put at your ngertips, and advisors exist all over the US. But what we pride ourselves on is that high level of service and responsiveness to our clients, and it makes them know that we care.”

Research shows clients now prioritize trust, communication, and personalized planning over raw investment performance, with the “human touch” eclipsing returns as the main driver of satisfaction and loyalty.

Cuplin and his team lean into that human element by deliberately positioning themselves as “bearers of good news” in an environment saturated with market scares, geopolitical shocks, and dire economic headlines. The goal is not to ignore risk but to pull clients out of a permanent state of anxiety and back toward the progress they are actually making. That optimism is grounded in process. He says, “We try to look at things in the big picture. That then is the blueprint that we use to make our decisions, to build out a portfolio, and to plan insurance coverages.”

Cuplin’s operating model is designed for ef ciency. Midwest Financial Group consolidated operations from three locations into a single agship of ce, allowing clients to meet the team’s specialists on the spot.

Matthew Cuplin: service, perspective, and planning Chief executive officer/ president of Midwest Financial Group (Wisconsin)

As portfolios and products increasingly feel commoditized, Matthew Cuplin is unapologetic

Community presence is another de ning theme. Cuplin attributes much of the recent organic growth to visibility and goodwill in the local area. He and his colleagues regularly teach no-cost classes at libraries and community centers, treating those sessions as education and outreach rather than prospecting events. That work lands against a national backdrop in which nancial illiteracy is estimated to cost American adults more than $200 billion a year, underscoring the stakes of better decision-making for everyday households.

“Some of the best meetings I’ve ever had were with people who didn’t end up working with us,” he says. “I’m a big believer in karma from the aspect of if you put something out there, it comes back to you.”

Cuplin sticks to the mantra of serving everyone, with a client walking in today experiencing the same level of care, discipline, and consistency as one who started a decade ago.

RJ Cunningham: planning first, products second Financial advisor–senior partner at Summit Global Private Wealth (Utah)

RJ Cunningham has a simple rule for rst meetings: no product talk, no annuities, no option strategies, and no alternatives. Instead, he focuses on mapping goals, trade-offs, and timelines before a single investment is proposed. “When I meet with a client, I’m not talking about options trading, stocks, or alternative investments,” Cunningham says. “First, we’ve got to get the plan in place.”

That planning- rst stance resonates in a market where anxiety is high and headlines are noisy. Nearly three in four US investors expect stock market volatility to persist through 2025, and a growing share say it is causing them to check accounts more often and second-guess decisions. Cunningham views those conditions not as a headwind but as an opportunity for differentiation. “Anytime volatility enters, I tell other advisors on our team, this is ‘go time’ – this is what’s going to separate you from every other advisor,” he says. In practice, that means phoning clients more when markets are rough and reaching out before nervous investors call him. His rst question when someone fears a looming recession is disarmingly basic: When do you actually need this money? If the goal is 15 or 20 years away, he argues, a short-term drawdown is usually a distraction, not the real risk.

Cunningham, who is a CFP® and ChFC®, leans heavily on metaphor and education to keep clients from making panicked moves. He likens market turbulence to a bumpy ight: when the plane shakes, the pilot doesn’t tell everyone to stand up and walk around – passengers are told to buckle up and ride it out. The same logic, he says, applies to portfolios mid-correction. Abandoning a longterm strategy in midair often does more damage than enduring volatility. That framing is backed by emerging research on advice: in a 2025 Vanguard study, 86 percent of advised investors reported greater peace of mind compared with managing nances on their own.

To identify outstanding nancial planners across the United States, InvestmentNews conducted a nationwide, nomination-based survey between November 3 and 28, 2025. The process was designed to recognize nancial professionals who demonstrate excellence, integrity, and a strong commitment to helping clients achieve their nancial goals, based on achievements during the past 12 months.

Nominations were accepted from industry peers, colleagues, clients, and self-nominated individuals. Only nancial planners who were formally nominated during the survey period were considered for evaluation. Nominators were required to submit detailed information for each nominee, including professional credentials, areas of expertise, and notable achievements from calendar year 2025. All nominations were subject to review and con rmation by the nominee’s compliance team to verify accuracy, authenticity, and adherence to ethical and regulatory standards before being accepted into the evaluation process.

A total of 231 nominations were received. Following an objective review and benchmarking process conducted by the IN editorial team, 80 nancial planners were ultimately selected for recognition.

Evaluation criteria

Each nomination was evaluated through a qualitative, information-based assessment focused on achievements and contributions over the previous 12 months. Evaluation considerations included:

• professional credentials and quali cations

• demonstrated areas of specialization or expertise

• signi cant professional or business achievements

• evidence of integrity, professionalism, and client-focused service

All entries were reviewed consistently to ensure fairness, objectivity, and editorial independence.

What the recognition measures

This recognition highlights nancial planners who demonstrated professional excellence and meaningful achievement during calendar year 2025, based solely on the information submitted and veri ed through the nomination process.

What the recognition does not measure

To comply with regulatory and advertising standards, this recognition is not based on:

• investment performance or portfolio returns

• client testimonials, endorsements, or satisfaction metrics

• quantitative business metrics such as assets under management (AUM)

• any criteria not expressly stated in this methodology

Fee and promotional disclosure

There is no fee to nominate, self-nominate, or be considered for this recognition. This award is not payto-play. Some recipients may choose to purchase optional promotional or marketing materials from IN after being selected; however, such purchases have no in uence on the nomination process, evaluation criteria, scoring, or nal selection.

Referrals tend to come from clients who felt listened to rather than pitched, whether the conversation centered on Roth conversions, Social Security timing, or sustainable withdrawal rates. This is a key driver of how Cunningham’s own metrics have scaled: assets under management (AUM) has grown from roughly $100 million to about $500 million in recent years, with a long-stated goal of reaching $1 billion. But he says the motivation behind that target has shifted. What began as an ambitious number he wrote down in his early 20s has evolved into a measure of how many retirements he can help steward over decades.

“I take assurance in knowing that I’m trying as hard as I can for the people we’re helping”

MATTHEW CUPLIN, MIDWEST FINANCIAL GROUP

That long-term commitment is rooted in a line he discovered in his great-grandmother’s journal: “You help other people get what they want, and you’ll get what you want tenfold.” For Cunningham, the compounding effect of that philosophy shows up less in asset totals than in something harder to quantify, clients who keep showing up or referring others.

Faiza Kedir: disciplined strategy meets human connection Managing director and partner at Steward Partners (Florida)

Clients don’t just come to Faiza Kedir for asset allocation or tax ef ciency; they come because she makes a point of understanding the people behind the balance sheets – their families, aspirations, and the legacy they hope to leave.

In a business that can default to spreadsheets and product menus, she positions herself as a longterm partner in her clients’ nancial lives. “Clients appreciate having someone who listens carefully, explains complex topics clearly, and helps them make thoughtful decisions during both calm and uncertain markets,” she says.

That philosophy has been stress tested over the past 12–18 months, as investors have navigated in ation worries, rate moves, and intermittent bouts of volatility. Rather than chase headlines or try to outguess every twist in the news cycle, Kedir has doubled down on fundamentals: a disciplined plan and the emotional discipline to stick with it. She emphasizes diversi ed portfolios, regular checkins on risk tolerance, and a cadence of proactive communication so clients understand not only what they own but also how each piece supports their objectives. Industry research continues to back that approach; investors with a written nancial plan report higher con dence and are less likely to make panic-driven changes during market swings.

Adaptability has been another de ning theme in Kedir’s recent work. She notes that markets, regulations, and client circumstances are in constant motion and that effective advice requires both technical uency and the willingness to adjust as life changes. In one recent case, a newly retired professional was shifting from accumulation to income. Rather than focus narrowly on withdrawal rates, Kedir designed a comprehensive roadmap that integrated retirement cash ow, tax strategy, estate planning, and charitable goals, giving the client clarity not only on “how much” to draw but also on how their money could support the causes and people they care about over time.

She cites the example of a recently retired professional transitioning from accumulating wealth to generating sustainable income. “Together

Percentage of respondents

we developed a comprehensive plan addressing retirement income, tax considerations, estate planning goals, and charitable giving priorities,” Kedir says. “While every client situation is unique, this re ects my philosophy of thoughtful planning and long-term partnership.”

Source: The Financial Planning Longitudinal Study

between professionals who won’t take ownership. That positioning is increasingly powerful in a landscape where tax ef ciency has become a central value driver for RIAs, with industry research highlighting tax-aware strategies as a key competitive edge in attracting high-net-worth clients.

Trevor

Scotto:

selling simplicity Partner at Fiduciary Financial Group (California)

By the time many wealthy retirees reach Trevor Scotto’s of ce, they are worn out from juggling a disjointed cast of CPAs, advisors, and specialists who never seem to be on the same page. Scotto’s differentiator is that tax and wealth management quite literally sit at the same table. Drawing on his own deep tax background, he and his in-house CPAs handle the heavy technical lifting, translating the results into plain English.

The same ethos has guided Scotto’s approach through the last year of market turbulence. Rather than reacting to every headline, he leans on a risk capacity, needs-based framework that starts with what a family actually requires to fund retirement and then works backward. It is an intentionally objective philosophy designed to strip out the emotion that so often derails investors. Once the plan is in place, the mandate is to stay disciplined, keep scanning for nancial and tax planning opportunities, and let clients focus on living their lives. Recent investor surveys suggest that advisors who proactively communicate around volatility and connect portfolio moves to long-term income needs enjoy signi cantly higher loyalty from retirementage clients, validating Scotto’s approach.

Clients receive high-level, integrated planning without having to decode acronyms or referee

Over the past year, one lesson has crystallized for Scotto: as wealth and business scale, the hunger for simplicity has to grow in parallel. Having recently crossed $1 billion in AUM while raising

FAIZA KEDIR, STEWARD PARTNERS

“Successful financial planning is not about predicting markets – it’s about building a thoughtful strategy that helps people live the life they want with confidence and clarity”

Scotto is part of this trend, as he, along with his team, uses a suite of AI tools to capture pristine meeting notes and automate documentation, particularly on complex retirement and tax plans where missing a detail can be costly. He says, “Right AMERICANS WORKING WITH CFP® PROFESSIONALS ARE CONFIDENT THEY WILL ACHIEVE THEIR

three young children, he has become even more convinced that time is the only truly non-renewable asset. That insight shapes both his rm and his life. He has surrounded himself with what he calls “insanely intelligent” specialists and built a culture where complexity is managed centrally so clients don’t have to carry it.

A recently retired couple illustrates how that plays out. For years, their advisor told them to “ask the CPA,” while the CPA sent them back to the advisor, promising strategies surfaced but were never implemented, and tax advice focused narrowly on the current year. Scotto’s team ended the ping-pong immediately. With tax and wealth experts in one room, they combed through the couple’s balance sheet, designed a uni ed, needsbased portfolio, executed a Roth conversion strategy, consolidated scattered retirement accounts, harvested tax losses and gains, updated bene ciary designations to match new legacy goals, and built a straightforward Social Security plan. What had been a source of frustration became a coherent, actionable roadmap.

AI is moving quickly from experiment to embedded tool. A 2026 Schwab study of RIAs found 63 percent of advisors are already using AI, most in early stage or “test and learn” mode, with the biggest impact showing up in administrative work and client communications rather than in pure investment selection.

now we use Gemini, Jump AI, and Contio, and we are also dipping our toes into Hazel AI.”

With the machines handling accuracy and admin, Scotto is able to be fully present in the room, asking better questions, spotting planning opportunities in real time, and maintaining the proactive engagement clients value most.

While Kedir incorporates portfolio management platforms, planning software, and secure portals to monitor accounts, model “what if” scenarios, and keep clients engaged. “Technology remains a tool – human judgment and experience are essential when guiding clients through complex nancial decisions,” she says.

This chimes with the market, as the Natixis 2025 global survey of individual investors shows only 40 percent say they trust algorithms and AI to support their nancial decisions, and separate research

nds nearly six in 10 expect the future of advice to be a human–AI partnership rather than a handoff to machines.

Advisory work has long been portrayed as a solo profession, but the data show a clear payoff toward team models.

Cuplin frames his own success as inseparable from his team. Clients go through the same disciplined process with outcomes tailored by other advisors, plus specialists in taxation, insurance, and administration. That structure creates deliberate redundancy – the “next person in line” can pick up right where he left off – giving clients continuity and peace of mind if life happens to any one advisor.

“The biggest lesson over the past year has been realizing that as wealth and business grow, your appetite for simplicity has to grow right alongside it”

TREVOR SCOTTO, FIDUCIARY FINANCIAL GROUP

Consolidating into a single agship of ce has ampli ed the bene ts: ef ciency is higher, “sharing of ideas” is easier, and the culture of camaraderie is now something clients can feel as they meet, in one place, a CPA for tax planning, a Medicare specialist, and other experts in an unusually polished but accessible setting designed for “millionaires to missionaries” alike. Emotionally, the team also helps him carry the weight of dif cult cases; having trusted colleagues to “bounce things off” matters when clients are facing illness or major life shocks.

Studies echo the advantage, with an analysis by Cerulli highlighting that team-based practices generate higher median AUM per advisor ($100 million versus $72 million for solo models) and are better positioned to offer a wider range of planning and high net worth services.

And Cunningham takes a similarly intentional approach. He insists every new prospect meeting includes at least two advisors so clients feel they are “working with a team,” typically pairing himself with a partner or junior planner. For households with more than $5 million in liquid assets, he extends that model into a dedicated family of ce group, ensuring multiple specialists are in the room for key decisions.

Client bene ts are both practical and emotional: broader listening, more perspectives, and better risk management during the volatile periods he calls “go time” for proactive outreach. Clients see that someone will always answer the phone and that their portfolio is backed by an actively managing investment team rather than a single decision-maker.

For Cunningham himself, the team model has improved close rates, exposed his own blind spots, and created a scalable path toward his billion-dollar AUM ambition. “What I’ve found is that 50 percent of something is better than 100 percent of nothing. It goes back to that quote ‘If you want to go fast, go alone. But if you want to go far, go with somebody else.’”

RJ Cunningham

Financial Advisor–Senior Partner

Summit Global Private Wealth

Phone: 385 509 0901

Email: rj@sgipw.com

Website: sgipw.com

Matthew Cuplin

Chief Executive Of cer/President

Midwest Financial Group

Phone: 608 807 4775

Email: matt@mfgteam.com

Website: mfgteam.com

Scott Van Den Berg

President Century Management Financial Advisors

Phone: 512 636 2026

Email: svandenberg@centman.com

Website: centman.com

Trevor Scotto

Partner

Fiduciary Financial Group

Phone: 415 578 6630

Email: tscotto@ffgwealth.com

Website: ffgwealth.com

Faiza Kedir

Managing Director and Partner Steward Partners

Phone: 941 217 7016

Email: faiza.kedir@stewardpartners.com

Website: sunshineprivatewealth.stewardpartners.com

Gideon Drucker

President and Chief Executive Of cer Drucker Wealth

Phone: 212 681 0460

Email: gideon@druckerwealth.com

Website: druckerwealth.com

Kate Feeney

Vice President and Wealth Advisor

Summit Place Financial Advisors

Phone: 908 517 5882

Email: kate.feeney@summitplace nancial.com

Website: summitplace nancial.com

Signature Estate & Investment Advisors, LLC (SEIA)

Phone: 310 712 2362

Email: mhurtienne@seia.com Website: seia.com

Robert Westley

Regional Wealth Advisor Northern Trust

Phone: 212 339 7293

Email: raw8@ntrs.com Website: northerntrust.com/united-states/home

Sammy Grant Senior Wealth Advisor and Shareholder HB Wealth

Phone: 404 459 0027

Email: sammy.grant@hbwealth.com Website: hbwealth.com

Thomas M. Dowling Head of Wealth Management Alliance Global Partners of the Lowcountry

Phone: 843 420 1993

Email: tdowling@allianceg.com Website: agplowcountry.com

Aaron Brachman Steward Partners

Adam Glassberg Savant Wealth Management

Anthony Consiglio Baird

Anthony Gerbi Stein Financial Group

Becca Mathis

Jeter Hrubala Wealth Strategies

Caitlyn Salloum Key Wealth Management

Carl Gravina Steward Partners

Carson Odom

Adams Wealth Partners

Chad Osmanski Baird

Charles Cooper III StrongBox Wealth

Christopher Crotty

Ameriprise

Christopher Detmer

Steward Partners

Christopher Ruedi

Savant Wealth Management

Corey Briggs

Plaza Advisory Group

Courtney Shrewsberry

Steward Partners

Danilo Kawasaki

Gerber Kawasaki Wealth & Investment Management

David Johnson

Signature Estate & Investment Advisors (SEIA)

DeHaven Becker

Steward Partners

Dominic Hubert

Schmidt Financial Management

Doug Peterson

Adams Wealth Advisors

Evan Schmidt

Schmidt Financial Management

Gary Williams

Williams Asset Management

George Nottingham

Steward Partners

George Webb

Pension & Wealth Management Advisors

Giancarlo Troncoso

Jaffe Tilchin Wealth Management

Greg Bogdan

Private Vista

Greg Giardino

Wealth Enhancement

Gregory Armstrong

Armstrong Dixon

Gregory Kurinec

Pennant Planning

Hannah Varnado

Wood Opal Financial Advisors

James Sahagian

Steward Partners

Jared Hoole

Lakeside Financial Planning

Jason Botten eld Steward Partners

Jason VanDuyn

AQuest Wealth Strategies

Jeremy DiTullio

Cleveland Financial Group

Joe Breslin

Armstrong Dixon

Joe Cilley

Merit Financial Advisors

John Ferguson

Steward Partners

John Litscher

The Capital Group

John Loyd

The Wealth Planner

Joseph Goldfeder

Valley National Financial Advisors

Julie Hall Labrune

Vision Capital Partners

Kathy Longo

Flourish Wealth Management

Keith Barberis Steward Partners

Kerry Meath-Sinkin

Meath Wealth Advisors

Lawrence Sprung

Mitlin Financial

Libby Muldowney

Savant Wealth Management

Louis Barajas International Private Wealth Advisors

Matt Parenti

Private Vista

Max Baer

Merit Financial Advisors

Michael Addessi

Addessi Financial Partners

Michael Englehart

Steward Partners

Michael Randall

Oak Summit Wealth Management

Miriam Falaki

Savant Wealth Management

Myles Zueger

Adams Wealth Partners

Navarone Simpson

Armstrong Dixon

Oliver Kollofski

Sweet Financial Partners

Ralph Leopold

Ameriprise

Rob Howland

Howland and Associates

Schuyler Engelhardt

Armstrong Dixon

Scott Gaynor

Navalign Wealth Partners

Sharon Nassir AIRE Advisors

Stephanie Petrosini

Morgan Stanley

Thomas Pontius

Kayne Anderson Rudnick

Tim Lonergan Westmount Partners

Todd Bryant

Signature Wealth Partners

Tucker Dunn

Armstrong Dixon

Wayne McCormick

Steward Partners

William Rodriguez

Briggs Wealth Management

CEO Jeff Dekko’s secret to growth? Keep building and never set a target

BY GREGG GREENBERG

JEFF DEKKO joined Wealth Enhancement as CEO back in 2003 when it was a regional advisory business with $600 million in AUM. Now, it’s a national firm with over $143 billion.

Not that he had a target number in mind, mind you.

“I was asked early on, ‘How big is big enough?’ and my answer was always the same: high-quality companies don’t set an end number. They focus on building something that lasts,” Dekko says.

For Dekko, that meant building a quality business centered on comprehensive financial planning and a client-first mindset. All that growth, in other words, has been a by-product of operating with a laser focus on those two areas.

ABOUT JEFF DEKKO

Assumed role as CEO of Wealth Enhancement in 2003

Prior to Wealth Enhancement, held key strategic and marketing roles at Fortune 500 companies such as General Mills

Serves on the board of trustees for the United States Ski and Snowboard Association

Enjoys fly fishing, hiking, and backcountry skiing

Currently trying to complete six marathons over the course of a year and a half

Earned MBA in finance and strategy from the University of Chicago Booth School of Business

Not that he hasn’t done his fair share of strategic corporate construction as well. Under Dekko’s leadership, Wealth Enhancement has completed over 100 strategic acquisitions, a sizable number even if he’s not counting, which, once again, he’s not.

If a deal is sensible and serves the firm’s stakeholders then he’ll make it. If that’s not the case, then he’ll wait for the next one to come along. And considering the red-hot, private equity−fueled M&A environment in the RIA space, suffice to say the wait has not been that long of late.

“We are thinking about clients, employees, and shareholders alike, not just the owners of the firm. Supporting all three in a balanced way is what drives better outcomes for clients and leads to sustainable growth. Over time, that approach has allowed us to expand well beyond our Minnesota roots into a truly national firm, while staying grounded in the same core principles we started with,” Dekko says.

Despite his dealmaking skills, Dekko was not a Wall Street investment banker prior to joining Wealth Enhancement. In fact, he spent over a decade as a marketing executive at General Mills and Recovery Engineering before getting into the wealth management business. And it was building all those brands as a marketer that helped shape his thinking about the RIA business from the very beginning.

“At General Mills, there was a strong focus on understanding your audience, and being clear about who you’re trying to serve, then building around their needs. That client-centric mindset translated directly into how we’ve built Wealth Enhancement,” Dekko says.

It also influenced how he thinks about growth. Rather than relying on a single source, Wealth Enhancement has built a diversified approach to marketing and lead generation that supports advisors and creates more consistent, long-term growth.

“For us, it is not about replacing personal service with digital. It is about using technology to strengthen it and ultimately deliver better outcomes for clients”

And speaking of growth, what about all those acquisitions? What in fact does Dekko look for in a partner?

“We pursue acquisitions to grow our reach and strengthen our team and capabilities so we can ultimately help more people. When we evaluate a firm, we start by looking for those that truly put clients and employees first, with a culture that reflects that in both words and actions,” Dekko says.

As for the advisors joining Wealth Enhancement, Dekko says they gain the ability to maintain and expand their promises to their clients by gaining access to the resources, infrastructure, and scale of a national organization.

Emphasizes Dekko: “At the end of the day, we see every acquisition as a long-term partnership,

where the commitments those firms have made to their clients become shared commitments moving forward.”

ORGANIC GROWTH COUNTS TOO Sure, Dekko does a lot of valuation exercises when acquiring a new advisor team. That’s literally part of the deal. But he also sees value in the relationships his advisors have with their clients, something that is far harder to hang a number on.

“Those relationships are an incredible asset, and we see a real opportunity to help advisors deepen them over time while also building new ones,” Dekko says.

Additionally, Wealth Enhancement has always had a strong marketing capability, which ties back

“When we evaluate a firm, we start by looking for those that truly put clients and employees first, with a culture that reflects that in both words and actions”

to his background as a consumer marketer. And it was one of the things that attracted him to the firm early on. That’s why he continues to invest in that capability in order to generate interest and connect with prospective clients, creating a steady flow of opportunities for our advisors.

“Many advisors see a meaningful acceleration in net asset flows after joining us, which reflects the strength of that engine,” Dekko says.

They also maintain relationships with custodial referral partners, which can be an important source of growth. At the same time, the firm has been very intentional about building a diversified portfolio of growth opportunities so they are not dependent on any single channel, which is where some firms can get challenged.

“We’re bringing new assets from multiple sources, not just relying on their programs. It needs to work for everyone, starting with the client, and then for the custodian and for us,” Dekko says.

Over a year ago, Dekko began taking prompt engineering courses because of his belief that AI is going to transform the business world. Put simply, if he expected the organization to embrace AI, then he felt obligated to learn it himself.

“In many ways, I think of AI skills today the same way we once thought about basic software skills like email, spreadsheets, and presentation tools. At one point, those were specialized capabilities. Today, they are simply part of how everyone gets their work done. I believe AI will follow a similar path, becoming a core skill set across roles and functions. My goal is to build a company where everyone has that level of capability,” Dekko says.

Nevertheless, while jumping into AI with both feet, Dekko also wants his employees to

remember where AI fits in Wealth Enhancement’s business.

“For us, it is not about replacing personal service with digital. It is about using technology to strengthen it and ultimately deliver better outcomes for clients,” Dekko says.

And just because he’s investing in technology does not mean he’s simultaneously scrimping on employees new and old. In Dekko’s opinion, attracting great talent starts with culture and extends to creating long-term alignment. To get everybody on the same page, Wealth Enhancement offers employees the opportunity to participate in equity.

“It’s not just about advisors. We invest in our corporate teams as well to strengthen capabilities across the organization, and we maintain a strong internship program to help build the next pipeline of talent,” Dekko says, adding that what he enjoys most about his role is working with interns, advisors, and all the other members of his team.

In a word: People. Not numbers.

“Earlier in my career, I was marketing inanimate products. They never had opinions. Today,

Founded in 1997

Headquartered in Plymouth, Minnesota

Provides wealth management services to over 82,000 households

182 offices nationwide

$143 billion in total client assets

Over 1,800 employees

I get to work with talented people who have strong ideas, perspectives, and a real passion for what they do. The leadership challenge, and the reward, is bringing those ideas together in a way that unifies us around a shared vision,” Dekko says.

Advisors discuss their use of AI now and how it will change going forward

BY GREGG GREENBERG

The numbers clearly show that wealth managers are moving toward an AI future.

They also show that – at least for now –they don’t know how to get there.

Approximately 95 percent of financial services and wealth management professionals plan to increase AI investment in the next three years, and 68 percent consider it important for future competitiveness, according to MSCI’s Wealth Trends 2026 report.

Nevertheless, despite that overwhelmingly supportive forecast surrounding the future adoption of AI, the MSCI study, which surveyed 250 wealth managers worldwide, indicated that many financial advisors are still unsure of how to best integrate the technology into their practices. While nearly all firms plan to increase investment in AI tools, the report showed that 44 percent believe the wealth segment’s AI adoption rate lags the broader financial services industry. Furthermore, only 27 percent feel wealth managers are leading the rest of the industry.

“I’m surprised many advisors say AI isn’t critical yet,” says Michael Mignosi, senior director of organic growth at Perigon Wealth Management. “Wealth management is still fundamentally a relationship business and technology doesn’t replace trust, but it certainly helps on many levels.”

Early on, Mignosi used AI mainly for productivity, such as content drafting, research, and helping advisors translate complex financial topics into clearer client communication. Now, he’s moving toward a more architectural approach, connecting AI across systems so that better data at the prospecting stage can inform onboarding and ultimately create more personalized client experiences.

“We approach AI with continuous experimentation and a scientific mindset. The goal isn’t just adopting tools but learning quickly and reducing

the technology fragmentation that has slowed innovation in our industry,” Mignosi says.

Meanwhile, Jason Hanavan, president and CFO at VestGen Wealth Partners, utilizes AI to identify M&A targets, recruit advisors, and drive strategic growth, while his advisors use it for notetaking, follow-ups, and task management after meetings with clients and prospects.

“Our AI tool integrates with our CRM, performance reporting system, and planning software to deliver a comprehensive data view. Our technology team uses AI to execute certain data migration tasks related to custodian and CRM data,” Hanavan says.

Elsewhere, Jacob Roos, a financial advisor with 49 Financial, is using AI most intentionally on the

“We view AI as a tool that increases advisor capacity to be able to provide services to more clients”

JASON HANAVAN, VESTGEN WEALTH PARTNERS

learning and development side of the business. He recently launched a tool called Virtual Coach, an AI-powered practice environment where advisors and leaders can rehearse client conversations with an avatar trained on the firm’s language and methodology.

“On the client side, I also use tools like Finmate to capture notes, key numbers, and specific quotes during conversations,” says Roos. “That allows me to stay fully present in the discussion, ask better

HOW ADVISORS USE AI NOW

Identify M&A targets

Recruit advisors

Notetaking, follow-ups, and task management after meetings Content drafting

Research

Translating complex financial topics

follow-up questions, and focus on what the client is actually saying rather than worrying about documentation.”

When it comes to budgeting for AI investments, Tim Thornberry, financial planner at Prudential Advisors and founding partner of Cornerstone Financial Partners, says he measures AI investment by what it unlocks, not what it saves. In his view, the real return is an advisor who can think more deeply, analyze more rigorously, and deliver better outcomes for clients.

“That’s the lens we apply,” Thornberry says, adding that the enterprise’s investments also give his team access to sophisticated tools without

bearing the full cost, enabling him to “focus our own spend where it directly improves client experience.”

Perigon’s Mignosi, for one, does not treat AI as a separate budget category. It’s increasingly embedded across his technology stack, from marketing tools to CRM and data infrastructure.

“One advantage we have is agility. At our size, we can move faster than many larger, more traditional firms that are constrained by layers of legacy systems and red tape,” Mignosi says.

His approach is to test new capabilities, measure the impact, and scale what works. If it helps advisors prospect more effectively, improves the client experience, or frees up advisor bandwidth for more meaningful conversations, it earns a place in his stack.

For his part, VestGen’s Hanavan is more than doubling the amount of third-party spend on AI tools in 2026, and he expects to continue to increase this investment in the coming years.

“We view AI as a tool that increases advisor capacity to be able to provide services to more clients,” Hanavan says.

And then 49 Financial’s Roos views AI as an accelerator embedded across multiple functions, including training, advisor productivity, and client engagement. And because the space is evolving quickly, he’s less focused on large upfront investments and more on iterative adoption − or, more specifically, on testing tools to see what’s working and scaling the ones that demonstrably improve advisor effectiveness or client experience.

Looking out a decade from now, Mignosi thinks AI will ultimately make the human side of advice even more important. As AI automates research, preparation, and documentation, he sees it freeing

“Ultimately, I see AI strengthening the human side of the profession rather than replacing it. The advisors who win in that future will be the ones who use technology to deepen relationships, not distance themselves from them”

JACOB ROOS, 49 FINANCIAL

advisors to spend more time understanding clients and guiding them through important financial decisions. He also foresees a shift in how trust is built between advisors and clients, as well as prospects.

“Historically, firms relied heavily on thought leadership content to demonstrate credibility. But with AI, everyone can generate expert-level information instantly. Clients and prospects are already coming to meetings with more sophisticated questions because they’ve explored topics through AI. When everyone can sound like an expert, the real differentiator becomes the human dimension,” Mignosi says.

Similarly, over the next decade, Roos thinks AI will increasingly handle the operational load that has historically consumed much of advisors’ time, which will free them up for more client-facing, relational work, “which is what clients really value.”

“Ultimately, I see AI strengthening the human side of the profession rather than replacing it,” Roos says.“The advisors who win in that future will be the ones who use technology to deepen relationships, not distance themselves from them.”

Finally, Cornerstone’s Thornberry thinks the advisors who win in the end won’t be the ones who

Freeing advisors to spend more time with clients

Strengthening human side of wealth management

Enabling better thinking, deeper planning, and lasting results for clients

Increasingly handling operational load

adopted AI first. They’ll be the ones who learned to ask better questions with it.

“For us, AI’s biggest promise is connecting the dots across tax planning, business succession, estate strategy, and investments − faster and more precisely than ever before,” says Thornberry. “The goal is always the same: better thinking, deeper planning, lasting results for our clients.”

Artificial intelligence could revolutionize how Americans receive financial advice by freeing advisors up to provide support to huge swaths of the population

BY ANDREW COHEN

As wealth management firms experiment with artificial intelligence, Orion CEO Natalie Wolfsen believes the technology could dramatically scale the advisory model − potentially doubling the number of Americans who receive financial advice.

“Personally, I want AI to increase our output. I want it to increase advisors’ productivity. Right now, about 20 percent of Americans benefit from advice, and if I can double every advisor’s productivity, then that means that 40-plus percent of Americans can benefit from advice,” Wolfsen tells InvestmentNews

A 2024 survey from YouGov found that 27 percent of Americans work with a professional financial advisor. Orion launched the enterprise version of its Denali AI for advisors earlier this year, opening the software to Orion’s ecosystem that spans $5.8 trillion in platform assets and $133 billion in wealth management assets across thousands of advisors and eight million end-client accounts.

“For me, it’s not about eking out an extra couple of dollars or an extra couple of points in margin, but instead, can I take functions of Orion and functions of advisory businesses and double the productivity in that area,” says Wolfsen.

Advisors using Orion had a 2025 organic asset growth rate that was approximately 40 percent higher than that of non-Orion client advisors, according to Orion’s Advisor Wealthtech Survey Orion has also debuted its AI-powered Report Assistant to draft automated reports for clients and its Query Studio assistant that lets operations teams ask questions in plain English to pull complex data.

“We know that this will replace this swivel chair that advisors have, where you go into your research, and then you go into your custodial system, and then your financial planning system, and then

your trading system, and then your portfolio construction system, and then your reporting. All of that information can be put in Denali AI, and then actions can be started and questions can be answered using this tool,” says Wolfsen.

All Orion employees have been tasked with individual “AI goals” for 2026. While some newer RIA startups believe AI can fully automate investment

portfolio decisions, Orion views the tech as being more limited to streamlining research and data entry.

“A lot of the basic work that goes into portfolio construction, like evaluating securities and evaluating scenarios, that’s really where the tools are able to help. Making the recommendation or making the decision, to me, that’s still very much an advisory act,” says Wolfsen.

“If I can double every advisor’s productivity, then that means that 40-plus percent of Americans can benefit from advice”

NATALIE WOLFSEN, ORION

ADVICE ADOPTION

A 2024 YouGov survey found 27 percent of Americans work with a professional financial advisor.

ADVISOR PRODUCTIVITY

Advisors using Orion had 2025 organic asset growth about 40 percent higher than non-Orion client advisors, according to Orion’s Advisor Wealthtech Survey

ADVISOR WORKFORCE OUTLOOK

• McKinsey & Company projects a shortage of roughly 100,000 advisors in the US wealth management industry by 2034.

• Mariner Wealth Advisors reported 30 percent organic growth from 2024 to 2025 while expanding AI-enabled advisor workflows.

Orion had previously planned to have a wealth innovation lab in San Francisco, but it has now pivoted to innovation hires in multiple locations − Omaha, Nebraska; Jacksonville, Florida; and Lehi, Utah, rather than concentrating them in a single San Francisco hub.

“Going into the AI innovation lab, we thought it would be great to have a team of people co-

located in San Francisco working on nothing but AI. Instead, we found we need AI capabilities across all of Orion, because the whole company needed to transform to an AI-native company,” says Wolfsen.

“So we pivoted, and we’ve hired the AI innovation resources, but instead of hiring them in one location, we’ve hired them in multiple

“AI will reshape the advisor workforce by making advisors more capable and scalable. It will also accelerate training and development”

KENNY POINTER, MARINER WEALTH ADVISORS

locations. Now, all of Orion is transforming into an innovation lab, rather than having a smaller, highly competent resource group do it.”

Orion touts having 17 of the top 20 largest RIA firms as clients, including its addition of Edelman Financial Engines announced in January. Another mega-RIA client of Orion is the Kansas-based RIA roll-up firm Mariner, which integrates its own AI tools for advisors on top of Orion’s wealthtech layer.

“Orion is part of our core infrastructure layer, helping organize and unify data,” says Mariner’s chief innovation officer, Kenny Pointer. “Our advisor-centric AI tools − like Sherpas, Zocks, LLMs − sit on top of that foundation to automate workflows and generate insights.”

The family office of Mariner Wealth Advisors founder and CEO Marty Bicknell, 1248, is a lead investor in AI startup Sherpas. About 125 Mariner advisors are using Sherpas, which automates the investment proposal process for prospective clients.

“Advisors are using Sherpas to accelerate the path from an initial prospect conversation to a personalized, high-quality recommendation. It automates much of the analysis and proposalbuilding process, reducing turnaround time from days to hours, while allowing the advisor to guide the strategy and final output,” says Pointer.

The tech stack for Mariner Wealth Advisors also includes meeting management via AI assistant Zocks and back-office automation from Humanity Labs. Mariner reported a 30 percent organic growth increase from 2024 to 2025 and said AI could help offset the roughly 100,000advisor shortage that McKinsey & Company projects for the US wealth management industry by 2034.

“AI will reshape the advisor workforce by making advisors more capable and scalable. It will also accelerate training and development, enabling more professionals to step into clientfacing roles and helping to address the industry’s looming advisor shortage,” says Pointer.

The prime minister of Antigua and Barbuda says the country is undergoing a renaissance and there has been an increase in American investment, from both developers and high-net-worth individuals

BY JAMES BURTON

The imposing cruise ships docked in St. John’s, Antigua, loom over the lowincome neighborhood of Point. A drive through these old, working-class streets contrasts sharply with the shiny, multimilliondollar floating towns. But rough-and-ready does not mean a lack of aspiration − just ask Gaston Browne.

The prime minister of Antigua and Barbuda, and leader of the Antigua and Barbuda Labour Party, grew up in Point, represents the area in parliament, and is the person responsible for transforming parts of it with overseas investment.

InvestmentNews spoke to him just before he dissolved parliament and announced a general election, seeking a fourth term in power. Attracting outside investment remains a core policy and a central part of his plan to build Antigua and Barbuda into a “lifestyle superpower” − one that can enrich the local community and attract wealthy Americans seeking both yield and quality of life.

From his office in St. John’s − a short ride but seemingly miles away from his humble Point beginnings − Browne opens his arms to the global elite and expresses confidence the country’s current phase will go down as a renaissance, not a bubble.

The bullishness of the prime minister, who entered politics after a career in banking, stems from what he believes is a sharp reversal of fortune under his watch. When his Labour Party returned to office in 2014, Antigua and Barbuda had just come through what he calls “total decay” − fiscal distress, crumbling infrastructure, and a 25 percent loss of gross domestic product between 2009 and 2014. Today, he argues, the macro picture has flipped in ways that matter to investors as much as to voters.

“When we came to office, there was total decay within our country,” he says. “There was infrastructural decay, social decay, economic decay, environmental decay.” Debt-to-GDP hovered around 104 percent. The country was in an IMF program.

In 2026, Browne reels off a list of his government’s accomplishments. Debt-to-GDP has fallen from about 104 percent to roughly 62 percent, close to international benchmarks; employment is up; and Antigua has recorded budget surpluses for the

past several years. He says these surpluses will be plowed into infrastructure and social programs designed to raise long-term productivity.

The macro repair job underpins an aggressive push upmarket. “We are transforming Antigua and Barbuda into an economic power in the Caribbean − what we consider to be a lifestyle superpower,” Browne says. And the focus is on luxury: “We’re not particularly keen on these low-end hotels.”

The result is a busy development pipeline. On Barbuda, the PLH development alone has attracted about $1 billion so far, and, Browne says, it “boasts some of the wealthiest people in the world.”The project is anchored by a Tom Fazio golf course, surrounded by nearly 300 degrees of beach and designed with native species and

shoreline engineering to reduce storm risk on an island that is naturally flat.

Robert De Niro’s Nobu resort is expected to open on Barbuda by late this year or early next, joining a slate of other approved luxury brands now completing environmental studies and preparing to break ground.

On Antigua itself, projects associated with Nikki Beach, One&Only, and Marriott are in various stages of land preparation and construction.

WHY THE WEALTHY ARE PAYING ATTENTION Browne makes the pitch that, per capita, “there’s no other destination in the Caribbean that has more luxury properties than Antigua and Barbuda,” and that the country has “attracted more billionaires

“Generally speaking, we keep out of geopolitical spats and we don’t want to get in the crosshairs of anybody. But, yes, we are seeing an increase from American applicants”

Gaston

Browne, prime minister of Antigua and Barbuda

“We are transforming Antigua and Barbuda into an economic power in the Caribbean”

Gaston

Browne, prime minister of Antigua and Barbuda

and multimillionaires than any other, per capita” in the region.

Antigua offers “very attractive concessions” for people building luxury homes, hotel properties, or any significant capital project, from duty-free treatment on building materials, fixtures, and fittings to broader investment incentives. The aim is to reduce upfront costs and compress payback periods in a small market where scale is finite but margins can be attractive.

Security is another part of Browne’s calling card. Antigua, he says, has “one of the lowest” levels of violent crime in the Caribbean, typically with no more than 10 homicides a year. Barbuda, with roughly 1,500 residents, has not had a homicide in more than four

decades. For clients accustomed to reading travel advisory headlines, he presents that as a core asset.

Two key elements may also stand out for US advisors evaluating Antigua and Barbuda as part of a broader wealth-planning strategy: citizenship by investment (CIP) and the personal tax regime.

Antigua’s citizenship-by-investment program, now about 13 years old, is explicitly framed as a tool “to de-risk investments” and provide constitutional protection to investors. Once investors are naturalized, “if the government wants to acquire any private property, it must be for public purpose and you must settle the full market value

Name: Gaston Browne

Born: St. John’s, Antigua Age: 59

Politics: Browne has been prime minister of Antigua and Barbuda since 2014. He was elected to parliament in 1999 and became leader of the Labour Party in 2012.

Career before politics: Commercial Banking

Manager, Swiss American Banking Group

Music: Browne writes and performs reggae under the name Gassy Dread.

immediately,” Browne explains. The constitution’s protection of private property, he notes, applies across both residential and commercial holdings.

The program also has a geopolitical dimension. Antigua does not process applications from individuals in sanctioned countries such as Iran and North Korea, and tends to “move in tandem” with the US and European positions when considering applicants from higher-risk states.

The conflict in the Middle East and the rise in oil prices have created economic uncertainty, but interest from the US remains strong. “Generally speaking,” Browne says, “we keep out of geopolitical spats and we don’t want to get in the crosshairs of anybody. But, yes, we are seeing an increase from American applicants.”

For developers, the citizenship-by-investment program can also be a funding tool. “You can literally use a CIP over a period of time to raise the capital,” he says, or “you can actually upfront the proceeds to build the hotel and then sell the units.”

For buyers, the structure offers real estate plus optionality. Investors purchasing qualifying units − typically at $350,000 or more − may be eligible for Antiguan citizenship as part of the package. “So it’s a win-win for everybody,” Browne says.

Tax policy is equally important. Within a year of taking office, Browne’s government eliminated personal income tax. The move, he says, was designed to increase disposable income, encourage saving and investment, and underpin what he describes as a “housing revolution” on the islands.

For individuals domiciled in Antigua, whatever you make, gross is net, although corporate tax is treated differently and set at 25 percent.

Behind the investor-facing messaging is a domestic development agenda that also reinforces Antigua’s appeal as a place to spend time, not just park capital. Browne is keen to emphasize that the lifestyle story is being built “for the benefit of our visitors, but for the locals alike.”

Housing, healthcare, infrastructure, and even the beautification of the landscape are all central pillars of the planned renaissance.

“In terms of the prospects of the country, I feel confident that Antigua has a very bright future ahead of it,” he says. “It’s a good time for investors to come and invest. A good time to acquire a luxury home.”

Antigua and Barbuda is clearly betting that its renaissance will show up on the next GDP chart − and on the balance sheets of those who invest early.