WEEKLY MARKETS REPORT

December 19, 2022

The Fed raised interest rate by .5% on Wednesday after the previous week’s PPI showed inflation weakening (slowly). The Fed did slow interest rate increases as the previous 3 rate increases were each .75%. The stock markets rallied after the interest rate announcement but turned sharply lower. The DOW, S&P 500 and NASDAQ all had higher highs,

Art Smith

Financial/ Equity Markets

Stocks

The Fed raised interest rate by .5% on Wednesday after the previous week’s PPI showed inflation weakening (slowly). The Fed did slow interest rate increases as the previous 3 rate increases were each .75%. The stock markets rallied after the interest rate announcement but turned sharply lower. The DOW, S&P 500 and NASDAQ all had higher highs, lower lows and lower closes on the week. The DOW settled on it previous trendline resistance, broken the first week of November. The S&P traded through its long-term resistance and then ended breaking a short-term and settling below that support. Is the stock markets’ rallies from their lows 2 ½ month ago over?

Interest Rates

This week’s calendar: U.S. Economic Calendar [Link]

Monday Fed’s 1 year inflation expectations (5.2% Nov vs 5.9% previous) Fed’s 10 year inflation

Bitcoin ended a relatively subdued rally since the first week on November.

Commodities

Metals, et. al.

In volatile trade Gold, Silver, Palladium, Copper and Aluminum were lower. Nickle higher in very volatile trade. Mid-West rolled steel and Iron Ore cif China were little changed. Lumber prices were lower; lowest since end of March 2020!

Ags Corn (Chicago) and CBOT Wheat were higher on the week, but still below their respective trend-line resistance. Kansa City Winter Wheat settled lower for the 7th week, just above its long-term supporting trendline. Soybeans were slightly lower with and Soybean Meal lower

after its previous week’s moonshot. Soybean Oil was higher and tested its resistant trend-line and failed.

Ethanol

Chicago Ethanol prices were higher $.02/gl

Natural Gas

Henry Hub NG was higher on the week, settling up $.304/MMbtu; above 21 and 50 day MA but still below its 100 day MA. The Snowmaggeddon forecast pushed the prices up to NG’s longterm resistance and then failed the end of the week; $.90/MMbtu price range on the week.

Dutch TTF and NBP were lower on the week and JKM prices continued higher. Dutch TTF (NWE) settled the week @$36.033/MMbtu (-$7.095), NBP settled @$35.01/MMbtu (-$7.59) and JKM settled @$35.546/MMbtu (+$3.18). US NG inventories declined 50Bcf; total stocks are now.5% below year ago and .4% below the 5-year average. Indonesian coal was higher after being sharply lower the previous week and South African coal was weaker for a second week.

Crude Oil and Refined Products Prices

The Petroleum markets were generally higher on the week! WTI and Brent were and HO, RB and GasOil were sharply higher after their 5 week selloff.

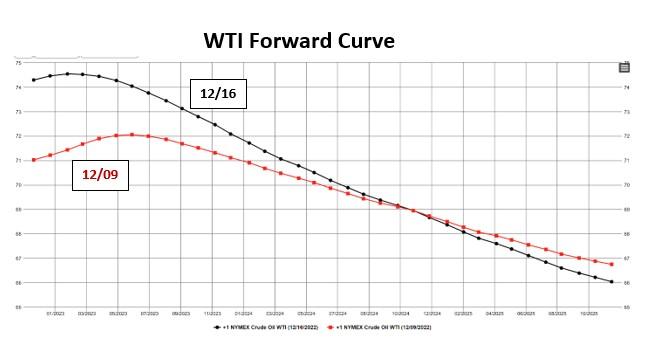

WTI settled @$74.29/bbl, higher on the week by $3.27/bbl, still above support ($67.64).

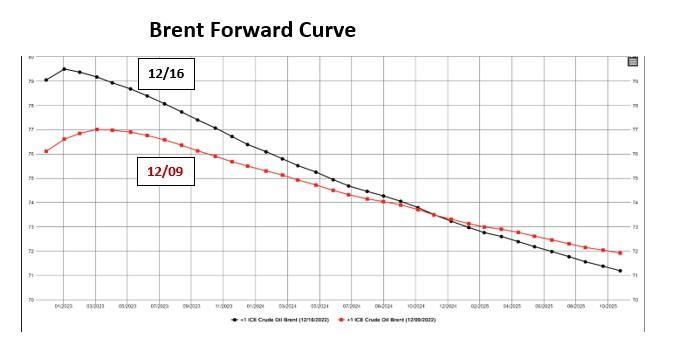

Brent settled @$79.04, higher on the week by $2.94/bbl, settling above support, after trading through it for a second week.

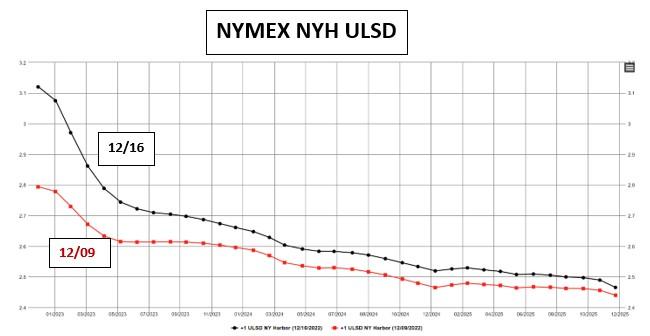

NYMEX LSD (HO) settled @$3.1199/gl, higher on the week by $13.70/bbl.

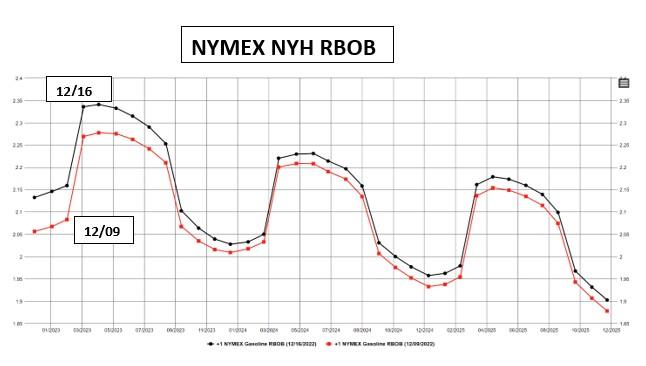

NYMEX RB settled @$2.1323/gl, higher on the week by $3.20/bbl

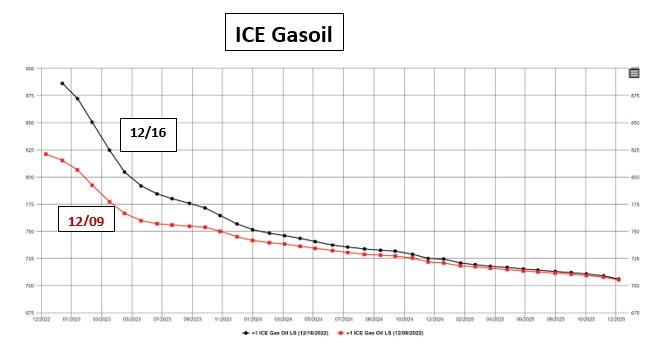

ICE GasOil settled @$886/tn, lower on the week by $8.267/bbl

Term structures (forward curves) were stronger the first 4 days of the weeks weak. The cracks were significantly higher for the first 4 days of the week but had a selloff on Friday.

The HO-WTI crack traded through resistance during the week but ended settling at that new support trend-line, selling off $5.66/bbl Friday. Short term correction in the cracks or a new move higher? Still waiting on the Hudson River ice flows down in NY Harbor?

Ukraine/Russia conflict is still a wild card! See Matrix Table below.

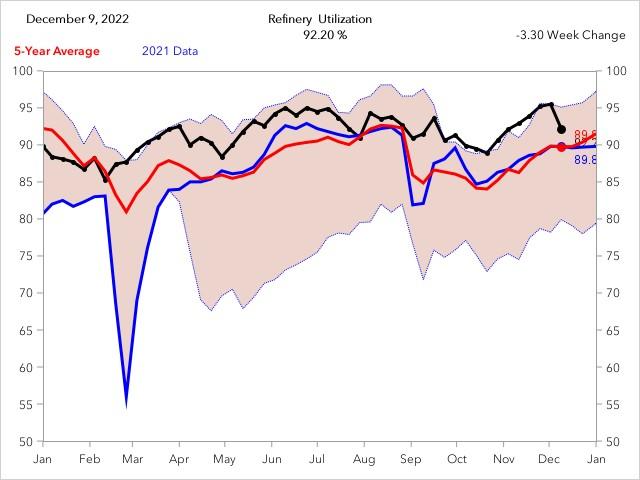

EIA

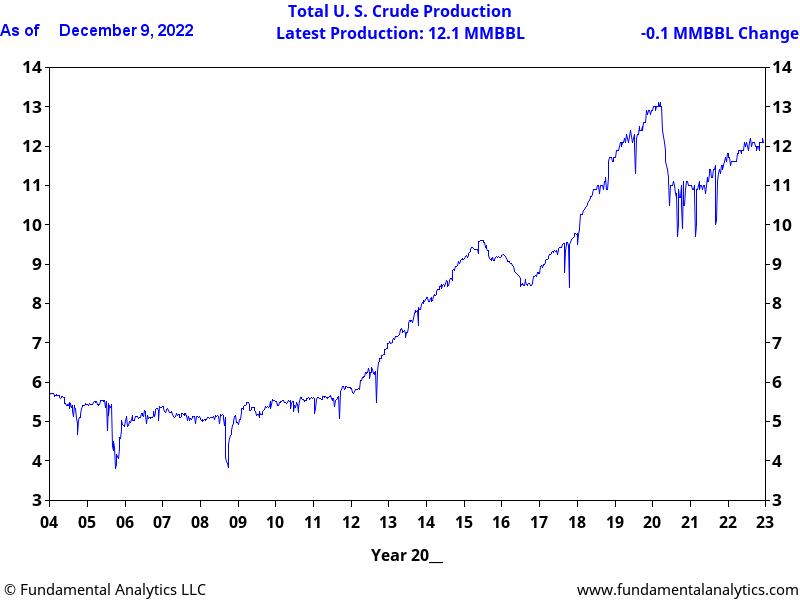

The EIA reported as of December 2, 2022 Crude

Crude Runs averaged 16.4MMbpd, which was 258kbpd higher than the previous week’s average [Link]

Refineries operated at 93.9% of their operable capacity.

Imports

Crude Imports averaged 7.1MMbpd, 1.5MMbpd higher [Link]

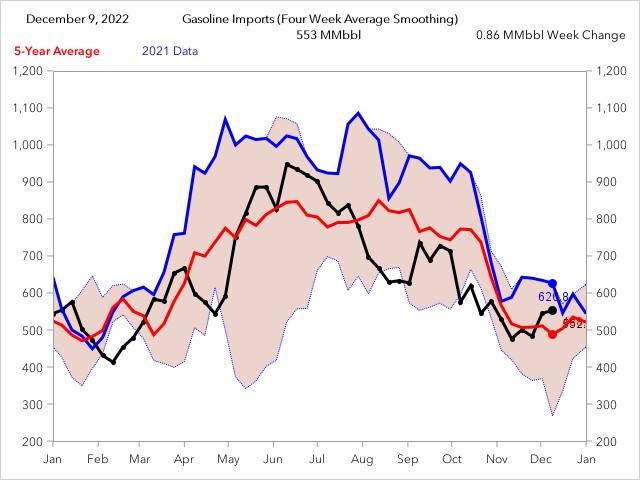

Gasoline imports averaged 585kbpd [Link]

Distillates imports averaged 128kbpd [Link]

Exports

Crude exports averaged 9.927MMbbls (+341kbpd) [Link]

Product exports averaged 5.685MMbbls (-340kbpd) [Link]

Stocks

Commercial crude oil inventories decreased by -3.7MMbls

(5% below 5 year avg.). [Link]

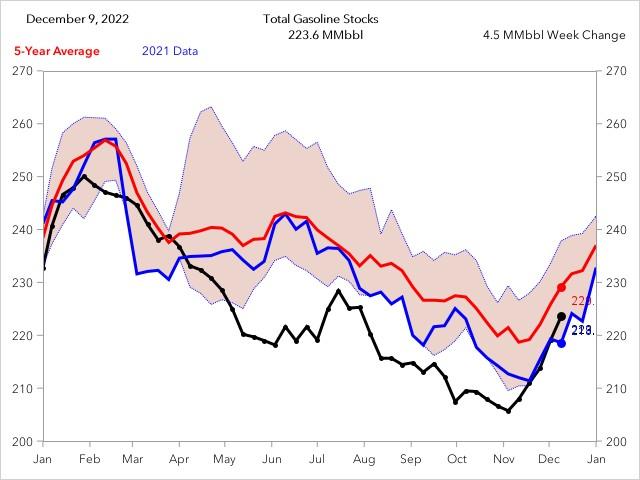

Gasoline inventories increased by 3.1 MMbbls (4% below 5 year avg.) [Link]

Distillate fuel inventories increased by 1.7MMbbls (13% below 5 year avg.) [Link]

The Baker Hughes Rigs Counts

Weekly Rig Count increased by 2 with Oil +4 and Gas -2. [Link]

3 -1-2 Crack