Spotlight on Senior Care M&A

The SeniorCare Investor is releasing a mid-year update of its key valuation statistics for the assisted living, independent living and skilled nursing sectors in its latest report: Spotlight on Senior Care M&A....

Read more on LevinPro HC

Evernorth invests in Shields Health

Evernorth Health Services, a subsidiary of The Cigna Group, announced a $3.5 billion investment in Shields Health Solutions... Read more on LevinPro HC

Table of Contents

Q3 Activity Rebounds

Private equity activity rose 10% QoQ, driving deal volume

Despite a tumultuous summer in the United States, healthcare M&A activity rebounded in the third quarter, hitting 524 deals across the 17 sectors tracked by LevinPro HC. Compared with the second quarter, activity levels increased roughly 6%, and yearover-year activity is effectively the same, with only a 1% difference in deal volume. These margins are likely to widen once deals and transactions are reported in upcoming quarterly reports and filings, however.

Spending skyrocketed, hitting $63.8 billion, more than double the $30 billion from the second quarter and 35% higher than the $47.09 billion spent in Q3:24. The largest deal was Waters Corporation ’s $17.5 billion acquisition of Becton, Dickinson and Company 's biosciences and diagnostic solutions business, which is expected to generate $3.4 billion in revenue in 2025.

The results from the third quarter were surprising for a few reasons,

Continued on page 2

Top Deals Page 14 Stat of the Month Page 15 Monthly Chart Page 16

Home Health Reimbursements

Insights from CLA analyze the impact of CMS' changes

Over the summer, the home health industry faced some new potential headwinds. On June 30, the Centers for Medicare & Medicaid Services (CMS) issued its proposed rule for calendar year (CY) 2026, which proposes significant rate adjustments for the home health prospective payment system.

In this article, we will explore the most significant changes and their impact on the home health market.

There is a litany of changes included in the CY 2026 Home Health proposed rule, but the payment cuts are causing the most alarm. Under the new rule for 2026, home health payments are expected to be reduced by approximately 6.4% overall, or $1.13 billion, compared to rates in 2025. These include a 4.1% permanent reduction to the standard payment rate to prevent

Read more on LevinPro HC

especially the level of headwinds hitting the market.

On the Fourth of July, President Trump signed the One Big Beautiful Bill Act, which promises significant changes to Medicaid eligibility and the methods that states can pay for the program. This change is poised to hit rural healthcare significantly, which is why the Republicans included a $50 billion funding measure to offset the cuts. Whether the extra $50 billion will be enough to slow the tide of hospital closures across rural America is yet to be determined. The Centers for Medicare and Medicaid Services also published its reimbursement changes for home health services, which could further destabilize an industry already under pressure.

Despite the wave of reimbursement changes, sectors like Home Health & Health only experienced a marginal decline in activity quarter over quarter, falling to 22 deals from 26. Details are scarce at the

moment, but UnitedHealth Group divested 164 home health and hospice locations (including one affiliated palliative care facility) across 19 states, accounting for approximately $528 million in annual revenue. No buyer was disclosed, but UnitedHealth agreed to sell the locations to resolve U.S. antitrust concerns over its $3.3 billion acquisition of Amedisys . The Justice Department and attorneys general from four states (Maryland, Illinois, New Jersey and New York) filed a civil antitrust lawsuit in November 2024 to block the deal, arguing it would reduce competition in the home health services market.

Hospital activity actually rose, hitting 16 deals, a quarterly high for the year. Most of the deals were struck by health systems such as the Medical University of South Carolina and the University of Colorado Health , but a few deals were closed by financial investors. IRA Capital acquired the real estate of Houston Physicians' Hospital , a 130,822-square-foot advanced surgical hospital with 55 beds located in Webster, Texas. The property is 100% leased to a joint venture between the physicians, Memorial Hermann Health System and United Surgical Partners International

ISSN#: 2375-7612

Published monthly by:

Irving Levin Associates LLC

P.O. Box 1117, New Canaan, CT 06840

Phone: 800-248-1668 Fax: 203-846-8300

info@levinassociates.com

www.levinassociates.com

Editor: Dylan Sammut

Analyst: Kate Humphrey

Analyst: Avery Swett

Advertising: Cristina Blazek-Hearty

The full, annual subscription includes 51 weekly e-newsletters, 12 monthly issues, four quarterly reports

©2025 Irving Levin Associates, LLC All rights reserved. Reproduction or quotation in whole or part without permission is forbidden.

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable but no representation is made as to their completeness or accuracy.

Investments in physician groups also increased, reaching 128 deals (also a quarterly high for 2025). Spending reached more than $5 billion, driven by several large deals from corporations and private equity investors. The largest was The Specialty Alliance ’s $1.9 billion acquisition of Solaris Health , a management services organization for urology providers. Solaris has a network of 750 physicians.

The Specialty Alliance is the management service organization branch of Cardinal Health, which is providing the cash for this deal and will own approximately 75% of the two groups after the transaction is complete. Solaris Health physicians and several members of management will join as equity holders and operators in The Specialty Alliance.

Other notable deals include GTCR’s $1.58 billion purchase of Dentalcorp, and Bridgepoint Group's... Continued On LevinPro HC

Top Stories September 2025

Navigating Rehab M&A in 2025: Insights from Paul Martin of Martin Healthcare Advisors

The Rehabilitation M&A market is showing signs of renewed vigor in 2025 after a period of moderation. With easing interest rates and persistent sector fragmentation, deal activity is picking up as private equity and strategic buyers position for consolidation.

To unpack these trends, the LevinPro HC team interviewed Paul Martin, President of Florida-based Martin Healthcare Advisors. Martin's insights highlight the market's current dynamics, buyer priorities and staffing challenges that could shape deals in the year ahead.

Martin Healthcare Advisors is a national leader in middle market healthcare mergers and acquisitions, valuations, profit building consulting and buyer-seller advisory services specializing in Outpatient Rehabilitation, and Applied Behavior Analysis. The firm has done more than 150 deals representing more than 400 clinics and a total payout to owners of more than $500 million.

“The rehab market is active but evolving. We’re not at the record pace of 2021–22 when COVID and close-tofree debt drove a surge in deals,” Martin noted.

According to LevinPro HC data, 34 Rehabilitation deals have been announced year to date as of September 29, 2025. This compares to 28 rehab deals during the same 2024 period, 38 during the same 2023 period, 66 during the same 2022 period and 65 during the same 2021 period. Full year totals show 46 Rehabilitation deals announced in fiscal 2024, 51 in fiscal 2023, 82 in fiscal 2022 and 96 in fiscal 2021. Among strategic acquirers, Ivy Rehab and its pediatric arm Ivy Rehab for Kids stand out as the most active so far in 2025, with four and three deals respectively.

While the uptick from 2024 is welcome, the market is still adjusting to higher borrowing costs that tempered

activity through much of the year. The Federal Reserve's September 17 rate cut, lowering the federal funds rate to a target range of 4.00% to 4.25%, could accelerate momentum further.

“We’ve had a rate cut recently. Lower borrowing costs tend to boost confidence across the industry,” said Martin.

This easing aligns with broader healthcare M&A recovery, where outpatient rehabilitation's fragmentation continues to attract buyers. The sector's structure, with thousands of independent clinics nationwide, creates ample room for platforms to scale through add-ons and tuck-ins.

According to Martin, larger deals, those targeting companies with $50 million or more in EBITDA, have been scarce but activity may thaw as capital flows improve.

At the heart of this activity are buyers seeking targets with solid fundamentals. In rehabilitation, operational efficiency and cash generation are key.

"Buyers are drawn to well-run practices: owners who understand their business, operate efficiently, and generate strong cash flow,” Martin explained. “Another motivation is competition. Companies will step up when they know they are in a competitive process; everyone wants the winning assets."

Martin emphasized that the competitive environment not only influences pricing but also accelerates the pace of deals. When multiple buyers are chasing the same target, diligence and negotiations often move faster, resulting in higher valuations for well-positioned sellers.

"When an acquirer knows peers are competing on the same timeline, they move faster, streamline diligence and push valuations higher," said Martin.

Fragmentation remains a defining feature of the outpatient rehabilitation market. According to Martin, the top three companies in the United States represent just 8-10% of the overall clinics, leaving significant opportunity for consolidation. Investors and

operators with the resources to scale can leverage this fragmentation to capture market share or create efficiencies that smaller, independent clinics cannot.

“Outpatient physical therapy remains highly fragmented. By clinic count, the three largest operators together control roughly 8% of U.S. clinics; even the top five to six combined are only ~10–11%, depending on the denominator you use,” Martin added.

Private equity firms specializing in healthcare services lead the charge, building platforms like Confluent Health and Upstream Rehabilitation through strategic add-ons. Of the 34 deals announced so far this year, 20 have involved private equity acquirers and/or their portfolio companies, encompassing nearly 59%. This compares to just nine private equity deals announced during 2024, encompassing 32%. Waud Capital Partners was the most active private equity backer, with involvement in seven Rehabilitation deals so far in 2025. Public players such as U.S. Physical Therapy add measured volume but face tighter oversight.

Looking ahead, Martin is positive about the market’s trajectory, though he warns that staffing constraints could influence future growth.

“I’m very optimistic about rehab into late 2025 and beyond, though staffing is the biggest wildcard. New PT graduates carry heavy debt loads, and current salary levels haven’t yet kept pace,” said Martin.

The staffing squeeze, driven by tuition costs often exceeding $100,000 for Doctor of Physical Therapy programs and entry-level pay averaging $101,000 annually, threatens clinic throughput and deal appeal. New grads enter the field saddled with massive debt, making it harder for clinics to attract and retain talent without competitive wages.

Without adjustments like higher starting salaries or efforts to lower program tuition (such as scholarships or cost reforms at schools), understaffing could erode cash flows and stall growth.

Operators pushing for better reimbursements and

Oct 14-15, 2025 Hyatt Regency Irvine | Irvine, CA

retention strategies like flexible scheduling and professional development programs will fare best. For instance, U.S. Physical Therapy, Inc. has rolled out clinician mentorship initiatives and work-life balance perks to combat turnover amid shortages.

For operators and investors navigating the Rehabilitation M&A landscape, Martin emphasizes the importance of taking proactive steps to stay resilient and capitalize on opportunities. Privately held companies, in particular, should step back periodically to gain perspective on shifting dynamics.

"For private firms: take a moment to lift your head, observe what’s happening in the market, who’s being acquired, how peers are repositioning. And ensure you’re constantly adding value to your business," Martin advised.

In practice this means regularly evaluating the company’s worth, monitoring comparable transactions and implementing enhancements such as expanding payer mixes or strengthening referral networks. These actions help businesses remain competitive, anticipate market shifts and prepare for smoother exits whether through a sale or strategic partnership.

For owners considering a transition, understanding the current value of their enterprise can guide targeted growth initiatives and turn potential weaknesses into strategic advantages.

Larger platforms and investors meanwhile often underestimate the value of front-line expertise in rehab operations.

"For larger companies and investors: come in with the humility that many clinician operators know how to run clinics, and those operators may be ideal partners for the future," said Martin.

Successful integrations often rely less on outside consultants or corporate managers and more on elevating experienced physical therapists who understand local operations. This approach preserves community relationships, drives clinician engagement

and accelerates post-deal performance.

In a sector where patient connections and referral networks are critical, blending scale with operator-led management can unlock long-term value, particularly as private equity players like Waud Capital expand their platforms.

Inside the 2025 Clinical Trials M&A Market

The clinical trials market, part of our newly formed Life Sciences R&D sector, has seen a shift in M&A deal volume over the last few years. The post-pandemic dealmaking frenzy has cooled, with acquirers now making more strategic and deliberate moves over the large-scale expansion of previous years.

According to data captured in the LevinPro HC database, deal volume was modest before the postpandemic surge, with 12 deals in 2019, 14 in 2020 and 18 in 2021. Volume escalated more than 66% in 2022 when 30 deals were reported. Deal volume hit a high in 2023 when 43 acquisitions were announced.

However, M&A activity fell 37% in 2024 with 27 deals. If activity continues at its current pace, the clinical trials deal volume will fall short of previous years; as of September 2025, 15 clinical trials acquisitions have been announced. Currently, clinical trials accounts for 26% of the 58 Life Sciences R&D deals of 2025.

As in many other sectors, private equity (PE) plays a dominating role in the clinical trials market. In 2025, 60% of the transactions have been completed by PE groups and their portfolio companies. This is a drop from 2024 when more than 70% of deals were PEbacked. However, it is on par with 2023 when just shy of 60% of the deals were completed by PE firms.

PE’s presence in the clinical trials space comes down to a few reasons. To save money and speed up drug development, pharmaceutical companies have, more and more, begun to outsource clinical trials to thirdparty providers. This creates a large demand for companies that specialize in clinical trials.

Additionally, there’s much less risk in buying a company on the R&D side than an entire pharmaceutical company, allowing for PE firms to enter the market with less risk. No other buyer type has had a notable presence in the field throughout 2025.

There have been no transactions in the Clinical Trials sector in 2025 with a purchase price. In 2024, the only transaction with a disclosed price was Audax Private Equity’s acquisition of Avantor’s clinical services business for $650 million.

In 2025, the only buyer to have announced more than one transaction is Flourish Research, a fully integrated clinical trial organization in North America backed by NMS Capital. Flourish has conducted more than 3,700 trials across more than 15 therapeutic areas and more than 60 indications. Since 2021, Flourish Research has announced 10 transactions, making it one of the busiest acquirers in the sector.

In February, Flourish Research acquired Diablo Clinical Research, a multi-therapeutic clinical research facility performing phase I-IV clinical trials and medical device studies. It is based in Walnut Creek, California and has conducted more than 1,000 trials across various therapeutic areas, including endocrinology, cardiovascular and metabolic studies.

In May, the company acquired Center for Advanced Research & Education, a multi-therapeutic research facility dedicated to advancing innovation in healthcare through conducting phase I-IV clinical trials. Founded in 1998 and headquartered in Gainesville, Georgia, the company has conducted more than 150 clinical trials across multiple therapeutic areas

While Velocity Clinical Research has made no deal announcements in 2025, it is still one of the more active buyers in the market. Like Flourish, it has reported 10 transactions since the start of 2021. Its most recent transaction was the acquisition of three European clinical trials companies: KO-MED Centra Kliniczne, which is based in Poland and The Pulmonary Research Institute and KLB Gesundheitsforschung Lübeck, which are both based in Germany.

Velocity Clinical Research supports global drug development by primarily conducting phase II and phase III clinical trials. The company has nearly 100 locations globally, including a technology hub in Hyderabad, India. Velocity Clinical Research was acquired by GHO Capital in April 2021.

Headlands Research has also shown prominence in the clinical trials space. Since 2021, it has announced nine transactions, with the bulk of them in 2023 (four deals). Headlands Research is a globally integrated clinical trial site organization. With a multinational network of 21 clinical trial sites, Headlands Research has successfully completed more than 5,000 clinical trials. It was founded in 2018 by KKR and sold to THL Partners in August 2025.

In July 2025, the company acquired CMRCenter, a clinical research site in San Juan, Puerto Rico, specializing in Phase II through IV clinical trials to advance medical treatments for diverse patient populations. This is the only transaction the company has announced so far this year.

Other active buyers over the last five years include The IMA Group (nine deals), Alcanza Clinical Research (five deals) and CenExel Clinical Research (five deals).

SUN Behavioral Health’s Acquisition Strategy: A Conversation with CEO Steve Page

Unlike many other healthcare sectors experiencing a decline in M&A deal volume, the Behavioral Health Care (BHC) market has seen a plethora of deal activity in 2025. According to data captured in the LevinPro HC database, there have been 74 BHC transactions announced since the start of the year, outpacing the 73 deals announced in 2024.

The deal volume of 2025 is on track to outpace the 83 deals reported in 2023 as well. However, 2022 and 2021 saw incredibly high deal volume; there were 113 deals reported in 2022 and 131 in 2021.

The large deal volume seen in 2022 and 2021 was

due to the high demand for mental health services resulting from the challenges faced by the country during the COVID-19 pandemic.

In 2025, so far, there have been three transactions in the BHC space with disclosed prices. The largest is Sevita’s acquisition of BrightSpring Health's community living business for $835 million.

Sevita is a provider of home and community-based health care that is backed by Centerbridge Partners L.P. The acquired assets include BrightSpring Health's ResCare Community Living. The community living business is expected to generate approximately $1.2 billion in revenue and approximately $128 million of adjusted EBITDA in 2024, according to the original deal press release from January 21, 2025.

Counseling & psychiatric care was the most active subsector with 37 transactions; substance use disorder treatment saw 11 deals; there were 10 autism spectrum disorder treatment provider deals.

With so many transactions, the LevinPro HC team wanted to delve into the process from a buyer’s perspective.

We spoke with Steve Page, CEO of SUN Behavioral Health, who was able to shed light on the transaction process, as well as discuss a recent acquisition.

SUN Behavioral Health is a provider of freestanding psychiatric hospitals, focusing on addressing unmet mental health needs in underserved communities. The company operates facilities that offer comprehensive inpatient and outpatient care. It received a $34 million growth capital investment from LLR Partners in November 2016.

In May, SUN Behavioral Health announced that it acquired Seaside Healthcare's home and community services unit. Previously backed by Pharos Capital, Seaside Healthcare provides behavioral health care across a full spectrum of care, including acute hospitalization and home and community-based services. Bailey & Co. represented Pharos Capital

Partners. The financial terms were not disclosed.

According to Page, the Seaside acquisition came to them through one of their current investors.

“The process was initiated sometime in late 2024 and closed on May 1, 2025,” said Page. “This roughly sixmonth period is about what we would expect from the introduction to closing of a transaction process."

Seaside was an appealing prospect for SUN because it expanded upon the company’s existing capabilities. According to Page, Seaside has roughly 25 different levels of services that span six states. The levels of services were a diverse offering that would allow SUN to expand its services into the home & community sector (which was something they previously didn’t offer) as well as broaden its geographical reach.

However, Page did make it clear that geographical reach is not the only approach to an acquisition.

“Our development strategy is focused on creating the full continuum of care as opposed to just building in various geographies,” Page said. "There’s a lot of opportunity in our existing footprint to create the full continuum of care.”

He touched lightly upon how often the most intriguing acquisition opportunities often address multiple unmet needs.

“Seaside was treating the same patient profile we treat but outside of the hospital through its home & community services,” said Page.

This allows for a seamless addition to its umbrella.

Extending the same level of care beyond the hospital was a key factor driving this transaction and a priority for Page.

“Over the years, we’ve thought a lot about the challenge many of our patients face transitioning from an acute stay back into the community,” Page said. “One area where patients consistently struggle after

leaving the hospital is with their discharge plan. For many, the biggest concern isn’t filling their prescription or making a therapy appointment; it’s figuring out where they’re going to sleep.”

This reflects a broader trend of emphasizing care beyond inpatient facilities. With the addition of Seaside, SUN is better equipped to care for patients outside of the inpatient setting. This will lead to a better and more successful recovery.

Perhaps the most important part of the transaction process is the closing, as there are a plethora of factors that can go wrong and stop a transaction. When speaking about ways that acquirers can ensure the transaction comes to fruition, Page’s commentary was centered around one thing.

“My strategy has always been to get the deal breakers out upfront; it allows us to prioritize projects that have a chance to get done and gives the other party some confidence they’re dealing with someone honest and straightforward,” he said.

He concluded our discussion by addressing a common concern patients may have: how does a new backer impact the quality of care?

“The patient shouldn’t see any difference in quality of care because all of Seaside’s local leadership stayed in place; the only impact should be more support,” he said. “We’re very conscientious about how staff feel about the transaction. We make every effort to communicate that the transaction reflects the great work they’re doing, and our intent is to invest and grow from the foundation they have helped create.”

Harbor Health Acquires 32 VillageMD Health Clinics

On September 17, VillageMD announced that it was divesting 32 health clinics to Harbor Health.

The clinics are based in Texas: 10 in Austin, 10 in San Antonio, six in El Paso and six in Dallas. Harbor Health is an Austin, Texas-based primary and

specialty care clinic group. It was founded in 2022 in Central Texas.

The acquisition nearly quadruples Harbor Health's clinical presence, growing from 11 to 43 total clinics and adding more than 80 clinicians to its team of physicians and advanced practice providers. The financial terms of the acquisition were not disclosed.

"Harbor Health has been honored to care for more than 50,000 people in Central Texas since we launched in 2022," said Dr. Clay Johnston, Harbor Health CoFounder. "We have an increasing demand for our care, and the Harbor Health and VillageMD teams are strongly aligned in our clinical model to operate in value, putting the consumer first and integrating care journeys, to result in better care and outcomes."

Montecito Medical Announces 23rd Acquisition of 2025

Montecito Medical Real Estate, based in Nashville, Tennessee, announced its third transaction of the month with the acquisition of a health system-affiliated medical outpatient building (MOB),.

Located in Tallahassee, Florida, the building is occupied by Tallahassee Memorial HealthCare and comprises 46,969 square feet. The space is used to primarily provide pulmonary care and physical therapy. Tallahassee Memorial HealthCare is a dominant nonprofit healthcare system serving a 21-county region across North Florida and South Georgia. The system operates a 772-bed acute care hospital and encompasses approximately 50 affiliated practices.

Montecito Medical specializes in healthcare-related real estate acquisitions and funding. Since 2006, it has completed transactions involving more than $6.5 billion in medical and veterinary real estate transactions.

This marks Montecito Medical's 23rd acquisition of 2025. The property represents the 12th acquisition for Montecito in Florida, and the second in Tallahassee since the beginning of 2024.

Additionally, in 2025, Montecito Medical has expanded its network by more than 45 properties across the United States, totaling more than 1.15 million square feet. It has purchased facilities in Florida, Texas, South Carolina, Rhode Island, New York, Georgia, Indiana, Minnesota, Arizona, Ohio and California.

Health System News & Activity

September was a busy month for health systems. The Centers for Medicare and Medicaid Services (CMS) revealed its details on applications for the Rural Health Transformation Program (RHTP), which was passed as part of the One Big Beautiful Bill in July. The RHTP provides $10 billion in annual funding (up through 2030) to each state to bolster rural hospitals and offset the looming Medicaid cuts. Hospitals and health systems will have to consider the five goals in the application, and the deadline on November 5 is approaching quickly.

There was also a new report from the Government Accountability Office (GAO) analyzing the drivers of hospital closures in urban areas and the effects they have on surrounding communities.

“All five urban hospitals included in GAO’s review experienced financial decline characterized by financial losses or declining profits in the 5 years leading to their closure,” the report writes. “Several other factors contributed to hospital financial decline and closure such as aging physical infrastructure, low inpatient volume, challenges operating as independent hospitals, poor management practices, and separate ownership interests.”

And the impact of these closures is not surprising.

“One hospital’s closure reduced the availability of emergency and inpatient services in the part of the city where it was located, which exacerbated pre-existing access to care challenges for community residents, according to stakeholders,” stated the report.

GAO conducted this study because it said that while the effect of rural hospital closures has been widely

documented, there was a scarce amount of literature and data surrounding urban hospital closures.

“Approximately half of U.S. hospitals are in urban areas, and closures of urban hospitals outpaced new openings from 2019 to 2023,” the report indicated. Systems (and patients) additionally faced a large setback in the “hospital-at-home" movement. Initially launched in 2020 by CMS, the program allows some patients who require acute-level care to receive care in their homes, rather than in a hospital. It was a temporary program established in response to the COVID-19 pandemic, but it was well-received by both patients and providers, so Congress renewed it several times. However, the program expired on October 1 (Congress did not renew it after the government went into shutdown) and some major systems have stopped admitting patients.

Despite the flurry of mostly negative news, health systems returned to the M&A market, investing in a wide range of sectors. These organizations announced 12 deals, split primarily between acquisitions in the Hospital sector and the Physician Medical Group sector.

There was one health system merger that closed in September in the United States. The Medical University of South Carolina acquired a majority stake in Tidelands Health, one of the largest healthcare systems in the Carolinas. Tidelands owns two acute care hospitals totaling 255 beds (Tidelands Georgetown Memorial Hospital and Tidelands Waccamaw Community Hospital), as well as two inpatient rehabilitation hospitals and more than 70 outpatient locations.

In 2024, Tidelands generated $523 million in net patient revenue and approximately $5.5 million in EBITDA. According to local reporting, however, MUSC leadership told South Carolina lawmakers that Tidelands is on track to lose $50 million for the fiscal year ending this September.

In New York, Westchester Medical Center Health Network (WMCHealth) and Bon Secours Mercy Health ended their joint venture partnership, prompting the

latter to take full ownership of the three hospitals the groups managed together.

WMCHealth acquired St. Anthony Community Hospital, Bon Secours Community Hospital and Good Samaritan Hospital of Suffern, all serving regions in Orange county, New York. Collectively, the hospitals generated $518 million in revenue in 2024 and have 432 beds among them. The deal also includes multiple nursing homes.

Health systems announced four deals in the physician space, all in the orthopaedic space. Hutchinson Regional Healthcare System in Kansas acquired two practices, and Atrium Health acquired Carolina NeuroSurgery & Spine Associates, a 44-physician group with nine locations. No price was disclosed in either deal.

The last two deals were for health clinics. St. Joseph Regional Medical Center purchased Catalyst Medical Group and HonorHealth acquired Evernorth Care Group in Phoenix, Arizona from the health insurance giant Cigna.

Private Equity News & Activity

Private equity (PE) activity in the healthcare M&A market dropped slightly in September 2025, with 56 PE deals announced in September, representing 30% of the 184 total healthcare transactions for the month. This marked a slight decline from August, which recorded 57 PE deals and a 34% share of activity, as well as from July, which saw 66 PE deals representing 38% of all healthcare transactions.

PE’s share of deal activity was also lower than the same period last year, when 60 of 163 total healthcare transactions in September 2024 involved a PE buyer or portfolio company, representing 37% of deals. The decline suggests some cooling after an active summer, although PE remains a significant force in healthcare dealmaking.

Physician Medical Group (PMG) was the most active sector for PE buyers, with 19 transactions announced

during the month, representing 43% of all PMG transactions in September. Dental practices were a major driver within the PMG segment, accounting for 10 of those 19 deals.

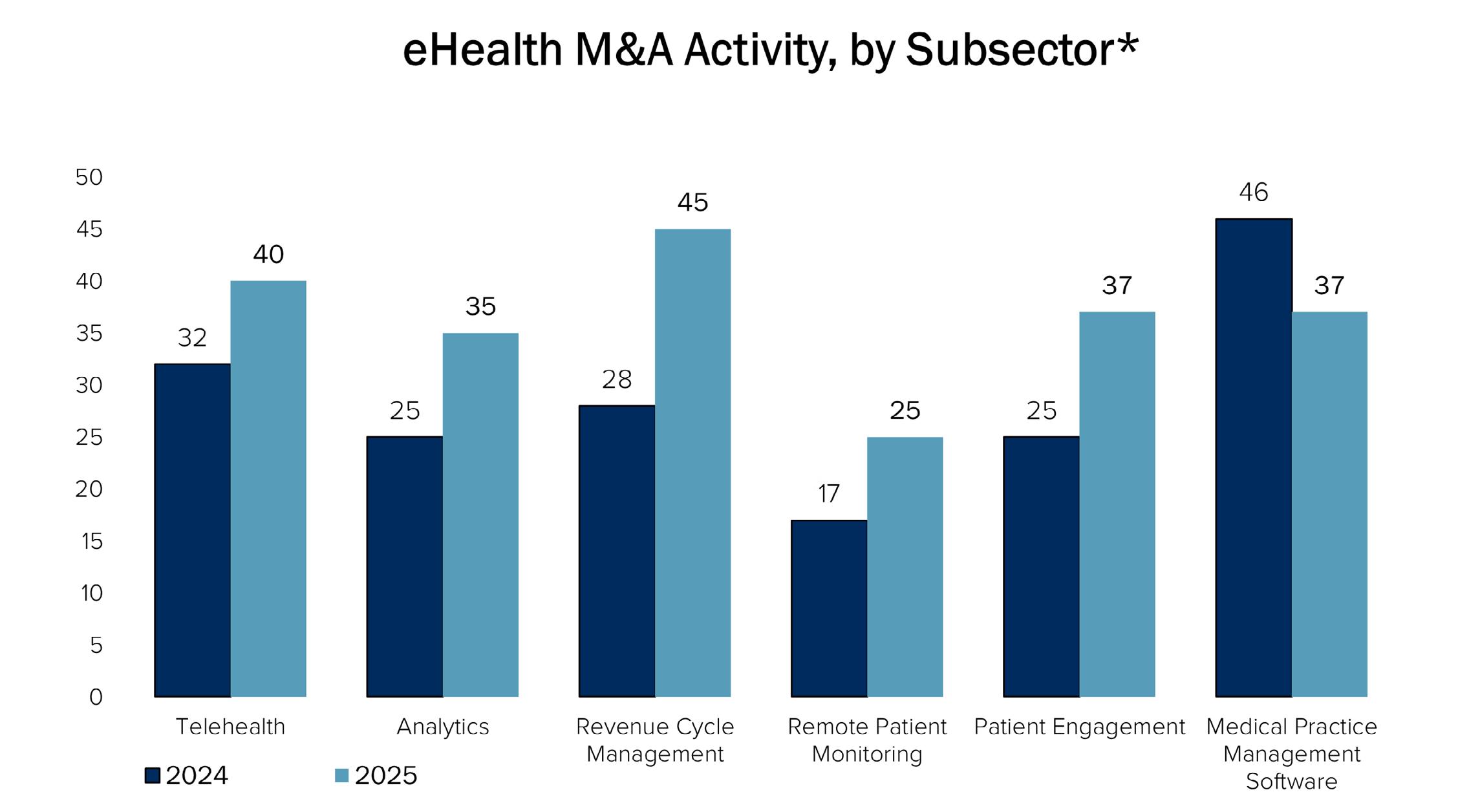

eHealth followed as the second most active sector, with 11 PE transactions, representing 39% of all eHealth deals. While deal flow in eHealth has settled into a steadier rhythm compared with the surge seen during the pandemic years (although it has been on the upand-up in recent months), PE remains a consistent participant in this space. The Rehabilitation sector also saw notable activity, with five PE transactions that made up 71% of all Rehabilitation deals for the month. Pharmaceuticals recorded three PE deals, representing 42% of the sector’s total activity.

Several PE investors were particularly active during the month. Waud Capital Partners was the most active PE backer, with three Rehabilitation transactions announced through its Ivy Rehab and Ivy Rehab for Kids platforms. Charlesbank Capital Partners and Warburg Pincus each supported two MB2 Dental transactions, continuing their involvement in the dental consolidation space. DuneGlass Capital backed two Phase 1 Equity orthodontic practice acquisitions, while LLR Partners participated in two deals supporting Genesee Scientific and Eye Health America Shore Capital Partners was also active, completing multiple practice acquisitions through its Southern Orthodontic Partners and Together Women’s Health platforms.

While most PE deals in September did not disclose financial terms, a handful of transactions provided insight into deal size. The largest was Patient Square Capital’s acquisition of Premier Inc. for $2.6 billion, representing the 13th largest healthcare deal by purchase price and the third largest deal announced during the month of September. Additionally, GTCR’s $1.58 billion acquisition of Dentalcorp highlighted the continued appeal of scaled dental platforms. On the smaller end, Polaris Partners-backed Phreesia acquired AccessOne for $160 million, and Privia Health Group, backed by Brighton Health Group Holdings, acquired Evolent Care Partners for $100 million.