International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

1Lecturer in Automobile Engineering, SSM Poly Technic College Tirur, Kerala, India 2Head of Department in Automobile Engineering, SSM PolyTechnic College, Tirur, Kerala, India

Abstract - This study also analyses the performances of industries during the lock down period due to Covid19 Pandemic situation. This chapter discusses about the finding by the investigator on the effect of COVID 19 to the Indian manufacturing industries. It is known that the pandemic brought a tremendous change in the industrial scenario throughout the globe. Most of the countries locked down their entire operations to limit the spread of COVID 19 and which highly affected the production, sales and consumption of the commodities. This made the industries to get stuck with their operations except for those industries related to medical/ health care. Hence this chapter is aimed at exploringtheeffect of COVID 19 over the Indian SMEs.

Keywords: Covid19,lean,SMEs,Questionnairesurvey

Atpresenttimeworldisfacingfromthecoronavirusdisease known as Covid-19. The first case of the coronavirus was reportedintheDecember,2019intheWuhancityofChina whichisknown asthe majortransportation hub ofChina. Due to the immediate and severe spread from person to person, most of the countries controlled the chance of spreading by implementing lockdown to their population. Manycountrieshaveshutdowntheirseaportsandairports (Agarwal et al. 2020). They have banned the import and export activities. All these affected the business firms and theirdaytodayoperations.

Itwasreallyunexpectedfortheindustriesthatthesudden closureoflocalandglobalmarketwhichhighlyaffectedtheir revenue. Similarly the lockdown forced them to stop the productionswhichleadtomanyotherdifficulties/lossesto the industries (Rakshit and Basistha, 2020). India is the developing country due to the Covid-19 spread the cases reportedintheIndiagovernmenthaslockdownthecountry for41dayswhichaffectedthemanufacturingactivitiesand majorly it affects the supply chains and economy of the country(Thiagarajan2021).

COVID 19 has affected the manufacturing firms and their supply chain over the world. COVID 19 is affecting the manufacturing operations daily. The lockdowns and the regulations at different nations have already affected the supplychainandforcedthousandsofindustriestothrottle

downorshutdowntheirassemblylinestemporarilyinthe U.S and Europe and in the developing nations like India (Pickert2020).Manyofglobalindustriesaredependsonthe Chinaforthematerialsandparts.Themanufacturingunitsin China was shut down initially and that had caused many dependentindustriestoshutdownfornextfewmonths.In these ways theimpactoftheCOVID19pandemicaffected thebusinessesallovertheworld.

1. Toanalysetheeffectoflock-downtothebusiness ofSMEs,duetotheCOVID19 Pandemic.

2. Tounderstandthesituationsoftheindustriesin thisnewnormalperiod.

Inthisresearch,theresearcherusedaquestionnairesurvey using a 11-question questionnaire with multiple choice questions.Thequestionsweremeanttoanalysethesituation of each respondent/ firm and the measures taken by the respective firm to improve the situations. Few of the questionswereofsingleoptiontypeandintheremaining therespondenthavethefreedomtoselectmultiplechoices accordingtotheirconditions.Thecountforeachresponse wasnoticedandtheinterpretationsweremadeandreported inthefollowingsessions.Thepercentageobtainedforeach responseswasthemeasuretakenfortheanalysis.

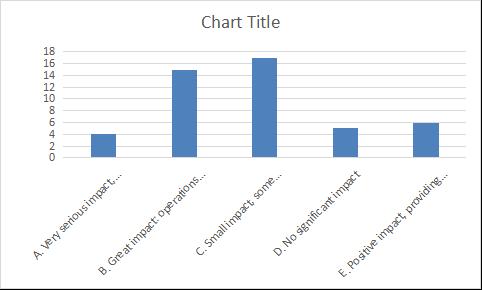

A. Very serious impact, leading to serious difficulties in business operationsandbankruptcy 4 8.5

B.Greatimpact:operationsbarely maintained 15 31.9

C.Smallimpact,somedifficultiesin business operations, but overall stability 17 36.2

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

D.Nosignificantimpact 5 10.6

E. Positive impact, providing new opportunitiesfordevelopment 6 12.8

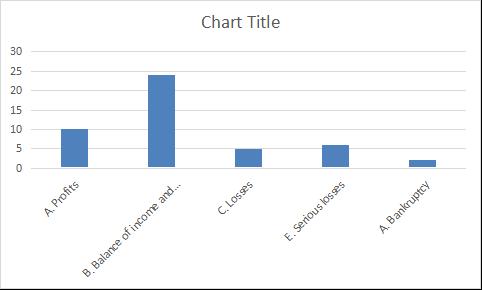

B. Balance of income and expenditure 24 51.1

C.Losses 5 10.6

E.Seriouslosses 6 12.8

A.Bankruptcy 2 4.3

Fromtheoverallresponse,itcanbeseenthatatotalof70% ofrespondents(28industries)reportedthatthelockdown has made some impact to their firm’s production and operations.Outofthese28firms,3firmsreportedthatthey hadseriousdifficultiesintheirbusinessandtheyhadhigh financiallossesduetothelockdown.Similarlyremaining12 of 28 responded that they also had seriously affected but theycouldmaintainthebasicoperationsforthemtokeep aliveandtheremaining13of28onlyhadasmallimpactdue tothepandemicandtheywereinastablepositionintheir operationsandmarket.

Theremaining30%oftherespondentsreportedthatthey hadeithernoimpactbythelockdown(5industriesof12)or theyhadpositiveimpactintheiroperationsandsales(7of 12industries).

Thedatawerecollectedthroughthequestionnairemethod. Theresearcherhaddirectlyvisitedasmuchaspossiblefirms and discussed with the respondent and given the questionnairetotherespondenttofill.Latertherespondent filled the questionnaire and given back to the researcher. Due to the pandemic condition few of the industries preferred online methods to fill the questionnaire. In that case,theresearchercontactedtherespondentanddiscussed thematterthroughphoneandlaterthequestionnairewas mailed. The respondent submitted back the filled questionnairethroughemail.Buttheresponseratethrough theonlinemodewasmuchlessthanthedirectmode.

2. To what extent did the lock-down affect your firm’s development?

Options No.ofResponses %

A.Profits 10 21.3

10of47(21.3%) respondentsmentionedthattheycould achieveprofitinthebusinessduetothelockdown.Another 24respondents(51.1%)reportedthattheywereabletorun the business by balancing the income and expenditure. Hence,itisunderstoodthat72.3%oftherespondentswere nothighlyaffectedbythelockdown.Whereas,theremaining 27.7%ofrespondentswerehighlyaffectedbythelockdown i.e.theywerenotabletomaintaintheproductivityandthe salesandhencetheirbusinesswasreachedintolosses(10.6 %),seriouslosses(12.8%)andbankruptcy(4.3%).

3.Whatarethereasonsforthesuspensionofproductionand operationsofyourfirm?

No. of Responses %

A.Shortageofproductionmaterials. 13 27.7

B.Difficultyindevelopingmarket 13 27.7

C. Impact of measures taken to respondtothepandemic 5 10.6

Shortage of production materials, Difficulty in developing market (A&B) 11 23.4

Shortage of production materials, Impact of measures taken to respondtothepandemic(A&C) 1 2.1

Difficulty in developing market, Impact of measures taken to respondtothepandemic(B&C) 2 4.3

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

A.Shortageofproductionmaterials.

B.DifficultyindevelopingmarketC. Impact of measures taken to respondtothepandemic(A,B&C) 2 4.3

27.6%oftherespondentsreportedthattheystoppedtheir operations due to they did not receive adequate rawmaterialstoactualisetheproduction processandanother 27.6%ofrespondentsreportedthatunavailabilityofmarket or reduced sales was the reason for cutting down the productionforthem.Andfurther10.6% (i.e.5of47)find difficultyintheactions/ measuresto betakenagainst the pandemic(Likelimitingthenumberofemployees,limiting scopeforsocialdistancing,limitationsinperiodicsanitizing etc.)

Asthisisamultiple-choicequestion11of47respondents reportedthattheyhadcutproductionbecauseofboththe shortageofproductionmaterialproductionandthedifficulty in developing market. Similarly, 1 of 47 notified that they had stopped the operations because of Shortage of production materials and impact of measures taken to respondtothepandemic.Another,2of47notifiedthatthey had stopped the operations because of difficulty in developingmarketandimpactofmeasurestakentorespond tothepandemic.Remaining2of47respondentsmentioned thatallthethreecauseswereaffectedtheminsuspending theoperations.

Fromthese,wecouldsummarisethatthemainreasonfor thesuspensionofindustrialoperationisthereductioninthe sales/marketanditcouldbelogicallytruetoo.Unlessthe salesarenothappeningthereisnopointinproducingthe product. The second major reason for the suspension of operationistheunavailabilityofproductionmaterials.Itwas difficultforthefirmstogetthematerialsifthesuppliersare much away from the industry. Another reason of product unavailability was the purchasing power or limitation in funding.

4.Whatarethemainoperatingpressuresthatyourfirmis currentlyfacing?(Multiplechoice)

Employee salaries, insurances, Repaymentofloans(A&C) 4 8.5

Employee salaries, insurances, PaymentofaccountspayableE (A&D) 2 4.3

Employee salaries, insurances, Cancellationoforders(A&E) 5 10.6

Rent (Buildings, Equipment), Repaymentofloans(B&C) 1 2.1

Payment of accounts payable, Cancellationoforders(D&E) 3 6.4

Employee salaries, insurances, Repaymentofloans,Paymentof accountspayable(A,C&D) 2 4.3

Rent (Buildings, Equipment), Payment of accounts payable, Cancellationoforders(B,D&E) 1 2.1 NONE 1 2.1

ALL 1 2.1

The question was of multiple option type and hence the respondentshadgivenavarietyofresponse.Thequestion checks the important operating pressures faced by the respective organisation in terms of their economic situations/ constraints. One of the 47 respondents mentioned that they did not have any constraints in their economicconditions.Itisalsonoticeablethatnoresponses mentionedrentasanoperatingpressure,independently.

Employeesalaries,insurances,Rent (Buildings,Equipment)(A&B) 2 4.3

15of47respondents(31.9%)reportedthattheyhadfaced difficultyinpayingtheaccountpayablesandwhichwasthe option that most of the respondents opted. The term Accounts payable (AP) represents the amount that a company owes to its creditors and suppliers. Further 5 responses shows that the respondents had operating pressuredduetothecombinationofpaymentofemployee salary and the loss due to the cancellation of orders. Four peoplerespondedthattheyhadcancellationofordersasthe mainoperatingpressureandanotherfourpeoplementioned that they had their operating pressure due to the combination of employee salaries, insurances and repaymentofloans.Threeresponseseachweremarkedfor employeesalariesandinsurances;repaymentofloans;and the combination of payment of accounts payable and cancellationoforders.Tworesponseseachwereobtained forthecombinationsofemployees’salaries,insurancesand rent; employee salaries, insurances and the payment of accounts payable; and employee salaries, insurances, repayment of loans and the payment of accounts payable. Singleresponseseachwerereportedforthecombinationsof

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

rent and repayment of loans; rent, payment of accounts payable and the cancellation of orders. One of the respondents reported that they could mark all the five optionsastheoperatingpressurefacedbythem.

5.Whatisthecurrentsituationregardingthesupplyofraw materials,sparepartsandotherproductionandoperation materialsinyourfirm?(singlechoice)

Options No. of Responses %

A. Total disruption of supply 1 2.1

B.Supplyshortage 18 38.3

C.Supplybarelymaintains production 5 10.6

D.Satisfactorysupply 10 21.3

E.Normalsupply 13 27.7

Majorityoftherespondents(18of47i.e.,38.3%)reported that there is a significant shortage of supply of the production and operation materials. Further 13 of 47 respondents(27.7%)mentionedthattheyreceivednormal supply during the pandemic. Another 10 respondents (21.3%) had been obtained a satisfactory supply of necessaryitemsfromtherespectivesuppliers.Afurther10.6 %orrespondents(5of47)reportedthattheyonlyreceived a supplythatcan maintain theproduction. The remaining one respondentinformedthattheyhadfounddifficultyin theiroperationsduetothetotaldisruptionofthesupply.

Whilesummarisingtheabovefacts,itcouldbenoticedthat 19 of 47 (40.4%) respondents were highly affected to precedetheir operationswiththe reducedsupplyandthe remaining 28 of 47 (59.6%) respondents were able to proceedwiththeirbusinessoperationswiththeavailable/ adequatesupplyofthematerials.

Whileconsideringtherespondentswhomarkedeachoption, thesufferersofpoormaterialsupplyaretheendcustomers ofanother/similarsmallscalebusinesses(Likesmallscale cottonindustry,diemanufacturingindustryetc.).Thosewho werepurchasingfromthelargescaleorganisationsorthose whopurchasingthenaturalmaterialsfromthelocalmarkets were not highly affected during the pandemic (like food, steelindustryetc.).

6. Did/ Does your company ‘reduce or increase/ plan to reduce or increase’ the number of employees? (Single choice)

A. Reduce greatly (30–50%) 4 8.5

B. Reduce slightly (10–30%) 12 25.5

C. Remain basically the same 29 61.7

D.Increaseslightly(10–30%) 2 4.3

E. Increase greatly (30–50%) 0 0.0

61.7%(29of47)ofrespondentsreportedthattheykeptthe number of employees same in their respective industry before and during the pandemic whereas another 25.5% (12)respondentswereforcedtoreduce/firetheir10-30% oflaboursduetotheeconomicconstraints.Further8.5%(4) ofrespondentsreducedgreatlyhighernumberofemployees about50%duetotheeffectofpandemicintotheirbusiness. Another 4.3% (2) industries needed to increase their strength of the workforce to meet their business demand and no one reported that they increased their number of employeesmorethan30%ofthepre-pandemicsituation.

Whilesummarising,itcouldbeconcludedthat66%oftotal respondents were in a position to keep their employees happywhereastheremaining34%ofindustries were not able run the business with their entire workforce. The industries those were reduced the number of employees followed different actions towards their employees as follows: They might have fired the employees; they have introducedarotationsystemfortheemployeessothatevery employee gets equal chance to work; the companies only assigned work for the needed/ skilled work force and the remainingemployeesweretemporarilylaidoff.

Theindustriesincreasedthenumberofworkforcewereof the food processing/ manufacturing small scale organisations.

7. How has the pandemic affected recruitment? (multiple choice)

No. of Responses %

A.Increaseinlaborcosts 4 8.5

B. Unable to find a suitable recruitmentchannel 2 4.3

C.Postponementorcancelationthe existingrecruitmentplan 24 51.1

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

D.Transitiontoonlinerecruitment 10 21.3

Increase in labor costs, Unable to findasuitablerecruitmentchannel (A&B) 1 2.1

Increase in labor costs, Postponement or cancelation the existingrecruitmentplan(A&C) 2 4.3

Unabletofindasuitablerecruitment channel, Postponement or cancelationtheexistingrecruitment plan(B&C) 2 4.3

Postponement or cancelation the existingrecruitmentplan,Transition toonlinerecruitment(C&D) 2 4.3

Thisisacontinuationtothequestionnumber6.Heremost commonresponse(51.1%,24responses)wasobtainedfor theoptionCwhichmentionseithertheyhadpostponedor cancelled their existing recruitment plan. Further 21.3% respondents reported that they had a transition to online recruitment.4(8.5%)respondentsmentionedthattheyhad anincreaseinthelabourcost(itmightbeeitherduetothe increasing the labour strength or by increasing the work time/ salary). 2 (4.3%) respondents each responded that theywereunabletofindasuitablerecruitmentchannel;a combination of increased labour cost & postponement or cancellationofrecruitmentplan;acombinationofdifficulty infindingasuitablerecruitmentchannelandpostponement orcancellationofrecruitmentplans;andacombinationof postponementorcancellationofrecruitmentplanandthe transitiontotheonlinerecruitment.Theremaining2.1%(1 of 47) respondent notified that the pandemic affected the recruitmentbyacombinationofincreasingthelabourcost and difficulty in finding a suitable channel for the recruitment.

Forthetermonlinerecruitmentdifferentrespondentsmight havetakendifferentopinions.Theopinionsnoticedduring thediscussionbytheresearchertotherespondentare:They had assigned work from home to the sales department employees;Someofthe(mediumscale)organisationthose cut down their number of employees were tried to get fresher’s/lowsalariedemployeesthroughonlinemodesso astocutdownthecost.

The responses obtained for the question 7 resembles the responses obtained for the question 6 and hence can be validated.

8.Howareyoucurrentlyorplanningtocopewiththecash flowshortage?(multiplechoice).

No. of Respons es %

A.Fundingfromexistingshareholders 6 12.8

B.Addingnewshareholders 2 4.3

C.Loans 15 31.9

D.Delayingpayment 1 2.1

E.Cuttingpayandjobs 2 4.3

Funding from existing shareholders, Addingnewshareholders(A&B) 1 2.1

Funding from existing shareholders, Loans(A&C) 4 8.5

Funding from existing shareholders, Delayingpayment(A&D) 2 4.3

Funding from existing shareholders, Cuttingpayandjobs(A&E) 7 14.9

Addingnewshareholders,Loans(B&C) 1 2.1

Loans,Delayingpayment(C&D) 2 4.3

Delayingpayment,Cuttingpayandjobs (D&E) 1 2.1

Funding from existing shareholders, Loans,Cuttingpayandjobs(A,C&E) 1 2.1

Loans, Delaying payment, Cutting pay andjobs(C,D&E) 1 2.1 NONE 1 2.1

ThemostcommonresponseforthequestionwasoptionC and those respondents planned to cope with cash flow shortagebytakingadditionalloans(15of47respondents, 21.9%).Another7respondents(14.9%)mentionedthatthey are planning to cope the situation by the combination of extrafundingfromtheexistingshareholdersandcuttingthe payandthejobs.Afurther6(12.8%)respondentsnotified thattheytriedtoimprovethecashflowbyfundingfromthe existing shareholders. Four (8.5%) respondents tried to improve the cash flow by combining the funding from existingshareholdersandtakingextraloansfromfinancial institutes.Two(4.3%)responseseachwerereportedforthe options: Adding new shareholders; cutting pay and jobs; combination of funding from existing shareholders and delayingthepayments;andthecombinationoftakingloans anddelayingthepayments.One(2.1%)responseeachwere noted for: delaying the payment; combination of funding from existing shareholders and adding new shareholders;

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

Combinationofaddingnewshareholdersandtakingloans; combinationofdelayingpaymentandcuttingpaysandjobs; combinationoffundingfromtheexistingshareholders,loans and cutting pays and jobs; and the combinations of loans, delaying payments and cutting pay and jobs. One of the respondents replied that the cash flow shortage did not affectfortheirbusiness.

9. Do you have the possibility to transform to online commerce?

Options No. of Responses %

A Veryunwilling 6 12.8

B Unwilling 18 38.3

C.Reasonablywilling 10 21.3 D.Willing 11 23.4

E Verywilling 2 4.3

Thequestiontestedtheresponsetowardsthewillingnessto transform to the online commerce by the companies. The optionoptedbyagreaternumberofrespondents(18of47, 38.3%) was the unwillingness towards online commerce. Further 23.4% (11) respondents confirmed that they are willing to move to online commerce. Another 21.2% (10) mentioned that they are reasonably willing for the transformation. 12.7% (6) respondents were not at all willing to transform into the online commerce and the remaining 4.3% (2) respondents were highly willing to transformintotheonlinecommerce.

Altogether 24 of 47 respondents were not willing for the transformation and the remaining 23 respondents were readyforthetransformation.Theunwillingnessmaybedue to the lack of technical/ online knowledge, myths on the onlineeconomyandtheinsufficientlowcostsupportfrom theITcompanies.

10. What self-help measures has your firm taken so far? (Multiplechoice)

Options No. of Responses %

A.Appliedforfinancing 9 19.1

B.Increasedonlineoperations 7 14.9

C.Cutpayandjobs. 12 25.5

D. Implemented a remote office (digitaloffice) 2 4.3

Applied for financing, Increased 2 4.3

onlineoperations(A&B)

Appliedforfinancing,Cutpayand jobs(A&C) 8 17.0

Increased online operations, Cut payandjobs(B&C) 4 8.5

Increased online operations, Implemented a remote office (digitaloffice)(B&D) 3 6.4

Thequestionanalysedthe measurestakenbythefirm for improvingtheirownsituation.12of47(25.5)respondents mentionedthattheyhadcutthepayandjobstoself-improve thesituation.Another9respondents(19.2%)reportedthat they have applied for external finance. Further 8 respondents (17%) confirmed that they had used a combinationofapplyingforfinanceandcuttingthepayand jobs. 7 (14.9%) respondents were able to take the safety measure by improving the online operations. 3 (6.4%) respondentshadtakenthecombinationofincreasedonline operationsandimplementingdigitalofficesasself-measure to improve the situation. 2 responses (4.3%) each were obtainedforthefollowingoptions:implementedaremote (digital)office;andacombinationofapplyingforfinanceand increasingtheonlineoperations.

11.Whatpoliciesdoyouexpectthegovernmentwillputin to place to help your firm overcome the difficulties? (Multiplechoice)

No. of Respons es %

A. Reduce, exempt or postpone valueadded tax, income tax, insurance premiumsandothertaxes 10 21.3

B.Stimulateconsumption 4 8.5

C. Allow firms to implement a staged flexiblesalarymethod 1 2.1

D.Providesubsidiesforrent,utilities,post stabilizationetc. 10 21.3

Reduce,exemptorpostponevalue-added tax,incometax,insurancepremiumsand othertaxes,Stimulateconsumption(A&B) 1 2.1

Reduce,exemptorpostponevalue-added tax,incometax,insurancepremiumsand other taxes, Allow firms to implement a stagedflexiblesalarymethod(A&C) 12 25.5

Reduce,exemptorpostponevalue-added tax,incometax,insurancepremiumsand 3 6.4

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

other taxes, Provide subsidies for rent, utilities,poststabilizationetc.(A&D)

Stimulateconsumption,Providesubsidies for rent, utilities, post stabilization etc. (B&D) 1 2.1

Reduce,exemptorpostponevalue-added tax,incometax,insurancepremiumsand other taxes, Stimulate consumption, Provide subsidies for rent, utilities, post stabilizationetc.(A,B&D) 2 4.3

Reduce,exemptorpostponevalue-added tax,incometax,insurancepremiumsand other taxes, Allow firms to implement a staged flexible salary method, Provide subsidies for rent, utilities, post stabilizationetc.(A,C&D) 2 4.3

NONE 1 2.1

Thequestionmeasuredtheexpectationofthefirmsabout thehelpfromthegovernmentdepartments.25.5%(12)of respondentswerepointedoutthatthegovernmentshould reducetheinsuranceandtaxesandaswellasgovernment should allow the firms to implement a flexible payment system to their workers according to their conditions. 10 (21.3%)responseseachwereobtainedfor;theoptionAi.e. reducethetaxesandinsurancepremiums;andtheoptionD i.e.providesubsidiesforrent,utilities,poststabilizationetc. 4 (8.5%) responses were obtained for stimulate consumption.Another3(6.4%)respondedthatgovernment should take adequate measures to reduce/ exempt/ postpone the taxes and insurance premiums and should provide subsidies for the rent, utilities and post stabilisations.2responses(4.3%)eachwereobtainedforthe combinations of: reduce/ exempt/ postpone taxes and insurances, stimulate consumptions, and provide the subsidies; and reduce/ exempt/ postpone taxes and insurances,allowtoimplementflexiblesalarypackages,and providethesubsidies.1responseeachwere obtainedfor: Allow firms to implement flexible salary methods; combinationofreduce/exempt/postponetaxes,insurances and stimulate consumptions; combination of stimulate consumptions, and provide the subsidies. One of the respondentsreportedthatthefirmdoesnotagreewithany ofthegivenoption.

Duringthediscussion/interviewwiththerespondentbythe researcher,andconsideringtheoverallresponsesobtained inthequestionnaire,thefollowingconclusionscanbemade:

Theindustrieswhichareproducingproductsrelatedtothe healthcarewerehadpositiveimpactduringthelockdown days.Becausegovernmentsweregivenrelaxationtothose

industriesandthemedicalproducts/equipmentwashighly movingduetothepandemic.

Similarly, the food processing units were either in the positively affected position or at least in a not affected position. Those who producing the packed/ bakery items were in a positively affected position. Because, due to the lockdownallthefamilymemberswereinsidethehomeand the consumption of packed items were slightly boomed. Whereasthecatering/massfoodproductionunitswerenot having that much sales during the lock down as the gatheringswererestricted

Thoseindustriesproducingnon-perishablegoods/products, are least affected by the lockdown. Their sales during the MarchtoJunemonthswerestopped,butstilltheydidnot havemanylosses.Thegovernmentsalsowerehelpedduring thattimebyextendingthetaxpayment/rent/loanpayment etc.

Theindustryproducingperishablegoods/seasonalproducts etc.hadhighlyaffectedbythelockdown.

Theindustrieswheretheprocessesarealmostmechanised/ automatedwerelessaffected,whereastheindustrieswhich highly dependent on man-power were find difficulty to operateduetotheCOVIDprotocols.

Even the government had given a moratorium period for loans,butthefirmswereinadilemmatorepaytheloanas theinterestwillbecumulatedifunpaidontime.

Similarly,manyoftheindustrieswereinapositiontocutthe salary of the employees, due to the forces from loan payments/un-soldproducts/unusedinventoryetc.

Byreferringtheabovepointstheinvestigatorcanconclude thattheCOVID19affecteddifferentindustriesindifferent ways.Fewoftheindustrieshadpositiveimpactduringthe pandemic whereas the most industries had their negative effectsduetothereducedsalesandconsumptions.Butan overall result shows that very few companies are largely affected by the pandemic which lead them to great losses andbankruptcyandfurtherforforcedshutdown.Whereas, most of the industries could manage the situation by devising their own method according to their situation, regarding the availability of materials and employees, marketdemand,thegovernmentpoliciesetc.

Agrawal,S.,Jamwal,A.andGupta,S.,2020.EffectofCOVID19ontheIndianEconomyandSupplyChain.

Rakshit, B. and Basistha, D., 2020. Can India stay immune enough to combat COVID‐19 pandemic? An economic query.JournalofPublicAffairs,20(4),p.e2157.

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 09 Issue: 12 | Dec 2022 www.irjet.net p-ISSN:2395-0072

Thiagarajan,K.,2021.WhyisIndiahavingacovid-19surge?. Pickert,R.(2020,March26).U.S.JoblessClaimsJumpto3.28 Million, Quadruple Prior Record. Bloomberg. Accessed 28 March 2021 at: https://www.bloomberg.com/news/articles/2020-03-26/usjobless-claims-surged-to-record-3-28-million-last-week