P20 | Ai Tools And Investing. Sebi’s Proposed Reforms

P36 | Harness The Power Of Compounding

P42 | Market Update

Dear Investors,

As we enter 2025, India’s financial landscape shows both optimism and caution. The Union Budget 2025 has significant implications, with GDP growth projected at 6.5%, supported by strong domestic demand and manufacturing.

FROM THE Desk CE O’s

Despite global uncertainties, India's growth prospects and government initiatives offer long-term potential. With a cautious outlook, we remain focused on navigating the evolving market to create value for investors. Let’s explore the latest updates.

The Union Budget 2025

The Union Budget 2025 emphasizes long-term economic sustainability through investments in infrastructure, renewable energy, and digitalization. Key allocations support clean energy and governance digitization to boost growth. The new tax regime makes income up to ₹12 lakh tax-free, easing the burden on salaried individuals and businesses while fostering a growth-friendly economic environment.

The Union Budget 2025

I n February 2025, India's Manufacturing PMI dropped to 56.3 from 57.7 the slowest expansion since December 2023, due to weaker output and sales. However, it stayed above 50, indicating continued growth. Meanwhile, CPI inflation fell to 4.31% in January, its lowest since August 2024, driven by lower food prices. Easing inflation may give the RBI room for potential rate cuts to support growth.

RBI’s Monetary Policy

T he RBI’s decision to maintain the repo rate at 6.25% reflects a cautious yet strategic approach to long-term economic resilience along with inflation control. This decision demonstrates the RBI's commitment to ensuring stability amid global uncertainties and rising commodity prices.

Impact of Rising Dollar and Weakening Rupee on Indian Markets

The strengthening U.S. dollar and weakening rupee have led to

foreign portfolio outflows, increasing market volatility in India. A weaker rupee has raised import costs, particularly for crude oil, worsening inflation and the trade deficit. However, export-driven sectors like IT and textiles benefit from improved competitiveness. The rupee’s recovery hinges on stabilizing capital flows, reducing the trade deficit, and RBI interventions. With improved global conditions and domestic indicators, the rupee could appreciate in late 2025, easing inflation and attracting foreign investment, which would stabilize the market.

Q4 FY25 Earnings Outlook and Market Implications

I ndia’s Q4 FY25 corporate earnings are expected to improve, with Nifty 50 companies projected to see 5.9% revenue growth, 8.6% EBITDA growth, and 6.9% PAT growth YoY. This recovery could stabilize markets and foster cautious investor optimism.

FII activity & Indian Stock Market

I n January, Indian equities saw a $11.75 billion foreign investment outflow due to rising U.S. Treasury yields and a strong dollar. On February 28, the Sensex fell 1.90% and Nifty 1.86%, impacted by global uncertainties and proposed U.S. tariffs. IT and financial sectors faced major losses, while Mahindra & Mahindra, Kotak Mahindra Bank, Maruti, Nestle, and ITC led the gains. India’s long-term market fundamentals remain strong.

Market Correction: A Buying Opportunity for Long-Term Investors

T he Indian equity markets have seen a sharp correction, with the Nifty 50 down 15% from its September 2024 high, while midcap and small-cap indices have fallen over 22-25%. Factors such as weak earnings, foreign outflows, global uncertainties, and inflation have contributed to this downturn. However, history shows that market corrections present long-term investment opportunities, as seen in 2008 when the Nifty 50 rebounded nearly 7x in 15 years.

Currently, large-cap valuations are nearing fair value, with the Nifty 50’s PE at 19.9x, but mid and small caps remain expensive. A strategic approach would be to deploy 30-35% of available funds now and add on dips. Potential catalysts like interest rate cuts and policy reforms could drive future growth. Sectors like FMCG, consumer durables, infrastructure, and chemicals appear attractive.

FII activity & Indian Stock Market

The m arket remains uncertain due to global volatility, a fluctuating US dollar, and domestic inflation. While caution is advised in the short term, the medium-term outlook is positive, driven by infrastructure growth and corporate earnings. Investors should consider phased approaches like SIPs or STPs to manage risks.

“

The current market environment remains uncertain due to global volatility, a fluctuating US dollar, and domestic inflation. In the short term, caution is advised, but the medium-term outlook is positive, driven by infrastructure growth and corporate earnings. Investors should adopt a phased approach via SIPs or STPs to manage risks.

“

Conclusion: While external headwinds persist, India’s economic resilience offers long-term opportunities. Staying informed, diversified, and disciplined will be key to navigating market challenges and capitalizing on India’s growth potential.

Abhinav Angirish Founder & CEO InvestOnline.in

Way to Money Moves Make You Rich

Understanding Generation Z: Digital Natives and Their Growing Financial Influence

Generation Z or Gen Z refers to people born between 1996 and 2010. They are typically characterized by being digital natives, the first generation to grow up with the internet, climate change concerns, and the financial shifts of recent years, including the impact of COVID-19. As the second-youngest generation, they are positioned between millennials and Generation Alpha. Their financial influence is growing, with their consumption power expected to surge in the coming years, especially as they enter the workforce. Known for their research-driven purchasing habit, Gen Z are likely to apply the same diligence to investing.

India has over 377 Million Gen Zers, thats more than the population of the US.

245 M 356 M

Millenials 1981 - 1996

377 M

Gen Z 1997- 2012

159 M

Silent Generation and Baby Boomers 1928 - 1964

Generation X 1965 - 1980

304 M

Gen Alpha 2013+

According to a recent report, India is a young nation with 377 million Gen Z population and they will be the biggest contributor to the country’s consumption growth, driving $1.8 trillion worth of direct spend by 2035.

By 2025, the Gen Z direct spend will total $250 billion, with half of them earning. The report by Snap Inc (NYSE: SNAP), partnered with Boston Consulting Group (BCG) states that Gen Z's collective spending power will surge from $860 billion to $2 trillion by 2035, and they are 1.5 times more likely to research their purchases compared to millennials. This generation is key to India's future consumption trends. A particularly notable aspect is Gen Z's purchasing behaviour, with this generation being 1.5 times more likely to research products before making a purchase compared to millennials. This trend suggests that Gen Z places a higher value on informed decision-making, likely influenced by digital tools, social media, and online reviews that facilitate easy access to product information. The financial and investment habits of Gen Z are heavily influenced by their tech-savviness, preference for self-management, values-driven decision-making, and growing interest in digital assets, particularly cryptocurrencies. These factors contribute to a unique approach to managing money and investing, one that differs significantly from previous generations.

Let’s break down how each of these elements is shaping Gen Z’s financial behaviours:

Tech-Savviness and Digital Finance

- From managing day-to-day finances to investing, Gen Z favours mobile apps and online platforms. They rely on fintech apps for easy money transfers, investments, and budgeting. They expect immediate, on-the-go access to financial tools and information. This reliance on digital finance leads to an increased use of robo-advisors for investment management and tools that automate savings.

Savings and Financial Security - While Gen Z is known for embracing digital investments, they are also conscious of long-term financial security like building an emergency fund. By using digital tools and platforms to automate savings and invest strategically, they are well-positioned to achieve long-term financial stability. This focus on both immediate opportunities and long-term security (such as retirement planning and diversified investments) reflects a comprehensive approach to wealth-building that will shape their financial futures.

Preference for Self-Management - Gen Z is highly self-reliant when it comes to learning about personal finance. They use blogs, social media influencers (finfluencers), podcasts, and YouTube channels to educate themselves on everything from budgeting to investing in stocks and crypto. Many Gen Z investors prefer to use online platforms where they can directly manage their portfolios, rather than relying on a traditional financial advisor. This includes DIY investing in stocks, bonds, and real estate via apps.

Values-driven financial and investment choices - Many Gen Z investors are drawn to sustainable investments like ESG (Environmental, Social and Governance). They prefer to put their money into companies that align with their social, environmental, and ethical values, supporting businesses that advocate for climate action, diversity, and corporate responsibility. Beyond just seeking profits, Gen Z is interested in investments that provide measurable positive social outcomes, such as supporting gender equality or funding green energy start-ups. They see financial success as a way to create meaningful change.

Focus on Digital Assets - A defining trait of Gen Z’s financial and investment behaviours is their interest in digital assets. Growing up with internet and digital technologies makes them more likely to embrace digital currencies like Bitcoins and Cryptocurrencies. They are more inclined to explore decentralized finance platforms (DeFi) that offer alternative ways to earn, lend, and borrow money. Gen Z is also seen engaging with the world of non-fungible tokens (NFTs), a form of digital ownership often associated with art, collectibles, and even virtual real estate. This generation sees NFTs as a blend of investment and culture.

Types of investments and products owned by generation

Data Source: The Motley Fool survey distributed via Pollfish on Jaunary 3, 2025

Social Media Influence - Many Gen Zers follow "finfluencers" (financial influencers) on social media for investment tips, financial advice, and the latest trends in personal finance. This has democratized financial education but also led to the spread of both good and bad advice. Peer pressure and trends on social media also influence Gen Z to participate in certain investment trends or to buy into "hot" stocks and digital assets, sometimes without fully understanding the risks involved.

Investment trends: How Gen Z is shaping their financial future through stocks, mutual funds, and gold.

The investment landscape in India is undergoing a significant transformation, driven largely by the financial behaviours of Gen Z (ages 12-28) and Millennials.

Recent surveys, including The Fin One: Young Indians’ Saving Habits Outlook 2024, conducted in collaboration with Nielsen, have shed light on the evolving approach these young adults are taking toward saving and investing. The survey reveals that 93% of young adults in India are consistently saving money, with many setting aside 20-30% of their monthly income for future financial goals. Interestingly, 45% of respondents expressed a preference for investing in stocks over more traditional options like gold and fixed deposits. This shift highlights the changing investment mindset among India's younger generation, who are increasingly seeking higher returns through the stock market rather than relying on conventional, low-risk investments.

The Fin One study shows that 68% of respondents use automated savings tools and Mobile apps to manage their finances, highlighting the power of digital platforms for this tech-savvy generation.

Key insights from the survey reveal the following trends:

Stocks Over Traditional Investments : According to The Fin One study, 58% of young Indian investors currently allocate their funds to stocks, while 39% prefer mutual funds. In contrast, traditional investment options like fixed deposits (22%) and recurring deposits (26%) have lower adoption rates among this demographic. This trend suggests that young investors in India are adopting a balanced investment approach, aiming for a combination of high returns through stocks and mutual funds, while still seeking stable savings through more traditional, lower-risk options. The shift towards a diversified portfolio reflects the youth's growing financial literacy and their desire for both growth and security in their investments.

Mutual Funds: According to a survey conducted by an asset management company, index funds are more widely preferred by Gen Z and Millennials, with 46-48% of investors under 43 choosing them. This is in contrast to only 35% among Gen X and Boomers.

An Index Mutual Fund invests in a portfolio of stocks that mirror the composition of a specific stock market index such as the NSE Nifty or BSE Sensex. These are passively managed funds, meaning the fund manager aims to replicate the index's performance by investing in the same securities in the same proportions as those in the underlying index, without actively altering the portfolio. The primary goal of these funds is to provide returns that closely match the performance of the index they track, offering investors a cost-effective way to gain broad market exposure with minimal management intervention.

funds are

gold, Nifty, Midcap

etc. The Gen Z prefer index funds over ETFs for better returns and liquidity, comprising 46% of younger investors. A recent report by Axis AMC also highlighted the growing appetite for ETFs, which witnessed net sales of Rs 15,403 crore in October 2024.

10. Hybrid Mutual Funds

Indian index

based on

index,

Gold: Gen Z’s approach to gold has evolved significantly, with digital gold and gold-backed securities emerging as popular investment choices. Gen Z is transforming gold investment trends by combining traditional value with modern convenience. Unlike previous generations, who typically purchased physical gold for adornment or as a symbol of social status, Gen Z is more focused on gold as an investment. This generation distinguishes between gold’s roles as jewelry and investment and is turning to more flexible and accessible options like digital gold and gold-backed securities (such as Sovereign Gold Bonds and Gold ETFs). These investment vehicles offer the advantage of easy access, greater liquidity, and the ability to diversify portfolios, aligning with Gen Z’s preference for convenience and financial growth. This shift reflects how Gen Z is blending tradition with modern investment opportunities.

rising costs of living, including expenses for food, utilities, and transportation. The study also reveals that 68% tech savvy generation’s reliance on digital platforms and technology solutions like automated savings tools and mobile apps help them manage their finances efficiently.

Key areas of improvement for Gen Z in overcoming financial pitfalls

Enhancing

Emergency Preparedness: Emergency preparedness addresses the concern that a significant portion of Gen Z (69%) is not adequately prepared for unexpected financial emergencies. This can include situations like job loss, medical emergencies, or urgent home repairs. The lack of an emergency fund, particularly one that covers at least six months' worth of living expenses in easily accessible liquid assets (such as a savings account), is a key vulnerability for Gen Z. In such a case it is crucial to keep some of your funds stashed away for emergency expenses. Setting up an automatic transfer to the savings every month, so that it happens not having to think about it or being tempted to spend it. In addition to a traditional savings account, it is a good idea to set up a fixed deposit account that offers higher returns (6% approx.) to help build an emergency fund for a long term perspective. However, one must keep in mind liquidity issues and penalty charges on early withdrawal while allocating funds to fixed deposits.

Opportunities for improvement

Gen Z who comprise 30% of the population are in the early stages of their financial journey, and while they have unique advantages, such as being digital natives with access to advanced financial tools, there are several areas where they could improve their approach to investments. The recent study conducted by Fin One on the Saving Habits Outlook 2024 revealed that, 93% of young Indians identify as consistent savers, with most allocating 20-30% of their monthly income for future financial goals. This trend is particularly strong in the 22-25 age group, reflecting an increasing awareness of financial discipline. Despite disciplined habits, 85% of respondents face challenges due to

Improve Insurance Coverage-

The statistic that 72% of Gen Z is underinsured in health coverage and 78% are underinsured in life insurance highlights significant gaps in their insurance protection. This underinsurance could leave many Gen Z individuals vulnerable in the event of unexpected health issues, accidents, or life events. Buying a life insurance is great way to ensure flow of income, financial security and wealth creation at an early age. Buying insurance is much simpler and more DIY for this generation with the advent of technology friendly apps. Life Insurance also alleviate financial instability, allowing one to focus on education, career, and personal growth,

while also easing the repayment of debts and loans. Investing in health insurance and maintaining good health habits is crucial for Gen Z's long-term well-being. This helps avoid potential financial burdens from unexpected medical expenses and ensures the overall quality of life.

Minimize Credit Usage- Gen Z shows a concerning trend of over-reliance on credit, with 1 in 5 individuals having taken out a personal loan. Furthermore, 29% of Gen Z carry both personal loan and credit card debt, underscoring the need for more responsible borrowing practices. Responsible borrowing helps protect from the dangers of overwhelming debt and financial strain by safeguarding credit scores, ensuring timely access to credit, and maintaining a positive reputation as a borrower.

This strategy should be tailored to individual comfort levels and life circumstances, ensuring that investors are neither too risk-averse nor overly exposed to market fluctuations. Essentially, the goal is to make investments work for you without causing undue stress or jeopardizing financial security.

Go for Simple Investments- As advocated by Radhika Gupta, CEO of Edelweiss, the use of straightforward, easy-to-understand financial products are both effectiveand reasonable in financial planning. She believes that choosing simple investment options, such as mutual funds or index funds, doesn’t diminish one’s intelligence or financial acumen. In fact, sometimes complexity can lead to confusion and unnecessary risks. For Gupta, the best investment is a SIP into a balanced advantage fund and a mid/small cap fund.

Financial literacy and skill development- Many Gen Z individuals have access to financial tools but lack comprehensive knowledge about investing, which may lead to poor decision-making. Focus on building stronger foundational knowledge in areas like asset allocation, risk management, investment vehicles (stocks, bonds, ETFs, etc.), and the importance of long-term growth. Investing in educational resources, online courses, and using apps designed to teach investment principles can boost confidence and decision-making.

The way forward

These insights indicate that while Gen Z has made progress in financial awareness and investing, they still face notable challenges in areas like emergency

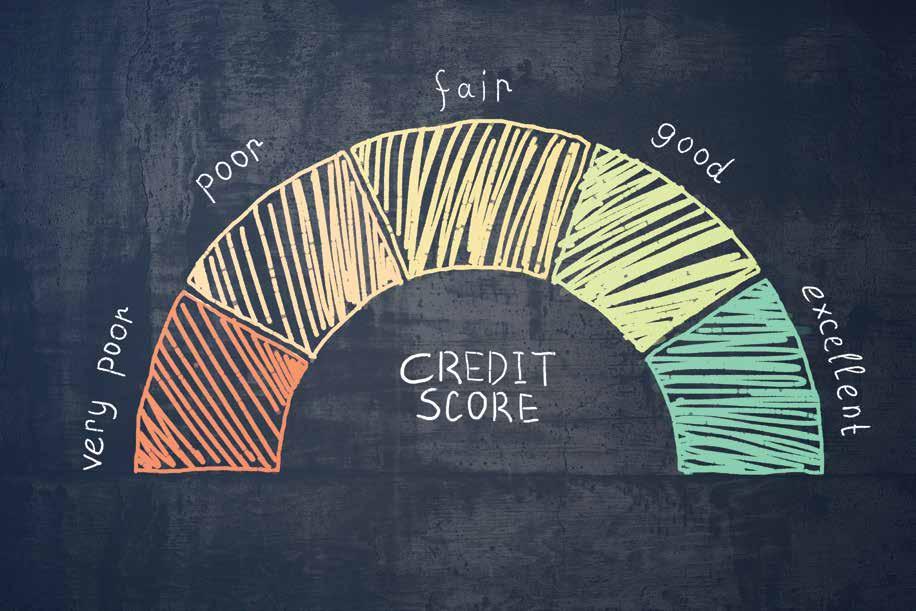

How healthy is your Credit Score?

out what it means for You!

What is Credit Score? What it means, key factors, and tips for improvement

A credit score is a three-digit number ranging from 300 to 900 that reflects an individual's creditworthiness. It is determined by Credit Bureaus also known as credit rating agencies or consumer reporting companies, based on factors such as credit history, loan repayment behavior, credit utilization, and the length of your credit

Your credit score plays a crucial role in major financial decisions. For instance, suppose you're looking

to finance a new car. When you apply for an auto loan, you find out that your credit score is lower than expected. You realize that not working on improving your credit score earlier could cost you. A lower credit score can greatly affect the interest rates and loan terms you’re offered, limiting your options and potentially making the loan more expensive.

I n I ndia, there are four credit bureaus:

• TransUnion CIBIL (Credit Information Bureau (India) Limited

• Experian Credit Information Company of India Private Limited

• CRIF High Mark Credit Information Services Private Limited

Credit Card market in India

In the past, credit cards were not widely accessible to the average Indian consumer due to strict eligibility criteria set by banks and financial institutions. These criteria often included factors like a high income, a stable job, and a good credit history, which made it difficult for many people to qualify for credit cards. However, over the past decade, the landscape has changed significantly.

According to a recent PwC report, the credit card market in India is expected to reach 200 million cards, with a Compound Annual Growth Rate (CAGR) of 15%. The report highlights significant industry expansion, with the number of credit cards issued doubling in the past five years.

This growth trend is set to continue, with the market projected to double again by fiscal year 2028-29, reaching 200 million cards. The industry, having seen a 100% increase in issued cards over the past five years, is on track to replicate this impressive growth within the next five years.

India ranks 8th globally with approximately 120 million active credit cards

REPORT CARD

The total number of credit cards in circulation increased by 18 per cent year-on-year (Y-o-Y) to 103.3 million in May 2024 from 87.4 million in the year ago period. The number of cards in force rose 0.76 million in May.

From poor to excellent: What your Credit Score range really means Your credit score is calculated on a scale ranging from 300 to 900. The higher your score, the more likely lenders are to approve you for new credit. Generally, a score of 750 and above is considered excellent and is highly preferred by lenders when applying for loans or credit cards. While there are various credit scoring models and score ranges, most models follow similar guidelines, which are outlined below:

It is the highest credit rating given by Experian, which indicates that the borrower has never defaulted on any payment. You will be considered a very low-risk borrower and may receive the best loan offer.

If you have a credit score above 750, lenders consider it favourable. It indicares that you have a strong credit record with timely payments and a low risk of default. Generally, 80% of potential borriwers get the loan if they have a credit score above 750.

It indicates a balances credit history the borrowers, which means the borrower has a decent credit history with fair credit managment. You may not qualify for unfavourable interest rate, but you may receive credit from the lender at a higher interest rate.

Lenders consider this score unfavourable as it indicates a high-risk, as the borrower may have defaulted on some payments or has had high credit utilisation. With this score range, you may avail of credit products such as loans or credit cards, but you may be offered higher interest rates.

This rating suggests that the borrower has a bad credit history, such as missed or late payments, high credit utilisation, loan defaults, etc. You will be considered borrower with very high risk and may face difficulty in availing credit. You are advised to improve your credit score if you are in this range.

Courtesy: ET Money

What can impact your Credit Score?

Payment History- Your payment history is a crucial factor in determining your credit score. It reflects how often you miss payments, with loan defaults or late payments negatively affecting your score. To maintain a good credit score, it’s important to manage your debts wisely and consistently make payments on time.

Credit Utilization – This refers to the percentage of your available credit that you use. In India, maintaining a credit utilization rate of under 30% is considered beneficial. Keeping this percentage low demonstrates responsible credit management and can have a positive effect on your credit score.

Length of Credit History: A longer credit history can boost your credit score, especially if you have managed your accounts responsibly over time.

Types of Credit Used: The types of credit accounts you have can also affect your credit score. A diverse mix of credit cards and loans demonstrates your ability to manage various forms of credit responsibly, which can help improve your score.

Credit Checks: When you apply for a new credit product, lenders conduct a hard inquiry on your credit report. Multiple hard inquiries within a short period can negatively affect your credit score, as they may signal a sense of urgency in seeking credit.

Errors in Credit Report: Mistakes in your credit report can negatively affect your credit score. These errors may include incorrect personal details, inaccurately reported late payments, or wrong account balances and credit limits. Such inaccuracies can mislead lenders about your creditworthiness, potentially lowering your score. Regularly reviewing your credit report and disputing any discrepancies with credit bureaus can help minimize the impact of these errors.

Busting common credit score myths, debunked for clarity:

Minimum Payments Are Enough: Paying only the minimum keeps your account current, but interest keeps adding up. Pay off the full balance to avoid extra charges.

Carrying a Balance Builds Credit: Carrying debt doesn’t improve your score. Paying off balances on time boosts your credit score.

Credit Cards Are Too Risky: Credit cards can be beneficial if used responsibly. Paying in full and on time helps build credit without accumulating debt.

Checking Your Score Hurts It: Checking your score is a soft inquiry and doesn’t impact your score. Only hard inquiries (from lenders) affect it.

Credit Cards Are Free: Most credit cards have annual fees. Be aware of these costs and use your card wisely to avoid unnecessary charges.

According to a report by TransUnion CIBIL, consumers who regularly monitor their credit have an average score of 729, while those who don’t monitor their credit score average 712. The report also highlights that 46% of individuals who track their credit saw improvements in their scores within six months, compared to 41% of those who did not engage in self-monitoring.

Simple steps to improve your Credit Score:

Timely Payments: Always pay bills on time to avoid penalties.

Credit Utilization: Keep your credit balances under 30% of your credit limit.

Credit Mix: Use different types of credit responsibly (e.g., credit cards, loans).

Limit Inquiries: Avoid applying for too much credit at once.

AI TOOLS IN INVESTING AND SEBI S PROPOSED REFORMS

Artificial Intelligence reshaping our everyday world

Artificial Intelligence (AI) refers to the ability of machines to perform tasks that typically require human intelligence, such as reasoning, problem-solving, learning, and adapting to new information. AI applications include expert systems, natural language processing (NLP), speech recognition and machine vision. AI systems analyse data, identify patterns, make decisions, and improve over time using methods like machine learning, where they learn from data, and deep learning, which employs neural networks to handle complex information. These systems can also interpret natural language, perceive their surroundings through sensors, and adapt their actions based on feedback, allowing them to carry out a variety of cognitive tasks independently.

AI continues to captivate our imagination, quietly transforming our daily lives at an incredible pace, often without us even noticing. From smart assistants like Siri and Alexa, which simplify everyday tasks, to personalized recommendations on entertainment platforms like Netflix and Amazon, AI is making our digital experiences more tailored and efficient across all areas. Whether in healthcare, aiding early disease detection, or in finance, with AI-driven tools like robo-advisors managing investments, AI is increasingly integrated into our routines, working behind the scenes to enhance the way we live, work, and interact with the world.

This article explores the latest and most exciting developments in the field of AI as tool in investing, customized portfolio management and transforming the length and breadth of wealth management industry.

Artificial Intelligence and the power of AI algorithms in Finance and Wealth Management

In the context of financial services, Artificial Intelligence (AI) refers to the use of advanced technologies to improve and automate processes such as decision-making, customer service, risk management, and data analysis. AI can help financial institutions, like banks and insurance companies, make faster and more accurate decisions by analysing large amounts of data quickly. For example, AI is used in fraud detection by identifying unusual patterns in transactions, in credit scoring by evaluating an individual's creditworthiness more accurately, and in customer service through chatbots that provide instant support. AI also powers investment strategies by analysing market trends, and helps in regulatory compliance by automatically monitoring transactions for suspicious activity. Overall, AI enhances efficiency, reduces human error, and provides better, more personalized services to customers. The disruptive power of Generative AI extends beyond banking to wealth management, insurance and payments, transforming customer engagement, transaction processing and fraud detection.

As AI contin ues to evolve, its influence on personal finance management is expected to expand significantly. Algorithms are already playing a pivotal role in reshaping how individuals manage their wealth, offering more personalized, efficient, and data-driven solutions. From automated budgeting tools to AI-powered robo-advisors, these systems are making financial planning more accessible and tailored to each person's unique financial goals and risk tolerance.

• Asia’s wealth managers aim to double assets under management by 2026, with relationship managers expected to drive 90% of the growth.

• While Generative AI isn’t a one-size-fits-all solution, it could generate hundreds of millions in revenue for wealth firms.

• Generative AI enables firms to personalize investment content, turning generic updates into tailored insights that drive client action and loyalty.

Source: Accenture

As AI technology advances, we can expect even greater improvements in areas such as investment strategies, debt management, and retirement planning, making personal wealth management more intuitive and effective than ever before.

Use cases of Generative AI in Wealth Management

Automation Through AI - powered tools : This is one of the most transformative aspects of personal finance today. By leveraging artificial intelligence, these tools streamline routine financial tasks, making them faster, more efficient, and less prone to human error. Handling routine tasks like tracking expenses, managing bills, budgeting and saving for the future are some of the automated systems that help individuals stay on top of their financial goals with less effort.

Personal Insights: AI’s ability to provide personalized insights is one of its most powerful applications in personal finance. By analysing individual spending patterns, financial goals, and even behavioural trends, AI can offer tailored recommendations that are far more specific and actionable than general financial advice.

Risk Management: AI helps individuals assess and reduce financial risks by forecasting market trends, detecting transaction anomalies, and providing real-time alerts on potential security threats.

Improved Security: AI technologies boost the protection of personal financial data with advanced encryption, biometric authentication, and fraud detection algorithms.

Better Decision-Making: AI analyses large volumes of data and identifies key patterns, helping individuals make informed financial decisions, such as the best times to buy or sell investments and optimize tax strategies.

Blue Dot Robo Advisors

Challenges and considerations

The adoption of AI in personal finance management offers many advantages but also presents several significant challenges. Privacy and data security are major concerns, as AI systems require access to sensitive financial information, increasing the risk of cyberattacks and data breaches. AI algorithms may unintentionally adopt biases from the data they are trained on, resulting in unfair outcomes and discrimination, especially toward marginalized groups. The lack of transparency in AI decision-making processes, often referred to as "black box" algorithms, complicates accountability, as it can be difficult to understand how certain financial recommendations are made. The fast development of AI is outpacing current regulations, causing uncertainty about compliance with data protection and financial laws. There are also technical barriers, such as the digital divide, where not everyone has access to the necessary technology or skills to fully utilize AI-driven tools, worsening inequalities in financial services. Lastly, an over-reliance on AI for financial decisions could lead to a loss of human touch and personalized advice, as well as decision fatigue, where users disengage from actively managing their finances. Addressing these challenges is essential to ensure that AI can be effectively and ethically in tegrated into personal finance management.

Regulatory bodies must keep pace with the evolving AI-driven finance landscape by creating clear guidelines and frameworks for its use in personal finance management. Establishing standards for data governance, algorithm transparency, and consumer protection is essential to ensure the integrity and trust of AI-powered financial services. Furthermore, financial institutions and service providers must prioritize regulatory compliance and risk management in their AI initiatives.

SEBI’s proposed regulations on AI for financial markets

AI is being increasingly adopted in investor services and compliance operations. Its use is helping stakeholders make more informed decisions, playing a growing role in market analysis, stock selection, investment strategies, and portfolio management of their securities. Recognizing the benefits of AI, such as improved efficiency, accuracy, and risk management, as well as the need for investor protection, SEBI has previously required entities like stock brokers, depositories, and mutual funds to report their use of AI. SEBI added that there is “a pressing need to assign responsibility on market infrastructure institutions, intermediaries and persons regulated by SEBI that use AI/ML (artificial intelligence or machine learning) in the conduct of their business and related activities to bring in more seriousness to such users while deploying AI/ML tools and at the same time ensure investors’ protection.”

"Every person regulated by Sebi that uses such artificial intelligence tools and techniques while conducting its activities in the securities markets and for servicing its clients, regardless of the scope and size of adoption of such tools, shall apart from complying with all applicable laws in force be solely responsible for all the consequences of such use including ensuring the privacy, security and integrity of the investors' and stakeholders' data especially the data maintained by it especially the data maintained by it in a fiduciary capacity, throughout the processes involved."...and shall be responsible if the output arising from the usage of such tools and techniques is relied upon or dealt with," Sebi said.

With every SIP, your wealth will gleam, Like Holi's colors, a vibrant dream! Don't just wish, take a smart SIP, With InvestOnline, let fortunes flip!

BUDGET 2025 KEY HIGHLIGHTS

The Middle-Class Boom, Tax Relief, Agricultural Reforms & More

On February 1, 2025, Finance Minister Nirmala Sitharaman presented her eighth consecutive Union Budget, outlining a vision for India's growth with a strong focus on agriculture, energy, and international trade. Wearing a Madhubani silk saree, a tribute to Bihar’s cultural heritage, she announced several significant measures, including tax relief for the middle class with no income tax on earnings up to ₹12 lakh, the launch of the PM Dhan-Dhaanya Krishi Yojana, and the creation of a Makhana Board.

The budget also highlighted initiatives like Aatmanirbharta in pulses and a new Nuclear Energy Mission. Calling it a budget "by the people, for the people," the Finance Minister’s proposals sparked discussions, even as they made waves in political circles. Amid an economic slowdown, with GDP growth at 6.4% compared to the 8.2% projected in the previous year, the government reiterated its commitment to unlocking India's potential under PM Modi's leadership. Finance Minister Sitharaman emphasized that Budget 2025 is focused on accelerating growth, viewing the next five years as a crucial period for realizing "Sabka Vikas" (development for all). With a focus on the Garib, Youth, Annadata, and Nari Shakti, she proposed major initiatives across 10 key areas to drive inclusive growth and strengthen the economy.

Major initiatives and key features of the Union Budget for the next financial year (2025-26):

The Path to Progress - Engines of Development

• Agriculture

• MSME

• Investment

• Exports

The driving force: Reforms

The guiding principle: Inclusivity

The goal: Viksit Bharat (Developed India)

Aspirations for Viksit Bharat

• Economic growth

• Technological upgradation

• Infrastructure development

• Social empowerment

• Sustainability

“Bharat cannot limit reform to just economic reforms. We must move forward in every aspect of life towards the direction and reform.

Our reforms should also align with the asperations of a VIKSIT BHARAT by 2047”

Shri Narendra Modi

Key Highlights of Budget

2025: A Path to Growth and Inclusivity

• New Tax Regime: Finance Minister Nirmala Sitharaman proposed a revised tax structure, offering a significant relief with zero income tax on earnings up to ₹12 lakh under the new regime.

• Capital Expenditure (Capex): The budget for FY2025-26 has allocated ₹11.21 lakh crore for capital expenditure, a rise from ₹11.11 lakh crore in FY2024-25, reflecting a strong push for infrastructure development.

• Bihar Makhana Board: A major initiative in Budget 2025 includes the creation of a Makhana Board in Bihar to boost production, processing, and marketing, strengthening India's position in the Makhana industry.

• Job Creation Scheme: The government has unveiled plans to generate 22 lakh jobs, particularly in the footwear and leather sector, aiming to enhance productivity, quality, and global competitiveness.

• UDAN Scheme Expansion (Aviation): A revamped UDAN scheme is set to enhance regional connectivity, with plans to add 120 new destinations and serve 4 crore passengers over the next decade.

• Supporting MSMEs: Enhanced funding options and credit facilities for medium and small businesses.

• Housing & Urban Development: The raise of TDS exemption limit on rental income from ₹2.4 lakh to ₹6 lakh and simplifies the TDS framework by reducing rates and increasing deduction thresholds for clarity.

• Education schemes: Key education initiatives, including 50,000 Tinkering Labs, national skilling centres, fellowships for tech researchers, broadband for rural schools and health centres, the Bharatiya Bhasha Pustak Scheme, and a ₹500 crore Centre of Excellence in AI for education

Sector-wise breakup of Budget 2025's major announcements:

Agriculture:

• Adopt crop diversification

• Improve irrigation facilities

• Facilitate short-term loans for 7.7 crore farmers, fishermen, and dairy farmers with enhanced loans of ₹5 lakh

• Six-year new mission for Atmanirbharta in pulses with a special focus on Tur, Urad, and Masoor

• Five Year Missions to facilitate improvement in cotton productivity

• Makhana board in Bihar; to improve production, processing, value addition, marketing

• A national mission on high-yielding seeds

• Sustainable harnessing of fisheries with a focus on Andaman and Nicobar and Lakshadweep

• Ample opportunities in rural areas so migration is an option and not a necessity

• The Focus Product Scheme for Footwear and Leather to create 22 lakh jobs, generate ₹4 lakh crore in turnover and boost exports by over ₹1.1 lakh crore

• India Post will be transformed into a major public logistics organization to support Viswakarmas, entrepreneurs, women, self-help groups, MSMEs, and large businesses

Healthcare & Education:

• Improved access to lifesaving medicines

• Addition of 36 lifesaving drugs/medicines in the exempted list; 6 medicines in 5% duty list; 37 medicines and 13 new patient assistance programmes in the exempt list. (Medicines for rare diseases, cancer, severe chronic diseases)

• 10,000 seats to be added in medical colleges and hospitals in FY26

• To set up day-care cancer centres in all district hospital

• Broadband connectivity to primary health centres in rural areas

• 50,000 Atal Tinkering Labs to be set up in govt schools in the next 5 years to cultivate the spirit of curiosity and innovation, and foster scientific temper

• A proposal to launch the Bharatiya Bhasha Pustak Scheme, offering digital Indian language books for school and higher education.

• Five National Centres of Excellence for skill development will be established.

• Additional infrastructure will be created at the five IITs established post-2014 to accommodate 6,500 more students.

• A Centre of Excellence in Artificial Intelligence for education will be set up.

• A new scheme will be launched to promote the socio-economic upliftment of urban workers, aimed at enhancing their income opportunities.

Development of Nuclear Reactors in India:

• ₹20,000 crore has been allocated for the development of small nuclear reactors, targeting the generation of 100 gigawatts of nuclear energy.

• Five indigenous small nuclear reactors are set to be developed by 2033.

Infrastructure and Economy Highlights:

• Each infrastructure ministry will create a 3-year project pipeline for implementation through the PPP (Public-Private Partnership) mod e.

• States will be encouraged to prepare similar pipelines and can access support from the IIPDF (India Infrastructure Project Development Fund) for PPP proposals.

• The government will provide ₹1.5 lakh crore in 50-year interest-free loans to states for infrastructure development.

• A Maritime Development Fund with a corpus of ₹25,000 crore will be established.

• A new policy will be introduced for the development of critical minerals.

DIRECT TAX

Key Highlights of the New Income Tax Bill:

• A new Income Tax Bill will be introduced next week.

• No income tax will be levied on earnings up to ₹12 lakh per annum.

• Salaried individuals will pay no tax on ₹12.75 lakh due to a ₹75,000 standard deduction.

• Tax slabs and rates will be revised across the board.

• A simplified tax structure is proposed under the new Income Tax Bill.

New Tax Slabs

• Up to ₹ 4 lakh – No tax

• ₹ 4 lakh – ₹ 8 lakh – 5%

• ₹ 8 lakh – ₹ 12 lakh – 12%

• ₹ 12 lakh – ₹ 16 lakh – 15%

• ₹ 16 lakh – ₹ 20 lakh – 20%

• ₹ 20 lakh – ₹ 24 lakh – 25%

• Above ₹ 24 lakh – 30%

Rationalization

of TDS/TCS for easing difficulties

Tax deduction limit for senior citizens doubled from ₹ 50,000 to ₹ 1 lakh.

A B C

D

Reducing compliance burden

Reduced compliance for small charitable trusts / institutions by increasing their period of registration from 5 years to 10 years.

Tax payers to be allowed to claim the annual value of 02 self occupied properties (previously 01) without any conditions (previously conditions attached).

Encouraging voluntary compliance

Extention of time limit to file updated returns, from the current limit of two years, to four years.

Employment and Investment

• Tax certainty for electronics manufacturing schemes

• Tonnage Tax Scheme for Inland Vessels

• Extention for incorporation by 5 years of Start-Ups

• Specific benefits to ship-leasing units, insurance offices and treasury centres of global companies which are set up in IFSC

• Certainty of taxation Catagory I and catogory II AIFs, undertaking investments in infrastructure and other such sectors, on the gains from securities.

MSME:

• Startup Funding: An additional ₹10,000 crore will be allocated to support startup incubation programs, fostering innovation and growth.

• MSME and Start-Up Credit Expansion: Enhanced credit guarantees will ease access to finance for MSMEs and startups, aiding recovery.

• Support for Gig Workers: Gig workers will receive health insurance under PM-JAY, along with identity cards and registration on the e-Shram portal for better welfare benefits.

• Research and Innovation: ₹20,000 crore will be invested in private-sector-driven research and innovation to support technological advancements.

• Revised MSME Classification: Investment and turnover limits for MSMEs will be increased, allowing more businesses to benefit from incentives.

• Boost for Footwear & Leather Industry: A new scheme aims to create 22 lakh jobs, generate ₹4 lakh crore in revenue, and drive ₹1.1 lakh crore in exports.

• Boost for the Toys Industry: A dedicated scheme will position India as a global hub for high-quality, made-in-India toys.

RESEARCH, DEVELOPMENT,

• ₹20,000 crore allocated for private sector-driven R&D and Innovation initiatives from the July Budget.

• Exploration of a Deep Tech Fund of Funds to boost next-gen st artups.

• 10,000 fellowships for tech research in IITs and IISc under the PM Research Fellowship scheme with increased financial support.

• Launch of a National Geospatial Mission.

₹1 LAKH CRORE

Set-up of Urban Challenge Fund

SWAMIH Fund 2: For completion of stressed housing project

Rationalisation of threshhold for withholding tax on rental income

₹2,40,000 ₹50,000

₹15,000 CRORE per annum per month or part of month

Technology And Telecom

₹6.81 LAKH CRORE ~13.44% Defence Budget of FY2025

Capital expenditure increased to ₹1.8 lakh crore of the total budget

₹20,000 CRORE

Allocated for India AI Mission

Setup of GCCs in tier 2 cities

BharatNet Project expenditure increased from

National framework for ₹6,500 CRORE Telecommunications Computer, & Information Services to India ranks as the second largest exporter in the world in ₹22,000 CRORE

Key Budget Numbers and Fiscal Policy:

• FY25 fiscal deficit estimated at 4.8%, and 4.4% in FY26.

• FY25 revised capex pegged at ₹10.18 lakh crore.

• Asset monetization plan to generate ₹10 lakh crore.

• FDI in the insurance sector to be increased to 100% from 74%.

• Foreign investment conditions to be reviewed and simplified.

• A forum for regulatory coordination on pension issues to be e stablished.

Conclusion Thoughts

In conclusion, the Union Budget 2025 lays out a strong plan to boost India's growth by focusing on key areas like innovation, education, and infrastructure. With measures to encourage private sector investment, increase foreign investment, and improve skills development, the budget aims to create more opportunities for the economy to grow. It also focuses on uplifting urban workers and supporting new technologies. Overall, the budget sets a positive path for a more inclusive and digitally advanced India.

How does compounding work?

Power of Compounding, what it means and how is it calculated

Compounding is essentially the magic of compound interest working on your money. In the context of investments, compounding refers to the process where the earnings on an investment (such as interest or dividends) are reinvested to generate additional earnings over time. The key concept in investment compounding is that not only the initial investment (principal) earns a return, but also the returns that have already been earned begin to generate their own earnings. The more frequently the earnings are reinvested, the faster the investment grows. This growth helps your wealth steadily increase as you invest, helping you to achieve your financial goals. By reinvesting earnings and letting them compound, you can accelerate the growth of your wealth, making it easier to achieve long-term financial goals such as retirement, buying a home, or funding education.

Compounding occurs when the earnings on an investment such as interest, dividends, or gains are reinvested, allowing you to earn returns on both your original investment (principal) and the accumulated earnings. This creates a cycle where your wealth grows at an increasingly faster rate over time, as each new return earns more returns. Essentially, compounding makes your money work for you by continuously generating additional returns on previously earned income.

To calculate compound interest, the formula used is:

A=P(1+nr)nt

Where:

• A = The total value of the investment after interest (including principal and interest).

• P = The principal amount (initial investment).

• r = The annual interest rate (expressed as a decimal).

• n = The number of times the interest is compounded per year.

• t = The number of years the money is invested.

Understanding compound interest with an example:

Imagine you invest Rs 15,000 at an 8% annual interest rate. Here's how your investment grows:

Year 1: You earn Rs 1,200 in interest, bringing your total to Rs 16,200.

Year 2: Now, you earn 8% on Rs 16,200, which amounts to Rs 1,296. Your new total balance becomes Rs 17,496.

Year 3 and beyond: Each year, the interest you earn is reinvested, increasing the principal for the next year's interest calculation.

This cycle of earning "interest on interest" leads to exponential growth. For instance, after 30 years, your initial Rs 15,000 investment at 8% annual interest would grow to over Rs 150,000, illustrating the powerful impact of compounding over time.

The Power of Compounding with SIPs in Mutual Funds

Investing in mutual funds offers two main approaches: lump sum investments and Systematic Investment Plans (SIPs). While both methods can be effective depending on your financial goals, SIPs have gained popularity due to their flexibility and ability to start with smaller amounts. SIPs are particularly beneficial for those looking to build wealth over time, as they harness the Power of Compounding. By consistently investing a fixed amount each month, you can gradually accumulate wealth and achieve substantial growth.

Strategies to maximize the benefits of compounding in SIP mutual fund investments

• Start Early -Time is the key to unlocking the true power of compounding. Investors can harness the full potential of compounding by starting early and maintaining consistency with their SIPs. Even small, regular investments can grow significantly over time. The longer your investment horizon, the greater the compounding effect.

For example, if two individuals start an SIP at age 30 and age 40, respectively, contributing the same amount, the person who begins at 30 will likely accumulate a larger corpus. This is because their money has had more time to compound, even if the second investor continues contributing for a longer period.

• Stay Consistent: Consistency plays a key role in SIP investments. By contributing a fixed amount regularly, regardless of market fluctuations, you can take advantage of rupee cost averaging. This strategy allows you to average the cost of your investments over time by consistently investing a set amount. SIPs automatically allocate a fixed sum to the plan, and you receive units based on the net asset value (NAV). As a result, the overall acquisition cost is lowered, and you can smooth out the impact of market volatility. Additionally, it’s important to avoid sudden withdrawals, as liquidating assets before the investment period may cause you to miss out on the compounding benefits you’ve accumulated.

• Reinvest Capital Gains and Dividends: Reinvesting capital gains and dividends means that instead of taking the profits or income you earn from your investments as cash, you use that money to purchase more units of the same mutual fund or stock. This process helps you take full advantage of compounding, which is the ability of your investment returns to generate their own returns over time. For example, if you receive a dividend payment from a mutual fund, reinvesting it means the dividend is used to buy more units of the fund. These additional units will, in turn, generate more returns in the future. Over time, this reinvestment leads to exponential growth because your investment is continually growing on a larger base.

• Select Mutual Funds with the Highest Growth Potential: To fully leverage the power of compounding, focus on researching and choosing mutual funds with the greatest growth potential. Look for funds that have shown strong performance in recent years. Evaluate other important aspects like the expense ratio, asset allocation, and risk profile to get a comprehensive view of the mutual fund. Lastly, if you're new to investing, it's wise to consult a financial expert before making any investment decisions to ensure you're choosing the right scheme for your needs.

So, with discipline, homework and long-term vision, enormous wealth can be created with the amazing power of compounding. It’s no wonder that the investors who created enormous wealth, are those, who stayed invested for a long time. Raise your investments via SIP Top-ups with rising income to harness the power of compounding. Identify a mutual fund that is in line with your financial goals and start investing via SIPs. Use SIP Calculator Tool at www.InvestOnline.in

Compounding of wealth

Below is table of returns given by different schemes over period of 15 years assuming Rs 50,000 SIP is done every month.

India Prima Fund

Birla Sunlife Flexi Cap Fund

Prudential Bluechip Fund

Magnum Global Fund

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns. The value of investments may fluctuate due to various factors, including market conditions, economic developments, and interest rate changes.

Smart investing starts here

Use InvestOnline's SIP Calculator and see your wealth grow!

MARKET UPDATE

Indices Performance Jan to Feb 2025

Some Recently Announced Bonus

The literacy gap between men and women continues to be significant, with a difference of 17.2 percentage points.

The Abchlor Foundation is dedicated to transforming lives by equipping individuals with financial literacy skills that open doors to better opportunities. With your help, we can empower young girls to finish their education and foster lasting change in communities.

If you want to be a part of this movement, contact us at InvestOnline.in