EDITOR’S NOTE

DECEMBER 2025

VOLUME 25

ISSUE 55

DECEMBER 2025

VOLUME 25

ISSUE 55

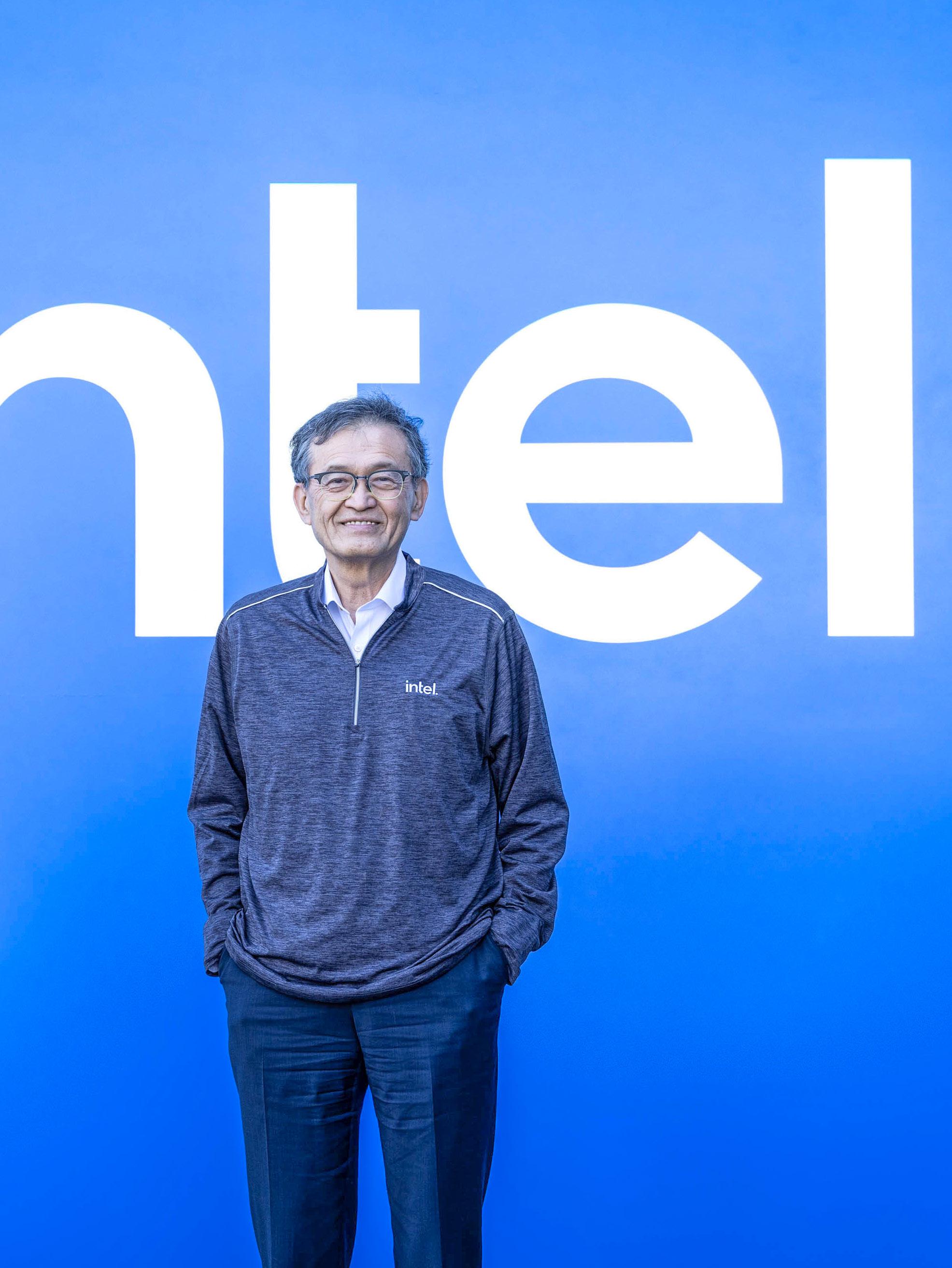

Intel, long regarded as a cornerstone of Silicon Valley, has faced mounting financial and competitive pressures under former CEO Pat Gelsinger. During his tenure, the company ceded technological leadership to rivals such as AMD and NVIDIA, particularly in advanced chips and AI. In response, Intel reinstated former board member Lip-Bu Tan as CEO in March 2025. A venture capitalist celebrated for steering Cadence Design Systems to a 3,200% surge in stock value, Tan is known for his bold, risk-tolerant leadership style. He now leads an aggressive turnaround strategy aimed at restoring innovation, rebuilding market share, and regaining investor confidence.

The year 2025 saw a significant surge in gold prices, marking a historic change in the market. Gold climbed 54.66% compared to 2024, reflecting persistent geopolitical tensions, inflation concerns, and strong central bank demand across both advanced and emerging economies. The rally culminated in October, when prices peaked at $4,381.58 per ounce, highlighting the metal’s renewed appeal as a safe-haven asset amid heightened global market volatility.

Looking at the Southern Hemisphere, Australia’s postpandemic recovery has begun to lose steam as the effects of sustained monetary tightening take hold across households and businesses. The recently released labour force data showed unemployment rising 4.5% since September, signalling a cooling jobs market, softer hiring intentions, and marking a clear departure from the era of ultra-low unemployment.

In the final edition of 2025, International Finance will examine the changing relationship between Saudi Arabia and the United States due to shifting geopolitical and economic priorities. Crown Prince Mohammed Bin Salman and Donald Trump have exchanged visits, overseeing agreements in energy, AI, and aviation—moves expected to advance the Kingdom’s Vision 2030 ambitions and deepen long-term strategic and investment cooperation.

editor@ifinancemag.com www.internationalfinance.com

The US and Saudi Arabia took decisive steps to strengthen their networks in critical minerals, aviation, and defence

ECONOMY

AUSTRALIA’S 'SOFT LANDING' AT RISK

A stronger Australian dollar makes imports cheaper, which provides a disinflationary impulse for tradable goods

UAE’S GREAT FISCAL TRANSFORMATION

Throughout 2025, the UAE maintained top-tier sovereign credit ratings, with Moody's rating it at Aa2, S&P at AA, and Fitch at AA-

CREATOR ECONOMY MONETISES ISOLATION

The creator economy is not a trend to be dabbled in but a condition to be mastered

FEAR TRADE SENDS GOLD SOARING

FEATURES

48 The making of a crypto dynasty 82 Demis Hassabis expands tech throne

When the board appointed Lip-Bu Tan as Intel CEO in March 2025, they handed the keys to a demolition expert 30 42 82 16

The World Gold Council notes that the metal has impressively set over 50 all-time highs in 2025 alone

GREEN CAPITALISM: A DEAD END

Eco-commerce delays action as capitalism’s growth imperative collides with ecological limits, producing greenwashing and injustice

LIP-BU TAN’S BRUTAL INTEL RESET

Director & Publisher Sunil Bhat

Editorial

Prajwal Wele, Agnivesh Harshan, CL Ramakrishnan, Prabuddha Ghosh

Production Merlin Cruz

Design & Layout Vikas Kapoor

Technical Team

Prashanth V Acharya, Bharath Kumar

Business Analysts

Alice Parker, Indra Kala, Stallone Edward, Jessica Smith, Harry Wilson, Susan Lee, Mark Pinto, Richard Samuel, Merl John

Business Development Managers Christy John, Alex Carter, Gwen Morgan, Janet George

Business Development Directors Sid Jain, Sarah Jones, Sid Nathan

Head of Operations Ryan Cooper

Accounts Angela Mathews

Registered Office INTERNATIONAL FINANCE is the trading name of INTERNATIONAL FINANCE Publications Ltd 843 Finchley Road, London, NW11 8NA

Phone

+44 (0) 208 123 9436

Fax

+44 (0) 208 181 6550

Email info@ifinancemag.com

Press Contact editor@ifinancemag.com

Associate Office

Zredhi Solutions Pvt. Ltd. 5th Floor, Sai Complex, #114/1, M G Road, Bengaluru 560001 Ph: +91-80-409901144

17: the OnePlus 15R, the OnePlus Pad Go 2, and the OnePlus Watch Lite. The company has revealed more details about the trio. Let's start with the OnePlus 15R smartphone. This is now confirmed to come with an AMOLED screen boasting "1.5K" resolution and a 165Hz refresh rate. The panel can go down to 2 nits at night, or even 1 nit when you activate Reduce White Point.

The Central Bank of Oman (CBO) has approved the fee structure for the national payment card "Maal," to be used for consumer debit and prepaid purposes, which was announced alongside the pilot launch of the product on November 20. While banks will issue the card to their customers, wider issuance and acceptance will come in the period thereafter. The initiative seeks to enhance the national payments framework by reducing costs for banks, merchants, and PSPs, and by expanding the use of digital payment methods across sectors. The approved framework includes the following: full exemption from card issuance fees and waiving annual fees for cardholders.

Germany's federal investigation agency, BKA, said that, in collaboration with Swiss and German law enforcement agencies, it had taken down cryptomixer.io, one of the biggest platforms used to obscure the trail of illicit bitcoin transactions. BKA worked with the regional prosecutor in Frankfurt and Zurich to shut down the site, which had been in operation since 2016 and was one of the largest bitcoin mixers. Three servers were seized in Switzerland alone. The entity made billions of euros in revenue, primarily derived from criminal activities.

NVIDIA released a new open-source software program designed to accelerate the development of self-driving cars using some of the latest "reasoning" techniques in AI. The world's most valuable tech giant has a large software research arm that releases open-source AI code for others, such as Palantir Technologies. The software, called Alpamayo-R1, is a vision-language-action AI model, meaning the self-driving car interprets what its sensor banks pick up on the road into a description using natural language.

Source:

South Africa reported that the economy grew 0.5% in the third quarter of 2025, slower than the 0.9% recorded in the second quarter, according to data from the country’s statistics agency. The third-quarter growth rate, in seasonally adjusted quarter-on-quarter terms, was in line with the median forecast of analysts polled by Reuters. Nine of the 10 sectors monitored by Statistics South Africa registered an increase in

output, with mining and agriculture performing well, although electricity, gas, and water contracted. Africa’s largest economy has struggled to gain traction over the past 10 years, with annual GDP growth averaging below 1%, according to the National Treasury, which expects growth to pick up slightly to 1.2% in 2025 and 1.5% in 2026. Third-quarter GDP increased 2.1%, beating economists’ expectations of 1.8% growth.

PATRICE MOTSEPE

FOUNDER OF AFRICAN RAINBOW MINERALS

Patrice Motsepe has proposed a major copper venture in Papua New Guinea with US firm Newmont Corporation, signalling significant cross-continental investments in the decarbonisation era of mining

BADR JAFAR

FCEO OF CRESCENT ENTERPRISES

Badr Jafar got recognised for his philanthropic and climate-change-related efforts, as he was appointed as Special Envoy for Business & Philanthropy for the UAE, apart from getting honours

KHALIFA JUMA AL QAMA

FOUNDER OF OPSYS

Khalifa Juma Al Qama’s push for updated fire safety norms across the globe, along with the leadership in the critical tech sector, has made him among the entrepreneurs to watch in 2025

Kuwait Petroleum Corporation recently opened several job vacancies, which generated high interest from young Kuwaiti applicants

Exports, which too faced similar protectionist measures, saw its shares of slump, with the total trade affected was worth about $2,966 billion

Kuwait Petroleum Corporation (KPC) CEO Sheikh Nawaf Al-Saud recently announced that the discovery of three offshore wells was an "unprecedented global achievement," adding that all operational work on the wells has been completed, with three more discoveries to be announced once their technical assessments are completed.

Speaking to reporters after the corporation's "Excellence Award" ceremony, Al-Saud said that the three newly discovered offshore wells, Al-Nukhatha, Al-Jali'a, and Jaza, have formed a system of promising hydrocarbon reservoirs. Although it is premature to provide specific numbers on production capacity or reserve volumes, preliminary results indicate a very positive outlook for Kuwait's offshore exploration programme.

Al-Saud also pointed out that the Kuwaiti oil sector was at the beginning of a new era that would include discoveries, organisational development, and strengthening of national talent, adding that KPC was moving on a clear strategic path to secure significant economic and strategic gains for the country in the years ahead.

He emphasised that the corporation has only one priority, maximising revenues from natural resources in Kuwait, but he insisted that “human capital is more important than oil itself.” He also expressed appreciation for the hard work of the KPC workforce, calling them the “driving force behind the sustainable success of KPC and its subsidiaries.”

KPC recently opened several job vacancies, which generated high interest from young Kuwaiti applicants. Vacancies are announced periodically as needed, AlSaud said, reiterating that youth should concentrate on academic excellence and professional development to compete effectively for positions in what he described as a rapidly expanding and increasingly diverse oil sector.

Regarding the status of ongoing merger plans within the oil sector, Al-Saud stated that integration efforts are proceeding in accordance with a comprehensive, phased strategy, unaffected by administrative or structural changes. He stated that the consolidation process will significantly accelerate in 2026.

Also, the transfer of the gas plant from the 'Kuwait Oil Tanker Company' to the 'Kuwait National Petroleum Company' has already been completed.

According to the World Trade Organisation (WTO) report, imports worldwide worth $2,640 billion were affected primarily by tariffs and other trade measures introduced between mid-October 2024 and mid-October 2025, more than four times the $611 billion coverage recorded in the preceding period.

Exports, which too faced similar protectionist measures, saw their share slump, with the total trade affected worth about $2,966 billion, more than three times the $888 billion recorded in the global body's previous report.

Over the same period, WTO members and observers also introduced a large number of new trade-facilitating measures on goods, 331 in total, covering trade estimated at $2,090 billion, approximately 1.5 times higher than the $1,441 billion recorded in the last report.

WTO Director-General Ngozi Okonjo-Iweala said, "The sharp jump in the trade coverage of tariffs reflects the increased protectionism we have seen since the start of the year. Nearly a fifth, 19.7%, of world imports are now affected by tariffs and other such measures introduced since 2009, compared to

12.6% only a year ago."

"At the same time, we see members acting to facilitate trade and engaging in dialogue rather than retaliation. This speaks to the value they continue to see in maintaining smooth cross-border trade flows. WTO members should use the current trade disruptions to advance long-overdue reforms of the WTO. Members have an opportunity to tackle some of the underlying concerns linked to recent unilateral measures, while repositioning the WTO to better help them seize exciting new trade opportunities," the official added.

WTO economists estimate world merchandise trade growth at 2.4% in 2025 and at 0.5% in 2026, with stronger-than-expected trade growth in the first half of 2025 driven by import frontloading, strong demand for AI-related products, and continuing trade growth among most WTO members, particularly developing economies.

During the review period, WTO members initiated 32.3 trade remedy investigations per month, just below the 2024 peak of 37.3 per month. While trade remedy investigations do not necessarily lead to the imposition of measures, a higher number of probe initiations often signals a potential increase in measures imposed.

The deployment of the quantum computer marks a massive step in accelerating the development of quantum applications in Gulf region

The new warehouse is also part of the €500 million investment DHL Group has planned for the Middle East through 2030

World's leading integrated energy and chemical giant Saudi Aramco, in partnership with Pasqal, a global leader in neutral-atom quantum computing, has achieved a breakthrough for the Middle East’s tech landscape by successfully deploying Saudi Arabia’s first quantum computer, which also became the region's first dedicated to industrial applications. The deployment of the quantum computer, powered by Pasqal's neutral-atom technology at Aramco’s Dhahran data centre, marks a massive step in building regional expertise and accelerating the development of quantum applications in the broader Gulf region. Aramco is currently looking to leverage tech route to enhance its operational efficiency. This milestone is expected to spur further innovation partnerships across the Kingdom and beyond.

Bank of Singapore (BOS) plans more investment in hiring and technology as it seeks to break into Asia's top five private banks by 2030 after assets under management (AuM) rose nearly 20% to exceed $145 billion in the third quarter. According to the company's CEO, Jason Moo, Asia's wealth surge is now anchoring BOS' latest expansion push. While global high-net-worth individual (HNWI) wealth rose 4.2% in 2024, Asia-Pacific's climbed 4.8%, second only to North America. Asia-Pacific's HNWI population also grew by 2.7%, expanding the banks' client base. BOS' AuM, which stood at about $120 billion when Moo took over in 2023, has climbed significantly in the third quarter despite the bank raising its minimum account size to $5 million from $3 million in 2024.

DHL Supply Chain will invest €130 million (SAR 561.50 million) to establish a new regional logistics and distribution hub at Riyadh's Special Integrated Logistics Zone (SILZ). The world’s leading contract logistics provider signed a land lease agreement with SILZ for the project, driving the Kingdom's ambition to become a global logistics hub. The new facility will occupy a 78,000 square metre land plot, featuring 53,000 square metres of advanced multi-user warehouse space, with leasehold commitments for a 26-year term. The construction phase is scheduled to begin in the first quarter (Q1) of 2026, with completion expected by Q2 2027. The new warehouse is also part of the €500 million investment DHL Group has planned for the Middle East through 2030.

As the latest stress tests concluded, the Bank of England (BoE) said that the seven biggest British lenders have sufficient capital to withstand a deep global recession, large falls in financial markets, and a jump in interest rates. The tests covered Barclays, HSBC, Lloyds Banking Group, NatWest Group, Santander UK, Standard Chartered, and building society Nationwide, which together account for 75% of lending to the UK real economy. As all participating banks remained above their minimum regulatory requirements, no lender was required to strengthen its capital position. While Standard Chartered and Barclays had the lowest capital positions after the stress test, Nationwide showed the strongest performance, reflecting its relatively resilient balance sheet.

The average annual cost of the 2025 tariffs for a household in the bottom income decile is approximately $900

IF CORRESPONDENT

The economic narrative of late 2025 is defined by a distinct bifurcation that was first identified in the depths of the pandemic years. It was an anonymous Twitter personality known as “Ivan the K” who first articulated the theory that would come to define the post-pandemic era.

When the top 10% continue to spend lavishly on luxury goods, travel, and services, it masks the severe contraction occurring in the bottom 90%

In 2020, he posed a question regarding why the economic recovery was being framed as a V or a U when the reality was far more disjointed. Ivan wrote that some would bounce back while others would not recover.

This dynamic is formally known in sociology and economics as the “Matthew Effect.” The term was coined by sociologist Robert Merton in 1968 and describes a process of cumulative advantage. It traces its sentiment back to the biblical Book of Matthew 25:29, which states that everyone who has will be given more and will have an abundance, but from the one who does not have, even what he has will be taken away. In the economic landscape of late 2025, this ancient text reads less like a parable and more like a precise description of the divergence between capital owners and wage earners.

Mark Zandi, the chief economist for Moody’s Analytics, suggests that this structural divergence began in the 1980s during the Reagan era, when productivity growth began to outpace median wage growth. However, the data from 2025 suggests that this long-standing trend has accelerated into a profound fracture.

The upper arm of this K-shaped economy is being driven by an unprecedented concentration of consumption among the wealthy. Research conducted by Mark Zandi at Moody’s Analytics revealed that in the second quarter of 2025, the top 10% of wealthiest Americans were responsible for 49.2% of all consumer spending. This figure represents the highest level of spending concentration since record-keeping began in 1989.

The economy has become so lopsided that the richest Americans essentially account for half of all economic activity. This concentration distorts aggregate economic data. When the top 10% continue to spend lavishly on luxury goods, travel, and services, it masks the severe contraction occurring in the bottom 90%. High-income households have benefited from a wealth effect driven by soaring asset prices, including record highs in the stock market and continued appreciation in home values.

Lisa Shalett, the chief investment officer at Morgan Stanley Wealth Management, has raised alarms about this disparity. In a research note from November 3, 2025, she described the income

inequality data as completely wackadoo and noted that the widening chasm between the haves and have-nots is critical to understanding the current economic cycle.

While the wealthy propel the markets to new heights, the lower arm of the K is extending downward with increasing velocity. This is visibly manifested in the earnings reports of major fast-food and fast-casual restaurant chains, which have historically served as reliable indicators of lower-income spending power.

Chains like McDonald’s and Chipotle have reported softening traffic as their core customers pull back on spending. Since 2019, the price of a chicken burrito at Chipotle has risen from $7.45 to $10.80 in 2025, while a McDonald’s Big Mac combo has jumped from $8.19 to $11.29. These price increases have forced a trade-down behaviour where consumers abandon fast-casual dining for home cooking or discount grocery options.

Dollar General reported a 4.6% increase in net

sales in the third quarter of 2025, which executives attributed to share gains in consumables as financially pressured shoppers hunted for value. This shift indicates that the lower-income consumer is not merely cutting back on luxuries but is struggling to afford basic conveniences.

This performative wealth signals a desire to participate in the upper arm of the K even as financial reality confines consumers to the lower arm. Charitable organisations are working overtime, with the Portland Press Herald Toy Fund reporting a notable influx of struggling families trying to keep the Christmas spirit alive despite cutting back on their expenses.

The labour market mirrors this bifurcation. While the headline unemployment rate remained relatively low at 4.4% in November 2025, beneath the surface lies a story of two distinct job markets. Companies are retaining talent but aren't hiring anymore, because of which the youth unemployment rate for those aged 16 to 24 reached 10.4% in September 2025.

Gen Z is struggling to find work as entry-level job

openings declined 29% since 2024. A part of the reason is that AI is wiping out low-skilled jobs. Now, the American youth from poor and lower-middle-class families can’t even get their foot on the rung of the career ladder. This is an important development, as resentful young people can create significant unrest in a nation.

There is also a white-collar recession. American employers announced 71,321 job cuts in November 2025, a 24% increase from the same month in 2024. Over 153,000 job cuts were announced year-to-date in 2025 in the IT sector as firms pivot toward AI and efficiency.

The disconnect is further highlighted by the fact that despite these layoffs, the broader layoff rate remains historically low because companies are reluctant to let go of workers in a labour-constrained environment.

The policy landscape of 2025 has played a significant role in calcifying this economic divide. The “Big Beautiful Bill” became law on Jul 4, 2025. The bill cuts taxes on overtime pay and tips, provides additional tax deductions for seniors, and introduces a new deduction for auto loan interest. However, it also makes a $3.4 trillion cut to social security for the next ten years, to make up for the lower tax revenue. Medicaid and the Supplemental Nutrition Assistance Programme (SNAP) will take a huge hit with $1.4 trillion in slashed government funding. The government is cutting social security and lowering taxes for the rich, which is a wealth

Over 1

58 100,000 To 1 Million 613 10,000 To 100,000 1608

Less Than 10,000 1488

Source: Statista

transfer mechanism from the poorest households to the richest in the country.

Trade policy has further exacerbated the strain on the lower arm of the K. The administration implemented widespread tariffs in 2025 with the stated goal of protecting American industry. However, the Yale Budget Lab estimates that these tariffs function as a regressive tax. The average annual cost of the 2025 tariffs for a household in the bottom income decile is approximately $900. While this is lower in absolute terms than the $3,900 cost for the top decile, it represents a much larger share of income. The burden on the bottom decile is 2.4% of their post-tax income compared to just 0.8% for the top decile. This policy directly erodes the purchasing power of those least able to afford it.

The administration had promised a tariff dividend check of $2,000 to offset these costs for working families. Trump fought his tariff war on the promise that

he would give the American people a piece of the tariff dividend and bring jobs back to America. No such dividend arrived in 2025, and Treasury Secretary Scott Bessent clarified that it is unlikely till mid-2026 and that there is also the question of whether the Supreme Court would uphold the legality of the tariffs.

And the math doesn’t add up either. The tariffs generated approximately $120 billion so far, which is not enough to send $2,000 checks to 150 million Americans. It would cost nearly $300 billion to do so. This leaves low-income households paying the higher prices associated with tariffs without receiving the promised financial relief.

The housing market stands as perhaps the most formidable barrier between the two arms of the K-shaped economy. A phenomenon known as the lock-in effect has paralysed the market and created a distinct advantage for existing

homeowners. As of late 2025, approximately 80% of mortgage holders have interest rates below 6%

These homeowners are effectively shielded from the current market reality, where the average 30-year fixed mortgage rate hovered around 6.34% in December 2025. This disparity has created a two-tiered housing society. Existing owners are building equity and enjoying low monthly payments that were secured during the pandemic era of cheap money. Aspiring buyers, particularly Millennials and Gen Z, face a market where the income needed to afford a median-priced home has nearly doubled since 2020.

High interest rates have not only made mortgages more expensive but have also suppressed inventory. Homeowners are unwilling to sell and trade a 3% mortgage for a 6% one, which keeps the supply of homes for sale near 30-year lows. This lack of supply keeps prices historically high despite the elevated rates. Consequently, renters find

themselves trapped. The housing ladder, once the primary vehicle for middle-class wealth creation in America, has been pulled up out of reach for those not already on it.

As 2025 draws to a close, the mechanisms driving the K-shaped economy appear to be entrenching themselves further. The Federal Reserve’s restrictive monetary policy, while necessary to fight inflation, disproportionately hurts those who rely on borrowing. The fiscal policies of the One Big Beautiful Bill Act reinforce the advantages of capital owners while fraying the safety net for the vulnerable.

The rich will continue to accumulate wealth through assets and favourable tax treatment, while the poor and the middle class will continue to navigate a landscape of high costs and limited mobility. The question remains regarding how long this divergence can sustain itself before the tension snaps the economy entirely.

With consumer spending so heavily reliant on the top 10%, any shock to asset prices could cause the upper arm of the K to falter. If the wealthy pull back, the illusion of resilience provided by the aggregate data will vanish, revealing the fragile state of the broader economy beneath. Until then, the United States remains a nation of two distinct economies operating in parallel but moving in opposite directions.

The K-shaped economy in 2025 is not a theory or a chart, but a lived reality that shapes everyday life, determining who can buy a home and who must rent, who can retire and who must keep working, and who can afford abundance while others cut back. Wealth, opportunity, and security continue to move upward, while costs, risk, and uncertainty are pushed downward, reinforced by policy choices and a stagnant housing market.

The economy seems strong mainly due to the spending of the wealthiest households. However, this strength is limited and fragile. Without better wages, improved housing access, and a more robust safety net, the divide will deepen, leading to enduring social and political tensions.

editor@ifinancemag.com

IF CORRESPONDENT

A stronger Australian dollar makes imports cheaper, which provides a disinflationary impulse for tradable goods

The Australian economy has arrived at a precarious intersection where the momentum of post-pandemic recovery is colliding with the restrictive realities of monetary tightening. Central to this unfolding economic narrative is the labour market, which has exhibited behaviour that defies simplistic categorisation. The release of labour force data in late 2025 provided a shock to the system that forced a re-evaluation of the Reserve Bank of Australia’s policy trajectory.

The rise in unemployment starting in September showed deeper changes happening in Australia’s workforce. It hit 4.5%, the highest since November 2021. Things got psychologically and economically worse as the unemployment rate crossed the 4% mark, signalling the conclusion of the era of ultra-low unemployment.

Jeff Borland, Professor of Economics at The University of Melbourne, recently prepared an analysis that highlighted a critical divergence where the economy was creating jobs at a slower pace than the population was expanding.

In 2025, the Australian economy added an average of approximately 12,900 new employed persons each month. While this indicates positive growth, it fell woefully short of the labour supply expansion. The number of people looking for work grew by an average of 22,100 per month during the same period.

This phenomenon is deeply rooted in Australia’s demographic trends, particularly the high rate of net overseas migration, which has sustained population growth at approximately 2.0% per annum. In contrast, total employment growth over the year to November was only 1.3%

This gap of 0.7 percentage points represents a structural widening of labour market slack that monetary policy is specifically designed to induce. The Reserve Bank of Australia has maintained a restrictive cash rate setting precisely to cool the demand for labour and align it more closely with supply capacity. The September 2025 data suggested that this transmission mechanism was working, perhaps faster than anticipated.

However, the narrative became more complex with the release of data for October and November 2025, which showed a reversion of the unemployment rate to 4.3%. This volatility raises questions

about the reliability of monthly seasonally adjusted figures and suggests that the September spike may have been amplified by statistical noise or temporary sampling variations.

Nevertheless, the broader trend lines confirm a softening market. By November, the stability of the 4.3% rate masked a deterioration in the quality and composition of employment. The Australian Bureau of Statistics reported that the total number of employed people actually fell by roughly 21,000 in November. The only reason the unemployment rate did not rise in response to this job shedding was a simultaneous decline in the participation rate, which fell from 66.8% to 66.7%.

The decline in participation is a critical indicator of discouraged workers exiting the labour force. When job seekers stop actively looking for work, they are no longer counted as unemployed, which artificially depresses the headline rate. This “hidden unemployment” suggests that the labour market is weaker than the 4.3% figure implies.

Full-time employment, which provides the income stability necessary for household consumption and debt servicing, plummeted by 56,500 positions in November. This loss was only partially offset by an increase of 35,200 part-time positions. This substitution of full-time roles for part-time roles is a classic defensive strategy by employers who are uncertain about the future economic outlook and unwilling to commit to permanent salary obligations.

The rise in the underemployment rate further corroborates the thesis of increasing slack. The underemployment rate, which measures employed persons who want and are available for more hours, rose to 6.2% in November. This metric is particularly sensitive to the cost-of-living crisis, as workers seek ad-

ditional hours to cope with high inflation and interest rates.

A rising underemployment rate in an environment of falling real wages represents a significant squeeze on household welfare. When combined with the unemployment rate, the total labour force underutilisation rate pushed above 10.5% in late 2025, signalling that despite the “tight” rhetoric, there is a substantial reserve of unutilised labour capacity building up in the economy.

It is also important to consider the independent estimates provided by Roy Morgan (Australia’s oldest and most well-known independent market research company), which utilise a different methodology to the Australian Bureau of Statistics.

In September 2025, Roy Morgan estimated the “real” unemployment rate at 10.8%, with a combined unemployment and underemployment count involving

3.2 million Australians.

While the Australian Bureau of Statistics definition is the global standard for monetary policy formulation, the Roy Morgan figures highlight the lived experience of millions of Australians who feel the bite of a slowing economy more acutely than the official statistics suggest.

The discrepancy between these measures often widens during economic downturns, as the strict criteria for being “unemployed” (active search within the last four weeks and availability to start immediately) exclude those on the margins of the workforce.

While the labour market is showing clear signs of cooling, the inflation landscape in Australia has remained stubbornly resistant to the dampening effects of monetary policy. Wages, prices, and productivity are feeding into each other,

creating a cycle that keeps inflation higher than the Reserve Bank of Australia’s 2% to 3% goal. New data from late 2025 showed that inflation is still a serious problem and will need strict policies for a longer time.

In October 2025, inflation rose to 3.8%, up from 3.6% in September, with increases seen across many basic goods. The trimmed mean inflation, which is the Reserve Bank’s preferred measure of underlying price pressures, also moved higher to 3.3%. These figures confirmed that the disinflationary process had stalled and, in some areas, reversed.

Housing costs have emerged as the single largest contributor to this inflationary persistence. In October, housing inflation ran at 5.9%. This category is driven by two powerful forces that are largely immune to interest rate hikes in the short term. The first is the rental market, which is experiencing a severe crisis

of supply. With vacancy rates at record lows and population growth continuing at a rapid pace, landlords have significant pricing power.

Rents have surged across all major capital cities, adding a heavy weight to the inflation basket. The second factor is the cost of new dwelling purchases, which remains elevated due to high construction costs. Labour shortages in the trades, combined with the high cost of materials, have kept the price of building new homes high even as demand for new approvals has softened.

The Wage Price Index for the September quarter rose by 0.8%, taking the annual growth rate to 3.4%. While this figure is below the peak seen in previous years, it remains high relative to the abysmal productivity performance of the Australian economy.

Productivity growth, which measures the output produced per hour worked, has been flat or negative for several quarters. When wages rise without a corresponding increase in productivity, the unit labour cost for businesses increases.

To maintain profit margins, businesses must pass these higher costs on to consumers in the form of higher prices. This wage-price dynamic is particularly evident in the service sector, where productivity gains are harder to achieve than in manufacturing or agriculture.

The divergence between public and private sector wage growth adds another layer of complexity. The 3.8% annual growth in public sector wages acts as a floor for wage expectations across the economy. State government enterprise agreements, particularly in the healthcare sector, have locked in wage increases that will sustain income growth for a large portion of the workforce.

While these increases are necessary to attract and retain essential workers,

they also support aggregate household income and spending power. This fiscal impulse counteracts the monetary contraction sought by the Reserve Bank. Private sector wages, which grew at a more modest 3.2%, are showing signs of responding to the slowing economy, but the aggregate effect is diluted by the strength of the public sector.

The persistence of inflation has forced a recalibration of the “soft landing” narrative. The hope that inflation would glide effortlessly back to target while unemployment remained low has been replaced by the realisation that a more prolonged period of sub-trend growth and higher unemployment may be required to break the back of domestic price pressures.

The Reserve Bank’s revised forecasts in the November Statement on Monetary Policy projected that inflation would remain above the target band for “a while” and would not return to the midpoint until late 2027. This extension of the timeline reflects an admission that the embedded inflation expectations in the economy are harder to dislodge than previously thought.

While the Consumer Price Index measures the rate of change in prices, the accumulated level of prices remains permanently higher. The price of essential goods and services such as food, health, and housing has absorbed a significant portion of household budgets, leaving less room for discretionary spending.

This is evident in the GDP data, which showed a 0.2% decline in discretionary consumption in the September quarter. Households are prioritising survival spending over lifestyle spending, a shift that has ripple effects through the retail and hospitality sectors.

The island’s policy of isolation

The Reserve Bank of Australia has en-

tered a phase of policy paralysis characterised by a high-wire act between a softening economy and sticky inflation. The decision by the board to leave the cash rate unchanged at 3.60% at its final meeting of 2025 was widely expected, yet it highlighted the unique and difficult position in which Australia finds itself relative to the rest of the developed world.

While other major central banks have commenced easing cycles to support growth, the Reserve Bank of Australia remains locked in a restrictive stance, with the threat of further hikes still lingering in its forward guidance.

The December decision was unanimous, but the accompanying statement revealed a hawkish tilt that surprised some market participants. Governor Michele Bullock made it unequivocally clear that “cuts were firmly off the table.”

The contrast with the United States Federal Reserve is particularly stark.

In December 2025, the Federal Reserve cut its benchmark interest rate by 25 basis points to a target range of 3.50%%to 3.75%. This marked the third consecutive rate cut by the US central bank, driven by a cooling labour market where unemployment had risen to 4.4% and a greater confidence that inflation was on a sustainable path to target. The European Central Bank (ECB) and the Bank of England (BoE) have also moved to lower rates, responding to weaker growth profiles in their respective economies.

This divergence in monetary policy trajectories has significant implications for the Australian economy, particularly through the exchange rate channel. Typically, when the Reserve Bank of Australia holds rates steady while the US Federal Reserve cuts the interest rate, the differential shifts in favour of the Australian dollar.

1381.11

1386.28

1362.61

1742.46 2024 1796.81

(In Billion US Dollars) Source: Statista

A stronger Australian dollar makes imports cheaper, which provides a disinflationary impulse for tradable goods such as electronics, fuel, and vehicles. However, the Reserve Bank cannot rely on this mechanism to solve its inflation problem because the current inflation basket is dominated by non-tradable items like housing and services, which are largely insensitive to exchange rate movements.

The banking sector has responded to this new reality by revising its interest rate forecasts for 2026. The consensus among the “Big Four” banks has fractured. Commonwealth Bank, National Australia Bank, and ANZ have all shifted their views to predict an extended pause throughout 2026. These institutions now believe that the cash rate will remain at 3.60% for the foreseeable future, acting

as a constant drag on the economy until inflation is decisively defeated.

In contrast, Westpac remains an outlier, forecasting two rate cuts in 2026, tentatively scheduled for May and August. Westpac’s economists argue that the current spike in inflation is driven by temporary anomalies that will wash out of the data, allowing the Reserve Bank to pivot mid-year to support growth.

Financial markets have taken an even more aggressive view, with interest rate swaps pricing in a significant probability of a rate hike by June 2026. This reflects the anxiety that inflation may have become structurally embedded at a level above 3%, which would require a second round of tightening to dislodge.

A return to rate hikes would be politically explosive and economically damaging given the fragility of the household

sector, but the Reserve Bank has consistently stated that it will do “whatever is necessary” to return inflation to target.

The impact of this “higher for longer” regime is evident in the flow of credit and investment. While business investment has remained surprisingly resilient, rising 3.4% in the September 2025 quarter due to spending on data centres and digital infrastructure, household credit growth has slowed.

The “mortgage cliff,” which referred to the transition of borrowers from low fixed rates to high variable rates, has now evolved into a “mortgage plateau.” Borrowers have absorbed the shock of higher payments, but they have done so by slashing discretionary spending and drawing down on savings buffers. The prospect of no rate relief in 2026 means that this financial stress will be pro-

longed, increasing the risk of mortgage arrears and defaults as savings pools are eventually exhausted.

The Reserve Bank’s strategy relies on the assumption that the labour market will remain “healthy” enough to absorb this prolonged period of restriction. The forecast that the unemployment rate will stabilise around 4.5% allows the bank to prioritise inflation fighting. However, as the September spike demonstrated, labour market dynamics can shift rapidly.

If the unemployment rate were to accelerate toward 5.0%, the Reserve Bank would face a much sharper dilemma involving a choice between abandoning its inflation target or accepting a recession. For now, the board judges that the risks to inflation are greater than the employment risks, but this calculus will be tested in the coming months as the full lag effects of monetary policy continue to work their way through the economy.

Should the unemployment rate be held below 4.7% while inflation slowly moderates, the economy may achieve the elusive “soft landing.” This would involve a period of below-trend growth but no catastrophic collapse. However, the risks are tilted to the downside.

If the September unemployment spike was not an anomaly but a leading indicator of a sharper deterioration, the Reserve Bank may be forced to pivot rapidly. A sudden jump in unemployment would likely shatter consumer confidence and trigger a rapid deleveraging cycle in the housing market.

editor@ifinancemag.com

ECONOMY

The United States and Saudi Arabia took decisive steps to strengthen their networks in critical minerals, aviation, and defence

IF CORRESPONDENT

November 2025 marked a significant chapter in the bilateral relations between Saudi Arabia and the United States, as President Donald Trump welcomed the Kingdom’s Crown Prince Mohammed

Bin Salman to his Oval Office. This was not the usual diplomatic call. This was his first visit to Washington since 2018, and this meeting marked the beginning of something important: a new chapter in the economic and security architecture between the two nations.

Since Saudi Arabia became a kingdom in 1931, Washington has provided diplomatic support. In the 1940s, President Franklin D. Roosevelt and King Abdulaziz formalised the oil-for-security deal aboard the USS Quincy, with the US promising military protection in exchange for a steady oil supply, an arrangement that continues to this day.

But the world of oil is slowly fading and making way for renewable energy. Crown Prince Mohammed Bin Salman, a visionary young leader, sees this truth. His oil-rich country has an advantage that won't last forever, so he's working hard to modernise and industrialise the Kingdom’s economy.

The headlines are staggering: Crown Prince Mohammed Bin Salman pledged to increase Saudi Arabia’s planned investments in the United States from $600 billion to $1 trillion.

During the meeting, both sides acknowledged shifting global realities. America wants fresh capital and supply chain security in a world that is quickly turning multipolar. The Saudis, on the other hand, have a deadline to meet. The Kingdom’s “Vision 2030” is as ambitious as they come.

They plan to be leaders in AI and aviation, produce nuclear energy, and build breathtaking cities in the desert. But it requires advanced technology and industrial partnerships that only American firms can provide for now. This partnership is a win-win for these G20 economies.

The Saudi-US partnership is not an alliance of convenience built on oil and security. They are now strategic partners with aligned goals of economic and technological supremacy. As they posed for pictures in front of the White House, it was clear to the whole world that the Saudis and Americans had tightened their alliance.

Technology was at the heart of the conversation between the two world leaders. The Saudis expressed their desire to be the global hub of AI and data. It seems this visit to America has brought that vision closer to reality, with pacts that would place the Kingdom as a central node in the global AI infrastructure.

At the heart of this transformation is authorisation by the US Commerce Department for the export of advanced AI chips to Saudi Arabia. This decision effectively clears the way for the shipment of up to 35,000

By pairing American innovation with Saudi infrastructure and capital, the xAI-HUMAIN alliance seeks to lower the barrier to entry for advanced AI development

Nvidia Blackwell chips to HUMAIN, a Saudi-backed national AI champion. This authorisation is more than just a trade deal.

It represents a stamp of approval from Washington that brings Saudi Arabia into the trusted circle of American technological partners. It addresses the long-standing bottleneck of access to high-performance compute power, which is the lifeblood of the modern AI economy.

HUMAIN was the undeniable star of the investment conference that ran parallel to the political meetings. The company, backed by the immense resources of the Public Investment Fund (PIF), announced a flurry of partnerships that read like a who’s who of the American tech sector.

The most headline-grabbing of these was the partnership with Elon Musk’s xAI. The two companies signed a framework agreement to build a massive network of low-cost GPU data centres within the Kingdom.

This project, which includes a flagship 500-megawatt facility, aims to leverage Saudi Arabia's abundant and low-cost energy resources to power the energy-hungry training and inference workloads of the next generation of AI models.

The logic behind this partnership is compelling. As AI models grow exponentially in size, the cost of electricity becomes a primary constraint. Saudi Arabia offers some of the lowest energy costs in the world, making it an ideal location for what industry insiders are calling computer factories. By pairing American innovation with Saudi infrastructure and capital, the xAI-HUMAIN alliance seeks to lower the barrier to entry for advanced AI development.

HUMAIN also signed a separate agreement with Groq, a company famous for its ultra-fast AI inference chips. This deal will see HUMAIN triple the Kingdom’s Groq-powered inference capacity. This is a crucial distinction.

Nvidia makes the best chips in the world. There is no doubt about it. Groq has technology optimised for running models in real-time applications. The Saudis have made deals with both the hardware and software developers. They are going to alchemise the union between xAI and Nvidia in their energy-rich and spacious deserts.

This isn’t a one-way street. HUMAIN and Global AI also plan to build high-density AI data centres in the US, using top-of-the-line Nvidia

technology. The Saudis are reciprocating capital flow and will soon lay the foundations of the great American digital economy.

In the venture capital space, the visit saw a major validation of the American startup ecosystem. Luma AI, a San Francisco-based startup working on Artificial General Intelligence (AGI), raised USD 900 million in a Series C funding round. HUMAIN led the round, with participation from major players like AMD Ventures, Andreessen Horowitz, Amplify Partners, and Matrix Partners.

This investment highlights the PIF’s strategy of taking significant equity stakes in companies that are defining the future of technology. It provides Luma AI with the runway to compete with giants like OpenAI and Google while giving Saudi Arabia a seat at the table of frontier AI research.

Microsoft also cemented its role in the Kingdom’s digital transformation. The tech giant signed a Memorandum of Understanding (MoU) with the PIF and the Saudi Information Technology Company. The agreement explores the delivery of Microsoft’s sovereign cloud services in Saudi Arabia.

The sovereign cloud restricts data to national borders and subjects it to local laws. It is essential technol-

ogy for governments and sensitive industries. Microsoft has secured a lucrative deal with one of the world’s wealthiest clients and will provide services in the Kingdom’s administration, healthcare, and finance sectors.

These agreements collectively signal a pivot. Saudi Arabia is moving beyond being a passive consumer of technology. It is positioning itself as a co-creator and a critical infrastructure provider for the global AI ecosystem. The Silicon Desert is no longer just a marketing slogan. With billions of dollars in hardware and infrastructure now in the pipeline, it is rapidly becoming a physical reality.

While technology captured the imagination, energy remained the bedrock of the discussions. However, the conversation has moved far beyond the traditional barrel of crude oil. The visit marked a historic turning point in energy cooperation with the announcement of a new agreement on civil nuclear cooperation.

This agreement has been years in the making. It establishes a framework for the United States to support Saudi Arabia in developing a civilian nuclear energy programme. For Riyadh, nuclear power is essential to its domestic energy strategy.

The Saudi plan is clever. With a rapidly growing population and expanding industry, the country needs more energy. They decided to build nuclear power plants to provide safe, low-cost energy while exporting oil to other countries, reducing their own carbon footprint. The Saudis aim to be the world’s largest oil exporter while using less oil at home.

The US sees this as a win. Without this deal, Saudi Arabia might have turned to Russia or China for their energy needs, which could have caused concern in Washington. Now, the Saudis are more likely to follow nuclear safety standards, and the agreement boosts US nuclear exports while strengthening long-term energy ties between the two countries.

The deal includes strict safeguards and non-proliferation standards. It addresses security concerns while allowing the Kingdom to join the club of nations with peaceful nuclear capabilities. At the same time as the nuclear deal, Saudi Aramco, the world’s largest oil producer, used the visit to grow its presence in the American energy sector.

Aramco announced 17 MoUs and agreements with a potential total value of more than USD 30 billion. These agreements were signed with major US companies and cover a diverse range of activities

Aramco announced 17 MoUs and agreements with a potential total value of more than USD 30 billion. These agreements were signed with major US companies and cover a diverse range of activities.

The deals are also about Liquefied Natural Gas (LNG). The world is moving away from coal to greener alternatives. LNG is now the critical transition fuel. The Saudi gas giant, Aramco, often cited as one of the most valuable companies in the world, is expanding its global portfolio aggressively. New partnerships are being made with MidOcean Energy and Commonwealth LNG.

This might involve offtake agreements and equity stakes in US LNG export terminals. It is a powerful move to become a major trader of US gas by leveraging its global marketing network to sell American LNG to buyers in Europe and Asia.

Aramco is signalling the corporation’s supply chain resilience. The oil titan has signed important contracts with US oilfield services companies such as SLB, Baker Hughes, and Halliburton. Most of them are procurement deals. It is a strategic move

that ensures continued access to reservoir management technologies and advanced drilling techniques. It is a vital step for maintaining production capacity and efficiency.

Furthermore, the energy partnership is increasingly looking at new vectors such as hydrogen and carbon capture. The investment conference featured discussions on how US technology can help Saudi Arabia achieve its goal of becoming the world’s largest exporter of clean hydrogen. Saudi Arabia brings low-cost gas and renewable energy potential. The US brings expertise and the machines, like electrolysers and carbon capture technologies, needed to make it viable.

This diversified energy portfolio reflects a mature relationship. It is no longer just about the US importing Saudi oil, which it does in far smaller quantities than in the past. The US and Saudi Arabia are partnering to address the global energy transition. Both countries want to maintain the lead they have held in the energy industry for the past century. They are investing heavily in clean-

er and cheaper hydrocarbons, as well as nuclear and renewable energy. The MoUs signed during this visit lay the legal and commercial groundwork for this multi-decade collaboration.

The third pillar of the visit focused on the physical backbone of the modern economy. Global trade tensions are at an all-time high, and supply chain threats are an existential crisis. The United States and Saudi Arabia took decisive steps to strengthen their networks in critical minerals, aviation, and defence.

There was a lot of talk about critical minerals. This is an important conversation for the US, considering its tariff wars and China’s decision to cut the US supply of rare earth minerals. Minerals such as cobalt, lithium, and rare earth elements are essential for making semiconductors and batteries that power AI and robotics. Most of these are mined in China.

Washington and Riyadh are seeking to diversify this dependency. Saudi Arabia sits on an estimated USD 2.5 trillion worth of untapped mineral resources. The new

framework agreement aims to unlock this potential. It facilitates US investment in Saudi mining projects and encourages the transfer of American processing technology to the Kingdom.

The mineral corridors are a boon to America. They are very timely, and without them, the US would have lagged in the chip wars. Both the United States and Saudi Arabia are preparing for potential geopolitical meltdowns. Both parties also discussed their commitment to meeting high environmental standards. Mineral mining was first sent to China decades ago because the work is dangerous for both the environment and local communities.

In the aviation sector, the visit yielded a major win for American manufacturing. Saudia Group, the owner of the Kingdom’s national flag carrier, entered into a strategic agreement with GE Aerospace. The deal will see GE equip the airline’s fleet with GEnx 1B engines. This covers the carrier’s 2023 order of 39 Boeing 787-9 and 787-10 aircraft.

This agreement is significant for several reasons. American aerospace technology gets to shine in one of the fastest-growing aviation markets. Saudi Arabia is soon to be a global leader in tourism and logistics and aims to triple tourist footfall by 2030. The Saudia-GE deal is a guarantee that American engines will power this transition.

The deal is also likely to have long-term maintenance and service contracts, which generate recurring revenue for GE and create high-skilled jobs in both countries. It’s a clear example of how one country’s growth can also benefit another, bringing real advantages to both industrial bases.

Minerals and aviation are becoming key areas of mutual reliance. Saudi Arabia will mine and export minerals, which will be used in batteries for American cars. In return, American jets and planes will transport global leaders and businesspeople to Saudi Arabia, fuelling the next stage of economic growth. It’s a mutually beneficial relationship that connects the industrial and physical needs of both countries.

As the Crown Prince’s jet lifted off from Andrews Air Force Base, the significance of the visit began to settle in. This was not a transactional meeting to fix oil prices or address a singular geopolitical crisis. It was a strategic

GDP per capita in Saudi Arabia from 2016 to 2025 (In 1,000 US Dollars)

Source: Statista

alignment of two nations looking toward the next decade.

In a broader context, Saudi Arabia has served as a key ally to the United States. And the geopolitics of the post-Gaza war Middle East is changing again, with Riyadh renewing its interest in a partnership with Israel on the condition that the twostate solution be implemented. Washington also has a special interest in Saudi Arabia because the Al-Saud family is the custodian of the two holiest mosques of Islam in Mecca and Medina. It also provides some soft power and legitimacy.

On the economic front, the pledge to increase investments to USD 1 trillion is a testament to the scale of the ambition. It signals that the Public

Investment Fund (PIF) and other Saudi entities view the US economy as the primary engine for their capital deployment. The significant presence of American CEOs at the investment conference indicates that both Wall Street and Silicon Valley consider Saudi Arabia to be the world’s most promising growth market.

The visit serves as a key opportunity. For the United States, it opens the door to the Gulf's vast capital and infrastructure projects. It’s a chance to revitalise parts of the American economy through foreign investment and secure future supply chains. For Saudi Arabia, it is a gateway to the technology and expertise required to realise Vision 2030. The Kingdom knows that it cannot build a post-oil economy in isolation. It relies on Nvidia's AI chips, Microsoft's cloud infrastructure, GE's engines, and the innovation from American startups.

cies in both capitals that getting to yes was the priority. The result is a roadmap that is ambitious, detailed, and remarkably comprehensive.

We are witnessing the birth of a new economic corridor. It is a corridor where data flows as freely as oil once did. It is a partnership defined by gigawatts of computing power, fleets of modern aircraft, and the secure supply of critical minerals. The November 2025 visit will likely be remembered as the moment when the United States-Saudi Arabia relationship finally stepped out of the shadow of the 20th century and firmly embraced the opportunities of the 21st century.

The success of this visit will be measured not just in the dollars pledged but in the execution of these vast projects. The foundation laid in Washington was solid, with the “Trillion Dollar Handshake” setting the stage. Now the real work of building the future begins.

The warm personal dynamics between the leadership provided the necessary political cover for these deals to flourish. It smoothed over bureaucratic friction and signalled to the bureaucra- editor@ifinancemag.com

The creator economy is not a trend to be dabbled in but a market condition to be mastered

IF CORRESPONDENT

The global marketing landscape is currently navigating a seismic structural transformation that has elevated the creator economy from a peripheral digital subculture to a central pillar of modern commerce. What began as a scattered collection of hobbyists sharing grainy videos from their bedrooms has matured into a sophisticated industrial complex that rivals the GDP of mid-sized nations. By 2027, the ecosystem is projected to reach a staggering valuation of approximately $480 billion. The market has doubled in size from $250 billion in 2023, driven by a compound annual growth rate that aligns with and often exceeds the broader trajectory of global digital advertising spend.

It was an explosive valuation underpinned by a massive expansion in the labour force itself. There are currently 50 million global creators, a population that exceeds the number of people working in many traditional industrial sectors. The workforce is growing at a compound annual growth rate of 10 to 20%, ensuring a steady supply of new talent and content inventory for platforms to monetise. Yet, despite the scale, the industry remains top-heavy. Research indicates that only about 4% of these 50 million creators are deemed professionals, defined as those earning more than $100,000 annually. The remaining 96% constitute a vast long tail of amateurs and aspiring professionals who are fighting for visibility in an increasingly saturated attention economy.

The economic engine of the creator economy is fuelled primarily by brand partnerships. Despite the hype surrounding direct-to-fan monetisation models, roughly 70% of creator revenue is still derived from brand deals. It statistically highlights a critical dependency (creators rely heavily on corporate marketing budgets) and explains why brands are paying such close attention. Brands are no longer viewing creator marketing as an experimental line item. They are a core component of their digital strategy. As digital media consumption rises, the efficacy of traditional interruptive advertising declines, forcing capital into environments where engagement is organic and trust is already established.

However, the integration of creators into the corporate machine requires sophisticated tooling, and the intersection of the creator economy and Customer Relationship Management (CRM) becomes vital. As Salesforce notes, a marketing CRM is now essential for man-

aging the potentially overwhelming process of creator campaigns. Brands are moving away from ad-hoc spreadsheets to enterprise-grade systems that track engagement, attribute website visits to specific creator posts, and calculate the lifetime value of customers acquired through these channels. By treating every creator as a mini-campaign, brands can use CRM data to log interest, nurture leads, and optimise content strategies based on hard performance metrics rather than vanity metrics like likes or views.

To understand the volatility and opportunity within such an economy, one must recognise the fundamental shift in how content is distributed. The industry has moved from the social graph to the interest graph, a transition that has redefined the mechanics of digital fame. In the era of the social graph (dominated by early Facebook and Instagram), content distribution was determined by connections. Users saw content because they followed a creator or were friends with them. Discovery was limited by the size of one's network, favouring established celebrities and those who accumulated large follower counts early on.

Today, platforms like TikTok, YouTube Shorts, and Instagram Reels utilise the interest graph. The model serves content based on user behaviour and predicted interest regardless of social connections. The algorithm analyses dwell time completion rates and interaction signals to build a dynamic profile of what the user wants to see. It then surfaces content from anyone (even a creator with zero followers) that matches those interests. The shift has democratised virality, allowing a creator to reach millions overnight without spending

years building a follower base. However, it has also introduced extreme volatility. A creator can have one video reach 10 million views and the next reach 10,000 because the concept of a follower is becoming less relevant. The algorithm does not guarantee that followers will see a creator's posts. Meaning reach must be earned with every single piece of content.

The "meritocratic" pressure creates a relentless psychological grind for creators. The need to constantly feed the algorithm has precipitated a severe mental health crisis within the industry. Recent studies reveal that 62% of crea-

tors experience burnout and 52% suffer from anxiety. Most alarmingly, 10% of creators report having suicidal thoughts related to their work, a rate nearly double the national average for US adults. It’s a crisis exacerbated by financial instability, as 69% of creators report feeling financially insecure despite their public success.

The psychological toll is compounded by the nature of the relationship between creator and audience and is known as a parasocial relationship, a one-sided bond where a viewer feels a sense of intimacy and friendship with a media figure. Unlike traditional celebri-

ties who are admired from afar, creators are relatable figures who film in their bedrooms and share their personal failures. Here, a pseudo-friendship is created that drives high conversion rates for brands because recommendations feel like advice from a trusted friend.

However, maintaining such a relationship requires constant identity work. Creators must balance authenticity with curation, presenting a filtered self that attracts followers while periodically revealing their "no filter" self to maintain relatability. The circular loop of performance is exhausting because the creator can never truly be "off" when

their personality is the product.

In response to saturation and the pressure to sell a new trend, a new trend known as "de-influencing" has emerged, which involves creators telling their followers what not to buy. Far from being a rejection of the creator economy, de-influencing represents its maturation. It addresses audience fatigue and growing scepticism toward constant product promotion. By being honest about bad products, creators prove they are not mere shills, which paradoxically increases their influence and trustworthiness when they do recommend a product in the future.

Given the fragility of algorithmic reach and the mental toll of the content grind, savvy creators are aggressively diversifying their revenue streams. The industry is moving beyond simple brand endorsements toward a more robust set of business models. Four primary pillars of monetisation are reshaping the landscape. They are donation, transaction, subscription, and membership.

The donation model functions as a digital tip jar relying on the altruism of the audience. Platforms like "Buy Me A Coffee" allow fans to make small one-off payments. While easy to set up, the model is highly unpredictable and often carries a stigma of begging, making it difficult to scale into a six-figure business. The Transactional model (selling a specific digital asset like an online course or eBook) allows creators to capture the full value of their IP immediately. These are launch-based business models, meaning revenue comes in spikes and requires constant marketing effort to find new customers.

The subscription model (popularised by Patreon) offers the holy grail of

recurring revenue. By gating content behind a monthly fee, creators can generate a predictable income. However, one needs a large, loyal existing audience and a consistent content output to prevent churn. The most evolved form is the membership model, which combines subscription with community. Here, the value proposition shifts from access to content to access to peers. A model that boasts the highest retention rates because members stay for the community even if they consume less content.

A critical tool in this diversification strategy is the evolution of the "Linkin-Bio." What started as a workaround for Instagram's restriction on outbound links has morphed into the creator's primary storefront. In 2025, tools like Hopp and PUSH.fm function as mini-websites that integrate branding, e-commerce, and lead capture. A creator might go viral on TikTok (the discovery engine) but will immediately funnel that traffic to their Link-in-Bio (the monetisation engine) to capture email addresses or sell merchandise. The defining playbook of the professional creator is simple. The rent reaches social platforms while owning the audience via email and direct sales.

Furthermore, the demographics of monetisation are shifting. Gen Z creators are approaching the industry with a different mindset than their Millennial predecessors. Data shows that 85% of Gen Z creators rely on native in-platform payouts, signalling a high trust in the platforms themselves, while Millennials are more likely to build diversified ecosystems off-platform. Gen Z values speed and transparency, rejecting "gatekeeping" and preferring "plug-andplay" tools that allow them to monetise from day one.

We are also witnessing the integration of Web3 technologies as a layer of ownership. While the speculative mania has faded, the utility of blockchain remains relevant for creators seeking true independence. Non-Fungible Tokens (NFTs) and smart contracts allow creators to enforce royalties on secondary sales, ensuring they participate in the value appreciation of their work. By 2025, the global NFT market is valued at roughly $49 billion, with gaming and utility tokens driving the majority of transaction volume. Token-gating allows creators to build portable communities, where the membership list lives on the blockchain rather than on a centralised server, giving them protection against de-platforming.

As the creator economy professionalises, it is becoming increasingly intertwined with corporate power structures and advanced technology. The most significant disruptor is artificial intelligence. In 2025, nearly 91% of creators utilise AI in their workflow. We have entered the era of the "Content Centaur," where human creativity is augmented by AI tools to script videos, generate thumbnail art, and even clone voices for dubbing. Efficiency is the name of the game, and it allows a single creator to output the volume of content that previously required a production team.

Beyond content creation, AI is automating the business side of influence. "AI Agents" are now capable of negotiating brand deals, managing calendars, and tracking invoices. Platforms are deploying autonomous agents that can scan brand databases, send personalised outreach emails, and negotiate preliminary contract terms without human intervention. For brands, it reduces the

Estimated global creator economy market from 2025 to 2034 (In Billion US Dollars)

Source: Statista

administrative burden of influencer marketing, which has historically been a high-friction channel involving endless email back-and-forth.

The rise of synthetic media and "Virtual Influencers" challenges the very definition of a creator. CGI or AI-generated personas like Lu do Magalu (Brazil) and Lil Miquela (USA) have amassed millions of followers and secured bluechip brand partnerships. Lu do Magalu is the most followed virtual influencer in the world with over 46 million followers, acting as a virtual employee who never sleeps, never ages and never generates a scandal. The virtual influencer market is projected to reach $8.5 billion by 2030, offering brands total control over their messaging.

However, the corporate and technological convergence has drawn the eye of regulators. The Federal Trade Commission (FTC) has aggressively updated its guidelines to govern this decentralised workforce. The days of ambiguous dis-

closures are over. New guidelines mandate that disclosures must be "clear and conspicuous" and "unavoidable" to the average consumer. Crucially, these regulations explicitly cover AI. If a brand uses a virtual influencer or an AI voice, it must be disclosed to avoid deceiving consumers. The FTC now holds brands and agencies liable for the compliance of their influencers, forcing companies to implement strict monitoring tools to avoid fines that can reach over $50,000 per violation.

The rapid professionalisation is reflected in the corporate hierarchy itself. We are seeing the emergence of the "Chief Creator Officer" (CCO), a C-suite executive dedicated to shaping an organisation's creative vision and managing relationships with the creator economy.

Companies like WPP Media in Australia have already appointed CCOs to bridge the gap between traditional marketing and the creator ecosystem.

It’s a role that acknowledges that creativity is no longer just a marketing tactic. Without a doubt, it’s a core business driver. Furthermore, universities are beginning to offer formal education, with institutions like Syracuse University launching dedicated centres for the creator economy to train the next generation of digital entrepreneurs.

Loneliness is no longer merely a public health crisis. In 2025, it has evolved into a sophisticated asset class. As social disconnection reaches epidemic levels globally, the technology sector has pivoted to monetise isolation with ruthless efficiency. Data reveals that one in four adults globally now report feeling chronically lonely, with the figures spiking to 73% among Gen Z. What was once viewed as a societal failure is now being treated as a total addressable market projected to reach a valuation of $140

billion by 2030.

The economic shift is driven by the rise of artificial intelligence companions, which offer a simulation of intimacy that is available on demand and immune to rejection. The explosive growth of the new sector is undeniable. Companion apps have recorded an 88% year-over-year growth rate with over 220 million downloads globally. The demand is so potent that even industry giants like OpenAI have adjusted their safety guidelines. The company recently updated its policies to allow for "erotica for verified adults," acknowledging the historical truth that intimacy (simulated or otherwise) is one of the few things consumers will reliably pay for online.

The business model behind this phenomenon is akin to a mobile game where emotional connection is gated behind microtransactions. Users can download a basic "girlfriend" or "boyfriend" bot for free, but must pay for the relationship to deepen. Features like image generation

or the ability for the AI to "remember" previous conversations often require the purchase of tokens or premium subscriptions. It’s a "pay-to-remember" mechanic that monetises the user's desire for continuity and care, turning emotional validation into a recurring revenue stream. The economics are starkly consolidated, with the top 10% of companion apps capturing 89% of the sector's revenue, indicating that the winners are those who can most effectively simulate a parasocial bond.

And by no means is it a trend limited to Western markets. In China, the "loneliness economy" is fuelled by a demographic shift in which the single population has exceeded 240 million people. Tech firms like Luobo Intelligence have launched "emotional robots" such as the Fuzai (or Fuzozo), which are marketed as "portable emotional companionship" for both single adults and the elderly. These devices bridge the gap between a pet and a chatbot, providing physical presence combined with algorithmic responsiveness.

The psychological implications of such an economy are profound. Platforms are manufacturing intimacy at scale using "micro-gestures" and first-person language to trigger the brain's social reward systems. The signal to move away from generic broadcasting to millions and prioritise one-on-one relationship simulations has already been received by thousands of creators worldwide. However, the financial extraction is explicit. As companies refine these tools, they are proving that in a world of increasing isolation, the most valuable product is not content but companionship itself. By 2030, the sector will likely rival the traditional gaming industry in size, entirely built on the monetisation of the

human need to be heard.

Most creators are running after attention. As we discussed earlier, some have parasocial bonds, but what this really does is create a new identity through repeated consumption. Identity alignment happens when a viewer consumes a creator's worldview, aesthetics, language, and lifestyle, and hence reconstructs themselves to mimic their favourite streamer or creator.

People may ignore an ad, but they will never ignore something that reinforces who they believe they are. Research in consumer psychology indicates that identity congruence significantly boosts repeated purchases and brand loyalty. A modern consumer is not just buying products. They are buying a self-image.

Fitness creators sell programmes, financial creators sell discipline, and lifestyle creators sell belonging. In this way, they aren't just peddling workouts, spreadsheets, or clothes, but are offering something deeper to their audiences.

Personal finance creators don't sell spreadsheets, but rather values and slogans such as “I am financially literate,” “I am different from my parents,” and “I am building generational wealth.” These core messages resonate with viewers far more effectively than mechanical to-do lists or sheets of data.

Robert Kiyosaki is an influencer who does this really well. In his book Rich Dad Poor Dad, he explains how to make money through investments rather than saving. He describes how to get money to work for you instead of working for money. But people are not just buying the book or the financial advice; they are buying a version of themselves that is financially smart and is

actively building wealth.

The same thing goes with beauty and lifestyle bloggers and creators: they're selling belonging. It's not just about lipsticks, mascaras, or foundations. What they sell is "I am that girl", “I'm clean, minimal, aesthetic,” and “I belong to this culture.”

Lisa Vanderpump, a lifestyle influencer, created a $90 million empire by channelling her reality TV exposure to her restaurants. Lisa was on TV shows like Real Housewives of Beverly Hills and Vanderpump Rules, and she used a zero-cost marketing engine to funnel all this attention to her business.