146 results for ‘bars & breweries’

146 results for ‘bars & breweries’

Small businesses are not always the owners of the building where they operate. That can limit what can be done to prepare for a natural disaster, but every business should be prepared regardless.

“Small business owners may be tenants of the building, so there is lessor’s risk, and with lessor’s risk, there’s often limitations about what can be done with that building,” said Ross Haigler, head of commercial lines at the Insurance Institute for Business & Home Safety (IBHS). “For example, who is responsible for building upgrades? Is it the tenant, is it the landlord, or is it the property management firm?” he asked.

Small business commercial properties, whether rented spaces or owned property, might also be older buildings, he added. “So, the aging infrastructure contributes to how well these buildings perform when they’re tested against extreme weather events,” Haigler added. “That exposure really highlights the risk of convective storms in older buildings and why they might have failure mechanisms such as a leaky roof.”

Haigler said IBHS often “preaches” that the roof is the first line of defense against natural disasters relating to wind, hail, and flooding, especially for small businesses where an aging roof or an aging roof covering can lead to a single breach of water into that building. That type of event could potentially close down that business, he said.

IBHS offers business continuity planning toolkits, free and accessible on their website, as a resource for small businesses. They recommend long-term strategies include taking preventative risk mitigation measures, such as trimming trees around the property to mitigate roof damage in the event of high winds, snow, or ice; installing a generator in case of power outages (especially for refrigeration-dependent businesses); and when owning the building, making sure the building materials are high quality.

Haigler said when possible, agents can help their small business clients prepare for future natural disasters by encouraging simple routine property inspections.

“Ensure that those facilities are routinely inspected and maintained and that the roof is up to standard and able to prevent rainfall from coming in,” he said. “Routine maintenance is one of the items that often goes unnoticed, but it also has one of the largest potential outcomes of a severe weather event.”

Most importantly, Haigler advised to have a plan for when disaster strikes.

“From a business continuity perspective, most important is to ask the important questions, like: Who are your major suppliers? What happens if that building is unable to return to working conditions quickly? Are you able to work offline? Who are your distributors? Who are your customers? How are you communicating? And then, have an up-to-date inventory of what is in your building just in case.”

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Chief Executive Officer Joshua Carlson | jcarlson@insurancejournal.com

ADMINISTRATION / CIRCULATION

Chief Financial Officer

Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: Mike Gulla, Monica Ningen, Matthew F. Power

Columnists: Chris Burand, Mary Newgard

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT)

Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

Graphic Designer

Chris Johnson

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator

George Jack | gjack@ijacademy.com

Andrea Wells V.P. of Content

By Chad Hemenway

Commercial property/casualty premiums across all account sizes in the fourth quarter of 2025 were the softest they have been since 2017, according to The Council of Insurance Agents & Brokers (CIAB) quarterly survey.

Overall, premiums across all account sizes rose by an average of just 0.2%, down from 1.6% in Q3 2025, when CIAB called out “clear soft market conditions.”

In its latest survey report, CIAB said, “Signs of softened market conditions were equally evident across lines of business.”

Nine lines of business—cyber, business interruption, commercial property, construction, directors & officers, employment practices, surety bonds, terrorism, and workers’ compensation—saw premiums decrease this quarter, up from six during Q3 2025. D&O decreased the most, down 3.8%, making it the eighth consecutive quarter of decreases for the line.

Even commercial auto, which led all lines with an average premium increase of 6.6% and marked 58 straight quarters of increases, fell from an increase of 7.4% in Q3 2025. Survey respondents continued to blame social inflation and

nuclear verdicts, and about half of them also reported an increase in claims. Respondents also noticed a decrease in capacity for commercial auto risk, according to the survey.

The 1.9% average premium increase across all lines of business in Q4 2025 was a 30% decrease from 2.7% in Q3 2025, said CIAB, who noted that for the first time since Q4 2017, large account premiums decreased at an average of -2.1%. Respondents cited more competition for upper-middle and large accounts.

2017 was the end of the last soft market cycle recorded by CIAB’s survey.

Foremost®, part of Farmers Insurance®, has a legacy of more than 70 years of industry leadership and excellent service. Built from decades of experience, we deliver customizable coverages for autos, homes, boats, personal watercrafts and much more.

Your customers can live confidently knowing Foremost has their back with our dedicated claims team who are there when you need them 24 hours a day, seven days a week. Look to Foremost for trusted stability, above-and-beyond service and coverage you can count on.

The total amount of claims tied to SRCC (strikes, riots, and civil commotion) between 2020 and 2024. The category of insurance risk that hardly existed a little over a decade ago has morphed into a meaningful source of losses as episodes of unrest increasingly lead to the destruction of property in Western democracies. Howden Re estimates that insured losses related to SRCC soared from negligible levels in 2013 to more than $8 billion between 2020 and 2024.

The total amount that two asphalt companies have agreed to pay to resolve False Claims Act allegations that they submitted fraudulent test results to the Ohio Department of Transportation (ODOT) for federally funded asphalt projects in Ohio. Ohio’s Construction and Materials Specifications require that companies performing asphalt projects must conduct certain mix design testing of their asphalt mixtures and submit the test results to ODOT before beginning their asphalt work on federally funded projects. $8B

33,750 pounds

The amount of frozen snow crabs stolen from a Worcester, Massachusetts, warehouse in July 2025 through hightech cargo theft. Nationally, estimated cargo theft losses surged 60% from 2024 numbers to nearly $725 million in 2025, while confirmed cargo theft incidents increased 18%. Prosecutors claim that before the alleged seafood heist, the same suspect allegedly stole a shipment of blueberries in New Jersey and approximately $433,830 worth of cologne in New York.

14

The number of crashes Tesla Inc.’s robotaxis have been involved in since service began eight months ago in Austin, Texas, according to reports the carmaker made to regulators. A federal order requires carmakers to report when automated driving systems are involved in certain crashes. Austin remains the only city where Tesla is offering robotaxi rides.

$30 Million

“There are no sectors of the economy that are insulated from the potential impact of AI. As an industry we need to prepare for how these rapidly evolving risks are underwritten across commercial insurance and what emerging claims patterns will look like.”

— Oliver Brew, co-author of the report and head of Cyber Centre of Excellence, Lockton Re, in a statement regarding a new report from Lockton Re, in collaboration with Lockton International and Armilla AI, which found rapid adoption of AI by organizations across all industries is changing the commercial risk landscape and suggested it’s time to consider making AI its own risk classification.

“Decades of fire suppression have allowed other plant species to move in, increasing competition and fuel buildup such as leaf litter, needles, and woody debris,”

— U.S. Forest Service’s Public Affairs Officer Ethan Ready, in an email to VTDigger, advocating for the Northern Escarpment Ecological Restoration and Fire Resilience program, designed to improve the area’s resistance to wildland fires, pest infestations, and drought. The project covers four areas spanning 2,770 acres of the Green Mountain National Forest and would begin in the spring of 2027. The project aims to reduce flammable materials and expand native plant communities that depend on regular, low-intensity fire in the forests.

“Texans should not be forced to endure offensive and harmful odors in their own communities, especially when a company is failing to comply with the standards required by law.”

— Texas Attorney General Ken Paxton filing a lawsuit against Darling Ingredients, Inc., an Irving-based company that turns used cooking oil, food waste, and inedible animal parts into animal feed and fertilizer. Residents have described odors coming from the facility as smelling like dog food, cooked grease, and burning feathers. The lawsuit claims emissions interfere with residents’ health and their ability to enjoy their land, a potential violation of the Texas Clean Air Act.

“Over the past year, federal policy changes have altered the federal-state partnership by shifting costs to states and reducing support for longstanding programs that serve working families. Unlike the federal government, states across the country— including Illinois—are required to balance their budgets, and as repeatedly stated, Illinois cannot backfill billions of dollars as the federal government makes reductions.”

— Press release from the Illinois Governor’s Office of Management and Budget warning of “unprecedented” budgetary pressures. Illinois is already expecting $587 million less in revenue for the year through June 30, due to provisions in Trump’s signature tax cut legislation.

“Increasingly, courts have recognized that the use of surveillance technologies can violate the Fourth Amendment’s protections against unreasonable searches and seizures. Although this area of law is still developing, the use of LPRs and predictive algorithms to track and flag individuals’ movements represents the type of sweeping surveillance that should raise constitutional concerns.”

— A letter from privacy and advocacy organizations calling on California Gov. Gavin Newsom to remove a network of license plate readers across Southern California that may feed data into a U.S. Border Patrol predictive domestic intelligence program.

“Without even a public meeting, TVA (Tennessee Valley Authority) is telling the people who live near these coal plants that they will breathe in toxic pollution from not one but two major power plants for the foreseeable future. This decision is salt in the wound after ignoring widespread calls for cleaner, cheaper replacements for the Kingston and Cumberland coal plants.”

— Gabi Lichtenstein, Tennessee Program Coordinator for Appalachian Voices, reacting to TVA’s (Tennessee Valley Authority) reconsidering two plant closures because of regulatory changes and increasing demand for electricity. TVA previously planned to shutter the plants by 2035.

By Allen Laman

More than two-thirds of independent agencies plan to increase use of artificial intelligence in the next 12 months, though just 8% said AI is currently embedded in their daily workflows, according to a new report from The Big “I” Agents Council for Technology.

In its annual tech trends report, ACT found that 38% of survey respondents are “very likely” to increase AI use, while 30% are “somewhat likely” to do so over the next year.

Operational efficiency (60%) and staff productivity (52%) were cited as leading motivations for adopting AI. Data privacy or compliance risks (24%) and inaccurate outputs (22%) topped the list of concerns.

Kasey Connors, executive director of ACT, called the report’s findings “a pivotal moment” for independent agencies. With growing AI interest signaling momentum, “long-term success hinges on clearer

governance, stronger training, and more integrated technology strategies,” she said in a statement.

Nearly a third of the national survey’s respondents (31%) said they are not currently using AI, while 33% described themselves as “just experimenting” with the technology. Another 22% said they are

using AI only in limited areas. ACT pointed to “a growing gap” between the promise of what AI can deliver and the operational readiness required to implement it responsibly and effectively. The council highlighted several constraints, including a lack of documented processes, vendor-related confusion, resource and

By Chad Hemenway

Success for the property/casualty industry in 2025 was marked by rate increases and investment income, but plateauing or softening rates in many lines of business may pressure financial results in 2026, said AM Best.

commercial property, and auto physical damage repairs, will likely lead to a slightly higher industry loss ratio,” Jacqalene Lentz, senior director at AM Best, said in a statement.

In a new report, the insurance industry financial rating analyst said it expects lower net premium growth in 2026 and has predicted that the P/C industry combined ratio will increase 1.9 points to 96.9.

“Macroeconomic headwinds, including rising claims costs attributable to higher prices of materials required for home,

In 2025, continued rate increases benefitted overall financial results and offset adverse trends such as social inflation, nuclear verdicts, and litigation financing, especially in general liability, said AM Best. Net premiums written increased 6.1% in 2025 compared with 8.7% in 2024. For most lines of business seeing premium growth, AM Best reported that the magnitude diminished throughout 2025 and into 2026. Cyber, D&O, commercial property, and workers’ compensation

recorded lower renewal pricing in 2025 compared with 2024.

The 95 combined ratio in 2025 improved on 2024’s combined ratio of 98—which was the first time under 100 in three years. State regulators’ approval of rate filings helped personal lines, as did insurers’ adoption of technology to improve underwriting and efficiency. However, home and auto could see profit margins squeezed in 2026 thanks to rising repair costs and higher fatality rates in auto.

“The segment should generate solid results, but with premium volume expected to be constrained as year-over-year rate changes flatten,” AM Best said.

Lower net premium growth in 2026 for commercial lines will lead to a higher combined ratio of 96.3 compared with

budget limitations, portal and multifactor authentication fatigue, security and governance gaps, as well as change fatigue and tool sprawl.

“AI is entering agencies at a time when many are already struggling with disconnected systems and limited automation,” Connors said. “That complexity makes it harder to move from experimentation to meaningful impact.”

“What we hear consistently is that agents aren’t worried about the price of AI—they’re worried about the cost of getting it wrong. Data privacy, compliance, and accuracy have to be addressed before agencies are comfortable scaling AI use,” she said.

Beyond privacy and compliance concerns, 17% of survey respondents said their top worry about using AI tools is losing human touch, while 16% said they don’t know how to apply the technology.

About half of survey respondents (45%) reported already using ChatGPT and other public large language models. Far fewer agencies said they use AI in policy comparison tools (20%), marketing tools (18%), chatbots and virtual assistants (13%), or document and data extraction tools (13%).

“AI in its current form should be treated like a junior colleague,” ACT said in the report. “Although it’s fast and capable of consuming large volumes of information, it still requires supervision for complex or high-impact decisions.”

The council’s survey found that only 13% of agencies have a formal AI policy.

More than half (56%) do not have a policy, and almost 44% reported relying on peer-to-peer training on new tech tools or systems.

“That will have to change in the coming year for agencies to close significant security and liability gaps,” ACT said in the report.

95.8 in 2025, AM Best estimated. Three commercial lines of business—auto, medical professional liability, and other/products liability—turned in combined ratios over 100 in 2025 (103.5, 106, and 108, respectively).

Net loss and loss adjustment reserves, often the largest liability to an insurers’ balance sheet and a leading cause of insolvency, remain a critical issue for AM Best, who said a re-estimation of the P/C industry’s ultimate reserves resulted in an overall reserve position for year-end 2024 reserves, including the statutory discount, to a $9 billion deficiency, almost $10 billion better than originally estimated.

The report also noted that the flow of risk to the excess & surplus market “was one of the defining factors” of 2025. Admitted carriers increasingly avoided risks in property, auto liability, and high-hazard casualty lines, but the E&S market jumped in to provide flexibility and customization.

Sompo Holdings Inc. received the necessary antitrust and insurance regulatory approvals required to complete its previously announced acquisition of Aspen Insurance Holdings Ltd., via a wholly owned subsidiary of Sompo International Holdings Ltd. (SIH).

Following closing, Sompo will begin the process of integrating Aspen’s capabilities to ensure a globally diversified property/ casualty platform.

Private equity firm Aquiline Capital has entered into a definitive agreement to sell independent insurance broker Relation to investment firm BayPine. Terms of the deal were not disclosed.

Founded in 2007, Relation provides risk management and benefits consulting services to deliver insurance solutions across commercial P/C, employee benefits, personal lines, private client services, retirement solutions, and wealth management to clients of all sizes across a range of industries such as construction, transportation, agriculture, entertainment, healthcare, manufacturing, hospitality, and real estate.

Since Aquiline’s initial investment in 2019, Relation has completed more than 100 acquisitions.

Boston-based BayPine said Relation’s management team will continue to lead the company.

SterlingRisk, ASZ International Inc.

Insurance broker SterlingRisk of Woodbury, New York, acquired ASZ International Inc., a Westchester County, New York, agency specializing in transportation risks.

As part of the transaction, ASZ principals Marc Zettl and Chris Zettl have joined SterlingRisk. Marc Zettl will serve as president of SterlingRisk’s Transportation Vertical, and Chris Zettl joins as account specialist, supporting the continued growth of the practice. The agency also sells personal and other business insurance.

ASZ International was advised by MidCap Advisors.

Arthur J. Gallagher & Co., B&W Insurance Agency Inc.

Arthur J. Gallagher & Co. announced the acquisition of Washington, Pennsylvaniabased B&W Insurance Agency Inc. Terms of the transaction were not disclosed.

B&W Insurance Agency offers personal lines and commercial brokerage services to clients in southwest Pennsylvania. Paul Barzd III, Jim Cote, and their team will remain in their current location under the direction of Jen Tadin, head of Gallagher Select, its U.S. property/casualty operations for small businesses and personal insurance.

Arthur J. Gallagher & Co. is a global insurance brokerage, risk management, and consulting services firm headquartered in Rolling Meadows, Illinois.

Gallagher operates in 130 countries through its owned operations and a network of correspondent brokers and consultants.

Tapco Underwriters Rebrands as CRC Tapco

Tapco Underwriters, a North Carolinabased managing general agent, has new livery and a new name, 17 years after it was acquired by CRC Insurance Services. The MGA will now be known as CRC Tapco and will continue to focus on specialty and surplus lines, the Birmingham, Alabamaheadquartered CRC Group said in a news release.

Tapco was launched in 1983. It was acquired by CRC in 2009 and continues to work as a wholesale broker with binding authority. CRC Group is one of the largest independent wholesale specialty insurance distributors, with some 6,000 associates in the U.S., Canada, and the U.K.

King Risk Partners, Hanc Group

Gainesville, Florida-based King Risk Partners has acquired the Hanc Group, an insurance agency that serves the KoreanAmerican community and others in north Georgia, King Risk announced this week. Rick Han, owner of Alpharetta-based Hanc Group, said the partnership will allow the agency to expand its personal and commercial insurance offerings. Hanc Group was formed in 2018. The agency is appointed with multiple carriers, including property/casualty, life, and accident and sickness, and offers home, auto, church, professional liability, and other lines.

Specialty Program Group LLC, Logistiq Insurance Solutions

Specialty Program Group LLC (SPG), an operator of specialty insurance distribution, underwriting, and consulting businesses, announced the acquisition of Logistiq Insurance Solutions and the subsequent integration of Logistiq with Anova Marine Insurance, a firm acquired by Specialty Program Group in 2025.

These new cargo and logistics capabilities will complement and enhance SPG Transportation’s position in marine cargo expertise.

Enstar Group Limited, a global insurance and reinsurance group backed by investment vehicles managed by affiliates of global investment firm Sixth Street, announced it has entered into a definitive stock purchase agreement to acquire 100% of the shares of Accident Fund Holdings, Inc. (AF Group) from Blue Cross Blue Shield of Michigan.

Headquartered in Lansing, Michigan, AF Group has been a provider of insurance solutions through its affiliate brands for more than a century. It was acquired by Blue Cross in 1994. Upon completion of the transaction, AF Group will become a wholly owned subsidiary of Enstar and operate largely as a standalone company. AF Group is expected to operate under its existing leadership team.

Inszone Insurance Services, Scarbrough, Medlin & Associates

Inszone Insurance Services acquired Scarbrough, Medlin & Associates, Inc., a Dallas, Texas-based agency with more than four decades of experience serving commercial property clients.

Scarbrough, Medlin & Associates specializes in commercial property insurance, with deep experience supporting property management firms, association management companies, and multifamily and mixed-use developments. The firm also has a long history of servicing other complex commercial classes, including large school districts, electric cooperatives, oil and gas operations, contractors, and restaurants and bars.

The Scarbrough, Medlin & Associates team will remain in place.

Alliant Insurance Services, Laredo Commercial Insurance Agency

Alliant Insurance Services has acquired Laredo Commercial Insurance Agency’s

For-Hire Trucking portfolio, establishing the firm’s local presence in Laredo, Texas.

As part of the acquisition, Steven Cadena has joined Alliant Transportation as Vice President.

Cadena brings extensive experience and understanding of the complex Laredo transportation market, strengthening the

roster of strategic broker hires with regional expertise in cross-border transportation risk.

Laredo is the third Texas-based agency to join Alliant in recent months, following the acquisitions of McAfee Insurance Agency in Mercedes and Highpoint Insurance Group in Friendswood.

National

Westfield, headquartered in Westfield Center, Ohio, appointed Lloyd Scholz as enterprise chief information officer (CIO). Scholz most recently served as senior managing director and chief technology officer at Markel.

chair of IICF’s board of governors. Adam McDonough, executive vice president of Lockton Insurance Brokers, will join Marohn in leading the IICF board of governors as its first vice chair.

U.S. business. Grippa will serve on the firm’s U.S. Executive Committee and act as a strategic advisor, helping advance BMS Re US’s multi-year strategic plan and accelerate organic growth across its programs, mutuals, and specialty segments.

development and growth of the energy sector team.

NFP, headquartered in New York City, named Tom Gillingham as president, commercial risk, expanding his executive leadership across NFP’s commercial P&C, programs, and wholesale businesses. The company also appointed John Mahoney head of programs, Totalis Program Underwriters, NFP’s Specialty MGA and MGU. Mahoney joined NFP via EverGuard in 2017.

Converge, headquartered in New York City, appointed Howie Altman as chief technology officer. Altman will oversee the continued evolution of the company’s technology infrastructure, including AI-powered risk assessment, automated underwriting workflows, and advanced portfolio management tools.

Marsh Risk, headquartered in New York City, made three leadership appointments.

Billingslea is based in Dallas, where he most recently served as an Energy Liability Underwriter at AXA XL.

Hub International Limited (HUB), headquartered in Chicago, Illinois, named Andrea Baldrica as chief sales officer of U.S. Employee Benefits.

Coalition, headquartered in San Francisco, California, appointed Frank Fumarola as chief product officer. Fumarola joins Coalition from Nubank.

W. R. Berkley Corporation, headquartered in Greenwich, Connecticut, named Lee Iannarone executive vice president. Iannarone is succeeded by Stephen Kennedy, who has been named senior vice president and general counsel.

The Insurance Industry Charitable Foundation (IICF), based in Los Angeles, California, named Steve Marohn, president, commercial lines at Grange Insurance, as

Crawford & Company, headquartered in Atlanta, Georgia, promoted Mike Hoberman to CEO of U.S. Operations. Canada will transition into International Operations under the leadership of Andrew Bart, CEO of international operations. Pat Van Bakel was named chief commercial & strategy officer.

Crawford also promoted Paul Kottler to president, U.S. Loss Adjusting; Lance Malcolm to president, U.S. Network Solutions; and Jeffrey Sickles to president, Crawford TPA: Broadspire.

BMS Re, the reinsurance arm of independent insurance and reinsurance broker BMS Group, headquartered in New York City, appointed Tony Grippa as chief strategy officer for the

Jimmy Tse was named U.S. financial institutions surety growth leader. Based in New York, Tse will report to Carrick Bligh, U.S. surety financial institutions leader.

Drew Vann was named U.S. construction surety leader. Based in Atlanta, Vann will report to Fran Curran, U.S. Surety Leader at Marsh Risk, where he will support U.S. construction clients with strategies to enhance credit capacity and manage financial risk.

Caroline Jardim was named U.S. multinational surety leader. She joins from Marsh Risk Brazil, where she most recently served as credit specialty leader. Based in New York, she will also report to Curran.

Baldrica has over 25 years of insurance industry experience, serving with HUB since 2014, when HUB acquired Baldrica & Company.

HUB also hired Ellen Sue Bernards to the HUB Complex Risk team as alternative risk solutions practice leader, a new role.

CRC Group named Tracey Fallon as office president for its first Virginia office. Fallon, who will lead CRC’s recently opened New Richmond office, has over a decade of experience in the insurance industry, with a background in E&S underwriting, binding authority, and commercial risk placement.

AXA XL, headquartered in Dallas, Texas, appointed Jason C. Billingslea as head of energy, E&S, where he will lead the

NFP, an Aon company headquartered in New York City, appointed Jack Spencer as senior vice president, commercial risk, in its Northeast region.

Spencer has over a decade of experience in commercial risk insurance in the New York City metro area.

company as chief customer success officer.

Lawley, headquartered in Buffalo, New York, promoted Michael Szymoniak Jr. and Adam Clouden to partners within the employee benefits division, and Michael Bandini to partner within the property & casualty division.

The Virginia Workers’ Compensation Commission reappointed Commissioner Robert A. Rapaport to serve an additional six-year term as a commissioner of the Virginia Workers’ Compensation Commission.

Smart AutoCare, headquartered in Richardson, Texas, appointed Christopher Murphy as president. Murphy has over 20 years of executive leadership experience, joining Smart AutoCare from OptionSoft Technologies, Inc., where he served as president.

Higginbotham hired Samuel Isaac Ritter, M.D., as medical director for employee benefits, adding a client-facing physician resource within its self-funded advisory work. Ritter is an award-winning emergency physician at Baylor University Medical Center.

Finys, a provider of insurance software solutions for property and casualty carriers, announced that Emeka Iheme has joined the

Unison Risk Advisors, headquartered in Cleveland, Ohio, appointed Nicole L. O’Sullivan as chief people officer. O’Sullivan joins Unison with more than 25 years of experience leading enterprise-wide people strategies for complex, growing organizations.

and Mississippi. These changes are effective April 1.

Jonathan Diessner has been promoted to president of Kraus-Anderson Insurance, one of Minnesota’s largest privately held independent insurance agencies and a member of the KrausAnderson family of companies.

ICW Group hired Travis Murnan as head of its new ICW Specialty business unit, Alternative Risk Transfer (ART). ART is expected to go to market later this year as part of ICW Specialty, which was launched in 2025 to support excess and surplus products and other coverage services.

Buckner Partners, an insurance brokerage with offices in Idaho Falls and Rexburg, Idaho, appointed Greg Taylor as president of Buckner of Idaho. Taylor previously held leadership roles with State Farm Insurance, John Deere Financial, and Farmers Mutual Hail.

Hub International Limited (HUB), headquartered in Chicago, Illinois, hired Cindy Ackerman as senior vice president (SVP), private client risk advisor in Colorado.

Alliant Insurance Services, headquartered in Irvine, California, added Amanda Quitmeyer, based in Chicago, Illinois, as assistant vice president within its employee benefits group.

Chubb, headquartered in Warren, New Jersey, appointed Ben Mortimer to the role of regional executive officer for the Southeast.

Kevin Kraselsky, senior vice president, Atlanta branch manager, will take on the additional responsibility of having the Birmingham branch territory report to him, overseeing distribution and production throughout Georgia, Alabama

Capital Insurance Group (CIG), headquartered in Monterey, California, promoted Kimberly Noel to regional field executive for its Northwest region, overseeing underwriting teams and line of business performance in Oregon and Washington. Noel has over 20 years of underwriting and leadership experience, including more than a decade with CIG, including roles as regional underwriting manager, underwriting team leader, and regional executive underwriter. She began her insurance career with Travelers Insurance.

Trucordia, headquartered in Lindon, Utah, hired Jason Nelson for the new role of vice president of public relations. Nelson has over two decades of experience across broadcasting, advertising, and publishing. He was a partner in a publishing group and the advertising agency Swell Media, where he worked closely with Trucordia.

Arrowhead Specialty named Jimmy Curcio executive vice president. Curcio most recently served as the chief strategy and analytics officer for Arrowhead Intermediaries and, previously, for Arrowhead Programs. Before joining Arrowhead, he held leadership roles at Munich Re.

Hub International Limited named Brandon Hetrick vice president, private client risk advisor in Newport Beach, California. Hetrick has 25 years of insurance experience. Before joining Hub, Hetrick spent more than a decade with an insurance brokerage firm.

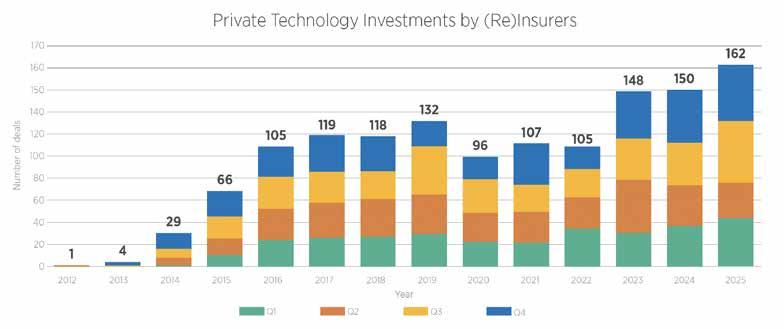

By L.S. Howard

Investments in global insurtech rose 19.5% during 2025 to US$5.08 billion from US$4.25 billion in FY 2024, marking the first annual increase since 2021, according to Gallagher Re’s Q4 Global Insurtech Report.

During the fourth quarter of 2025, global insurtech funding surged 66.8% to US$1.68 billion from US$1.01 billion during Q3, said Gallagher Re, noting that Q4 funding was the largest quarterly amount seen since Q3 2022 when US$2.35 billion was raised.

Gallagher Re attributed the surge to a combination of factors such as growing investments from insurers and reinsurers (as opposed to private equity companies); funding for insurtechs that are focused on artificial intelligence (AI); and the return of “mega-rounds,” where more than US$100 million is raised in a single round.

During 2025, re/insurers made more private technology investments into insurtechs—162 deals—than any other year on record, said the report, which pointed to a “changing of the guard” or a “notable shift in the insurtech investor community.”

“This suggests that re/insurers are not

only more comfortable investing, but also that they see insurtechs as a route forward in their own strategies,” the report said.

Regarding the effects of artificial intelligence, Gallagher noted that twothirds of insurtech funding last year went to AI-centered insurtechs, which raised US$3.35 billion across 227 deals—66% of funding and 62% of deals, respectively. This level of investment demonstrates the extent to which the re/insurance industry is invested in this technology, the report added.

For Q4 2025, AI-centered insurtechs raised US$1.31 billion across 66 deals, with an average deal size of US$22.14 million, or slightly above the overall Q4 2025 average, the report said, noting that 77.9% of insurtech funding during the quarter went to AI-centered companies.

“AI is squarely the focus of most of the contemporary insurtech world. Over time, we see AI becoming so integrated into insurtech that the two may well become synonymous,” said Andrew Johnston, global head of Insurtech at Gallagher Re, in comments accompanying the report.

In a forward to the report, Johnston said that three-quarters of all funding is going

into insurtech businesses with an AI label— whether they are AI powered themselves or provide AI tools to other businesses.

“We do not see this trend slowing down. In fact, we see AI becoming so integrated into insurtech over time that the two may well become effectively synonymous—in much the same way as we could already argue that ‘insurtech’ is itself a meaningless label, because all insurers are technology businesses now,” Johnston said.

Property/casualty insurtech funding rebounded from 2024’s low, increasing 34.9% to US$3.49 billion in 2025, the Gallagher Re report said, explaining that mega-rounds fueled P/C’s rebound, with funding up from US$320 million in 2024 to US$1.06 billion, while deal count rose 20% to 264.”

In P/C insurtech funding, there was a 90.5% quarter-on-quarter hike to US$1.31 billion, driven by mega-round deals, the report said, adding that five companies— CyberCube, ICEYE, Creditas, Federato, and Nirvana—collectively secured US$662.81 million in mega-rounds during the fourth quarter.

Unlike P/C, life and health (L&H)

insurtech funding and deal count both declined last year, with funding dipping by 4.6%, year-on-year, to $1.59 billion and deal count falling 17.7% to 102, Gallagher added.

Additional notable findings from the report include:

• Tech vendors saw record-high dealshares across P/C and L&H insurtech. Nearly 60% (58%) of P/C deals went

to business-to-business insurtechs, a 12-percentage-point increase from 2021’s funding boom.

• Deal shares to insurtechs in the category of lead generator/broker/MGA fell from 42% in 2024 to 35% in 2025—the lowest on record.

• The global deal share of U.S.-based insurtechs rose 5.16 percentage points between 2024 and 2025—the largest gain

among all countries. Specifically, the U.S. deal share increased from 50.58% in 2024 to 55.74% in 2025.

• Other than the U.S., only Bermuda saw its deal share increase by more than one percentage point, year-on-year.

• Re/insurers are using AI for machine learning, data entry and classification, advanced and predictive analytics, large language models, and automation.

By Allen Laman

Cyberattacks are no longer designed solely to cause immediate business disruption.

Instead, they are increasingly engineered to inflict sustained financial, regulatory, and reputational damage that lingers well beyond the initial incident, according to a new portfolio study from Resilience, a cyber risk solutions company.

In its 2025 Cyber Risk Report, Resilience said the cyber threat landscape has shifted away from ransomware campaigns centered on encrypting data and toward pure extortion based on data theft.

As a result, the primary risk is no longer simply going offline, the company wrote.

“[It] is the multi-year legal, regulatory, and reputational ‘tail’ that follows a data exposure event,” the report said. “As the business of cybercrime reaches higher maturity levels, the real risk comes not just from disruption—but duration.”

Resilience found that data theft-only attacks rose from 49% of extortion claims in the first half of last year to 65% in the second half. The company described the shift as a move to a strategy centered on stealing sensitive data, threatening to publish it, and demanding payment.

That approach diminishes the effectiveness of backup-based defenses, which are “ineffective against the primary threat: reputational and regulatory damage from data exposure,” the report said. Resilience also reported seeing instances in which an insured pays a threat actor to suppress stolen data, only to face class-action litigation

after affected individuals are notified of the breach.

And there’s still no guarantee that threat actors won’t sell the data they were paid to suppress.

Resilience predicted this extortion-only model may represent the majority of extortion incidents by the end of 2026. The insurer said organizations must move from recovery-focused strategies to prevention-focused strategies that include data loss prevention, zero trust architecture, encryption at rest, and identity containment.

“Cyber risk is constantly changing,” Vishaal “V8” Hariprasad, co-founder and CEO of Resilience, said in a press release. “As cybercriminals shift their tactics, a new reality is setting in: The real risk is about more than a security incident’s immediate disruption; it’s about the longtail aftershocks that follow.”

In the report, Resilience urged organizations to “prepare for the reality that successful attacks, driven by the shift from

operational disruption to reputational and regulatory exposure, now carry substantially higher financial severity than in previous years.”

Scattered Spider, a cybercriminal group that targets large companies, made industry headlines for its cross-industry campaigns last summer. The group’s series of attacks on U.K. retailers were felt at Resilience; the company reported that the retail sector went from near-zero material losses in its portfolio in 2024 to one of the top three industries for cyber losses, with an average severity of $2.6 million.

Manufacturing remained the highest total loss industry in Resilience’s portfolio—though average severity declined by approximately 29% from the prior year—and health care remained the highest-severity sector. Combined with retail, these three industries accounted for 68% of all portfolio losses.

By Andrea Wells

Small businesses are not immune to the increasing frequency and intensity of severe weather-related events. Even a lengthy power

outage from a winter storm can be a threat to small businesses, leading to economic damage that is difficult to overcome.

“Winter risk is no longer defined solely by snow accumulation or short-lived

disruptions,” writes Monica Ningen, CEO of Swiss Re’s US P&C business, for this issue’s Closing Quote (see page 50).

“Today’s storms bring a combination of extreme cold, heavy precipitation, ice, flooding,

power outages, and extended recovery timelines.”

Research suggests the primary risk facing small businesses after natural disasters is an extended business disruption which can sometimes lead to

permanent closure. The longer it takes for a business to recover from a disastrous event, the more likely that business is to fail.

The trend of billion-dollar natural disaster events is continuing. Billion-dollar events increased from 6.7 events per year from 2000-2009, to an average of 23 events per year from 2020-2024, according to the National Centers for Environmental Information. Insured losses from natural catastrophes topped the $100 billion mark in 2025 for the sixth consecutive year. While the main driver of loss in 2025 stemmed from the Los Angeles wildfires, severe convective storms remain a major global loss driver, reports Swiss Re Institute. Global insured losses from severe convective storms alone were $50 billion last year, making 2025 the third costliest year after 2023 and 2024.

So, what can small businesses do to prepare for the next disaster, and how can their insurance partners help? To safeguard against disastrous scenarios for the small business client, insurance partners should make sure that before disaster strikes, their clients have insurance coverage that is adequate and preparedness plans that will ensure business continuity.

The small business insurance market, as well as the personal lines sector, have both entered 2026 in a stable position, according to Amwins’ Small Business and Personal Lines Outlook. After years of disruption and rate escalation, market conditions have begun to normalize with average rates softening in

some property classes, and capacity and underwriting appetite returning to segments that had become constrained. But natural catastrophe exposures remain key areas of concern, especially in highly populated areas, the report said.

“Severe convective storms, once principally confined to ‘tornado alley,’ have become a nationwide concern. In response, underwriters are deploying detailed geographic modeling to assess micro-region risk (i.e., Los Angeles hill area). Carriers are also increasing scrutiny of roof age, considering it even more important than building age in how a property responds to a wind event,” the report said.

Like much of the personal lines market, the small business owners’ insurance market faced severe frequency and severity of natural disasters over the last several years, William King Sr., director of commercial underwriting at Progressive Insurance, told Insurance Journal. “As a result, geographically disaster-prone areas experienced higher premiums, limited availability, and/or increased use of cost sharing terms from insurers,” King said, adding that because small businesses often operate with tighter or limited safety nets, closing after a natural disaster can be challenging.

Kristin Thelen, assistant vice president, account management at Insureon, Hub International’s small business focused digital agency, said that while the market overall has softened, there’s still a lot of volatility on pricing for small business in higher-risk areas.

“We’ve definitely seen a shift in specific states wanting to write business property; in particular, Florida and California are still problematic,” she said. “We have carriers pulling out of states. The carriers remaining in those states, (have) very high premiums, very high deductibles, and lots of natural disaster exclusions, if you will.” Thus, retaining business has been a challenge for some carriers, she added.

Jerry Palmioli, director of sales at Insureon, said that changing carrier appetites remain an issue. “Carriers are changing their appetite almost monthly,” Palmioli said. “One disaster, one big claim, one storm happens, and carriers are worried about their profit loss margins.”

‘When

a secondary peril event occurs, like flooding, especially like the inland flash flooding that dominated 2025, small business owners oftentimes are left with zero recovery funds.’

Palmioli said that disasters can also lead to a changing risk profile for some small businesses. “We see that on the underwriting side. … It could be a contractor, and because a storm came through an area, now everyone wants to be a carpenter in Florida after a storm, so the underwriting guidelines could change very dramatically for getting insurance,” he said.

Counseling insureds to purchase coverage for the long term is just as important for

the small business client as it is for larger commercial clients. “Don’t just buy coverage for the project, buy it for the long term, otherwise you may never get insured again in the standard markets,” Palmioli said.

Insureon’s Thelen added that success in small business, like with any other commercial insurance, comes from ensuring that the right coverage is offered through a consultative approach. Making sure to have proactive conversations on how the business can mitigate losses—whether it’s property, cyber, or umbrella coverage— and tying those conversations to real life scenarios is key, she advised.

Small businesses are more vulnerable in post-disaster situations oftentimes due to limited cash reserves that could help keep the business afloat. The disaster disrupts operations, creating an uncertain path to recovery.

Flooding poses a significant threat to small businesses, impacting operations, finances, and long-term stability. “When a secondary peril event occurs, like flooding, especially like the inland flash flooding that dominated 2025, small business owners oftentimes are left with zero recovery funds,” said Colin Tinley, senior vice president at Amwins Access. “If you don’t have coverage for those secondary perils like flood, you may have a gap when it comes to recovery.”

Ensuring that small businesses have adequate business income can reduce the coverage gap and help the business outlast disaster-relatcontinued on page 22

continued from page 21

ed closures. But it’s important to choose the right type of business income coverage, according to Progressive’s King.

“Some policies cover the actual loss sustained (ALS) for a certain period of time, and others have specific business income limits,” King explained. “If your coverage is ALS, it is important that the covered time period is substantial enough for the potential closures you may experience. If you have specific limits, then you need to ensure the limits are high enough to support your business needs during the potential closures.”

Amwins’ Tinley added that while small business owners have become more aware of the need for business interruption coverage, there’s still a protection gap in coverage, especially when it comes to floods.

“At the end of the day, if a business isn’t carrying a separate flood policy and a flood shuts them down, their standard BI is typically not going to trigger,” he said. “In addition, if you have a small business and you have an NFIP policy, business interruption is not going to be covered on that policy. So, you could have flood coverage but not have business interruption coverage.”

That’s where the private market can play a key role, he said. “The private market can come in, provide a solution,” he said. “With overall property rate softening, now is a good time to think about how those coverage gaps can be covered,” Tinley suggested. “Because if they’re getting significant rate reductions on their property, we can then come in and say, ‘well, your client may now have some extra funds to increase their overall coverage. So, have you thought about coverage for flood? Have you thought about coverage for business interruption?’ Something like that,” he said.

With climate-related disasters rising in the past decade, business interruption claims have surged, said Ross Sinclair, founder and CEO at UK-based EIP, an embedded insurance program provider. Sinclair believes parametric insurance coverage can play a key role in helping small businesses recover faster than relying solely on traditional insurance.

Parametric products aren’t new, but they are still unfamiliar to many small business owners, Sinclair said. This is starting to change as the impacts of weather-related events escalate, he said.

“Climate-related disasters have increased by more than 80% in the last four decades and, in the first half of 2025 alone, natural disasters caused about $131 billion in losses worldwide, with only roughly $80 billion insured, leaving many businesses exposed when they need cash

the most,” he told Insurance Journal. “At the same time, more frequent disputes and delays around business interruption coverage can force firms into litigation just to access a payout.”

“This is where parametrics structures can be particularly attractive as they reduce ambiguity and the incentives to litigate,” he said.

In his view parametric products can alleviate the administrative burden and deliver faster payouts for the business, especially for weather-related insurance, resulting in less disgruntled end customers. “From the insurers’ perspective, not only is this reputationally beneficial, but the reliance on pre-agreed triggers verified by third-party data supports pricing modeling and reduces the operational costs of claims processing overall,” Sinclair added.

With parametric insurance, the insurer and the policy-

holder agree upfront on the payout and the circumstances that trigger the release of the payout.

“That means there’s no debate after the event about what happened or how much should be paid,” he said. “Simply put, if the trigger is met, the money is released.”

The payout structure can be a fixed amount, resulting in a single, pre-set payment once the threshold is reached, or tiered, where the payment increases in line with the intensity of the event.

For example, imagine a small business in an area prone to winter flooding that wants protection if flooding interrupts operations, he said. “The trigger might be floodwater reaching a specified depth, say one metre, measured using an agreed third-party data source,” Sinclair explained.

“If the policy is written with a fixed payout, then as soon as floodwater reaches one metre,

the pre-agreed amount is automatically paid.”

Sinclair said that quick access to cash can help the business keep paying rent, suppliers, and wages in the immediate aftermath of a flooding disaster, while business income may be disrupted and traditional claims processes proceed.

Parametric insurance isn’t designed to replace the full end-to-end insurance lifecycle, he said, but instead serves as means of first response.

“As the trigger and payout are agreed in advance, business can access liquidity quickly and avoid the kind of cashflow death spiral that can follow a major disruption,” Sinclair noted. “Traditional business interruption indemnities can then sit above it, dealing with repairs and more complex loss calculations over a longer restoration period once the firm has a bit of breathing room.”

Simple parametric products

often are embedded into the sales process for consumer products such as flight delays or cancellations due to weather-related incidents. Other more complex parametric insurance products such as flood may require that the client and insurer both agree on the triggers and payout beforehand, Sinclair said.

“Parametric insurance first gained traction in flood scenarios because the triggers were relatively straightforward to define—flood depth is measurable and it can be linked cleanly to a payout,” he said. “Since then, the concept has broadened and can be applied to a wide range of risk factors as long as there is a clearly defined trigger that can be measured consistently using agreed data. It’s less about the type of disaster and more about whether the event can be measured reliably with objective data.”

Because parametric

policies are built on preagreed triggers, payouts are easier to model and price and operational costs can be lower since claims aren’t being adjusted in the traditional way, Sinclair explained. Plus, the growing availability of realtime, AI-powered climate and hazard data from sources such as satellites makes it easier to monitor events quickly and verify whether triggers have been met. “This can help insurers and communities coordinate recovery faster because funding arrives sooner and with less administrative friction,” he said. “It also helps reduce the reputational and financial drain of prolonged claim disputes, which can be damaging for insurers and devastating for policyholders trying to reopen and rebuild.”

The U.S. parametrics market is predicted to grow. “The market is currently valued at $4.29 billion, which forecasts estimate will grow to $7.84

Progressive’s King encourages agents to check in on their small business clients periodically to possibly adjust coverage limits that might better align with the business’s changing needs, especially as the small business grows over time. This is where working with an agent can help, he said. “Working with an agent can help provide more confidence and expertise in choosing the right coverage and policy for your business needs and also assist with navigating the claims process,” King said. “Often, growth or changing business operations could result in different insurance needs like expanding locations,

higher sales, or hiring more employees, so it’s encouraged for business owners to engage with their agents on a regular basis.”

Small businesses, whether they have business income coverage or not, can potentially reduce impact and loss from weather events with business continuity planning, King added. “Business continuity planning helps small business owners understand their risks and identify preventative measures, including actions they can take pre- and post-event to reduce loss.” He also suggested that small businesses revisit their plan often to ensure it is up to date.

billion by 2035 at a compound annual growth rate of 7.82%,” he said. “This aligns with the idea that as climate volatility increases, demand for products that allow subjective and comprehensive cover will follow suit.”

In late February, Floodbase, an insurance platform for insuring flood risk, and Liberty Mutual announced the launch of an instant quoting application for parametric flood (re) insurance in the U.S.

“It’s the same coverage—just delivered faster and with far less friction, enabling the brokers to effectively explore and customize a client’s flood coverage in seconds before even emailing an underwriter,” said Jean-Christophe Garaix, head of Parametrics & Agriculture at Liberty Mutual, in a media statement. The collaboration “not only improves the client and distribution experience, it enables us to respond to evolving flood risk

with novel parametric products for small-and-medium market segments.”

“Parametric flood can be an effective risk management instrument bridging protection gaps in traditional policies for small-and-medium businesses in the U.S.—but that requires rapid distribution at scale,” added Bessie Schwarz, co-founder and CEO of Floodbase.

A quick search on MyNewMarkets.com, a division of Insurance Journal, showed several other parametric products for disaster related risks for small businesses, including:

• Parametric Wind by Siracusa Risk Management

• Parametric Flood, Wind and Business Interruption by Parametric Risk

• Parametric Earthquake Insurance by Jumpstart

• Auto Dealer’s Open Lot with a hail parametric offering by Amwins

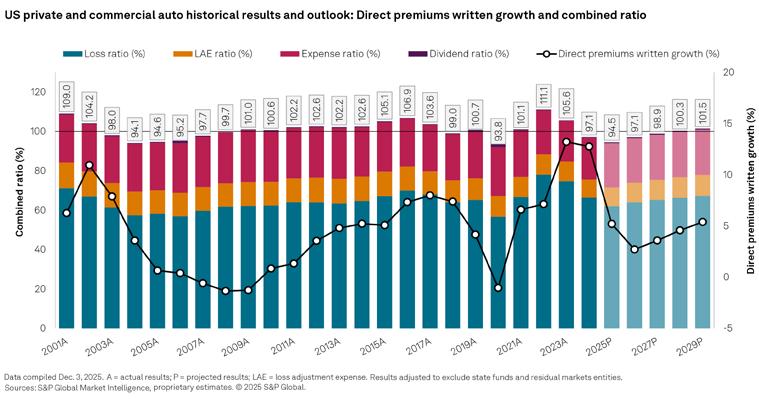

By Susanne Sclafane

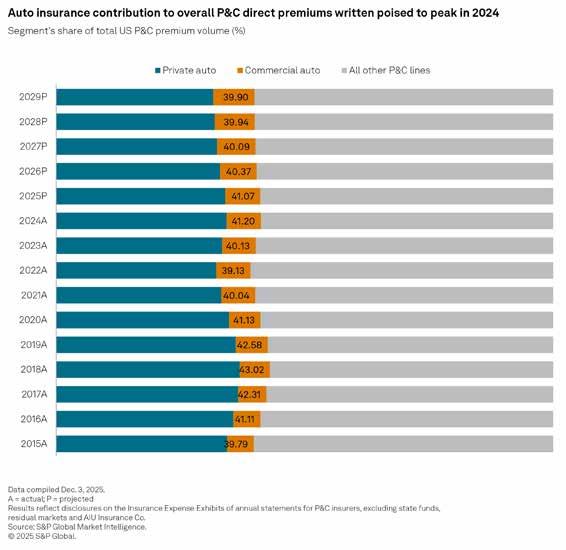

In their latest report on the U.S. auto insurance market, analysts from S&P Global Market Intelligence predict the strongest overall U.S. property/ casualty insurance underwriting results in 18 years for 2025, driven by favorable private passenger auto outcomes.

Still, while their 2025 projected combined ratio across all lines is now 96.2, three points better than a midyear projection of 99.2 estimated for the year in August, “success is anticipated

to be temporary due to various market dynamics and challenges,” S&P GMI said in a December statement.

The media statement announced the publication of the firm’s 2025 U.S. Auto Insurance Market Report, which stresses the significant weight that auto insurance has on overall P/C insurance industry results.

Together, S&P GMI estimates that private and commercial auto insurance will account for 41.1% of total U.S. P/C direct premiums written in 2025 when final results are

tallied—slipping down slightly from a five-year high of 41.2% achieved in 2024, reflecting the impact of competition emerging in the private auto market.

the first sub-97 results in successive years since 2006-2007, according to the statement.

S&P GMI projects a 94.5 2025 combined ratio for auto insurance (personal and commercial together), driving the all-lines P/C combined ratio down to 96.2, compared to 96.5 in 2024. This marks

Offering reasons for the industry’s success in 2025, S&P GMI noted the impact of “a generational hard market in personal lines,” as well as a benign year for natural catastrophes. “These factors are unlikely to recur, suggesting that the current level of success may be fleeting,” S&P GMI said.

In particular, the private auto business has seen accelerated competitive dynamics, “with rate decreases matching rate increases and increased advertising spending,” the statement said.

Focusing on the 94.5 combined ratio projected for the combination of personal and commercial auto lines, the report notes that in the last two decades, the auto insurance business only produced a better result once—93.8 in 2020—when COVID-19 lockdowns fueled a precipitous drop in claims frequency. Even sub-100 combined ratios had been scarce from 2009 through 2023, with 2018 marking the only year other than 2020 with a result below breakeven.

Looking ahead, S&P GMI expects auto insurance combined ratios to breach the breakeven level again in 2028, edging up to 97.1 in 2026 (matching 2024’s auto com-

bined ratio) and 98.9 in 2027, according to the full report.

“Though we project that the combination of the private and commercial auto insurance businesses will post some of their strongest underwriting results on record in the near term, this is not to imply that the market is devoid of risks,” the report says. “Social inflation, or the escalation in claims severity due to adverse litigation trends, has vexed the commercial auto business for years, and recent results suggest that it is becoming a more significant threat to the private auto business—particularly among at-fault drivers with higher limits of liability under personal umbrella policies.”

“The political environment remains a wildcard as elected officials propose and/or implement policies with direct or indirect implications for auto insurance….[T]he generational hard market of the past several

years in both private auto and homeowners has prompted calls for revisions to rate filing regimes that are likely to crescendo in 2026 to the extent our projections for continued historically favorable levels of profitability pan out.”

Also mentioned in the report is the tariff wildcard. Even though tariffs received a lot of attention earlier this year, they ultimately did not impact auto physical damage results. Still, future emergence cannot be entirely ruled out, S&P GMI suggests.

(Editor’s Note: Separately, S&P GMI projects a 92.7 combined ratio for personal auto in 2025 and 104.3 for commercial auto. If it actually lands at 92.7, the personal auto combined ratio result “would rival 2020 for the best private auto combined ratio [92.5] in at least 30 years,” without the material changes in driving behavior that accompanied a

global pandemic.

Although S&P GMI doesn’t project that the personal auto combined ratio will rise above 100 until 2029, the text of the report suggests that a nearly 3-point improvement in the commercial auto combined ratio could be short-lived. The official forecast is for commercial auto combined ratios to move up slowly—from 104.4 in 2026 to 106.3 in 2029. But referring to historical results that could repeat, the text said that a 3.5-point improvement in 2014 was followed by five years of pre-pandemic ratios ranging from roughly 109-111.)

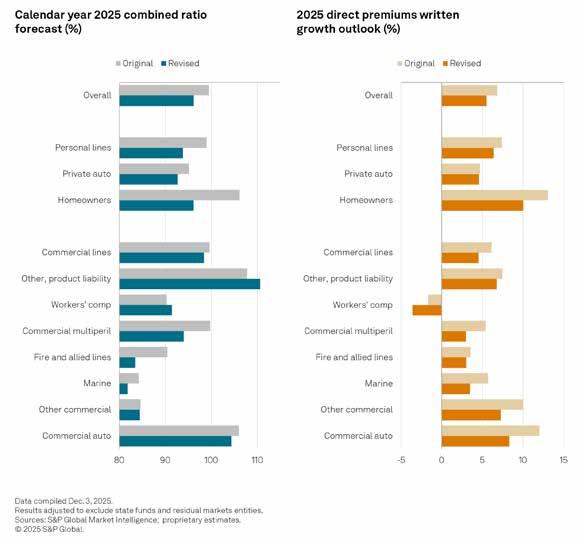

In addition to auto insurance, the 2025 U.S. Auto Insurance report, published in late December, includes full-year 2025 combined ratio projections for homeowners insurance in personal lines and for several commercial lines,

as well as projections of direct written premium growth for the same lines.

Comparisons to earlier projections delivered in S&P GMI’s 2025 U.S. Property and Casualty Insurance Market Report, published in August 2025, are shown graphically in the latest report on auto lines and set forth below.

The latest combined ratio projections are generally better than the August projections, with the homeowners line showing the greatest change—falling down from a forecast of 106.1 in August to below 100 (96.2) in December. The only line for which the forecasted full-year combined ratio moved in the opposite direction is commercial liability (other liability and product liability), which moved from 107.8 in the August report to over 110 in December.

Previously, the homeowners continued on page 26

continued from page 25

combined ratio projection had incorporated expectations for another active severe convective storm season in the second quarter and an average hurricane season in the third quarter—neither of which materialized.

“Meanwhile, adverse reserve development in certain casualty lines is running ahead of what we presumed to have been conservative projections,” the report says, commenting on the commercial liability lines. “This is particularly worrisome given that the fourth quarter, when companies occasionally implement ‘kitchen-sink’ reserve charges, lies ahead.”

As for premium growth, S&P GMI hasn’t changed its personal auto forecast of a jump of about 5% in 2025, compared with 2024, but analysts now project commercial auto insurance direct premiums “expanding at a more sluggish pace” than previously expected. In the August report, S&P GMI put commercial auto premium growth at 12%, but the forecast now falls below 10%, according to the graphical comparison.

On the personal lines side, S&P GMI has also taken down its projected growth rate for homeowners insurance—to roughly 10%, according to the December auto insurance report, down from 13.1% in the August analysis.

S&P GMI’s December auto insurance report also includes:

• A discussion of macroeconomic factors and their impact on the auto insurance business.

• Separate analyses of liability and physical damage combined ratios and growth rates for personal and commercial auto insurance segments.

• Lists of the top 20 personal and commercial auto insurers, showing five years of direct premiums and loss ratios for each insurer (2020-2024).

• Maps providing state-bystate loss ratio comparisons (five-year loss ratios for 20202024, presented separately for personal auto liability, personal auto physical damage, commercial auto liability, and commercial auto physical damage).

• Maps indicating 2025 rate-change relativities for

personal auto by state, and cumulative rate changes from 2021 through 2024.

• Discussion and analysis of advertising spending of major personal lines direct writers.

• Crash frequency statistics for commercial trucks and the analysis of E&S growth in the commercial auto market.

Throughout the report, S&P GMI also reminds auto insurers of long-term challenges on the horizon as the potential shift toward autonomous vehicles requires insurers to plan for a future with different risk profiles and coverage needs.

Conceding that “the promise of full autonomy

within the private passenger fleet seemingly remains years away,” the report advises that “no matter how distant the transition, auto insurers have had no choice but to plan for a future that may look very different than the present and past.”

Sclafane is Executive Editor of Carrier Management, a publication of Wells Media Group serving property/casualty insurance carrier executives. She is a media professional with deep background in the P/C insurance industry including 25 years as editor and reporter for trade magazines, online news services, digital journals. Her prior experience includes 14 years as a casualty actuary.

By Jonathan Stempel

PacifiCorp, a utility owned by Berkshire Hathaway, agreed to pay $575 million to resolve U.S. government damages claims related to six wildfires in Oregon and California that burned nearly 290,000 acres of federal land, the U.S. Department of Justice said this month.

The settlement resolves claims that PacifiCorp’s electrical lines negligently started the fires.

Five of the fires – Archie Creek, Echo Mountain Complex, Slater, South Obenchain and 242 – began during Labor Day weekend in 2020 and burned approximately 250,000 acres of federal land. The sixth fire, McKinney, began in July 2022 and burned 39,000 acres of

Acontractor in Washington was fined $200,000 for putting workers at risk during a demolition project at a home in Bellevue, Washington.

The Washington State Department of Labor & Industries cited Seattle Environmental Services LLC for knowingly exposing workers to toxic conditions on a 2025 project while telling inspectors that the site was safe.

negative for asbestos, making respiratory gear optional.

However, Seattle Environmental Services couldn’t provide evidence that they actually tested the material that they planned to tear out for asbestos, so inspectors posted an order to stop the work, according to L&I.

When inspectors were called to a home in Bellevue, the owner of the company reportedly told inspectors that the job was a general demolition project, and that samples that were tested came out as

L&I said evidence was present that looked like the contractor was treating the jobsite like an asbestos removal project. Inspectors took pictures of yellow bags designed for asbestos waste, and a negative air machine was also found with an exhaust tube running through the property’s sliding door, inspectors say. When the contractor produced test

federal land.

PacifiCorp’s payment will help repay the government for firefighting costs, and allow the Forest Service and Bureau of Land Management to restore some of the burned land.

The settlement “ensures fair compensation to the American taxpayer,” and “strikes a balance by addressing the government’s significant fire-suppression costs and loss of natural resources without preventing PacifiCorp from offering electricity at fair prices,” Principal Deputy Assistant Attorney General Adam Gustafson said in a statement.

PacifiCorp denied liability in agreeing to settle, the Justice Department said. The utility did not immediately respond to requests for comment.

The settlement was announced three days after PacifiCorp said it planned to sell many of its assets in Washington state to Portland General Electric POR.N for $1.9 billion, to bolster liquidity as it defends against wildfire litigation.

(Reporting by Stempel in New York; Additional reporting by Costas Pitas and Ismail Shakil; Editing by David Ljunggren and Deepa Babington) Copyright 2026 Reuters. All rights reserved.

results hours after the work stopage, it was confirmed that nearly 3,000 square feet of walls and ceilings contained asbestos. By the time the test results were available, three workers had already removed the toxic material without using proper respirators and decontamination showers, according to L&I.

L&I said that after the initial story, the employer said he mixed up the abatement job with another. He worked with inspectors to make sure that the asbestos debris was removed, which led L&I to allow the company to restart the work on the site.

Seattle Environmental Services was cited 10 times for willful serious violations, as well as six serious and four general violations for ignoring rules for removing asbestos and for providing inaccurate information to L&I.

E&S is now SPG Wholesale | Specialty Program Group

Anew bill in California would require insurers to offer homeowners insurance to those who meet state home hardening and defensible space requirements.

Senate Bill 1076, the Insurance Coverage for Fire-Safe Homes Act, was introduced by Senator Sasha Renée Pérez (D-Pasadena) and is co-sponsored by the Eaton Fire Survivors Network and Consumer Watchdog in response to wildfire survivors’ concerns that they could lose coverage after they rebuild, even if they meet the highest wildfire safety standards.

SB 1076 requires insurers to offer homeowners insurance to Californians who meet state home hardening and defensible space requirements set by the insurance commissioner.

“I’ve spoken with Eaton Fire survivors whose newly built homes will meet the highest levels of protection against wildfires but still fear they won’t be able to purchase insurance,” Pérez stated. “Being denied coverage after meeting safety standards sends the wrong message and is akin to being penalized for doing the right thing. SB 1076 will ensure that our communities’ insurance needs are met by making coverage available to them for making existing neighborhoods safer.”

The legislation would:

• Require carriers to offer and renew coverage for any home that meets

wildfire-safety standards adopted by the insurance commissioner, including home hardening measures and defensible-space requirements.

• Allow the insurance commissioner to impose a five-year bar from both home and auto markets for insurers that refuse to comply.

“On and after January 1, 2028, this bill would prohibit an admitted insurer that offers or sells residential property insurance in this state from refusing to offer, sell, or renew a policy of residential property insurance for an applicant or insured whose property meets minimum

Abill intended to combat insurance fraud by updating a 20-year-old law passed the Washington state senate in late February.

Senate Bill 6031 defines insurance fraud as its own crime, a Class B felony.

The bill passed on a unanimous vote.

Insurance Commissioner Patty Kuderer.

SB 6031 was pushed for by Washington

State law established the Office of the Insurance Commissioner’s Criminal Investigation Unit in 2006, but the law hasn’t been updated since.

With SB 6031, Kuderer believes this gives the unit modern tools to investigate modern fraud.

The bill expands “victims of insurance

home hardening and wildfire mitigation standards, except as provided,” the text of the bill states. “The bill would authorize an admitted insurer to apply to the commissioner for a temporary waiver of that prohibition in a particular geographic area of the state, as specified. On and after January 1, 2028, the bill would also require any residential property insurance offered or sold to, at a minimum, provide coverage equivalent in scope to the residential property coverage the admitted insurer most commonly offers or sells in this state.”

The bill is awaiting referral to a committee.

fraud” to include insurance consumers and insurance beneficiaries, making them eligible for criminal restitution.

SB 6031 would also expand statutory reporting of suspected insurance fraud to the commissioner by adding regulators of healthcare or financial services professions, and other law enforcement and public safety agencies as among the required reporters of suspected fraud.

The bill now moves to the state House of Representatives for consideration.

Commercial & Recreational Marine

Market Detail: RISCO has marine expertise for commercial and recreational marine business. We assist brokers with all their marine needs. Available Products & Services, including but not limited to:

Commercial Marine: Marine Contractors, Ship Repairers, Boat Builders, Boat Dealers, Terminal Operators, Vessel Operation (passenger vessels, tour boats, ferry services), Marine and Allied Industries (including Manufacturers & Wholesalers), and Cargo.

Recreational Marine: Marinas, Boatyards, Yacht Clubs, Boat Dealers, Yacht Builders, and Marine Artisans.

Coverages: Hull & Machinery, Protection & Indemnity, Jones Act (crew coverage), Builders Risk, Builders Risk P&I, Property, Contractors Equipment, Commercial Liability, Product Liability, Marina Operators Legal Liability, Ship Repairers Legal Liability, Vessel Pollution, Wharfingers, Piers, Wharfs & Docks, and Bumpershoot.

Available Limits: Not disclosed.

Carrier: Admitted and non-admitted. States: Connecticut, Maine, Massachusetts, New Hampshire, and Rhode Island.

Contact: Charles Finnegan, riscocl@ risco-inc.com, 800-533-3649

Market Detail: Optimal Property Coverage Solutions - Expert IGP Specialty Property team provides optimal solutions for property clients. Their team leverages its extensive experience and market partnerships to build property programs tailored to the needs of insureds. They focus on schedules of all sizes; CAT and non-CAT; and specialized lines of property coverage.

Specialized Coverage: Builder’s Risk, Catastrophic Exposed Property, Deductible Buydown, DIC, Flood, Inland Marine, Multi-Peril, Shared/Layered Schedules, Stock Through-Put, and Terrorism.

Target Areas of Expertise: Real Estate, Condominiums, Commercial, Mixed Use, Multi-Family/Apartments, Vacant Property, Hospitality and Entertainment, Bars/ Nightclubs, and Hotels/Motels.

Other Industries: Agribusiness, Environmental and Energy Facilities,

Healthcare Risks and Manufacturing/ Distribution/Warehousing.

Available Limits: Not disclosed. Carrier: Not disclosed.

States: All 50 states and the District of Columbia except Alaska and Hawaii.

Contact: Alan Griesemer, alan.griesemer@ usi.com, 800-241-6633

Assisted and Independent Living

Market Detail: Convelo brings decades of experience providing insurance for senior living clients, supported by a deep understanding of the industry today. Expertise and strategic alliances put the company in a prime position to offer foundational products like package insurance and workers’ compensation, along with supporting products like cyber and management liability. Lean on Convelo’s expertise to help win clients’ business and trust by offering the best possible protection. The program is a true package product on A+ admitted paper—a winning combination that clients would be hard-pressed to find anywhere else.

Coverages: Property, Liability, Auto, and Excess.

Target accounts for Assisted and Independent Living program include nonprofit assisted and independent living facilities with ambulatory residents age 55 and up; best-in-class facilities with multiline premiums $25K and up; operations in all states except AL, AK, CA, LA, MS, WA, and WY. Facilities must be in operation for at least five years with historic loss ratios consistent with well-controlled operations. Buildings must be equipped with automatic sprinkler systems.