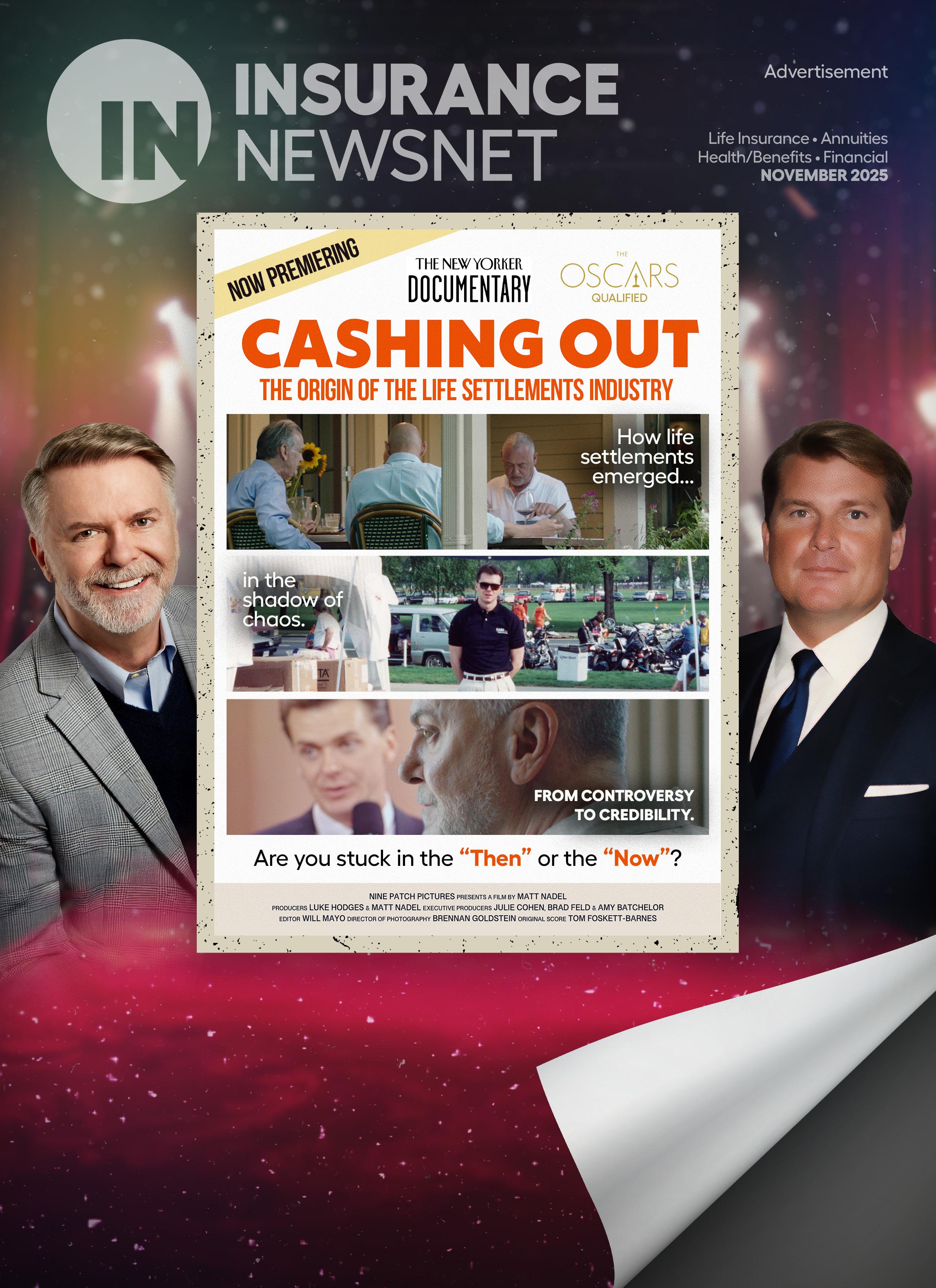

As featured in the Oscar-qualified documentary, Cashing Out, entrepreneur Scott Page founded the settlement industry in 1989 by pioneering viatical settlements for people with AIDS, launching what has evolved into a regulated and credible planning tool trusted by advisors and clients today.

Back then: policies were sold to survive.

Today: life settlements unlock value, choice, and dignity in financial plans.

Proof: An Industry with Roots and Stability

• $601M paid to policyowners in 2024 (often over 6.5x surrender value).

• $842M paid in 2023—putting $707M more in consumers’ pockets than surrender or lapse.

• Since 2021: nearly $16B of policies settled; over $3B in direct consumer value.

• Regulated in 45 states with licensing, disclosures, and oversight.

The Power of LISA

Since 1994, the Life Insurance Settlement Association (LISA) has been the industry’s voice, setting standards, educating professionals, and aligning capital, compliance, and client value so that life settlements consistently deliver on their promise.

The Film: Cashing Out

Directed by Matt Nadel, produced by Luke Hodges and Matt Nadel, Cashing Out connects the industry’s origins to its modern legitimacy — featuring pioneers like Scott Page. This film was produced with the generous support from the Life Insurance Settlement Association.

It’s how the Then became the Now.

Scan to Take the Next Step

• Download the LISA Life Settlement Guide

• Watch Cashing Out

• Connect with Rob Haynie & Life Insurance Settlements, Inc.

The Trailblazers Who Paved the Way

SCOTT PAGE — The Visionary Who Started It All

• Founded The Lifeline Program (1989), originating the market.

• Testified before regulators and legislators; advanced consumer protections.

• Featured by national media (Newsweek, New York Times, NBC Nightly News, Fox Business, 20/20, WSJ, The Economist).

• Continues as an expert witness, educator, and advocate for client choice.

ROB HAYNIE — Managing Director of Life Insurance Settlements, Inc.

• 32-year veteran and industry leader; his company has negotiated thousands of settlements

• Vice Chair, LISA Board; incoming Chairman (2026).

• LISA Leadership Award recipient.

• Global speaker; Life Settlements topic author; co-host, Unlocking the Hidden Value of Your Life Insurance

• Widely recognized as Mr. Life Settlements, advancing best practices, education, and adoption.

Sponsored by Life Insurance Settlements, Inc. In partnership with LISA and Cashing Out

IN THIS ISSUE

INTERVIEW

8 Annuities are for everyone

Annuity sales are skyrocket ing, and Mike Downing is on the front lines of those record-busting sales. The copresident of Athene discusses the demand for annuities and where sales could go in the future.

FEATURE How AI is reshaping the insurance industry

By Rayne Morgan

How carriers are leveraging technology and transforming the value chain.

ANNUITY

30 Fixed annuities give clients more money to spend in retirement By Kourtney Gibson and Colbert Narcisse

Annuity income can be the difference between a frugal retirement and one that provides a retiree with dignity and happiness.

HEALTH/BENEFITS

34 The care gap: Medicare and insurance won’t cover this By Paul Feldman

Advisors avoiding senior care discussions are putting their clients at risk.

INSURTECH

IN THE FIELD

20 Saving money and relationships

By Susan Rupe

Claire Dubé teaches financial self-care and healthy financial behaviors.

LIFE

26 How life insurance closes the financial confidence gap By Ramon Casanova Life insurance builds security amid consumers’ financial concerns.

38 Consumer insights reveal how insurers can ‘plant a flag’ with agentic AI By

Rayne Morgan

A study shows consumers are comfortable using artificial intelligence when researching a product or service.

BUSINESS

40 AI won’t save your leadership: It will expose it By Casey Cunningham

AI helps great leaders shine while exposing weak leaders.

IN THE KNOW

42 The architect behind Manulife’s AI revolution By Rayne Morgan

Jodie Wallis describes how Manulife is using AI in all its operations.

Will we need AI to monitor AI?

As we look at technology in this month’s issue, artificial intelligence jumps out as the trend that continues to receive the most buzz in the insurance industry.

One survey, for example, found that 88% of auto insurers currently use, plan to use or plan to explore using AI intelligence or machine learning as part of their everyday operations. Seventy percent of home insurers plan to do the same.

AI has been employed across the industry at many levels:

• Underwriting: AI is used to assess risk by analyzing vast amounts of data, including historical claims, demographics and real-time data such as weather patterns and social trends.

• Claims processing: AI automates claims processing by quickly evaluating damage, evaluating damage and fraud detection and determining payouts. This reduces the time it takes to settle claims and ensures accuracy.

• Customer service and chatbots: AI-driven chatbots and virtual assistants provide 24/7 customer support. They can answer policyholders’ questions, help with policy changes and even initiate claims reporting.

• Predictive analytics: AI algorithms analyze data to predict future trends, such as identifying high-risk areas for specific types of claims (e.g., auto accidents or property damage). Insurers can use this information to adjust pricing and underwriting strategies.

• Fraud detection: AI helps detect fraudulent claims by identifying patterns and anomalies in data. It can flag suspicious activities, reducing insurance fraud and reducing costs for insurers.

• Risk assessment : Insurers use AI to more accurately assess the risk of insuring specific individuals or properties. This leads to more personalized pricing and coverage options.

• Customer engagement: AIpowered tools personalize marketing and communication efforts, improving customer engagement and retention. Insurers can offer relevant policy

You're AI!

recommendations and incentives based on customer behavior.

• Telematics: In auto insurance, telematics devices and AI analyze driving behavior, allowing insurers to offer usage-based insurance policies. Safer drivers may receive lower premiums.

• Data analysis: AI can process and analyze vast amounts of data to uncover insights, helping insurers refine their business strategies, improve operational efficiency and make datadriven decisions.

• Policy management: AI streamlines policy administration by automating tasks like policy issuance, endorsements and renewals, reducing manual errors and administrative costs.

• Risk modeling: AI helps insurers create sophisticated risk models by considering a wide range of variables and scenarios, enhancing their ability to manage risk effectively.

• Health insurance: AI is used to assess health risks, optimize pricing for health insurance policies and support claims processing in the health insurance sector.

• Property/casualty insurance: In P/C insurance, AI can assess property values, calculate replacement costs and estimate the risk of natural disasters.

• Reinsurance: AI is employed in reinsurance to assess and price risks more accurately, helping reinsurance companies manage their portfolios effectively.

• Regulatory compliance: AI can assist insurers in staying compliant with evolving regulations by monitoring and adapting policies and practices.

One of the more interesting uses for AI is developing what is called “synthetic

No you're AI! Bro, we're all AI.

data,” which can be used to improve predictive modeling when, for example, there may be a lack of actual data for certain models.

Overall, AI has the potential to modernize and make more accurate and efficient many aspects of the insurance industry. At the same time, there are concerns about oversight and regulation — to ensure that its use does not create discrimination issues, for example. As Senior Editor John Hilton writes about in this issue, the National Association of Insurance Commissioners has been surveying each segment of the insurance industry to quantify exactly who is using AI and how they are using it. The NAIC will use this information in developing AI guidelines for the industry. As rules and regulations evolve, including at the state level, we will see how the oversight of AI develops.

Overseeing AI, however, has a number of wrinkles. There are, for example, “AI hallucinations” where AI programs make up information out of whole cloth, based on no real data or information. As we see more uses of AI to create images and video, there is more opportunity to move away from “reality” and create very convincing content that misrepresents the facts.

The next question after regulation is developed, though, is how to monitor AI use. Many uses of the technology are so complex, they may require AI tools to monitor and ensure compliance.

At that point, will we have AI overseeing AI?

John Forcucci Editor-in-chief

A TIME-SAVING WAY TO GET YOUR BUSINESS ISSUED FAST

Save time and get paid fast by using our e-App Storefront, your go-to place to submit Medicare supplement, dental insurance and hospital indemnity business.

Get Paid Sooner

Applications are typically issued in days, which means you get paid faster.

Ensures Apps Are in Good Order

Look for alerts notifying you to enter any missing information before continuing to the next step. This ensures all apps are submitted in good order.

Sell More at Once

Quickly pivot from a Med supp to a dental plan to a hospital indemnity plan application once a customer’s information is entered.

Keep Track of Your Apps

Check the dashboard to get realtime updates on the status of your submitted apps.

More Signature Options

Choose the signature option that best meets your clients’ needs and payment method. Access the e-App Storefront today! mutualofomaha.com/broker

GLP-1 drugs could slash mortality rates

The continued use of GLP-1 weight loss drugs could cut mortality rates by up to 6.4% by 2045, according to new research spearheaded by Swiss Re. The study considers the long-term ram ifications of the explosive growth of GLP-1s.

Among U.S. adults, usage of GLP-1 drugs for weight control and Type 2 diabetes treatment rose to more than 4% in 2024, a fivefold increase in five years, according to FAIR Health data.

The market size for GLP-1s is expected to grow at about 26% annually through 2033, Grand View Research estimated. It is large enough to change the mortality projections that are crucial to life insurance and annuity pricing.

Under optimistic scenarios, Swiss Re projects that GLP-1 medications could reduce all-cause mortality in the United States by as much as 6.4% by 2045. In the United Kingdom, the research suggests a reduction of over 5% is possible.

AUTO LOAN DEFAULTS ARE SOARING

The cost of buying and maintaining a car continues to grow, so it shouldn’t be much of a surprise that auto loan defaults and repossessions are rising as well. The Consumer Federation of America warned that the record number of defaults “is a canary in the coal mine for large-scale economic problems.”

Americans owe more than $1.66 trillion in auto debt and a crisis is happening “just as our nation’s federal watchdogs — the Consumer Financial Protection Bureau and the Federal Trade Commission — have taken significant steps back from oversight and enforcement of predatory practices in the auto market,” a recent CFA report said.

The average vehicle sells for nearly $50,000 and almost 20% of new car buyers are paying $1,000 or more a

month on their loan, the report said. Nearly 1 in 5 new car buyers in the first quarter of 2025 have a loan that is seven years long. Used car prices also rose 6.3% year over year.

There is this big dichotomy between higherincome and lower-income consumers which continues and is a real issue.”

— Charles Scharf, Wells Fargo CEO

Insurance challenges have forced onethird of home searchers to completely change the geographic area where they are looking for a home, and another 30% have cast a wider net and expanded their initial target geography. Nearly one-quarter of home searchers have completely changed strategies based on insurance challenges.

NEW AND PROSPECTIVE HOMEOWNERS FACE INSURANCE WOES

Nearly half of recent and prospective homebuyers have faced trouble or expect to face trouble obtaining or renewing homeowners insurance, according to a recent Realtor.com survey. Some said the situation is so bad they could forgo homeowners insurance altogether.

Nearly 9 out of 10 of those surveyed believe that they will pay more for homeowners insurance in the future and 42% have already confirmed they have experienced a rise in home insurance costs. Three-quarters believe homeowners insurance could ultimately become unaffordable.

CLEVELAND FED CHIEF WARNS OF CHALLENGES

Cleveland Federal Reserve President Beth Hammack said it’s “a challenging time for monetary policy” as the Fed cuts interest rates in the midst of sticky inflation.

In an interview with CNBC, Hammack said the Fed faces challenges as it attempts to balance fighting stubborn inflation and protecting jobs.

The Fed approved a rate cut in early September, lowering its benchmark overnight lending rate by a quarter percentage point to a range of 4.00%-4.25%, and signaled more cuts were on the way before the end of the year.

Hammack

65%+ INCOME REPLACEMENT

THE LAYERED SOLUTION

The High Limit Disability income protection plan was developed specifically to meet the needs of those needing supplemental disability insurance. A High Limit Disability plan through Lloyd’s of London provides coverage to those who would like to obtain more protection beyond their existing inadequate disability plans. Our goal is to provide at least 65% replacement of income. Lloyd’s of London is the only market that makes this available.

As incomes increase, the issue and participation limits of traditional Disability Insurance carriers decrease. To properly insure a highly compensated individual at 65% of income, multiple disability income plans are often required and are layered to provide sufficient income protection.

The following scenario illustrates the way income protection plans can be layered to provide an individual with 65% coverage of monthly income.

EXECUTIVE

INCOME: $900,000 annually

$75,000 monthly

What’s in the news on InsuranceNewsNet.com

Regulators move closer to finalizing AG 49-A and new reinsurance rules. Copyright lawsuits over AI training raise risks for advisors. And Gen Z warns insurance’s slow AI adoption is worsening the talent gap.

[Editor’s Note: These are some of the major stories to which we are devoting ongoing coverage at INN. Visit our website to sign up for our free newsletters at insurancenewsnet.com/subscribe and don’t miss another important story!]

Copyright lawsuits highlight potential risks for agents using AI tools in marketing

By John Forcucci

Artificial intelligence has quickly become a staple for independent insurance agents and financial advisors seeking to streamline client communications and build a presence on social media. But experts warn that the same tools fueling efficiency also carry significant copyright risks.

That was the message from a panel of international copyright attorneys and industry leaders hosted by the Copyright

Clearance Center. Speakers detailed a wave of lawsuits in the United States and abroad targeting AI companies over how they gather, train on and reproduce copyrighted content.

Dozens of US lawsuits

Nancy Wolff, a veteran copyright attorney, noted that more than 50 lawsuits are pending in U.S. courts, largely in California and New York, with publishers and authors challenging AI developers

Using outputs directly in advertising or client-facing materials could expose firms to claims if the generated text or images resemble copyrighted works.

such as OpenAI and Anthropic.

“These cases will take years to resolve, but the central questions involve whether AI training is a substitute for original works and whether licensing is required,” Wolff said. She emphasized that under U.S. law, copyright protection is territorial, and fair use — the doctrine allowing limited use of copyrighted material without permission — is highly fact-specific.

For financial professionals, the lesson is that AI tools may be built on content whose legal status is unsettled. Using outputs directly in advertising or client-facing materials could expose firms to claims if the generated text or images resemble copyrighted works.

International disputes

Across the Atlantic, the U.K. and the European Union are also wrestling with AI and copyright. British attorney Hayleigh Bosher pointed to Getty Images’ lawsuit against Stability AI, alleging that millions of photos were scraped without permission to train the popular image generator Stable Diffusion.

Unlike the U.S., the U.K. relies on narrower “fair dealing” exceptions, which make it harder for AI developers to argue that mass data scraping is permissible. The European Union has introduced new rules for text and data mining, but courts are already fielding challenges about how they apply to AI systems.

Read the full story online: https://bit.ly/copylaw25

John Forcucci is InsuranceNewsNet editor-in-chief. He has had a long career in daily and weekly journalism. Contact him at johnf@innemail.com.

NAIC moves closer to finalizing AG 49-A

By John Hilton

A

National

Association of Insurance

Commissioners’ group took another step toward finalizing a pair of key guidelines.

The Life Actuarial Task Force posted Actuarial Guideline 49-A and the new AG 55 for a 21-day comment period following the meeting. Minor language tweaks are involved with the former guideline, while regulators seek comment on draft templates for AG 55.

But there remains a bigger issue still to be resolved with AG 49-A.

Approved in 2020, AG 49-A limits the maximum illustrated rate that insurers can use in policy projections to prevent unrealistic growth assumptions. It includes restrictions on exaggerated benefits from indexed loans, a strategy that previously allowed aggressive return assumptions.

Illustration irregularities were uncovered after regulators reviewed illustrations

from 13 companies, which prompted regulators to attempt a quick fix.

Regulators found that insurers often displayed multiple historical averages over different time frames, often side by side with the maximum illustrated rate. The historical averages were sometimes two to four times the maximum illustrated rate.

In addition to discouraging side-byside comparisons, regulators aim to standardize the historical period for index components that lack 25 years of

Gen Z says insurance’s slow AI adoption fuels talent crisis

By Rayne Morgan

A new survey finds the insurance industry’s slower adoption of AI is keeping Gen Z from making insurance a top career choice, adding to the industry’s talent crisis.

Counterpart, an agentic insurance platform, and Young Risk Professionals surveyed U.S. insurance professionals aged 21 to 35 and found that most of them highly valued the stability the industry can provide. However, the survey also found a “striking disconnect” between Gen Z’s expectations regarding AI

and the reality on the ground.

“There’s a big gap happening between what we’re seeing in the broader economy versus what’s happening in insurance. These young professionals are smart. They’re recognizing, ‘Wait, hold on, the world is changing around me and we’re sitting still in insurance,’” Tanner Hackett, CEO, Counterpart, told InsuranceNewsNet.

Hackett urged the insurance industry to find solutions on how to cross that chasm, acknowledging that AI is likely going to be broadly entwined into

historical data. Regulators discussed setting the minimum historical period at five years, but some regulators preferred 10.

Rachel Hemphill, chief actuary at the Texas Department of Insurance, is chair of LATF. She supports holding a final exposure for comment on the five- or 10-year issue.

“That would be a decision for LATF to decide, once we had all our exposures and we didn’t feel like other tweaking needed to be made, and that was just really the remaining decision,” she said during Thursday’s call.

Read the full story online:

InsuranceNewsNet Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback.com.

everyday practice for many aspects of the business.

For Gen Z, an AI disconnect

At a time when attracting new talent to insurance is critical, Counterpart’s survey found job stability and career advancement opportunities are the two biggest draws for young professionals.

Sixty-four percent of respondents strongly valued stability and said it was their main reason for going into insurance, while 54% said career advancement was their main reason. Over two-thirds of all respondents said the job benefits and compensation offered by insurance are a major attraction.

However, a clear gap emerged when it came to AI. According to the study, Gen Z does not view AI as a threat or a major risk to be avoided, but as a beneficial tool they both expect to use and want to use.

Read the full story online: https://bit.ly/talentcrisis25

Rayne Morgan is a journalist, copywriter and editor with over 10 years’ combined experience in digital content and print media. You can reach her at rayne.morgan@innfeedback.com.

An interview with Athene’s Mike Downing by Paul Feldman, publisher

Annuity sales are skyrocketing, and Mike Downing is on the front lines of those record-busting sales. Downing is co-president of Athene USA and chief operating officer of Athene Holding. He is responsible for the day-to-day operations and is an advocate for unlocking the demand for annuities by improving the customer experience.

Downing believes the annuity industry is on the brink of transformation as the population ages and younger workers see the need for guaranteed income for their post-employment years.

In this interview with publisher Paul Feldman, Downing describes where he sees the demand for annuities going in the future, as well as the role the technology has in making annuities more accessible to consumers.

PAUL FELDMAN: Tell me how you started in the industry.

MIKE DOWNING: I’ve been in the retirement industry for my whole career — 30-plus years. My technical qualification is that I’m a pension actuary. I started in the retirement industry as a pension consultant, working with large companies that had traditional defined benefit plans for the first 15 years of my career. I saw the apex of that market; I really started to see that market through its slow decline as the nature of a defined benefit promise became less compelling. For employees, there was a lack of portability, and it was hard to understand. Some of the costs and risks became prohibitive for employers. I started to see these plans begin to freeze and even terminate.

I joined the insurance industry during the financial crisis in 2008. I think one of the interesting aspects of my background is that I’ve been in retirement and saw both sides: guaranteed income when it existed and the decline of guaranteed income. The part of the business that I’m excited about today is insurance that is uniquely positioned to restore the lost promise that existed with traditional defined benefit plans and can help consumers and plan participants transition from savings to spending in retirement. Only insurance can solve that equation, because we can provide guaranteed income and no one else can.

It’s almost two stories: the story of the decline of one system and the story that we are in the nascent days of a new system that I think will result in protection as well as portability and flexibility.

FELDMAN: As you talk about the rise of a new system, how can we do a better job of getting people to think about annuities instead of just putting their money in the stock market?

DOWNING: One thing we can do is dispel a lot of the myths around annuities. I’m often asked what is the average age of someone who buys an annuity? That age is typically near or at retirement. But when you look at the products that exist today, as opposed to what existed 30 years ago, annuities are really for everyone.

A big feature of annuities is tax deferral. Tax deferral is a young person’s benefit. Tax deferring starting at age 40 is a lot more effective than starting tax deferral at age 60.

And the array of products is much more diverse today than 30 years ago. Thirty years ago, the choices were simple: a single premium immediate annuity — which is guaranteed income for life — or a simple accumulation annuity. Today we have fixed indexed annuities, which provide market upside. The index can be pegged to an S&P index or, at Athene, we have multiple other indexes you can plug into. This offers a more compelling proposition for a younger customer where you have principal protection but you still have equity-like upside. The newest segment that is emerging is the registered index-linked annuity, which provides even more upside with less downside protection, but still has guardrails. That should attract an even younger customer base.

The big thing we need to do is to continue to simplify the products and educate the customer base around the fact that annuities are really for everyone, and the amount of protection they can provide against your traditional portfolio is substantial. The value proposition is quite strong.

FELDMAN: I completely believe in portfolio diversity. How are you creating diversity with the different indexes you offer?

DOWNING: We’re offering two flavors. One is choice. We allow advisors to kind of pick and choose and advise their clients on a particular type of index. And then there is the other where we try to simplify the sales process by coming up with preblended indexes, where we might take three of our indexes and blend them together to create more stable outcomes. We call that a preselect process, where you preset your strategy and it can take a set-it-and-forget-it mode.

We also have lock-in opportunities, which create more active engagement. The idea is to have an index for every type of economic environment that is less correlated with the S&P for diversification.

FELDMAN: I was told 60% of annuities sold are tied to the S&P index. Is that your experience?

DOWNING: Our experience is quite the opposite. We have the vast majority going into custom indexes. That’s partly because we were an early adopter of custom indexes with the idea of creating diversification for customers and choices for financial advisors to present to their customers. Part of the reason our success is so strong is we’ve been able to build a track record. The challenge with new custom indexes is that they are based on historical theoretical performance, but the real proof is how they perform on an ongoing basis. Some of our oldest indexes have been around for a decade and have great track records. Those track records in combination with Athene as a brand has created a large following for our custom indexes, and they continue to perform.

FELDMAN: Athene has been one of the top annuity sellers over the years. What’s the secret of your success?

DOWNING: Our secret has been focus, execution, having an excess supply of capital to meet the doubling of demand in the industry, and consistently having great relationships with our distribution partners. The combination of the doubling of overall industry growth with a large increase in our distribution footprint gives us the ability to serve our largest distribution partners. We put a lot of focus on our back-office operations,

and we pride ourselves on having a market-leading operation that is able to deliver the largest volumes in the industry.

FELDMAN: How do you see technology and artificial intelligence affecting the annuity industry?

DOWNING: People immediately see AI as having chatbots replace individuals in the call centers instead of having a representative provide the human interface. I would say that’s probably the wrong way to look at applying AI in the insurance space.

The best way to use AI in the insurance sector is to use it in a way to stop the call from coming in the first place.

We’ve been able to rebuild our operations center on the fly while we’ve grown explosively. And today, we have some of the best technology in the market, and we’re in the midst of rebuilding that technology again.

tech, it will accelerate the creation of industry standards, which will allow us to reach more customers.

FELDMAN: How would you describe where you thought you would be in 2015 to where you are now?

DOWNING: I think we all thought our business model was a great model. We felt it was a better mousetrap, although unproven; I would say our success even exceeded our initial optimistic projections.

I think it’s a testament to three things. One is the fact that building around retirement services has proven to be a smart business decision. The retirement market is immense, and there are many different

A lot of calls come in because of confusion. There’s confusion in the process. The customer doesn’t understand, the advisor doesn’t understand, so they pick up the phone and call in. AI can help understand what’s causing the confusion in the first place and then set up your infrastructure and process to avoid that confusion altogether.

It’s like a pizza tracker or an Amazontype experience of, my policy left the building, it’s in good order or it’s not in good order. If it’s not in good order, what information is needed? All of that communication can be done through better investment in technology to anticipate the types of questions customers and advisors have and get ahead of those questions.

We know what drives the questions, so we can start to build the technology and insights to prevent those questions in the first place. If all companies invest more in

ways to participate in it. You can scale up a business in an efficient way by centering it around retirement and all the spreadbased opportunities in that market.

The second is the large influx of capital that Apollo has been able to bring in. An insurance company can grow only as much as its earnings support without having capital infused from the outside.

And third is investment insurance, high-grade insurance, quality assets that are nearly all investment-grade but also looking at a more diverse asset pool to back our liabilities. This has created a modest amount of excess yield, but we’re able to pass that on to the customer.

The combination of structure, our ability to compete and this availability of capital has allowed us to grow and take advantage of the doubling of the market that happened when rates reverted to more historical norms.

FELDMAN: Private equity has changed the annuity landscape. How has it helped Athene?

DOWNING: I believe the notion of private equity is a misnomer. Our structure of an insurance company married with an asset management company is a standard structure that has been in effect for decades. MetLife has a similar structure. Prudential has a similar structure. The other aspect of Apollo’s investment skills that sit in Athene’s general account is the investment in private credit, which is just taking advantage of an asset class that has a little less liquidity and still has the same credit superiority. We’ve proven through our track record that there’s such a thing as good private credit, just as there are good corporate bonds and bad corporate bonds and potentially bad private credit, but it’s all about putting the right assets inside an insurance balance sheet.

The complete integration of Apollo and Athene as a single organized company creates a lot of synergies in terms of being able to create a management team that is entirely centered around Athene’s general account. Athene is still highly regulated; it’s still an insurance company like any other company. It has been a huge positive, and I think it’s going to be a huge positive for the industry.

FELDMAN: What does it take in the back office for a carrier to scale the way Athene has?

DOWNING: We don’t outsource any of our back office. It’s all done right here in Des Moines, and it’s centrally located, which helps in terms of investing in technology and moving the company forward. We’ve been able to rebuild our operations center on the fly while we’ve grown explosively. And today, we have some of the best technology in the market, and we’re in the midst of rebuilding that technology again.

FELDMAN: What are you looking at rebuilding?

DOWNING: We believe that every three or four years, technology changes enough to consider incorporating some

of that new technology into our infrastructure. As a recent example, there has been an industry effort to address the challenges of customers who have an insurance product with one company and want to buy an insurance product with another company, the process being a 1035 exchange. The process historically took almost 20 business days. That’s almost a calendar month in which a customer wants to exchange one policy for another and they’re stuck in limbo while the advisor is frustrated with the process.

The technology that we’ve built and invested in has allowed for paperless exchanges, something that has been eluding the industry for about three decades. Now we can shorten that process to 24 hours. That totally transforms the experience.

FELDMAN: What must the industry do to obtain more business?

DOWNING: I believe a lot of things must happen. When you look at simple, lazy money — certificates of deposit and money market accounts that are just sitting around — I think that’s an aggregate that’s close to $10 trillion. What if 20% of that were converted to simple annuities? That’s a $2 trillion opportunity.

Another opportunity is individual retirement accounts. That market is close to $20.5 trillion when you combine IRAtype savings with nonqualified savings. If you treat insurance like part of your investment portfolio, and you can get about half of that money into various types of annuities, you can increase a retirement paycheck by almost 50% because you can raise your withdrawal rate and never run out of paychecks.

We need to do a better job of messaging as well as making the experience simple for the customer.

FELDMAN: How do we get more young people to consider annuities?

DOWNING: One step is to start with some of the simple money. Ask a 40-yearold what money they have sitting in a CD today that they’re just going to continue to park, and have them put that in a multiyear guaranteed annuity and see the extra dollars they get in savings.

The second is to focus on some of the products, such as registered indexlinked annuities, which have more significant upside. A younger saver will have the comfort to say, “I’m not giving up much in the way of upside because of the structure of these products, but I’m actually getting better tax deferral that I can’t otherwise get,” which is a huge selling point. And if things really go wrong, they’re protected.

When you look at the alternatives to volatile equity markets and uncertain rate environments, it’s compelling.

FELDMAN: Where do you think the biggest opportunity is for annuities with advisors?

DOWNING: Focusing on the money that’s sitting outside the sector. Unlocking the market that’s sitting in CDs and money markets and money that’s already in defined contribution plans and converting that into annuities.

I think advisors have the best message and can simplify the pitch in ways consumers can understand.

Over time, as more consumers adopt annuities at younger ages and start to see the benefits, it will transform the industry and protect people the way they need to be protected today.

FELDMAN: There are so many benefits, such as riders, in annuities. What are some of the best and some of the new things coming out?

DOWNING: The one that I think really resonates the most with consumers is fixed indexed annuities that have income riders attached to them because they provide two things consumers want. One is the option of having income if they want, and when they want it. The consumer can choose when they want to take income. They can take it right away. They can take it in year five or in year 10 but the flexibility is there.

Another option is simple accumulation products. The advantage of these is there is not a rider. They typically offer a little bit more upside in terms of accumulation. Imagine a scenario where a consumer buys a RILA at age 40 or 45. It has more upside and a little less downside protection, but it looks and feels like you’re in

the market. And when you’re in that for five or 10 years, the whole time you’re getting tax deferral. Then maybe at age 55, to preserve all that upside, you move it into a traditional FIA that has 100% principal protection and still have equity upside, and then perhaps five or 10 years later, you then roll that same one into an FIA with a guaranteed income rider.

And that’s the cycle that I think advisors can plan with their customers in terms of reaching a younger customer base. It’s showing the progression of products and how you can preserve massive amounts of upside, and then over time, slowly provide the downside protection.

FELDMAN: Where do you see RILA sales versus FIA sales going into the future, from an Athene perspective and also as an industry perspective?

DOWNING: A large part of the explosive RILA growth has been a movement away from variable annuities. The RILA tends to provide much better outcomes and more value overall because of the way they’re structured. I see that segment continue to grow alongside FIAs because they serve different risk/return profiles. RILA offers more upside with less downside protection, whereas the FIA offers reasonable upside, but you’re giving up some extra upside for more downside protection. And I think the two live side by side, and it’s going to be a combination, and they’ll both continue to grow.

FELDMAN: What do you think about offering annuities within defined contribution retirement plans?

DOWNING: I believe bringing guaranteed income directly into the defined contribution landscape or the 401(k) landscape can do wonders to close the retirement gap in simple ways.

I think the next big chapter in defined contribution is integrating annuities inside 401(k) plans. This will solve a lot of portability issues while still being able to provide lifetime guarantees and do it in a way that’s easy for consumers to understand. I think that’s the next big frontier, and we’re starting to see the initial forays into that space, but there’s a lot more to come and a lot of opportunity.

HOW AI IS

RESHAPING

THE INSURANCE INDUSTRY

If insurers can get out of their own way, a reactive industry can transform into a proactive partner.

BY RAYNE MORGAN

Wide-scale adoption of artificial intelligence is transforming the modern insurance industry from a primarily reactive business to a proactive risk-management and life partner that clients can rely on for personalized, empowering advice and services. At least, this is what Joe Khoury, managing director and partner, Boston Consulting Group’s Insurance Practice, believes.

diabetic policyholder could receive AIdriven lifestyle coaching bundled with their coverage.

“AI is shifting insurance from being primarily a reactive risk-transfer business toward becoming a proactive risk-prevention partner. Insurers are no longer just paying claims; they are increasingly using AI-driven insights to anticipate risks, offer mitigation services and personalize products in real time,” Khoury said. He suggested that in the next five to 10 years, insurers will begin to function more like risk managers and life partners than product providers as AI enables real-time, contextual interventions. For example, a homeowner could receive a personalized alert from their insurer advising them to turn off a valve before a pipe bursts, or a

This prediction comes into sharper focus every day, as some carriers are already leveraging technology for vehicle telematics that not only provides an insurer with information but also actively coaches drivers toward safer behavior. And others, such as John Hancock’s Vitality program, encourage policyholders to live a healthy lifestyle through special benefits and rewards.

In this way, “risk prevention as a service” could become a significant new revenue stream for innovative carriers ready to embrace an AI-powered future.

“Over time, AI could blur the line between insurer, health care provider and consumer tech company. Whoever controls the customer interface and data ecosystem will define the value chain,” Khoury said.

At the same time, AI can potentially level the playing field between some of the largest firms and mid-tier insurers, effectively “democratizing advanced capabilities for regional players” as it gives them access to powerful analytics once reserved for major corporations.

However, today’s insurance industry

has many hurdles to overcome before it can fully realize the many possibilities offered by AI.

What hurdles do insurers face with AI?

AI leaders and experts such as Khoury believe insurers face five major challenges when it comes to fully embracing AI:

1. Adoption and scale

2. Talent

3. Regulation, ethics and trust

4. Data ecosystems

5. Internal reluctance

Pilot purgatory

Khoury noted that although many insurers are keenly interested in AI, “many insurers are stuck in ‘pilot purgatory’” — they started enthusiastically with pilot projects but never managed to successfully scale those efforts.

In fact, the 2024 BCG Build for the Future Global Study and Digital Acceleration Index scored insurance at a high 42 AI maturity. This indicates a strong interest in AI adoption, and the only industry with a higher score was tech, media and telecom at 46. BCG noted this score marks “active experimentation.”

Khoury

That same report found that only 7% of insurance companies managed to scale after that pilot stage, however. It noted that while the pilot phase starts strong, insurers soon “scale back,” as “even when successful on their own terms, these projects raise concerns about the impact they will have on the rest of the company and existing ways of doing business.”

Khoury emphasized that scaling from dozens of pilots to enterprisewide deployment is critical for insurers to realize the full value potential of AI.

AI translators

The insurance industry also needs what Khoury referred to as “translators — professionals who understand both insurance operations and AI capabilities.”

But that is a unique challenge for the industry, as tech-savvy professionals are often more drawn to high-tech careers. A 2025 study conducted by agentic AI platform Counterpart and the Young Risk Professionals organization underscored this issue. It found the insurance industry’s slow adoption of AI is keeping young professionals from seeing insurance as a top career choice.

transparency that builds trust with clients. Khoury said these issues should not be afterthoughts but must be table stakes.

A “bold improvement” would be “industrywide collaboration to establish shared ethical standards and data trusts” that enable competition based on customer experience, he suggested.

At the same time, he said insurers should not wait for “perfect clarity” from regulators, who tend to move more slowly than technology. Instead, he urged them to engage regulators early and “help shape the guardrails rather than waiting passively.”

“The key is governance by design. Leading insurers embed explainability, fairness checks and auditability into AI models from Day 1,” Khoury said.

Much of the same has been expressed by other experts, who urge insurers not to “hold their breath” on outside regulation but to establish their own internal frameworks. Data and AI solutions firm SAS has even developed a free tool to help companies with this.

before being able to scale AI solutions. “There are many foundational problems that the insurance companies have, which limits their ability to accelerate. One is the multiplicity of admin systems, and second is their data landscape is still very siloed. Unstructured data has not been managed properly, so using some of that data for AI is still a few months or maybe a year away,” Taneja said.

Risky reluctance

While AI adoption is steamrolling ahead in insurance, some reluctance remains. This sentiment is another reason, Khoury believes, why many companies have not managed to scale past pilot programs.

He noted that resistance at both the organizational and individual levels, unclear roles and responsibilities, limited business engagement and inconsistent support all contribute to an AI strategy “stalling.” And this is a major risk in an age when many competitors are pulling ahead with advancements.

“If you look at the results from our YRP survey, around 70% of Generation Z workers believe that AI will improve their workflows, but only less than 10% are strongly encouraged to use it. So there’s a big gap happening between what we’re seeing in the broader economy versus what’s happening in insurance,” Tanner Hackett, Counterpart CEO, noted.

Experts on a panel hosted by insurance software solutions company Send suggested the insurance industry must figure out how to change the perception that it is a “boring,” antiquated industry and effectively “bring sexy back” if it hopes to attract young professionals with AI skills. They acknowledged that the rapid advance of AI is expected to change job roles and create new skills, urging insurers not to ignore the fact that younger professionals want to and expect to use technology in their daily tasks.

Ethical standards

Some of the biggest risks with adopting AI center around regulation, ethics and

“We believe that it’s table stakes to do AI responsibly, and that it’s essential for us, as a society, to make sure we get this right,” Kristi Boyd, senior trustworthy AI specialist with SAS’s Data Ethics Practice, said.

Rich, structured data

On a more technical level, Khoury noted that insurers must expand partnerships to access richer, alternative data sources — and he’s not the first to note this shortcoming.

In an earlier interview, Sumit Taneja, EXL’s senior vice president and global head of AI consulting and implementation, said that the insurance data landscape is “still very siloed,” noting in one case that an insurer had up to 28 different legacy systems, all with different, unstructured data.

Taneja likewise asserted that this foundational data challenge is limiting insurers’ ability to scale faster. Further, he believes this may take years for some companies to address because they would have to invest in data warehouses and platform modernization

“Laggards will face margin compression. If a top-tier player uses AI to process claims in minutes instead of weeks, customers will demand that as the industry standard. Those who can’t deliver will see churn rise sharply,” Khoury said.

Considering that BCG’s 2024 Build for the Future Global Study found 27% of insurance companies had not begun taking any action on AI at all, reluctance to embrace technology could prove a critical weakness.

It also highlights a clear differentiation in the approach taken by globally recognized companies such as Manulife, which operates primarily as John Hancock in the U.S.

For comparison,

Jodie Wallis, the global chief AI officer spearheading Manulife’s award-winning AI rollout, recently revealed that the company’s vision is to incorporate the technology throughout its entire business model.

“Prior to large language models coming on the stage, we would have said AI is suitable for parts of our business and less suitable for other parts. Now, our perspective is it’s really suitable for all parts of our business,” Wallis said. (You can read more about Manulife’s AI revolution on page 42.)

Hackett

Taneja

Boyd

Wallis

What are the key areas for AI transformation?

If these challenges can be managed, Khoury noted that AI will continue to transform four key areas in insurance:

• Client interactions

• Distribution and lead generation

• Underwriting

• Claims

Client interactions

Artificial intelligence technologies such as large language models and natural language processing have changed the way clients engage with businesses. AI chatbots and virtual assistants are now capable of resolving routine queries instantly, providing faster service and granting advisors more time to deal with complex tasks.

Chatbots, in particular, are a major AI advancement and are being used for customer service, sales, claims processing and underwriting functions. The chatbot market has experienced such enormous growth in the last few years that Allied Market Research predicts it will hit nearly $5 billion by 2032.

Additionally, Cognizant’s AI Inclination Index 2025 shows insurance customers are increasingly comfortable with using AI for research, learning more about certain products before speaking with a professional to make the actual purchase. While this varies based on type of insurance, such as life and annuities or property/casualty, and client age, the overall trend indicates consumers are slowly becoming more willing to engage with AI tools.

Craig Weber, head of insurance strategy at Cognizant, said this represents an opportunity for insurers to make huge gains with their AI adoption and innovation strategy, perhaps even looking to agentic AI as a solution.

“There are small subsets of buyers and users of insurance who are willing to entertain the use of AI. So, my best advice to an insurer is to build the skills around AI and plant the flag because this trend is only strengthening over time,” Weber said.

Distribution and lead generation

Many believe the customization capabilities offered by AI will be a huge

differentiator that drives leads, sales and competition from here on out. One such individual is Joe Crawford , director of professional services at Glassbox, a digital experience intelligence platform.

Glassbox has leveraged AI to fight both traditional forms of insurance fraud and the new methods that are emerging in a digitally advanced age. He believes that using AI tools to deliver customization is “pretty much a must these days.”

“We’re in a situation today where people are looking for personalized experiences. They are looking for instant experiences. They’re looking for intuitive experiences, frictionless experiences with their digital platforms,” Crawford said.

To this end, BCG underscored how AI-assisted agents can “efficiently process large volumes of unqualified leads, directing customers to the most suitable sales journey,” whether that’s fully digital, phone assisted or in person.

“AI-driven analytics help brokers identify micro-segments and design hyper-personalized outreach,” Khoury said.

Underwriting

One of the most important aspects of insurance being transformed by AI is underwriting. In recent times, dozens of new patented underwriting technologies have emerged to speed up the process and even provide instant decisions.

“Models can process nontraditional data such as IoT sensors or satellite images to sharpen risk selection,” Khoury noted.

Munich Re’s alitheia platform is just one example of the many AI-powered underwriting tools that have emerged in recent times, using machine learning and

a patented natural language processing tool to accurately determine risk.

Insurance Software Automation’s Best Plan Pro is another tool assisting with prequalification from the moment a customer calls in to get a quote — before the application process even begins.

But experts have pointed out that technology has also enabled underwriters to assess new factors they previously may not have had access to, making risk analysis more robust.

For example, Darcy Rittinger, chief risk officer at global insurtech provider Cover Genius, said insurance carriers are looking at traditional underwriting parameters such as age and health in smarter ways thanks to alternative data sources.

“By accessing this enhanced data and utilizing AI, insurtechs can create more tailored products and better risk models and streamline the underwriting processes,” she said.

Claims

Claims processing, being one of the biggest aspects of the insurance business, is likewise a major aspect of insurance that has been permanently transformed by AI for staff and clients alike.

“Historically, claims have been the most painful customer moment,” Khoury said. “With AI-powered image recognition and straight-through processing, settlements can now occur within hours. This redefines customer trust.”

As an example, he noted how generative AI tools can draft settlement communications and analyze images of car damage with “near-human accuracy.”

Now, specialized AI-powered tools are being developed for claims in specific areas

“My best advice to an insurer is to build the skills around AI and plant the flag because this trend is only strengthening over time.”

Weber

Rittinger

Crawford

Fixed income investments make up of our invested assets.

Commitment to customers

“We’re seeing much more use of AI, much more heavy use of data-driven insights as part of the sales, the selling model and sales enablement process by brokers.”

or at specific points of the journey — such as for health insurance, P/C and more.

One recent example is Qumis, an attorney-trained AI platform designed to support insurance professionals with complex policies and documents. While it helps with analyzing claims, the platform is versatile and can also be used for insurance marketing documents and content, for example.

free up 15% to 20% of costs but maintained that “true transformation comes from new streams — personalized wellness add-ons, pay-as-you-live coverage and real-time risk advisory.”

Qumis founder Dan Schuleman emphasized how this level of technology is especially necessary as social inflation drives claims costs higher and never-before-seen forms of coverage are emerging, such as cyber insurance.

“The claimants are only going to get more sophisticated, the claim types are only going to get more complex, and so the carriers are going to need tools that radically help with that in order to combat the very unsustainable trends happening,” Schuleman said.

Efficiency gains are just step one

Perhaps the biggest shift brought about by AI is the speed of decision-making in insurance. Khoury noted, for instance, that what once took weeks — such as underwriting a complex risk — can increasingly be done in hours or even in minutes.

However, he noted that stopping at efficiency gains would be a mistake. While those are a crucial part of the equation, he said insurers should also think about how AI can aid growth and provide a pathway to new revenue streams.

“If insurers stop at efficiency, they will simply be leaner versions of today’s business. Growth requires the courage to rethink products, not just processes,” Khoury said.

He estimated that efficiency gains may

AI can drive growth not just through traditional sales but also through merger and acquisition activity, according to David Crofts, insurance M&A lead, West Monroe Partners, who noted a trend of larger insurance brokers shedding underperforming assets in favor of diversifying their product landscape, finding cross-sell opportunities and pursuing strong adjacencies.

“For a broker to be successful in the wholesale and managing general agency space, it’s becoming more and more table stakes to have a very strong data and analytics competency,” Crofts said. “We’re seeing much more use of AI, much more heavy use of data-driven insights as part of the sales, the selling model and sales enablement process by brokers.”

Khoury noted that if insurers can succeed with maximizing growth opportunities through AI and technology, they may “substantially reduce claims volume, shrinking the traditional premium pool while opening new service-based business lines.”

“There is growing discussion in the market about how AI will generate revenue streams beyond traditional risk-based offerings,” Khoury said.

Rayne Morgan is a journalist, copywriter and editor with over 10 years’ combined experience in digital content and print media. You can reach her at rayne.morgan@ innfeedback.com.

With AI and advanced technology reshaping the industry, advisors can enhance efficiency, improve client insights, and stay ahead in a competitive market. Read up on the latest tools and technology for smarter, faster growth.

INSIDE

The Why of AI by Sean Van Moorleghem, Chief Technology Officer, Cambridge Investment Research, Inc.

PAGE 17

Carrying the Torch: Karen Essary Leads Ideal Producers Group into a Bold New Era by Ideal Producers Group

Schuleman

Crofts

Karen emphasizes, “It’s not about selling; it’s about showing agents what’s possible and giving them the resources to make it happen.”

The Why of AI How to unlock this technology’s potential for your company

Cultivating Relationships That Last

“We don’t steer agents toward solutions because of bonuses,” Karen says. “We give them what’s best. That trust forms the foundation of long-term relationships and is why agents grow with us year after year.”

By Sean Van Moorleghem, Chief Technology Officer, Cambridge Investment Research, Inc.

One of IPG’s signature strengths is relationship cultivation. Karen believes agents thrive when part of a network that values long-term connection over short-term gain.

Independence allows IPG to customize solutions, refine processes, and provide tools that genuinely work while maintaining a personal touch.

“Too many agents experience the ‘one and done’ approach,” she says. “Take the time to know your clients, follow up, and make an impact. They’ll remember, refer others, and even if you don’t close a sale today, you may make a difference years later.”

If there was ever a case for embarking on a project with a clearly defined end in mind, it is building out your firm’s artificial intelligence (AI) capabilities within the framework of your current tech stack. Given the breadth of its applications, AI often is deployed as a tactical measure … to gather, analyze, automate, and execute better, faster, and more accurately. However, its real power lies in its indirect impact on your firm’s other operational elements. It has the ability to impact every aspect of your business – if you’ve designed its application with that end goal in mind.

Visionary Leadership, Bold New Era

expand their ability to deliver personalized support to our financial professionals, elevate their skill sets, and enjoy a more fulfilling and collaborative work environment.

Stepping into leadership after Ron’s loss was not easy. Today, Karen is one of the few female CEOs in the IMO space, a distinction she doesn’t take lightly.

Ensure everyone is on board

“At Ideal, you’ll never be just another number. Whether you bring in $10,000 or $20 million, you get the same attention and care. You’ll never find another IMO that will love and care for you more than we do.”

This philosophy extends internally. IPG honors top-performing agents quarterly, celebrates milestones at conventions, and recognizes first-time achievers. “At Ideal, you’ll never be just another number,” Karen says.

“Whether you bring in $10,000 or $20 million, you get the same attention and care. You’ll never find another IMO that will love and care for you more than we do.”

Elevating Advisors at Every Stage

Know your goal going in AI not only has the ability to simplify or even eliminate labor-intensive and often mundane tasks, it can offer impressive cost savings. It can create scale and deliver unprecedented speed of execution. Workflows can also be streamlined, risk management can be enhanced, and personalization can be further expanded. Separately, these are fine outcomes. Together, they can drive unmatched synergies. Companies that have enjoyed success in utilizing AI understand that iterative advancements in AI happen when they are part of an integrated, long-range strategy and not merely a series of siloed wins.

At the core of IPG’s philosophy is a simple but powerful belief: every advisor deserves the chance to succeed. Whether new or seasoned, IPG offers personal support, world-class resources, and genuine partnership.

“This industry has been shaped by incredible men and women, but it’s no secret that female leadership is rare,” Karen says. “I see that as both a challenge and an opportunity. My goal is to bring fresh perspective while staying true to the values that built IPG. If my leadership inspires others, especially women, to step forward with confidence, that’s something Ron would be proud of.”

Her style is grounded in empathy, collaboration, and vision, qualities that resonate with the IPG team and advisors. It’s no surprise IPG continues to thrive during this transition.

Ultimately, firm leadership is tasked with developing, executing, and promoting a viable AI strategy that is clear, flexible, and tangible. At Cambridge, transparency is central to our value proposition, and we take great efforts to ensure our associates are part of our AI journey. They are primary stakeholders of our strategy and have both insight into our plans and input into our entire process from start to finish. Working toward our common goal, which for us was freeing up our associates to focus on more meaningful, relationship-building work and creating higher value engagement, was at the forefront during every step of the process.

The Ideal Future

The future of AI is intentional

Under Karen’s leadership, IPG is investing in technology, expanding its marketing resources, and forging stronger partnerships with carriers, all while maintaining the personal, relationship-driven culture that has defined IPG from the start.

Karen is especially passionate about that culture of inclusivity and growth.

“Ron never believed in putting advisors into boxes or ranking them in ways that left some behind. He wanted everyone to feel valued,” Karen says. “That spirit is alive here. Every advisor has access to tools, training, and strategies to grow, and we celebrate their success.”

This culture translates into advanced case design, marketing programs, lead-generation strategies, and access to exclusive solutions—combined with a genuine sense of partnership.

For example, at Cambridge, we recently built upon our existing success with generative AI to introduce the wealth management industry’s first fully agentic AI-powered account opening tool. Agentic AI tools are designed to act and make decisions with limited (or no) human input. Our internal testing established that our new “digital associates” deliver in minutes what previously took a small team over multiple days to accomplish – without compromising accuracy or precision. And, in just a few hours, the tool has the capacity to match a year’s worth of account-opening productivity. These results do not exist in a vacuum; they have positive repercussions across our entire organization.

“We don’t just hand someone a contract and disappear,” Karen says. “We’re in this with them every step of the way. That’s what makes us different.”

Independence as a Competitive Edge

Independence is a core tenet. Unlike many firms constrained by corporate incentives, IPG operates freely, giving agents the right product for every client.

Importantly, it’s essential that your employees understand the firm’s goals. When your team realizes that integrating AI is designed to support rather than replace them, their initial fear will turn into enthusiasm and embracement of a tool capable of enhancing their roles and freeing up time to focus on more valuable aspects of their day-to-day. At Cambridge, we’re investing in agentic AI to help our team

“Ron used to say, ‘If you take care of people, the business will take care of itself.’ That’s still our guiding principle,” Karen affirms. “We’re growing, innovating, and keeping people first — advisors, clients, and our team. That’s what makes Ideal Producers Group truly Ideal.”

Carrying the Torch

On the surface, the rapid pace of AI innovation is a great advantage for firms. However, it’s potentially an expensive endeavor to remain current both in terms of infrastructure, integration, and expertise. Persistent challenges, including data integrity and cybersecurity, make predictions about its future applications and capabilities haphazard. There are opportunities to be captured and hurdles to overcome. The winners in the space will be firms that leverage core elements of traditional strategic planning and execution to navigate the choppy AI waters. Transparency, ongoing oversight, and adaptability are foundational. Most importantly, maintaining a clear line of sight to your ultimate goal, and understanding how AI can help you achieve it, should guide all your tactical tech stack upgrades.

With the foundation of Ron Essary’s legacy, and now under Karen Essary’s leadership, Ideal Producers Group stands as a beacon of independence, partnership, and opportunity for financial professionals nationwide.

For Karen, the mission is clear: “Ron laid the foundation. Now it’s my honor to build the future.”

To find out more, go to idealpg.com.

Carrying the Torch: Karen Essary Leads Ideal Producers Group into a Bold New Era

The insurance industry has always been shaped by visionaries. Few names carried as much weight as Ron Essary, a pioneer who forever changed the way marketing organizations partnered with financial professionals. His passing left a void, but also a legacy — one that continues to inspire Ideal Producers Group (IPG). Today, that legacy is not only preserved but propelled forward under the leadership of Karen Essary, co-founder and CEO

Karen’s journey spans decades, starting humbly as one of the first employees at Creative Marketing. She worked her way through every corner of the business; answering phones, supporting recruiters, building service models, even creating “Keep in Touch” programs still in use today. That foundation gave her rare, hands-on insight into how to build something that lasts.

“I started at the ground level,” Karen recalls. “Every step taught me what matters most — relationships. You don’t build a great business by treating people like numbers. You build it by caring, listening, and growing alongside your agents.”

That philosophy became the cornerstone of IPG, which she and Ron launched over 16 years ago. What began as a boutique firm has grown into a powerhouse offering innovative programs, advanced lead-generation strategies, and a culture that consistently puts agents first.

Honoring a Legend, Building the Future

Ron Essary was a legend in every sense. From introducing actuarial expertise into marketing organizations to shaping and designing products that drove well over $60 billion in sales, his influence remains evident throughout the in-

dustry. Yet, Karen notes, Ron’s greatest strength was not just his innovation. It was his humility.

“Ron never needed credit,” she says. “His dream was always that IPG would outlast us, serving agents and building something bigger than ourselves.”

That dream is alive and thriving. Karen has seamlessly stepped into the CEO role, guiding with the same relentless commitment to service, as well as a bold vision for what’s next.

Agents First: The Ideal Difference

For many financial professionals, finding an IMO that truly prioritizes their growth can feel like navigating a maze. Karen and her team have built a different model, one centered on partnership, not transactions.

“We don’t just take cases,” Karen explains. “We work with our agents — every client, every opportunity, every question. Our goal is to give them the tools, support, and guidance they need to succeed.”

This philosophy translates into tangible advantages:

• Hands-on support: IPG collaborates with agents from the first client conversation to post-sale follow-ups. Agents receive guidance on product selection, case structuring, and client education, making them more effective and confident.

• Innovation with intention: IPG focuses on practical, impactful tools, including CRM systems, lead-generation programs, college funding, and social media toolkits. Every solution helps agents grow smarter and faster.

• Boutique services and top compensation for every agent: Whether you’re a new agent selling annuities for the first time or a high producer, you can count on IPG to help grow your practice.

Karen Essary

Ron Essary

Karen emphasizes, “It’s not about selling; it’s about showing agents what’s possible and giving them the resources to make it happen.”

Cultivating Relationships That Last

One of IPG’s signature strengths is relationship cultivation. Karen believes agents thrive when part of a network that values long-term connection over short-term gain.

“Too many agents experience the ‘one and done’ approach,” she says. “Take the time to know your clients, follow up, and make an impact. They’ll remember, refer others, and even if you don’t close a sale today, you may make a difference years later.”

“We don’t steer agents toward solutions because of bonuses,” Karen says. “We give them what’s best. That trust forms the foundation of long-term relationships and is why agents grow with us year after year.”

Independence allows IPG to customize solutions, refine processes, and provide tools that genuinely work while maintaining a personal touch.

Visionary Leadership, Bold New Era

Stepping into leadership after Ron’s loss was not easy. Today, Karen is one of the few female CEOs in the IMO space, a distinction she doesn’t take lightly.

“At Ideal, you’ll never be just another number. Whether you bring in $10,000 or $20 million, you get the same attention and care. You’ll never find another IMO that will love and care for you more than we do.”

This philosophy extends internally. IPG honors top-performing agents quarterly, celebrates milestones at conventions, and recognizes first-time achievers. “At Ideal, you’ll never be just another number,” Karen says.

“Whether you bring in $10,000 or $20 million, you get the same attention and care. You’ll never find another IMO that will love and care for you more than we do.”

Elevating Advisors at Every Stage

At the core of IPG’s philosophy is a simple but powerful belief: every advisor deserves the chance to succeed. Whether new or seasoned, IPG offers personal support, world-class resources, and genuine partnership.

Karen is especially passionate about that culture of inclusivity and growth.

“Ron never believed in putting advisors into boxes or ranking them in ways that left some behind. He wanted everyone to feel valued,” Karen says. “That spirit is alive here. Every advisor has access to tools, training, and strategies to grow, and we celebrate their success.”

This culture translates into advanced case design, marketing programs, lead-generation strategies, and access to exclusive solutions—combined with a genuine sense of partnership.

“We don’t just hand someone a contract and disappear,” Karen says. “We’re in this with them every step of the way. That’s what makes us different.”

Independence as a Competitive Edge

Independence is a core tenet. Unlike many firms constrained by corporate incentives, IPG operates freely, giving agents the right product for every client.

“This industry has been shaped by incredible men and women, but it’s no secret that female leadership is rare,” Karen says. “I see that as both a challenge and an opportunity. My goal is to bring fresh perspective while staying true to the values that built IPG. If my leadership inspires others, especially women, to step forward with confidence, that’s something Ron would be proud of.”

Her style is grounded in empathy, collaboration, and vision, qualities that resonate with the IPG team and advisors. It’s no surprise IPG continues to thrive during this transition.

The Ideal Future

Under Karen’s leadership, IPG is investing in technology, expanding its marketing resources, and forging stronger partnerships with carriers, all while maintaining the personal, relationship-driven culture that has defined IPG from the start.

“Ron used to say, ‘If you take care of people, the business will take care of itself.’ That’s still our guiding principle,” Karen affirms. “We’re growing, innovating, and keeping people first — advisors, clients, and our team. That’s what makes Ideal Producers Group truly Ideal.”

Carrying the Torch

With the foundation of Ron Essary’s legacy, and now under Karen Essary’s leadership, Ideal Producers Group stands as a beacon of independence, partnership, and opportunity for financial professionals nationwide.

For Karen, the mission is clear: “Ron laid the foundation. Now it’s my honor to build the future.”

Saving money & relationships

with Clare Dubé of the Financial Social Work Collaborative

CLARE DUBÉ coaches people in resolving their financial conflicts while teaching financial self-care to those in the helping professions.

By Susan Rupe

Seek clarity. Take action. Do better to be better.

Those are the words Clare Dubé lives by as she gets people to discuss a topic that many still consider taboo — and that topic is money.

Dubé is cofounder and chief financial officer of the Financial Social Work Collaborative, which was established in January 2024. At the collaborative, she focuses on teaching financial self-care to social workers, caregivers and other helping professionals. She facilitates conversations around money thoughts, beliefs and emotions. She also founded Clare Dubé Financial Therapy in 2004, working with those in money conflicts who desire to improve their communications and money behaviors and to strengthen their personal relationships around money.

She works with clients to improve their financial well-being by coaching them through many of the financial problems that plague couples, families, business partners and others.

She currently makes her home in Myrtle Beach, S.C., and divides her time between there and her native Connecticut.

Dubé said she was “terrible with money” when she was young, but that changed when she began working with clients in her family’s custom home building business. She had her first taste of financial conflict when she worked with clients over change orders in their future homes and the added expenses those changes brought to the cost of construction.

“I saw and heard a lot of battles over money, and at first I was taken aback by them,” she said. “But then I became fascinated by it.”

She earned a degree in finance from Nichols College and then went on to obtain additional education in social sciences at Albert Magnus College.

“When I went to school for social sciences, I got more of the human side of the money aspect,” she said. “That’s how I fell into financial social work. I never thought this would be a career path. It just came about by my being curious about it.”

Currently, she is focusing much of her work on the Financial Social Work Collaborative, where she trains people who are certified in financial social work.

“I’m helping to build new financial social workers, to help them build their practices, help them work with their clients and help them with their own money aspects as well, so that they can then be better working with their clients,” she explained.

Social workers on the front lines

Reeta Wolfson founded the financial social work discipline. Wolfson raised awareness of “femonomics,” how the “gender of money” impacts women, men, children and families.

Dubé said femonomics evolved into financial social work, and social workers became the first group of clients for this advice.

“Social workers are on the front lines of people needing help,” she said. “Social workers often struggle with money, yet it’s kind of taboo for them to talk about money. But money is the thing that touches everything social workers work with. Wolfson had this brilliant insight into money. It was about discussing the human side of money. It goes beyond spreadsheets and budgets. It’s about the emotional and financial trauma behind money.”

Money is symbolic of an individual’s belief system, Dubé said, which makes “personal finance” personal.

In coaching social workers, Dubé said, she found that many of them were told during their education that “they’re in it for the outcome, not the income.” But that message is outdated.

“Social work encompasses so many skills,” she said. “Those skill sets are so broad and in so much demand that they don’t need to have that old belief. You can do good in a lot of ways and still make money. I mean, you should not be ashamed to take a paycheck.”

Couples + conflict = ‘a fascinating dynamic’

Dubé described her work with couples and money conflict as “a fascinating dynamic.” Money was what prompted couples to come to her for help, but there frequently was more than money at play in the conflict.

“It was really about the money messages they received or interpreted growing up and the culture that they brought into the relationship,” she said.