As President Donald Trump moves closer to the midpoint of his second term, the full impact of his agenda is being felt. What does it mean for advisors?

PAGE 16

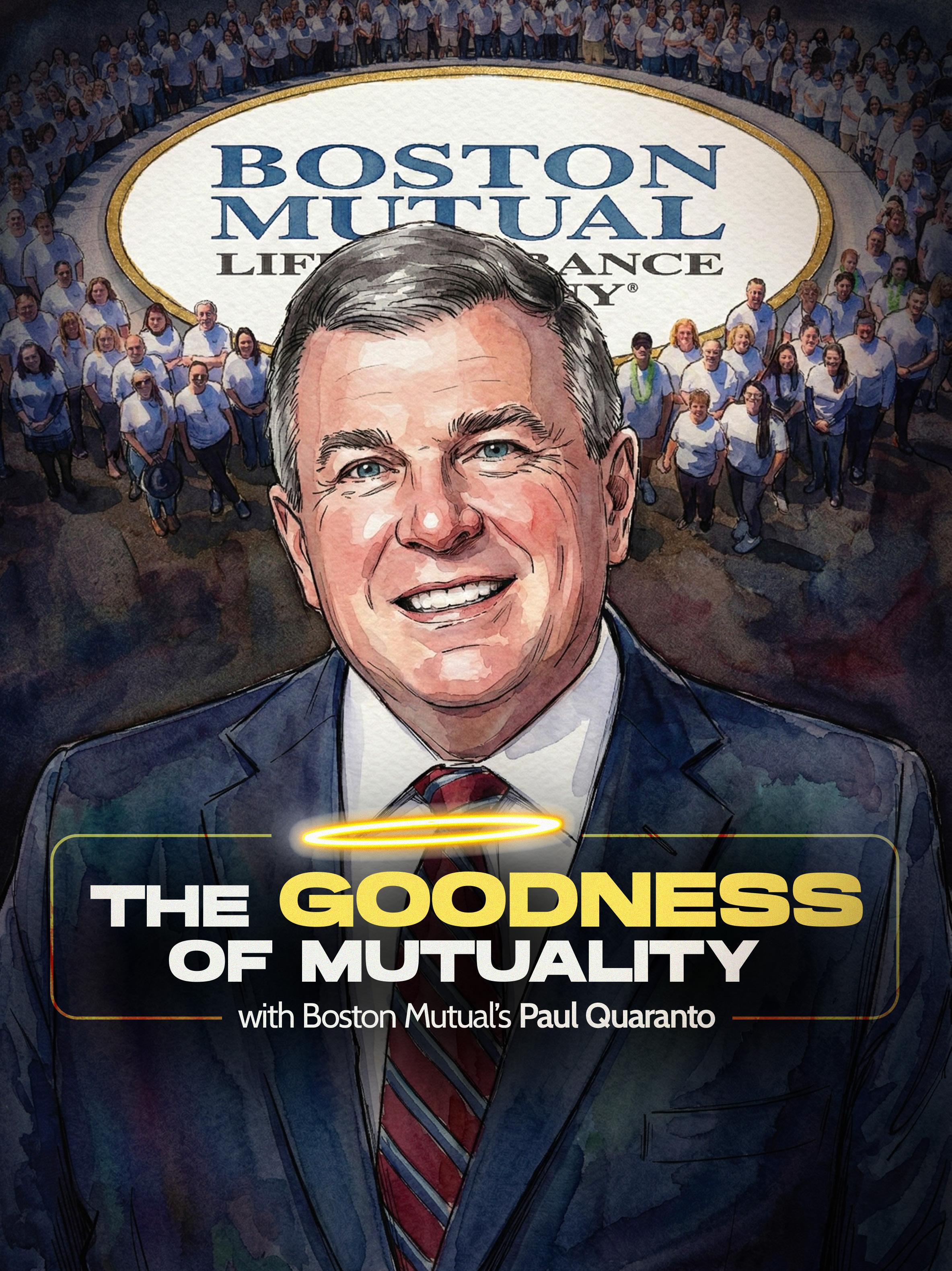

The goodness of mutuality — With Boston Mutual’s Paul Quaranto

PAGE 10

What to know about market‑ linked life strategies

PAGE 28

Can AI be trusted for premium finance planning?

PAGE 42

Navigating Success, Together

Knighthead Insurance Group is a family of global insurance companies helping customers around the world protect and grow their wealth for more than a decade.

A Legacy of Growth

For over a decade, Knighthead Insurance Group has been dedicated to one thing—helping our global customers preserve and grow their wealth, their way. Across our insurance businesses, high ratings from AM Best and KBRA reflect our financial strength.

The Knighthead Insurance Group Businesses

Established 2024 Annuities for US-based customers. WWW.KNIGHTHEADLIFE.COM

Established 2014 Annuities for customers outside the US.

WWW.KNIGHTHEADINTERNATIONAL.COM

Established 2017 Reinsurance for life and annuity companies.

WWW.KNIGHTHEADRE.COM

Knighthead Life is the brand name of Knighthead US Holdings, Inc. and its subsidiaries, Merit Life Insurance Co. (“Merit Life”) and Knighthead American Life Insurance Company (“KALIC”). Knighthead International and Knighthead Re are the brand names for Knighthead Annuity & Life Assurance Company.

With the Smart Start Accumulator series, clients begin with an immediate edge thanks to the

Reduce market timing anxiety

Sidestep early volatility swings Capture favorable growth opportunities

IN THIS ISSUE

FEATURE

Trump 2.0: Financial chains unleashed or unraveled?

By John Hilton

The Trump administration’s economic program continues to take effect. What does it mean for advisors and their clients?

INTERVIEW

10 The goodness of mutuality

In a world that often believes bigger is better, 133-year-old Boston Mutual is focused on serving Americans of more modest means. Paul Quaranto discusses how his company stayed true to its roots during its long history.

IN THE FIELD

20 Coach Pete for the win

By Susan Rupe

Pete D’Arruda uses radio, books and billboards to reach clients, while coaching other advisors how to position themselves to deliver to a wider audience.

LIFE

28 What to know about market-linked life insurance strategies

By Darrel Tedrow

HEALTH/BENEFITS

36 Disability succession planning: What’s at stake, when to pivot By Sean McNiff

The right disability insurance coverage helps prevent a catastrophic liquidity event from becoming a defining challenge for the business.

ADVISORNEWS

40 Why advisors can’t afford to delay succession planning

By David Blake

The last thing any advisor wants is to be forced to sell their practice or scramble for a buyer when they’re out of options.

It’s important to look past the name of an index and understand how it’s built.

ANNUITY

32 Customizing FIAs with riders meets a broad set of client needs

By Val Majewski Advisors who focus solely on caps and participation rates miss the real marketing edge.

INSURTECH

42 Can AI be trusted for premium finance planning?

By Rayne Morgan

AI can do complex risk calculations more quickly and accurately than humans can.

IN THE KNOW

44 The wolf of AI

By Sue Kuraja

A tale of the

Diversified Brokerage Specialists 80 Years of Independent Expertise

Then. Now. Always.

Today’s clients expect speed. Advisors need efficiency. And underwriting shouldn’t slow great opportunities down.

Whether it’s life insurance, disability, long-term care, or annuities, we handle it all — from illustrations and presentations to applications and processing. Bring us a client, and we’ll deliver tailored solutions every step of the way.

And when traditional underwriting becomes the bottleneck, there’s a better way.

We make selling insurance easy:

• Life, Disability, LTC, and Annuities with full-service support

• Professional illustrations & client-ready presentations

• Application management that keeps cases moving

• Guaranteed Standard Issue (GSI) programs that minimize underwriting and speed approvals

Over 200 years of combined experience. Proudly independent. Always focused on you.

The April explosion

An exceptionally cold and snowy winter put most of us here in Pennsylvania into some kind of holding pattern in the early part of this year. Subfreezing temperatures, uncertainty about travel conditions and a general reluctance to venture outdoors made many of us hunker down and put life on hold until things began to thaw.

But then April comes along — and everything explodes.

Those first few warm days hit, and everyone goes crazy. People emerge from their winter cocoons and begin doing all those outdoor tasks that signal the change of season — washing cars, getting the porch furniture out of storage, pressure-washing decks — all while wearing shorts. Trees burst into bloom, and the pollen count goes through the roof.

Here at InsuranceNewsNet, we are feeling that April explosion.

We started a few weeks ago, as our editorial staff resumed travel and attended the first of the 2026 lineup of industry events. It’s crucial that we get out there and mingle with experts in the business as well as rank-and-file members of industry associations. These trips result in timely articles for the magazine and website, valuable relationships as we interpret the latest industry movements, and a better overall understanding of what our readers face as they serve their clients and manage their practices.

Our April issue reflects the explosion of new laws and deregulation in the industry as well as the snowball effect of technology.

What does OBBBA mean for taxpayers and advisors?

The One Big Beautiful Bill Act dominated the news when this landmark legislation was signed into law on July 4, 2025. Aggressive deregulation and protectionist trade policies contributed to a period of robust growth, with real gross domestic product reportedly rising by 4.3% in the third quarter of 2025. The Dow Jones Industrial Average

exploded above 50,000 for the first time in February.

What does this mean for everyday Americans and those who advise them? John Hilton breaks it down in our April feature article.

While the administration touts “largest tax refund season in history” and rising blue-collar wages, critics point out that the OBBBA is projected to increase the federal deficit by $3.4 trillion over the coming decade.

Analysis suggests a K-shaped impact where the top 1% of earners see significant net income increases, while middle-income and lower-income households may face net losses as the costs of tariffs and potential spending cuts to social services offset direct tax savings.

John discusses what advisors need to know as their clients are impacted by changes to the tax laws.

In addition, Trump Accounts that were established as part of OBBBA provide eligible children with $1,000 in government seed money. Although this is an attractive “free money” entry point, these accounts have significant planning drawbacks compared to traditional 529 plans. John discusses what these funds can mean to families as they plan for their children’s futures.

Meanwhile, the Trump administration has actively moved to roll back the

Retirement Security Rule — also known as the fiduciary rule — dropping legal defenses as of November 2024 and planning to have a new deregulatory framework by May of this year.

Will deregulation prioritize sales over fiduciary duty? John discusses some possible answers.

A lighthearted look at a serious subject

Technology — especially artificial intelligence — is exploding into every aspect of our personal and professional lives. In this month’s issue, Sue Kuraja takes a lighthearted look at a serious subject, the capabilities and potential pitfalls of using AI models. Sue uses the story “The Three Little Pigs” to illustrate ways organizations can scale their AI strategies responsibly.

And this month’s In the Field features an interview with the high-energy Pete D’Arruda, also known as Coach Pete. He exploded on the radio scene, dispensing practical financial advice to callers, and now helps other advisors position themselves as thought leaders in their own communities.

Spring is brief, and the April explosion doesn’t last long. Go out and enjoy it while you can.

Susan Rupe Editor in Chief, magazine

What’s in the news on InsuranceNewsNet.com

Judge orders Greg Lindberg to pay $526 million to policyholders

By John Hilton

A North Carolina judge ordered Greg Lindberg to pay $526 million to long-suffering policyholders following a civil trial.

Wake County Superior Court Judge Graham Shirley oversaw the trial to determine the amount of financial damages Lindberg and his companies owed to insurers they were found to have defrauded.

It was the culmination of a long-standing civil lawsuit originally filed in October 2019 by life insurers formerly owned by Lindberg: Southland National Insurance Corp., Bankers Life Insurance Co., Colorado Bankers Life Insurance Co. and Southland National Reinsurance Corp.

The majority of the award, $351 million of it, consists of punitive damages. Shirley stated this was intended “to punish him

and discourage others from committing similar wrongful acts.”

On June 27, 2019, all four insurers were placed in rehabilitation by order of the Superior Court of Wake County. On the same date, the parties entered into a memorandum of understanding under which Lindberg agreed to place certain special-purpose insurance companies — known as special purpose captive insurers — under a new holding company governed by an independent board tasked with protecting policyholders.

Judge: Money was ‘stolen’

The plaintiffs later sued, claiming that Lindberg violated the memorandum. Plaintiffs also brought claims of fraud and negligent misrepresentation, “alleging that Defendants made misstatements in the text of the MOU that induced Defendants to enter into two other agreements: the Revolving Credit Agreement and Interim Amendment to Loan Agreement,” court documents say.

Local TV station WRAL covered the proceedings and quoted Shirley, who stated that he’s confident Lindberg has the money to pay up from funds “that he has, to put it lightly, stolen.”

This ruling is separate from other recent legal developments, such as the $122 million contempt order that Lindberg petitioned the North Carolina Supreme Court to review.

Investors holding $130M in PHL benefits slam liquidation, seek to intervene

By John Hilton

Investors holding PHL Variable universal life policies with combined death benefits totaling more than $130 million say they paid monthly premiums north of $1 million while Connecticut regulators fed them false hopes of a company rehabilitation.

The hefty premiums helped pad the PHL bottom line for 19 months, and now investors stand on the losing end of potential liquidation.

Investors are not happy.

BroadRiver Asset Management filed an emergency motion to intervene. The firm represents policyholders who own 32 inforce UL policies with cumulative death benefits of $130.3 million.

Large UL policyholders “have funded the PHL estate in reliance on persistent, false representations by the Rehabilitator

that a rehabilitation plan — where death benefits would remain due and owing by PHL with various premium cost adjustments to address actuarial projections — would be forthcoming,” reads a memorandum accompanying the motion.

The BroadRiver policyholders have paid $57.1 million in premium payments, $19.7 million in the 19 months since Connecticut regulators began their rehabilitation of PHL Variable, the memo reads.

From the end of 2023 to September 2025, the amount of cash and short-term

investments held by the PHL companies increased from $103 million to $437.5 million. Regulators fattened PHL’s coffers via the large premiums paid by investors, the BroadRiver motion says.

A liquidation order would result in the termination of UL policies. That means BroadRiver policyholders would be left with nothing more than guaranty association coverage (limited by the $300,000 cap or whatever else the guaranty association agrees to) and a subordinated claim in a PHL liquidation.

Read the full story online: https://bit.ly/phl2026

InsuranceNewsNet Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback.com.

CVS Health CEO David Joyner fires back at

AOC’s monopoly criticism

By John Hilton

CVS Health President and CEO David Joyner took the brunt of Rep. Alexandria Ocasio-Cortez’s viral broadside on health insurers.

The New York City Democrat called out CVS Health’s corporate strategy to “monopolize patient care” during a hearing held by the Health Subcommittee of the Committee on Energy and Commerce. Joyner responded during a fourth-quarter and full-year earnings call update for Wall Street analysts, where he devoted a significant portion of his prepared remarks to addressing the legislative criticism of CVS’s “vertical integration.”

While never mentioning OcasioCortez, Joyner said CVS Health’s control of the health insurer, medical provider, pharmacy benefit manager, drug manufacturer and pharmacy — meaning its members rarely leave a CVS-owned health business — saves the patient money.

“We can provide a connected solution for consumers that delivers better experiences and improves health outcomes at lower cost,” Joyner said. “Aetna members who have a combined medical and pharmacy offering have lower medical costs. Aetna members who consistently use CVS Pharmacy have higher medication adherence and lower ER utilization.”

During the hearing, Ocasio-Cortez noted that CVS Caremark, a PBM, processes nearly 30% of all prescriptions in a given year and helps determine what millions of patients pay for needed drugs.

She described a fictional patient named “Kate,” who has an Aetna health insurance plan, goes to a CVS Pharmacy and is connected to an Oak Street Health medical clinic. That led to a snarky exchange when Ocasio-Cortez pointed out the financial benefits for CVS.

“I would suggest it’s a model that works really well for the consumer,” Joyner said.

“Yeah. I think it works very well for CVS,” Ocasio-Cortez shot back.

Read the full story online: https://bit.ly/cvsjoyner

InsuranceNewsNet Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback.com.

About 3M kids signed up for Trump Accounts

Families have filled out about 2 million Trump Account forms for about 3 mil lion kids, Treasury Secretary Scott Bessent said.

Parents or guardians can elect to open Trump Accounts for their kids with IRS Form 4547. Families can file Form 4547 with their 2025 tax return or through TrumpAccounts.gov. Once their account is open, babies born between 2025 and 2028 are eligible for $1,000 in seed money from the U.S. Department of the Treasury. The money will be placed in the accounts on July 4.

Parents, guardians and others can contribute up to $5,000 annually to Trump Accounts until children turn 18 years old.

A growing number of companies have pledged to match the Treasury’s initial deposit for the children of employees. Employers can deposit up to $2,500 as part of the $5,000 limit.

‘BOOMCESSION’

The economy seems to be in a boom and a recession at the same time, which may explain why many Americans don’t feel the economic growth that appears on paper.

This so-called boomcession describes how the average American’s feeling that they are not reaping the benefits of an economy that — by many indications — is humming along. That’s according to the American Economic Liberties Project.

Economic output and the stock market are on the rise, consumers are spending big and the post-pandemic recession that many expected never materialized. But many Americans feel pessimistic about their finances, and debt is at alltime highs.

MIDDLE-CLASS HOUSEHOLDS FACE A WORSENING SQUEEZE

Middle-class households face worsening cost pressures for the first time since October 2024, the American Council of Life Insurers conducted its first Financial Resilience Index survey.

The Financial Resilience Index also found that more than 4 in 10 middle-class households (42%) are not confident that they could pay an unexpected expense of $5,000 and bounce back financially.

Despite these pressures, middle-class households are taking some steps to improve or maintain financial stability, but there is room for improvement. More than half (52%) of middle-class households are putting money into a savings account and almost 6 in 10 (58%) said they are paying off debt or making debt payments.

Strong stock markets don’t mean a lick to you if you don’t own any stocks.”

— Joanne Hsu, director of the University of Michigan’s Surveys of Consumers

AMERICANS SACRIFICE TO AFFORD HOMEOWNERS INSURANCE

High home insurance rates are hitting Americans hard in 2026. A new survey from Insurify found that 59% of policyholders said their costs increased last year, and 57% made financial sacrifices to help pay for coverage.

Forty percent say they spend more on home insurance than they do on other coverages, such as car or health insurance. More than 1 in 4 homeowners (28%) said they would drop their home insurance if they could because of unexpected stress over high premiums.

To cut their insurance costs in half, 30% would allow insurers to install and monitor internal or external home cameras, and 19% say they

Nearly three-fifths of Americans believe the U.S. economy is currently in a recession

In a world that often believes bigger is better, 133-year-old Boston Mutual is focused on serving Americans of more modest means.

An interview with PAUL FELDMAN, publisher

In a world that often believes bigger is better, a 133-year-old mutual insurer is focused on serving Americans of more modest means. Boston Mutual was founded with the purpose of providing working Americans with financial peace of mind in their time of need. The company provides life, accident and related insurance products through the workplace as well as in the individual market.

Paul Quaranto led Boston Mutual from 2012 to 2025 and currently serves as chair of Boston Mutual’s board of directors and of the board of Life Insurance Company of Boston & New York. He also served as chairman of the American Council of Life Insurers from 2023 to 2024, helping raise awareness of the life insurance industry among lawmakers, policymakers and consumers.

In this interview with publisher Paul Feldman, Quaranto describes the philosophy that has led Boston Mutual through more than a century of serving its policyholders, as well as the company’s efforts in using artificial intelligence and data analytics to improve the customer experience.

PAUL FELDMAN: How did you get into this industry?

PAUL QUARANTO: It’s a simple story. My wife and I were engaged to be married — it was almost 45 years ago — and it was my senior year of college. Her father suggested that I should have a job before I married his daughter. I interviewed on campus for a company called Paul Revere — it later became part of the Unum companies — and I had the opportunity to take a job there as a group insurance underwriter.

That’s where I began. It began by default. It’s amazing to think that 45 years later, I’ve been blessed to have the opportunity to work in this industry and to grow into a leadership role that I never thought could happen. It has been a fantastic run, and I’m very humbled and honored to have had this happen.

One of the problems we have as an industry is that people don’t look at this industry as giving you real professional opportunity. We developed an intern program here, and I try to remind the interns that this industry has evolved. It’s not only about actuaries and accountants and

attorneys anymore. Everything they find in other walks of life — whether it’s technology, project management, public relations, investments — exists in this world. We need to compete in all those areas. This industry provides incredible opportunities for younger people. I believe it’s an industry that serves what many younger people want, which is balance in their life, purpose and mission, the feeling that they’re not only growing professionally but they’re meeting some of their personal goals of serving in a meaningful role and giving something back. I think this industry can provide that for people. We need to do a better job of telling that story.

FELDMAN: What can we do as industry tell our story better?

QUARANTO: A year ago, I was chosen to chair the American Council of Life Insurers. For a company like Boston Mutual, to be selected to do that was truly an honor.

nobody knows that. That was my pitch when I served my year at ACLI: Let’s tell our story better.

We must do a better job of saying we serve people from all walks of life. We need to make life insurance simpler and understandable. It’s a complex business, and what goes on behind the curtain can be complex, but we must do a better job of telling that story. I hear every day how a $5,000 or $10,000 or $15,000 life insurance policy is saving a family. Think about that. We don’t live in that world every day, but most people in this country live in that world. That’s pretty powerful stuff.

FELDMAN: Boston Mutual serves the lower-to-middle-income market. It’s such an underserved market. What made you choose that market?

QUARANTO: Part of Boston Mutual’s metamorphosis was we started by selling life insurance policies at the kitchen table, and today, we sell them at the cafeteria ta-

“We’re owned by policyholders for the benefit of our policyholders. We’re not trying to appease quarterly market returns versus long-term promises to clients ... . It affords us this opportunity to say we want to serve our customers. We know who they are.”

I think it was a recognition by companies of all sizes of a company of our size — which is small to midsized by industry standards and serves in a unique space. More than 130 years ago, Boston Mutual’s first president said we want to be a progressive life insurance company serving the needs of working families who, at that time, didn’t have the opportunity to secure any level of financial security. Fast-forward to today and we’re still that company. I think it has been a wonderful opportunity to be the face of an organization saying we serve people in all walks of life and then having the opportunity to say we need to tell that story better so that people can understand what we do is affordable. We need to make things simpler.

I think this industry is a noble one. It is a noble industry doing good things, yet

ble. We’re using the workplace as a leverage point, and I think a lot of companies are looking at that. When you get to the markets we serve, when you think about access and you think about payroll deductions, there is a means that’s more efficient in terms of selling the products. Our market for group products is companies with five all the way up to 50 employees.

We sell some group life chassis products, but we still sell a traditional individual whole life product that is built to serve those markets. That’s a policy that the employee owns. Regardless of whether they stay with that employer, they have the opportunity to maintain the policy forever. Part of what we want to represent through the agents who sell our product is that if an employer is concerned about their people and they want to give them products that can provide a

level of protection they believe they need, then let’s have a conversation. Because for us, it’s about giving employees that level of security and a product they can own and carry forward.

If an employer is just looking to put a menu of products out there and leverage an insurance buy with a technology platform that can also serve as an HR system for them, and all they want are products that will plug into that, and they don’t care if only 3% of the group signs up, that’s not who we want to talk to. I want to talk to Paul who’s got 30 employees, who knows most of them and is concerned that if the worst were to happen, he knows the family and doesn’t want to be in a position where he hasn’t done anything.

Now he can give them that policy — life, accident, critical illness, whatever — and they have a level of protection. If someone has that sort of sense as an employer, then that’s someone we want to talk to. There’s something that’s a value we can bring to them. We don’t want to be a commodity. We want to be a value-add for a family.

business and do it the right way but align all those pieces as well.

FELDMAN: What’s new and exciting at your company?

QUARANTO: I think it’s a combination of what is new and exciting and what isn’t new and exciting. I believe in the power of our story. I was the seventh president of Boston Mutual. We are in the middle of a leadership transition, and I am now the chairman and CEO. We have named a new president who will transition into the role.

be another 100-plus years of good stuff going forward?

We launched the first phase of a new policy administration platform and a new customer service model. These are incredibly exciting and will serve this company well.

FELDMAN: How has technology improved your processes?

QUARANTO: We needed to bolster our IT area. We needed a project management discipline to come into the company. We not only needed actuaries but we

FELDMAN: Boston Mutual is a 133-year-old mutual company. Tell us what that means to you.

QUARANTO: At Boston Mutual, we talk about the goodness of mutuality. We’re owned by policyholders for the benefit of our policyholders. We’re not trying to appease quarterly market returns versus long-term promises to clients. I think it allows us to live everything in terms of our brand and the value that we want to bring to the table. It affords us this opportunity to say we want to serve our customers. We know who they are. We want to serve the people who sell us. We want to serve our employees. We want to serve our communities. We’ve developed the Making an Impact program. We’ve been recognized for seven years as one of the most charitable organizations in Massachusetts. There is a bigger picture, a greater good that exists, and as a mutual company we can touch all those, but at the end of the day, we must be successful. We must grow our

“I hear every day how a $5,000 or $10,000 or $15,000 life insurance policy is saving a family. Think about that. We don’t live in that world every day, but most people in this country live in that world. That’s pretty powerful stuff.”

John Wheeler, our company’s first president, said our mission was to provide working Americans with the opportunity to take care of their families. That’s who we are today. Who we are, what we do, why we do it and who we do it for haven’t changed. But it’s how we do it that needs to change.

With 100-plus-year-old mutual companies, you’re dealing with all these legacy systems. Your ability to put product on the street, make that product simple and understandable and affordable, and your ability to serve your customers better with these legacy technology systems are real challenges. We’re not only competing with each other, but we’re competing against every customer experience that people have.

So what’s new and different is how do we take all of that good stuff and move it into a world where we can be better at how we do it? That’s the transition going on here. That has been the theme of the vision I had, the strategic plan we had — how do we prepare ourselves for the future so that 130 years of good stuff can

needed data scientists who could begin to help us understand where our data was stored and how we were going to put it into a new system.

Our organization had some gaps to fill, and then we needed to be sure that we had people in the organization who were capable of handling the change that would take place and who would be excited to be part of that journey. We recognized that some of us had to hold down the fort today while we build out tomorrow. All this required a thoughtful strategy on the people side of things as well.

It took two or three years of getting ready for this before we went to market. But we found what we wanted, and by doing it right, you give yourself a greater chance of success.

As we wrap up our strategic plan, we had several milestones for this year. One was to get this thing launched and move it forward. We’re excited about it. Having the combination of the organization and its people supporting a vision and a strategy was how we approached this, and it worked well for us.

FELDMAN: Tell me how your data scientists work. I don’t believe a lot of people think about data science in life insurance.

QUARANTO: I would always joke with our chief actuary that we need to morph from actuaries to data scientists. He would say, ‘What do you mean by that?’ I said, ‘Actuaries are great at looking backward. Data scientists will be the ones who look forward, take that data and begin to do more predictive analytics. They will use that data to help us better understand and give us a greater chance of success for the things that we want to do going forward.’

This is where you get into discussions about where artificial intelligence takes us in the long run. It’s about access to data, which is difficult with legacy systems, and how you will use that data to support future planning.

FELDMAN: What are you doing with the data, and how is that helping Boston Mutual?

QUARANTO: First, we had to identify how to access our data. With a 130-yearold company, we have lots of data, but with some of our legacy systems, a lot of that data was not readily available. A lot of data was baked into some of our programming, so we had to come up with a strategy to access the data and scrub that data so that we’re using accurate data.

We’ve made great progress on that. It’s critical not only for using your data today but preparing your organization for converting from those old legacy systems to a new system because you need clean data to bring forward into the new system.

We also looked to apply more science, if you will, to our distribution and sales efforts. Where are our target markets? Who is our customer? What can we learn about them from a socioeconomic standpoint? How can we use data to identify where they live, where they work, the types of jobs they’re in, and how can we go from a broad-based approach to a narrower focus with our sales team?

Helping our people to be better at identifying these things improves our closing ratios. It also improves our participation levels with our voluntary benefit products.

We’ve also used data as far as our own employees are concerned. This gives us a better understanding of what it is about our company that makes us a viable professional employment opportunity for them and how we get feedback on who they are, what they want and how they want to grow personally and professionally — and how do we create an environment where that can happen.

FELDMAN: What are some surprising discoveries you made from using data analytics?

QUARANTO: One surprise was how hard it was to get at our data. But a good surprise was how the data validated the socioeconomic profile of who we serve. We serve a lower-middle-income market, including a lot of single mothers. Now all of a sudden, the data validated that. It helped us do a better job of thinking about the products we need to serve those people if we want to move the needle to a broader base of customers.

The people we serve are probably some of the most economically challenged people in the marketplace. Many of them want to do right by their families, and they look to us for some sort of guaranteed solution if something bad happens in their lives. But we’re seeing people struggle to make their premium payments. So we’re making sure what we do is simple and helps people understand what their options are but also allows us as a company to sort of push up and be more relevant. This gives us a little bit more stability and growth opportunities in the market we serve.

FELDMAN: Where do you see artificial intelligence taking this industry?

QUARANTO: I think that for smaller companies, AI will be used to create efficiencies of scale. We’re already on that path.

I want to apply technology to process and people to our customers. You apply technology to the process so that your people aren’t doing the process. They’re talking to the customers and creating the customer experience.

FELDMAN: You served as chairman of ACLI in 2023-2024. What are you seeing at that organization?

QUARANTO: I think the industry has come together in understanding that we must be unified in terms of presenting who we are and what our needs are, and why the industry is important. We are letting those in Washington and in the state capitals know that if there are things that will affect us, please give us a call and at least have a conversation with us.

I think ACLI is focused on the optics of the industry — showing a more positive side of what we do and the opportunities we present.

The better job we do of articulating the value of this industry at all levels — the economic level, the community level, the level of financial security for Americans — all of those other conversations become easier.

FELDMAN: What should an agent understand about the industry as you see it?

QUARANTO: When I get an opportunity to chat with our agents, the first thing I always do is just thank them. I tell them, ‘You are the front line of this industry. You’re the people out there educating people on the need to have some level of financial security. And then, God forbid, if they need to tap into that, you’re the ones who deliver the checks.’

I think we need to remind our people that this is a noble industry, doing good things for people. There are financial opportunities for agents in that, but it’s not only about financial opportunities; it’s about the ability to give back and help people.

The distribution in the industry — the sellers and the manufacturers — must come together to work on that. Because you don’t put most of what we sell on a platform and expect people to wake up and say, ‘I’m going to buy life insurance today’ and figure out what’s right for them. They still need counsel and advice. That’s what we must provide, and we must find an efficient way to do that and find good people who are happy with making a living doing that.

Like this article or any other?

Take advantage of our award-winning journalism, licensure and reprint options. Find out more at innreprints.com

Financial chains unleashed or unraveled?

As President Donald Trump moves closer to the midpoint of his second term, the full impact of his agenda is being felt. What does it mean for advisors?

BY JOHN HILTON

April showers may bring May flowers, but for advisors and clients, they also bring a torrential downpour of forms, figures and that age-old question: “Is my dog finally tax-deductible?”

Rest assured that Fido remains off limits. Still, taxing questions remain as the Trump administration’s economic program continues to take effect.

Of course, the centerpiece of the Trump return was signed in a July Rose Garden event: the One Big Beautiful Bill Act, a landmark piece of legislation that permanently extended many of the 2017 Tax Cuts and Jobs Act provisions while adding highly visible, targeted benefits.

On the economic front, the administration’s second term has been defined by aggressive deregulation and protectionist trade policies, which contributed to a period of robust growth. Real gross domestic product rose by 4.3% in the third quarter of 2025. The Dow Jones Industrial Average hit a historic high of 50,000 in February.

The long-term fiscal and distributional impacts of Trump’s policies remain a point of significant debate. While the administration touts “the largest tax refund season in history” and rising blue-collar wages, critics point out that the OBBBA is projected to increase the federal deficit by $3.4 trillion over the coming decade.

Analysis suggests a K-shaped impact where the top 1% of earners see significant net income increases, while middle-income and lower-income households may face net losses as the cost of tariffs and potential spending cuts to social services offset direct tax savings.

One certain thing is that financial advisors and retirement planners will earn their fees. Advisors will want to pay particular attention to the following three areas.

1. Fiscal stability and the 2028 sunset

The OBBA provided immediate tax relief, but it carries long-term fiscal risks.

» Debt and yield pressure: The OBBBA authorizes a $5 trillion debt limit increase, which may flood the market with

Treasurys, lowering bond prices and putting upward pressure on yields.

» Sunset planning: Although many TCJA provisions were made permanent, others are still slated to expire after 2028. Advisors are warning clients to consider Roth conversions now to lock in today’s lower tax rates before potential increases in 2029.

The most important thing the OBBBA did for advisors and their clients was to bring stability to their financial planning, said Dennis Bielik, executive vice president and managing director at Hub International.

the portion of total charitable contributions that exceeds 0.5% of adjusted gross income will be deductible.

The OBBBA also reduces the marginal value of charitable deductions for top-bracket taxpayers. Under current law, donors in the highest bracket receive a deduction that offsets tax at about 37%. Beginning in 2026, the value of that same deduction will fall to roughly 35%, modestly increasing the net after-tax cost of each dollar given.

Future charitable giving and the tax impacts of that giving were the main topics of a recent webinar hosted by the National Association of Insurance and Financial Advisors.

“A common mistake with the estate tax is taking the word ‘permanent’ too literally. The law can very easily change again next week.”

“The new standard deduction is $15,750 for individuals and $31,500 for couples, while the state and local tax cap expands to $40,000 for the next five years. Combined with higher income thresholds for the alternative minimum tax exemption and continued limits on itemized deductions, these provisions favor income and liquidity management over estate tax planning,” Bielik wrote in a recent column for InsuranceNewsNet.

“For high-net-worth clients, that means shifting attention from legacy transfers to active income timing, Roth conversions and charitable strategies,” he added.

Among the many changes ushered in by the OBBBA, how charitable deductions are handled is among the biggest. These changes reduce the tax value of charitable giving for many high-income individuals and introduce new limitations on itemized deductions. The changes are significant, tax experts say, and not favorable to the taxpayer.

There are strategies to maximize charitable giving. But first, the changes.

For starters, a new 0.5% “floor” on charitable deductions means that only

Steve Gorin is a trust and estate lawyer and partner at the law firm Thompson Coburn. Business owners can convert charitable contributions into business expenses if they receive a financial return commensurate with the payment, he explained.

Examples include paying for an advertisement in a charity’s program, or a restaurant donating a percentage of sales on a specific night.

“There’s a direct correlation between the sales and the charitable payment,” Gorin noted. “That restaurant can deduct that charitable payment as a business expense relating to the sales.”

For wealthy clients, the OBBBA brought relief by increasing the federal estate tax exemption and making that increase permanent. The federal estate and gift tax exemption was scheduled to drop to $7 million but instead rises to $15 million per person and $30 million for married couples.

The worry now is complacency, the NAIFA panel agreed.

Michael Tessler is president of Brokerage Unlimited, where he assists

financial professionals with wealth transfer and wealth protection strategies.

A common mistake with the estate tax is taking the word “permanent” too literally, he said. The law can very easily change again next week. Tessler gave the example of a fictional couple who put a life insurance policy in an irrevocable trust with the idea that it would provide liquidity for their estate. After the OBBBA, the couple removed the life insurance, assuming the estate tax exemption would be $30 million forever.

“If things change, one, they’re going to be older and it’s going to cost more,” Tessler explained. “And two, insurability is always in question. To have a strategy in place, completely ditch it and then wind up needing or wanting it back in place — when it comes to life insurance, not so simple.”

There certainly are clients who will want to surrender a life insurance policy in this situation, Tessler acknowledged. Advisors must consider many factors from a financial standpoint.

“What is the rate of return on that death benefit, depending upon how many years the client lives?” Tessler asked rhetorically. “And keep in mind that if the client’s health has deteriorated since the time they purchased the policy, that only makes the rate of return go up based on a shorter life expectancy.”

as ordinary income rather than being tax free like a 529, which can push students into higher tax brackets and reduce the usable value of the savings.

» The “public benefits trap”: Assets in these accounts are currently not exempt from eligibility tests for Medicaid or Supplemental Nutrition Assistance Program, potentially disqualifying low-income families from essential aid.

Chris Gandy, NAIFA president, is a big fan of the Trump Accounts.

that compound over a lifetime.”

Parents and relatives can each provide up to $5,000 annually to the account, while employers are limited to a $2,500 annual contribution. The funds will be invested in the stocks of “American companies” through what is described as a “broad stock-market index.”

At least 28 companies have pledged a $1,000 match, including Bank of America Corp., JPMorgan Chase & Co. and Wells Fargo & Co.

But some economists doubt the true effectiveness of the accounts beyond the seed money given investment limitations, compared with a state-sponsored 529 plan. Likewise, critics say the realistic inability of low-to-moderate-income parents to contribute funds on a consistent basis will serve to widen the wealth inequality.

“Analysis suggests a K-shaped impact where the top 1% of earners see significant net income increases, while middle-income and lower-income households may face net losses as the cost of tariffs and potential spending cuts to social services offset direct tax savings.”

2. The ‘Trump Account’ structural risks

While the $1,000 government seed is an attractive “free money” entry point, these accounts have significant planning drawbacks compared to traditional 529 plans:

» Sequence of returns risk: Unlike 529s, Trump Accounts lack age-based “glide paths.” A 17-year-old’s account is 100% invested in U.S. stocks, exposing the entire balance to a market crash right when it’s needed for college.

» Tax friction: Withdrawals are taxed

Part of the OBBBA, the tax-deferred savings accounts provide $1,000 from the U.S. Treasury as investment seed money. Children eligible for the $1,000 seed money are those born to U.S. citizens between Jan. 1, 2025, and Dec. 31, 2028.

An initial $1,000 investment in a lowcost stock index fund can grow meaningfully over 18 years, Gandy noted in a recent column for InsuranceNewsNet.

“But the true promise of Trump Accounts lies in steady contributions from parents, grandparents, employers and even community organizations,” he wrote. “These accounts can support long-term objectives such as college, firsthome savings or early investing habits

With one-third of American households having less than $2,000 in emergency savings, “it makes them unlikely to contribute to their children’s Trump Accounts,” the Urban Institute said.

The money in Trump Accounts can grow tax deferred, but any withdrawals — even for the approved uses of college tuition, a first home or starting a business — are taxed at capital gains rates. Only half of the money can be withdrawn at age 18, and the rest at age 31.

Many financial experts believe 529 plans are a better option for committed savers. A 529 plan is a state-sponsored, tax-advantaged investment account designed to save for future education costs, including college, vocational school and up to $10,000 annually for K-12 tuition.

Earnings grow tax free, and withdrawals are tax exempt when used for qualified education expenses. Anyone can open a 529 account, and the plans offer high contribution limits with no income restrictions.

At the very least, Trump Accounts give those less-motivated savers something to get started.

“For many middle-income families, a structured, tax-advantaged, early-start investment vehicle is something they’ve wanted but never had the infrastructure or guidance to use,” Gandy said.

In late-February comments to the IRS on establishing the accounts, NAIFA recommended that the Treasury Department work with Congress to amend current investment restrictions that limit Trump Accounts primarily to index funds and exchange-traded funds. Although these investments can be appropriate in many circumstances, NAIFA cautioned that overly restrictive investment menus could limit customization and long-term performance.

“Restricting access to broader investment options limits customization and

say the best-interest framework created by the National Association of Insurance Commissioners and adopted in nearly every state is fair and thorough.

» Risky assets in 401(k)s: New executive orders aim to “democratize” access to private equity and digital assets in retirement plans. Advisors warn that these are often illiquid and hard to value and could lead to “life-altering losses” for ordinary savers.

All eyes are on the Department of Labor and its May regulatory agenda. It could contain a resolution to a more than 10-year pursuit of an extension of fiduciary duties to a broader range of financial professionals.

With one-third of American households having less than $2,000 in emergency savings, “it makes them unlikely to contribute to their children’s Trump Accounts.”

— The Urban Institute

prevents advisors from tailoring strategies to the specific needs of the individual,” Gandy said. “Financial experts are positioned to responsibly advise their clients on the multitude of investment options available to them and then use that knowledge to maximize value and returns over time.”

3. Weakened fiduciary protections and ‘buyer beware’ advice

The Trump administration has actively moved to roll back the Retirement Security Rule (fiduciary rule), dropping legal defenses as of November 2024 and planning a new deregulatory framework by May 2026.

» Conflict of interest? Deregulation may prioritize sales over fiduciary duty, making it harder for clients to know whether an advisor is acting in their best interest or chasing commissions. Industry officials

With Trump’s return, the DOL has effectively abandoned its defense of the Biden-era Retirement Security Rule, essentially a rerun of the fiduciary rule published during the Obama administration.

On Nov. 28, 2025, the Court of Appeals for the Fifth Circuit granted the DOL’s motion to dismiss its own appeal of lower court rulings that had blocked the rule. Because the government stopped defending the rule, nationwide stays issued by Texas district courts remain in place, preventing the expanded fiduciary definition from taking effect.

The industry has returned to the “fivepart test” established in 1975 to determine fiduciary status, supplemented by existing exemptions like PTE 2020-02.

But while it might seem a sure thing that a Trump DOL will pursue light regulation, history tells us a different story. The first Trump administration left us with PTE 2020-02, which allows

investment advisers to receive compensation for retirement advice, aligning with the Securities and Exchange Commission’s Regulation Best Interest.

The exemption mandates that advisors adhere to “Impartial Conduct Standards,” which include acting in a client’s best interest, providing written fiduciary acknowledgment, documenting rollover advice and conducting annual reviews.

Lawsuits challenged PTE 2020-02, and a federal court tossed portions of the preamble that allowed one-time rollover advice to trigger fiduciary status.

Recent Supreme Court rulings, specifically Loper Bright Enterprises v. Raimondo, have weakened the DOL’s ability to broadly interpret its authority under the Employee Retirement Income Security Act, making a return to the Biden-era expansive definition unlikely.

Meanwhile, a best-interest model law compiled by the NAIC has been passed in all 50 states. More recently, regulators signaled that they are looking at more active monitoring of compliance issues.

In March 2024, Iowa Insurance Commissioner Doug Ommen first noted that reviews of compliance with the best-interest regulation turned up “deficiencies” in producer monitoring. Ommen chairs the Annuity Suitability Working Group, which is behind the draft guideline.

After more than 18 months of discussion, the NAIC approved the Annuity Suitability Safe Harbor Guidance document during its 2025 fall meeting.

“To meet safe harbor requirements, insurers must monitor the insurance producer or their supervising entity,” the guidance reads. “An effective monitoring program involves the insurer taking active steps to assure itself that the supervising entity is complying with its obligations. Simply awaiting complaints or regulatory actions after regulatory exams are passive approaches that are inadequate in and of themselves.”

InsuranceNewsNet

Senior Editor John Hilton covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback.com. Follow him on X @INNJohnH.

A Visit With Agents of Change

PETE D’ARRUDA uses radio, books and billboards to deliver his message of financial security.

By Susan Rupe

One of Pete D’Arruda’s fondest childhood memories is of when his family would pile into the station wagon and take vacation trips to a national park. While spending hours driving to and from their destination, the family would be entertained by listening to the radio — and one particular radio personality sparked something in D’Arruda.

Bruce Williams had a nationally syndicated advice program that ran for nearly three decades. He was known for offering practical, sometimes blunt advice on listener problems, earning the nickname “America’s Answer Man.”

D’Arruda was inspired by Williams to take to the airwaves after launching his insurance and financial services career. D’Arruda is president and founding principal of Capital Financial, with offices in North Carolina, South Carolina, Arizona and Nevada.

But he is best known as “Coach Pete” and “America’s Wealth Coach,” dispensing advice about annuities, life insurance, tax planning and retirement issues in the 20 books he has authored, the most recent one being “Tax $avvy Retirement.” His multimillion-dollar production and broadcasting company, Broadcasting Experts, produces more than 80 weekly radio shows and long-form video and audio podcasts heard and seen nationwide. His national show, “The Financial Safari,” can be heard at FinancialSafari.com.

He has won three Emmy Awards.

He founded Capital Financial to help his clients “cross the street of life.“ His goal is to help clients take the worry out of living in retirement.

But although D’Arruda seems to be everywhere in the world of financial communication, his 32 years in the industry had a modest beginning.

D’Arruda told InsuranceNewsNet that he became a mortgage broker when he was newly graduated from the

University of North Carolina. He soon realized that he wasn’t helping people the way he wanted to in that career. He thought about his former girlfriend’s father, who sold 403(b) annuities to teachers, and he began to do the same.

“My mom was a teacher and my dad was a college professor,” he said. “I knew that each school had a room with little cubbyhole mailboxes for each teacher. So I designed a postage-paid card for the principal to put in each box, saying, ‘You’re entitled to your tax shelter benefits, and your enrollment agent will be here in the next two weeks. Send this back.’”

A new way to get out there

As his teacher clients eventually retired, D’Arruda pivoted to retirement planning, doing dinner seminars as a way of prospecting. But he eventually became dissatisfied with the turnout and response to those dinners, so it was time to try a new way to get his name in front of the public.

He walked into each of the radio stations in Raleigh, N.C., and asked the staff whether they would sell him broadcast time to do a show about retirement planning. “And they all laughed me out of there,” he said. “They had never thought about selling radio time for someone to do that.”

D’Arruda made his way to a smaller radio station in Aberdeen, N.C., where the station manager offered him a time slot and recorded the show for him. The show began to pick up steam, and eventually the radio staff in Raleigh who had laughed at him were asking him to be part of their programming lineup.

“So now I have seven hours every weekend on the biggest Raleigh station, doing a live call-in show,” he said. He began calling his show “Money Matters with Coach Pete,” but now calls the show “The Financial Safari.”

His popularity caught the attention of other advisors, who asked him to help them get started with on-air shows of their own. D’Arruda found himself branching out from advising clients about life insurance and retirement to producing radio programming for other financial professionals.

“We have about 80 advisors that we do weekly shows for,” he said. “We also do TV shows and podcasts for advisors,

and we do them for ourselves as well. I’m on the local TV news every week. They have a segment on planning, but also whenever anything happens in the economy, they call on me to do some commentary, so it has been a big credibility builder.”

What listeners want to know

Questions from listeners run the gamut from how to pay off a mortgage early to what to do with the money in their 401(k) accounts. D’Arruda said some of the hot topics from his audience include concerns about market risk, how to generate lifetime income in retirement and whether to invest in cryptocurrency. He also has interviewed a number of personalities, including Barbara Corcoran of TV’s “Shark Tank” and former NBA coach Dick Vitale.

to follow to be successful, D’Arruda said. “You have to figure out what you’re going to say, and you need to say it the right way,” he said. “You must make sure you have calls to action. You must make sure you don’t come across too ‘salesy’ — you don’t want to come across as someone from a late-night infomercial. You want to be educational, and you want to give people ways to contact you.”

D’Arruda also has developed the Financial Speakeasy, a website that will offer 24/7 multimedia content on everything from mortgages to real estate to a show called “Bucketing on a Budget” that describes ways people can check off experiences on their bucket list without breaking the bank. D’Arruda has lined up a number of

We all want something. I call it

“gratisfaction.” We want immediate return. Especially insurance and financial professionals, we want immediate return for what we spend.

The need for information on what to do with money accumulating in retirement accounts led D’Arruda to devise what he calls the “financial fill-up strategy.” When he discusses it on his radio show, the conversation is accompanied by the “ding-ding” sound that used to be heard when a car drove up to a full-service gas station pump in years past. He even has an antique gas pump in his office. It’s all part of his branding efforts.

“We all want something. I call it ‘gratisfaction,’” he said. “We want immediate return. Especially insurance and financial professionals, we want immediate return for what we spend. But you have to take a longer-term approach and build so you become known as somebody people can trust.”

Don’t be too ‘salesy’

Advisors who want to use media to build their own brand have a few steps they need

experts to present the programming, which will be produced in his studio that includes seating for a live audience of up to 20 people. The site is scheduled to go live later this year.

Airport billboard advertising is another avenue D’Arruda has used to get his name in front of people. He has airport billboards in his home community of Raleigh and also has billboards in the departure terminal at the airport in Aruba. Being in the departure terminal costs him far less than in other parts of the airport, where hotels and tour operators pay a premium for advertising to tourists.

“But if I have some people from Raleigh who are in Aruba and they see my advertising, it’s another way to build recognition and credibility. Do I expect immediate return? No, and if you expect immediate return in this business, you’ll be sadly disappointed,” he said.

the Fıeld A Visit With Agents of Change

Protecting against market risk

You must make sure you have calls to action. You must make sure you don’t come across too ‘salesy’ — you don’t want to come across as someone from a late-night infomercial.

2 26 PREMIUM FINANCING & HIGH NET WORTH SOLUTIONS

In his years of advising, D’Arruda said he sees consumers making several bad financial decisions, and the most common bad decision revolves around market risk.

“People are way too impulsive. Everyone thinks they can take on a lot of risk until they experience the downside of risk. It’s easy to say, ‘Oh, yeah, I can take that risk,’ but when you look at it in real dollars, can they really take that risk?

“Let’s say someone is two years away from retirement and they have $1 million saved. But maybe it’s exposed to risk, so you ask, what’s their goal in keeping that money at risk? And sometimes they say they want to make another 20% on it. All right, so 20% of the $1 million is another $200,000, and now they have $1.2 million when they reach retirement. Is that really going to change their lifestyle, going from $1 million to $1.2 million? Not really. But when they realize if they lost 20% and now they have $800,000 instead of $1 million, their whole attitude changes.”

The financial fill-up strategy

That’s where D’Arruda’s financial fill-up strategy comes in.

It’s a guaranteed lifetime retirement income plan where clients receive

another “fill-up,” another payment, every month for life.

“The people who have this fill-up are the happiest people in the world because they don’t care what the market’s doing anymore,” he said. “They keep some money in the market, but even if they lost that money, they still have their lifetime income plans together. And I can sleep a lot easier at night knowing I’m not putting people right in front of a train coming toward them.”

D’Arruda calls himself “a multitasker extraordinaire” and said he wants to inject some fun into a business that deals with serious topics.

“I like to have fun doing what I’m doing. And if you’re not having fun, you’re in the wrong business. Life’s too short to not have fun. We only have a certain number of minutes here on Earth, so we need to make sure we’re having fun.”

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at srupe@ insurancenewsnet.com.

Premium finance solutions and wealth management are top of mind for affluent clients and the businesses that serve them. Read up on the latest from trusted partners and finacial leaders in our special sponsored section.

Adapt or Die — HNW and UHNW Clients Need Intentional Coordination by Jeff Wick, First VP, Client Solutions, Cambridge Investment Research, Inc. PAGE 23

Legacy Planning with Non-Qualified Deferred Annuities by Allison Anne Hoyt, JD, CLU, VP Head of Advanced Sales Consulting, MassMutual Ascend PAGE 24

Adapt or Die – HNW and UHNW Clients Need Intentional Coordination

By Jeff Wick, First Vice President, Client Solutions, Cambridge Investment Research, Inc.

For years, the wealth management industry has buzzed about “holistic planning.” But for today’s high-net-worth (HNW) and ultra-high-net-worth (UHNW) clients, that popular phrase isn’t just something to aspire to; it has become table stakes. As the financial lives of HNW and UHNW clients have grown more complex, more interconnected, and more multigenerational, the old-school, fragmented advisory model simply can’t keep up.

The industry is at an inflection point, and firms that don’t adapt to the evolving expectations of highly affluent clients will be left behind. It’s adapt or die.

From Fragmentation to Intentional Coordination

One of the biggest pain points HNW and UHNW clients face today is fragmentation; it’s not uncommon for them to work with a dozen or more professionals. They have financial advisors, CPAs, estate attorneys, insurance specialists, investment managers, and others, but often with scant coordination among them. The solution isn’t about advisors becoming experts in everything – it’s about taking responsibility for orchestration.

Allow me to coin a new phrase: “intentional coordination.” In practice, that means an advisor acts as the quarterback. They coach, consult, and coordinate across disciplines to ensure decisions are made in concert, instead of in silos. What we see far too often is a fragmented approach, when clients really want a single point of contact and intentional coordination with all the professionals they rely on.

True holistic planning goes beyond portfolio construction. It comprises a wide range of interconnected considerations: tax strategy, estate planning, asset management, risk mitigation, philanthropic goals, access to alternative investments, business succession planning, and more.

Pressure Is Intensifying

While complexity has always existed in the HNW and UHNW space, expectations have rocketed over the past decade. New technologies have democratized investment tools, and once-exclusive strategies are now widely available. With lesser-funded families having access to many of the same tools and opportunities, HNW and UHNW clients are asking, “What’s unique for me?”

That demand extends to private capital opportunities, specialized tax planning, and access to networks that, realistically, a single advisor or even a single firm can’t provide in-house. At the same time, the migration of advisors from wirehouses to independent and RIA models

has forced independent firms to evolve. There’s been a lot of lip service in the independent space, but there’s a lack of firms actually building the infrastructure required to deliver intentional coordination and a seamless client experience.

At Cambridge, we made a deliberate decision several years ago to invest heavily in serving HNW and UHNW clients. That commitment led to the creation of our Private Client Solutions group with a focus on intentional coordination.

From the top down, we put real resources behind it. This included strategic partnerships with nationwide attorney and Personal CFO networks, enabling Cambridge advisors to access specialized expertise across all 50 states without trying to replicate it internally. While it’s not economically feasible for any one firm to have that expertise in-house, it’s feasible to intentionally coordinate it for the client.

Asking The Right Questions

Another differentiator in serving HNW and UHNW clients isn’t access to products or platforms; it’s the willingness to ask deeper, sometimes uncomfortable questions.

One of the simplest but most powerful questions we ask is, “What is this money for?” What’s for the spouse? What’s for the kids? What’s philanthropic? And what happens if something unexpected occurs?

Engaging in these conversations builds trust and positions advisors as true partners instead of transactional providers. When an advisor understands where clients want their money to go and why, it’s easier for them to align the client’s wealth with their long-term objectives.

The Bottom Line

Firms must recognize that many HNW and UHNW clients now expect their advisor to function much like a family CFO. They want greater visibility into their entire financial ecosystem and demand more sophistication and personalization. Firms that are reliant on surface-level offerings will fall short. And while there is a significant opportunity for firms willing to invest in intentional coordination, the future of wealth management is not willing to wait for firms that aren’t.

Legacy Planning with Non-Qualified Deferred Annuities

Using a Revocable Living Trust to Give the Gift of Guaranteed Income

by Allison Anne Hoyt, JD, CLU, VP Head of Advanced Sales Consulting, MassMutual Ascend

Two of the most common reasons retirees and pre-retirees engage a financial professional are to assess their level of retirement savings and to learn about options to save and invest outside of their employer-sponsored retirement plan.1 For those retirees who planned ahead and previously purchased a non-qualified deferred annuity (NQDA), some may find themselves in the enviable position of not needing their NQDA for their own retirement security. With these fortunate individuals, financial advisors can shift the conversation from retirement planning with NQDAs to legacy planning and discuss how to pass the NQDA to the next generation.

Imagine a parent (Suzy) who purchased an NQDA in her 50s for $100,000. Now in her 70s, Suzy has been happily retired for a few years and does not anticipate needing to access the nearly $265,000 in her NQDA. Suzy has two children, Mark and Mindy. Mindy is a public high school teacher and has access to a pension plan and has also saved for retirement through voluntary contributions to an employer plan. Mark has been an entrepreneur all of his life and has a spattering of thinly funded retirement accounts and IRAs with multiple custodians. After discussing the options with her financial professional, Suzy decides that the NQDA would better serve its purpose of providing guaranteed income in retirement for Mark.2

As the owner and annuitant of her NQDA, Suzy has a couple of different options to achieve her objective. Let’s explore a potentially tax efficient way for Suzy to make the transfer of her NQDA to her son, Mark.3

First, Suzy would fill out the appropriate paperwork at the insurance carrier to change the annuitant of the contract to Mark. By making Mark the annuitant, his life will ultimately be determinative of any future life-contingent annuity payout benefits provided by the NQDA so that future payments can provide him with lifetime income in retirement and so that, after the second step, only Mark’s death would trigger a death benefit. Second, Suzy would change the owner (and beneficiary) of the NQDA contract to her revocable living trust (RLT). It is important that Suzy complete these steps in this order because many NQDAs do not allow an annuitant change when the annuity contract

is owned by a non-natural person, like a trust. If allowed, an annuitant change when the annuity contract is owned by a non-natural person would require the NQDA to begin distributions or lose the tax deferral for its accumulated earnings.4 Note that generally there is neither income tax nor transfer tax consequences when an individual transfers an asset into or out of their RLT.5

Ultimately, as the trustee of her RLT, Suzy remains in control of the NQDA during her life — maintaining access to its account value in case she’s ever in a pinch or if her plans change. Further, Suzy could authorize a successor trustee to exercise ownership rights over the NQDA in case she is incapacitated in the future. For example, the successor trustee could change the investment allocations in Suzy’s fixed-indexed annuity (FIA) or registered index-linked annuity (RILA) as the successor trustee deemed prudent. Assuming that Mark is alive, Suzy’s death will not trigger a death benefit. This is because it is the life of the annuitant (Mark) that determines whether a death benefit is payable. The NQDA remains intact. Also, at Suzy’s death, her RLT will become an irrevocable, non-grantor trust. At this point, the NQDA is still owned by the trust, the trust is still the beneficiary of the NQDA, and Mark is still the annuitant.

“…financial advisors can shift the conversation from retirement planning with NQDAs to legacy planning and discuss how to pass the NQDA to the next generation.”

Allison Anne Hoyt

The ability to impact the financial security of multiple generations with a single asset is a gift that is worth giving...

Assuming Mark is a trust beneficiary, or a member of a class of trust beneficiaries, and certain other trust provisions are present, the successor trustee of the trust can make an in-kind distribution of the NQDA to Mark, allowing him to become the new owner of the annuity contract.6 Ideally, the terms of the trust will grant the trustee the discretion to distribute trust principal to Mark and the authority to make distributions of assets in-kind (which virtually all trustees will have).

If mandatory distributions depend on the age of a trust beneficiary, the trustee will have to ascertain whether/ when distribution of the entire NQDA would be possible. If discretionary distributions are limited to a HEMS (health, education, maintenance, or support) standard, the in-kind distribution of the NQDA may not be permitted.7

In most cases, the in-kind distribution of the NQDA from the trust to Mark should not be a taxable transaction, and the investment in the contract immediately prior to the distribution will be Mark’s carryover basis in the annuity contract. The taxation of non-grantor trusts can be a fairly intimidating topic. However, in-kind distributions of assets

from such trusts are a little less so. In Private Letter Ruling (PLR) 1999050151, the Internal Revenue Service found that an in-kind distribution of a NQDA from an irrevocable, non-grantor trust to a trust beneficiary was not a transfer of an annuity contract “without full and adequate consideration” and thus was not taxable.8

As the new owner of the NQDA, Mark should name an appropriate beneficiary and will be able to exercise all the rights of ownership.

Mark has inherited a valuable and versatile asset to aid him in his retirement, which can be annuitized to provide income for him for life based on his age and his life expectancy. It’s a wonderful gift to have received from his mother.9 And, depending on the type of NQDA and the success of Mark’s investment choices, the value of his NQDA will likely far surpass the $265,000 contract value at the time Suzy transfers it to her trust, and play a significant role in allowing Mark to achieve a safe and secure financial future.

The wealth transfer potential of NQDAs should not be overlooked. Suzy and her advisor were able to accomplish a valuable shift in the function of the NQDA in her overall financial plan: From retirement asset to legacy asset, and, in so doing, will provide a meaningful and substantial gift to her son. The ability to impact the financial security of multiple generations with a single asset is a gift that is worth giving, and one that will hopefully serve to reinforce family financial values that include responsibility, prudence, and generosity.

Find out more

To learn more about how we can help, scan the code or visit www.massmutualascend.com.

1. Employee Benefit Research Institute/Greenwald Retirement Confidence Survey 2025.

2. Note, if Suzy is currently married and has ever lived in a community property state during her marriage, spousal consent may be required to name a beneficiary other than her spouse.

3. This article assumes that Suzy has an “owner-driven” annuity contract. An “annuitant-driven” annuity contract may have different considerations. This article also assumes that the NQDA does not have a living benefit rider or death benefit rider that would be negatively affected by the proposed use of the NQDA. It is also important to ascertain with the insurance carrier that certain contract changes are allowable as different carriers may have different practices.

4. See I.R.C. § 72(s)(7).

5. See Rev. Rul. 85-13, 1985-1 C.B. 184.

6. If a charitable organization is also a beneficiary of the trust, an attorney should be consulted to determine whether the NQDA is eligible for tax deferral after Suzy’s death. See IRC 72(u)(1).

7. The trustee of the now irrevocable non-grantor trust should seek the opinion and guidance of an attorney to resolve the various legal, tax, and factual issues presented by making an in-kind distribution of a NQDA contract.

8. Although other taxpayers cannot rely upon PLRs, they do provide insight into the position of the IRS on various issues.

9. Alternatively, Mark may decide to name his spouse as a joint owner and/or as a joint annuitant and thus achieve other valuable planning objectives.

Global life insurance market to hit

$16.35T by 2033

The global life insurance market was valued at $7.59 trillion in 2024 and is expected to reach $16.35 trillion by 2033, growing at a compound annual growth rate of 8.9% from 2025 to 2033, according to an Astute Analytica report.

A substantial underinsured population is creating a powerful opportunity within the life insurance market, the report’s authors said. An estimated 102 million U.S. adults recognize a personal demand for more life insurance coverage. Key segments driving this demand include 50 million middle-income Americans and 54 million women who have identified specific gaps in their financial protection.

The current scale is already vast, with 134.93 million individual policies in force and more than 118 million people covered by group plans in 2024. These figures point to a widespread and acknowledged demand for coverage, signaling a clear runway for growth.

LIMRA PREDICTS GROWTH IN LIFE PREMIUM

After several years of remarkable expansion, the U.S. life insurance industry enters 2026 with both strong momentum and a shifting economic landscape. LIMRA’s 2026 forecast suggests that while growth will continue, it will be moderated as consumers’ concern about economic uncertainty increases.

In announcing its optimistic forecast, LIMRA cited several factors fueling future premium growth, including heightened awareness of the need for life insurance following the pandemic and favorable economic conditions boosting the appeal of indexed universal life and variable universal life products.

In addition, LIMRA said innovation in products aimed at the middle market and advances in distribution also will lead to premium growth.

NAIC LOOKS AT EVALUATING INSURERS’ USE OF AI

A National Association of Insurance Commissioners group moved closer to launching a multistate pilot of a new artificial intelligence system evaluation tool, a move that industry trade groups have criticized.

The AI system evaluation tool is expected to enter a pilot phase, with Colorado, Maryland, Louisiana, Virginia, Connecticut, Pennsylvania, Wisconsin, Florida, Rhode Island, Iowa and Vermont participating.

Insurance companies have steadily expanded their use of AI over the past decade, moving from basic automation to more sophisticated applications throughout the insurance value chain. More recently, generative AI and advanced automation have reshaped how insurers engage with customers and manage internal operations.

IUL makes up 25% of new life insurance premiums in the U.S.

Source: LIMRA

We think this year’s narrative theme is one of strategic adaptation.”

—

Scott Hawkins, head of insurance research, Conning

Through it all, NAIC regulators have struggled to establish guardrails to preserve fairness, transparency and consumer protection.

HOW LIFE INSURANCE IS GOING HIGH TECH

Life insurers are increasingly turning to technology tools to help their policyholders live longer, healthier lives and, in turn, help boost the insurers’ bottom lines.

Companies such as John Hancock and MassMutual have spent the past few years looking at programs to help improve their policyholders’ health

MassMutual created its Health and Wellness Program in 2023. This year, it is looking to offer the program as a rider to all its eligible life insurance policyowners. MassMutual also said about 20% of the policyholders who took genetic testing learned that they were predisposed to certain medical conditions, such as heart disease.

Meanwhile, John Hancock has been offering policyholders wellness incentives through its John Hancock Vitality program for more than a decade. The company offered Vitality after observing that leading causes of death in the U.S. were diseases often influenced by lifestyle, such as diabetes, stroke and heart disease. About 80% of John Hancock policyholders who participate in the program said their health was about the same or better than it was 10 years ago.

Celebrating 60 Years of Serving Medicare Clients