Prepared by Ben Albright President & CEO

Prepared by Ben Albright President & CEO

Source: © A.M. Best Company Used by Permission

You are being provided this 2023 Louisiana Annual P&C Marketplace Summary covering the Louisiana property and casualty (P&C) insurance marketplace as a benefit of your membership in the Independent Insurance Agents & Brokers of Louisiana.

What follows is a graphic and numeric presentation of the Louisiana P&C industry data from an independent agent’s perspective. The data used is the most recently available from A.M. Best Company. For this Summary that is the annual data for 2022

This Summary emphasizes direct premiums, direct losses, and the associated direct underwriting results before reinsurance. Also included is data from nearly 3,000 insurers that are domiciled in the United States, and if they have written premiums in Louisiana then their data is incorporated. As independent agents, this is the marketplace experience for the business we place (or compete against) for our clients in Louisiana

This 2023 Louisiana Annual P&C Marketplace Summary provides you with the following important information on the Louisiana P&C Marketplace: Premiums for all 32 P&C lines of business in Louisiana, The Top 10 lines for independent agents, Growth rates, Loss ratios, Penetration rates and trends, Commission rates, and Surplus lines utilization rates

United States national data on each of the above is also furnished, to give perspective

For those readers interested in line of business details, a separate page is provided for each of the lines of business that independent agents work with most in Louisiana. For each of these lines of business data on premiums, loss and combined ratios, top insurers, surplus lines utilization rates and other facts are provided.

For detailed information on approaches taken in the research, formulation, and presentation of this 2023 Louisiana P&C Marketplace Summary, four appendices are provided for the reader.

Louisiana Premiums: All 32 P&C Lines of Business

Louisiana Top 10 Independent Agent Lines of Business.

Louisiana Loss Ratios.

Louisiana Premium Growth Rates

Louisiana Penetration Rates.

Louisiana Commissions Rates

Louisiana Surplus Lines.

Louisiana Line of Business Details.

Total All P&C Lines of Business.

Aircraft (all perils).

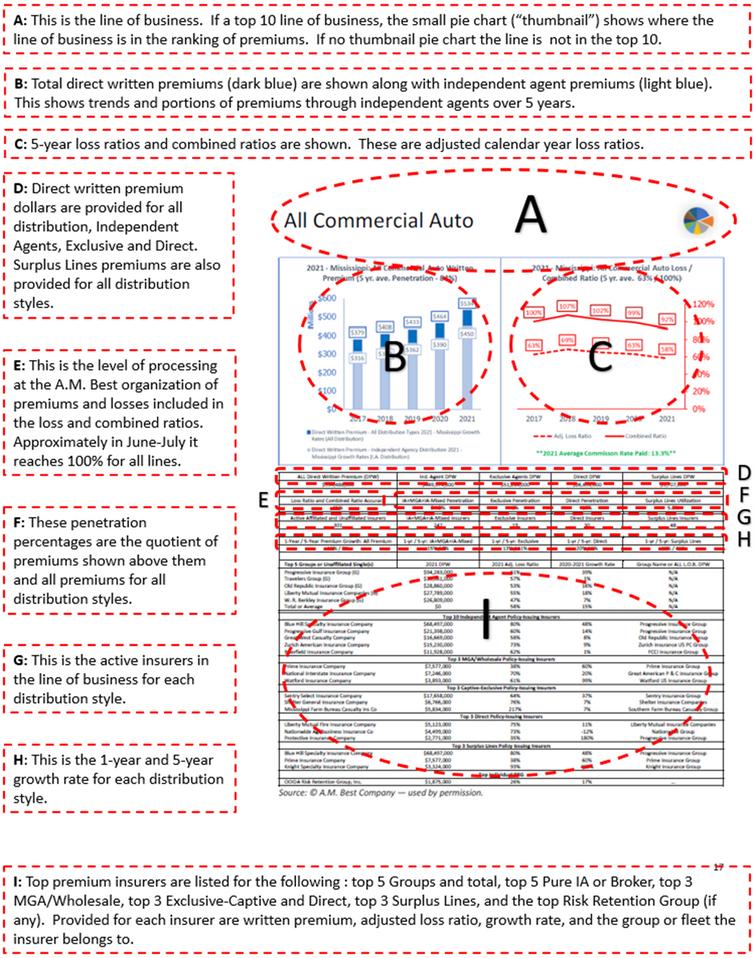

All Commercial Auto

All Private Passenger Auto.

Allied Perils Only.

Boiler & Machinery.

Burglary & Theft.

Commercial Multi-Peril Earthquake.

Excess

Farmowners

The below chart shows all 32 P&C lines of business that P&C insurers are required to report on, state-bystate, in their annual statement. They are listed in alphabetical order and in all subsequent tables/charts and graphs in this Summary. Of these 32 lines, 26 are primarily focused on by independent agents in Louisiana and are emphasized above with an asterisk (*).

For more detail Appendix #1: All Lines of Business-Additional Details provides further data on the premiums, loss ratios, growth and penetration of these 32 P&C lines of business.

Accident&Health

Aggregate Write-ins

*Aircra� (all perils)

*All Commercial Auto

*All Private Passenger Auto

*Allied Perils Only

*Boiler and Machinery

*Burglary and The�

*Commercial Mul�-Peril Credit

*Earthquake

*Excess Workers' Comp

*Farmowners Mul�-Peril

*Federal Flood

*Fidelity

Financial Guaranty

*Fire Peril Only

*Homeowners Mul�-Peril

*Inland Marine

*Interna�onal

*Medical Malprac�ce

Mortgage Guaranty

*Mul�-Peril Crop

*Ocean Marine

*Other Liability (Claims-made)

*Other Liability (Occurrence)

*Private Crop

*Private Flood

*Products Liability

*Surety Warranty

*Workers' Compensa�on

$87,623,000

$18,599,000

$50,864,000

$1,049,954,000 $4,963,961,000

$923,740,000

$53,014,000

$5,877,000

$33,049,000

$695,381,000

$7,717,000

$58,690,000

$16,075,000

$259,324,000

$14,634,000

$1,086,000

$578,891,000

$583,062,000

$3,000

$116,083,000

$63,412,000 $154,389,000 $171,833,000 $299,807,000 $1,016,247,000

$5,503,000

$28,921,000

$53,098,000

$152,499,000

$6,907,000

$874,832,000

$2,465,855,000

To provide perspective, in the table below is comparative data on Louisiana P&C premiums; and how Louisiana premiums compare to the United States in total, including some common groupings of lines of business, on a per capita basis. Also provided are the smallest/lowest state, and largest/highest state for either total premiums, or per capita premiums.

Each of these groupings are organized as follows:

Total (All Lines) includes premiums for all 32 P&C lines of business; Personal Lines includes All Private Passenger Auto, and Homeowners Multi-Peril; Commercial Lines includes All Commercial Auto, Commercial Multi-Peril, Other Liability (ClaimsMade), Other Liability (Occurrence), Products Liability, and Workers’ Compensation; and Agricultural Lines includes Farmowners Multi-Peril, Multi-Peril Crop, and Private Crop.

In each case, the basis of the per capita comparative premium uses the most recent population estimate from the U S Census

Billion $3,227 (Rank is 7 of 51) $1,619 (Rank is 3 of 51)

(Rank is 18 of 51)

Billion)

$861,485,443,000 ($16.9 Billion) $2,585 $1,233

$860 $77

(Rank is 29 of 51)

Source: © A.M. Best Company used by permission and U.S. Census Bureau, Population Division and Annual Estimates of Resident Population (Release Date: December 2022)

The below pie charts show which lines of business are the most important to independent agents, based on direct written premiums The top 10 lines of business are shown in each pie chart, with premiums from all other lines of business combined in the “All Other” pie section.

Data for Louisiana is used in the top two pie charts, with the lines of business ordered by rank order of premiums through independent agents in Louisiana. The left pie chart includes premiums only through independent agents. The right pie chart adds all premiums from all distribution styles included in each pie section

For comparison, data for the United States is used for the second two pie charts. The rank-order for the United States pie charts is based on premiums through independent agents in all of the United States.

For further information Appendix #2: Distribution Style Classifications gives the reader a detailed explanation of the classification of insurers into distribution styles, based on insurer reported marketing types Also included in Appendix #2 is additional data on premiums by line of business for each distribution style, as well as the Top 10 insurers for each distribution style

To illustrate how Louisiana relates to other states, below is a table of comparative data on all 32 P&C lines of business The top 10 lines of business shown for Louisiana are the same as those shown in the previous pie chart. Then, data on top lines of business in other states is provided.

As can be seen in the third column labeled “Percent of Time #1 LOB (All States),” the #1 line of business is most often All Private Passenger Auto which equals 73% of the time, meaning it is #1 in 37 states. However, that is not the case in every state. And the fourth column labeled “Percent of Time in Top 10 LOB (All States)” shows that some lines of business are always in a state’s top 10 lines of business For example, Commercial Multi-Peril is in every state’s Top 10 lines of business

Line of Business

Accident & Health

Aggregate Write-ins

Aircraft (all perils)

All Commercial Auto

All private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Credit Earthquake

Excess Workers’ Comp

Farmowners Multi-Peril

Federal Flood

Fidelity

Financial Guaranty

Fire Peril Only

Homeowners Multi-Peril

Inland Marine

International

Medical Malpractice

Mortgage Guaranty

Multi-Peril Crop

Ocean Marine

Other Liability (Claims-made)

Other Liability (Occurrence)

Private Crop

Private Flood

Products Liability

Surety

Warranty

Workers’ Compensation

Louisiana LOB Ranking

#5-LOB

#1-LOB

#7-LOB

#6-LOB

#8-LOB

#2-LOB

#9-LOB

#10-LOB

#3-LOB

#4-LOB

Source: © A M Best Company used by permission

Percent of Time #1 LOB (All States)

of Time in Top 10 LOB (All States)

Aircra� (all perils)

Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary&The�

Commercial Mul�-Peril

Earthquake

ExcessWorkers'Comp

Farmowners Mul�-Peril

Federal Flood Fidelity

Fire Peril Only

Homeowners Mul�-Peril

Inland Marine

Medical Malprac�ce

Mul�-Peril Crop

Ocean Marine

Other Liabili�es (Claims-Made)

Other Liability (Occurrence)

Private Crop

Private Flood

Product Liability

Surety

Workers' Compensa�on Total (All Lines)

Source: © A.M. Best Company used by permission. (International not shown, less than 5 years data is available)

+

The first table below shows data which illustrates Louisiana's 1-Year and 5-Year average loss ratios, as compared to the United States. Also provided is the state with the highest, and the lowest 1-Year and 5Year loss ratios.

For additional perspective, the second table shows average loss ratios for the 26 P&C lines of business focused on by independent agents in Louisiana, as compared to United States averages

All Lines Average Loss Ratio

Line of Business Average Loss Ratios

Aircraft (all perils)

All Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Earthquake

Excess Workers' Comp

Farmowners Multi-Peril

Federal Flood

Fidelity

Fire Peril Only

Homeowners Multi-Peril

Inland Marine

International

Medical Malpractice

Multi-Peril Crop

Ocean Marine

Other Liability (Claims-made)

Other Liability (Occurrence)

Private Crop

Private Flood

Products Liability

Surety

Workers' Compensation Louisiana

Source: © A.M. Best Company used by permission.

United States 1-

The below bar chart shows the percentage change in direct written premiums for the 26 P&C lines of business focused on by independent agents. The 1-year growth rate is the percentage change in premiums from 2021 to 2022. The 5-year growth rate is the constant percentage from the first year to the last year, so the first year (2018) premium exactly equals the direct written

in 2022 The Total (IA-Focused Lines) shown last is the average

rates for the 26

lines of business focused on by independent agents

Aircra� (all perils)

All Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary&The�

Commercial Mul�-Peril

Earthquake

ExcessWorkers'Comp

Farmowners Mul�-Peril

Federal Flood Fidelity

Fire Peril Only

Homeowners Mul�-Peril

Inland Marine

Medical Malprac�ce

Mul�-Peril Crop

Ocean Marine

Other Liabili�es (Claims-Made)

Other Liability (Occurrence)

Private Crop

Private Flood

Product Liability

Surety

Workers' Compensa�on

(IA-Focused Lines)

Source: © A M Best Company used by permission (International not shown, as less than 5 years data is available)

The first table below shows average growth rate data, provide perspective on Louisiana's 1-year and 5year premium growth rates, as compared to the United States Also provided is the state with the fastest, and the slowest 1-year and 5-year growth rates.

The second table provides the 1-year and 5-year average line of business premium growth rates for the 26 P&C lines of business focused on by independent agents in Louisiana, as compared to United States averages.

Total (IA-Focused Lines) Average

Line of Business Average Average Growth

(all perils)

All Commercial Auto

Boiler & Machinery

Louisiana 1-Year

Louisiana 5-Year

United States 1-

Source: © A.M. Best Company used by permission.

The clustered bar chart below shows 5 years of penetration rates for the top 10 lines of business, written through independent agents, in order of direct written premium The final cluster of bars labeled Total (IA-Focused Lines) is the trend for all 26 P&C lines of business focused on by independent agents in Louisiana.

The formula shown below the clustered bar chart shows how the percentages are calculated, based on premiums written through independent agents in Louisiana, divided by all premiums for each line of business in Louisiana Independent Agent Top 10 Lines of Business: 5-Year Penetration Rates

The first table below shows comparative data to give perspective on Louisiana's independent agent penetration rates Provided are the 1-year and 5-year average penetration rates For additional perspective, the state with the highest, and the lowest independent agent penetration rate is shown.

The second table shows penetration rates for the 26 P&C lines of business focused on by independent agents in Louisiana, as compared to the United States averages.

Total (IA-Focused Lines)

Average Penetration

Line of Business Average

Average Penetration Rates

Aircraft (all perils)

All Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Earthquake

Excess Workers' Comp

Farmowners Multi-Peril

Federal Flood

Fidelity

Fire Peril Only

Homeowners Multi-Peril

Inland Marine

International

Medical Malpractice

Multi-Peril Crop

Ocean Marine

Other Liability (Claims-made)

Other Liability (Occurrence)

Private Crop

Private Flood

Products Liability

Surety

Workers' Compensation

Louisiana 1-Year

Louisiana 5-Year

United States 1Year

Source: © A.M. Best Company used by permission.

Below are 5-year penetration trends in Louisiana shown for distribution styles and 4 groupings of lines of business If the reader needs a reminder of what is included in these lines of business groupings, refer to the Louisiana Total Premiums Comparisons section on page 4.

The below bar chart shows the commission rate paid by all insurers for 26 independent agent-focused P&C lines of business, in alphabetical order Shown last (Total IA-Focused Lines) is the average commission paid on all lines of business focused on by independent agents.

The formula below the bar chart shows how commission percentages are calculated, where the commission % equals the line of business direct and contingent commissions, divided by the line of business written premium.

Homeowners

The first table below gives comparative data to provide perspective on Louisiana's 1-year commission rates Provided is the overall average commission for all lines of business in Louisiana, compared with the United States. For additional perspective, the state with the highest, and the lowest 1-year commission rate is shown.

The second table gives 1-year commission data for the 26 P&C lines of business focused on by independent agents in Louisiana, as compared to the United States.

Total (IA-Focused Lines)

Average Commission

Line of Business Average

Commission Rates

Aircraft (all perils)

All Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Earthquake

Excess Workers' Comp

Farmowners Multi-Peril

Federal Flood

Fidelity

Fire Peril Only

Homeowners Multi-Peril

Inland Marine

International

Medical Malpractice

Multi-Peril Crop

Ocean Marine

Other Liability (Claims-made)

Other Liability (Occurrence)

Private Crop

Private Flood

Products Liability Surety

Source: © A.M. Best Company used by permission.

United States 1Year Commission

Below is information on surplus lines in Louisiana The pie chart shows the Top 10 lines of business by percentage of all surplus lines premiums in Louisiana for 2022

Next is the total surplus lines premiums in Louisiana for 2018 to 2022, with the corresponding percentage provided of those surplus lines premiums to all P&C premiums in Louisiana.

Readers should note the below data does not include alien insurers (insurers not domiciled in one of the 51 states) If alien premiums were included, it would increase the amount of surplus lines premiums by about 1 percentage point An example of an alien surplus lines insurer is Lloyds of London Alien insurer data is not included, as it is not tracked as consistently across states nor in the same time-frame.

The first table below gives comparative data to give perspective on Louisiana's surplus lines utilization rates Provided is the average 1-year and 5-year surplus lines utilization rate in Louisiana, as compared to the United States. For additional perspective, the state with the highest, and the lowest average 1-year and 5-year surplus lines utilization rates is shown.

The second table gives surplus lines utilization rates for the 26 P&C lines of business focused on by independent agents in Louisiana, as compared to the United States.

All Lines Surplus Lines Utilization Rates

Line of Business Surplus Lines Utilization Rates

Aircraft (all perils)

All Commercial Auto All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Earthquake

Excess

Louisiana 1-Year

Louisiana 5-Year

United States 1-

Source: © A.M. Best Company used by permission.

The following pages provide in-depth detail on the 26 P&C lines of business focused on by independent agents in Louisiana. The lines of business are presented in alphabetical order

The facts and details provided on the following pages, for each line of business focused on by independent agents in Louisiana include the following

A bar chart of 5-years data on premiums for all distribution types (dark blue), and premiums written through independent agents (light blue) For the premium chart the classification of premiums through independent agents is based on a categorization of agents by distribution style. The categorization approach is explained in Appendix #2: Distribution Style Classifications 5-year line charts, showing the loss ratio (dashed red line) and combined ratio (solid red line)

The direct written premium for independent agents, exclusive-captive agents, and direct insurers, with the percentage of the direct written premium to the total premium. Also, surplus lines premiums through any distribution style, with its corresponding percentage of all premiums

The number of active insurers, with the number of independent agent, exclusive-captive agent and direct insurers for each line of business Also, the number of active surplus lines insurers 1-year and 5-year growth rates for independent agent, exclusive-captive and direct insurers. The percentage premiums through insurers licensed as surplus lines is also provided

The top 5 insurer groups in each line of business, with that group’s premiums, 1-year loss ratio, and 1year growth rate. Groups of insurers sometimes are made up of multiple policy-issuing insurers in a particular group, but it can also be only one policyissuing insurer in that group.

Listed after the top insurer groups are the top policy-issuing insurers distributing insurance through independent agents, exclusive-captive agents, direct insurers, surplus lines insurers, and the top risk retention group (if any) for the line of business For each policy-issuing insurer the premium for the insurer in that line of business is shown with the 1-year loss ratio and 1-year growth rate.

As you scroll through the following pages, take notice if a small pie chart thumbnail is presented at the upperright. If there is a pie chart present, that means the product is in the top 10 lines of business for independent agents in Louisiana A broken-out pie slice in that small pie chart represents the position of that line of business and its rank-order, based on independent agent premium volume The rank-order is based on direct written premium and corresponds to the pie chart slice highlighted on Page 5 of this 2023 Louisiana P&C Marketplace Summary.

For further clarification Appendix #3: NAIC Line of Business Definitions furnishes the reader with the definitions set forth and used by the NAIC for each line of business

And Appendix #4: Line of Business Facts Visual Reference gives the reader a visual guide to the details presented for each line of business

Louisiana: Total (All Lines) Written Premium (5 yr. ave. Penetration - 54%)

Louisiana: Total (All Lines) Loss/Combined Ratio (5 yr. ave. 90%/125%)

5 Pure Independent Agent-Broker

Louisiana: Aircraft (All Perils) Written Premium (5 yr. ave. Penetration - 98%)

Louisiana: Aircraft (All Perils) Loss/Combined Ratio (5 yr. ave. 60%/96%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: All Commercial Auto Written Premium (5 yr. ave. Penetration - 78%)

Louisiana: All Commercial Auto Loss/Combined Ratio (5 yr. ave. 84%/124%)

(G) Berkshire Hathaway Insurance Group (G) Total or

Top 5 Pure Independent Agent-Broker Policy Issuing

Louisiana: All Private Passenger Auto Written Premium (5 yr. ave. Penetration - 25%)

Louisiana: All Private Passenger Auto Loss/Combined Ratio (5 yr. ave. 68%/95%)

Louisiana: Allied Perils Only Written Premium (5 yr. ave. Penetration - 25%)

Louisiana: Allied Perils Only Loss/Combined Ratio (5 yr. ave. 218%/253%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Boiler & Machinery Written Premium (5 yr. ave. Penetration - 95%) Louisiana: Boiler & Machinery Loss/Combined Ratio (5 yr. ave. 87%/109%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Burglary & Theft Written Premium (5 yr. ave. Penetration - 79%)

Louisiana: Burglary & Theft Loss/Combined Ratio (5 yr. ave. 32%/65%)

Top 5 Pure Independent Agent-Broker Policy

Louisiana: Commercial Multi-Peril Written Premium (5 yr. ave. Penetration - 83%)

Louisiana: Commercial Multi-Peril Loss/Combined Ratio (5 yr. ave. 149%/195%)

State Farm Group (G)

Mutual Insurance Companies (G)

Corporation Group (G) Chubb INA Group (G) Travelers Group (G)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Earthquake Written Premium (5 yr. ave. Penetration - 82%) Louisiana: Earthquake Loss/Combined Ratio (5 yr. ave. 3%/27%)

Sompo Holdings US Group (G)

Markel Corporation Group (G) Total or

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Excess Workers’ Comp Written Premium (5 yr. ave. Penetration - 98%)

Louisiana: Excess Workers’ Comp Loss/Combined Ratio (5 yr. ave. 43%/80%)

5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Farmowners Multi-Peril Written Premium (5 yr. ave. Penetration - 39%) Louisiana: Farmowners Mutli-Peril Loss/Combined Ratio (5 yr. ave. 113%/148%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Federal Flood Written Premium (5 yr. ave. Penetration - 72%)

Louisiana: Federal Flood Loss/Combined Ratio (5 yr. ave. 75%/116%)

Top 5 Pure Independent Agent-Broker

Louisiana: Fire Peril Only Written Premium (5 yr. ave. Penetration - 81%)

Louisiana: Fire Peril Only Loss/Combined

(5 yr. ave. 159%/194%)

Top 5 Groups or Unaffiliated Single(s)

Starr International Group (G)

Louisiana Citizens Property Ins Corp

Core Specialty Insurance Group (G)

Berkshire Hathaway Insurance Group (G)

Dorinco Reinsurance Company

Total or Average

Louisiana:

Louisiana: Inland Marine Written Premium (5 yr. ave. Penetration - 78%)

Louisiana: Inland Marine Loss/Combined Ratio (5 yr. ave. 58%/94%)

Top 5 Pure Independent Agent-Broker Policy Issuing

Louisiana: International Written Premium (5 yr. ave. Penetration)

Penetration 0% Direct Insurers

1-yr / 5-yr: Direct #DIV/0!

Louisiana: Medical Malpractice Written Premium (5 yr. ave. Penetration - 92%)

Louisiana: Multi-Peril Crop Written Premium (5 yr. ave. Penetration - 100%)

Louisiana: Multi-Peril Crop Loss/Combined Ratio (5 yr. ave. 117%/136%)

QBE North America Insurance Group (G) Chubb INA Group (G) Sompo Holdings US Group (G)

Insurance US PC Group (G) FMH Insurance Group (G)

Louisiana: Ocean Marine Crop Written Premium (5 yr. ave. Penetration - 96%)

Louisiana: Ocean Marine Crop Loss/Combined Ratio (5 yr. ave. 80%/125%)

Louisiana: Other Liability (claims-made) Written Premium (5 yr. ave. Penetration - 94%)

Louisiana: Other Liability (claims-made) Loss/Combined Ratio (5 yr. ave. 80%/125%)

Louisiana: Other Liability (Occurrence) Written Premium (5 yr. ave. Penetration - 88%)

Louisiana: Other Liability (Occurrence) Loss/Combined Ratio (5 yr. ave. 63%/105%)

Travelers Group (G) Fairfax Financial (USA) Group (G) Chubb INA Group (G) W. R. Berkley Insurance Group (G) Nationwide Group (G) Total or

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Private Crop Written Premium (5 yr. ave. Penetration - 100%)

Louisiana: Private Crop Loss/Combined Ratio (5 yr. ave. 194%/235%)

QBE North America Insurance Group (G)

Sompo Holdings US Group (G)

Chubb INA Group (G)

American International Group (G)

Great American P & C Insurance Group (G)

Total or Average

Louisiana: Private Flood Written Premium (5 yr. ave. Penetration - 76%)

Louisiana: Private Flood Loss/Combined Ratio (5 yr. ave. 24%/48%)

Assurant

Group (G) Berkshire Hathaway Insurance Group (G) Zurich Insurance US PC Group (G) Arch Insurance Group (G) Total or

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Products Liability Written Premium (5 yr. ave. Penetration - 96%) Louisiana: Products Liability Loss/Combined Ratio (5 yr. ave. 54%/107%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

Louisiana: Surety Written Premium (5 yr. ave. Penetration - 86%) Louisiana: Surety Loss/Combined Ratio (5 yr. ave. 54%/107%)

Financial (USA) Group (G)

Louisiana: Workers’ Compensation Written Premium (5 yr. ave. Penetration - 95%) Louisiana: Workers’ Compensation Loss/Combined Ratio (5 yr. ave. 51%/94%)

Top 5 Pure Independent Agent-Broker Policy Issuing Insurers

All P-C Lines of P-C Business

Accident & Health

Aggregate Write-ins

Aircraft (all perils)

All Commercial Auto

All Private Passenger Auto

Allied Perils Only

Boiler & Machinery

Burglary & Theft

Commercial Multi-Peril

Credit

Earthquake

Excess Workers' Comp

Farmowners Multi-Peril

Federal Flood Fidelity

Financial Guaranty Fire Peril Only

Homeowners Multi-Peril

Inland Marine

International

Medical Malpractice

Mortgage Guaranty

Multi-Peril Crop

Ocean Marine

Other Liability (Claims-made)

Other Liability (Occurrence)

Private Crop

Private Flood

Products Liability

Surety

Warranty

Workers' Compensation

Total (All Lines)

Total (IA-Focused Lines)

3,000 116,083,000 63,412,000 154,389,000

Source: © A M Best Company used by permission (Note: Independent Agentfocused lines of business are bold and underlined, and the total for just those lines is provided in the last line of the compendium, Total (IA-Focused Lines)

This Louisiana P&C Marketplace Summary classifies insurers into distribution styles based on the insurer’s reported marketing type(s) These marketing types are provided as part of what is known as a “Galley Process,” and made available by A M Best as part of various insurer attributes in their Best’s Financial Suite Below are the various marketing types reported by insurers in 2022

Marketing Types:

Affinity Group Marketing

Bank

Broker

Career Agent

Direct Response

Exclusive/Captive Agent

General Agent

Inactive

Independent Agency

Internet

Managing General Agent

Not Available

Other

Other Agency

Other Direct

Worksite Marketing

Distribution Style Classifications:

The approach used by this P&C Marketplace Summary is to take each insurer’s reported marketing type and put data from that insurer into one of 6 distribution styles Some insurer classifications are obvious and straight forward Others less so When insurers list multiple marketing types, more weight is given to the marketing type listed first that closest aligns to each distribution style About 10% of insurers have “Not Available” for their listed marketing type These insurers represent less than 1% of all written premiums in 2022, and those insurers are categorized as “Other ”

There are 6 distribution styles into which each insurer is categorized in this Summary: (1) Pure IA or Broker, (2) MGA/Wholesale, (3) IA-Mixed, (4) Exclusive-Captive, (5) Direct, and (6) Other When general independent agent distribution figures are needed, data for the first three distribution styles are combined, and are of the most interest. The remaining three distribution styles stand on their own. Other industry analysis of distribution and penetration may vary in how the impact of insurer distribution choices are determined, but generally the results are similar to the approach taken in this Summary.

By controlling the distribution style classification in this way for each insurer, flexibility is attained in providing data that matches an independent agent’s view of the marketplace. It allows determination of approximate penetrations of the distribution styles by line of business. It also allows creating lists of insurers by line of business for each distribution style.

Featured in the table below are the premiums as calculated based on the proprietary classification of insurers into distribution styles Premiums are shown first for each line of business and All Distribution styles combined, and then for the 6 distribution styles just listed above separately Bold and underlined in the table below are the 26 P&C independent agent-focused lines of business The total for those 26 lines is provided in the last line of the table,

Total (IA-Focused Lines)

2022 - Louisiana: All Lines of Business Distribution Style - DPW (Premiums) in Millions of Dollars

Louisiana All P-C Lines of P-C

Business Accident & Health

Write-ins

(all perils)

Source: © A.M. Best Company used by permission. (Note: Independent Agent-focused lines of business are bold and underlined, and the total for just those lines is provided in the last line of the compendium, Total (IA-Focused Lines)

To provide examples of the classification approach results, the top insurers in each distribution style are shown below with the reported marketing type and premiums for Louisiana

LouisianaPolicy-IssuingInsurers

ProgressiveSecurityInsuranceCompany

LouisianaWorkers'CompensationCorp

ImperialFireandCasualtyInsuranceCo

ContinentalCasualtyCompany

SafecoInsuranceCompanyofOregon

ProgressivePropertyInsuranceCompany

NationalUnionFireInsCoPittsburghPA

ForemostInsuranceCoGrandRapids,MI

ScottsdaleInsuranceCompany

TravelersPropertyCasualtyCoofAmer

LouisianaPolicy-IssuingInsurers

GoAutoInsuranceCompany

SureChoiceUnderwriitersReciprocalExch

WrightNationalFloodInsuranceCompany

HoustonSpecialtyInsuranceCompany

AlliedTrustInsuranceCompany

EvanstonInsuranceCompany

CentauriNationalInsuranceCompany

OldAmericanIndemnityCompany

US SpecialtyInsuranceCompany

ClearBlueSpecialtyInsuranceCompany

LouisianaPolicy-IssuingInsurers

LouisianaCitizensPropertyInsCorp

FactoryMutualInsuranceCompany

AmericanModernProperty&CasualtyIns

LAMMICO

AmericanAgri-BusinessInsuranceCompany

UnitedFinancialCasualtyCompany

ChurchMutualInsuranceCompany,SI

AutomobileClubInter-InsuranceExchange

AffiliatedFMInsuranceCompany

PrincetonExcess&SurplusLinesInsCo

LouisianaPolicy-IssuingInsurers

StateFarmMutualAutomobileInsCo

StateFarmFireandCasualtyCompany

AllstatePropertyandCasualtyInsCo

AllstateInsuranceCompany

LouisianaFarmBureauCasualtyInsCo

ShelterMutualInsuranceCompany

AmericanNationalProperty&CasualtyCo

AllstateIndemnityCompany

LibertyInsuranceUnderwriters Inc

SouthernFarmBureauCasualtyInsCo

LouisianaPolicy-IssuingInsurers

ProgressivePaloverdeInsuranceCompany

GEICOCasualtyCompany

LouisianaFarmBureauMutualInsCo

UnitedServicesAutomobileAssociation

GEICOSecureInsuranceCompany

USAAGeneralIndemnityCompany

USAACasualtyInsuranceCompany

LibertyPersonalInsuranceCompany

GarrisonPropertyandCasualtyInsCo

LibertyMutualFireInsuranceCompany

LouisianaPolicy-IssuingInsurers

BridgewayInsuranceCompany

BerkshireHathawaySpecialtyInsCo

EssentGuaranty Inc

AccreditedSpecialtyInsuranceCompany

SpinnakerSpecialtyInsuranceCompany

WestfieldSpecialtyInsuranceCompany

UplandSpecialtyInsuranceCompany

NationalMortgageInsuranceCorporation

GreenwichInsuranceCompany

Top10InsurersClassifiedasIAorBroker-DPW(Premiums)inMillionsofDollars

AllstateInsuranceGroup

CNAInsuranceCompanies

LibertyMutualInsuranceCompanies

Top10InsurersClassifiedasMGA/Wholesale-DPW(Premiums)inMillionsofDollars

SkywardSpecialtyInsuranceGroup

MarkelCorporationGroup

Top10InsurersClassifiedasIA-Mixed-DPW(Premiums)inMillionsofDollars

Group

FMGlobalGroup

Munich-AmericanHoldingCorpCompanies

LAMMICOGroup

SompoHoldingsUSGroup

ProgressiveInsuranceGroup

ChurchMutualInsuranceGroup

AutoClubEnterprisesInsuranceGroup

FMGlobalGroup

Munich-AmericanHoldingCorpCompanies

ManagingGeneralAgent,IndependentAgency

ManagingGeneralAgent

Other DirectResponse,Broker

WorksiteMarketing

DirectResponse,IndependentAgency

OtherAgency

IndependentAgency,DirectResponse

DirectResponse,IndependentAgency

IndependentAgency,Exclusive/CaptiveAgent Broker,DirectResponse

AffinityGroupMarketing,Broker

Top10InsurersClassifiedasExclusive-Captive-DPW(Premiums)inMillionsofDollars

Group

StateFarmGroup

StateFarmGroup

AllstateInsuranceGroup

AllstateInsuranceGroup

SouthernFarmBureauCasualtyGroup

ShelterInsuranceCompanies

AmericanNationalProp&CasGroup

AllstateInsuranceGroup

LibertyMutualInsuranceCompanies

SouthernFarmBureauCasualtyGroup

Top10InsurersClassifiedasDirect-DPW(Premiums)inMillionsofDollars

Group ProgressiveInsuranceGroup

BerkshireHathawayInsuranceGroup

USAAGroup

BerkshireHathawayInsuranceGroup

USAAGroup USAAGroup

LibertyMutualInsuranceCompanies

USAAGroup

LibertyMutualInsuranceCompanies

Top10InsurersClassifiedasOther-DPW(Premiums)inMillionsofDollars

BerkshireHathawayInsuranceGroup

EssentGuarantyGroup

RandallGroup

SpinnakerInsuranceGroup

WestfieldGroup

EnduranceAssuranceCorporation Group Munich-AmericanHoldingCorpCompanies

Source: © A M Best Company used by permission, and the

ListedMarketingType

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent

Exclusive/CaptiveAgent DirectResponse

Exclusive/CaptiveAgent

ListedMarketingType

DirectResponse DirectResponse DirectResponse DirectResponse

DirectResponse DirectResponse DirectResponse DirectResponse DirectResponse

DirectResponse

ListedMarketingType Inactive

Definition

Explained coverage written in that do not fit elsewhere

Coverage for aircraft (hull) and their contents; aircraft owners’ and aircraft manufacturers’ liability to passengers, airports and other third parties

Commercial Auto No-Fault (Personal Injury Protection) Other Commercial Auto Passenger Liability (Include-BI, PD, UM and UIM) Commercial Auto Physical Damage

Private Passenger Auto No-Fault (Personal Injury Protection) Other Private Passenger Auto Liability (Include-BI/PD/UM and UIM) Private Passenger Auto Physical Damage

Coverage for the failure of boilers, machinery and electrical equipment Benefits include: (i) property of the insured that has been directly damaged by the accident (ii) Costs of temporary repairs and expediting expenses (iii) Liability for damage to the property of others

Coverage for property taken or destroyed by breaking and entering the insured’s premises, burglary or theft, forgery or counterfeiting, fraud, kidnap and ransom, and off-premises exposure

A contract for a commercial enterprise that packages two or more insurance coverages protecting an enterprise from various property and liability risk exposures Frequently includes fire, allied lines, various other coverages (e g , difference in conditions) and liability coverage (such coverages would be included in other annual statement lines, if written individually) Include multi-peril policies (other than farmowners, homeowners and automobile policies) that include coverage for liability other than auto (Builders’ Risk Policies, Businessowners, Commercial Package Policies, Manufacturers Output Policies, e-Commerce and Difference-inConditions)

Coverage purchased by consumers, manufacturers, merchants, educational institutions or other providers of goods and services extending credit, for indemnification of losses or damages resulting from the nonpayment of debts owed to/from them for goods or services provided in the normal course of their business

Indemnification coverage provided to self-insured employers on an excess of loss basis

A package policy for farming and ranching risks, similar to a homeowners policy, that has been adopted for farms and ranches and includes both property and liability coverages for personal and business losses Coverages include farm dwellings and their contents, barns, stables, other farm structures and farm inland marine, such as mobile equipment and livestock A commercial package policy for farming and ranching risks that includes both property and liability coverage Coverage includes barns, stables, other farm structures and farm inland marine, such as mobile equipment and livestock.

A bond covering an employer’s loss resulting from an employee’s dishonest act (e.g., loss of cash, securities, valuables, etc )

A surety bond, insurance policy, or when issued by an insurer, an indemnity contract and any guaranty similar to the foregoing types, under which loss is payable upon proof of occurrence of financial loss to an insured claimant, obligee or indemnitee as a result of failure to perform a financial obligation (see Financial Guaranty Insurance Guideline (#1626)).

Fire, Allied Lines, Multi-Peril Crop, Federal Flood, Private Crop, Private Flood and Earthquake (see further descriptions of each under Fire & Allied Lines)

A package policy combining broad property coverage for the personal property and/or structure with broad personal liability coverage. Coverage applicable to the dwelling, appurtenant structures, unscheduled personal property and additional living expense are typical Includes mobile homes at a fixed location. (Alternative Workers’ Compensation, Employers’ Liability and Standard Workers’ Compensation)

Coverage for property that may be in transit, held by a bailee, at a fixed location, a movable good that is often at different locations (e.g., off-road construction equipment) or scheduled property (e g , Homeowners Personal Property Floater), including items such as live animals, property with antique or collector’s value, etc. This line also includes instrumentalities of transportation and communication, such as bridges, tunnels, piers, wharves, docks, pipelines, power and phone lines, and radio and television towers. (Animal Mortality, EDP Policies, Pet Insurance Plans, Communication Equipment, Event Cancellation, Travel Coverage, Vehicle Excess Waiver, Boatowners, Other Commercial Inland Marine, Other Personal Marine and Cash and Cash in Transit Insurance)

Includes all business transacted outside the U S and its territories and possessions where the appropriate line of business is not determinable

Insurance coverage protecting a licensed health care provider or health care facility against legal liability resulting from the death or injury of any person due to the insured’s misconduct, negligence, or incompetence in rendering professional services Medical Professional Liability is also known as Medical Malpractice

Insurance that indemnifies a lender from loss if a borrower fails to meet required mortgage payments

Coverage for ocean and inland water transportation exposures; goods or cargoes; ships or hulls; earnings; and liability

Same as 17 1 but on a Claims-Made Basis These policies cover insured events that are reported (as defined in the policy) within the effective dates of the policy, subject to retroactive dates and extended reporting periods when applicable

Occurrence Based: These policies cover insured events that occur within the effective dates of the policy, regardless of when they are reported to the reporting entity Insurance coverage protecting the insured against legal liability resulting from negligence, carelessness or a failure to act, causing property damage or personal injury to others Typically, coverages include construction and alteration liability; contingent liability; contractual liability; elevators and escalators liability; errors and omissions liability, environmental pollution liability; excess stop loss, excess over insured or self-insured amounts and umbrella liability; liquor liability; personal injury liability; premises and operations liability; completed operations liability, nonmedical professional liability, etc Also includes indemnification coverage provided to self-insured employers on an excess of loss basis (excess workers’ compensation) (Completed Operations, Construction Liability, Contingent Liability, Contractual Liability, Elevators, Error and Omissions, Environmental Pollution, Excess and Umbrella, Personal Liability, Premises and Operations, Excess Workers’ Compensation, Commercial General Liability, Comprehensive Personal Liability, Day Care Centers, Directors and Officers, Employee Benefit Liability, Employers’ Liability, Employment Practices, Fire Legal, Municipal Liability, Nuclear Energy, Veterinarian, Internet Liability and Cyber Liability) Excludes excess workers’ compensation

Insurance coverage protecting the manufacturer, distributor, seller or lessor of a product against legal liability resulting from a defective condition causing personal injury, or damage, to any individual or entity, associated with the use of the product

A three–party agreement where the insurer agrees to pay a second party (the obligee) or make complete an obligation in response to the default, acts or omissions of a third party (the principal)

Coverage that protects against manufacturer’s defects past the normal warranty period and for repair after breakdown to return a product to its originally intended use Warranty insurance generally protects consumers from financial loss caused by the seller’s failure to rectify or compensate for defective or incomplete work and cost of parts and labor necessary to restore a product’s usefulness Includes, but is not limited to, coverage for all obligations and liabilities incurred by a service contract provider, mechanical breakdown insurance and service contracts written by insurers (Mechanical Breakdown and Service Contracts)

Insurance that covers an employer’s liability for injuries, disability or death to persons in their employment, without regard to fault, as prescribed by state or Federal workers’ compensation laws and other statutes Includes employer’s liability coverage against the common law liability for injuries to employees (as distinguished from the liability imposed by Workers’ Compensation Laws) Excludes excess workers’ compensation

Definition

Coverage protecting the insured against the loss to real or personal property from damage caused by the peril of fire or lightning, including business interruption, loss of rents, etc

Extended coverage; glass; tornado, windstorm and hail; sprinkler and water damage; explosion, riot and civil commotion; rain; and damage from aircraft and vehicle

Insurance protection that is subsidized or reinsured by the Federal Crop Insurance Corporation for protection against losses due to damage, decreases in revenues and/or gross margins from crop, livestock and other agricultural-related production from unfavorable weather conditions, drought, wind, frost, fire or lightning, flood, hail, insect infestation, disease or other yieldreducing conditions or perils

Coverage provided by the Federal Insurance Administration (FIA) of the Federal Emergency Management Agency (FEMA) through insurers participating in the National Flood Insurance Program’s (NFIP) Write Your Own (WYO) program Coverage is subject to the terms and conditions provided in the Financial Assistance/Subsidy Arrangement between the reporting entity and the FIA

Private market coverage for crop insurance and agricultural-related protection, such as hail and fire, and is not reinsured by the Federal Crop Ins

Private market coverage (primary standalone, first dollar policies that cover the flood peril and excess flood) for flood insurance that is not offered through the National Flood Insurance Program (Sewer/water backup coverage issued as an endorsement homeowners or commercial policy )

Property coverages for losses resulting from a sudden trembling or shaking of the earth, including that caused by volcanic eruption Excluded are losses resulting from fire, explosion, flood or tidal wave following the covered event

Below is an image of a sample Top Line of Business detail page It is provided with notations (A-I) to assist in understanding the components of the product details provided for each line of business

This 2023 Louisiana Annual P&C Marketplace Summary has provided the reader with both visual and numeric presentations of the Louisiana P&C marketplace data, as a benefit of your membership with the Independent Insurance Agents & Brokers of Louisiana

Two additional, informative products are available from Real Insurance Solutions Consulting:

Quarterly state marketplace summaries are made available during the calendar year, as the data is reported by P&C insurers becomes available

Individual insurer summaries are also available, based on the same data provided in the annual and quarterly summaries, with data provided both on a national and Louisiana-specific basis

All questions and comments or need for further analysis are welcomed at the contact information below

Real Insurance Solutions Consulting, LLC

Paul A. Buse, Principal www.realinsurancesc.com 301-842-7472