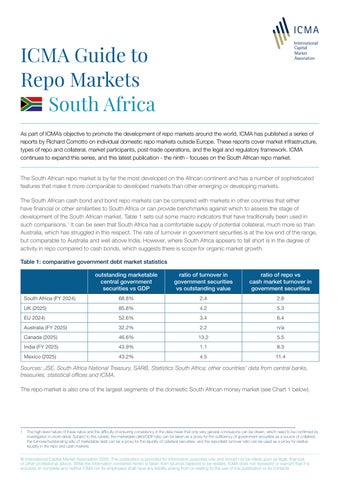

ICMA Guide to Repo Markets South Africa As part of ICMA’s objective to promote the development of repo markets around the world, ICMA has published a series of reports by Richard Comotto on individual domestic repo markets outside Europe. These reports cover market infrastructure, types of repo and collateral, market participants, post-trade operations, and the legal and regulatory framework. ICMA continues to expand this series, and this latest publication - the ninth - focuses on the South African repo market. The South African repo market is by far the most developed on the African continent and has a number of sophisticated features that make it more comparable to developed markets than other emerging or developing markets. The South African cash bond and bond repo markets can be compared with markets in other countries that either have financial or other similarities to South Africa or can provide benchmarks against which to assess the stage of development of the South African market. Table 1 sets out some macro indicators that have traditionally been used in such comparisons.1 It can be seen that South Africa has a comfortable supply of potential collateral, much more so than Australia, which has struggled in this respect. The rate of turnover in government securities is at the low end of the range, but comparable to Australia and well above India. However, where South Africa appears to fall short is in the degree of activity in repo compared to cash bonds, which suggests there is scope for organic market growth. Table 1: comparative government debt market statistics outstanding marketable central government securities vs GDP

ratio of turnover in government securities vs outstanding value

ratio of repo vs cash market turnover in government securities

South Africa (FY 2024)

68.8%

2.4

2.8

UK (2025)

85.8%

4.2

5.3

EU 2024)

52.6%

3.4

6.4

Australia (FY 2025)

32.2%

2.2

n/a

Canada (2025)

46.6%

13.2

5.5

India (FY 2025)

43.9%

1.1

8.3

Mexico (2025)

43.2%

4.5

11.4

Sources: JSE, South Africa National Treasury, SARB, Statistics South Africa; other countries’ data from central banks, treasuries, statistical offices and ICMA. The repo market is also one of the largest segments of the domestic South African money market (see Chart 1 below).

1

The high-level nature of these ratios and the difficulty of ensuring consistency in the data mean that only very general conclusions can be drawn, which need to be confirmed by investigation in more detail. Subject to this caveat, the marketable debt/GDP ratio can be taken as a proxy for the sufficiency of government securities as a source of collateral; the turnover/outstanding ratio of marketable debt can be a proxy for the liquidity of collateral securities; and the repo/debt turnover ratio can be used as a proxy for relative liquidity in the repo and cash markets.

© International Capital Market Association 2026. This publication is provided for information purposes only and should not be relied upon as legal, financial, or other professional advice. While the information contained herein is taken from sources believed to be reliable, ICMA does not represent or warrant that it is accurate or complete and neither ICMA nor its employees shall have any liability arising from or relating to the use of this publication or its contents.