Use this quick test to classify a lease under ASC 842 It helps you decide if a lease is operating or finance It also shows what changes in the financials Full guide link is inside

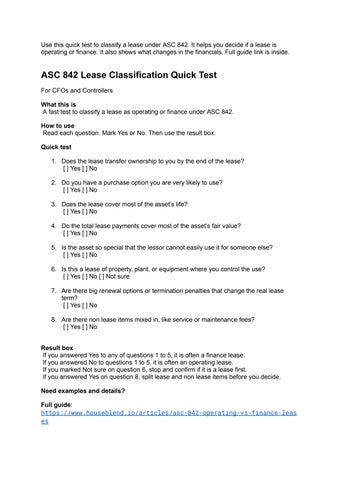

ASC 842 Lease Classification Quick Test

For CFOs and Controllers

What this is A fast test to classify a lease as operating or finance under ASC 842

How to use

Read each question Mark Yes or No Then use the result box

Quick test

1 Does the lease transfer ownership to you by the end of the lease?

[ ] Yes [ ] No

2 Do you have a purchase option you are very likely to use? [ ] Yes [ ] No

3 Does the lease cover most of the asset’s life? [ ] Yes [ ] No

4 Do the total lease payments cover most of the asset’s fair value? [ ] Yes [ ] No

5 Is the asset so special that the lessor cannot easily use it for someone else? [ ] Yes [ ] No

6 Is this a lease of property, plant, or equipment where you control the use? [ ] Yes [ ] No [ ] Not sure

7 Are there big renewal options or termination penalties that change the real lease term? [ ] Yes [ ] No

8 Are there non lease items mixed in, like service or maintenance fees? [ ] Yes [ ] No

Result box

If you answered Yes to any of questions 1 to 5, it is often a finance lease. If you answered No to questions 1 to 5, it is often an operating lease. If you marked Not sure on question 6, stop and confirm if it is a lease first. If you answered Yes on question 8, split lease and non lease items before you decide.

Need examples and details?

Full guide: https://www.houseblend.io/articles/asc-842-operating-vs-finance-leas es

What changes in the

financials

Both lease types usually record a right of use asset and a lease liability at start

The big change is how expense shows up in profit and loss.

Operating lease, common pattern

One lease cost each period, often smoother over time

Finance lease, common pattern

Amortization of the right of use asset, plus interest on the lease liability.

Total expense can be higher early and lower later.

What to watch

EBITDA can change because interest and amortization are shown below EBITDA in many models.

Debt like ratios can change because lease liabilities sit on the balance sheet.

Close time can increase if lease data is messy.

Common mistakes

Forgetting to split service fees from lease payments. Using the wrong lease term because renewals were not reviewed Using a discount rate that is not supported by your policy. Missing embedded leases inside supplier contracts.

Next step

If this is material, build a lease data list before audit season. Keep a clear policy and keep it consistent.

Talk to Houseblend

If you want a fast review of your lease list and close process, book a call. https://www.houseblend.io/book-a-meeting