A practical checklist for hedge accounting readiness under ASC 815 Use it to confirm hedge type, required documents, and close steps. Built for finance teams who want fewer surprises in audit. Full guide link is inside.

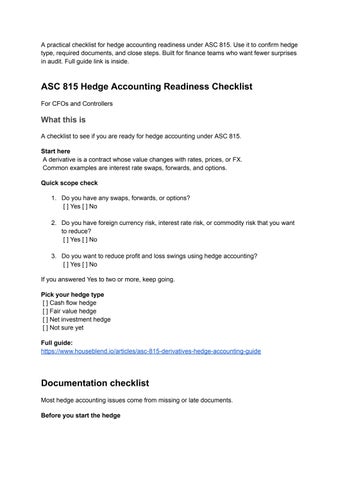

ASC 815 Hedge Accounting Readiness Checklist

For CFOs and Controllers

What this is

A checklist to see if you are ready for hedge accounting under ASC 815.

Start here

A derivative is a contract whose value changes with rates, prices, or FX. Common examples are interest rate swaps, forwards, and options

Quick scope check

1 Do you have any swaps, forwards, or options?

[ ] Yes [ ] No

2. Do you have foreign currency risk, interest rate risk, or commodity risk that you want to reduce?

[ ] Yes [ ] No

3 Do you want to reduce profit and loss swings using hedge accounting?

[ ] Yes [ ] No

If you answered Yes to two or more, keep going.

Pick your hedge type

[ ] Cash flow hedge

[ ] Fair value hedge

[ ] Net investment hedge

[ ] Not sure yet

Full guide: https://wwwhouseblend io/articles/asc-815-derivatives-hedge-accounting-guide

Documentation checklist

Most hedge accounting issues come from missing or late documents. Before you start the hedge

1 Hedge designation is written and dated on time [ ] Done [ ] Not done

2 Hedged item is clearly named Example, variable rate debt, forecast purchase, forecast sale [ ] Done [ ] Not done

3 Risk being hedged is clear Example, interest rate risk, FX risk [ ] Done [ ] Not done

4 Hedge objective is clear What are you trying to reduce? [ ] Done [ ] Not done

5 Hedge instrument details are saved Terms, dates, notional, counterparty [ ] Done [ ] Not done

6. Method to test effectiveness is defined. [ ] Done [ ] Not done

7. Who approves and who reviews is documented. [ ] Done [ ] Not done

Data you should have ready Trade confirmations

Debt or contract details for the hedged item

Forecast support if it is a forecast transaction

Market data source you will use A repeatable close process and owner

Close and reporting checklist

1 You can value the derivative each close [ ] Yes [ ] No

2 You can record fair value changes each close [ ] Yes [ ] No

3 You can run effectiveness testing on your schedule

[ ] Yes [ ] No

4 You can track what goes to earnings vs OCI when needed [ ] Yes [ ] No

5 You can track reclass entries when the hedged item affects earnings [ ] Yes [ ] No

6 Disclosures are prepared and reviewed each period [ ] Yes [ ] No

Common failure points

Documents signed late Forecast support is weak or unclear. Effectiveness method changes with no support No clear owner for valuation, entries, and disclosures

Next step

If you answered No to any close items, fix the process before adding more hedges

Talk to Houseblend

If you want a clean hedge accounting workflow and close checklist, book a call https://wwwhouseblend io/book-a-meeting