What is better than the stability of a stable coin and the price increase of a meme token? $FUSD!

“

By fusing together the tokenomic model of a stable coin and adding the taxation structure of a meme token, we have been able to create the perfect win-win cryptocurrency, that benefits everyone without the risks associated with traditional crypto investing

“

FUSD is a stable coin mechanism with a strong continual growth element. FUST is the other half of this dual-token ecosystem which allows investors to earn a steady supply of FUSD just by holding a bag. The unique tokenomics completely flip the current models most investors are familiar with and create WIN-WIN outcomes every time.

Whether you are risk taker looking for x’s (FUST) or an investor looking for a stable coin (FUSD), the ecosystem offers a fresh new approach to accumulating digital wealth without the risk of getting stuck holding a worthless investment.

FUSD creates the opportunity to pair liquidity with an appreciating stable coin which delivers an ever increasing stable value.

Unlike the typical pairings with natives that are subject to extreme volatility, FUSD remains stable and grows over time. Tie that into a model where each transaction has a positive impact on the underlying native FUSD and the projects can quickly see the “value” in FUSD.

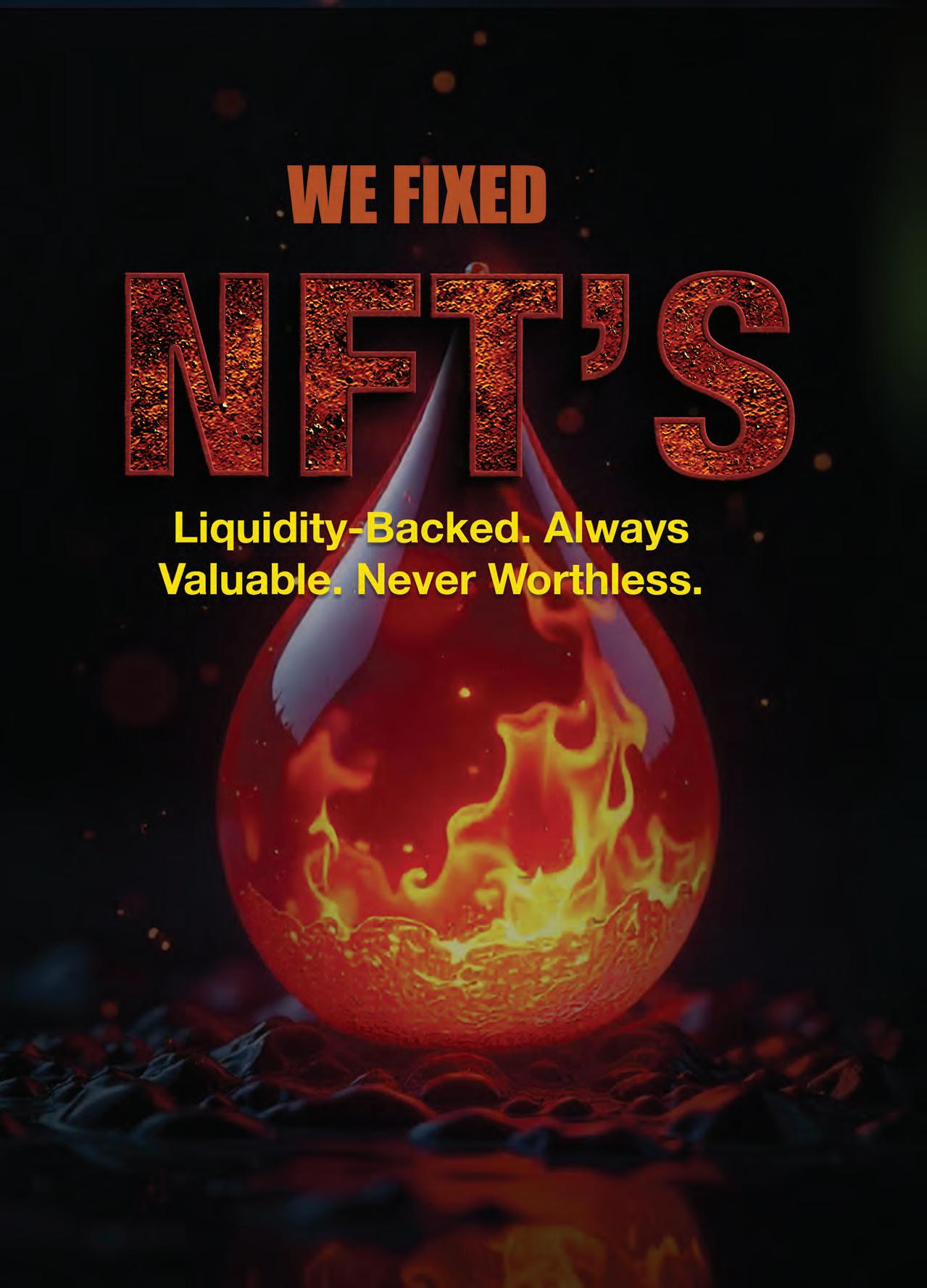

The NFT market promised ownership. It delivered illiquidity, rug pulls, and worthless JPEGs gathering dust in wallets. Liquid NFTs changes everything. Half your purchase price locks into the NFT’s liquidity pool. Forever. If the developer disappears, if the project dies, if the hype fades—your value remains. Guaranteed. Every transaction on the platform splits 5% evenly amongst all NFT holders. The more the ecosystem grows, the more your assets appreciate. Passive rewards. Automatic growth. Real value.This is how NFTs should have been built from the beginning.

9 I lliquidity Crisis

9 Value That Grows

9 Developer Protection

Traditional NFTs require finding buyers. Liquid NFTs let you cash out instantly using embedded liquidity.

Your NFT’s worth increases with locked liquidity and transaction rewards, not hype cycles.

Even if projects fail, your siloed value remains accessible. Security by design.

9 Passive Income 5% of every marketplace transaction flows to all holders. You earn whilst you sleep.

CEO | Nathan Hill Nathan@thecmccompany.com

Editor | Colin Woolley editor@cryptomag.finance

Deputy Editor | Robert Stone

Business Development| Jose Ortiz jo@CryptoMag.Finance

Art Director | Dilin Divan

Contributors

Robert Stone

Adele

Tokin Trip

Advertising Enquiries sales@cryptomag.finance

Crypto Magazine is published by the Crypto Marketing Company 71-75 Shelton Street, Covent Garden, London, United Kingdom, WC2H 9JQ

Distribution By

Telephone: 01326 319 119 7a Arwenack Street Falmouth, Cornwall TR11 3HZ office@raandollyltd.com

Welcome to Issue 11, where the speculative becomes structural.

I’m Robert Stone, Deputy Editor, and this edition arrives at a moment when cryptocurrency transitions from financial rebellion to institutional infrastructure. President Trump’s embrace of stablecoins, Chairman Bowdre’s municipal crypto framework in Miami-Dade, banks worldwide preparing Bitcoin custody services— these aren’t isolated events. They mark a fundamental shift in how power, money, and governance intersect with cryptographic reality.

The old narrative positioned crypto as an alternative to traditional finance. That framing is obsolete. When a sitting president launches a dollar-pegged stablecoin and signs the GENIUS Act into law, when major banks race to offer Bitcoin custody, when local governments build digital asset frameworks before federal mandates arrive—we’re documenting transformation, not disruption.

This issue explores that transformation from multiple angles. We examine Trump’s political calculus in making America the crypto capital. We reveal how Chairman Bowdre’s early vision in Miami created a blueprint now scaling nationally. We track Bitcoin’s original millionaires fifteen years on. We investigate MEV bots extracting millions from DeFi protocols. We confront the wallet security fundamentals that separate financial sovereignty from catastrophic loss.

But beneath the analysis runs a more fundamental question: Does institutional adoption fulfil crypto’s promise or betray it? When banks custody your Bitcoin, when governments regulate stablecoins—does this validate the revolution or co-opt it?

The ownership revolution I described in our last issue now competes with something equally powerful: the legitimisation revolution. Both forces will shape crypto’s next chapter. Understanding their collision requires moving past simplistic narratives.

Crypto Magazine exists because this space needs journalism that neither shills nor dismisses. We examine the mechanics, interrogate the incentives, and follow the money without predetermined conclusions.

Share your perspectives on this institutional shift—validation or capture?

Robert Stone Deputy

Editor editor@cryptomag.finance

10 America’s First Crypto President: From Bitcoin Sceptic to Digital Dollar Champion Volatility

Chairman Elijah Bowdre: From Visionary to Leader 20 The Biggest Crypto Giveaway in History Has Arrived

Building on Stability: USD1 and the Rise of FUSD

26 The Complete DYOR Guide: How to Research Crypto Projects Like a Pro 36 Market Caps and Tokenomics: The Numbers That Actually Matter

The Algori thm Whisperers: Inside the Secretive World of MEV Bots

From Pizza to Penthouses: Tracking Bitcoin’s First Millionaires 15 Years Later

74 Why Crypto Exists: Understanding Monetary Policy, Inflation, and the Case for Digital Money

86 Building and Preserving Your Digital Fortune Once You Have One

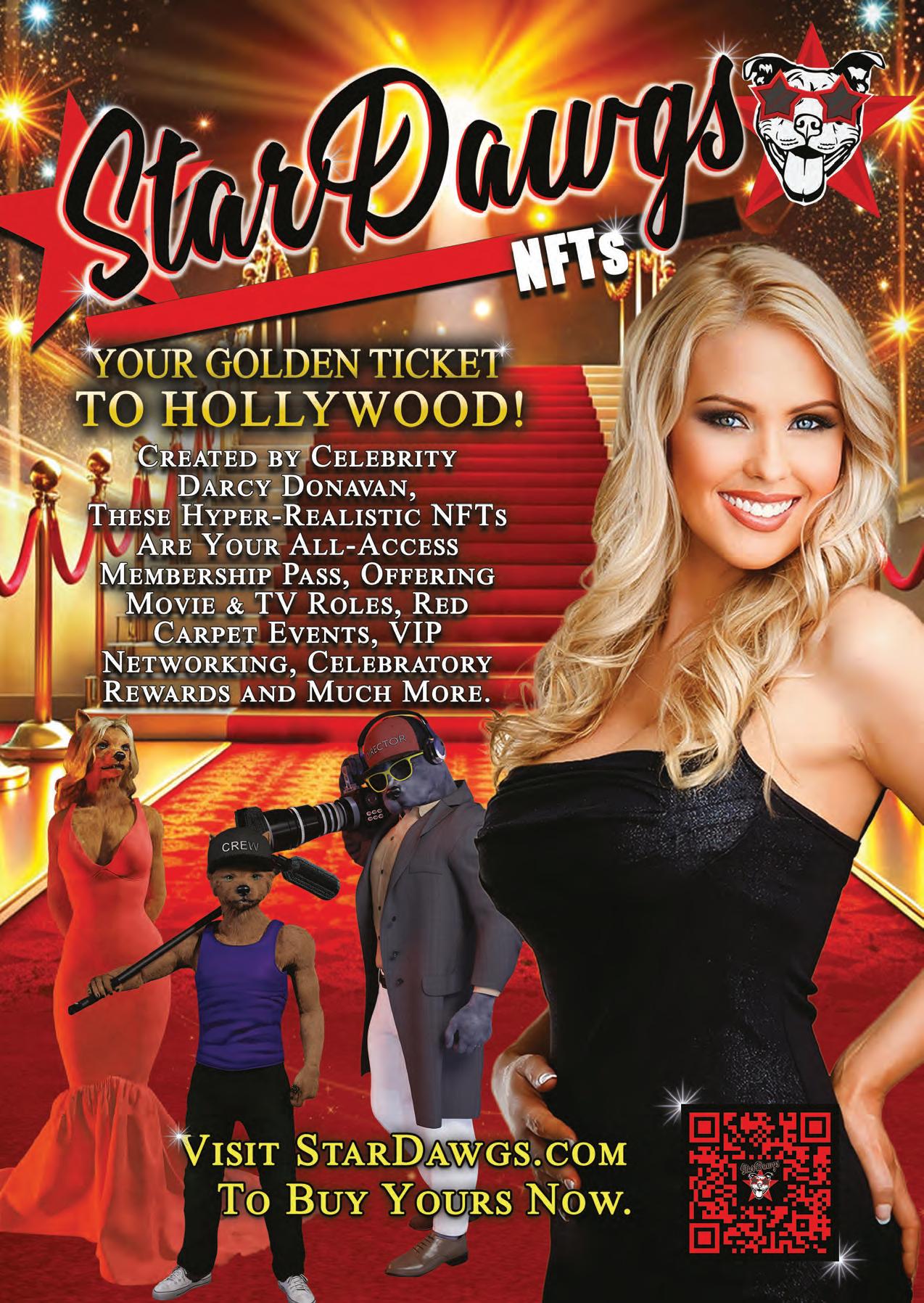

95 StarDawgs: The NFT Collection Aiming to Break Hollywood’s Glass Ceiling

98 The 0.1 Bitcoin Retirement Dream: Can a $10,000 Investment Secure Your Golden Years?

105 From Builders to Contenders: The Rise of BESC LLC

109 The Privacy Revolution: When Confidentiality Becomes Invisible by Design

Donald Trump’s journey from cryptocurrency critic to blockchain advocate has redefined the intersection of politics and digital finance.

Donald J. Trump has done what no other U.S. president has dared to do; he’s made cryptocurrency part of his political brand, his business empire, and America’s financial future. He has always thrived on spectacle, but his latest legacy move is not about theatre; it’s about strategy. By embracing cryptocurrency not just as policy, but as personal enterprise, Trump has become the first U.S. president to weave digital assets into the fabric of American politics.

When Trump released his NFT trading cards in late 2021, the project was widely dismissed as a gimmick. However, the collection sold out within hours, generating millions of dollars and proving that the former president could mobilise not just voters, but blockchain buyers. Within two years, Trump-themed meme coins were exploding across decentralised exchanges, cementing his cultural footprint inside crypto’s most chaotic marketplace.

But those early experiments were only the opening gambit. This year, Trump made his boldest move yet, backing the launch of USD1, a fully dollar-

pegged stablecoin designed to bring U.S. currency into the digital age. Paired with the passage of the Genius Crypto Act, the project marked a watershed moment; America’s head of state, the leader of the free world, was no longer just commenting on crypto. He was building it.

Politics is about winning elections and passing laws. Statecraft is about taking those laws, policies, and tools and using them to shape the nation’s role in the world.

Crypto is no longer a niche asset — it’s a significant tool of U.S. statecraft.

For Trump, this pivot was more than a financial bet. It was a political weapon, an ideological banner, and a declaration that the United States must lead in digital finance. His personal journey - from dismissing Bitcoin in 2019 to championing stablecoins as the future of the dollar - mirrors crypto’s own evolution from fringe experiment to mainstream power player.

Trump embracing crypto was not just a financial calculation; it was a political instinct. Where many saw risk, he saw resonance. In a landscape where distrust of Washington, Wall Street, and the Federal Reserve runs deep, crypto became the perfect populist tool; a symbol of financial freedom, sovereignty, and rebellion against entrenched and outmoded elites.

In 2019, Trump famously tweeted that he was ‘not a fan of Bitcoin.’ By 2024, the calculation had shifted. Campaign rallies began to feature not just the familiar chants of ‘USA!’ but placards from supporters boasting

‘Paid in Bitcoin’ and ‘MAGA on the Blockchain’. The former president recognised the energy - and the donor base - bubbling up from crypto’s grassroots.

By re-casting crypto as a pillar of his ‘America First’ agenda, Trump reframed digital assets from fringe speculation into a patriotic cause. Stablecoins weren’t just tokens; they were weapons of economic dominance. Meme coins weren’t a joke; they were proof of cultural firepower. And when crypto donations began pouring into political action committees, it became abundantly clear that digital finance had become a new front in U.S. politics.

Trump didn’t just join the crypto movement - he turned it into a political machine.

This pivot laid the foundation for the Genius Crypto Act, (Guiding and Establishing National Innovation for U.S. Stablecoins Act) which is brand new legislation designed to cement America’s role as the global leader in digital assets.

When Trump signed the Genius Crypto Act in early 2025, it was actually more than legislation; it was a manifesto. For the first time, the United States had a clear framework

to recognise, regulate, and deploy digital assets at scale. Supporters hailed it as the most important financial law since the repeal of Glass-Steagall by Clinton in 1999, which allowed big financial institutions to re-integrate commercial and investment banking. Critics called it a reckless gamble. Either way, it marks a turning point.

At its core, the Act gave stablecoins - dollar-pegged cryptocurrencies like Trump’s own USD1- formal legal standing. Issuers would be required to hold transparent reserves, undergo regular audits, and integrate with U.S. banks. In return, stablecoins could be used for everyday payments, federal procurement, and even government benefits distribution.

The law also laid out a roadmap for cross-border crypto transactions, positioning the dollar as the world’s default digital currency. By embracing

blockchain rails, Trump sought to outpace China’s digital yuan and reclaim America’s monetary advantage in the global economy.

Perhaps most striking was the political theatre around it. Trump didn’t present the Act as a technical finance bill; he sold it as an ‘America First Digital Dollar Revolution’. Standing alongside crypto CEOs and waving a gold-embossed copy of the legislation, he cast himself not just as a president, but as the architect of a new monetary order.

If the 20th century was defined by the petrodollar, Trump wants the 21st defined by the cryptodollar.

Stablecoins & USD1 - The Heart of Trump’s Crypto Gambit

For all the spectacle of NFTs and meme coins, it is Trump’s involvement with USD1 that may prove the most consequential. Unlike the hypefueled tokens of the past, USD1 is designed to be the steady backbone of digital finance; a fully dollar-pegged stablecoin with ambitions far beyond speculative trading.

Launched through World Liberty Financial, USD1 arrived at the same moment the Genesis Act gave it legal standing. The synergy was intentional. With federal recognition, USD1 could be deployed in everyday

transactions, integrated into government contracts, and circulated globally as a secure digital extension of the U.S. dollar.

The implications were enormous. Stablecoins had already been gaining traction worldwide, offering the speed of crypto with the reliability of fiat. But Trump’s decision to tie his name and presidency to USD1 gave stablecoins a new political dimension. It wasn’t just another token; it was branded as a symbol of American dominance in the digital age.

Critics called it selfdealing, a dangerous blend of statecraft and personal business. Supporters insisted that USD1 could become a geopolitical asset, countering rivals like China’s digital yuan and reinforcing the dollar’s supremacy in global trade. Either way, the message was clear; stablecoins had moved from the margins of fintech into the very centre of U.S. monetary policy.

Trump’s embrace of digital assets didn’t just reshape markets; it reshaped politics. What began as a niche issue for libertarians and Silicon Valley entrepreneurs has become a litmus test for national power, campaign finance, and party identity.

By 2024, crypto donations were flowing into political action committees (PACs) at unprecedented levels, many of them aligned with Trump’s campaign. Supporters touted it as proof that digital

finance could fuel grassroots democracy, whilst critics warned of unchecked influence and regulatory loopholes. Either way, crypto had become a new artery of American political money.

At the state level, Trump’s vision found eager allies. Florida introduced tax incentives for crypto businesses, Texas positioned itself as the Bitcoin mining capital of the world, and Wyoming pushed forward with pioneering digital bank charters. Together, these moves built a pro-crypto map of ‘Trump territory’, where blockchain was not just tolerated but celebrated as an engine of growth and sovereignty.

The Democratic Party, long cautious on crypto, was forced to respond. Some lawmakers called for tighter oversight, while others proposed rival frameworks. But the narrative was already set; Trump had planted the flag. In the 2025 political landscape, crypto was no longer a fringe talking point; it was a frontline issue. Like it or not, Washington was forced to play catch-up.

For Trump, crypto is not just about markets or politics; it’s about governance. With the Genesis Act passed and USD1 in circulation, his administration

began laying out a blueprint for integrating blockchain directly into the machinery of the U.S. government.

The vision was sweeping. Federal payments - from procurement contracts to overseas aid - could be settled in stablecoins, ensuring faster, cheaper, and more transparent flows of money. Social programs and benefits could be distributed digitally, reducing fraud and enabling instant access to citizens. Treasury operations could

leverage blockchain for global settlements, reinforcing the dollar’s supremacy at a time when rivals were experimenting with central bank digital currencies.

Beyond finance, Trump’s allies floated the idea of blockchainbased systems for elections, identity verification, and public records, framing them as tools of autonomy and efficiency. To Trump, these weren’t abstract reforms. They were tangible expressions of his broader philosophy: decentralisation

at home, and dominance overseas.

Critics warned of blurred lines, especially with the president personally tied to USD1. Trump’s supporters argued that government adoption of crypto wasn’t about private enrichment, it was about defending America’s financial primacy in a rapidly digitalising world.

Not everyone is convinced that Trump’s crypto crusade is the future of finance. For his detractors, the president’s intertwining of public policy and personal enterprise raises red flags as glaring as the gold trim on his rally stage.

They argue that tying the presidency to USD1 creates conflicts of interest unprecedented in American history; a commander-in-chief who could directly profit from the very monetary system he regulates.

Some economists warn that stablecoins, while useful, still carry risks of liquidity crises and systemic shocks if not carefully managed. Others fear that embedding crypto into government infrastructure opens new avenues for cyber-attacks and financial instability.

Trump’s opponents also frame the move as political opportunism. They argue his pivot from crypto sceptic to crypto evangelist wasn’t born of conviction, but calculation; a way to capture donors, energise voters and build another revenue stream under the guise of national policy.

But his supporters see it differently. To them, Trump is doing what Washington has always done best: leveraging American innovation to maintain global dominance. They argue that if the U.S. doesn’t lead in digital finance, China, Russia, and other rivals will fill the void. And they point out that Trump’s policies, although controversial, have

already given the dollar a head start in the digital age.

Whether history remembers it as brilliance or folly, Trump’s crypto push has already redrawn the boundaries of American politics and finance. He is the first U.S. president to not only regulate digital assets but to embody them, blending personal enterprise, national policy, and geopolitical ambition into a single, audacious vision.

With the Genius Crypto Act as law, USD1 in circulation, and blockchain woven into the language of statecraft, Trump

Trump’s supporters argued that government adoption of crypto wasn’t about private enrichment, it was about defending America’s financial primacy in a rapidly digitalising world

has positioned himself as the architect of America’s digital monetary era. In his telling, the dollar’s destiny is no longer tied to oil, banks, or bureaucrats, but to code, cryptography, and global adoption.

Supporters hail it as a renaissance, a chance for the U.S. to seize leadership in the 21st century’s financial systems. Critics call it a dangerous experiment that risks politicising the foundations of money itself. Yet even his fiercest opponents admit the undeniable: Trump has forced the world to take crypto seriously.

Donald J. Trump may not just be remembered as the 45th and 47th president, but as America’s first crypto president.

In the end, Trump’s crypto doctrine is less about technology than power. It is the belief that the U.S. must not only adapt to the future of finance, but define it. And in his trademark style, like so many of his ventures, it is a gamble; high risk, high reward, and impossible to ignore.

In 2021, when most U.S. politicians still dismissed cryptocurrency as a fad, Miami was already charting a different course. As chairman of the Miami-Dade Cryptocurrency Task Force, Elijah John Bowdre began asking the questions others avoided: How could digital assets serve real communities? How could blockchain reduce inequality, unlock new streams of growth, and give ordinary people a stake in the financial future?

While Washington debated whether crypto should even be taken seriously, Miami-Dade County understood it was infrastructure. Under Chairman

Adele Adele60370277

Bowdre’s leadership, Miami positioned itself as a testbed for adoption, exploring municipal applications, consulting with innovators in Wyoming, and framing crypto not as a speculative gamble, but as a tool for long-term economic resilience.

Today, in 2025, the world has caught up. President Trump’s USD1 stablecoin has taken digital dollars into the mainstream. Congress has passed the GENIUS Act to regulate them at a federal level and crypto is moving from the periphery to the very heart of U.S. policy, as Trump pushes to establish a new kind of digital stability.

Long before stablecoins became the talk of Congress, Chairman Bowdre was working to prove their value at the local level. In his role as chair of the MiamiDade Cryptocurrency Task Force, he convened business leaders, technologists, and community representatives to explore how digital assets could strengthen the region’s economy.

For Chairman Bowdre, it’s never been about hype, just practicality. Could residents pay utility bills in crypto? Could local businesses tap blockchain tools to cut costs and expand markets? Could

Miami-Dade attract investment by positioning itself as the most forward-thinking county in America?

Under his guidance, the MiamiDade Digital Commission Task Force studied adoption models, from Wyoming’s pioneering legislation to global pilots in Europe and Asia. The result was a blueprint for Miami that went beyond branding the city as a ‘Crypto Capital’. It was a serious attempt to embed digital finance into both local

government and the everyday lives of ordinary people.

That early work positioned Miami as a laboratory for what digital assets could achieve in government, years before Washington or Wall Street embraced the idea. And now, as the U.S. moves to integrate stablecoins at a federal level, Chairman Bowdre’s local vision looks less like an experiment, and more like a preview of the future. An alignment with Trump’s National Vision

What Chairman Bowdre began in Miami, President Trump has scaled across the nation. When he pushed the GENIUS Act through Congress in 2025 and unveiled USD1, the first federally sanctioned stablecoin, it marked a turning point; digital dollars were no longer a local experiment, but a matter of national policy.

The parallels are clear. Bowdre treated crypto as infrastructure in Miami; a tool for efficiency, growth, and empowerment. Trump echoed that same philosophy at the federal level, harnessing stablecoins to reinforce U.S. monetary leadership. Both leaders share a conviction that digital assets are not fringe speculation, but strategic levers for financial resilience.

This alignment is more than coincidence - it reflects a broader shift. From city halls to the White House, crypto is being recognised as a pillar of the next financial era. And for Chairman Bowdre, it validates what he argued years earlier; that local innovation can shape national destiny.

The FUSD Connection

If Trump’s USD1 proved stablecoins could command global attention, Bowdre sees them as foundational to Miami’s fintech leadership in the 21st century. USDT (Tether) is liquid and globally accepted for settlements. USDC (USD

Coin) is transparent, compliant and trusted for large scale transactions. USD1 - President Trump’s stablecoin, is a digital anchor pegged to the US Dollar. And FUSD (Fused) is a next generation stabletoken merging a USDC peg with growth, well suited for public finance. FUSD’s unique tokenomics are engineered not just to preserve value, but to grow it consistently for everyday stakeholders.

A long-time advocate of broadening access to wealthbuilding tools, Chairman Bowdre supports FUSD’s model of appreciating stability. Unlike traditional stablecoins, where the upside flows to the issuer, FUSD directs growth back

to the holders themselves.

For Chairman Bowdre, that alignment is more than financial engineering; it is a matter of principle.

“Stable value shouldn’t just serve institutions,” he has argued. “It should serve people.”

That belief is why Bowdre has pledged to act as an ambassador for stable coins in municipal use. He sees them as a tool to tackle the same challenges he wrestled with on the Miami-Dade Cryptocurrency Task Force; financial exclusion, unequal access to growth, and the need for communities to share in the prosperity of the systems they support.

As an advocate of the nextgeneration appreciating stable token model, Bowdre ties his early vision to the present moment, building bridges between local communities, national policy, and a financial model that puts the investor first.

For Chairman Bowdre, the promise of crypto has never been abstract. It isn’t about speculation, memes, or market charts, it’s about real people and real challenges. In MiamiDade, that means families struggling with rising costs, small businesses trying to expand, and communities hit hardest by cycles of economic boom and bust.

Bowdre believes digital assets can help close those gaps. Stable value tokens can give residents a hedge against volatility in traditional systems. Blockchain-based tools can reduce fees for remittances, a lifeline for Miami’s immigrant families. An appreciating stabletoken like FUSD, where tangible growth benefits holders, gives everyday investors a chance to share in the upside of financial innovation, instead of the banks, issuers, or hedge funds.

This vision is practical as much as it is principled. By embedding crypto into everyday transactions, Chairman Bowdre believes that Miami could strengthen its

resilience, broaden opportunity, and serve as a model city for inclusive digital finance.

It’s a vision rooted not in ideology, but in empathy. An insistence that the next wave of financial infrastructure must be designed for the people who use it, not just the institutions that issue it.

As a passionate advocate of the benefits of crypto currency

for US Citizens, Chairman Bowdre has received a warm welcome into the distinguished alumni of contributors to Crypto Magazine, which is the world’s largest printed crypto publication, with more than 500,000 readers worldwide. Crypto Magazine will continue to champion the role digital assets can play in everyday lives, giving a global audience advanced access.

The arrangement is mutually reinforcing. Crypto Magazine gains a trusted voice at the

intersection of politics and blockchain. Chairman Bowdre gains an outlet to amplify his message that crypto should not just serve institutions and insiders, but empower communities and ordinary investors.

It is a dual stage - political and media - that will continue to position him as a thought leader and a pioneer, determined to reshape finance in a way that supports the growth and prosperity of all.

Chairman Bowdre’s story is one of consistency; a leader who saw the potential of digital assets long before they became fashionable, and who has carried that vision from committees and community incubators. In Miami, he pioneered the idea that crypto could be more than speculation; it could be infrastructure for resilience. Nationally, his philosophy has found echoes in President Trump’s push to make stablecoins part of U.S. strategy. And now, through his advocacy of FUSD, Bowdre is hoping to shape the next chapter - a model where ordinary investors share directly in the benefits of appreciating stability.

We very much look forward to his wisdom and insight as the global political landscape embraces the possibilities of digital currency.

Adele Adele60370277

Crypto has seen a decade of airdrops, incentives, loyalty schemes, and headlinegrabbing token launches, but nothing comes close to what’s about to hit the industry this January.

To celebrate the multichain launch of FUSD and FUST tokens, and the highly anticipated relaunch of the upgraded multi-chain Liquid NFT Platform, the team behind Liquid is preparing

to unleash what may be the most aggressive, ambitious, and value-packed marketing campaign the crypto space has ever witnessed.

This isn’t just another airdrop. This is a six-month wealth engine powered directly by platform revenue, and it’s going straight into the hands of one lucky participant.

And the numbers are staggering.

10% of Liquid Revenue for Six Months. Up to $1 Million Per Month. One

Yes, you read that correctly.

Liquid is giving away 10% of total platform revenue for six entire months, capped at a jaw-dropping $1,000,000 per month. For perspective: to buy that kind of revenue share through Liquid’s Genesis NFTs, you’d need to own 66 of them,

worth a combined $335,000.

Instead, someone is about to win it. For free. From a simple competition entry.

Rather than handing over a lump sum, Liquid is taking a far more strategic, bullish approach.

The winner will receive a monthly investment portfolio of 10 tokens, delivered for six months. The portfolio will include:

Major Coins including BTC & ETH - final line-up still under wraps!

Emerging Tokens, all partnered in some way with the Liquid NFT eco-system from brands like Roburna Labs, Milestone Millions, The CMC Group and BESC LLC

1 Token (or NFT) chosen personally by the winner, valued at one-tenth of the monthly portfolio

And here’s where it gets really interesting:

Liquid will buy these tokens from the open market using the revenue share. At full volume. Every month.

That means this campaign doesn’t just reward the winner; it potentially drives up to $100,000 in monthly buy pressure on each selected token, depending on platform activity.

It’s a win-win for the winner and the ecosystem.

Liquid is opening the floodgates to entries, making participation accessible to everyone in crypto - newcomers, traders, degens, builders, influencers and beyond.

Here’s how entries work:

Main Entry Methods

Buy FUSD 1 entry per $1 spent

Buy FUST 2 entries per $1 spent

Sell FUSD or FUST Yes, sells also qualify!

This is the first competition of its kind where both buys and sells generate entries, rewarding activity, not just accumulation.

Visit TheBigCryptoGiveaway.com and earn 10 free entries

Subscribe to Crypto Magazine and earn 100 free entries

Follow FUSD, FUST, and Liquid NFTs on social media to earn 10 entries per handle

Refer friends and get unlimited entries, plus a MASSIVE bonus opportunity...

Treasure hunts on partner websites - find codes to earn additional entries

Participating projects pairing FUSD liquidity will have their buys qualify too

NFT entry routes through the Liquid NFTs platform

And here’s the kicker

If you refer the winner, you earn big too.The referring wallet receives 1% of platform revenue (paid in FUSD) for six months.

That’s the kind of upside normally reserved for early investors, not competition referrers!

Liquid isn’t whispering about this giveaway. They’re going to shout it from the mountaintops.

The campaign will run across YouTube, TikTok, partner websites, social channels, and mainstream media outlets, supported by a seamless clickthrough flow that sends users directly to buy FUST and FUSD on BESC Hyperchain and BNB Chain.

To bring new users into crypto, onboard new liquidity, elevate the Liquid ecosystem, and ignite visibility across sectors far beyond the Web3 bubble.

This is crypto entering true mass-market marketing territory. Most crypto giveaways are short-term hype with no long-term value engine.

Liquid is flipping that model on its head.

Revenue fuels the prize.

The prize drives major token buys.

The buys support the ecosystem.

The ecosystem activity drives more revenue.

The cycle compoundspublicly and transparently - every month.

This is incentive engineering at its most powerful; a first-ofits-kind value loop in crypto. It’s potentially the biggest giveaway ever and could just be the catalyst for the next wave of adoption.

The competition begins in January 2026 and runs for three months. One participant will walk away with a six-month investment stream worth potentially millions.

But the real story isn’t just the prize.

It’s the scale. The ambition.

The fact that a decentralised ecosystem is willing to put real revenue on the line to ignite growth the entire industry can feel.

This isn’t a stunt. It’s a statement.

Adele Adele60370277

2025 has become the year of the stablecoin. From the State of Wyoming’s Frontier Token to Société Générale’s dollar-backed USDCV, financial institutions, state governments and even retailers are rushing to mint their own digital dollars. Yet none has captured the world’s attention like USD1; the politically charged stablecoin tied directly to President Donald J. Trump.

USD1 was launched with a bold mission: to reinforce the U.S. dollar’s dominance in a digital era. Fully backed by treasuries and cash equivalents, it offers the stability and transparency that have helped move stablecoins out of the crypto fringe and into the heart of U.S. monetary policy. For holders, it delivers what every

stablecoin promises: a dollar that moves at internet speed. But the real rewards and wealth generation flow elsewhere.

It flows to the issuer, World Liberty Financial, majorityowned by the Trump family, who capture the yield on the billions held in reserves.

It’s fair to say that USD1 has showed the world what stablecoins can do for governments and issuers, but the convenience and reassurance of stability doesn’t pay dividends to the everyday investor. And that’s where the next chapter begins.

USD1 has been the crypto lightning rod; it exploded onto

the world stage and drew the most attention, excitement, and criticism, shining the spotlight onto stablecoins as a whole. But it was hardly alone. In the wake of its launch, governments, banks, and Fortune 500 companies rushed to unveil their own digital dollars. Wyoming issued the Frontier Token (FRNT), the first state-backed stablecoin. Société Générale, one of the big four financial institutions in France, announced USDCV, a dollar-pegged token for institutional clients. In the U.S. it seems like everyone from banks to retailers are preparing to launch stablecoins under the new federal framework.

The message is clear; stablecoins are no longer experiments, they are infrastructure. They move money faster than traditional

methods, clear borders without friction, and open the door to programmable finance. And yet, across all of these launches, the model remains the same.

Holders get stability, speed and reassurance, and issuers get the yield. For everyday investors, the benefit is limited to convenience, while the real economic upside accrues to the companies behind the coins.

This is the context into which a new model emerges: a stabletoken that doesn’t just line the pockets of institutions and issuers, but directly benefits its holders.

If USD1 was the catalyst for mainstream adoption, FUSD is the evolution. Where traditional stablecoins lock value into reserves that benefit the issuer, FUSD flips the model on its head; it’s an appreciating stabletoken, engineered to be an appreciating store of value where benefits flow to the investor.

FUSD combines the stability investors expect with a steady appreciation in value, by fusing together the mint/burn tokenomics of a stabletoken with the taxation structure of

a meme or utility token. That means every buy and every sell injects liquidity directly into the smart contract and the underlying value grows. It is dollar backed 1:1 with USDC but as adoption grows, the upside doesn’t vanish into institutional pockets; it compounds directly for those who hold the token.

Just as importantly, FUSD doesn’t reject the stablecoin framework that USD1 has helped legitimise. Instead, embracing it is central to its growth plans. As an already fully-functioning multi-chain token, FUSD will add to its current liquidity pairs - ETH, BNB Chain, BESC HyperChain and Polygon - and create further pairs over time including a liquidity pair with USD1.

FUSD both supports the ethos that stablecoins are the future of money, and strategically positions itself alongside the most politically significant token in existence. The result? Holders continue to benefit from FUSD’s appreciating value while tapping into the global dominance that USD1 has unleashed.

Stablecoins have already proven their place in global finance. They are faster than bank transfers, more accessible than traditional payments, and increasingly recognised by

regulators and governments alike. USD1 showed how they could be leveraged as tools of state power. FRNT and USDCV demonstrated that states and banks are ready to issue their own. Together, these projects have cemented stablecoins as the financial backbone of Web3.

But the question has always lingered; who really benefits? Until now, the answer has been issuers and institutions, the ones earning the yield on billions parked in reserves. Holders got stability, but rarely more.

FUSD is different. By aligning stability with appreciation it ensures that growth in adoption translates into value for its community of investors. It salutes the spirit of USD1 as a catalyst for mass adoption, whilst refusing to accept a model where only the issuer wins.

Its liquidity pair with USD1 will be both symbolic and strategic; a way to honour the door USD1 opened, while offering a new path where holders share directly in the upside.

In that sense, FUSD represents more than just a token. It represents a new philosophy for digital money. One where stability and investor empowerment go hand in hand. If USD1 was the beginning of the stablecoin era, FUSD may well be the start of the stabletoken revolution!

Robert Stone @StoneOnChain

In the fast-moving world of cryptocurrency, fortunes are made and lost on the quality of research. While social media influencers shout “to the moon” and telegram groups pump the latest “gem,” professional investors quietly conduct systematic due diligence that separates legitimate projects from elaborate scams.

DYOR—Do Your Own Research— isn’t just crypto slang. It’s the difference between strategic investment and expensive gambling. Whether you’re evaluating Bitcoin, analysing the latest DeFi protocol, or investigating a promising Layer 1 blockchain, the principles remain the same: systematic analysis, healthy scepticism, and thorough verification.

As editor of this magazine, I’ve been researching crypto projects since the early days when Bitcoin Talk was the epicentre of everything that mattered in cryptocurrency. Back then, anyone who was someone in crypto would descend on those forums with their projects, whitepapers clutched in digital hands, seeking validation from a community that was equal parts brilliant and sceptical.

I remember the excitement of discovering Ethereum when Vitalik first posted about it, the heated debates over proof-ofstake versus proof-of-work, and the wild west atmosphere where a single forum post could launch or destroy a project overnight.

Those Bitcoin Talk days taught me something crucial: the fundamentals of good research haven’t changed, even as the ecosystem has exploded from a few thousand enthusiasts to a trillion-dollar market. The same red flags that appeared in 2013 altcoin announcements still appear in today’s Layer 2 launches, just dressed in more sophisticated language. The same patterns that identified legitimate innovations like Chainlink or Uniswap in their early stages still work now, but you need to know what to look for. What has changed is the sophistication of both the projects and the scams, the speed at which information moves, and the sheer volume of new projects launching daily.

I’ve watched thousands of projects come and go, seen genuine innovations emerge from unknown developers, and witnessed elaborate scams that fooled even experienced investors. I’ve made my share of mistakes—falling for projects with impressive teams but no real substance, missing obvious red flags because I got caught up in the hype, and occasionally discovering gems that everyone else

overlooked. Each experience taught me something new about separating signal from noise in this chaotic but fascinating space.

The framework I’m sharing here has been battle-tested through multiple market cycles, from the early altcoin experiments through the ICO boom, the DeFi summer, the NFT craze, and beyond. It’s saved me from countless costly mistakes and helped identify opportunities that others missed. More importantly, it’s teachable—these aren’t mystical skills available only to crypto veterans, but systematic approaches anyone can learn and apply.

This guide will teach you to research crypto projects with the rigour of a venture capitalist and the scepticism of a forensic accountant. By the end, you’ll have a framework that can save you from costly mistakes and help you identify genuine opportunities before the crowd catches on.

The Problem Statement

Every legitimate crypto project starts with a real problem. Before diving into tokenomics or technical specifications, ask fundamental questions: What problem does this project claim to solve? Is this problem

significant enough to warrant a blockchain solution? Does the solution require a new token, or could it work with existing infrastructure?

In my early days at Bitcoin Talk, I learned to identify projects that were solutions looking for problems. One project I remember claimed to revolutionise the pet food industry with blockchain technology. When pressed for details, the team couldn’t explain why pet food distribution needed immutable ledgers or why existing supply chain solutions wouldn’t work. The project raised significant funds but predictably failed within six months.

Red flag example: Projects that create tokens for problems that don’t exist or could be solved more efficiently with traditional technology. If a project’s whitepaper spends more time explaining potential returns than explaining the underlying problem, proceed with extreme caution.

Research the total addressable market for the problem being solved. Is this a billion-dollar problem or a niche issue affecting a small community? Timing matters enormously in crypto. Projects launching DeFi protocols in 2019 had very different prospects than identical projects launching in 2024.

Use tools like Google Trends, industry reports, and competitor analysis to understand market dynamics. A brilliant solution to yesterday’s problem is still a poor investment.

No crypto project exists in isolation. Map out direct competitors, indirect competitors, and potential threats from traditional industries. How does this project differentiate itself? What advantages does it have that competitors cannot easily replicate?

Strong projects often acknowledge competitors directly and explain their specific advantages. Projects that claim to have no competition either haven’t done their homework or are operating in a market too small to matter.

Understanding the underlying technology doesn’t require a computer science degree, but it does require careful reading. Key questions include: Is this project building on an existing blockchain or creating its own? What consensus mechanism does it use? How does it handle scalability, security, and decentralisation trade-offs?

For projects building on existing blockchains like Ethereum or Solana, evaluate why they chose that specific platform. For projects creating new blockchains, scrutinise their technical innovations and whether they solve real limitations of existing chains.

If the project involves smart contracts, these should

be publicly viewable and preferably audited by reputable firms. You don’t need to read Solidity code, but you should verify that contracts exist, match the project’s claims, and have been professionally audited.

Major audit firms include Trail of Bits, ConsenSys Diligence, and Quantstamp. Independent audits from multiple firms provide greater confidence than single audits or self-audits.

Active development indicates a serious project. Use GitHub to examine the project’s code repositories. Look for regular commits, multiple contributors, comprehensive documentation, and responsive issue resolution. A repository with no activity for months suggests an abandoned or stagnant project.

This lesson came hard during my early research days. I invested in a project with an impressive whitepaper and strong marketing, but I failed to check their GitHub repository. Had I looked, I would have discovered their last code commit was eight months old, and their promised “revolutionary consensus algorithm” existed only in marketing materials. The project eventually exit scammed, but the warning signs were there for anyone who bothered to look.

Compare development activity to similar projects. Healthy projects typically show consistent development velocity with periodic major updates and regular bug fixes.

Examine the project’s technical roadmap critically. Are milestones specific and measurable? Do they align with realistic timelines? Have previous milestones been met on schedule? Vague roadmaps with distant, undefined goals often indicate poor planning or intentional misdirection.

Cross-reference roadmap claims with actual development progress. Projects that consistently miss deadlines or quietly abandon promised features deserve additional scrutiny.

Research team members individually. Look for relevant experience, previous successes or failures, and current commitments. LinkedIn profiles, previous project involvement, and academic credentials all provide valuable context.

Be particularly cautious of anonymous teams unless the project has compelling reasons for anonymity and has

demonstrated competence through other means. While some legitimate projects maintain anonymity for security or philosophical reasons, this adds additional risk that should be factored into your analysis.

Examine the project’s advisors and their actual involvement. Legitimate advisors typically have relevant expertise and active engagement with the project. Be cautious of “advisor collections” that list impressive names, but have minimal actual involvement.

I’ve seen this pattern repeatedly: projects list impressive advisors who have no real connection to the project. A simple social media check often reveals that these “advisors” have never publicly mentioned the project or, in some cases, have never heard of it. Always verify advisor claims by checking their social media

activity and public statements about the project.

How are decisions made within the project? Is there a clear governance process? Are token holders involved in decisionmaking? Centralised control can enable rapid development, but it also creates risks if key individuals leave or make poor decisions.

Evaluate the project’s approach to decentralisation. Many projects start centralised and promise progressive decentralisation. Assess whether they have concrete plans and timelines for transferring control to the community.

Research the project’s funding sources and investor profile. Reputable institutional investors often conduct their own due diligence, providing additional validation. However, celebrity endorsements or influencer backing should be treated with scepticism unless accompanied by substantial technical and business analysis.

Examine funding terms if available. Projects that have raised excessive amounts relative to their development stage may face pressure to deliver unrealistic returns, potentially leading to rushed launches or pivot decisions.

Understand the total token supply, circulating supply, and emission schedule. How many tokens exist? How many will exist in the future? Are there mechanisms for burning tokens or controlling inflation?

Excessive token inflation can erode value over time, while fixed supplies may create artificial scarcity. Look for thoughtful tokenomics that align with the project’s longterm sustainability rather than short-term price appreciation.

What specific functions does the token serve within the project’s ecosystem? Can these functions be performed only with this specific token, or are there alternatives? The strongest tokens have multiple compelling use cases that create sustained demand.

Be sceptical of tokens whose primary utility is governance voting, unless the governance decisions have a meaningful economic impact. Many governance tokens trade primarily on speculation rather than utility demand.

How are tokens distributed among different stakeholders? What percentage goes to the

team, investors, treasury, and public? Are there vesting schedules that prevent massive dumps? Heavily concentrated ownership creates risks of market manipulation and governance centralisation.

Look for fair distribution mechanisms and reasonable vesting schedules that align team incentives with long-term project success.

Analyse the project’s revenue model and sustainability. How does the project generate value? Are transaction fees, staking rewards, or other mechanisms economically viable long-term? Projects that depend entirely on new user growth without underlying value creation often resemble pyramid schemes.

During the ICO boom, I evaluated dozens of projects with tokens that served no real purpose beyond fundraising. Teams would create elaborate tokenomics documents explaining complex staking mechanisms and governance features, but the fundamental question remained unanswered: why does this need a token at all? The strongest projects I’ve discovered over the years have tokens that are genuinely necessary for their core functionality, not just fundraising vehicles.

Strong projects typically have multiple revenue streams and

clear paths to self-sustainability without depending on continuous token price appreciation.

Examine the project’s social media presence across multiple platforms. Look for organic engagement rather than artificial metrics. Real communities ask technical questions, discuss use cases, and provide constructive feedback. Bot-driven communities tend to focus on price predictions and hype.

Monitor social sentiment using tools like Sentiment Trader or Social Blade. However, remember that social media can be gamed, so treat these metrics as supporting evidence rather than primary indicators.

For platform projects, evaluate the developer ecosystem.

How many applications are being built on the platform? Are there developer tools, documentation, and support programs? Growing developer activity often precedes mainstream adoption.

Check developer forums, documentation quality, and third-party integrations. Thriving developer ecosystems create network effects that enhance project value.

Research the project’s partnerships and integrations. Are these genuine business partnerships or marketing announcements? Real partnerships typically involve technical integration, shared development, or mutual business benefits.

Verify partnership claims by checking partner websites and public statements. Many projects exaggerate the significance of partnerships or list tentative discussions as confirmed relationships.

For launched projects, analyse actual usage metrics. Daily active users, transaction volume, total value locked, and other on-chain metrics provide objective measures of adoption. Compare these metrics to similar projects and track trends over time.

Be cautious of vanity metrics that can be easily gamed. Focus on metrics that indicate real economic activity and user engagement.

Review all available security audits carefully. Professional audits should identify potential vulnerabilities and confirm their resolution. Multiple audits from different firms provide greater confidence than single audits.Pay attention to audit timing relative to code changes. Audits become less relevant as code evolves, so recent audits of current code are more valuable than old audits of previous versions.

Research the project’s security history. Have there been hacks, exploits, or other security incidents? How did the team respond? While past incidents don’t disqualify projects, they provide insights into team competence and crisis management capabilities.

Evaluate whether previous security issues have been addressed systematically or just patched superficially.

Consider regulatory risks in relevant jurisdictions. Some

projects operate in legal grey areas or could face future regulatory challenges. Research the regulatory environment for similar projects and the project’s approach to compliance.

Projects with proactive legal strategies and compliance frameworks typically face lower regulatory risks than those that ignore legal considerations entirely.

Assess technical risks specific to the project’s architecture. New consensus mechanisms, experimental cryptography, or complex economic models may introduce unforeseen risks. Cutting-edge technology often offers advantages but comes with higher technical risk.

Consider your own risk tolerance and diversification when evaluating hightechnical-risk projects.

Be extremely wary of projects that emphasise returns over utility, promise guaranteed profits, or use high-pressure sales tactics. Legitimate projects focus on building technology and solving problems, not generating shortterm price appreciation.

Celebrity endorsements, influencer partnerships, and aggressive social media marketing often indicate projects prioritising hype over substance.

Closed-source code, lack of technical documentation, or teams that cannot discuss their technology coherently all indicate potential problems. Legitimate technical teams can explain their innovations clearly and provide detailed documentation.

One pattern I noticed during the ICO era that persists today is that teams often speak in buzzwords without being able to explain their technology in simple terms. I once interviewed a team claiming to use “quantum-resistant blockchain sharding with AIoptimised consensus.” When I asked them to explain how their consensus mechanism actually worked, they gave me marketing speak about “revolutionary algorithms” but couldn’t describe a single technical detail. Their project raised millions but never delivered a working product.

Be cautious of projects that claim revolutionary breakthroughs without peer review or academic validation. Most genuine innovations build incrementally on existing knowledge.

Unsustainable tokenomics, excessive team allocations, or economic models that depend entirely on new user growth often indicate Ponzi-like structures. Be particularly cautious of projects offering extremely high yields without clear value creation mechanisms.

Projects that cannot explain how they generate value or sustain promised returns should be avoided regardless of their marketing sophistication.

Centralised control without decentralisation plans, lack of transparency in decisionmaking, or teams that dismiss community feedback often indicate poor governance structures that could lead to arbitrary or harmful decisions.

Anonymous teams making major decisions without community input create additional risks that should factor into your analysis.

Etherscan, BscScan, and similar block explorers provide transaction histories, contract interactions, and token distributions. Use these tools to verify project claims and

analyse on-chain activity.

Advanced tools like Nansen, Dune Analytics, and The Graph provide sophisticated on-chain analysis capabilities for deeper research.

GitHub provides code repositories, development activity, and issue tracking.

CryptoMiso and Electric Capital Developer Reports analyse development activity across projects.

Use these tools to assess development velocity, code quality, and team responsiveness to community feedback.

CoinGecko and CoinMarketCap provide basic market data, but tools like TokenTerminal, DeFiPulse, and L2Beat offer more sophisticated financial and usage analytics.

For DeFi projects, tools like DeBank, Zapper, and APY.vision provide portfolio tracking and

yield analysis capabilities.

LunarCrush and Sentiment Trader analyse social media sentiment and engagement. Discord and Telegram analysis tools can help assess community quality and engagement levels.

Remember that social metrics can be gamed, so use them as supporting evidence rather than primary research tools.

Develop a standardised checklist that covers all major research areas. This ensures consistent evaluation across different projects and helps prevent emotional decisionmaking.

Assign weighted scores to different criteria based on your investment priorities. Technical innovation might be more important for some investors, while others prioritise team experience or market opportunity.

Maintain detailed research notes for each project you evaluate. Include sources, reasoning, and specific concerns or strengths identified during research.

Track your research predictions against actual outcomes to improve your analytical skills over time. Understanding where your analysis was right or wrong enhances future research quality.

Initial research is just the beginning. Establish processes for monitoring ongoing developments, team updates, competitive changes, and market evolution.

Set specific triggers that would prompt additional research or reconsideration of your initial conclusions. Projects evolve continuously, and your understanding should evolve with them.

Integrate research conclusions with position sizing and risk management decisions. Higherrisk projects merit smaller allocations regardless of their potential upside.

Consider correlation risks when building a portfolio. Projects that appear independent may face similar regulatory,

technical, or market risks that could affect multiple positions simultaneously.

Apply your research framework to current projects you’re considering. Work through each section systematically, documenting findings and sources.

Compare your independent analysis with community sentiment and expert opinions. Significant divergences often indicate either overlooked factors or market inefficiencies worth investigating further.

Study failed projects that initially appeared promising. What warning signs were missed? How did the research community react? What information was available but ignored?

Some of my most valuable learning experiences came from analyzing my research failures. I once invested in a

project with an impressive technical team and solid use case, but I failed to notice that their token distribution heavily favored early investors with no vesting requirements. When the project launched, early investors immediately dumped their tokens, crashing the price despite the project’s technical merit. The warning signs were there in the tokenomics, but I was too focused on the technology to notice the economic red flags.

Analysing failures provides valuable lessons that improve future research quality and helps identify patterns that indicate potential problems.

Crypto moves rapidly, and research skills must evolve with the ecosystem. Follow security researchers, technical analysts, and experienced investors who share detailed analysis publicly.

Participate in research communities where experienced analysts share methodologies and discuss emerging trends. Learning from others’ experiences accelerates your own skill development.

DYOR isn’t just about avoiding scams—it’s about developing the analytical skills to identify genuine opportunities before they become apparent to

everyone else. The framework outlined here provides systematic approaches to evaluating crypto projects, but remember that research is a skill that improves with practice and experience.

The crypto space rewards those who combine healthy scepticism with genuine curiosity. Question everything, verify claims independently, and always remember that even thorough research cannot

eliminate all risks. The goal is making informed decisions with clearly understood tradeoffs, not finding risk-free opportunities that don’t exist.

Looking back on over a decade of researching crypto projects, from those early Bitcoin Talk discussions to today’s sophisticated DeFi protocols, I’ve learned that the most successful investors aren’t necessarily the smartest or the luckiest—they’re the

most disciplined. They follow systematic research processes, learn from their mistakes, and resist the emotional extremes that drive most crypto market cycles.

Start with small positions while you develop confidence in your research abilities. Track your analyses against outcomes, learn from both successes and failures, and gradually increase position sizes as your skills improve.

Most importantly, remember that the best research in the world is worthless without proper risk management. No single investment, regardless of how thoroughly researched, should represent a life-changing loss if it fails completely.

The crypto ecosystem needs more informed participants who make decisions based on careful analysis rather than hype and speculation. By developing these research skills, you not only improve your own investment outcomes but also contribute to a more rational and sustainable crypto market for everyone.

The tools and frameworks are available. The information is accessible. The only question is whether you’re willing to do the work that separates successful investors from those who simply got lucky during bull markets and gave it all back during the inevitable downturns.

Most crypto investors obsess over price movements while completely ignoring the mathematical foundations that determine whether those prices make any sense. They’ll debate whether Ethereum will hit $5,000 while having no idea what Ethereum’s market capitalization actually represents, or why a coin with a billion tokens can’t realistically reach $1,000 per token.

This isn’t just academic knowledge, understanding market caps and tokenomics is the difference between making informed investment decisions and falling for elaborate mathematical illusions designed

Robert Stone @StoneOnChain

to separate you from your money. After over a decade of evaluating crypto projects, I’ve seen brilliant technologies fail because of terrible tokenomics, and complete garbage succeed temporarily because they understood how to manipulate these numbers.

As someone who believes deeply in individual financial sovereignty and the power of decentralized systems to liberate people from centralized monetary control, I’ve learned that tokenomics represents either the path to genuine economic freedom or the most sophisticated financial trap ever devised. The difference lies in understanding what these

numbers actually mean and how they’re designed to work— or work against you.

The crypto space is filled with projects that talk about “democratizing finance” while creating token structures that benefit insiders at the expense of retail investors. Understanding tokenomics helps you identify which projects genuinely align with libertarian principles of fair distribution and individual empowerment, versus those that simply use freedom-oriented marketing to disguise old-fashioned wealth extraction schemes.

This isn’t just about making money, though understanding

these concepts will dramatically improve your investment outcomes. It’s about recognizing which projects are building the financial infrastructure for a more free and equitable future, and which ones are simply replicating traditional financial exploitation with blockchain technology.

Market capitalization equals price per token multiplied by total supply. Everyone knows this formula, but most people fundamentally misunderstand what it represents. When someone says “Bitcoin has a market cap of $800 billion,” they’re not saying that $800 billion worth of money has been invested in Bitcoin, or that you could sell all Bitcoin for $800 billion.

Market cap represents the theoretical value if every single token could be sold at the current market price—which is mathematically impossible. It’s a useful metric for comparison, but treating it as “total invested money” or “total value” leads to catastrophic misunderstandings about how crypto markets actually work.

I learned this lesson painfully during the 2017 ICO boom when I watched a project’s market cap “increase” by $500 million in a single day on less than $2 million in trading volume. The price moved from $0.50 to $5.00 per token, not because hundreds of millions in new money flowed in, but because there were so few sellers that small buy orders pushed the price dramatically higher.

When the inevitable crash came, that same “market cap” evaporated just as quickly, but now investors were stuck holding tokens they couldn’t sell at anywhere near the theoretical market cap price. The market cap was always an illusion based on the last trade price, not a reflection of actual market depth or liquidity.

This is why you can see altcoins with “billion-dollar market caps” that crash 90% on relatively small selling pressure. The market cap was never real in any meaningful economic sense—it was just

the mathematical result of multiplying a temporarily inflated price by the total token supply.

Most price tracking websites show multiple market cap figures that tell completely different stories about a project’s valuation. Circulating market cap uses only tokens currently available for trading. Total supply market cap includes all tokens that exist but might be locked or unavailable. Fully diluted market cap assumes all possible tokens have been created and are trading.

These differences can be enormous. A project might show a $100 million circulating market cap while having a $2 billion fully diluted market cap, meaning 95% of the tokens haven’t entered circulation yet. When those tokens unlock—through vesting schedules, staking rewards, or team allocations—the circulating supply will increase dramatically, likely crushing the price unless demand increases proportionally.

I’ve seen countless retail investors get excited about projects with “low market caps” based on circulating supply, only to watch their investments get diluted as locked tokens entered circulation. Always check the fully diluted market

cap and token unlock schedule before making investment decisions.

Comparing market caps across different crypto projects seems logical but often leads to flawed conclusions. Saying “Project X has half the market cap of Project Y, so it has more upside potential” ignores fundamental differences in tokenomics, utility, and distribution that make such comparisons meaningless.

A DeFi protocol with tokens that generate fees might justify a higher market cap than a governance token with no cash flows. A project with wide token distribution might sustain higher valuations than one with concentrated ownership. A utility token with real demand might deserve premium valuations compared to pure speculation tokens.

Market cap provides a starting point for analysis, but treating it as the primary

valuation metric leads to poor investment decisions. Focus on understanding what drives demand for specific tokens and whether the tokenomics support sustainable value creation.

Bitcoin’s fixed 21 million supply cap represents one extreme of token design—absolute scarcity that creates deflationary pressure as demand increases. This appeals to libertarian sensibilities because it prevents arbitrary supply manipulation by centralized authorities, but it also creates challenges for projects that need flexible monetary policy.

Ethereum transitioned from an inflationary model to potentially deflationary through EIP-1559, which burns a portion of transaction fees. This creates interesting dynamics where network usage directly affects token supply, aligning user activity with token holder interests in ways that traditional monetary systems cannot achieve.

Some projects use inflationary models to fund development, reward network participants, or maintain price stability. The key question isn’t whether inflation is inherently good or bad, but whether the inflation

serves legitimate purposes and whether token holders understand and consent to the monetary policy.

Avoid projects that can arbitrarily change their monetary policy without clear governance processes. Sound money requires predictable rules that cannot be changed on political whims or insider interests.

Understanding when and how new tokens enter circulation is crucial for predicting price movements and assessing long-term value. Bitcoin’s emission schedule is programmed into the protocol and decreases over time through halvings, creating predictable scarcity increases.

Many newer projects have complex emission schedules with team allocations, investor unlocks, ecosystem incentives, and staking rewards all releasing tokens at different times. I always create a timeline showing when major unlock events occur and how they’ll affect circulating supply.

One project I analyzed looked attractive until I mapped out their token unlocks. Over the following 18 months, circulating supply would triple as team and investor tokens vested. Even if the project succeeded technically, token holders

would face massive dilution that made positive price performance nearly impossible.

Pay special attention to cliff unlocks where large quantities of tokens become available simultaneously. These events often trigger significant selling pressure as insiders take profits or diversify their holdings.

Token burning permanently removes tokens from circulation, potentially creating deflationary pressure that benefits remaining holders. However, not all burn mechanisms are created equal, and some are pure marketing gimmicks designed to create temporary price pumps.

Effective burn mechanisms tie token destruction to real economic activity. Binance’s quarterly BNB burns based on exchange profits create genuine deflationary pressure tied to business performance. Ethereum’s EIP-1559 burns correlate with network usage, aligning token scarcity with actual demand for blockspace.

Be skeptical of arbitrary burn schedules or burns funded by team tokens rather than real revenue. These create temporary supply reduction but don’t address fundamental tokenomics if the underlying project doesn’t generate real value or demand.

Some projects announce massive burn percentages to generate excitement, but if the burned tokens were never in circulation anyway, the economic impact is zero. Always verify that burns affect actual circulating supply, not just theoretical totals.

How tokens are initially distributed reveals enormous amounts about a project’s true intentions and long-term sustainability. Projects where teams and founders control the majority of tokens face inherent conflicts between enriching insiders and creating value for the broader community.

During the ICO era, I evaluated projects where teams allocated 60-70% of tokens to themselves and early investors, leaving retail participants to fight over scraps while taking all the risk. These distribution models are fundamentally extractive and antithetical to the decentralized, democratizing principles that attracted many of us to crypto in the first place.

Look for projects with reasonable team allocations (typically 10-20%) subject to multi-year vesting schedules that align team incentives with long-term success. Teams that refuse to vest their tokens or demand excessive allocations are signaling that they view the project as a quick wealth extraction opportunity rather than a long-term commitment.

Institutional investor participation can provide validation and resources, but it can also create problematic dynamics for retail participants. VCs typically receive tokens at significant discounts to public prices and may have different time horizons and risk tolerances than community members.

Large VC allocations can create selling pressure when funds distribute tokens to their limited partners or take profits to return capital. This isn’t necessarily bad, but retail investors should understand they’re buying tokens that institutions acquired much cheaper.

Some projects structure multiple funding rounds with different prices, creating complex dynamics where early investors have dramatically lower cost bases than public participants. Transparency about funding terms helps

assess whether current prices provide reasonable riskadjusted returns.

Be particularly wary of projects with concentrated institutional ownership combined with low float—small amounts of selling can dramatically impact prices when few tokens are available for public trading.

The strongest projects allocate significant portions of tokens to community development, ecosystem growth, and user incentives. This creates network effects where token distribution helps build the user base needed for project success.

Airdrop strategies can effectively distribute tokens to genuine users while building community engagement. However, many airdrops are gamed by sophisticated actors who create multiple accounts to capture larger allocations, undermining the democratizing intent. This has always been a

serious problem in crypto since the beginning.

Liquidity mining and yield farming programs can bootstrap network usage but often attract mercenary capital that leaves once incentives decrease. Evaluate whether these programs create genuine long-term value or just temporary activity that disappears when rewards end.

The best community incentive programs identify and reward behaviors that create lasting value for the network— development contributions, governance participation, longterm usage, or network security provision.

“Fair launch” projects attempt to distribute tokens more equitably by avoiding premines, team allocations, or investor sales. While appealing philosophically, these models create their own challenges around funding development and incentivizing creators.

Some fair launch projects struggle with sustainability because teams lack token incentives to continue development once initial enthusiasm wanes. Others face governance challenges when no clear leadership structure exists to guide evolution.

Premines aren’t inherently problematic if they’re transparent, reasonably sized, and properly vested. The key is ensuring that premined tokens serve legitimate purposes rather than enriching insiders at community expense.

Evaluate fair launch claims carefully—some projects claim fair launches while giving insiders advance notice, better mining equipment, or other advantages that undermine the fairness principle.

Pure governance tokens face a fundamental challenge: voting rights alone rarely justify significant economic value unless the governance decisions have meaningful financial impact. Many governance tokens trade purely on speculation rather than actual utility demand.

Effective governance tokens control valuable resources like protocol fees, treasury funds, or

upgrade decisions that directly affect token holder wealth. MakerDAO’s MKR token accrues value because governance decisions affect the stability and profitability of the DAI system, creating real economic stakes for voters.

Be sceptical of governance tokens where the main decisions involve spending other people’s money (token holders) rather than managing shared resources that benefit all participants. These often become vehicles for insiders to extract value through “governance” decisions.

Look for governance systems with skin in the game—where bad decisions cost governance token holders real money, creating incentives for thoughtful decision-making rather than political theatre.

The strongest utility tokens provide access to services or networks that become more valuable as more people use them. Ethereum’s ETH is required for transaction fees and smart contract execution, creating demand that scales with network usage.

Utility tokens work best when the token is necessary for core functionality rather than artificially required. Some projects force token usage through smart contracts when

traditional payment methods would be more efficient, creating artificial utility that doesn’t enhance user experience.

Network effect utility tokens can create powerful positive feedback loops where increased usage drives token demand, higher prices attract more development and users, and the cycle continues. However, these same dynamics can work in reverse during downturns.

Evaluate whether the token utility is genuinely necessary or whether it’s just a way to capture value from users who would prefer alternative payment methods.

Tokens that generate fees or cash flows from real economic activity represent some of the strongest value propositions in crypto. These create measurable returns that can be evaluated using traditional financial metrics like price-toearnings ratios.

DeFi protocols often distribute trading fees, lending interest, or other revenues to token holders, creating cash flow streams that justify valuations. However, verify that these cash flows come from real economic activity rather than circular token incentives.

Some projects promise fee distributions but actually pay token holders with newly minted tokens rather than real revenue. This creates the illusion of cash flows while actually just diluting the token supply.

Calculate the actual yield rates and compare them to alternative investments after accounting for token price volatility and potential regulatory risks.

Proof-of-stake networks require token holders to stake their holdings to participate in network security, creating demand pressure as staked tokens are removed from circulation. This can create positive supply/demand dynamics for successful networks.

However, staking rewards often come from inflation rather than real economic value, meaning stakers maintain their percentage ownership while non-stakers get diluted. The real return depends on network

adoption and fee generation, not just the nominal staking rate.

Some projects offer artificially high staking rewards to incentivize participation, but these high rates are often unsustainable without genuine economic value creation. Calculate the real returns after accounting for token inflation and potential price impacts.

Consider the opportunity cost of staking, locked tokens can’t be traded, used in DeFi, or deployed elsewhere. Staking only makes sense when the total return (rewards plus potential price appreciation) exceeds alternatives.

NVT ratios attempt to apply price-to-earnings style analysis to crypto networks by comparing market capitalisation to transaction volume. Like traditional valuation metrics, NVT works best for mature networks with stable usage patterns.

High NVT ratios might indicate overvaluation or network optimisation (more value transferred per transaction). Low ratios could signal undervaluation or network inefficiency. Context matters enormously, comparing NVT across different types

of networks often produces misleading conclusions.