BLINK – AND HERE WE ARE – OUR ANNUAL CONFERENCE IS COMING!

That’s right…it’s the most wonderful time of the year for local government nance folk. The time when nancial plan and tax rate bylaws are adopted, nancial statements are audited and LGDE data is submitted. Now is the time for us to gather, laugh, console, and marvel at the shared challenges and successes of our membership. To learn more about best practices, strategies and updates to issues a ecting our sector.

This year’s conference in Kelowna aims to build on the conference theme and sessions from 2025 with a twist - we hope to inspire more in session discussions through the use of case studies. Some of the issues we will be tackling include housing, long-term nancial and capital planning, and intergenerational equity as we build, and sustain, our local governments.

While we lean in on these topics we will also be exing our leadership competencies and grow our abilities to best manage the challenges and the opportunities. The Leadership Competency Framework established by GFOABC helps activate thinking

pathways to problem solving, which we do every day; so, they are certainly skills worth honing.

We’re not only building strong communities that can withstand growth, climate, and economic impacts, but also protecting existing services in the face of retraction. Being resilient means being responsive to change, adapting to moves on the chess board and planning with imperfect information and limited nancial resources. This year is also an election year, so yes, to a degree, the players may morph, but the goal is the same, providing quality service for the lives of people today and leaving quality infrastructure, environment and security for those of tomorrow - at a fair price.

When I attend the conference, I am repeatedly reminded of our similarities and the resourcefulness, passion, strength and unity within our membership. It is an opportunity for colleagues to learn from and with each other - so we can continue providing the best advice to keep our communities thriving in all the various life cycles, natural elements

and time periods that our part in this journey plays. I look forward to the energy and conversations that the 2026 conference will inspire. So, see you in Kelowna, where building resilient communities is the theme and building lasting friendships with fellow colleagues is always on the agenda.

Corinne Bomben, GFOABC President

GFOABC STAFF

Kala Harris, Executive Director

Anne Adidu-Lawal, Manager, Professional Development & Education

Tim Thakker, Manager, Member Services & Communications

Charlotte Osborne City of Cranbrook SECRETARY TREASURER

Teri Fong

Alberni-Clayoquot Regional District DIRECTOR AT LARGE

Carla Fox Thompson Nicola Regional District DIRECTOR AT LARGE

Elio Iorio District of North Vancouver

AT LARGE

BOARD OF DIRECTORS

Corinne Bomben, President

Kelly Lownsbrough, Vice President

Charlotte Osborne, Secretary Treasurer

Rianna Lachance, Past President

Kelly Lownsbrough Fraser Valley Regional District VICE PRESIDENT

Rianna Lachance District of Oak Bay PAST PRESIDENT

Nicole Gervais MFABC DIRECTOR AT LARGE

Lenora Lee KPMG DIRECTOR AT LARGE

Dave Hallinan City of Kamloops DIRECTOR AT LARGE

Jeffrey Lovell City of Port Coquitlam

DIRECTORS AT LARGE

Teri Fong, Alberni-Clayoquot Regional District

Carla Fox, Thompson Nicola Regional District

Nicole Gervais, MFABC

Dave Hallinan, City of Kamloops

Elio Iorio, District of North Vancouver

Lenora Lee, KPMG

Je rey Lovell, City of Port Coquitlam

DIRECTOR

DIRECTOR AT LARGE

LEANING IN ON RESILIENCE

“Resilience” may be one of the most overused words in recent years. It appears in strategic plans, policy documents, conference themes, and council reports. And yet — despite its frequency — it is di cult to deny that resilience underpins much of what is required of local government today.

The landscape is changing. Housing pressures, infrastructure demands, shifting economic realities, and growing community expectations require steady judgment

and long-term thinking. They require professionals who can balance immediate needs with future obligations.

Behind the scenes, our team has been working steadily to ensure we are ready — ready to welcome you to Kelowna, ready to facilitate meaningful conversations, and ready to build on the momentum of last year’s conference. That momentum has not been lost. In fact, we are seeing a signi cant increase in participation, which speaks to the continued commitment of this membership.

This year’s theme — Building Resilient Communities: Housing and Infrastructure — speaks directly to the stewardship role nance professionals carry. Housing pressures and infrastructure demands are not short-term challenges. They require disciplined planning, thoughtful risk assessment, and careful balancing of today’s priorities with tomorrow’s responsibilities.

The shift toward more case-based discussions is intentional. It is tied directly to a strategic goal: positioning the conference not only as a forum for information, but as a platform for dialogue. The issues we are exploring require more than presentations. They require judgment, exchange, and the opportunity to think through complexity together.

Creating space for meaningful dialogue strengthens professional practice — and, in turn, strengthens the resilience of the Association itself. GFOABC is most resilient when its members are actively engaged, sharing insight, challenging assumptions, and learning from one another.

Our keynote will invite us to consider another dimension of resilience: gratitude. Not as a platitude, but as a practice. In professions that demand rigour and accountability, gratitude can feel secondary — yet it often sustains teams and reinforces the purpose behind the work.

Resilience is not only about nancial plans and infrastructure strategies. It is also about community — about the professional networks that allow us to test ideas, seek advice, and support one another.

The Welcome Reception at King Taps will o er space to reconnect with colleagues who understand the realities of this work. Our Gala evening at 50th Parallel Estate Winery will give us the opportunity to gather and celebrate together — not through formal presentations or interruptions, but through conversation and connection.

Finance professionals may not always speak openly about how demanding the work can be — but they do value time together. So come raise a glass. Share a story. Reconnect with peers who understand both the weight and the purpose of what you do.

Resilient communities depend on resilient nancial leadership. And resilient leadership is strengthened when we gather — to learn, to re ect, and to support one another.

I look forward to seeing you in Kelowna.

Kala Harris, Executive Director

Manager, Professional Development & Education

ANNE ADIDU-LAWAL

I’M ANNE LAWAL, AND IT’S GREAT TO BE PART OF THE GFOABC TEAM!

If someone had told me a decade ago that I’d be genuinely enthusiastic about understanding nancial lingo and poring over the implications of budget changes for local governments and nancial stewardship, I probably would have said, “Nope, not me”, especially considering I ran away from the banking sector once upon a time, but here I am! I am thrilled to be part of the Government Finance O cers Association of British Columbia—and yes, nancial governance and everything that comes with it has begun to grow on me.

My professional journey has taken me through various stages, including my work in nonpro t leadership, gender inclusion initiatives, and organizational development. Along the way, I’ve facilitated leadership programs, supported strategic planning sessions, and helped organizations strengthen governance and accountability. At the heart of it all has been one consistent goal: building capacity, improving systems, and making sure the work I do has a meaningful impact on the communities I serve.

What drew me to GFOABC? Well, di erent phases of life come with upgrades. I decided to upgrade to the premium ‘next level’ package, and public nance came with it! Well, jokes aside, I genuinely believe public nance is the centre of real community impact. Having worked in the development sector, I have seen rsthand how important resource management and allocation are in the development and transformation of communities. I was drawn to the organization’s commitment to excellence

and its vital role in supporting local governments across British Columbia.

I’m particularly energized by the opportunity to develop training programs and resources that make nancial processes more accessible and easier to navigate. My approach tends to be translational—I enjoy bridging the gap between complex nancial frameworks and clear, practical language. I believe in breaking down concepts into manageable steps, because good information shouldn’t be buried in documentation that no one has time to read.

My working style is collaborative, and I value environments where diverse perspectives are welcomed, where integrity and innovation go hand in hand, and where we can learn along the way.

These days, I look forward to travelling, having meaningful conversations, or spending quality time with my daughters, who, incidentally, are excellent teachers of negotiation and resource allocation. I’m a lifelong learner, always exploring new ideas that inspire both my professional path and my personal growth.

I’m looking forward to contributing to this association and to the work ahead. Public nance matters, and I’m glad to be a part of the people who take it seriously.

Manager, Member Services & Communications

TIM THAKKER

DEAR GFOABC COMMUNITY,

I am absolutely thrilled to introduce myself as your new Manager of Member Services & Communications, so that you can access timely learning and stronger peer connections. Stepping into this role is an exciting milestone for me, and I am eager to get to know the incredible professionals who make up this association.

To give you some background on my professional journey, I hold a Bachelor of Commerce in Entrepreneurial Management from Royal Roads University. I started my career on the investment side as a nancial planner at RBC before spending the last eight years with the Canada Revenue Agency in Collections. Navigating the complexities of nance and regulatory environments has given me a deep appreciation for the important, often challenging work that local government nance professionals do every day.

Alongside my nance background, I have a strong passion for communication and community building. For the past six years, I have been an active member of Toastmasters, serving in various executive roles and currently as a Division Director. This experience has strengthened my belief in the importance of active listening, clear communication, and empowering others— principles I intend to apply in supporting all of you at GFOABC.

On a more personal note, when I’m not focused on member services, you can usually nd me in the kitchen experimenting with new baking recipes, currently testing my patience at making sourdough bread. If anyone has

a tried-and-true recipe or baking tip, I would love to hear from you! I also love getting out on the golf course, though I will be the rst to admit that my swing is a work in progress and I am absolutely terrible at the game (I should probably buy a new Driver).

My primary goal right now is to listen and learn from you. I want to understand how GFOABC can best support your professional growth and day-to-day challenges. As a rst step, I would love to hear from you: What is one resource or tool that would make your job easier this quarter? Please feel free to reach out with your thoughts, introduce yourself, or say hello if you see me at any of our upcoming events.

I look forward to connecting with you soon!

Warm regards, Tim

ANNUAL CONFERENCE

ANNUAL CONFERENCE AND AGM

Wednesday, May 27, 2026 – Friday, May 29, 2026

The 2026 Annual Conference will take place at the Delta Hotels Grand Okanagan Resort in Kelowna. The conference will address the dual challenges of a ordability and a widening infrastructure gap. Through keynote presentations, panel discussions, and interactive sessions, participants will explore how nance leaders can approach a ordability and infrastructure challenges with innovation and resilience.

PRE-CONFERENCE WORKSHOPS

Monday, May 25, 2026 – Tuesday, May 26, 2026

Pre-Conference Workshops are o ered in-person and separately from the Annual Conference. These workshops o er a fantastic opportunity for further professional development, and to explore a speci c local government nance topic in-depth. Past PreConference Workshop topics include development cost charges, municipal property tax sales and a session dedicated to regional district topics.

SPRING PD FALL PD

PROPERTY TAX 101 WORKSHOP

Tuesday, April 7, 2026

Tuesday, April 14, 2026

Tuesday, April 21, 2026

Property Tax is the single largest source of local government revenue. Learn more about property tax collection through this three-part virtual workshop.

All sessions run from 9:00 am to 11:30 am

FALL PD

November 24-25, 2026

The annual Fall PD Workshops take place in Vancouver every November. These in-person, full-day workshops cover a breadth of local government nance topics and are an opportunity to network with peers one last time before the end of the year. Past sessions include Financial Reporting, Budgeting Best Practices, and Ethics and Leadership.

DELTA HOTELS GRAND OKANAGAN RESORT, 1310 WATER ST, KELOWNA, BC

BOOT CAMP

BOOT CAMP FINANCE OFFICERS DEVELOPMENT PROGRAM

Monday, August 10, 2026 - Friday, August 14, 2026

Boot Camp is our agship residential program. Grounded in the legislation that guides the role of the nancial o cer and the Leadership Competency Framework (LCF), it helps participants connect statutory responsibilities with the leadership behaviours needed to guide teams and in uence decisions. Each participant receives the Boot Camp Toolkit — a comprehensive binder of templates, legislative references, and leadership resources to support continued growth as con dent, capable nancial leaders.

STRATEGIC FINANCIAL LEADERSHIP

STRATEGIC FINANCIAL LEADERSHIP

This cohort-based program is a blend of in-person workshops, virtual meetings, one-on-one executive coaching, self-guided learning, and collaboration – helping participants develop leadership competencies, build relationships, and make a bigger impact on their organization.

UNIVERSITY OF VICTORIA MORE INFORMATION

VICTORIA

MORE INFORMATION

STEVE FORAN

Steve Foran’s mission is to create one billion happier people. A former electrical engineer, his career pivoted during his MBA when he uncovered the powerful connection between gratitude and leadership. Awarded the Gold Medal for academic excellence, Steve laid the groundwork for a career dedicated to helping leaders and organizations thrive through gratitude.

With more than 18 years of research and practice, Steve has become a leading expert in gratitude-driven leadership, combining positive psychology and business strategies to foster happier, more engaged workplaces. In 2006, he founded Gratitude at Work, a global initiative helping leaders embed gratitude into their cultures, resulting in higher employee engagement, morale, and business performance.

Steve is the author of Surviving to Thriving: The 10 Laws of Grateful Leadership, which is recommended by The Greater Good Science Centre at UC Berkeley. Steve has delivered keynotes and workshops internationally, connecting with audiences from Asia to Europe to North & South America. He resides in Halifax, Nova Scotia, with his wife Lynda, where they bribe their kids Nick and Stef (with promises of sleep) in order to spend time with their grandkids—Max, Liam, Maesey, and Sophie.

Committed to inspiring the next generation of leaders, Steve continues to empower organizations through gratitude, helping them unlock their full potential and achieve lasting happiness and success.

WELCOME RECEPTION

Join us at King Taps Kelowna Lakeside on Tuesday, May 26 from 6:30–8:30 pm to kick o the conference with our Welcome Reception. It’s a relaxed waterfront gathering where members, partners, and exhibitors can reconnect and meet new colleagues over appies and drinks. A drink ticket is included, we look forward to welcoming you in Kelowna!

SPONSORED BY:

KEYNOTE SPEAKER

We respectfully acknowledge that this conference will take place on the traditional, ancestral, and unceded territory of the Syilx Okanagan people. We are grateful for the opportunity to gather, learn, and share knowledge on these lands.

ANNUAL CONFERENCE

CASE STUDIES

FOUR CONVERSATIONS THAT WON’T STAY COMFORTABLE: 2026 ANNUAL CONFERENCE

Applying the GFOABC Leadership Competency Framework in Practice. At the 2026 Annual Conference in Kelowna, we will host four member-led dialogue sessions to bring the GFOABC Leadership Competency Framework to life. Instead of presenting abstract theories, these sessions focus on practical applications of strategic leadership, critical thinking, and collaborative problem-solving. By engaging with unresolved questions and real-world limitations, nance leaders will exercise their professional judgment through structured, member-to-member discussions on the sector’s most urgent challenges.

ERP CHALLENGES AND OPPORTUNITIES

Moving away from legacy nancial systems is more than a technical challenge; it requires signi cant leadership and organizational change. This session recognizes that the human costs of ERP implementations— such as strained sta capacity, operational disruption, and potential loss of institutional knowledge—are often underestimated. Participants at all levels of ERP maturity will share their experiences in making a strong case for change, reducing risks, and maintaining daily operations during a lengthy transition.

LONG-TERM FINANCIAL PLANNING AND CAPITAL PLANNING

There is often a signi cant gap between community expectations outlined in a ve-year nancial plan and an organization’s actual capacity to deliver. Focusing on practical judgment rather than theoretical frameworks, this session addresses the complexities of planning when delivery expectations exceed sta ng, procurement bandwidth, and council alignment. Through member consulting, attendees will share real-world lessons and best practices for managing the political, governance, and data issues that complicate e ective capital planning.

ANNUAL CONFERENCE

CASE STUDIES

INTERGENERATIONAL EQUITY AND ASSET MANAGEMENT

Every capital decision in uences the nancial future for upcoming councils, often leading to deferred maintenance or infrastructure that is a ordable to build but unsustainable to upkeep. This discussion frames intergenerational equity as a core duty of leadership, challenging participants to balance immediate political and service demands with long-term community stewardship. Finance leaders will share examples of how short-term decisions create long-term obstacles and work together on strategies to address systemic barriers to more sustainable choices.

HOUSING: FINANCIAL REALITIES AND SYSTEM CONTEXT

Finance o cers are increasingly responsible for reconciling rapid provincial housing targets and council-supported development with revenue frameworks that were not designed for such swift growth. This session moves beyond policy debates to critically examine where these housing expectations most sharply clash with local government nancial realities. Using a triad consulting format, participants will explore the hidden risks, organizational strains, and di cult nancial trade-o s created by mounting housing pressures.

GALA EVENING

Celebrate the highlight of the conference at our Gala Evening on Thursday, May 28, set among the vineyard views of 50th Parallel Estate Winery in Lake Country. Members, partners, and exhibitors will gather for a reception and gala dinner featuring exceptional local cuisine and warm community spirit. Transportation is included, so all you need to do is show up and enjoy the evening — from 6:30 pm until late. We look forward to welcoming you!

SPONSORED BY:

FOCUS GROUP

THE LEARNINGS BEHIND THE DATA: UNPACKING RESULTS IN CAPITAL PLANNING AND DELIVERY THROUGH DISCUSSION

Local governments across BC are navigating increasingly complex capital programs — balancing aging infrastructure, growth pressures, a ordability, and limited organizational capacity. While many communities are strengthening their capital plans, delivering those plans as intended remains a shared challenge.

In the December Quarterly Question survey, members re ected on where local governments are strongest in capital planning and delivery, where challenges are most acute, and how e ectively key nancial tools are being used. The results are a starting point — but the real value is in the conversation.

At the Annual Conference, we are hosting a facilitated focus group to explore these results and learn from one another’s experiences. Participants will dig into what supports e ective capital prioritization, what contributes to the gap between plans and delivery, and what actions have worked in practice.

WHO SHOULD JOIN

This session is for nance professionals and sta involved in capital budgeting, asset management, or capital program oversight. Whether your organization delivers most of its capital budget or struggles to do so, your perspective is valuable.

Can’t attend? Indicate your interest when registering to receive follow-up insights, or contact o ce@gfoabc.ca.

What’s Trending in the Online Forum?

BC BUDGET

2026: MEMBERS DIG INTO THE DETAILS

WHEN THE PROVINCE PRESENTED BUDGET 2026 ON FEBRUARY 17, GFOABC PROMPTED A DISCUSSION ON THE FORUM WITH A BRIEF OVERVIEW OF WHAT THE FISCAL PLAN MEANS FOR LOCAL GOVERNMENT FINANCES. MEMBERS CONTINUE TO ENGAGE BY ASKING QUESTIONS, FOCUSING ON SPECIFIC LINE ITEMS AND EXAMINING THE IMPACT ON THEIR COMMUNITIES.

PST ON PROFESSIONAL SERVICES

The new application of PST to architectural, engineering, and geoscience services, applied to 30% of the purchase price, has garnered the most attention. Members have been exploring what this means for their budgets, with one example estimating the cost at about $35,000 on $500,000 in consulting fees. The discussion includes how local governments are planning to absorb these additional costs.

For local governments with signi cant capital programs, the issue also involves grant-funded projects. Members are considering whether the new PST diminishes the purchasing power of provincial and federal infrastructure grants, and the implications for capital output over the planning period. The discussion also

addresses potential impacts on development costs and residential construction.

Members have raised the question of whether local governments should seek an exemption from this change, and the thread includes early discussion of how that case might be advanced.

TRANSFER REDUCTIONS

The budget reduces local government appropriations from $218 million to $208 million in 2026/27 — a $10 million reduction. UBCM has stated it is seeking clarity on which speci c programs will be a ected. Members are watching this closely, particularly where provincial transfers represent a larger share of operating revenue.

OTHER ITEMS MEMBERS ARE FLAGGING

Forum members have also uncovered details beyond the headline gures. Discussion in the thread has identi ed the removal of the Rural and Northern Home Owner Bene t — reported as a $200 per-property change — as an item to consider in tax roll preparation and ratepayer communications. Members are encouraged to verify the speci cs as they relate to their own communities.

The thread also references increases to the Speculation and Vacancy Tax, changes to the Additional School Tax rates on higher-value properties, and a shift from simple to compound interest on the Property Tax Deferment Program. Each carries implications for revenue managers and property tax teams during the current budget cycle.

JOIN THE CONVERSATION

The Budget 2026 thread remains active. If your community has started working through the impacts, whether adjusting capital timelines, revising fee estimates, or preparing ratepayer communications, the forum is the place to share what you’re seeing.

IMPLEMENTING SOCIAL PROCUREMENT IN SMALL CANADIAN MUNICIPALITIES: PRACTICAL LESSONS

SOCIAL PROCUREMENT IS INCREASINGLY RECOGNIZED AS A MEANINGFUL WAY FOR MUNICIPALITIES TO ALIGN PURCHASING DECISIONS WITH COMMUNITY VALUES. FOR SMALL CANADIAN MUNICIPALITIES, HOWEVER, IMPLEMENTATION PRESENTS UNIQUE AND OFTEN UNDERESTIMATED CHALLENGES. THE VILLAGE OF PEMBERTON’S EXPERIENCE OFFERS PRACTICAL INSIGHTS INTO HOW SOCIAL PROCUREMENT CAN BE ADVANCED PRAGMATICALLY, EVEN WITH LIMITED CAPACITY. Pemberton’s approach is grounded in long-standing collaboration with the Lil’wat Nation and a broader commitment to equity, inclusion, and local economic development. In late 2024, the municipality updated its procurement policy to embed social objectives, including support for Indigenous-owned and local businesses. While the policy was implemented quickly, operationalizing it has proven more complex.

Three core challenges emerged. First, an inconsistent understanding of social procurement across departments risks uneven application and administrative burden. Second, the absence of standardized social impact metrics makes it di cult to balance social value against scal responsibility, particularly when local options carry higher costs. Third, limited sta capacity constrains the use of complex environmental or social evaluation tools.

In response, Pemberton adopted a pragmatic, decentralized approach. Departments integrate social considerations where feasible; preference is given to Indigenous and local suppliers when bids are otherwise equal; and knowledge sharing across departments is prioritized. The municipality is also strengthening outreach to Indigenous and local suppliers, recognizing that limited visibility into supplier capacity is a barrier in itself.

Critically, social procurement is being integrated into the annual budget process, reinforcing awareness that every tax dollar can deliver broader community value. Pemberton’s experience demonstrates that, for small municipalities, success lies not in perfection, but in incremental, capacity-aligned progress supported by collaboration and shared learning.

“FOR SMALL MUNICIPALITIES, SUCCESS LIES NOT IN PERFECTION, BUT IN INCREMENTAL, CAPACITYALIGNED PROGRESS SUPPORTED BY COLLABORATION AND SHARED LEARNING.”

SOCIAL PROCUREMENT AT SCALE: LESSONS FROM A MEDIUM-SIZED MUNICIPALITY

In contrast to smaller local governments, mediumsized municipalities often have greater organizational capacity to implement social procurement consistently and measurably. The City of Courtenay provides a useful example of how scale, governance alignment, and modest resourcing can translate policy into practice.

Driven by Council’s strategic priorities, the City adopted its social procurement policy in 2023. Unlike pilot or discretionary models, Courtenay’s approach integrates social procurement considerations into all competitive bidding processes. Vendor evaluations explicitly consider social value, environmental responsibility, and ethical business practices alongside traditional criteria such as experience, quality, and cost. Importantly, social considerations inform, but do not disproportionately impact, best-value decision-making, preserving scal accountability.

To expand access for local small and medium-sized enterprises (SMEs), the City increased its three-quote and direct-award thresholds. This adjustment enables greater participation by local suppliers while remaining fully compliant with applicable trade agreements, as the thresholds remain within the limits of the New West Partnership Trade Agreement and other trade agreements.

Since its implementation, the City’s social procurement framework has been applied to more than 100 competitive procurements, totalling tens of millions of dollars in spend across a wide range of industries. One notable lesson has been that the private sector is often ahead of government in this space. Environmental, Social, and Governance (ESG) frameworks are now commonplace in private enterprise, and many vendors are already wellpositioned to address social value considerations.

“THE FULL POTENTIAL OF SOCIAL PROCUREMENT WILL ONLY BE REALIZED THROUGH BROADER, COORDINATED ADOPTION ACROSS ALL LEVELS OF GOVERNMENT.”

Looking ahead, the City is focused on improving reporting and outcome measurement. However, Courtenay also recognizes that the full potential of social procurement will only be realized through broader, coordinated adoption across all levels of government, ensuring consistency, shared learning, and meaningful impact at scale.

SCOTT HAINSWORTH has over 25 years of procurement experience, including more than 15 years in the public sector. He holds a Bachelor of Commerce and is completing an MBA. His background includes roles in the private sector, local government, post-secondary education, and a provincial Crown corporation.

YUN KE (DAVID) NI is Chief Financial OfÏcer for the Village of Pemberton. He brings over 12 years of experience as a CFO/Director of Finance/Treasurer across multiple local governments, with expertise in nancial planning, analysis, reporting, risk management, cash management, and long-term nancial planning. Originally from China, he holds a CPA (Canada), CICPA (China), and an MBA from China University of Mining & Technology. He believes efÏcient nancial services are key to helping organizations and communities achieve their strategic goals.

STRONGER TOGETHER: THE PIPELINE ASSESSMENT STORY

“...WORKING COLLABORATIVELY, LOCAL GOVERNMENTS CAN MEANINGFULLY INFLUENCE OUTCOMES.”

In September 2025, the District of Hope was noti ed of a substantial reduction in the assessed value of transmission pipeline properties for the 2026 taxation year. The projected decrease was approximately 28% compared to 2025 values. This reduction represented an estimated $640,000 decrease in property tax revenue.

A secondary concern was the lack of communication from BC Assessment to municipalities regarding the revaluation process. The District received this information with little warning while already in the midst of our nancial planning process. Based on preliminary analysis, o setting the lost revenue would have required an approximate 8.0% tax rate increase for residents.

Recognizing that Hope was unlikely to be the only municipality a ected, I raised the issue through the GFOABC forum. Immediate responses con rmed that other communities were experiencing similar impacts. Within weeks, regional Directors of Finance (with Mike Veenbas helping coordinate discussions) were sharing information and aligning on a consistent approach. The agreed strategy included:

• Bringing the issue forward to Council

• Council issuing letters to the Ministry of Finance and the Premier

• Advocating through local MLAs

As municipalities began informing their Councils and engaging the media, momentum built across the province. While each region acted independently, the coordinated response elevated the issue and increased provincial awareness.

For our Financial Plan, we presented Council with a budget that clearly re ected the pipeline valuation impact to ensure full transparency. We also outlined contingency measures should the valuation be adjusted. Following adoption of the Financial Plan, BC Assessment reversed the revaluation.

Although the immediate impact was resolved, the issue underscores the need for improved communication between agencies such as BC Assessment and municipalities. It also demonstrates the e ectiveness of coordinated municipal advocacy. By working collaboratively, local governments can meaningfully in uence outcomes that a ect our communities.

for the past four years. On top of Finance, Mike’s role encompasses, IT, Communications, Risk Management and Social Media. Mike’s goal for the upcoming year is to shoot under 100 at least three times during the year, which for his golf game would qualify as a miracle.

MIKE OLSON has been the Director of Finance at the District of Hope

Collectors’ Corner:

TAX SALE – ESCHEAT REVISITED

the Province at the time of dissolution of the corporation. However, the Escheat Act S4 also states that if, within 2 years from the date of its dissolution, a corporation is revived under any Act, the revival has the e ect as if the land of the corporation had not escheated to the government, and the land vests back in the corporation.

Business Corporations Act S364 which states that a company that is restored is deemed to have continued in existence as if it had not been dissolved. How does this a ect tax sale?

Local Government Act S645 (1) states: “At 10 a.m. on the last Monday in September, at the council chambers, the collector must conduct the annual tax sale by o ering for sale by public auction each parcel of real property on which taxes are delinquent.” So, with regards to a property that has delinquent taxes that is owned by a whether active or dissolved, the property is subject to tax sale. The company could also be dissolved after the tax sale during the one year redemption period. What if the company is dissolved and the property is sold at tax sale and subsequently redeemed within the one year redemption period? Then the property remains owned by the dissolved company. But what if the property is not redeemed after the one year redemption period? Land Titles will not transfer the ownership of a property that has escheated to the Crown without rst receiving a letter of non-objection from the Province (Resource, Environment and Land Law Group, Legal Services, Ministry of Attorney General). The question at this point is what would happen if the Province refused to issue the letter of non-objection thus retaining ownership of the property that was previously sold at tax sale and not redeemed? The LGA S664 says that if the registrar of land titles refuses to register the title in the name of a purchaser of property at a tax sale (subject to appeal), Sub (2) states: “The municipality is deemed to have been declared the purchaser of the property at the tax sale and the municipality must refund the purchase price, without interest, to the purchaser.”

A couple of side points are that the Province does not proactively check if a company is dissolved. Therefore, the taxes may have been paid though the company had been dissolved for many years. Unless there is a reason,

the Province does not initiate a transfer of an escheated property title to the Province. Once a letter of nonobjection has been requested, it may take a long time for the Province to reply. Also, it is assumed that the municipality applies for the letter of non-objection from the Province.

PS: Check out Michael Moll’s article in the GFOABC September 2025 Newsletter “Aboriginal Title and Tax Sales”.

DOUG STEIN has worked in municipal nance for over 40 years. He retired from his position as Manager of Revenue Services for the District of Saanich in 2011 and now facilitates GFOABC workshops and webinars and consults on property taxation issues. Doug is very involved with the Collectors’ Forum, is a GFOABC Life Member and a CPA, CMA.

CLIMATE-RELATED RISK ASSESSMENT AND DISCLOSURE REQUIREMENTS

There is no shortage of new climate-related regulations, standards, and resources for assessing and documenting disaster risk and resilience. Speci c to local governments in BC, I’m primarily referring to:

1. the regulations, arising from the Emergency and Disaster Management Act (EDMA) adopted in 2023, and expected to drop this spring, which outline local government requirements and post-disaster nancial assistance eligibility and processes for local governments and the private sector,

2. the IPSASB public sector climate disclosure standards published last month, and expected to be adopted (possibly with modi cation) in the Public Sector Accounting Handbook by the end of the year.

3. the excellent resources, made publicly available, through the ClimateReadyBC platform, which can assist local governments in nding and using the best available data and practices to satisfy both the climaterelated legislated requirements and the new disclosure standard

These policy documents and guides are numerous, voluminous, and technical. Even with the growing repository of resources, just thinking about how to comply with these upcoming requirements can be overwhelming, particularly for local governments already running at full capacity, and having nance departments with no shortage of existing reporting burdens.

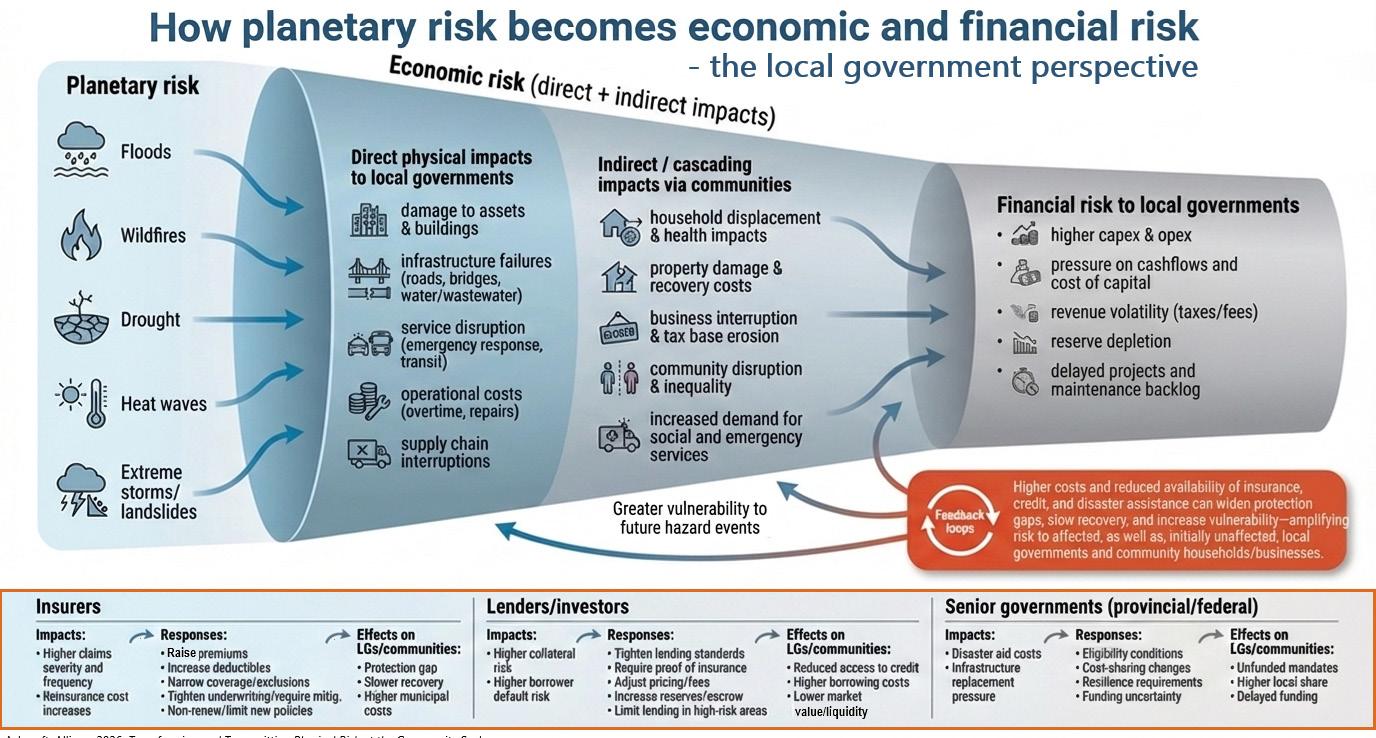

This has me thinking about how the Municipal Finance Authority might be helpful to Finance departments and the development of their climate risk disclosures?

As a preliminary step, I’m writing this article to talk a bit about how I’ve been approaching this nascent work and to share some ideas for how Finance teams in local government might make some strides of their own.

From my current perch as MFA’s Sustainability Director, I am privileged to have the mandate (and bandwidth) to explore the actual and potential nancial implications to communities, local governments, and the MFA, arising from climate-related risks and how we might retain/ improve our nancial health and long-term stability through climate-resilient strategies and investments.

I’m stepping into this conversation as someone with relevant experience and complementary skills to the work of climate-related risk and disclosures through a combined 30 years working rst in audit at a Big Four, and subsequently on climate and sustainability in (and with) local governments.

A. THE IMPORTANCE OF ESTABLISHING GUIDEPOSTS

I have erected these guideposts as reminders to myself when tackling the work of identi cation, assessment, management, measurement and disclosure of climate risks to the Municipal Finance Authority of BC (MFA) and the governments we lend to and invest in.

These have been helpful for establishing boundaries and balancing the MFA’s priorities in this area, and also when trying (not always succeeding) with maintaining focus amidst the seemingly endless (and everchanging) stream of data, information, questions, and guidance that encircle us like a tornado around this topic.

• Understand how climate risk is transformed and transmitted across the system within which you operate

• Consider which changes in macro-level circumstances create nancial risk ampli ers

Continued on page 24...

...continued from page 23

• Monitor and manage what matters most

• Measure what is meaningful, not just what is quanti able

• Document and disclose that which is needed to be decision-useful to di erent users, both internal and external to the organization.

B. FINANCE ON THE MOVE

Some ideas around how nance departments might:

• Participate in EDMA-related projects (leading up to compliance by January 2027)

• Produce their assessment of climate-related nancial risks and the corresponding strategies and controls they’ve put in place for managing and monitoring them (in anticipation of climate disclosures being included alongside your nancial statements and annual reports for scal years beginning in 2028).

I recognize that many of you have already embarked on some or all of these. I also o er the caveat that this isn’t a comprehensive list.

The areas below represent opportunities to leverage new and existing work being done inside your organizations or by/with various trusted partner organizations. By connecting these dots, greater e ciencies and consistency in climate disclosures may prevail.

1. Support the development of EDMA-required documents, and participate where and when you can.

The development of climate-integrated hazard risk and vulnerability assessments (HRVAs), and corresponding Emergency Management Plan (EMP) and Business Continuity Plan (BCP) will help Finance teams in better understanding the:

a. Managed and unmanaged planetary (physical)risks for di erent hazards (and for di erent scales and scope of each foreseeable hazard),

b. Impact these physical risks, are having, or may have:

i. Directly, to your organization’s assets, infrastructure, and operations

ii. Indirectly, to your organization through impacts to your local economy and residents.

c. Options available, and priorities for responding to these physical risks and their economic impacts

2. Leverage the EDMA-required internal use documents (which name and score the locally-relevant physical risks over the short to long-term, and the strategies for managing and monitoring/updating these risks), to identify and evaluate the:

a. Transmission channels through which the harm (damage and disruption) to people, assets, and infrastructure in your community can have:

i. Direct economic impacts to your organization and your residential, commercial, and industrial taxpayers

ii. Direct nancial risk a ecting the long-term scal sustainability of your organization, and the nancial stability and ongoing viability of your residential, commercial, and industrial taxpayers

iii. Indirect nancial risk to your organization from the cascading e ects of any sustained economic impacts, which result in nancial strain and instability for your community and the other municipalities (and their taxpayers) within your regional district.

iv. Financial risk ampli ers to emerge through the creation of feedback loops which compound economic impacts and nancial

risk to your organization, your taxpayers, or your regional district and neighbouring municipalities.

b. Structures and mechanisms which protect your organization, your taxpayers, the local economy, or the broader nancial system through risk mitigation or risk transfer (sharing).

The MFA has identi ed three areas as having the potential to materially a ect the MFA’s assessment of our climate-related nancial risk pro le over the medium to long-term. We would need to amend some of our key assumptions were signi cant changes in these policy, market, and legal realms to occur. Any such changes are also relevant to a local government’s assessment of its nancial risks from climate-related shocks (acute disaster events) and stressors (chronic e ects of climate change).

Future change and uncertainty around protection gaps:

i. Senior government policy related to disaster nancial assistance programs and the eligibility, adequacy, and timeliness of nancial assistance for local governments and the private sector;

ii. Market measures such as, the availability and a ordability of mortgages, loans, and insurance with comprehensive coverage (whether from private or public sector suppliers);

iii. BC’s legal system and tort law pertaining to local governments in BC, and any established precedence from successful claims of negligence or nuisance.

ALLISON ASHCROFT Director of Sustainability at Municipal Finance Authority of BC.

PREPARING FOR NEXT YEAR’S AUDIT (TODAY!)

WHEN THIS ARTICLE IS PUBLISHED, MANY YEAR-END CLOSE PROCESSES HAVE BEEN COMPLETED, AND THE YEAR-END AUDIT MAY BE UNDERWAY OR WILL START SHORTLY. IT IS “GAME TIME” AND COMPLETING THE AUDIT ON TIME IS YOUR TOP PRIORITY. THE FURTHEST THING ON YOUR MIND MUST BE NEXT YEAR’S AUDIT!

However, the current year audit provides useful insight and learnings on how to better prepare for a successful audit. Below are ideas to consider during the coming weeks to inform a better process next year.

“PAIN POINTS” LIST (AND “WHAT WENT WELL”)

Start a live collaboration document where your team members can note both “pain points” and “what went well” as the audit is undertaken. Be speci c as opposed to thematic with the items. Having concrete details helps to better direct the conversation with your auditors on a speci c point. The little things add up, and oftentimes only the bigger issues are remembered post-mortem. Having a contemporaneous list helps to ensure all items are captured.

SHIFTING AWAY FROM ONCE A YEAR

What reporting processes are only done at year-end? Identify what activities can be shifted from year-end to month-end. Generally, processes only performed once a year have an increased risk of error and take longer compared to processes performed monthly. Team members become more familiar with the process, as it is done multiple times throughout the year. This increases e ciency and reduces mistakes over time. In addition, issues can be identi ed during the year for resolution as opposed to accumulating and waiting until year-end.

FINANCIAL REPORTING AWARD CHECKLISTS

There are several GFOA of the US and Canada award programs that have been established to encourage local governments to improve the quality of their nancial management and nancial reporting. Award programs typically provide a checklist of what is reviewed. These checklists can be reviewed during your downtime against your most recent nancial statements to identify improvement points for next year. In addition to being

recognized for your achievement, having nancial statements prepared with all necessary disclosures will reduce the number of comments from auditors.

SCHEDULE AN AUDIT DEBRIEF

The last thing you want is another meeting with your auditors after the audit report is issued and nancial statements are led for another year. Take the time to celebrate another successful year, but you would be remiss to not talk to your auditors until the fall. Ideally, a “debrief” or “post-mortem” should happen as soon as possible after the completion of the audit. The most valuable insights come when the experience is fresh and recent. Waiting too long risks not only reducing the e ectiveness of the discussion, but certain planning points need time to implement, and it could be too late if these are surfaced later in the year.

LOOKING AHEAD

Several new accounting standards became e ective in the past few years, from asset retirement obligations to revenues and more. While there are no new standards e ective for calendar 2026, there will be signi cant changes to nancial reporting for calendar 2027 with the adoption of the Conceptual Framework and PS 1202 Financial statement presentation. 2026 is a great opportunity to set out a project charter and timeline for these signi cant new standards.

Get Ready for PS 1202 Financial Statement Presentation

Effective April 1, 2026, the standard introduces new statements, revised presentation, and other reporting considerations.

Learn more about PS 1202.

Connect with your local KPMG audit team today.

Contact us

Asifa Hirji Partner

asifahirji@kpmg.ca 604 777 3921

Brandon Ma Partner

bjma@kpmg.ca 604 691 3562

BRANDON MA is an audit partner in KPMG’s BC Public Sector practice with over 20 years of experience providing nancial statement audit and advisory for many local governments in the Lower Mainland, and other public sector and not-forpro t organizations. He currently is a champion in KPMG for BC Audit Quality for non-public companies, having previously been in rm leadership roles for People, Lean Services, and Technology.

FROM PLANNING TO CONSTRUCTION:

WHY INSURANCE NEEDS A HEAD START

LOCAL GOVERNMENTS CONTINUE TO EMBARK ON ESSENTIAL CAPITAL PROJECTS, INCLUDING NEW CONSTRUCTION AND LARGE-SCALE UPGRADES TO FACILITIES, UTILITIES AND INFRASTRUCTURE. THESE PROJECTS NOW TAKE PLACE IN AN ENVIRONMENT WHERE INSURANCE IS HARDER TO SECURE AND CAN TAKE LONGER TO FINALIZE.

Insurance for construction projects remains available in Canada; however, when projects are in wild re-prone or other catastrophe-exposed areas, span multiple budget cycles, or have long planning periods, underwriters apply greater scrutiny and insure these projects more selectively.

This makes insurance a critical part of the project planning timeline, as underwriting delays can impact start dates, a ect budgets, and stall projects that are otherwise ready to proceed.

UNDERSTANDING THE COVERAGE

Most construction projects require two key types of insurance:

1. Builder’s Risk, which provides coverage for physical damage to the project as it’s being built.

2. Liability Coverage, which provides protection to parties involved in the project for liability arising from their work.

These coverages can be arranged in two ways.

• Contractor-Controlled: The general contractor buys the Builder’s Risk, and each contractor/subcontractor brings their own liability insurance, which can lead to variations in limits and coverage.

• Owner-Controlled (OCIP): The owner purchases Builder’s Risk and Wrap-Up Liability policies, creating one centralized and consistent insurance program for the project.

OCIPs are often preferred because they give owners greater control over coverage quality, help align limits with the project’s scale, simplify administration and reduce uncertainty.

EVOLVING UNDERWRITING REQUIREMENTS

Regardless of who purchases the insurance, more complex projects require underwriters to gather additional information on location, timelines, emergency response plans and environmental exposures. Changes in scope, valuations, site conditions or risk pro les can also a ect underwriting just as coverage is about to be placed.

IMPACT OF WILDFIRE SEASON

Wild re risk is now a major factor in underwriting decisions. Even when underwriters are willing to quote, many will not allow coverage to begin within 50km of an active wild re, even if it is considered under control. This can lead to last-minute information requests, reduced exibility as start dates approach and project delays if coverage cannot be secured when needed.

WHEN INSURANCE DELAYS BECOME CONSTRUCTION DELAYS

Construction should not begin without appropriate coverage. If the insurance process starts too late, delays can quickly cascade—pushing start dates, disrupting services, extending facility closures, and increasing sta

pressure. Costs may also rise if coverage needs to be re-quoted, restructured or extended due to changing conditions.

MANAGING THE RISK

These actions can help local governments reduce the risk of insurance-related project delays:

• Identify insurance requirements early: Ensure capital planning, procurement and risk management teams know which projects need coverage, who will place it, and any potential challenges.

• Keep insurance on your radar: For projects with long planning periods, revisit insurance as they move between planning and execution.

• Secure coverage early: Engage your insurance provider early for OCIPs or check in regularly with the contractor on coverage status.

Embedding insurance into the project’s critical path reduces uncertainty, keeps construction on schedule, and maintains service continuity when external factors delay coverage placement.

JOSH BROCKLEBANK has nearly a decade of experience working on complex insurance programs, including large property portfolios and construction projects. At the MIABC, he works closely with local governments to support their insurance needs through coverage placement, practical risk management advice and specialized expertise in construction and cyber coverage. He also helps develop insurance programs that re ect the evolving needs of B.C. communities.

A CYBER MATURITY PLAYBOOK FOR FINANCIAL LEADERS

WHY CYBERSECURITY SHOULD BE TREATED LIKE CORE INFRASTRUCTURE

WITH THE CANADIAN CENTRE FOR CYBER SECURITY NOTING INCREASING ATTACKS AGAINST MUNICIPAL GOVERNMENTS, LOCAL FINANCIAL LEADERS MUST INVEST IN CYBERSECURITY THE SAME WAY THEY PLAN AND BUDGET FOR ESSENTIAL INFRASTRUCTURE.

Why do cybercriminals routinely target local government? Because of the critical services they deliver and the pressure to restore operations quickly.

Municipalities are at risk because they rely on operational technology, store large volumes of personal data, use third-party platforms and process signi cant payments, often while operating with dated technology and small teams.

Several Canadian incidents over recent years — from ransomware disrupting local services to large-scale data theft and denied cyber insurance claims due to lacking cyber controls — illustrate the operational and nancial stakes for municipalities.

The results of ransomware, phishing, vendor breaches and business email compromise are a higher likelihood of ransom payment, reputational fallout and signi cant recovery costs that extend far beyond the breach itself.

For CAOs and nancial leaders, the message is clear: Insurance supports recovery, but cyber maturity reduces both the likelihood and severity of an incident.

WHAT CYBER INSURERS EXPECT

Cyber insurance markets increasingly require evidence of proven controls. The following are no longer ‘nice to have;’ they are prerequisites to obtain and maintain cyber insurance, and they can materially in uence premium stability and market appetite:

• Multi-factor authentication

• Endpoint detection and response solutions

• Secure and o ine backups

• Network segmentation

• Privileged access management

• Continuous sta training

• Tested incident response plan

While the cyber controls required by each insurer can vary and should be discussed with an insurance broker, the above requirements demonstrate that carriers expect local governments to take proven precautions to minimize the likelihood and reduce the severity of cyberattacks.

BUDGETING FOR CYBER INFRASTRUCTURE

Budgeting for critical cyber infrastructure should move beyond a percentage of IT spend and involve an analysis of the true risk.

Costs to factor in include, but may not be limited to:

• People, like specialists and training programs for all employees.

• Processes and policies, like password policies and vendor oversight.

• Tools, like multi-factor authentication, endpoint detection and response solutions, and privileged access management.

• Recovery, like o ine backups and network segmentation.

• Cyber insurance, which can help cover costs associated with operational downtime, data recovery or restoration, noti cation and regulatory requirements, future-proo ng against other attacks and more.

It’s important to note that cyber insurance and cybersecurity are interdependent.

Cyber controls minimize the likelihood of a breach while helping to maintain market appetite and premium stability. Whereas cyber insurance helps to cover expert response and recovery if attackers slip through safeguards.

CYBER MATURITY SUPPORTS CONTINUITY

Municipalities that plan their cyber investment the same way they budget for roads, water systems or eet maintenance are better positioned to safeguard continuity of operations.

Treating cyber preparedness as core infrastructure, and not as discretionary spending, helps to protect insurability, public trust and service resilience.

Cyber risk isn’t just technical. It’s strategic and leadership driven

DANIEL TASSONI

2026 OUTLOOK: RESILIENCE AND RISKS

The best that can be said about Canada’s economy in 2025 is that it likely skirted a recession, thanks to the duty-free status of USMCA-compliant goods, supportive scal and monetary policies, and the TSX’s blistering 28% rally. Still, real GDP growth likely slowed to 1.7% from 2.0% in 2024. Moreover, the annual average gure likely understates the true deceleration in activity, with GDP likely rising just 0.8% on a Q4/Q4 basis after surging 3.1% in 2024. We expect stronger 1.9% growth in 2026 (Q4/Q4, or 1.4% annual), assuming no nasty surprises on the trade front.

Our critical assumption for 2026 is that the USMCA review will extend beyond this year, keeping the U.S. in the Agreement and preserving the compliance exemption on most Canadian goods. Potential issues for discussion include supply management and the Online Streaming and News Acts. The review could lead to a reduction of some sectoral duties, notably the 50% import

tax on steel, aluminum, and some copper products, trimming the U.S. average tari on Canadian imports from its current level of around 7%. Apart from a few hard-hit industries, the economy will largely adjust to the lower level of exports. Ongoing uncertainty, however, could cast a longer shadow on business con dence and investment. The impact of a USMCA breakdown would be far worse, potentially spiking the average tari rate and triggering a moderate recession in Canada, even with signi cant policy support. Manufacturing industries that depend heavily on U.S. sales, including automobiles, electrical equipment, machinery, computers, and chemicals, would face dire consequences.

Stimulative scal policies at both the federal and provincial level should continue to cushion tari e ects in 2026. Combined deficits are projected at near 4% of GDP this scal year, or more than 2 percentage points

above FY2024/25. Federal initiatives aim to jump-start

investment by accelerating infrastructure, mining and energy projects, while reinstating full and immediate capital expense deductions and supporting tari -impacted industries.

The economy will also bene t from last year’s 100 bps of rate cuts from the Bank of Canada. However, with rates now at the low end of neutral and inΌation still moderately above target, the easing cycle is probably over. Nevertheless, we don’t see the Bank reversing gears this year. Although employment, as measured in the household survey, has rebounded strongly after contracting last summer, ongoing weakness depicted in the establishment survey likely better reΌects reality. It may be no coincidence that both industry payrolls and real GDP have grown a mere 0.4% in the past year to October.

Home price risks remain contained to Ontario and British Columbia, where a ordability (though improving) remains poor. The Toronto area faces extra price risks from a glut of unsold condos and a surge in purposebuilt rental construction, made worse by meaningful immigration curbs. However, as long as mortgage rates remain near neutral levels and the jobless rate holds relatively still—we see the current 6.5% rate peaking at 6.8% before declining—home prices in the two provinces should stabilize this year. Elsewhere, prices could climb modestly, with regions currently seeing outsized gains, such as Quebec City, St. John’s, and Moncton, reverting to more normal increases.

After rising moderately against a weak greenback in 2025, the Canadian dollar is expected to appreciate further to C$1.333 (US$0.752) by year-end as Fed rate cuts compress bond spreads in the two countries. Just don’t expect it to travel a straight line until the USMCA drama is settled. Another currency risk is that U.S. in uence in Venezuela could lead to more oil exports to the U.S., displacing some Canadian sales over time while lowering crude prices.

Strategic guidance to help your organization.

FROM AWARENESS TO ACTION: WHAT AI READINESS REALLY REQUIRES IN LOCAL GOVERNMENT INFRASTRUCTURE

Across local governments, awareness of arti cial intelligence (AI) has grown quickly. The conversation has moved beyond “What is AI?” to a more practical question: What needs to be in place to use it responsibly? That question gets to the heart of AI readiness.

In conversations with local governments across British Columbia, a common pattern is emerging. AI tools are already being used across organizations, sometimes without formal policies or oversight, a phenomenon often referred to as Shadow AI. The readiness gap is not about stopping innovation, but about bringing it into the light.

READINESS IS NOT A TECHNOLOGY PROBLEM

AI readiness is often mistaken for a software decision. In reality, it is an organizational one. Before deploying new tools, local governments need a clear understanding of how data is managed, who has access to it, and how decisions are governed.

For nance leaders, this matters deeply. AI systems rely on data, and if that data is incomplete, inconsistently labelled, or overly accessible, automation can amplify risk rather than reduce it. Readiness means ensuring the foundation is solid before asking AI to build on top of it.

WHAT AI READINESS ACTUALLY REQUIRES

Based on our advisory conversations with municipal teams and industry AI readiness guidance, preparedness consistently centers on four practical areas:

1. Data clarity

Beyond knowing your ERP, readiness means understanding where nancial and operational data also lives — across email, shared drives, reporting tools, and work ow systems. This matters because AI draws from all these sources. Without clear ownership and intentional permissions, AI can surface incomplete or inappropriate information, increasing risk instead of insight.

2. Security and access controls

AI should only surface information that sta are already authorized to see. For nance leaders, this is critical. Automation can unintentionally expose sensitive nancial or personnel data if roles and permissions have not been reviewed. Strong access controls ensure AI reinforces existing safeguards rather than weakening them.

3. Governance and policy

Clear guidance on acceptable AI use does more than build sta con dence. It ensures AI is used consistently and responsibly, and that its use can be explained to council, auditors, or the public if questions arise. Governance turns experimentation into accountable practice.

4. Change readiness

AI adoption a ects work ows, not just systems. Finance teams need time, training, and support to adapt, especially in environments where sta already wear multiple hats. Without this readiness, even welldesigned tools may go unused or introduce friction instead of e ciency.

START SMALL AND BUILD CONFIDENCE

AI readiness does not require large-scale transformation. In fact, the most successful organizations start small. For nance teams, small does not mean trivial. Low-risk use cases include generating rst-draft variance explanations for budget reports, agging unusual vendor payment patterns for review, or summarizing large volumes of nancial data for council brie ngs. These tasks still require professional judgment, but AI can reduce manual e ort and free sta to focus on analysis.

WHY THIS MATTERS NOW

AI is no longer a future consideration. Capabilities such as work ow automation, analytics, and Microsoft 365 Copilot are increasingly embedded in the systems local governments already use. The opportunity is not adoption, but preparation.

ALPHA IT helps municipalities and local governments modernize outdated systems, unlock automation with Microsoft 365, and reduce IT costs, all while providing proactive support and enterprise-grade security.

HOW WE HELP

KIM ARSENAULT is the Director of Marketing at ALPHA IT. She works with local governments and small businesses to strengthen cybersecurity, modernize systems, and prepare for responsible AI adoption, with a focus on clarity, governance, and practical outcomes.

HOW MUNICIPAL FINANCE TEAMS CAN IMPROVE FINANCIAL VISIBILITY WITH LIMITED STAFF

IF YOU WORK IN MUNICIPAL FINANCE, YOU KNOW THE WORKLOAD DOESN’T SHRINK JUST BECAUSE THE TEAM IS SMALL. MONTH-END CLOSE, BUDGET PREP, AND AUDIT REQUESTS OFTEN PILE UP AT ONCE, WHILE DEPARTMENT HEADS AND COUNCIL NEED UP-TO-DATE, ACCURATE REPORTS—ALWAYS ON A DEADLINE. EVEN FOR SMALLER MUNICIPALITIES, FINANCIAL COMPLEXITY KEEPS INCREASING, ALONG WITH PUBLIC EXPECTATIONS FOR TRANSPARENCY.

You’re often tracking multiple funds, grants, capital projects, and interdepartmental allocations. Every new reporting requirement or cost centre adds another layer to the job. Citizens, leadership, and council all depend on you for timely, accurate nancial information.

SAME EXPECTATIONS, LEANER TEAMS

Whether you serve 2,000 or 2,000,000 people, the core reporting requirements are similar: prepare statements, track budgets, audit preparation, grant and fund reporting, in addition to providing clear insights for decision-makers.

For smaller teams—sometimes just one or two people— this means doing it all, from data entry to presentations. Delivering accurate, accessible nancial visibility isn’t optional; it’s essential for public trust and e ective decision-making.

THE COST OF LIMITED FINANCIAL VISIBILITY

Many teams still rely on manual data exports, disconnected spreadsheets, and time-consuming reconciliations. Common results include:

• Hours lost to gathering and consolidating data

• Greater risk of errors that undermine report accuracy and trust

• Delays in providing up-to-date nancial reports for informed decision-making.

• Frequent interruptions from departments needing numbers fast

• Dependence on a “spreadsheet expert”

• Sta burnout as manual work becomes overwhelming

As one director of nance stated, “We spend more time formatting and reconciling than analyzing.” Manual reporting limits nancial visibility to leadership, causing reactive rather than proactive decision making.

BOOST FINANCIAL VISIBILITY — WITHOUT ADDING STAFF

The good news is that improving nancial visibility isn’t about adding people. It’s about making reporting simpler and more centralized by leveraging tools that t how nance teams work.

1. Automate Data Flow: Link nancial reports directly to your nancial system data. Automation eliminates manual exports or data entry and reduces errors, so reports are up-to-date and accurate.

2. Automate Reporting: Ensure data integrity by centralizing data, enforcing standardized formats, and automating data input. This allows you to spend less

time worrying about inconsistencies and more time leveraging accurate data to deliver strategic value.

3. Empower Department Heads: Give managers selfservice access to reports providing detailed, actionable insights through advanced analytics and drill-down capabilities to empower proactive decision-making based on comprehensive nancial data.

4. Centralize Configuration: Adjust reporting logic or account de nitions once and see the change everywhere. This is especially helpful in complying with new PSAS reporting requirements.

5. Keep Reporting Finance-Owned: Letting nance manage reports without relying on IT or 3rd party providers keeps your team agile and responsive to meet new regulatory or internal reporting demands.

THE BOTTOM LINE

When you shift from manual to automated reporting, your council gets faster updates, managers gain clear insight to their budgets, audit is less stressful, and your team spends more time on analysis—not chasing numbers. One nance leader shared: “Now, with automation, our close is faster, cleaner, and we’re not working late to x broken links.”

Improved visibility doesn’t require more sta —just better tools. Simplifying nancial reporting can help your municipality deliver the transparency and stewardship your community deserves.

Curious how Vivid Reports can help your team automate, consolidate, and simplify municipal nancial reporting without leaving Excel? Let’s connect and explore the possibilities.

LAURINDA BROWN, Client Solutions Manager at Vivid Reports, brings 15+ years of experience helping municipal and public sector nance teams boost efÏciency through automation and smart technology. Her expertise spans ERP systems, nancial reporting, document management, and automation of AP/AR — streamlining operations and enhancing visibility across public sector organizations.

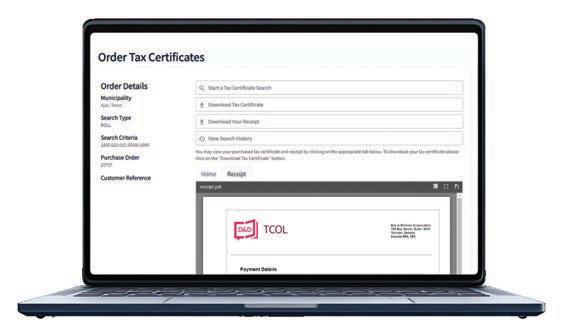

IMPROVING MUNICIPAL TAX CERTIFICATE PROCESSING THROUGH SYSTEM INTEGRATION

MUNICIPAL FINANCE TEAMS ARE UNDER PRESSURE TO DELIVER TIMELY, ACCURATE SERVICES WHILE MANAGING FLUCTUATING TRANSACTION VOLUMES AND LIMITED STAFF CAPACITY. TAX AND UTILITY CERTIFICATE

PROCESSING IS A CLEAR EXAMPLE. IT IS HIGH VOLUME, TIME SENSITIVE, AND ESSENTIAL TO REAL ESTATE TRANSACTIONS ACROSS BRITISH COLUMBIA.

For many local governments, the challenge is not issuing certi cates. It is issuing them e ciently, consistently, and with strong audit integrity.

THE COST OF FRAGMENTED WORKFLOWS

In some municipalities, requests still arrive through a mix of email, mail, phone calls, and fax. Even where online portals exist, sta may need to verify property details, con rm balances, generate documents, and return certi cates across separate systems.

Each manual step increases the risk of delay or error. During peak real estate periods, small ine ciencies scale quickly.

Digital access alone is not enough; e ciency comes from integration.

WHY INTEGRATION MATTERS

When municipal systems connect directly with the platforms used by legal professionals, standardized requests ow into nance work ows with complete, structured data. Rather than treating each certi cate as an isolated task, integration reduces duplication and minimizes administrative back and forth.

Additionally, having tax and utility certi cates easily accessible and integrated makes it less attractive for legal professionals to order full-coverage insurance policies that cover municipal arrears.

Integrated electronic ordering platforms, such as Dye & Durham’s Tax Certi cates Online (TCOL), address both the standardization and integration gap. Serving communities from large urban centres to small rural towns, TCOL accounts for over 90% of all B.C. tax and utility certi cates delivered on behalf of all B.C. municipalities. The operating model carries no sign-up or maintenance costs, allowing adoption without new budget allocations and helping teams move away from fragmented intake channels.

TCOL also integrates directly with Unity®, Canada’s most widely used conveyancing platform, which processes more than 350,000 real estate transactions annually. Because many legal professionals already work within Unity®, tax and utility certi cate requests can be submitted as part of their existing work ow, with matter data owing directly

into the request. For municipalities, this means more complete, standardized submissions at intake and fewer manual touchpoints.

A PRACTICAL STEP TOWARD MODERNIZATION

As property transfers and development activity continue across the province, nance teams are asked to do more without proportional sta ng increases. Technology cannot replace professional oversight, but it can remove unnecessary handling.

For municipalities advancing digital transformation initiatives, tax and utility certi cate processing is a practical and measurable starting point. It is visible, high impact, and essential to the success of real estate transactions. Adopting an integrated digital solution for tax and utility certi cate processing allows municipalities to improve service delivery and reduce administrative strain while maintaining scal discipline.

INTEGRATING TAX & UTILITY CERTIFICATES INTO CONVEYANCING WORKFLOWS

Learn more about how TCOL supports municipalities across British Columbia at dyedurham.ca/solution/tcol.

Tax Certificates Online (TCOL) streamlines property tax and utility certification requests by delivering complete, consistent submissions electronically, reducing processing time without requiring any implementation costs.

OVER Trusted to process 90% of all British Columbia Tax Certificates.

WICK is a customer success and strategy leader specializing in municipal technology. With an MBA in Finance, she works closely with local governments across Canada to drive digital transformation, strengthen client partnerships, and deliver innovative solutions that improve efÏciency, transparency, and service delivery.

See how it works:

MISHARA

HOW ARE BC LOCAL GOVERNMENTS PLANNING AND DELIVERING CAPITAL?

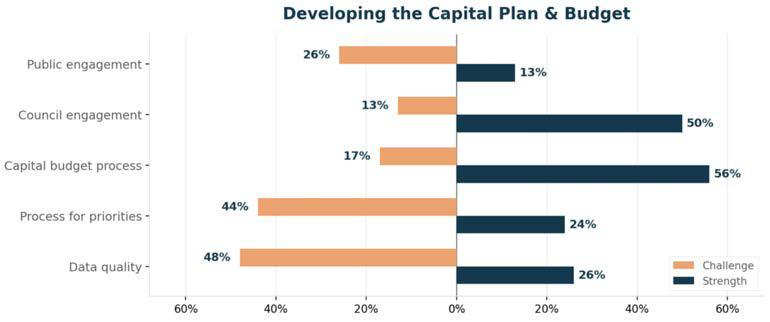

SURVEY RESULTS FROM 54 LOCAL GOVERNMENTS REVEAL COMMON STRENGTHS IN CAPITAL BUDGETING — AND A STAFFING CRUNCH THAT’S LIMITING WHAT THOSE PROCESSES CAN DELIVER.

We asked members about their experience developing and delivering capital plans and budgets. Fifty-four local governments responded, representing a diverse crosssection of community types. The results paint a clear and consistent picture: most local governments have sound budgeting processes in place, but systemic resource constraints limit what those processes can actually deliver.

STRONG PROCESSES, WEAK INPUTS

More than half of respondents (56%) say they have a clear process for developing their capital budget, and 50% report e ective council engagement. These are genuine strengths. But nearly the same proportion (48%) say they lack the data quality needed to inform good decisions, and 44% have no clear method for establishing priorities. The machinery is there — what’s missing are the raw materials: reliable asset data, structured prioritization frameworks, and the sta time to pull it all together.

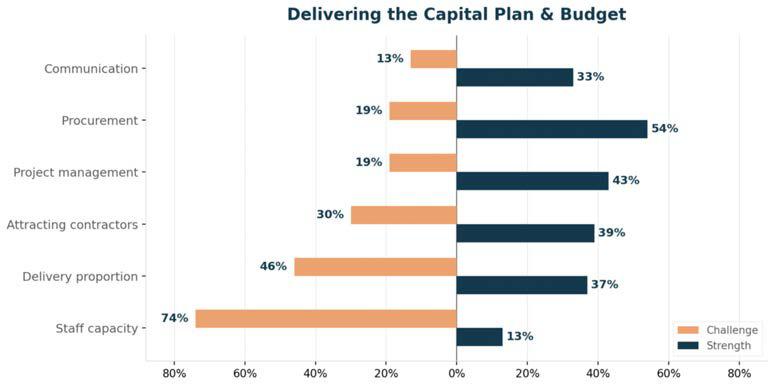

THE STAFFING CHALLENGE DOMINATES DELIVERY

When we shift from planning to delivery, one nding stands out: 74% of respondents cite insu cient internal sta capacity as a barrier. This isn’t con ned to any one type of local government; cities, districts, and regional districts all agged it. Meanwhile, the areas where members report strength — procurement (54%), project management (43%), and attracting contractors (39%) — suggest that once projects are resourced and moving, local governments generally execute well. The bottleneck is getting projects from plan to active status, even though everyone is already stretched thin.

“56% HAVE A CLEAR CAPITAL BUDGET PROCESS — BUT 48% LACK THE DATA QUALITY TO INFORM IT.”

“74% IDENTIFY INSUFFICIENT STAFF CAPACITY AS A DELIVERY BARRIER.”

Continued on page 42...

Figure 1: Self-reported strengths vs. challenges in developing the capital plan (% of respondents)

Figure 2: Self-reported strengths vs. challenges in delivering the capital plan (% of respondents)

...continued from page 41

WHAT’S GETTING DELIVERED — AND

HOW IT’S

FUNDED

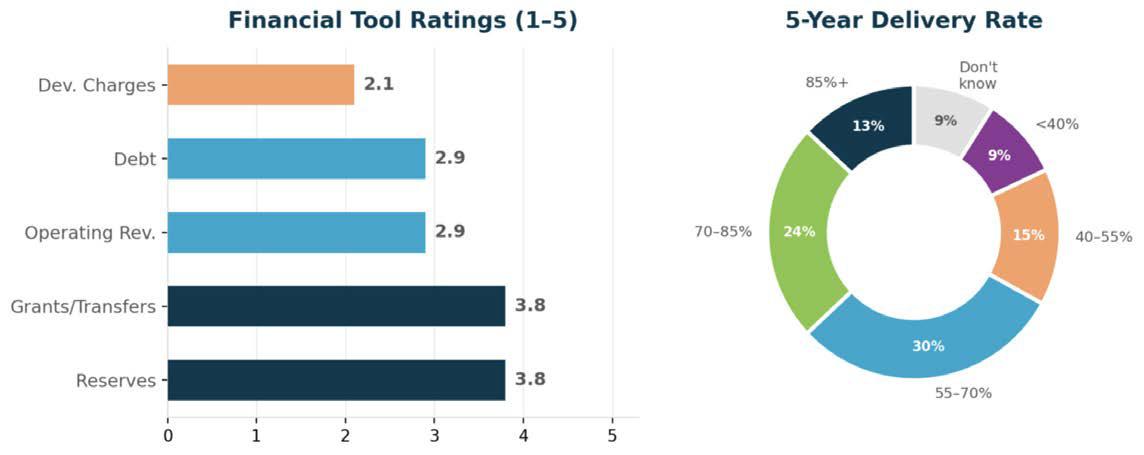

Just over one in three respondents (37%) reported delivering 70% or more of their annual capital budget over the past ve years. Nearly 30% fall within the 55–70% range, while 24% fall below 55%, and another 9% are unsure. On the funding side, nancial reserves and grants or transfers are rated as most useful, both averaging 3.8 out of 5. Development charges score lowest at 2.1. Several respondents shared approaches worth a closer look: internal borrowing between reserves, multi-year fee bylaws linked directly to asset renewal plans, and partnerships with First Nations — strategies that re ect the range of tools BC communities are actually using. The open-ended responses reinforce a consistent theme: local governments know what needs to be

THE NEXT QUARTERLY QUESTION WILL BE ON Housing Growth

Quarterly Question is a joint initiative of GFOABC and CivicInfo BC.

“RESERVES AND GRANTS BOTH RATE 3.8 OUT OF 5 AS FUNDING TOOLS. DEVELOPMENT CHARGES SCORE JUST 2.1 — POTENTIALLY REFLECTING THE REALITY OF SMALLER LOCAL GOVERNMENTS.”

done but face a fundamental tension between aging infrastructure and limited revenue tools. Several respondents noted that without senior government grants, they cannot maintain capital infrastructure, given their tax base. Others pointed to in ation eroding project budgets between planning and procurement. These are shared challenges, and exactly the kind of practical problems where member-to-member knowledge sharing can make a real di erence. If your organization has found approaches that work, we’d encourage you to share them on the GFOABC forum.

Please use this link to be a contributor. This short survey should take less than 5 minutes to complete.

If you would like to contribute topics for upcoming questions, please contact o ce@gfoabc.ca or call (250) 382-6871.

Figure 3: Financial tool ratings (left) and ve-year average capital delivery rate (right)

CALL FOR JUNE NEWSLETTER ARTICLE IDEAS

SHARING PRACTICAL SOLUTIONS AND INSIGHTS ACROSS BC’S LOCAL GOVERNMENT FINANCE COMMUNITY.

Dollars & Sense Perspectives showcases innovations, practical solutions, and emerging ideas shaping local government nance. We invite GFOABC members, sponsors, and partners to share experiences that support stronger, more resilient communities.

Articles often grow into conference sessions, webinars, and workshops— expanding conversations across the sector.

ARTICLE FOCUS: Submissions should provide thought leadership addressing challenges or opportunities such as:

• Governance or regulatory change

• Financial sustainability & a ordability

• Capital & long-term nancial planning

• Service delivery innovation

• Infrastructure & asset management

• Practical solutions & lessons learned

SUBMISSION REQUIREMENTS

• Article (~500 words, Word format)

• Image or photo (optional)

• Author photo & short bio (50 words max)

• Organization logo

OPTIONAL ADVERTISEMENT:

Organizations may include an advertisement:

• Full bleed: 4.3” × 11.25”

• Visible area: 4.17” × 11”

• Resolution: 300 dpi preferred

• Format: JPEG or PDF

JUNE NEWSLETTER

• Topic Due: April 6

• Article Due: April 27

• Publish Date: June 15

!Questions or ready to submit? Contact us here.

THANK YOU EXHIBITORS

Would you like to see your logo here? Become a GFOABC sponsor today.