As this year swiftly comes to a close, we reflect on the past and begin to think about what’s ahead. If retirement is on the horizon, you’re in the right place! This issue of Fragasso’s The Advisor magazine is packed with retirement strategies for both individuals and business owners.

From the time we begin our career, retirement is in the back of our mind as the ultimate goal. With Americans living longer than ever before, retirement can often last two decades. 1 Workers need to start saving as soon as possible and save more to prepare for the long term. And once retirement approaches, the mindset switches to wealth preservation, retirement income, and tax and legacy planning.

It can be overwhelming to manage, and that is why we’re here at Fragasso. We are committed to educating and guiding our clients to the realization of their goals. This Retirement Guide was compiled to help you navigate your unique retirement experience.

Featured articles consist of these and more:

• How can you tell if you are ready for retirement?

• Understanding the new IRA rules for beneficiaries

• Capitalize on everchanging tax laws: Roth IRA conversions and planning opportunities

• Preparing portfolios for retirement

• The importance of exit planning for business owners

We have also launched a new Can You Afford to Retire? online quiz. Learn more about how the quiz can help in tracking your retirement planning journey on page 15.

Thank you for reading the fall/winter 2024 issue of The Advisor . We publish this magazine three times a year – spring, summer and fall/winter. The interactive digital version of this publication is available for complimentary download at www.fragassoadvisors.com , under Resources, Magazine. You are welcome to share this publication with anyone who may benefit from this educational resource.

MARSHA POSSET Director of Marketing Editor in Chief

Robert Fragasso, CFP Board Emeritus

LEADERSHIP PITTSBURGH INC.

Marsha Posset

DR. KENTON AND LAUREN REXFORD

Brandon Schwan, CFP ®, CPWA®

PLEASE NOTE that you should be receiving account statements directly from the custodian of your accounts on at least a quarterly basis, and perhaps monthly. We encourage you to review these statements. If you are not receiving your statements, please contact your FFA advisor immediately to remedy the situation.

ROBERT FRAGASSO, CFP BOARD EMERITUS® Founder and Chairman, Chief Executive Officer Publisher

MARSHA POSSET Director of Marketing Editor in Chief

NADINE KUNDROD

Senior Graphic Designer Art Director

JENNAE BACKO

Digital Content Manager Associate Editor

WHAT DOES RE . TIRE . MENT MEAN TO YOU?

Re.tire.ment.

We all read that word and have unique imagery of what that means.

Consider the range of people that you know who are retired. Retirement is a significant life transition, and how individuals adjust can vary widely. Some find joy and fulfillment in pursuing hobbies, spending time with family, or traveling, while others may struggle with feelings of loss, boredom, or lack of purpose. Compounding the emotional issue can be just as important as financial considerations. So, in stating our retirement vision as a concrete goal, we can begin to plan for its achievement.

A successful retirement is different for each of us, but the process can, and should be, uniform and lead to good results. Begin with the lifestyle and emotional components of retirement planning and then factor in the financial.

Describe your ideal retirement. This includes family considerations, lifestyle choices and time usage. Generalized statements like “play lots of golf” are not helpful and lead nowhere. So, spend all the time necessary to map out your retirement life. Include family in your deliberations.

Once you have a clear vison of where you want to go, you can begin the planning process. Read the next article for a description of that step-by-step mapping toward your retirement success.

RE . TIRE . MENT RE . TIRE MENT

How Can You Tell If You Are Ready for Retirement?

Retirement readiness is both a lifestyle and a financial decision. First determine if you are ready to retire. Do you love what you do? Are you working in an environment that values your contribution? Readiness is not determined by age but by a desire to live differently. Is it time to do the things that greater time freedom would allow? Does your spouse or partner agree? Skipping this lifestyle evaluation can lead to unhappiness.

Once lifestyle readiness is determined, finances can be evaluated based on that vision of life and its attendant costs. Rules of thumb to determine readiness are simple and eye-catching but ineffective. The correct course is both logical and step-oriented, meaning you can follow through to actionable conclusions.

1. Put a cost to your desired lifestyle. This includes the monthly cost as well as the periodic, such as annual insurance premiums and travel. Then add 10 – 20% for the unexpected or spontaneous opportunities.

2. Factor in inflation. Do not be lulled by today’s rate as the recurring average is 3-4% over many decades, so use 3 ½ percent. You will be retired for 20 years or more. Consider that 4% inflation, compounded, means you will need about 50% more income in each decade of life just to maintain purchasing power.

3. Take an inventory of your liquid and non-liquid assets , adjusting for changes such as buying a different home. Account for paying down debt over time. Gauge the productivity of your investment assets and see what income they will provide along with other income streams such as Social Security and pensions.

4. Run all the data through retirement security planning software. The answers will present themselves along with the adjustments you must make for retirement financial security. This comes down to a simple equation: money invested at a certain earnings rate over time should equal money withdrawn over time plus the desired estate you wish to leave. If the equation doesn’t come out even, you need to adjust the factors like saving more, retiring later, or spending less in retirement. But once you have the data, you are equipped to make those decisions and adjustments.

5. Seek professional assistance. This cannot be a do-it-yourself project as most people do not possess the expertise, time, and resources to do it alone.

Now you can move confidently forward into the next phase of your life called retirement. Planning can help make it happy and fulfilling. At Fragasso, we have this type of conversation with clients frequently. Each situation is different, and we are here to guide you toward the best outcome for you and your family’s unique circumstances. Don’t hesitate to reach out to us. f

ROBERT FRAGASSO CFP BOARD EMERITUS® Chairman and Chief Executive Officer rfragasso @ fragassoadvisors.com

BRIANNE KING CFP® Manager of Financial Planning bking @ fragassoadvisors.com

Your risk profile is not something that should change annually but rather be reviewed as you near or achieve milestones in your life.

As we know from history and our own experience, when equities enter a period of extended volatility or loss, it can be detrimental to our financial and mental well-being. Your composition of stocks and bonds makes up what is called your asset allocation. Determining the appropriate asset allocation for our clients is an important step of the financial planning process. We do this by trying to understand what our client’s risk comfort level is, often referred to in the industry as risk profiling

We believe your risk profile is determined by many factors:

, which means how much market loss can you sustain before you want to react. If you find yourself wanting to liquidate investments in a down market, your allocation to equities may be too high for your risk comfort.

simply refers to how you view and make other financial decisions. A few examples of this are comfort level of fluctuating income, views on debt, and desire to maintain purchasing power. By understanding how a client perceives risk in situations outside of the stock market can be a powerful tool in determining one’s allocation.

is the process of determining the amount of risk needed to be taken on for

is an art and not a science. We use the tools to help guide us to an appropriate allocation, and along with frequent communication regarding your desired level of

Your risk profile is not something that should change annually but rather be reviewed as you near or achieve milestones in your life. Retirement can be one of the biggest life transitions you will go through financially. When clients move from the phase of asset accumulation to asset distribution, their ability to handle volatility may not be

It is important to begin the conversation on risk comfort prior to entering retirement. If changes are needed to your overall asset allocation it may have an impact on your cash flow projections. Just as your retirement income and expenses will affect your overall net worth, the projected rate of return that your assets may return each year is also a

Preparedness across all areas of your financial plan is essential to achieving a successful retirement. When your risk profile is in line with your asset allocation, periods of market volatility can be weathered with a much calmer approach. This can help ensure that you stay on the guided path of your financial plan and without making knee-jerk decisions that may compromise

Understanding the NEW IRA RULES for Beneficiaries

WHAT YOU NEED TO KNOW WHAT YOU NEED TO KNOW

On July 18, 2024, the IRS issued new guidance regarding the Secure Act of 2019, specifically regarding the rules for inherited Individual Retirement Accounts (IRAs), clarifying several key points regarding mandatory Required Minimum Distributions (RMDs) for all-designated and non-designated beneficiaries.

Let’s walk through the differences between designated and non-designated beneficiaries and key changes you should be aware of to properly plan for your inherited IRAs.

Individuals named by the IRA owner as inheritors including:

Eligible Designated Beneficiaries surviving spouses, minor children, disabled or chronically ill individuals, and those less than 10 years younger than the decedent

Non-Eligible Designated Beneficiaries

adult children, grandchildren, distant relatives, and friends

KEY DIFFERENCE

For designated beneficiaries, especially Eligible Designated Beneficiaries, they often have more flexibility in taking distributions, potentially stretching them over their lifetime vs. the 10 years for Non-Eligible Designated Beneficiaries.

VS.

NON-DESIGNATED BENEFICIARIES

DEFINITION

Entities like trusts, estates, or charities that are not individuals

KEY DIFFERENCE

These beneficiaries often must distribute the entire IRA within 5 years if the original owner passed away before their required beginning date (RBD) for RMDs. If the owner had started RMDs, distributions might be based on the decedent’s life expectancy or other factors.

Changes Regarding Non-Spouse Beneficiaries

For non-spouse designated beneficiaries such as children, relatives, or friends, several significant changes have occurred, including:

1. The 10-Year Rule

What’s changed?

The IRS now requires most non-spouse beneficiaries to fully distribute the IRA within ten years of the original account holder’s death. The previous option to stretch withdrawals over a lifetime is no longer available.

Annual RMDs

Starting in 2025, if the original IRA holder was already taking RMDs at the time of death, the beneficiary must take annual RMDs throughout the 10-year period. If the original owner hadn’t started RMDs, you’re allowed to wait until the end of the ten years to take the full distribution, though spreading distributions over time may be more tax efficient for the beneficiary.

Example: A parent passed away in 2023 at age 75. The parent has begun RMDs, thus distributions must begin in 2025 and be fully distributed by 2033. Annual withdrawals will increase taxable income, so proactive planning is crucial.

2. Waiver of RMDs Until 2025

Relief Period:

Due to the lack of clarifications by IRS from 2019 until 2024, the IRS has provided a grace period waiving the requirement for annual RMDs in 2021 through 2024. This means beneficiaries have time to adjust to the new rules without facing penalties for prior non-compliance.

3. Penalties for Non-Compliance

Excise Tax:

If you fail to start taking the required RMDs starting in 2025, the IRS can impose a 25% excise tax on the amount that should have been withdrawn. However, this penalty is reduced to 10% if the mistake is corrected within two years.

What should you do next?

1. Review information on your beneficiaries.

Ensure that your IRA beneficiaries’ information is up to date and accurately reflects your plans, particularly given the new distribution requirements and how these may affect your beneficiary.

2. Plan for distributions and their impact.

Tax Impact:

Annual RMDs may push you into a higher tax bracket. Consider spreading withdrawals over the given 10-year period in a tax-efficient manner or if you expect your income to fluctuate, you might plan to take larger distributions in lower-income years to soften the impact. This helps reduce the overall tax impact and keeps more of your money working for you in the long run.

If you qualify as an EDB, such as being a surviving spouse or a minor child, you may be able to stretch out the distributions over your lifetime, providing greater flexibility and lesser tax impact.

3. Consult with your financial advisor along with a tax professional.

Given the complexity of the above-described rules, work with your financial advisor along with a tax professional to create a strategy that aligns with your goals and minimizes tax liabilities.

These new rules represent a significant shift in managing inherited IRAs, especially for non-spouse beneficiaries. Understanding these changes and planning accordingly can help you make informed decisions to protect your financial future and minimize tax burdens. If you have any questions or need further guidance, feel free to reach out to your financial advisor at Fragasso.

We’re here to help you navigate these new regulations. f "Retirement topics - Required Minimum Distributions (RMDs)”, www.IRS.gov Page Last Reviewed or Updated: 20-Aug-2024, Retirement topics - Required Minimum Distributions (RMDs) | Internal Revenue Service (irs.gov) Dayna E. Roane, CPA, CGMA; Beneficiary IRAs: A guide to the RMD maze, March 30, 2023 Beneficiary IRAs: A guide to the RMD maze - Journal of Accountancy

CAPITALIZE on Everchanging Tax Laws CAPITALIZE on Everchanging Tax Laws

ROTH IRA CONVERSIONS AND PLANNING OPPORTUNITIES

We have seen an unprecedented amount of changes in tax law over the past 5 years. With so many changes diligence is required to make favorable planning decisions that consider tax ramifications now and into the future.

The Tax Cuts and Jobs Act (TCJA) of 2017 brought with it lower tax brackets, but these reductions are scheduled to sunset at the end of 2025.

The Secure Act (Setting Every Community Up for Retirement Enhancement Act), enacted in 2019, eliminated the “stretch IRA” provision for most beneficiaries, requiring them to deplete the IRA within 10 years. It also increased the required minimum distribution age from 70 ½ to 72.

• Secure Act 2.0 , passed in 2022, increased the RMD age again based on the year you were born. If you were born between 1951 and 1959 your RMD age is 73. If you were born 1960 or after your RMD age is 75.

As financial planners, we feel Roth IRA conversions are an excellent opportunity to provide tax diversification especially while tax brackets for individuals are lower and as RMD ages increase.

A Roth IRA conversion is the process of transferring funds from a Traditional IRA, which holds all pre-tax dollars, to a Roth IRA, which holds after-tax dollars. This conversion requires you to pay taxes on the converted amount upfront, but future withdrawals from the Roth IRA will be tax-free if you meet certain conditions.

The most significant advantage of a Roth IRA conversion is that future earnings and withdrawals are tax-free, provided you are at least 59.5 years old and have held the Roth IRA for at least five years.

2. No Required Minimum Distributions (RMDs)

Unlike traditional IRAs, Roth IRAs do not have RMDs, allowing your investments to grow tax-free for a longer period

3. Estate Planning Benefits

Roth IRAs can be a powerful estate planning tool as they can be passed on to beneficiaries, allowing them to take tax free withdrawals.

Examples of Roth IRA Conversion Planning Opportunities:

1 2 3

Partial Conversions : If you have a substantial traditional IRA balance, you will not want to convert the entire amount at once due to the tax liability. Instead, converting a portion of your IRA each year allows you to take advantage of lower tax brackets. By spreading the conversion over several years, you can minimize the tax impact.

Example: Rick has a traditional IRA with a balance of $300,000. He is currently in the lower end of the 24% tax bracket. Instead of converting the entire IRA balance in one year, the balance is converted $100,000 a year for three years. This strategy allows him to stay within the 24% tax bracket and avoid pushing his income into a higher bracket.

4

Tax Bracket Management: If you have a year with lower income, it may be an opportune time to perform a Roth conversion. By doing so, you can take advantage of the lower tax brackets while they are still in effect.

Example: Mark is a freelance consultant who had a lower income year due to the loss of a major client. He finds himself in the 12% tax bracket, down from his usual 22% bracket. Mark, with the guidance of his financial advisor and tax professional, decides to convert $50,000 from his traditional IRA to a Roth IRA, taking advantage of the lower tax rate.

Early Retirement Planning: If you are planning to retire early, converting your traditional IRA to a Roth IRA can provide tax-free income during your retirement years.

Example: Suzi is 55 years old and plans to retire at 60. She converts her traditional IRA to a Roth IRA while in the 22% tax bracket. By the time she retires, the five-year holding period for the Roth IRA will have passed, allowing her to withdraw funds tax-free during her retirement. If early retirement is considered, this plan can be helpful to keep income low prior to Medicare age so Suzi can qualify for less expensive, private medical coverage.

Market Downturns: It can be advantageous during a bear market to convert all or a portion of a pre-tax IRA account to a Roth account. By converting when the market is down you can pay taxes on the reduced value and be positioned to participate in any potential future growth in a tax-free account.

Example: Linda has an IRA worth $100,000 when the market drops 20%. She decides to convert and pay taxes on the IRA, now worth $80,000, to a Roth IRA. If the market rebounds the following year, Linda is positioned to realize any growth in the new tax-free account.

5

Required Minimum Distribution (RMD) Management: Roth conversions can be a valuable strategy to manage the size of one’s RMDs. It may be beneficial to convert an IRA to a Roth IRA if you do not think you will need the income from these distributions. Because Roth IRA’s do not require distributions this enables you to manage your overall tax liability in conjunction with other income sources.

Example: Beth and Hank are retired and have assets in both pre-tax IRAs and Roth IRAs. When they retire, they have a six-year window until RMDs begin. By converting $100,000 per year for six years from their pre-tax IRAs to their Roth IRAs, they reduce the eventual amount of their RMD while building a balance in their Roth IRAs.

6

Estate Planning Post-Secure Act: Most beneficiaries are now required to deplete an inherited IRA or Roth IRA by the 10th year following the death of the IRA owner. Even though the Roth IRA will require this depletion, the withdrawals are not taxable to the beneficiary. Therefore, it may make sense to convert some or all your IRA over time over your lifetime. Evaluating what your tax bracket would be upon the conversion versus what you believe your beneficiaries tax brackets will be upon your death is imperative.

Example: Dale and Kathleen are retired and in the 24% tax bracket. Their son, Evan, is the sole beneficiary of Dale’s Roth IRA, which they plan to use as their primary legacy planning tool. Dale decides to convert $100,000 from his IRA to his Roth IRA each year for the next 5 years, paying the tax in their 24% bracket. When Evan inherits the Roth IRA, they believe he will be in the 35% tax bracket. By Dale assuming the tax burden of the converted amount years ago, Evan can now take out the balance, which has grown tax free. If Evan were to inherit a Traditional IRA, any distributions would be taxed in his higher income bracket.

The sunsetting of the current tax plan as well as the extended RMD ages presents a unique opportunity for taxpayers to take advantage of lower brackets by considering Roth IRA conversions. By implementing strategic tax planning with Roth IRA conversions, your advisor at Fragasso, alongside your tax professional, can help you consider a strategy designed to optimize your long-term financial goals and enjoy tax-free income in retirement.

STRATEGIES TO HELP Minimize Your Tax Implications in Retirement

Americans typically begin their careers in their early twenties and continue working until their mid-to-late sixties, or later. Your ideal retirement date is an individualized choice, and it can be a big adjustment when regular paychecks cease regardless of how much has been stashed away in savings. Planning for retirement and managing income sources efficiently are crucial for maintaining financial stability during your later years. Creating a customized, tax-efficient income plan is a big reason you work with an experienced and knowledgeable advisor as it needs to be appropriate for YOU and your circumstances in addition to being fluid as you get deeper into retirement. Here are some basis tips to keep in mind and consider when putting together a retirement income plan.

BE AWARE OF THE TAX RAMIFICATIONS OF YOUR RETIREMENT INCOME

Your retirement income plan should not only cover your expenses but should also be as tax efficient as possible. The goal is to maximize income while minimizing the tax burden.

Utilizing Current Sources of Income

Earnings from part-time work, social security, pension payments, and rental income can all help to offset spending needs in retirement and, in some cases, may be enough to fully fund your retirement lifestyle on a consistent basis. Using these funds for day-to-day expenses can help minimize the need for tapping into your investments thus allowing your nest egg to continue to grow.

Interest and Dividends from Investment Portfolios

Interest and dividends held in an after-tax account are generally taxed – either as ordinary income or at your capital gains rate if the dividends come from stocks. These are taxable whether they are withdrawn or reinvested, so it often makes sense to use these to supplement any of the income sources mentioned above. Using this “income only” approach to your non-qualified accounts still allows them to stay invested and grow in a diversified portfolio.

TAP INTO YOUR NON-QUALIFIED (AFTER-TAX) ACCOUNTS

Once all the aforementioned income sources are exhausted, tapping into your taxable accounts normally makes the most sense. These are accounts for which you pay taxes annually on the dividends and/or interest they generate as well as capital gains from security sales.

Required Minimum Distributions (RMDs)

Once you reach a certain age (either 73 or 75 currently) you must withdraw a certain percentage from your tax-deferred retirement accounts, per IRS regulations (all except for Roth IRAs). These withdrawals are subject to ordinary income tax and may be subject to state tax as well, depending on where you live. This is often the primary source of retirement “income” for retirees as it’s very common for the majority of one’s liquid assets to be socked away in their former company’s retirement plan or a subsequent IRA.

It ’ s normally recommended that a certain percentage of this RMD is withheld for Federal taxes. This amount should be close to the account owner’s effective tax rate which can change from year to year. You can work with your advisor and/ or your tax preparer to determine what this should be.

Tax Considerations

TAXABLE TAX DEFERRED ROTH

Taxes on interest, dividends and net realized gains due annually (1099)

Tax-deferred growth until withdrawn; Withdrwawals taxed as ordinary

Contributions go in after-tax but grow tax-deferred and come out tax free if 5 year holding period is satisfied

Types of Accounts

Bank Accounts Stock/Bond Accounts Mutual Fund Accounts titled in single or joint names

Traditional Roth IRA, Roth 401(k), Roth Conversions

Remember, everyone’s financial situation is unique, and there is no one-size-fits-all approach to retirement planning. This traditional withdrawal sequence might need to be altered or customized for you, depending on how much you have saved in each type of account and the sum of your other retirement income sources. Before any decisions are made, it is imperative that you collaborate with your advisor at Fragasso and your tax professional to customize a strategy that aligns with your specific income needs, retirement goals, and tax position. This collaboration can have a meaningful impact on the longevity of assets and a retirement income plan’s success.

Women’s increasing wealth is a positive trend that has emerged in recent years as they continue earning more, inheriting more, and taking a more active role in managing their finances. As a result, women’s financial power is growing. Women are in control of a third of U.S. household financial assets – more than $10 Trillion, a figure expected to triple to $30 trillion by 2030. 1

As women’s wealth and investment footprint has grown so has their priority to plan for retirement judiciously. According to a study done by Cerulli Associates, the financial planning process is paramount to women investors. They found that women investors would rather engage in a holistic, goals-based process that prioritizes financial planning over portfolio construction. 2 Women face unique retirement planning considerations due to a variety of factors including gender pay gaps, career breaks for caregiving, longer life expectancy, and other societal and economic factors. Keeping in mind that every individual and family’s situation requires unique planning, here are key retirement planning considerations that should be evaluated.

1 Retirement Savings

As women continue to increase their income streams, simply saving into your retirement plan may no longer be sufficient for you to meet your goals. If you are already maximizing your retirement plan savings ($23,000 for a 401(k) in 2024 with an additional catchup contribution of $7,500 for those over the age of 50), saving into other vehicles and the tax implications of those savings techniques should be considered.

2

Investment Management

While women are known for investing less than men, their returns have historically been higher while taking on less risk in their portfolios. 3 Regardless of your investment style, investing for your own retirement goals can be an overwhelming task. Our advisors, along with the expert guidance from our portfolio management team, are diligent in selecting appropriately structured models that support in meeting your retirement goals and risk tolerance.

3 Social Security

As you get closer to retirement, having an understanding of your Social Security options should be a part of your plan. This includes strategies as a spouse, ex-spouse, or widow. While you may be able to collect on your own retirement benefit as early as age 62, this may not be the best option for you given your retirement goals and other financial circumstances.

“WOMEN BELONG IN ALL PLACES WHERE DECISIONS ARE BEING MADE. IT SHOULD NOT BE THE EXCEPTION ."

4 Protection for Your Family

Unexpected illness or premature death can occur in any family. And women are taking the steps to insure themselves and their partners so that their retirement and other financial goals can still be met regardless of what life brings them. It’s crucial to conduct an in-depth analysis to determine that the appropriate life insurance, disability insurance, and long-term care insurance strategies are in place to protect loved ones.

5 Education Planning

While saving for your children’s education may not directly impact your retirement, it does allow for separate buckets of savings for separate goals. And given the significant cost of education, starting a tax efficient Education Savings plan early means less chance you’ll take distributions from your retirement accounts to fund these costs later on.

Ruth Bader Ginsburg said, “Women belong in all places where decisions are being made. It should not be the exception.” As women’s careers continue to flourish and with inheritances often passed to a surviving spouse, now is the time for women to take an active role in their family’s finances and prioritize retirement planning. Utilizing a financial advisor can help you navigate these considerations and create a personalized plan that meets your unique needs and circumstances. And while the task may be overwhelming, rest assured that Fragasso Financial Advisors is here to help you every step of the way.

With so many factors impacting one’s retirement, there is no “one size fits all” answer. There is a data driven formula that can project your assets, retirement income, spending and estimated timeframe. However, retirement is not just a data driven event. It’s emotional as much as it is analytical. It’s your lifestyle, your family, your health, even where you live can impact your retirement needs. The factors contributing to your answer are as unique as your fingerprint!

To help evaluate your progress towards retirement security, Fragasso has created a new tool – a Can You Afford to Retire? Quiz. If you are nearing retirement and have at least $250,000 of investible assets saved outside of your retirement account(s), we invite you to take this complimentary quiz. It takes just a few minutes for you to enter the data driven points into the quiz. From there, a financial advisor will review your data and conduct an introductory consultation to discuss your unique circumstances and goals.

This process will provide more clarity. The peace of mind that comes along with your unique plan is invaluable. The Can You Afford to Retire? Quiz is designed to uncover your financial and emotional needs - coupled with the knowledge of retirement planning strategies from the team at Fragasso, a passing grade on your quiz is possible!

START PLANNING NOW

CAN YOU AFFORD TO RETIRE?

LEGACY AND ESTATE PLANNING CHARITABLE PLANNING NO YES WHEN DO YOU WANT TO RETIRE? UNSURE ARE YOU PLANNING FOR YOU OR YOU AND A SPOUSE? NO YES DO YOU OWN A HOME?

INVESTMENT ARE YOU A BUSINESS OWNER? RETIREMENT STRATEGIES

INCOME TAX STRATEGIES

PREPARING PORTFOLIOS

FOR RETIREMENT

Retirement is the summit of the investment mountain, and arguably the key event in the portfolio management lifetime. Investors spend most of their working life saving for retirement before suddenly shifting their financial priorities to focus on wealth preservation and income. This change can be stressful and complex, but a well-considered portfolio management plan can ease the transition. Our portfolio management team works in concert with our advisors and financial planners to balance the four key needs of clients in retirement: Portfolio stability | Inflation protection

1. Portfolio Stability Rises in Importance at Retirement

The most pressing concern for the retiring investor is often the need for additional stability. Younger investors with stable employment income can typically tolerate more volatility on a daily or yearly basis than those who are depending on their investment portfolio as the primary source of funds. For this reason, assets are usually reallocated from stocks to bonds as investors age. Price movements in the bond market are typically much smaller than those seen in stocks.

However, this is not the only way to lower portfolio volatility. Within the universe of stocks, stable companies like those in the consumer staples and healthcare sectors tend to move only half as much as riskier stocks in the technology or energy sectors—this can be an important consideration within equity portfolios:

Source: FactSet

Structured products can also limit the ups and downs experienced by retired investors. By giving up some potential for outsized returns, investors can also insure themselves against a portion of losses if markets fall. The chart below illustrates how a hypothetical structured note might perform in a variety of market environments:

Hypothetical performance of a structured note with 15% loss buffer and 15% cap.

We utilize a range of products and asset classes to customize portfolios to individual client risk tolerance.

Source: Fragasso Financial Advisors

2. Inflation Protection Should Not be Neglected

Inflation protection should be another high priority for retired investors, but it is one that is often overlooked in favor of stability. Cash in the bank offers safety, but the relentless effects of inflation almost guarantee a loss of purchasing power over time. Younger investors have only felt the effects of inflation recently, as the world rebounded from COVID-19. However, inflation averaged almost 4% annually over the last 50 years, and some would argue that easy fiscal and monetary policy in recent years heightens the chances that inflation will remain above the low levels we enjoyed over the last three decades. Thus, investments that are unlikely to keep pace with inflation can be very risky, even if their price stability is attractive.

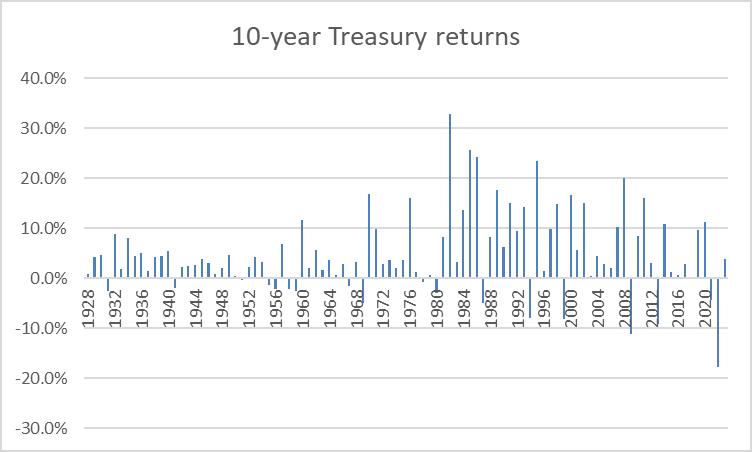

The unusually bad performance of fixed income investments in 2022 highlighted the risks of bonds in an environment of rising inflation and rising interest rates.

2022 was Unusally Bad for Bonds

Source: NYU Stern School of Business

While we believe stocks and bonds should remain the foundation of most portfolios, we think assets that perform well in inflationary environments can be a useful addition. These include incomegenerating hard assets like real estate and infrastructure, as replacement value for such assets increases with inflation and their rents and other revenues often climb along with other prices. Bonds with adjustable interest rates can also be helpful, as the prices of long-term bonds can move substantially as inflation expectations change. We don’t typically include commodities like gold, which generate no income and can be expensive to buy and hold. Such holdings can be counterproductive for retirees in need of consistent income.

3. Thoughtful Income Supplementation is Necessary

Retirees also need income to replace their regular paychecks. Many types of high-yielding investments are appealing at first glance, but often add unnecessary risk as well—there is a good reason that below-investment grade bonds are referred to as “junk”. Additionally, high-yield bonds can be highly correlated to the stock market, providing little diversification benefit.

High-yield Bonds

In fact, investors often underestimate the role of stocks in producing retirement income. Dividend income is typically tax-efficient, but may come at the cost of total return—mature companies that

pay high dividend yields often lack growth opportunities, and are forced to return capital to shareholders rather than reinvest for growth. Tobacco companies are one such example—high dividend yields are offset by a shrinking market of smokers and additional regulatory and litigation risk. In general, however, the high total returns generated by equities mean that investors can potentially generate income from sales of stocks while still enjoying some of the benefits of portfolio growth.

The average investor can also benefit from an increasing menu of fixed income options beyond high-yield bonds. Government bonds, asset-backed securities, structured products, residential and commercial mortgages, and other such categories can now be complemented with niche asset classes like music royalties or litigation finance. These asset classes provide a degree of useful diversification and typically yield more than U.S. treasuries.

4. Asset Growth and Tax Management Prepare Portfolios for Generational Transfer

While some of our clients will want or need to spend down their portfolios during their lifetimes, others wish to leave a legacy for their heirs or for charity. In order to do so, portfolios must grow beyond spending plans and be shielded from unnecessary taxes and expenses.

One extremely valuable tool is direct indexing—breaking up a fund or index into its components. Separately managed accounts that hold individual securities are extremely valuable in creating tax assets. Even in years when the market is up, numerous stocks go down in value and can be sold to generate tax savings.

Asset location is another valuable tool in this process. One simple example of this strategy is placing bonds and other incomegenerating investments in tax-deferred accounts, where profits are shielded from taxes. Growth stocks and related instruments can be placed in taxable accounts and held indefinitely, deferring tax liabilities on unrealized gains.

Finally, long holding periods and low turnover also help minimize taxes. Before a security with significant capital gains is replaced, we calculate the tax liability that must be overcome in order to make the change worthwhile. In many cases, the cost overwhelms the potential benefit—this is one reason why Warren Buffett’s favorite holding period is “forever”. Low turnover also reduces the complexity of client portfolios and statements.

A Consistent Approach Helps Simplify Portfolios

Many of our clients approach retirement with a variety of holdings accumulated over their investment lifetimes, including employersponsored retirement accounts, taxable and tax-free personal accounts, bank balances, and health savings accounts. We analyze and recommend portfolios on a consolidated basis, ensuring that a risk/return profile consistent with client preferences is considered across the board. As mentioned above, we are also able to locate assets in the most appropriate type of account to minimize taxes. Finally, we employ a systematic process of asset allocation and security selection so that clients can understand how each individual holding fits into a diversified portfolio and contributes to their needs as retirees. While we utilize a wide range of securities and solutions within portfolios, our holistic approach to portfolio management helps provide clarity and peace of mind for our clients as they transition into retirement. f

MICHAEL GODWIN, CFA Chief Investment Officer

JIM

SINEGAL Senior Investment Analyst

SERHIY ZAYATS

Investment Analyst

WILL SKIDMORE Trading

Analyst

FRAGASSO'S PORTFOLIO MANAGEMENT TEAM

DR. KENTON AND LAUREN REXFORD

Dr. Kenton Rexford, a native of Bellefonte, Pennsylvania, moved west to Franklin, Pennsylvania at a young age. From the age of four, he was determined to become a veterinarian, according to accounts from his mother, Carol. Kenton’s dedication to this aspiration led him back to Central Pennsylvania to pursue his undergraduate degree in Animal Bio Science at Penn State University. He furthered his education at the University of Pennsylvania’s School of Veterinary Medicine, where he earned his Veterinariae Medicinae Doctoris (VMD) degree.

Kenton’s entrepreneurial spirit shone brightly throughout his career. His vision and drive were pivotal in being a founder of Pittsburgh Veterinary Specialty and Emergency Center (PVSEC), one of the country’s premier animal hospitals and emergency centers. PVSEC stands as a testament to Kenton’s commitment to advancing veterinary care, offering critical and specialty services that have significantly improved the lives of countless pets and their families.

In retirement, Kenton and his wife, Lauren, remain deeply committed to their community. Kenton’s passion for animal welfare continues through the Animal Care and Assistance Fund (ACAF), a non-profit organization he established in 2008. ACAF provides vital financial assistance to pet owners facing economic hardships, helping them avoid the heartwrenching decision of euthanasia for pets with treatable but life-threatening conditions. The fund alleviates the financial burden for families, ensuring that the cost of care does not compromise a pet’s chance at recovery and a good quality of life.

Kenton’s dedication to education is reflected in the scholarships he has endowed at Penn State University and the University of Pennsylvania. These scholarships support students pursuing degrees in Animal Science, underscoring Kenton’s belief in the transformative power of education— a value deeply ingrained in him by his late father, Dr. Gene Rexford, a respected educator and superintendent.

Beyond his professional and philanthropic endeavors, Kenton and Lauren lead an active personal life. They take pleasure in hosting gatherings for family and friends at their home north of Pittsburgh. Their fall weekends are often dedicated to Penn State football, where they passionately support Kenton’s alma mater, whether from the stands or at home. Their travels are diverse, ranging from sailing in the Caribbean to snowboarding at Seven Springs and various destinations out west. A particularly memorable experience was their European adventure last summer, where they traveled around the Tuscany region of Italy.

Kenton and Lauren share their home with three beloved pets: Russett, a 140-pound French Mastiff, and their two cats, Violet and Scarlett.

Dr. Kenton Rexford’s journey from a young boy with a dream to a distinguished veterinarian and philanthropist illustrates his unwavering dedication to animal care, education, and community service. His legacy lives on through PVSEC and ACAF, and his vibrant personal interests add a rich, adventurous dimension to his life. Kenton and Lauren’s story is one of dedication, compassion, and a deep commitment to making a difference both professionally and personally.

This issue of The Advisor is all about retirement, but for those who own their own business, the act of retiring may also include exiting a business. Just as everyone’s retirement vision is different, each business owner has a unique vision for what happens to their company once they retire. Making that vision a reality takes detailed planning.

With the baby boomer generation entering the retirement phase, the number of business transitions to happen in the next decade is substantial. According to a 2022 study from BEI, a survey with over 200 business owners with revenue of over $2.5 million and more than 10 employees throughout the U.S. and Canada resulted in the following: 1

43% of business owners want to sell or transfer theopir ownership within the next 10 years.

80% of business owners want to stop working in their businesses in the next 10 years.

Only 20% of owners have created written plans to transfer ownership.

This creates a huge opportunity for exit planning. In the pages ahead, you will learn more about the factors that need addressing in an exit plan as well as advice on how to maximize your retirement assets as a business owner.

1

Q A

& WITH A CERTIFIED EXIT PLANNING ADVISOR (CEPA®)

Many business owners invest deeply in their businesses, and when the time comes to transition, whether to retire, start something new, or hand over the reins, the process can be complex. Two of our professionals at Fragasso have recently earned the Certified Exit Planning Advisor (CEPA) designation, which better equips them to help business owners plan and execute successful exits.

This certification, offered by the Exit Planning Institute (EPI), enhances the advisor’s ability to engage with business owners, focusing on building company value, aligning personal goals, and considering all aspects—financial, emotional, and operational—of the transition process.

In this Q&A, we’ll provide a comprehensive overview of the certification and how it can ultimately help benefit our clients.

Q&A with BRYAN REFT , CFP®, CEPA®

QWhat encouraged you to pursue the CEPA® designation?

AI’ve always admired business owners. I believe that it takes a lot of courage and determination to follow their dreams and build something from the ground up, or in some cases, continue a business as a second or third generation owner. It’s an amazing accomplishment. Although I am not a business owner in the traditional sense of the term, we are an employee-owned company, and so I get to experience the privileges and challenges of being an owner myself. I began researching business transitions and exit planning, and after reviewing the statistics, I was floored by how often owners are unsuccessful at exiting their business on attractive terms to them and their families. My article on page 27 talks about more about those statistics.

QHow is this designation obtained?

A

It was obtained through an organization called the Exit Planning Institute, or EPI. The program consists of coursework through self-study and online classes. After the coursework is complete, there is an exam that you need to pass to obtain the credentials.

Q

What are the yearly education requirements to maintain your credentials?

A

There is a continuing education requirement of 40 hours of exit planning professional development which needs to be completed every 3 years. Along with continuing education, there are professional and ethical standards that must be adhered to as well.

QHow can the skills you developed help clients navigate a successful business transition more effectively?

AIt helps by preparing owners for their exit as of today. That may sound a bit strange at first, but after obtaining this designation, I’ve come to believe that a big reason why business owners fail in transitioning their businesses is because that they don’t plan for their exit soon enough. The one thing we can never get back is time. Proper planning today can help increase the value of your business at the time of exit, as well as expand the exit options available to you.

WATCH THE VIDEO BLOG

Q&A with CHRISTINE ROBINETTE , CFP®, CPWA®, CEPA®

QWhat encouraged you to pursue this designation?

AAt Fragasso Financial Advisors, we have had the privilege of guiding many small business owners through their financial journeys. Over the years, we have witnessed their dedication and passion in building their businesses. As they approach retirement and begin to consider how best to transition their business—whether that means maximizing its value or passing it on to family—we recognized the need to deepen our understanding of their unique challenges. Transitioning a business requires meticulous planning and expert guidance to align one’s business, personal, and financial goals.

QWho can benefit from working with a CEPA® advisor? A

It is vital that every business owner engages in a structured and comprehensive planning process before transitioning their business. Navigating an exit plan is complex and emotional. A CEPA® takes an integrated approach to exit planning. A CEPA® can be the quarterback of this process to guide all professionals involved in developing a personalized exit strategy that considers financial needs, family dynamics, and longterm goals.

Q What does it mean to you to be a CEPA®?

AWhen I was a financial advisor for almost 20 years with our firm and now the manager of our client experience, every decision I made in the past and make now is guided by what is best for our clients. The decision for Bryan and I to obtain the CEPA® certification was made to deepen our knowledge of succession planning. We thrive on providing our clients with a holistic and comprehensive approach to one of the biggest decisions of their lives.

JENNAE BACKO Digital Content Manager

jbacko

@ fragassoadvisors.com

>

TPresident,

Advisor

he benefits of owning your own business can be endless. Financial rewards are a primary benefit but so is the independence, flexibility, and control of running your own company. While extremely rewarding, being a business owner is challenging work. Business owners can be so focused on the day-to-day activities involved with sustaining a successful business that they neglect planning for the future of their company. Creating an individualized, robust, well-orchestrated succession plan is imperative for a company to provide stability and continuity in a time of crisis like death, disability, or a transition, such as retirement. Failing to plan well in advance can be costly and detrimental, yet this planning continues to be commonly neglected. Most surveys indicate that 60% of small businesses do not have an exit plan in place.

PROTECT YOUR LIFE’S WORK AND LEGACY WITH A BUSINESS SUCCESSION PLAN

REASONS OWNERS AVOID SUCCESSION PLANNING

They are unsure where to begin. They believe they will never leave their business or retire.

They do not know what professionals can help create their plan. They feel they have no time to develop the plan. They feel they have plenty of time to worry about succession planning later.

Not only is succession planning imperative, but it also needs to occur as early as possible. Successfully transitioning a business is directly correlated to how early you begin planning. According to one research study, business owners who begin planning for their succession ten years ahead of time had an 85% success rate while owners planning two years or less resulted in only a 25% success rate.1 A main reason for this disparity is that the longer you wait to create your plan the less options you have.

WILLIAM WOLFE CFP®

Senior Vice

Financial

wwolfe @ fragassoadvisors.com

BENEFITS OF SUCCESSION PLANNING

There are many benefits for companies and owners who plan early, properly, and strategically for the orderly transition of management and ownership. They include but are not limited to:

Maximizing the survival and value of the business.

Whether you plan to sell to a family member, employee, business partner or third party, a comprehensive plan can assist in obtaining the most advantageous value for your business.

Establish financial security and maintain your lifestyle in retirement.

It is important for the business owner to determine their income needs and assets needed to live comfortably in retirement. This must be factored into the succession plan.

Provide for family members.

In the event of disability or premature death, a succession plan can help ensure that family members have access to much-needed liquidity.

Minimize taxes and efficiently transfer wealth.

Estate taxes and other costs can be extensive and can ultimately cause businesses to fail. Beneficiaries may be forced into a too-quick sale to pay those taxes.

Ability to retain control.

Business owners have spent their lifetime making their own decisions to grow their company; a plan allows them to control the process and outcome.

KEY STEPS TO A GOOD SUCCESSION PLAN

1. Define your succession goals.

The owner needs to pinpoint their individual needs, their family’s needs, and the needs of the ongoing business before they can determine the succession tools needed to meet those requirements.

2. Determine options for future leadership.

The future leaders could be family, a business partner, a third-party buyout, or employees of the business.

3. Obtain a valuation for your business by a certified professional. There are three main valuation methods. One method could be utilized, or it can be a combination of these approaches.

Income-based approach – This approach utilizes a discount rate to calculate the present value of future cash flows. There are several types of discount rates that can be used.

Market-based approach – This approach estimates the value of the business by comparing the market price of comparable businesses.

Asset-based (cost) approach – Estimates the business’s value by calculating the company’s assets minus its liabilities.

4. Finalize who will be the successor.

Once you have decided on a successor, you want to also determine what support and training this successor may need.

5. Design the succession plan.

Outline the succession details, organizational structure, and timeline. Depending on whom ownership will be transferred to will ultimately determine the vehicles needed to ensure a smooth transition. These vehicles may include life insurance, family trusts, buy-sell agreements, or an employee stock ownership plan (ESOP), to name a few.

6. Communicate the plan.

To be effective it is important to share the details with those impacted so they can clearly understand their roles with respect to the company. The more communication the better.

7. Review the plan on a regular basis.

Key employees may leave, family members could change their mind, or the owners’ goals and plans may change.

Every business owner will eventually exit their business. Whether it be for retirement, disability, or death. There are many steps and decisions that need to be made so that your tireless work to build your business remains your legacy. Having your professional “board of directors” (attorney, CPA, financial advisor, etc.) involved every step of the way is critical.

Your advisor at Fragasso Financial Advisors can be the coordinator of these professionals to help make sure not only your business financial planning is taken care of, but also your individual financial planning to create a cohesive solution that incorporates all areas of your financial picture. f

The importance of planning BUSINESS OWNERS EXIT

If you do not know where you are going, how do you know what road to take to get there?

Now that is a great philosophical question for us all, but it is an even more important question for a business owner. for

According to the Exit Planning Institute, 250,000 U.S. companies between $5 million-$100 million in sales plan to exit by the year 2030.

Of those 250,000: only 50,000 will be deemed ‘market ready’.

30,000 will transact, whether it is a sale, merger, or acquisition.

16,000 will sell with some type of concession. And only 14,000 will sell at their desired value.3

Let us imagine for a second that we are taking a road trip across this beautiful country of ours. We will start here in Pittsburgh and our destination will be Huntington Beach, California. Do you just get in your car and start driving west? Of course not! Before you even leave your house, you have already mapped out the route that will get you to your destination, usually, in the most efficient way possible. There are checkpoints at various locations that you want to visit along the way. Well, the same practices we apply to our personal journeys can be applied to businesses. If you don’t know where you want your business to be in the next 5, 10, or even 20 years, then how do you know what your checkpoints are to ensure that you get to your destination, or in other words, your inevitable exit from the business? Without a roadmap, it is easy to miss important opportunities, or end up somewhere you did not intend to be. Regularly assessing where you are allows you to adjust your course, navigate challenges, and stay focused on your goals.

Chris Snider, CEO of the Exit Planning Institute, and author of Walking to Destiny, states that “Exit Planning is simply good business strategy.” As an owner, it is extremely easy to put your eventual exit from your business on the back burner because it is usually, in your mind, a distant point in the future, and quite honestly I understand. With all the demands of running your business day in and day out, it is quite common for business owners to put their own personal and financial planning on the back burner and devote their attention to the needs of the business. The reality though is that exit planning is not just some future event that will happen years from now. Exit planning needs to be thought of in the present tense. Every decision you make will influence the options available when you exit as you will see in the following examples.

Typically, 80% of a business owner’s net worth is tied up in their business. I would venture to say that most owners who are reading this are pausing to do a quick calculation of their own personal balance sheet right about now, but that statistic makes sense. As an owner, most of your time and capital has gone into building your business over the years. Chris Snider states that only 20%- 30% of businesses that go to market will sell.1 Let’s think about this for a second. 70% to 80% of business owners, who have worked tirelessly for years on end, in some cases for their entire lives, will never be able to sell their business. I do not know about you, but that is staggering to me! Even more unsettling is the fact that those business owners will, unfortunately, never unlock the value of their business after all their hard work.

Why is that so unsettling? Remember, typically the business is an owner’s largest personal asset making up about 80% of their net worth.

Can most business owners afford to write off 80% of their net worth and rely on the other 20% to get them through retirement? Probably not. At least not without drastically changing one’s quality of life in retirement.

What about those business owners that do not want to sell to a third party, but instead, would like to transition their business to their family members? Well, for owners that plan on a family transition as their exit option, the statistics, unfortunately, are not much better. Only 40% of U.S. family-owned businesses survive to the secondgeneration, and only 13% of businesses survive into the third generation.2

I will leave you with one last staggering statistic per the 2023 National State of Owner Readiness Report conducted by the Exit Planning Institute,2 75% of business owners would like to exit their business in the next 10 years, while 49% of business owners would like to exit in the next 5 years. That equates to a massive amount of business value that has the potential to be unlocked. My question to you as an owner is, what side of the statistics are you and your business most likely to fall on?

I recently obtained my Certified Exit Planning Advisor (CEPA®) designation (see more on page 23). I am committed to walk alongside my business owner clients to help create a well thought out plan that can not only help an owner increase the value of their business but also to align all facets of their livespersonal, financial, and business.

With the largest transition of wealth on the horizon, we have the opportunity to educate and act upon exit planning strategies to sway the statistics in favor of business owners. Look for consistent content in future issues of The Advisor magazine, and feel free to reach out to me to discuss this topic further. f

1 Snider, Christopher M., Walking to Destiny: 11 Actions An Owner MUST Take To Rapidly Grow Value & Unlock Wealth, ThinkTank Publishing House, 2023

How a Cash Balance Plan Can Help Business Owners BOOST RETIREMENT SAVINGS

Retirement plans such as a 401(k) or a 403(b) offer employees an easy way to save for their future in a tax advantaged manner. These types of plans are an important part of an overall benefits package to help attract and retain key employees. This is especially important in an increasingly competitive labor market.

These plans can also allow business owners and key personnel to save up to $69,000 in 2024 on a tax deferred basis ($76,500 for those over age 50). These savings limits can help business owners build retirement accounts as well as reduce current taxes. Cash balance plans could be a consideration for those that would like to save above and beyond the limits of a 401(k) plan.

WHAT IS A CASH BALANCE PLAN?

Like a 401(k), the IRS considers cash balance plans as qualified retirement plans. They share some features, but they also have some important differences. Cash balance plans are a form of a defined benefit plan, while a 401(k) is a defined contribution plan. The company makes contributions on behalf of employees; individual employees do not contribute to a cash balance plan. These contributions are tax deductible to the company and any growth in the plan is tax deferred until withdrawal. The contribution limits of a cash balance plan increase with age and are much higher than a 401(k).

As an example, a 58-year-old may be able to contribute up to $288,000 in 2024 and a 62-year-old up to $351,000 depending on the design of the plan. A cash balance plan can be a standalone plan or set up in conjunction with a 401(k) plan to allow plan sponsors to maximize the benefits of both plans.

DANIEL TATOMIR , AIF® Vice President, Manager of Retirement Plan Advisors dtatomir @ fragassoadvisors.com >

WHAT ARE THE CONSIDERATIONS OF A CASH BALANCE PLAN?

The tax savings and higher saving ability of a cash balance plan can be very attractive, but all aspects should be fully understood before deciding to start a plan. Unlike a 401(k) plan where the investment risk is born by each participant, the risk of a cash balance plan is born by the employer. Contributions grow at a predetermined rate – remember with a cash balance plan, the benefit is defined. Often this is set at 4% or 5% annually. Generally, contributions are required each year, although there is some flexibility in the amount you contribute each year.

Plan assets are pooled together and invested with the goal of working towards the predetermined rate of return. Costs of a cash balance plan are usually higher than 401(k) plans due to the complexities in set up and the annual testing and reporting that is required.

WHAT TYPE OF COMPANY IS A CASH BALANCE PLAN APPROPRIATE FOR?

The usual candidate for a cash balance plan is an employer looking to maximize the tax benefits and retirement savings ability above the limits of a 401(k) plan. Medical groups and law firms have historically been frequent sponsors of cash balance plans, but any company with sustainable income looking to increase retirement funding can open a plan. They work well for small employers. In 2020, 94% of cash balance plans were sponsored by companies with less than 100 employees and 59% had 10 or fewer employees.1

Cash balance plans are also a potentially attractive option for self-employed individuals who are looking to maximize retirement savings.

If you would like discuss the possibility of implementing a cash balance plan for your company or would like to review your current retirement plan to maximize its benefits to the company and employees, our dedicated retirement plan department at Fragasso will always welcome the conversation.

1. Kravitz National Cash Balance Plan Research Report. https://www.cashbalancedesign.com/resources/research-report/

by MARSHA POSSET, LDI XXI, YALP VI mposset@fragassoadvisors.com

LEADERSHIP PITTSBURGH INC. C RNER

I became aware of Leadership Pittsburgh Inc. like most of their program participants do – a colleague and/ or an alumni encouraged me to learn more and apply. That is a common beginning to one’s journey with Leadership Pittsburgh Inc. For me, however, after I was accepted and even graduated from the program, my experience circled back to that awareness stage. As a marketing director, I am no stranger to a sales cycle, and therefore, Leadership Pittsburgh Inc. offered me the opportunity to serve as a junior board member and on their marketing and recruitment committee.

It has been ten years since I graduated Leadership Development Initiative (LDI) Class XXI and started serving in a volunteer capacity on a committee that drives the awareness of Leadership Pittsburgh Inc. and the asset that they are to our community. Their programs are designed to cultivate a deep understanding of the complex issues and opportunities impacting Southwestern Pennsylvania. Diverse groups of leaders are selected each year to take part in Leadership Pittsburgh Inc.’s three different programs:

1. Leadership Pittsburgh - for established leaders,

2. Leadership Development Initiative - for emerging leaders, and

3. Community Leadership Course for Veterans - for former military service members.

Each program is unique, but all participants benefit from personal growth, expanded professional networks, and are inspired to foster positive change for our region.

Since their inception in 1983, Leadership Pittsburgh Inc. has remained dedicated to shaping exceptional leaders, fostering community engagement, and driving positive change. They boast an influential alumni network comprised of over 3,500 civic leaders working together to maximize the potential of our community. As an independent 501(c)(3) nonprofit organization, they have grown to become the premier resource for community leadership in the region.

As my personal journey with Leadership Pittsburgh Inc. continues, in 2024 I was presented the opportunity to participate in Harvard Business School’s Young American Leaders Program (YALP) . Harvard Business School (HBS) invites rising leaders from American cities who reach across sectors to help their communities prosper. This program exists because of Harvard Business School’s hope for growth amongst U.S. competitiveness, and the purpose of this annual leadership summit is to inspire public/private cross-sector collaboration.

During the last week of June, fourteen cities are asked to each send ten diverse leaders to convene at the HBS campus. These select leaders participate in open discussions centered around the most challenging issues facing our cities today, such as but not limited to, infrastructure, racial disparity, health care, education, workforce/employment challenges, and climate change. These discussions are based on Harvard case studies and facilitated primarily by tenured Harvard professors along with a few other accomplished guest speakers.

Every agenda item and all the groups of people you interact with at YALP have been organized with an intention. The intentions for the participants are:

1. To realize commonalities and learn from one another

2. To expand your network and perspectives

3. To identify the skills and processes required to create successful cross-collaboration efforts

4. To be inspired to take action for the future benefit of our hometowns

I am truly honored to have experienced both Leadership Development Initiative and the HBS Young American Leaders Program. I am committed to utilizing the skills, insights, and networks gained from these programs for the betterment of Fragasso Financial Advisors and the other communities/organizations I serve.

For more information on Leadership Pittsburgh Inc., VISIT WWW.LPINC.ORG

Congratulations to our President and Executive Director of Portfolio Management, Daniel Dingus, on being accepted to Leadership Pittsburgh's current 2024-2025 class!

Daniel J. Dingus

Leadership Pittsburgh, Class XLI

Daniel is currently participating in LP Inc.’s flagship program, Leadership Pittsburgh. This is a ten-month program for established senior-level leaders. He will be joining a group of approximately sixty professionals who attend monthly sessions to obtain a deeper, behind-the-scenes understanding of the connected systems of the region. The class is comprised of our region’s most influential stakeholders and together they will explore the challenges and opportunities of our community in a new and profound way.

YALP Participating Cities:

“We open eyes, minds, and doors.” Leadership Pittsburgh Inc.

Pittsburgh's 2024 YALP participants (from left to right): Jacqueline Brown, Sharon Novak, Sharjeel Farooq, Evan Rosenberg, Kyle Chintalapalli, Ryan Niemeyer, Marsha Posset, Lauren Connelly, and Melissa Pearlman

PITTSBURGH BUSINESS TIMES, 2024 BEST PLACES TO WORK

Employees from Fragasso attended a celebratory awards event followed by the Pirates ’ last home game of the season at PNC Park. Fragasso Financial Advisors earned the No. 7 spot in the medium category for this year ’ s rankings.

The results of Best Places to Work are based on an online survey of employees, which was conducted in 2024. Companies are surveyed on a variety of factors ranging from employee job satisfaction to salary satisfaction to perspectives on management. Small companies have between 10 and 24 employees, medium 25-49, large 50-149 and extra-large 150-plus.

NEW HIRES

Tricia Bodamer, client account specialist works in Fragasso’s South Hills office supporting the financial advisors in performing daily administrative and operational functions. She serves as the point person connecting clients with their advisor overseeing their requests and ensuring an efficient flow of communication. Tricia has previous experience working in investment advisory firms in Pittsburgh, and prior to that, in Boston.

Tricia is originally from a small town near the Jersey Shore. She met her husband in college. He is originally from Pittsburgh and now they are raising their family here. Outside of the office, Tricia’s interests are cheering on her daughters’ soccer teams, walking her dogs, and she looks forward to spending time with extended family each year during their beach vacation.

Luigi Scognamiglio, technology and operations analyst is part of Fragasso’s technology and operations department. Luigi ’ s focus is on optimizing operational processes through technology-driven solutions, pursuing efficiencies, and supporting the company’s technological infrastructure. Before joining Fragasso, Luigi worked as an IT analyst/project manager for the University of Pittsburgh where he was responsible for managing infrastructure projects, troubleshooting technology issues, and collaborating with teams to ensure successful project execution and system enhancements.

Luigi was born and raised in Caserta, a small city just outside Naples, Italy. He spent the first sixteen years of his life there before embarking his journey to the U.S. during his junior year of high school as part of a year abroad program. This experience was transformative and led Luigi to pursue further education in the U.S. He attended Seton Hill University and earned a bachelor’s degree in computer science and an MBA in project management.

Luigi is passionate about travel and exploration. He has a personal goal to visit all fifty states by the time he turns thirty and to see all seven wonders of the world by his fortieth birthday. Besides travel, his hobbies include volleyball, and he enjoys taking cooking classes where he can immerse himself in different culinary techniques.

THANKSGIVING FOOD DRIVE AND PANTRY SORTING

On October 22, 2014, Fragasso Financial Advisors participated in a volunteer day with the South Hills Interfaith Movement (SHIM). The "Wealth of Kindness" crew brought Thanksgiving food pantry donations and assisted with a surprise delivery truck that arrived while they were on-site. Volunteers sorted additional donations and packaged rice and dog food, and toured one of SHIM’s thirteen gardens after the work was done.

Participants: Back (L to R): Bonnie Katz, Brian Robinette, T.J. Drost, Daniel Dingus, Daniel Tatomir, Giovanni Morgano. Middle (L to R): Andrew Silver, Brenda Beam, Yvette Dirani. Front (L to R): Leigh Fleming, Brianne King, Marsha Posset, and Mike Fertig (not pictured)

The work done by SHIM and its volunteers is a true blessing for the community!

Mike Fertig, senior vice president and financial advisor, beams with pride as he walks his daughter , Katie down the aisle.

WEDDING BLISS

Congratulations to Katie (Fertig) Shawley, our finanical planning assistant, on her marriage to Ryan Shawley on July 5, 2024! It was a stunning day! Wishing them a lifetime of health and happiness