Balancing Cereal Recovery with Structural Import Dependence Chair of the Bakery Subsector - Kenya Association of Manufacturers

Perfecting Your Flour Quality Through Innovation

and Expertise

With over 50 years of experience, Pakmaya stands by your side from diagnosis to solution. We offer practical and expert approaches tailored to your needs.

The Focus of Our Business

Flour Improvers Flour Fortification (vitamin and mineral premixes)

Year 4 | Issue No.18 | Jan - Mar 2026

FOUNDER & PUBLISHER

Francis Juma

SENIOR EDITOR

Martha Kuria

EDITOR

Stephen Kibe

Caroline Maina

EXTERNAL CONTRIBUTORS

Luca E. Mattei

William Gatama

DR.Fatima Maira

BUSINESS DEVELOPMENT

DIRECTOR

Virginia Nyoro

BUSINESS DEVELOPMENT ASSOCIATE

Johna Sambai

Wangari Kamau

HEAD OF DESIGN

Clare Ngode

DESIGN

Emmaculate Ouma

ACCOUNTS

Anita Kinyua

Published By: FW BRANDS MEA P.O. Box 1874-00621, Nairobi Kenya Tel: +254725 343932

Email: info@fwbrandsmea.com

Company Website: www.fwbrandsmea.com

We publish some of the most influential magazines and websites in Africa & the Middle East regions. Please visit the websites below for more information about our publications.

Milling & Feed Middle East & Africa is published 4 times a year by FW Brands MEA. Reproduction of the whole or any part of the contents without written permission from the editor is prohibited. All information is published in good faith. While care is taken to prevent inaccuracies, the publishers accept no liability for any errors or omissions or for the consequences of any action taken on the basis of information published.

www.foodbusinessmea.com

www.millingmea.com

www.horecamea.com

www.dairybusinessmea.com

FEE BUSINESS

www.feedbusinessmea.com

www.healthcaremea.com

www.sustainabilitymea.com

www.hpcmagmea.com

Flour in Focus

Issue 18 of Milling & Feed Middle East & Africa arrives at a pivotal moment in March 2026, coinciding with World Flour Month. Flour is the backbone of food security not only across Africa and the Middle East, but globally. March 20 was chosen for World Flour Day because it is the beginning of spring in the northern hemisphere and the start of harvest season in the southern hemisphere. The day stands for beginnings, change and abundance. In 2026, as World Food Day is commemorated for the seventh time, we launch this edition and pause to reflect on how the production of this staple commodity involves an interplay of agriculture, trade, technology, and policy.

Flour does not begin on the shelf. It begins in the field, moves through global trade corridors, and passes through silos, cleaning lines, conditioning systems, roller mills, sifters, and laboratories. Each stage is shaped by procurement decisions, extraction targets, and energy benchmarks. Behind every metric ton stands a network of professionals whose daily choices determine availability, affordability, and performance.

This issue deliberately focuses on data-driven mills. The operating environment has become more volatile, with weather variability, freight fluctuations, and currency pressures reshaping procurement strategies. Mills that embrace digitization, through predictive maintenance, ERP integration, and real-time analytics, are achieving higher extraction consistency, reduced downtime, and stronger audit readiness.

We also spotlight Tunisia, a net importer of wheat. Its dependence on global markets illustrates the vulnerability of economies where any disruption reverberates directly through the milling sector.To bring the industry home, this edition features key voices that the industry resonates with. Michael Ndukwe from Niger Mills provides technical insights from the plant floor, reflecting the realities of daily operations and the challenges of maintaining efficiency under pressure.

Abdallah Juma, Chair of the Bakery Subsector at the Kenya Association of Manufacturers, offers a broader perspective on regional dynamics, policy frameworks, and the role of bakeries in sustaining demand. Their contributions, alongside other experts, reinforce our commitment to making this platform inclusive and industry-driven.

A NEW PHASE FOR MILLING MEA

Since its inception in 2022, Milling Middle East & Africa has published six editions annually. Beginning this year, we transition to four issues per year. This strategic shift allows us to deliver deeper analysis, stronger market intelligence, and broader technical contributions. “Rather than increasing volume, we are increasing value. Each issue will carry greater analytical rigor and structured visibility for the practical knowledge held by key stakeholders across the sector, thereby offering value to the industry we passionately serve,” said Francis Juma, CEO and Publisher MMEA.

As flour continues to anchor daily diets, the systems behind it must become more resilient, more data-informed, and more collaborative. Issue 18 is not only the beginning of a new publishing cycle, it is a call to collective thinking about procurement strategy, operational efficiency, and long-term sustainability. We encourage all industry players to continue investing in systems that drive sustainable growth in the grains, milling, and baking sectors.

Finally, this issue provides a comprehensive roundup of the latest developments in the baking, milling, grains, and cereals sectors, featuring expert insights and the latest news updates.

Enjoy your read!

Martha Kuria, Senior Editor, FW Brands MEA Publications.

EVENTS CALENDAR

Africa Dairy Innovations Summit

APRIL 16-17, 2026

Nairobi, Kenya www.africadairysummit.com

VIV Select India 2026

April 22-24, 2026

New Delhi, India www.india.viv.net/

IAOM MEA

May 4– 5, 2026

Amman, Jordan www.iaom-mea.com/

Africa MILLING & FEEDTECH Expo

May 13-15, 2026

Lusaka, Zambia www.graintech.afmass.com/south/

AFRICA BAKERY EXPO

May 13-15, 2026

Lusaka, Zambia www.bakery.afmass.com/south/

IDMA

June 25-27, 2026

Istabul Expo Center www.idma.com.tr/

Africa MILLING & FEEDTECH Expo

July 15 -17, 2026

Nairobi, Kenya www.graintech.afmass.com/east/

Africa Food Awards

July 16, 2026

Nairobi, Kenya www.manawards.fwafrica.net/food

Africa MILLING & FEEDTECH Expo

September 15-17, 2026

Lagos, Nigeria www.graintech.afmass.com/west/

IBATECH

Oct 14 – 17, 2026

Turkey www.ibaktech.com/en/startseite/

CONSITUENT EVENTS

SIGN UP TO ATTEND, SPONSOR & EXHIBIT

EXPO MEAT & P ULTRY

AFRICA

NEWS UPDATES

REMORA completes 500 TPD flour mill installation in Senegal

SENEGAL – Industrial engineering firm REMORA recently completed key structural and electromechanical works for a new 500 tonnes-per-day (TPD) wheat flour mill project in Senegal, adding modern milling capacity to the country’s expanding grain processing sector.

The project was delivered in collaboration with Bühler Group and SCE Silo Construction & Engineering, combining expertise in milling technology, steel construction and industrial process installation.

According to Remora, the flour mill was completed in just four months, highlighting the efficiency of the engineering and installation teams involved.

As part of the project scope, REMORA carried out the structural assembly of the SCE building and completed the full electromechanical installation of the 500 TPD milling process line.

Founded in 1994 and headquartered in Casablanca, REMORA has developed into a specialized engineering contractor, with technical expertise covering flour mills, semolina mills, pasta production plants and animal feed factories.

Over the past three decades, REMORA has carried out industrial installations across Africa and the Middle East, supporting large-scale agro-processing projects for international technology suppliers and regional food manufacturers.

The new flour mill comes as Senegal’s wheat processing sector continues to expand alongside growing demand for wheat-based foods.

Although the country produces traditional cereals such as millet and sorghum, wheat is largely imported and processed domestically through industrial milling facilities.

According to the Food and Agriculture Organization Senegal imports more than 1.18 million tonnes of wheat annually to supply domestic flour mills and meet the demand for bakery products.

Bread remains a staple food across the country, particularly in urban centers such as Dakar, where thousands of bakeries depend on locally milled wheat flour.

Industry estimates place national flour demand at roughly 1,400 tonnes per day, driven by population growth, urbanization and the expansion of food processing industries.

Oman Flour Mills acquires majority stake in Arabian Food Production

OMAN - Oman Flour Mills Company SAOG (OFM), a cornerstone of the Sultanate’s food sector, has signed a share purchase agreement to increase its stake in Arabian Food Production Company SAOC from 33.33% to 66.67%, thereby securing majority control through its wholly owned subsidiary, Atyab Investments LLC. The deal acquires the remaining 33.34% stake from Gulf Japan Poultry Farm, subject to regulatory approvals and conditions.

Upon completion of the transaction and subject to the fulfilment of agreed conditions, its stake will rise to 66.67 per cent, giving the OFM group a controlling interest in the company.This vertical integration play enhances OFM’s dominance in Oman’s integrated food chain, from milling to finished products like breads, pastries, and poultry feeds produced by Arabian Food.

INVESTMENTS

Soufflet Malt breaks ground on US$118M malting facility in SA

SOUTH AFRICA - Global maltster Soufflet Malt has broken ground on a R2 billion (US$117.92M) malting facility in Midvaal, Gauteng, marking one of the most significant recent investments in South Africa’s brewing and agricultural value chain. Soufflet Malt, which operates 40 malting plants across 20 countries and produces about 3.7 million tonnes of malt annually, said the new malthouse will strengthen local supply chains and reduce reliance on imported malt.

The project follows the signing of a commercial partnership in March 2025 between Soufflet Malt and HEINEKEN Beverages to supply malt for HEINEKEN’s South African brewing operations. Strategically located next to HEINEKEN Beverages’ Sedibeng Brewery near Johannesburg, the Midvaal facility will have an annual production capacity of approximately 100,000 tonnes of malt. Once fully operational, it is expected to source 100% of its barley from South African farmers.

Olam Agri expands pasta manufacturing in Ghana, secures US$100M rice trade facility

GHANA - Olam Agri, a leader in food, feed and fibre, is set to commission a US$40 million pasta production plant in Tema, marking a major expansion of its wheat value chain and reinforcing its long-term commitment to local agro-processing.

The new facility, scheduled for inauguration soon, marks the next phase of integration at the Tema complex, extending value addition from milling into finished consumer products and reducing reliance on imported pasta.The investment builds on the US$55 million wheat milling plant launched in 2012 under former President John Evans Atta Mills. That facility, which employs 300 people and holds FSSC food safety certification, integrates grain storage, milling and packaging, and operates an in-house bakery and technical support services for customers. A 2017 expansion doubled annual capacity to 275,000 metric tons, positioning Ghana as an exporter of flour to Togo, Benin, Niger and Burkina Faso.

According to the agri-food giant, the new pasta plant will create 200 additional jobs, bringing total direct employment at the Tema complex to 500. “With this facility, we will be able to bring high-quality, highly nutritious, and affordable pasta products closer to our Ghanaian consumers than ever before,” said Baibhav Biswas, Country Head of Olam Agri in Ghana.

Alongside manufacturing expansion, Olam Agri has secured a seven-year US$100 million financing facility from FMO to support rice trade flows from India, Thailand and Vietnam into African markets. The facility, initially guaranteed by Olam Group, will later transition as part of the proposed sale of a 44.58% stake in Olam Agri to Saudi Agricultural and Livestock Investment Company. With Africa accounting for about 40% of global rice imports, the financing strengthens procurement cycles and working capital management in volatile grain markets, reinforcing Olam Agri’s role across origination, processing and distribution in key staple segments.

Africa’s wheat market projected to reach 84 MT by 2035

AFRICA – Africa’s wheat market is expected to return to a growth trajectory over the next decade, with total market volume forecast to expand at a compound annual growth rate (CAGR) of 3.3% to reach 84 million tons by 2035, according to a new report by IndexBox Market Intelligence. Wheat consumption declined for the fourth consecutive year, falling by 14.8% to 59 million tons. Market value dropped more sharply, down 25.1% year on year to US$18.1 billion, compared with a peak of US$26 billion recorded earlier in the decade.

Egypt remains the central pillar of Africa’s wheat market. In value terms, Egypt also led the continent, with a wheat market valued at US$7.1 billion. Nigeria, Algeria, Morocco and South Africa together accounted for a further 42%. Egypt also paid the highest average import price on the continent, at US$436 per ton, compared with an African average of US$317 per ton.

FINANCIALS

Invictus posts 184% EBITDA growth year-on-year in 2025

UAE - Invictus Investment Company PLC has reported its strongest financial performance since listing on the Abu Dhabi Securities Exchange in 2022, with EBITDA rising 184% year-on-year in 2025, supported by acquisitions, geographic expansion and product diversification across Africa and the Middle East. For the 12 months ended December 31, 2025, EBITDA reached AED 458.5 million (US$ 125 million), up from AED 161.4 million (US$ 44 million) in 2024.

Revenue increased 49% to AED 13.3 billion (US$ 3.62 billion), compared with AED 8.9 billion (US$ 2.42 billion) the previous year. Net profit rose 37% to AED 227.6 million (US$ 62 million), while return on equity reached 18%. Commodity transaction volumes expanded 73% year-on-year to 14.2 million metric tonnes, up from 8.2 million metric tonnes in 2024, reflecting stronger trade flows and the integration of newly acquired assets.

AGI unveils customer-driven bucket elevator

USA - Ag Growth International (AGI) has introduced a new bucket elevator engineered around operator and maintenance feedback, underscoring a shift toward serviceability and uptime in heavy-duty grain handling. The equipment was officially unveiled at the Grain Elevator and Processing Society (GEAPS) Exchange held at the Kansas City Convention Center, reported by the Word Grain.

The newly launched AGI Bucket Elevator delivers capacities ranging from 10,000 to 120,000 bushels per hour (bph), positioning it for use across commercial elevators, port terminals, ethanol plants and oilseed crush facilities.However, company executives emphasized that scale was not the only focus. Nearly a year of structured discussions with operators, maintenance teams, and engineering specialists shaped the final design. “For me, that was the most exciting, which was going to the customers, and instead of bringing them something we think they want, we ask them what they want,” said Ashley Gierok, enterprise sales manager at AGI.

The debut comes after the agricultural equipment and Technology Company, recently appointed Brad Wall and George Armoyan to its Board of Directors. AGI confirmed the appointment of the Honourable Brad Wall and George Armoyan to its Board of Directors further stating that Mary Shafer Malicki resigned from the board, while Rohit Bhardwaj and Mike Frank will not stand for reelection at the 2026 annual shareholder meeting.

AGI thanked Shafer Malicki, Bhardwaj and Frank for their work during a difficult period for the sector and for their continued support as the company adjusts its priorities. Wall brings public sector and agriculture policy experience shaped during his time as Premier of Saskatchewan from 2007 to 2018.Armoyan adds private sector and investment experience built over more than four decades. He serves as Executive Chairman of G2S2 Capital Inc., President of Armco Capital Inc., and Chief Executive Officer of Clarke Inc.

APPOINTMENTS

Bühler Group confirms

Samuel Schär as CEO

SWITZERLAND - Swiss technology and processing equipment leader Bühler Group has confirmed the appointment of Samuel Schär as Chief Executive Officer, effective January 1, 2026, concluding a succession plan first announced in April 2025. Samuel Schär assumed the role of Chief Executive Officer on January 1, 2026, succeeding Stefan Scheiber, who was elected Chairman of the Board in February 2026. The transition concludes a succession process first announced in April 2025 and maintains continuity in strategy and operations for the family-owned group headquartered in Uzwil, Switzerland.

“I am excited to lead the company into its next stage of development. Our focus will remain on creating value for our customers, driving meaningful innovation, and growing our business sustainably. Together with our global teams, we will continue to build strong partnerships and deliver solutions that enable our customers’ success,” said Samuel Schär. Scheiber’s move to the Board follows a 35-year career with the company, including 10 years as CEO.

The leadership change comes as Africa emerged in 2025 as Bühler’s largest regional market for its food and feed businesses. The shift reflects rising investment in grain milling capacity, value-added food production, and supply chain modernization across the continent. At Group level, order intake declined 0.5% in local currencies, totaling CHF 2.7 billion (USD 3.0 billion). Turnover decreased 7.8% to CHF 2.8 billion (USD 3.1 billion), mainly due to lower prior-year orders and project execution timing. Despite softer volumes, EBIT margin improved to 8.0%, up from 7.6%, supported by strict cost control and productivity gains. Within Grains & Food, orders declined 1.1% to CHF 2.15 billion (USD 2.36 billion), though segments such as Chocolate & Coffee and Value Nutrition posted growth. Bühler expects continued market volatility in 2026 but aims to reinforce its positions across grain processing, food, feed, and advanced materials through innovation and expanded services.

INVESTMENTS

SCE expands Africa footprint with new regional office in Côte d’Ivoire

CÔTE D’IVOIRE – SCE Silo Construction & Engineering, a global player in designing, developing and building silo solutions has opened a new regional office in Abidjan, Côte d’Ivoire, marking a further step in its expansion strategy across West Africa.Announcing the development, the company stated that the new office in Abidjan serves as a commercial hub for Francophone West Africa, offering strong logistics links, access to regional markets, and proximity to key customers across Côte d’Ivoire, Ghana, Burkina Faso, Mali, and Senegal.“We’re proud to announce the opening of our new regional office in Abidjan, strengthening our presence and long-term commitment to the region.”

SCE said the decision to establish a physical presence in the region is intended to improve customer engagement and technical responsiveness.According to the company, for sectors such as grains handling, storage, milling, and food processing, local technical support is increasingly critical as operators invest in modern facilities to reduce post-harvest

INVESTMENTS

losses, improve food safety, and meet stricter quality standards. West Africa remains one of the world’s most dynamic agricultural regions, with cereals such as maize, rice, sorghum, and wheat playing a central role in food security. According to FAO data, post-harvest losses for grains in parts of subSaharan Africa can reach 15–20%, largely due to inadequate storage and handling infrastructure. This has driven growing interest in engineered storage buildings, processing facilities, and integrated solutions that can operate reliably in tropical climates.

Alongside the office opening, SCE announced a key leadership appointment, naming Nahoua Soro as Area Sales Manager for West Africa.With over 10 years of experience in the region and a strong technical and commercial background, Nahoua will deliver excellent insight and support to our customers in the region. The appointment is expected to strengthen SCE’s market intelligence and project execution capabilities, particularly for customers planning new builds or expansions.

AGRIMAC, Sudan’s Rotana Flour Mill partner to boost milling capacity

SUDAN – AGRIMAC Makina Limited (AGRIMAC), a Turkish grain processing and milling technology provider, and Sudan’s Rotana Flour Mills have formalised a contract for a turnkey flour milling project that will increase Rotana Group’s total milling capacity from 2,800 tonnes per day (TPD) to 4,800 TPD. According to the contract, the deal also includes the construction of 90,000 tonnes of steel silo storage, supporting integrated grain handling and long-term operational continuity for one of Sudan’s key flour producers. The enhanced capacity will not only support domestic demand but also strengthen Sudan’s milling industry’s ability to respond to regional flour demand.

The signing ceremony, held on January 3, reinforces the strategic relationship between AGRIMAC and Sudan’s private milling sector. Under the agreement, AGRIMAC will engineer, procure, and install two new 1,000 TPD milling lines with associated storage and handling systems. Rotana Flour Mills, established in April 2014, plays a pivotal role in Sudan’s wheat milling sector and broader food supply infrastructure. Once commissioned, these additions will raise Rotana Group’s installed capacity by more than 70 percent, significantly enhancing its ability to meet domestic demand and strengthen supply chain resilience.

AGRIMAC has expanded its global grain-processing footprint beyond this project. The deal reflects a trend in the Middle East and Africa toward modernising milling operations

with technology-driven, high-capacity plants.Recently, the company commissioned a 600 TPD semolina production facility in Mardin, Türkiye, supporting downstream wheat processing sectors such as pasta and couscous production. AGRIMAC’s portfolio includes engineering services for flour, semolina, feed mills, silo systems, and port handling equipment, signalling its capability to deliver complex and large-scale agribusiness infrastructure projects.

PRE-EVENT REVIEW

Lusaka prepares to host Southern Africa’s leading agri-food, logistics, hospitality and agriculture industries

On May 13-15, 2026, all roads lead to Lusaka, Zambia

For three days, Zambia’s capital will be a meeting point for the region’s most influential players in the grain, milling, and feed industries, alongside the wider agri-food ecosystem. AFMASS Trade Expo Zambia & Southern Africa 2026, powered by Andritz Feed & Biofuel, will take centre stage at the Radisson Blu Hotel, bringing together innovation, insight, and opportunity under one roof.

Buhler Group, one of the leaders in the grain milling and processing industries in Africa, will also feature prominently as Technical Session Sponsor.

Now in its third edition in Zambia, the event has rapidly evolved into one of the most important trade platforms in Southern Africa. For millers,

feed manufacturers, hospitality and agribusiness professionals, it offers something increasingly rare in today’s fast-moving industry: direct access to the technologies, partnerships, and ideas shaping the future of food and related industries across the region.

A TIMELY PLATFORM FOR A GROWING INDUSTRY

Southern Africa’s agrifood and related industries are expanding steadily, driven by rising demand for processed foods and animal protein, as well as for efficient storage, processing and packaging systems. As businesses scale and competition intensifies, the need for smarter, more efficient, and more sustainable operations has never been greater.

The AFMASS Trade Expo arrives at this critical moment, providing a platform not just to

observe change but to engage with it actively.

Across the exhibition floor, visitors will encounter a comprehensive showcase of solutions spanning the entire Agri-food and related value chain.

From advanced grain storage systems and silos to modern milling equipment and feed processing technologies, to ingredients, packaging and other supply chain solutions, the expo is designed to address the everyday operational challenges faced by processors of all sizes.

Bulk material handling systems, food formulation, packaging, logistics, quality control technologies, and digital tools for plant optimisation will further highlight the industry’s shift toward automation and precision.

Leading global and regional players, including Andritz Feed & Biofuel and a wide range of equipment manufacturers, ingredient suppliers, and service providers, will be present, offering practical solutions and technical expertise tailored to the realities of African markets.

Some of the household names that will grace the exhibition

floor include Altinbilek Nilpeter, IFF, Pakmaya, Sefar, and Cift Kartal, among others.

Over the three days, Lusaka will host a diverse and influential audience, including business owners, plant managers, technical experts, procurement specialists, and policymakers.

Delegations are expected from across the SADC region, Zimbabwe, Botswana, South Africa, Namibia, Angola, the Democratic Republic of Congo, Malawi, Mozambique, and beyond, making the expo a true regional hub for business exchange.

INSIGHTS, INNOVATION AND STRATEGIC CONNECTIONS

Complementing the exhibition is a carefully curated twoday conference programme, supported by Andritz Feed and Biofuel and Bühler. The sessions are designed to reflect the industry's most pressing priorities, balancing strategic vision with practical application.

The programme opens with a high-level CEO and industry leadership roundtable, setting the tone with discussions on investment trends and market dynamics across the food, milling, and feed sectors. From there, technical sessions dive into key areas such as grain storage and milling innovations, advancements in animal feed processing, and emerging trends in food and beverage manufacturing.

On the second day, the conversation broadens to address the region’s protein gap, evolving regulatory frameworks, and the growing importance of food safety and quality standards. It will end with a high-level cocktail, bringing industry leaders together to network and connect further, away from the expo and the conference

Logistics and cold chain infrastructure, critical enablers of regional and international trade, will also take centre stage, alongside entrepreneurship-focused sessions offering realworld insights from industry players.

On the final day, the momentum continues with a dedicated Customer Day hosted by Andritz Feed & Biofuel, offering invited participants deeper engagement through focused sessions and discussions.

The Expo Hall will remain open on the last day and will continue welcoming attendees who shall engage directly with exhibitors or have one-to-one meetings to close deals and discuss future opportunities.

The day will conclude with the exclusive Andritz Networking Cocktail, bringing together selected industry executives for high-level interactions and relationship-building, even as the wider expo floor remains open for continued meetings and business exchanges.

As Zambia continues to strengthen its position as a regional hub for commerce and industry, the AFMASS Trade Expo stands out as a must-attend event for those looking to stay competitive, build partnerships, and unlock new avenues for growth.

In a region full of potential, Lusaka is where the next chapter begins. MMEA

Flour Mills Data Driven

Redefining Efficiency and Competitive Performance

NBY MARTHA KURIA

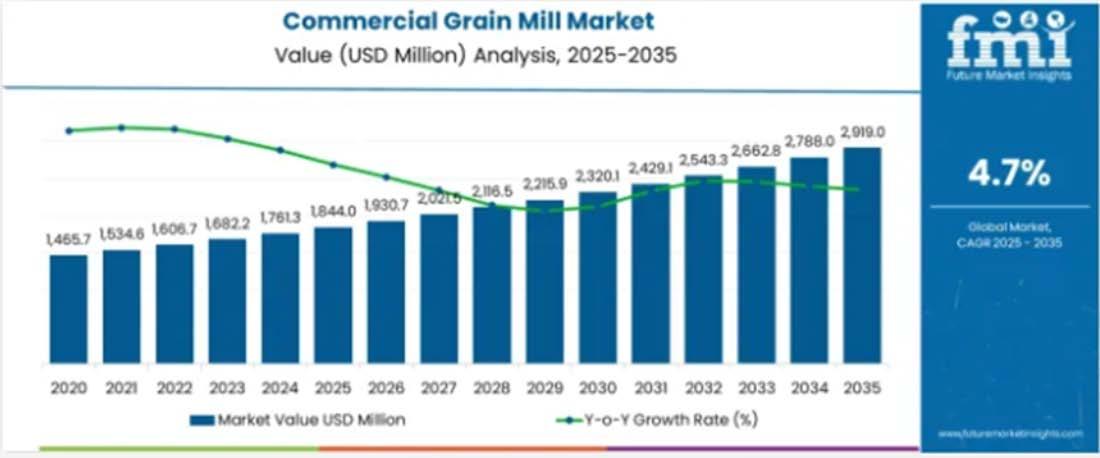

ot long ago, the performance of a flour mill depended largely on mechanical reliability and the experience of its head miller. Adjustments to roll gaps, feed rates and tempering moisture were guided by skill, observation and laboratory results that often arrived hours later. Today, that operating model is steadily giving way to something more interconnected. The flour milling industry is entering a phase where performance is no longer defined solely by mechanical precision. Instead, it is increasingly determined by how effectively mills capture, interpret and act upon operational data. Globally, millers are investing in digital integration not as a luxury but as a structural requirement to maintain extraction rates, reduce energy intensity, and meet tighter food safety regulations. According to Future Market Insights, the commercial grain mill market is projected

to reach USD 2919.0 million by 2035,driven by increasing demand for flour production, feed processing, and specialty grain products that require precise particle size control and contamination-free processing environments. The ability of flour mills to support bulk processing with efficiency and cost effectiveness has further reinforced their adoption. According to industry data, modern milling technologies can increase flour extraction rates from wheat while reducing energy consumption by 25-30%.

CENTRALIZED DATA PLATFORMS: MOVING BEYOND CONVENTIONAL AUTOMATION

For many milling operations, automation once meant installing PLCs and linking them to a SCADA (Supervisory Control and Data Acquisition) screen in the control room. Operators could see alarms, start and stop machines, and monitor throughput. It was a major step forward at the time. But today’s competitive flour, feed and grain markets require more than visibility. They require intelligence. The shift is now clearly toward centralised data platforms that bring together every signal from the plant floor, from intake to packaging, and convert it into actionable insight. Leading technology suppliers are embedding this capability directly into their equipment and digital ecosystems.

At Bühler Group, the transition is visible through its Mercury MES and Bühler Insights platforms. These systems aggregate data from roller mills, purifiers, sifters and sensors into

unified dashboards that track yield, energy use, downtime and quality deviations in real time. Combined with its SmartMill concept, temperature, vibration and energy data are continuously analysed to enable predictive maintenance and autonomous process adjustments. A similar integration approach is seen at Andritz AG through Metris Plant Insights. By building digital twins of processing lines, Andritz enables millers to simulate process changes before implementation. Machine learning tools detect anomalies early, reducing unplanned shutdowns and stabilizing production.

Turkish supplier Alapala combines its roller mills and plansifters with plant-wide automation systems that link cleaning, milling and packaging under a single control architecture. This ensures recipe management, traceability and KPI tracking operate seamlessly across departments.The same technology has been reported from Omas and IMAS, which have high-efficiency grinding systems equipped with real-time control sensors that optimise energy and extraction rates. Meanwhile, Henry Simon Milling integrates advanced sensor packages within its roller mills to capture grinding temperature, roll gap and load data, feeding centralized monitoring systems focused on consistent flour quality.

Asian manufacturers such as Pingle Group and Haiyun Grain Machinery are also embedding PLC-based controls with digital interfaces in roller mills, purifiers and cleaning systems, allowing easier integration into centralized dashboards. Such systems also calculate Overall Equipment SOURCE: FUTURE MARKET INSIGHTS

AS MILLS CONNECT MACHINERY TO CLOUD DASHBOARDS AND REMOTE DIAGNOSTICS, OPERATIONAL TECHNOLOGY BECOMES VULNERABLE TO DIGITAL INTRUSION

Effectiveness (OEE), combining availability, performance and quality metrics into a single measurable indicator. For mills operating at 400 to 600 tonnes per day, even a one percent improvement in OEE can translate into significant annual production gains.

INTELLIGENT GRINDING SYSTEMS: PRECISION AT THE CORE

Grinding remains the heart of flour milling, and digital integration is redefining how roller mills operate. Modern systems incorporate sensors that monitor roller surface temperature, vibration amplitude and bearing conditions. Automatic roll gap adjustment ensures stable grinding pressure even when wheat hardness varies.

Omas Industries has advanced this approach with its Leonardo roller mill, featuring direct-drive motors that eliminate traditional belt systems. Operating speeds are electronically controlled, reducing energy losses and enabling precise differential adjustments. The absence of belts reduces maintenance intervals and improves energy efficiency. Installed in several European and African mills, Leonardo systems report lower power consumption per tonne compared to conventional belt-driven mills.

Meanwhile, Satake Corporation integrates sensor-based monitoring within its grinding and sorting lines. Although widely recognized for rice technology, Satake’s flour milling installations incorporate real-time moisture measurement and impurity detection systems that feed data back into plant control software.

OPTICAL SORTING AND AI-BASED GRAIN CLEANING

Downtime in the grain industry is costly. Improving reliability and enhancing safety with predictive maintenance supports operations and profitability. Accurate measurement of material flow and weights optimizes processes, reduces waste and promotes productivity. Before wheat reaches the roller mill, digital intelligence is already shaping quality control. Optical sorters now use multi-spectral cameras and artificial intelligence to detect foreign material and defective kernels.

Bühler’s SORTEX H SpectraVision system captures high-

resolution imagery across multiple wavelengths, enabling precise rejection of ergot, fusarium-damaged kernels and foreign grains. These machines operate at high throughput while logging rejection rates and defect categories into centralized dashboards. The data can be analyzed to identify supplier trends or seasonal quality fluctuations. Satake’s optical sorting systems employ infrared and color imaging to detect impurities invisible to the human eye. In export-focused mills, such precision enhances compliance with international maximum residue limits and food safety standards.

In grain handling and storage, Ag Growth International integrates temperature cables, aeration controls and drying systems into digital monitoring networks that protect grain quality throughout storage cycles. Similarly, Cimbria connects its SEA.IQ optical sorters and silo monitoring systems to automation platforms that continuously track raw material condition and cleaning efficiency. Operationally, these systems process several tonnes per hour depending on configuration, with rapid data refresh rates that allow continuous adjustment without halting production.

“The grain storage industry is on the cusp of an intelligent revolution,” said Martino Celeghini, chief executive officer of CESCO. “Artificial intelligence is rapidly transforming how facilities operate, optimizing processes, maximizing efficiency and safeguarding grain quality. From predictive maintenance to automated quality assessment, AI is poised to significantly enhance every step of the grain storage cycle.”

NEAR-INFRARED (NIR) ANALYSIS: REAL-TIME QUALITY CONTROL

Laboratory analysis traditionally delayed corrective action. In modern milling operations, manufacturers are investing in energy-efficient designs, digital control systems, and hygienic milling solutions to align with food safety regulations and sustainable production practices.

With embedded NIR sensors, mills now measure moisture, protein and ash content directly in the production line. Data feeds automatically into blending and tempering control systems. For example, automated tempering adjusts water addition based on live moisture readings, ensuring consistent conditioning before grinding. If protein levels fluctuate, blending strategies can be modified instantly to maintain flour specification.

While MES platforms provide analytics, the foundation remains robust PLC and SCADA infrastructure. Modern SCADA systems allow centralized visualization of thousands of data points, including motor currents, bearing temperatures and pneumatic pressures. Deviations trigger alerts before mechanical failure occurs. An example is Alapala supplied Pioneer Foods in Durban, South Africa, with an automated system combining SCADA control, NIR quality analysis and traceability modules. The digital architecture generates detailed batch records, supporting food safety compliance and export requirements. For mills serving multinational bakery clients, traceability is increasingly a contractual necessity.

Beyond in-process detection during flour milling, rheological devices such as farinographs and alveographs have been designed to generate performance data that can be uploaded into MES platforms. Such integration reduces reliance on postproduction corrections and minimizes out-of-spec batches. In large-scale operations, this translates into lower rework volumes and reduced quality-related waste.

NAVIGATING STRUCTURAL CHALLENGES IN DIGITAL MILLING

As digital technologies become embedded across flour milling operations, the industry faces a pivotal transition. While the operational benefits are increasingly measurable, improved extraction stability, reduced downtime, optimized energy use and enhanced traceability, the pathway to full digital maturity remains complex. The sector must now balance capital investment, workforce capability and cybersecurity risks against the promise of higher productivity and stronger margins.

One of the primary challenges is capital intensity. Advanced MES platforms, AI-enabled optical sorters, sensorrich roller mills and integrated SCADA architectures require significant upfront investment. For mid-sized millers operating in cost-sensitive markets, return on investment must be clearly quantified. Energy savings of 10–15%, extraction improvements of 0.5–1.5%, and reductions in unplanned stoppages are compelling, but they demand disciplined data utilization to

convert technical capability into financial performance.

Integration complexity presents another barrier. Many mills in Africa and emerging markets operate hybrid environments where legacy mechanical equipment coexists with modern digital systems. Retrofitting older lines to communicate with new platforms is not always straightforward. Compatibility between PLC brands, data protocols and cloud systems requires structured planning and skilled engineering support. Suppliers such as Bühler Group, Alapala, Omas Industries and İmaş Makina Sanayi A.Ş. increasingly emphasize modular upgrades to address this reality, yet execution remains site-specific.

Cybersecurity is emerging as a strategic concern. As mills connect machinery to cloud dashboards and remote diagnostics, operational technology becomes vulnerable to digital intrusion. A disruption in plant control systems could halt production or compromise quality assurance data. Consequently, secure network architecture and controlled remote access protocols are becoming as critical as mechanical reliability.

Workforce readiness also defines the pace of adoption. Digital dashboards and predictive maintenance alerts are only effective when operators and plant managers can interpret and act upon them. The transition from mechanical troubleshooting to data-based decision-making requires continuous training. Without this capability, digital tools risk being underutilized. Despite these challenges, the trajectory of the digital milling industry is clear. Over the next decade, several structural shifts are likely to shape its evolution.

DON’T RUSH THE PROCESS

Why Discipline Still Defines Great Milling Technologists

BY MARTHA KURIA

Across Africa, flour millers are navigating a complex operating environment shaped by high energy costs, volatile wheat import prices, infrastructure constraints, and growing regulatory and consumer expectations around food safety and sustainability. In this executive interview, Milling Middle East & Africa Magazine speaks with Michael Ndukwe, Shift Head Miller at Niger Mills Company, a division of Flour Mills of Nigeria, who shares a comprehensive perspective on the flour milling industry across Africa. With more than 12 years of professional experience, Ndukwe gives a grounded, operations-driven account of the realities of modern milling, offering insights into plant efficiency, food safety systems, workforce development, and the technological and sustainability shifts reshaping the sector.

MMEA: Can you briefly introduce yourself and provide an overview of your experience in the flour milling industry?

I am Ndukwe Michael Scott, a Shift Head Miller at Niger Mills Company, a division of Flour Mills of Nigeria. I am a seasoned professional miller with over 12 years of experience in

the industry, and I have developed the skills and expertise necessary to contribute meaningfully to team and organizational success. Throughout my career, I have gained extensive experience across all aspects of the flour milling industry, including automation, food safety systems, hygiene practices, and process control. My responsibilities have covered staff supervision, inventory management, cost analysis, and customer service. I am a strong communicator and leader with a proven ability to motivate teams to achieve both departmental and organizational goals. I also have a solid track record of improving profitability through effective cost management and reduced downtime, while remaining committed to delivering high professional milling standards.

MMEA: What initially drew you to the field of flour milling, and how did you develop your expertise?

I started my career in Engineering Department, initially I never intended nor imagined to be a Flour Miller, nor do I know what it takes to be a Miller, but I was involved in the Erection and Installation of Our C-Mill year 2007 – 2008.

Michael Ndukwe - Shift Head Miller, Niger Mills Company.

(500 metric tons per 24 hours Mill) from the installation of Steel Silos and Cat-Walks to installation of Building Structures, Steel Columns, Concrete of the floors and finally the installation of All Buhler Milling machines. In the Technical Department as a Mechanical Fitter, during the installation work, I wanted to know more how those machines works, I later developed passion and interest to be a professional miller, oppourtunity now presented itself while i was still in the technical department, an opening to be trained as a qualified personnel in the art-offlour-milling, the trade. (the magic of processing raw wheat into good consumable flour used for various purposes such as Bread, Biscuit, Noodles etc.) Examination and interviews was set, I passed internal prerequisite examinations that qualified me to work as a Mill Assistant. From there, I pursued further professional studies and advanced training, including programmes such as NABIM, which enabled me to progress to Assistant Miller and subsequently to Shift Miller.

MMEA:What would you consider the most significant achievement of your career in flour milling?

My most significant achievement is the daily responsibility of ensuring the production of safe wheat flour, semolina, and whole wheat meal that consistently meet statutory, regulatory, and mutually agreed customer food safety requirements. This includes implementing and continuously improving an effective quality and food safety management system that supports a long-term food safety culture across operations.

MMEA: In your current role, how do you ensure smooth and efficient milling operations?

Efficient operations begin with disciplined execution across the entire production chain, including wheat intake operations, correct storage practices, raw material cleaning, gristing, tempering and conditioning, milling, finished product storage, and product blending to meet customer specifications. I also validate the effectiveness of the food safety management system through internal and external audits and inspections. Any deficiencies identified are addressed promptly, with lessons applied to improve processes and strengthen food safety competencies. Risk-based controls aligned with our operating context are applied to achieve food safety objectives and drive continuous improvement.

MMEA: How do you motivate and equip your production team to achieve operational excellence?

I prioritize regular communication with every team member to effectively manage food safety risks associated with changes in products, processes, and technologies. This approach promotes continuous improvement, accountability, and alignment with operational objectives.

MMEA: You recently graduated from the African Milling School. What does that training mean for your career?

The programme provided hands-on exposure within milling facilities alongside structured classroom discussions, helping me develop a deeper conceptual understanding of the milling process. The training focused on mill balance, identification of critical control points, and the milling of different wheat classes. It enhanced my understanding of how raw materials and milling systems influence cleaning, conditioning, milling, and finished product quality, while reinforcing the critical role employees play in controlling and optimizing the process.

MMEA: What is the biggest challenge facing the flour milling industry in Nigeria and Africa today, and how is it being addressed?

One of the most significant challenges is the high cost of energy and operations. Consistent energy supply is essential for continuous milling operations, yet high electricity costs place heavy pressure on manufacturers, particularly in the milling and baking sectors. Currency fluctuations and foreign exchange scarcity also significantly impact the cost of importing wheat, which remains the primary raw material for most African millers. In addition, infrastructure and logistics challenges, especially poor road networks around major ports such as Apapa in Nigeria, increase transportation costs and disrupt supply chains.

To address these challenges, companies are pursuing mergers and acquisitions to streamline operations and improve efficiency, such as Flour Mills of Nigeria’s acquisition of Honeywell. Others are diversifying wheat import origins to more cost-effective markets and investing in local wheat value chain development. Increased private-sector investment in logistics and vertical integration into farming is also gaining momentum. A notable example is the Grain

Processing and Innovation Center launched in Kano in July 2024 through collaboration between Bühler and Flour Mills of Nigeria.

MMEA:What emerging trends or innovations are shaping the flour milling industry?

Key innovations include the integration of artificial intelligence and the Internet of Things for predictive maintenance, which plays a critical role in reducing operational costs. There is also a strong focus on energy efficiency to support net-zero goals, alongside product diversification into alternative grains, specialty flours, and fortified flour products.

MMEA: How does Africa compare with the rest of the world in terms of industry advancement?

In contrast to developed markets such as Europe and North America, which focus on incremental efficiency gains, Africa is expanding production capacity rapidly to meet growing demand for staple foods. The continent is also experiencing accelerated modernization, with increased investment in industrial milling and the adoption of modern, high-capacity machinery supplied by international manufacturers.

MMEA: How do you envision the future of flour milling amid technological and consumer changes?

Food safety and sustainability will become core competencies for the industry. Mills are increasingly adopting renewable energy solutions such as solar power and investing in compact, high-efficiency machinery capable of reducing energy consumption by up to 30%. Circular economy practices will expand, with by-products such as bran repurposed for bioenergy or high-value food ingredients. Traceability will also become more critical, as consumers demand transparency regarding food origins, supported by blockchain technology and advanced data management systems. The future belongs to producers who combine high-capacity automated production with flexibility to meet niche and health-focused consumer demands.

MMEA: How can the industry contribute to addressing climate change?

The industry can significantly reduce its environmental impact by transitioning to renewable energy sources, adopting electric vehicle fleets, and implementing closed-loop systems to minimize waste. Increased use of recyclable and biodegradable

materials and extended product life cycles will further reduce environmental pressure and emissions.

MMEA:Have you experienced setbacks that provided valuable lessons?

Yes, as a professional, I have encountered situations where flour did not meet customer specifications, such as incorrect ash content, poor granulation, or unacceptable color, resulting in rejected loads. These experiences highlighted the importance of strict raw material intake controls, proper wheat tempering, and frequent monitoring of roller mills. Addressing such challenges reinforces the value of robust quality control systems and often leads to stronger, more automated quality assurance processes.

MMEA: How do you envision the future of your career, and what challenges do you foresee?

As the industry evolves, several structural and operational challenges are likely to shape both my career path and the broader flour milling landscape. One of the most pressing issues is the skilled labour gap. There is a growing shortage of qualified professionals capable of operating, maintaining, and troubleshooting advanced, automated milling machinery. As mills increasingly adopt digital and high-capacity systems, the demand for technically competent personnel continues to outpace supply.

Another major challenge is energy and raw material volatility. Rising energy costs, where milling activities account

for approximately 75% of a mill’s total energy consumption, combined with volatile wheat prices driven by climate change, place sustained pressure on operational profitability and cost management.

Cybersecurity risks are also emerging as a critical concern. As mills become more connected and increasingly reliant on remote monitoring, automation, and data-driven decisionmaking, they face heightened exposure to cyberattacks. This shift requires not only technological investment but also knowledge and awareness of industrial data security and system protection.

Finally, there remains resistance to technological change in many regions. A significant portion of the industry still operates with traditional, aging machinery. Transitioning to digital and automated systems demands substantial capital investment, as well as a shift in mindset, particularly among long-serving workers accustomed to conventional milling methods.

MMEA: What advice would you give aspiring flour milling professionals?

My advice is to have role models. You will always learn something valuable from people who have walked the path before you. In my own journey, I have been influenced by professionals such as Engr. Chris Leicester, Mr. Edgar Stewart, my General Manager Mr. Gregory Ehimen, Mr. Samuel Olisa, Mr. Sudhakar Padmaraju, and Dr. Osy Michael. These individuals have helped shape my focus, resilience, dedication, and professional principles. In many ways, their guidance serves as a reference guide, though it is important to remember that no one is perfect, as we all have individual strengths and weaknesses.

Milling, much like the transformation of raw wheat into quality flour, happens in stages. Do not rush the process, and do not take shortcuts, shortcuts will always show, somewhere and somehow. Respect the process. Follow established protocols, continuously improve your knowledge and skills, and remain adaptable. Ask questions and ensure you receive satisfactory answers. If you do not, ask someone else. Growth in milling is built on patience, discipline, and continuous learning.

MMEA: Do you have any final insights on animal feed milling?

Animal feed milling places strong emphasis on safety and quality control, with digital traceability and rapid mycotoxin testing increasingly replacing long laboratory turnaround times. Operational challenges include steam and moisture management, pellet quality control, and raw material volatility, particularly in markets such as Nigeria. Energy consumption remains a major concern, with pellet mills accounting for about 50% of total feed mill energy use, driving demand for energy-efficient equipment. There is also growing interest in alternative protein sources, including insect protein, microbial proteins, and upcycled food waste, as the industry seeks sustainable solutions. MMEA

TUNISIA

Balancing Cereal Recovery with Structural Import Dependence

BY MARTHA KURIA

Tunisia, situated along the Mediterranean coast with Algeria to the west and Libya to the southeast, is home to nearly 13 million people. Agriculture plays a central role in the country’s economy, contributing approximately 10–14% of GDP and employing 13–16% of the workforce. Predominantly composed of smallholder farms, 62% of which occupy less than 10 hectares, the agricultural sector focuses on olive oil, dates, and cereal production. While Tunisia is globally recognized as a top olive oil producer, its wheat and barley production remains crucial to the domestic milling sector.

CEREAL PRODUCTION RECOVERS AFTER FAVORABLE RAINS

Cereal production in Tunisia is dominated by durum wheat, soft wheat, and barley, and is highly sensitive to annual climate fluctuations. The sector, however, faces significant constraints due to drought conditions that affect crop yields, water availability, and food security. The country experienced three consecutive years of drought, causing reservoir levels to fall to 25% of capacity and requiring water rationing by authorities. Grain harvests decreased by 60%, with domestic production falling to 250,000 metric tons. However, improved winter rainfall has significantly influenced production prospects. For marketing year (MY) 2025/26, Tunisian authorities forecast wheat output at 1.35 million metric tons (MMT) and barley at 500,000 metric tons (MT), reflecting increases of approximately 14% and 80%, respectively, over the previous year.

Durum wheat, essential for semolina and pasta production, is cultivated extensively in central and southern regions, while soft wheat is primarily used for bread. Despite ongoing government programs, Tunisia continues to rely on imports to meet domestic demand.

Wheat remains Tunisia’s most strategic grain commodity. Production for MY 2025/26 is projected at 1.35 MMT, covering only about 45% of domestic needs. National consumption is expected to reach 2.99 MMT, up from 2.885 MMT in MY 2024/25, reflecting annual population growth of approximately 2%. Per capita wheat consumption stands at an estimated 236 kg, among the highest in North Africa. To close the supply gap, Tunisia is forecast to import approximately 1.7–2.0 MMT of wheat in MY 2025/26, equivalent to nearly

55% of total demand.

In 2023, the government introduced a strategy aimed at achieving greater wheat selfsufficiency by expanding durum wheat acreage to 800,000 hectares and strengthening extension services. The program targeted 1.05 MMT of grain output, including 945,000 metric tons of durum wheat. However, structural constraints and climatic volatility have limited progress toward full independence.

The Office des Céréales (ODC), Tunisia’s state grain agency, plays a pivotal role in securing wheat imports. By the end of 2025, ODC awarded tenders for 125,000 MT of soft wheat to companies including Soufflet (France), Finagrit (Italy), Buildcom (Bulgaria), and Louis Dreyfus (Netherlands), at an average price of US$256.84 per ton. Durum wheat tenders totaling 100,000 MT were awarded to Casillo, a leading Italian processor, and UAE-based Amber Grains, at an average price of US$319.69 per ton.

A tender held on January 28, 2026, by ODC sought 100,000 MT each of soft and durum wheat for early 2026 delivery, reflecting continued import activity. USDA projections indicate domestic wheat consumption for MY 2025/26 will reach 2.99 MMT, up from 2.885 MMT the previous year, driven by population growth of approximately 2% and per capita consumption of 236 kg. With domestic production meeting only 45% of demand, Tunisia remains reliant on imports for roughly 55% of its wheat needs.

The wheat subsidy program ensures the affordability of flour, semolina, and bread, with the government covering price differentials. While the program strains the national budget, it remains a cornerstone of Tunisia’s food security policy. According to USDA data, the Cereal Board maintains exclusive control over wheat importation and distribution, including all domestic tenders.

BARLEY: EXPANDING ROLE IN FEED AND BREWING

Barley, while a secondary cereal crop, plays a vital role in Tunisia’s livestock feed sector and brewing industry. Marketing Year 2025–26 forecasts indicate barley consumption will reach 940,000 MT, reflecting steady annual growth of about 2%. Barley production increased to 412,000 hectares from 395,000 hectares in MY 2024–25. The crop primarily supports feedlots and supplemental feeding for livestock in regions with stressed rangelands.

The brewing industry has further driven

demand, with imports rising sharply to 1.43 MMT in 2023, nearly doubling the 0.71 MMT imported in 2022. Tunisia has liberalized barley imports, moving from a state-controlled monopoly under ODC to private sector participation. This aligns with recommendations from international institutions, reduces government expenditure, and encourages market efficiency.

STORAGE AND LOGISTICS: STRUCTURAL BOTTLENECKS PERSIST

Tunisia’s cereal supply chain faces critical infrastructure constraints. Storage capacity is insufficient, with the silo network accommodating only 508,000 MT—short by approximately 300,000 MT, forcing reliance on open-air storage, which increases aflatoxin contamination risks. Post-harvest losses range from 10–15%, reducing farmer income and heightening import dependence. Farmers in interior regions often transport grain over 150 km on poor-quality roads to reach certified storage facilities, adding significant costs.

To address these gaps, the government plans to invest US$66 million (205 million dinars) in new silo construction by 2027, increasing storage capacity by 24% to 628,000 MT. New facilities will be strategically located in Rades (40,000 MT), Sousse (58,000 MT), and Sfax (38,000 MT). Additionally, US$45 million (143 million dinars) will renovate existing silos, modernizing 206,000 MT of capacity. A further US$1.9 million

THE MILLING INDUSTRY IS HIGHLY REGULATED, PRIVATE MILLS OPERATES UNDER GOV'T

OVERSIGHT

(6 million dinars) investment will digitize grain collection processes, enhancing efficiency and transparency across 200 collection centers.

Resolving these storage and logistics constraints could reduce wheat import volumes by 7–10%, according to World Bank analysis, improving overall sector resilience. Despite these investments, Tunisia imported 4.1 MMT of cereals in 2024, with soft wheat accounting for 36.5% of those imports, highlighting its ongoing dependence on foreign supplies.

THE MILLING SECTOR

IN NUMBERS 24%

PERCENTILE BOOST OF STORAGE CAPACITY BY 2027

The milling industry covers 2 main activities particularly, flour milling and semolina production. The country’s milling industry is highly regulated, with private mills operating under government oversight. Wheat and barley account for 87–88% of grain processed. Production targets the local market, supplying subsidized flour for bread and semolina for couscous and pasta. While the state controls imports and distribution via the Cereal Board, over 50% of wheat flows through private industrial mills that process it under organized channels.

According to the ODC website, mills are concentrated near coastal urban centres like Tunis, Sousse, and Sfax, where infrastructure supports large-scale production and distribution, representing nearly 80% of the national crushing capacity. Leading players include Les Grands Moulins du Cap Bon (GMC SARL), part of the La Rose Blanche Group, GMC ranks third in durum wheat milling and eighth in bread wheat milling. It produces flour and semolina under the "EL KHOMSA" brand. M.C.S.R (Central and Sahel United Mills): Also part of the Rose Blanche Group, M.C.S.R operates modern facilities capable of milling 900 tons/day of durum wheat and 450 tons/day of soft wheat, dominating domestic markets. Other notable mills include Les Grands Moulins de Tunis, Mezzouna Mills, and Société Tunisienne des Grands Moulins, which focus on flour for industrial bakeries, couscous, and pasta production. Milling operations leverage modern roller and stone milling technologies, though integration with digital inventory and quality control systems remains limited.

In Tunisia, livestock feed units (LFUs) fall under the private sector. According to ODC, any natural or legal person is authorised to operate in this field according to the conditions of the technical specifications for the manufacture of livestock feed. The majority of livestock feed units are located around large urban areas as well as in governorates known for the importance of animal husbandry activity such as the northwest and the central west.

POLICY AND MARKET DYNAMICS

Tunisia faces a complex set of challenges and opportunities in its cereal and milling sectors. Climatic variability, insufficient storage, and transportation bottlenecks are key constraints that heighten import dependency. Government policy heavily influences the grain and milling sectors. Subsidy programs for wheat and flour ensure food affordability but impose fiscal pressure. International institutions, including the World Bank and FAO, have advised gradual liberalization, infrastructure investment, and digitalization to improve efficiency and reduce dependence on imports.

Tunisia’s cereal market is transitioning toward private sector participation, particularly in barley imports, while the state maintains oversight of wheat to guarantee strategic food security. Price fluctuations, climatic variability, and reliance on imports continue to create market volatility, affecting both producers and consumers. MMEA

JULY 15-17, 2026

SARIT EXPO CENTRE, NAIROBI, KENYA

SEPTEMBER 15-17, 2026

LAGOS, NIGERIA

How will African Mills Meet Rising Demand & Rising Standards?

Africa’s Milling: Smarter, Efficient, Digital, Ready For The Next Industrial Era.

BY OMAS INDUSTRIES

In 2026, Africa’s milling industry is entering a decisive phase. For years, growth was measured primarily in installed capacity. New plants, expanded lines and increased throughput defined progress. Today, the conversation has shifted. Capacity alone is no longer enough. Across West, East and Southern Africa, millers are asking a different question: how do we convert growth into long-term competitiveness?

With urban populations expanding rapidly and wheat-based consumption steadily rising, the sector stands at the intersection of food security, industrial policy and private investment. The opportunity is significant. So is the responsibility.

Discover how tailored engineering solutions can make this transition smoother: explore Omas’ approach today.

Omas Machinery equipment at Foodtec / Naval Group, a milling plant in Luanda, Angola, dedicated to the production of bakery flour and semolina for pasta.

Omas rollermills in operation at Foodtec, ensuring high-efficiency grinding and consistent flour quality.

A STRATEGIC INDUSTRY IN A CHANGING GLOBAL CONTEXT

Several African nations remain among the world’s leading wheat importers, linking local food systems directly to global grain markets. Price volatility in recent years has highlighted how exposed margins can be to international dynamics. At the same time, governments across the continent are reinforcing policies that support local value addition and agro-industrial development. Milling sits at the center of this strategy: it connects global raw material flows to domestic food supply and industrial employment. In this environment, performance is not just a private concern, it is a structural priority. Learn how Omas supports mills in navigating global market challenges: contact experts for insights.

WHERE MARGINS ARE WON, AND LOST

In today’s market conditions, small technical differences produce significant financial consequences. A marginal increase in extraction rate can translate into thousands of additional tons of sellable flour over the course of a year. A reduction in energy consumption per ton processed directly

improves cost structure resilience. Improved process stability reduces downtime and protects customer relationships. Competitiveness is increasingly built inside the mill, in mechanical efficiency, in digital precision, in process control. This is where technology makes the difference.

See how African mills are achieving measurable gains with Omas technology: request a consultation.

ENGINEERING FOR MEASURABLE IMPACT

At Oma Industries, an Italian company with over 40 years of experience designing and manufacturing milling machinery, development has focused on the variables that matter most to millers operating in dynamic markets:

• Maximizing yield through precise grinding control

• Reducing energy dispersion via direct-drive systems

• Improving reliability with simplified mechanical design

• Integrating intelligent automation for real-time supervision

Omas rollermill technology eliminates unnecessary transmission losses, while the automation platforms transform operational data into actionable insights. Omas plant designs are conceived to balance performance, scalability and long-

Omas Flour Extraction Booster at Foodtec, designed to maximize yield and improve efficiency while maintaining consistent flour quality.

term efficiency. The objective is simple: measurable industrial performance. Not theoretical innovation, but tangible economic results.

Explore Omas solutions: find the system that fits your plant’s specific needs.

AFRICA’S MILLS: GROWTH, INNOVATION AND THE NEED FOR PARTNERSHIP

While expansion continues, African mills face a unique set of challenges: fluctuating wheat quality, energy variability and operational pressure to meet both consumer expectations and industrial standards. In this environment, having a trusted technological partner is crucial. Omas works with African mills not just to supply machinery, but to engineer solutions tailored to local conditions. From upgrading aging plants to designing entirely new lines, Omas integrates advanced rollermills, precision sifters and digital control systems that give operators real-time insight into production parameters: turning data into actionable decisions. For example, in several recent projects across West and East Africa, Omas solutions allowed mills to increase extraction efficiency by 2–3%, reduce energy consumption per ton by over 10%, and cut unplanned downtime through predictive maintenance programs. These improvements directly translate into higher margins, consistent quality and competitive advantage, without requiring radical operational changes.

Learn how your mill can gain a competitive edge: contact Omas today.

THE DIGITAL MILL IN AFRICA

Digitalization is no longer a trend: it’s a requirement for competitiveness. African mills now have access to supervisory systems that monitor every stage of the milling process, from

raw wheat intake to final flour output. Omas’ automation platforms integrate seamlessly with existing plants, enabling operators to:

• Track performance and yield in real time

• Adjust grinding parameters based on wheat variability

• Predict maintenance needs before issues cause downtime

• Ensure consistent flour quality across batches

The combination of robust mechanical engineering and digital oversight empowers local teams, allowing them to respond quickly to challenges and maximize both efficiency and product quality.

Discover the benefits of a digitally integrated mill with Omas.

SHAPING THE FUTURE: AFRICA’S MILLING TRANSFORMATION

The African milling sector is moving beyond raw capacity. The new competitive edge comes from engineering, process optimization, and digital intelligence. By partnering with Omas, millers gain more than equipment: they gain industrial know-how, long-term technical support, and scalable solutions that adapt to changing markets and supply conditions. This approach ensures that each investment is not only operationally successful but positioned for long-term growth and resilience. For African millers, the message is clear: strategic partnerships and advanced technology are the foundations for future competitiveness. MMEA

Ready to take your mill to the next level? Reach out to Omas Industries and explore tailored solutions for your plant.

Omas Purifiers in operation at Foodtec, ensuring precise bran separation and consistently high-quality flour output

Breakfast Cereals Industry in Africa

A Growing but Uneven Market

HBY STEPHEN KIBE

istorically viewed as a niche market catering to the post-colonial elite, the breakfast cereal industry in Africa has evolved into a multibillion-dollar commodity ecosystem driven by rapid urbanization, a burgeoning middle class, and a profound shift in dietary habits among the youth. As of 2024, the African breakfast cereal market reached an estimated volume of 3.9 million tons, with a market value of approximately US$9.1 billion.

The consumption market is characterized by high regional concentration and a significant shift toward ready-to-eat (RTE) formats. While the global breakfast cereal market is expected to grow from US$63.08 billion in 2024 to US$78.82 billion by 2029, the African segment is particularly dynamic due to its unique demographic profile. Projections for the next decade suggest a continued, albeit slightly decelerating, growth trajectory, with the market expected to reach 4.6 million tons and a value

of US$11.5 billion by 2035. Key drivers include rising middleclass demand for convenient, fortified products, but challenges such as supply chain issues and traditional diets hinder the full potential.

PRODUCTION VS CONSUMPTION

As of 2023, Sagaci Research reported that the commodity penetration rate led in the five anglophone countries, led by South Africa (69%), Botswana (60%), Zimbabwe (57%), Ghana (43%), and Nigeria (41%). On the other hand, the countries with some of the lowest breakfast cereal consumption tend to be francophone: Algeria (12%), Guinea (13%), Burkina Faso (15%), and Mali (17%).

According to the study, the penetration rate of breakfast cereals is generally higher in Southern Africa. Conversely, it tends to be lower in North Africa in countries like Algeria,

THE CONSUMPTION

MARKET IS CHARACTERIZED BY HIGH REGIONAL CONCENTRATION AND A SIGNIFICANT SHIFT

TOWARD READY-TO-EAT FORMATS

Egypt and Morocco, countries all under 20% penetration and where traditional breakfast food is still very popular.

In 2024, approx. 3.9M tons of breakfast cereals were consumed in Africa according to Index Box. The countries with the highest volumes of consumption in 2024 were Nigeria (548K tons), Ethiopia (357K tons) and Democratic Republic of the Congo (264K tons), together comprising 30% of total consumption. Egypt, Tanzania, South Africa, Uganda, Kenya, Algeria and Sudan lagged somewhat behind, together comprising a further 29%. Three nations, Nigeria, Ethiopia, and the Democratic Republic of Congo, accounted for 30% of the total volume of breakfast cereal consumed on the continent.

On the production front, Africa produced 3.9 million tons of breakfast cereals in 2024, up 3.3% annually since 2013, led by Nigeria (523K tons), Ethiopia (345K tons), and Egypt (265K tons), accounting for 29% of output. Several factors, including the availability of raw grains. The South Africa breakfast cereal market is projected to lead the regional market in terms of revenue in 2030.

Manufacturing capacity and Import substitution, influence production volumes. The production of breakfast cereals in Africa is anchored by a few industrial powerhouses that serve as regional supply centers. South Africa, Nigeria, and Egypt are the primary engines of manufacturing, although each faces distinct operational challenges.

Major players such as PepsiCo's Bokomo, Kellogg's, General Mills, and Nestlé dominate, investing in fortified, ready-toeat (RTE) lines amid urbanization. When viewed through the lens of market value, the rankings shift slightly, reflecting the premiumization of products in certain regions. Ethiopia maintains the highest market value at US$1.2 billion, followed by Nigeria at US$972 million and Egypt at US$891 million. A critical driver of the industry's expansion is the shifting behaviour of the youth population.

In East Africa, research indicates that nearly 44% of the "Gen Z" population frequently choose breakfast cereal as a snack rather than a traditional morning meal. This trend is fueled by a demand for portability and convenience; four out of ten respondents in regional surveys highlighted a preference

SOUTH AFRICA ACCOUNTS

52% OF TOTAL AFRICAN SHIPMENTS IN 2024

for food that can be eaten on the go. This shift signals a move away from traditional fried snacks and toward grain-based ready-to-eat products, which are perceived as offering more health benefits beyond basic satiety. Manufacturers are responding by expanding variety and convenience, moving into cereal bar and singleserve pouch production to capture this "anytime" consumption market.

Additionally, increasing health and nutrition awareness is driving the consumption of fortified, whole-grain, and health-oriented breakfast cereals. Fortified cereals and instant porridges are increasingly positioned as solutions to micronutrient deficiencies, especially for children. Public-private partnerships and school feeding initiatives have created demand for fortified cereal products, which can be both a public-health tool and a commercial opportunity.

South Africa is the most mature breakfast cereal market on the continent and dominates exports, accounting for approximately 52% of total African shipments in 2024. The industry is characterized by a sophisticated mix of multinational subsidiaries and large-scale domestic corporations. Major players include Tiger Brands Ltd, Pioneer Voedsel (Pty) Ltd, and the local operations of global giants such as Kellogg’s (Kellanova), Mondelez, and Nestlé. The South African market is currently shaped by a strong health and wellness trend. Consumers are increasingly seeking cereals fortified with protein, fiber, and micronutrients.

For instance, brands like FUTURELIFE have expanded their "Smart Foods" range to include cereals scientifically formulated for athletes, containing probiotics and high-protein ingredients for sustained energy release.

Similarly, Bokomo introduced an improved Corn Flakes recipe in late 2024, focusing on an "extra toasty" flavour and fortification with nine B vitamins, iron, and zinc. Despite its strength, the South African production sector is currently navigating significant hurdles. Extreme weather conditions have impacted the yields of key cereal crops, and the industry is facing stricter government regulations targeting sugar content and artificial dyes. Furthermore, production value has fluctuated, reaching a historical peak in 2022 before declining in the following years.

MARKET GAPS AND STRUCTURAL CHALLENGES

Production nearly equals consumption, but gaps emerge in quality and variety: local output favours basic maize and sorghum flakes, while demand skews to imported wheatbased, fortified RTE cereals. Despite growth momentum, the breakfast cereals sector faces significant obstacles, including supply chain disruptions such as droughts and logistics costs, which cause shortages and price hikes, hitting affordability in low-income markets. Health concerns over sugar content, marketing bans to children, and recalls erode trust; competition from traditional foods like sadza or injera persists in rural areas.

High production costs, regulatory hurdles related to food labelling and food safety, and economic volatility limit scalability. SSA's cereal self-sufficiency rose to 92% (20102020), but breakfast-specific gaps remain due to processing tech deficits. Import Dependency for Ingredients: Many manufacturers still rely on imported grains like oats or barley,

increasing production costs and supply risks. Imports of breakfast cereals into Africa have generally been small relative to production, around 170,000 to 175,000 tons in 2024, and have even declined in recent years. Major importer markets include Nigeria (26K tons) and Botswana (15K), driven by demand outstripping local production or specific product preferences. However, reliance on imports exposes markets to foreign-exchange pressures and supply-chain volatility. However, exports are modest but growing, with countries such as South Africa, Egypt and Zambia emerging as key exporters.