From the first quarter of 2026, the global market landscape is once again being reshaped by historic upheaval. On March 5, the day when Taiwan CSC held a conference with Taiwanese fastener companies, the U.S. and Israel were charging intense strikes on Iran, igniting fierce conflict. Industry insiders were stunned: If the Strait of Hormuz is blockaded and the Middle East war drags on for months, supply chains could fracture again, with soaring oil prices triggering inflation and skyrocketing manufacturing costs! Taiwan Industrial Fasteners Institute (TIFI) Chairman Yung-Yu Tsai warned in his opening remarks that the industry's next turning point is clear: "Securing materials will be the key to overtaking competitors on the next bend!"

Taiwan CSC Conference with Fastener Companies:

From Middle East to Material Scramble, Fasteners Brace for Resource War Era

Chairman Tsai cautioned that the Middle East war directly hits oil, natural gas, and power supplies. For Taiwan importing 96% of its energy, the impact is massive! From Trump's pre-war deploying to his heavy-handed strikes, it's evident he's wielding an iron fist over control of global "strategic resources," including materials. Drawing lessons from afar, Chairman Tsai urged Taiwan's fastener business owners: The world has entered the "resource war" ignited by Trump—prices for gold, silver, copper, iron, tin, nickel, steel, and wire rod are all surging! He likened the international situation to the 1962 Cuban Missile Crisis, with stagflation looming. "Wire rod is the lifeblood of fastener production costs and a 'critical strategic resource'! Makers without control over wire rod will risk elimination in this resource war!"

Chairman Tsai elaborated that the biggest challenge now is: Who can grab the most revenue in the harshest conditions? He called strongly for a mindset shift: "Break free from relying on traders and importers! Think deeply: Who to sell to? Who's the most critical customer? Find the right partners!" Taiwan's fasteners, with 70 years of glorious history, are essential parts that safeguard human life and won't be obsolete. "Fasteners aren't low-end parts—they're 'premium products'! Their value isn't measured by price alone, so don't sell them cheap!"

Beyond the inflation threat from Middle East fires, Taiwanese makers must counter China's lowprice dumping. Getting trapped in price wars is a quagmire! Instead of chasing orders with just 3-5% margins, pursue highvalue fastener orders—Taiwan's technology can absolutely deliver! Chairman Tsai urged makers to communicate with overseas clients, letting them understand that Taiwanese fasteners are premium. Highlight Taiwan's trustworthiness, seamless collaboration, and longterm partnership potential!

6,500,000,000

6,000,000,000

5,500,000,000

5,000,000,000

4,500,000,000

Global Economic Recovery Affirmed—But Monitor Middle East Risks

4,000,000,000

Economic data from Taiwan CSC’s briefing shows global GDP growth projected at 2.7-3% this year, with Taiwan at 3-7%. Other than China's ongoing structural slowdown, recovery in the U.S., Europe, and India is solidified. Last year's growth was driven largely by AI; this year, it's shifting to traditional industries. Yet Trump's unpredictable strategies and the broad fallout from Middle East conflict mean close monitoring of the war is essential amid this rebound.

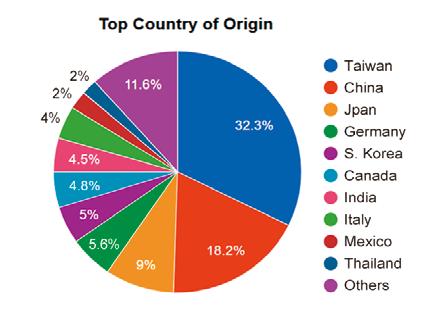

According to TIFI’s statistics, Taiwan's 2025 fastener exports totaled 1.23 million tons, down 4.1% year-over-year, with an average price of USD 3.53 per kg, up 0.8%.

Taiwan’s Customs data reveals 2025 fastener exports to all 5 major continents declined, except for ASEAN, which grew 9.7% as the top growth region for Taiwan. Over the past three years, Taiwan's fastener export value has fallen cumulatively by 8.3%, and 2025 may not have hit bottom yet (Figure 1) , signaling clear contraction of Taiwan’s fastener export.

Fig 1. Value of Taiw an's Fastener Export to the World

6,500,000,000

6,000,000,000

5,500,000,000

5,000,000,000

4,500,000,000

4,000,000,000

4,600,022,138 4,374,025,745 4,215,769,519

Turn Crisis into Opportunity: Treat Fasteners as Premium and Products

With Middle East flames and resource wars ignited, Taiwan's fastener companies must stand strong. Facing inflation woes and China's lowprice onslaught, Taiwan's fastener companies are urged to secure wire rod, target high-value partners, reject cheap sales, and leverage 70 years of craftsmanship to forge the "premium" value of Taiwanese fasteners—breaking free from the low-price trap. Chaos reveals true heroes; the future belongs to bold transformers who overtake on the next bend and claim global high ground!

Table 1: TIFI's Fastener Statistics

Sharing Key Policy Direction with Member Companies -Sunco Industries Held Sunco-kai Year-End Gathering

Ayear-end gathering of the Sunco-kai, hosted by Sunco Industries Co., Ltd., was held on November 21 last year at Hotel Nikko Osaka. The Sunco-kai is an association made up of manufacturers that supply products to Sunco Industries, with the aim of exchanging information and fostering mutual growth. This year’s year-end gathering was held on a grand scale, welcoming 171 member companies and a total of 244 participants. The event opened in a warm and friendly atmosphere.

Opening Address (Mr.Yasuhiro

President

of Nishi Seiko Co., Ltd.)

Nishi,

At the outset, an opening address was delivered by Mr. Nishi, President of Nishi Seiko Co., Ltd. and Chairman of the Sunco-kai. He touched on social topics that became prominent in Japan in 2025, including the Expo 2025 Osaka, Kansai, as well as the achievements of Japanese athletes active on the domestic and international sports scene. He then expressed his view that fasteners are also an industry Japan can be proud of. In closing, he stated, “Even as the yen is expected to continue weakening, we will remain steadily committed to manufacturing, and I hope Sunco Industries will continue to expand its exports,” concluding his remarks with words of expectation for the future of the fastener industry.

Speech by Mr. Yoshihide Okuyama, President of Sunco Industries Co., Ltd.

Next, President Mr. Okuyama took the stage and delivered a speech on the company’s performance in 2025 and its policies for the coming fiscal year. From March to October, the company’s sales increased by 101.6% compared to the same period last year, while the volume of products sold slightly declined to 98.3%. President Mr. Okuyama analyzed this by noting, “Even though the sales amount is growing, the decrease in units sold suggests that the real economy lacks strength,” presenting a measured assessment of the current situation.

As the main theme of his speech, President Mr. Okuyama emphasized strengthening information sharing with Sunco-kai member companies, and announced that, starting in early December 2025, the company will distribute the “SUNCO Trend Report”, which summarizes inventory circulation, quantities, and shipment volumes at Sunco Industries. Unlike reports organized by individual products, this report provides an overview of supply

and demand across the entire company and is scheduled to be distributed regularly at the beginning of each month. The report will be shared with all Sunco-kai members, and President Mr. Okuyama stated, “We hope that by providing an overview of the company as a whole, it will help you better understand the current situation.”

In addition, he announced plans to make available to members the company’s internal demand forecast data, which has long been used within Sunco Industries and summarizes daily shipment volumes. President Mr. Okuyama explained, “By sharing the same indicators, we can discuss issues from a common perspective and make our work proceed more smoothly,” encouraging members to make use of the data.

Guest Address (Mr. Yoshikazu Noda, Mayor of Higashiosaka City)

As a guest, Mayor Noda took the stage and spoke about the international recognition of Japan’s fastener industry. He mentioned the 3rd Japan International Art Festival, highlighting the diorama of the Grand Roof Ring made entirely of fasteners, which attracted attention at the festival. He noted that the exhibit demonstrated the high level of technology and quality of Japanese fasteners. Finally, he expressed that Higashiosaka City will continue to support the development of local industries, concluding his address.

This year’s Sunco-kai Year-End Gathering provided a valuable opportunity to share the current state of the industry and key policies for the coming fiscal year. In particular, President Mr. Okuyama’s speech, which emphasized creating a common language for business through data sharing to facilitate smoother operations, drew great interest from the participants. The Sunco-kai will continue its activities aimed at promoting mutual development among member companies and contributing to the growth of the industry.

Expo 2025 Osaka, Kansai, Japan

Expo 2025 Osaka, Kansai, Japan was an international exposition held for 184 days from April 13 to October 13, 2025, on Yumeshima, an artificial island in Osaka, Japan. It was the first World Expo in Osaka in 55 years and the first large scale Expo in Japan since the 2005 Aichi World Expo. People and exhibits from around the world gathered in large numbers, and more than 160 countries and regions introduced their latest technologies and unique cultures through national pavilions.

Section 232, CBAM, and Price-Cutting Editorial3 Major Challenges for Taiwan Fastener Industry in 2026:

The war between the U.S. and Iran began the end of February, but for fastener manufacturers, the 50% steel & aluminum tariffs have already been a grueling battle lasting nearly a year. Facing this seemingly endless tariff war which started in mid2025, Taiwanese fastener manufacturers must not only overcome rising distribution costs, but also confront multiple internal and external pressures. These include carbon

reduction requirements from the EU CBAM, labor shortages in traditional industries fueled by the high-tech boom, and relentless lowprice competition from Chinese and emerging market rivals flooding global markets. These challenges have placed unprecedented survival pressure on Taiwan fastener industry, which once had a glorious era. Some industry players openly warn that if these issues remain unaddressed, the much-touted “golden decade” of future growth will only grow increasingly distant for Taiwan fastener industry.

Taiwan's Fastener Exports Slightly Declined in 2025; Unresolved High Costs May Hinder Competitiveness

Last year, Taiwan exported nearly 1.2 million tons of fasteners, marking a slight YoY decrease of approx. 4%. Objectively speaking, this fluctuation aligns with normal market fluctuations when reviewing performance from previous years. However, January exports this year saw a significant YoY decline exceeding 13%, with February exports potentially falling further due to the longer Lunar New Year bank holidays. Among the top 20 export partners, many European and American countries showed declines of at least 10% (U.S. down 12.29%, Germany down 35.66%, and the Netherlands down 18.02%), indicating a short-term reduction in procurement demand from major European and American buyers, with full-year performance still to be observed. If this situation is not due to a cooling local market or simply seasonal factors reducing demand, it may be time to worry whether this is an early warning sign of order loss or diversion.

COST

The competitiveness of fastener exports largely stems from cost control. Over 60% of fastener manufacturing costs come from wire rod. Despite manufacturers' persistent feedback, Taiwan CSC's quarterly wire rod pricing seems consistently out of touch with market realities. Although CSC offers preferential project pricing to loyal customers, the nearly 4-fold surge in Taiwan's imports of cold heading wire rod from South Korea this year indicates that some Taiwanese manufacturers are no longer buying CSC's wire rod, whose price remains 15-20% higher than that of South Korean alternatives even with discounts. Compounding this, the EU CBAM has entered its formal implementation phase this year (requiring carbon emissions from 2026 onwards to be included in carbon fee declarations and certificate submissions), significantly increasing operational costs associated with CBAM compliance. With CBAM costs becoming the new normal, Taiwanese fastener manufacturers failing to narrow the cost gap with low-price competitors by addressing raw material expenses (the largest cost driver) may face increasingly challenging business conditions over the next 3-5 years. A sharp 20% decline in annual export performance may also become possible.

Taiwan's current industrial development environment has become increasingly unfavorable for fastener manufacturing. High-tech factories in industrial parks have snatched up many skilled workers. YoY increases in land costs and electricity expenses that remain higher than in other countries have also left many fastener manufacturers unable to offer competitive pricing even if they wanted to. Taiwan's fastener exports once peaked at 1.65 million tons annually, but in recent years have hovered around 1.2 million tons. Previously, manufacturers would selectively take orders from importers or distributors. Now, they accept whatever OEM/ODM orders they can get (e.g., small batches, diverse products, special designs, and high-tech requirements), highlighting the situation that against the backdrop of stagnant demand in the U.S. market, economic downturn in Europe, aggressive price competition from emerging economies, and Chinese companies expanding overseas production and sales networks to capture market share, Taiwanese manufacturers face limited options if they wish to retain their orders.

Detailed Regulations Should be Expedited for Refinement, Although CBAM is Well-Intentioned

Although CBAM is intended to promote industrial decarbonization and requires non-EU businesses to participate through regulations to prevent unfair competition, theses businesses still face significant implementation challenges, such as questions remaining unanswered regarding the authorized certification bodies for reporting, the documentation and complex calculation methods required for reporting fastener carbon emissions, difficulties in obtaining carbon emission data from subcontractors, the issue of offsetting carbon fees between the EU and certain countries, etc. Taiwanese manufacturers are highly willing to comply with regulations and are actively pursuing energy saving and carbon reduction across all fronts. They have even invested substantial resources in obtaining ISO 14064, 14067, and related certifications. Yet, with many aspects still lacking clear guidance, even those genuinely committed to implementation find themselves stymied at every turn, facing exponentially increased cost pressures. Compounding these challenges, the recent US-Iran conflict has raised the specter of a full blockade of the Strait of Hormuz, a vital transit point for many containers bound for Europe. Should containers be forced to reroute, transit times could increase by 1.5 times. Manufacturers must brace for the possibility of shipping costs to Europe rising by thousands of US dollars. If the detailed regulations of CBAM could be published ASAP to provide manufacturers with a clear basis for implementation, it would likely prevent the generation of unnecessary operational costs.

Does It Make Sense to Have Fasteners Subject to the Steel and Aluminum Tariffs, Even Though U.S. Consumers May Bear the Brunt?

Hand tools and components are also steel derivatives yet remain excluded from the steel and aluminum tariffs. Conversely, fasteners which inherently carry low added value and profit margins face an additional 50% tariff. This discrepancy appears ripe for further discussion. Many industry players privately lament that “imposing such high tariffs on basic necessities used in manufacturing across most industries makes no sense whatsoever.” Under the spirit of the U.S. Section 232, the criteria for including items in the steel and aluminum tariffs include: their steel content, whether they are derivative products of steel, and whether they are essential to the steel industry's core development, etc. Hand tools and components, being functional processed goods with added value far exceeding the proportion of their original materials, inherently fall outside the scope of the steel and aluminum tariffs. While theoretically sound, this approach may fail to protect the domestic steel industry when applied to the U.S. fastener sector. Instead, it could increase fastener procurement costs for U.S. consumers, as over 70% of U.S. imported fasteners are items either not produced or unattractive for domestic manufacturers to produce. Despite the Trump administration's push for U.S. manufacturing, the high labor costs in the U.S. make it impractical for fastener manufacturers already facing substantial production expenses to invest in local factories. Ultimately, cost pass-through could lead to higher fastener prices for U.S. consumers. Is this truly beneficial for many domestic manufacturing sectors reliant on fasteners? The answer is self-evident.

Fastener Taiwan Ready to be Held This April: Presence of European, American, and Japanese Visitors Will Be Key

Taiwan International Fastener Show (Fastener Taiwan) will be held at Kaohsiung Exhibition Center from April 22-24. Over 300 Taiwanese and international exhibitors are expected to participate. Fastener World welcomes all industry friends to visit us at Booth 1202 in the South Hall. On-site, you can obtain the latest supplier information for finished/semi-finished fasteners, raw materials, molds & dies, machinery & equipment, secondary processing, and peripheral services. Our professional marketing team will also be present to assist with procurement matchmaking. Many exhibitors have already expressed high expectations for this year's visitor turnout. Equipment and mold & die manufacturers anticipate meeting buyers from emerging markets, while finished product manufacturers urgently seek opportunities to connect with buyers from Europe, the US, and Japan. However, in recent years, some voices have suggested that Fastener Taiwan should be held every 3-4 years to better align with Taiwan's fastener production and sales cycles. Taiwan fastener industry possesses a globally unique, complete supply chain capable of meeting diverse buyer demands worldwide. We sincerely invite you to visit. In today's uncertain global market, Taiwan's stable fastener supply chain remains your best choice for sustained success.

Copyright owned by Fastener World / Article by Gang Hao Chang, Vice Editor-in-Chief

Financial Reports of Fastener Companies

U.S.A (in million USD)

Alcoa's 2025 net sales were USD 12,831 million, up 7.8% from USD 11,895 million in 2024. Net income was USD 1,170 million in 2025, up 1,850% from USD 60 million in 2024. Total assets increased to USD 16,212 million in 2025 from USD 14,064 million in 2024. EACO Corporation's 2025 revenues were USD 427.931 million, up 20.1% from USD 356.231 million in 2024. Net income was USD 34.650 million in 2025, up 7.5% from USD 32.218 million in 2024. Total assets increased to USD 230.153 million in 2025 from USD 188.538 million in 2024.

Fastenal’s 2025 net sales were USD 8,200.5 million, up 8.7% from USD 7,546.0 million in 2024. Net income was USD 1,258.4 million in 2025, up 9.4% from USD 1,150.6 million in 2024. Total assets increased to USD 5,052.9 million in 2025 from USD 4,698.0 million in 2024.

Nucor's 2025 net sales were USD 32,494 million, up 5.7% from USD 30,734 million in 2024. Net income was USD 1,744 million in 2025, down 13.9% from USD 2,027 million in 2024. Total assets increased to USD 35,104 million in 2025 from USD 33,940 million in 2024.

Simpson Manufacturing's 2025 net sales were USD 2,332.808 million, up 4.5% from USD 2,232.139 million in 2024. Net income was USD 345.083 million in 2025, up 7.1% from USD 322.224 million in 2024. Total assets increased to USD 3,073.626 million in 2025 from USD 2,736.168 million in 2024.

Compiled by Fastener World

Japan (in million JPY)

JPF’s 2025 revenues were JPY 5,064 million, up 0.5% from JPY 5,040 million in 2024. The company ended the year with a net loss of JPY 30 million in 2025, down from a net profit of JPY 509 million in 2024. Total assets decreased to JPY 5,619 million in 2025 from JPY 5,785 million in 2024. The company forecasts 2026’s revenue at JPY 5,300 million, up 4.7%.

Kyowa

Kogyosyo’s 2025 revenues were JPY 10,457 million, down 4.7% from JPY 10,972 million in 2024. The company ended the year with a net profit of JPY 708 million in 2025, down 50.9% from JPY 1,443 million in 2024. Total assets increased to JPY 18,151 million in 2025 from JPY 17,903 million in 2024. The company forecasts 2025’s revenues at JPY 10,300 million, down 1.5%.

Mitsuchi’s 2025 revenues were JPY 12,411 million, down 5.6% from JPY 13,147 million in 2024. The company ended the year with a net loss of JPY 95 million in 2025, down from a net profit of JPY 419 million in 2024. Total assets decreased to JPY 15,858 million in 2025 from JPY 16,450 million in 2024. The company forecasts 2026’s revenues at JPY 12,522 million, up 0.9%.

Nitto Seiko’s 2025 revenues were JPY 50,238 million, up 6.7% from JPY 47,069 million in 2024. The company ended the year with a net profit of JPY 2,152 million in 2025, down 2.2% from JPY 2,199 million in 2024. Total assets increased to JPY 57,673 million in 2025 from JPY 55,604 million in 2024. The company forecasts 2026’s revenues at JPY 52,000 million, up 3.5%.

Torq’s 2025 revenues were JPY 22,538 million, up 0.6% from JPY 22,409 million in 2024. The company ended the year with a net profit of JPY 904 million in 2025, up 1.0% from JPY 895 million in 2024. Total assets increased to JPY 34,042 million in 2025 from JPY 33,680 million in 2024. The company forecasts 2025’s revenues at JPY 21,000 million, down 6.8%.

Europe

Bufab's 2025 net sales were SEK 8,072 million, up 0.4% from SEK 8,035 million in 2024. Net profit was SEK 626 million in 2025, up 13.6% from SEK 551 million in 2024. Total assets increased to SEK 9,319 million in 2025 from SEK 9,191 million in 2024.

Bulten's 2025 net sales were SEK 5,045 million, down 13.1% from SEK 5,807 million in 2024. Net income was SEK 18 million in 2025, down 88.8% from SEK 161 million in 2024. Total assets decreased to SEK 4,447 million in 2025 from SEK 5,099 million in 2024.

Trifast

’s 2025 revenues were GBP 223.466 million, down 4.3% from GBP 233.671 million in 2024. Net profit was GBP 1.040 million in 2025, down from a net loss of GBP 4.440 million in 2024. Total assets decreased to GBP 41,165 million in 2025 from GBP 44,557 million in 2024.

Fastener World News

U.S. Export Tariffs at 50% Unchanged, TIFI: “Taiwan Fasteners Shift to Higher Quality & Differentiation”

Taiwan and the U.S. have finalized reciprocal tariffs—now at 15%—but Taiwan's fasteners sector remains under Section 232 provisions, maintaining 50% U.S. import duties. Secretary-General Mr. Fang-Yi Yang of Taiwan Industrial Fasteners Institute (TIFI) stated that global steel exports to the U.S. face the same 50% rate; Taiwan firms must compete via high quality, product differentiation, and international strategies. Yang noted the industry had been impacted before the negotiation and urges the government to keep NTD exchange rate stablized.

Kaohsiung City Government highlighted Kaohsiung as Taiwan's fastener production hub, accounting for over 50% of national output, with North America as a key market. The government collaborates with industry associations for real-time impact assessment, guiding firms toward high-value, digital, and low-carbon development to boost global competitiveness.

Market Watch: Trump Tariff 2.0

Reciprocal Tariff for Taiwan Totals No More Than 15%, Including Auto Parts

Taiwan-U.S. tariff negotiations achieved significant progress on January 15, reaching four agreements on key areas: “Taiwan's reciprocal tariffs reduced to 15% without accumulation,” “Semiconductors and related derivative products subject to Section 232 tariffs are granted MFN treatment,” “Expanded supply chain investment cooperation,” and “Deepening the Taiwan-U.S. AI strategic partnership.” Representatives from the Taipei Economic and Cultural Representative Office (TECRO) and the American Institute in Taiwan (AIT) signed a memorandum of cooperation at the U.S. Department of Commerce.

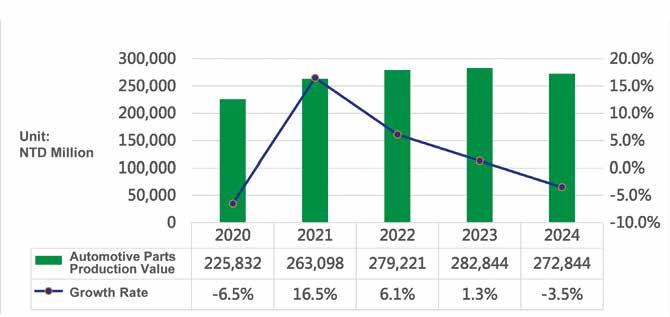

The reduction of reciprocal tariffs to 15% without accumulation will grant Taiwan “most-favored-nation treatment” among major U.S. trade deficit countries, placing it on par with trading partners like the EU, Japan, and South Korea. While the agreement primarily focuses on future investment plans in the U.S. and tariff incentives for Taiwan's semiconductor, chip, and high-tech industries, traditional industry sectors like hand tools and machine tools—previously subject to 20% reciprocal tariffs—along with the auto parts industry (facing 25% tariffs under Section 232 starting May 2025) will also see rates reduced to 15%. Additionally, according to the announcement of U.S. Department of Commerce, aircraft components falling under reciprocal tariff coverage will enjoy a 0% tariff rate, benefiting manufacturers in related sectors.

According to Taiwan's negotiation task force, the U.S. has committed that raw materials, equipment, and components required for Taiwanese enterprises investing in, establishing factories in, and operating within the U.S. will be exempted from reciprocal tariffs and Section 232 tariffs. Additionally, regarding potential new items added under the U.S. Section 232 measures in the future, both Taiwan and the U.S. have also agreed to establish a mechanism for ongoing negotiation on mostfavored-nation treatment.

Fastener Importer Challenges CBP's Section 232 Tariff Valuation Method in U.S. CIT Lawsuit

Illinois-based fastener importer Express Fasteners, Ltd. has filed a lawsuit at the U.S. Court of International Trade (CIT), contesting the U.S. Customs and Border Protection (CBP)'s valuation and application of Section 232 tariffs on imported steel and aluminum derivative products. The plaintiff argues that CBP unlawfully imposed 50% steel duties on its imported fasteners by applying the tariff to the full product value— including machining, manufacturing, factory overhead, and other non-steel costs—rather than limiting it to steel content alone. This shift violates longstanding CSMS guidance, FAQs, and Customs rulings, and was implemented without public notice, comment, or rulemaking procedures, constituting an arbitrary and unlawful change.

At the heart of the case is an internal, unpublished memorandum from CBP's Base Metals Center of Excellence and Expertise (CEE) issued last December. Express alleges the memo redefines manufacturing, machining, overhead, and profit as "steel content," inflating duties dramatically. The company claims this generally applicable rule required Administrative Procedure Act notice-and-comment processes, which CBP failed to follow. Express seeks a court declaration invalidating CBP's approach, reliquidation based solely on steel content, and refund of excess duties plus interest.

Record China 2025 Trade Surplus Defies US Tariffs

National Bureau of Statistics of China announced that the Chinese economy grew 5% in 2025, hitting its target, fueled by a historic USD 1.19 trillion trade surplus. Despite Q4 slowing to 4.5%, exports defy Trump tariffs, a slumping property market, and weak consumer spending.

However, analysts call it a "dual-speed economy": robust manufacturing and exports contrast with lagging domestic demand and real estate. Capital Economics suggests the data overstates growth by 1.5 points. Compounding woes, births hit a record low of 7.9 million, with the population dropping 3.4 million to 1.4 billion. Natixis (France trade bank) warns lowprice exports aren't sustainable. Last December saw home prices fall 2.7%, investment drop 17.2%, and retail rise just 0.9%. The head of National Bureau of Statistics of China acknowledges supply-demand imbalance but expects stability. Beijing plans proactive policies to boost confidence, curb debt, and reduce export reliance.

Industry Development

Market Watch: CBAM

Taiwan Environment Minister Confirms EU CBAM Exemptions in His Europe Visit: 2,600 Taiwan Firms Relieved of Carbon Tariff Pressure

Environment Minister Chi-Ming Peng visited the EU on February 21 for in-depth discussions on CBAM, confirming that SMEs can apply simplified carbon emission formulas and de minimis exemptions. With annual imports under 50 tons fully exempt, approximately 2,600 Taiwan SMEs exporting to Europe will benefit, significantly easing administrative burdens.

Presenting on "Taiwan Green Strategy," the minister outlined net-zero pathways, carbon fee mechanisms, and climate governance plans. The EU praised Taiwan's carbon fee deductions covering Scope 2 emissions. Discussions focused on three key issues: carbon price deduction calculations and certification, mutual verifier recognition, and technical exchanges. The EU revealed that multiple countries have complained about high verifier administrative costs and is amending regulations to include mutual recognition provisions, potentially validating Taiwan certificates.

Taiwan ranks 13th among the EU's top 20 CBAM product import sources during the transition period, with 3.74 million metric tons mainly being steel products including screws, fasteners, stainless steel, and carbon steel. The Climate Agency noted Taiwan's carbon fees are CBAM-recognized but awaits EU’s deduction formulas, urging clearer calculation methods and proof requirements. The minister emphasized Taiwan's precision manufacturing and urban mining recycling strengths, positioning it as a "global green solution" to deepen Taiwan-EU climate collaboration.

War, Price Cutting, and Import Surge: Taiwan Fasteners Hit by Freight Spike and Chinese Undercutting

U.S. strikes on Iran have nearly halted Hormuz Strait shipping, with carriers suspending Middle East cargo acceptance. Spot rates to Europe and Middle East have surged USD 1,000 above contract rates plus surcharges. Evergreen Marine maintains all scheduled services but closely monitors Middle East, Red Sea, and Hormuz developments, promising timely customer notifications for any adjustments.

On the other end of the world, China's 2025 fastener exports hit 6.23 million tons, up 6.7% YoY, but average price fell to USD 1.9/kg from USD 2/kg, continuing the decline. Taiwanese manufacturers note that China's low-price dumping and intense internal competition have customers using Chinese quotes to pressure Taiwanese suppliers for lower prices. Taiwan's high costs make it hard to compete, leading to a "severe competition" in standard products, with Taiwanese firms opting to reject orders to avoid losses.

In steel trends, according to Taiwan CSC's statistics, cold heading material imports in Taiwan from South Korea surged 395% in 2025 to 26,857 tons. Taiwanese manufacturers shifted purchase because Korean material is 10-15% cheaper, with cold heading mainly used for automotive cold-forged bolts, nuts, etc. Taiwan CSC's price plan to balance the price gap still struggles against the appeal of Korean material.

Taiwan's fastener industry confronts freight spikes, Chinese low price, and Korean steel substitution in a perfect storm of challenges.

Companies Development

Tariffs Ease, Sumeeko Aims for Recovery with European Factory Boosting Annual Operations

Automotive fasteners leader Sumeeko welcomes a turning point, with profit structure improving significantly this year, paving the way for operations to return to normal levels.

Sumeeko's consolidated revenue last year reached NTD 2.554 billion, down 7.64% year-over-year, mainly due to advance payments for high tariffs and the ongoing optimization of its German plant. Around 60-70% of revenue comes from OEM clients. Last year, orders from its Taiwan plant to Europe and the U.S. remained stable. However, the company shipped goods to U.S. warehouses in advance and held them there until customers placed orders, which required it to pay tariffs upfront and significantly hurt profits. In the second half, Sumeeko actively negotiated with clients; some have agreed to cover tariffs, while others adjusted shipping strategies. With the Taiwan-U.S. tariff situation finalized, pressures have clearly eased. Sumeeko announced that its German subsidiary, MAX MOTHES GmbH, invested €1.8 million to establish a wholly-owned new subsidiary, Beco Group GmbH, targeting acquisitions of suppliers to German OEM clients. This is expected to add €3-5 million in annual revenue, directly boosting this year's revenue and profits. Positive news also came from the U.S. plant, which is undergoing customer certification and is slated for production in the first quarter, aligning with localization demands. Sumeeko's operations look promising this year, with the market optimistic about these dual positives driving a recovery.

General Fasteners Company Appoints New President

U.S. Suburban Detroitbased fastener and Class C components distributor General Fasteners Company has named John Hickey as its new president. Previously vice president of strategic operations and sales, Hickey was promoted as announced via social media. Company officials described him as the "driving force" behind operations, growth, and corporate culture. "I'm honored to step into this role and continue building on General Fasteners' legacy of reliability, innovation, and partnership," Hickey stated.

The 70-year-old distributor rebranded to General Fasteners last year, symbolizing its evolution from fasteners to a "trusted partner in global supply chain management."

Edson Manufacturing Expands, Investing USD 4 Million in New Facility in Connecticut

Edson Manufacturing (Connecticut, USA) is rapidly expanding its operations and has announced a roughly USD 4 million investment to relocate to a new facility exceeding 38,000 square feet on over 36 acres of land. The move is expected to be completed by mid-2026. Combined with existing facilities, the total space will surpass 78,000 square feet, enhancing service to customers.

Established in 1964 as an eyelet manufacturer, Edson has evolved from a small 5,200 sq ft shop with just seven employees into a powerhouse producing over 450 million fasteners, tools, and components annually for thousands of customers across industries. It now employs more than 50 people and specializes in domestic blind rivets made from stainless steel, steel, aluminum, copper, and monel. Since 1987, under current ownership, the company has prioritized quality assurance, on-time deliveries, competitive pricing, and exceptional customer service.

ARP Launches New Specialty Nuts and Washers Lineup

U.S. high-performance fastener manufacturer ARP has expanded its nuts and washers offerings, introducing nearly 60 new kits for 2026 to complement its diverse bolts and studs. The washer lineup features polished stainless steel or black oxidetreated 8740 chrome moly in SAE sizes from 1/4" to 3/4", with standard or chamfered options; metric sizes M6 to M18 are also available. Special insert washers prevent hole galling or collapsing in popular SAE and metric sizes.

Founded in 1968 as a family-owned and operated company, ARP in-house manufactures premium nuts to the industry's strictest specs. These include polished stainless steel and black oxide 8740 chrome moly 12-point and hex nuts for SAE coarse/ fine and metric uses, plus Nyloc self-locking hex "Jet" nuts, 12-point "K" nuts, and serrated flange nuts.

Bulten Group to Invest Rs 525cr in Tamil Nadu Fastener Plant

Sweden-based fastener leader Bulten Group, through its Indian subsidiary PSM Fasteners India, has signed a Memorandum of Understanding with the Tamil Nadu government to establish a new manufacturing facility in Oragadam. The project involves a Rs 525 crore investment, as announced by Tamil Nadu Industries Minister T R B Rajaa on social media. It is expected to create around 2,000 jobs.

The new plant will produce a full range of microfasteners to meet domestic demand and target key export markets in Europe and the United States. This move strengthens Bulten's southern India manufacturing base, combining advanced technology with local advantages to enhance global supply chain competitiveness and boost the regional economy.

U.S. structural fastening leader Simpson Strong-Tie is expanding its RFB retrofit bolt series with new diameters and lengths in Grade 36 rod, plus new Grade 55, 105, and Stainless Steel 304/316 options. These precut, precleaned threaded rods come fully assembled with nut and washer, pairing seamlessly with anchoring adhesives for quick anchoring into existing concrete and masonry, saving significant jobsite time. RFBs stand out with clear dual-end markings: length stamped in inches (for 1/2" diameters and up) and color-coding by steel grade for easy identification. Paired with Simpson adhesives, they form a complete engineered system.

Associate Product Manager Jerry Miller stated: "Field engineers struggling to verify post-install specs will appreciate our stamped and color-coded RFBs for time savings and peace of mind in inspection. The expanded line now offers greater versatility, including 3/8" diameter, shorter lengths for 1/2"-3/4" bolts, and 7/8"-1" zinc-plated carbon steel to meet diverse capacity needs."

Punch Industry and Misumi Group Launch Mold Parts Logistics Partnership

Punch Industry began outsourcing logistics operations to Misumi Group’s East Japan Distribution Center, starting October 2025. Punch's former Tokyo Logistics Center is integrated into Misumi's facility, with Misumi providing third-party logistics services. Results include 110 hours/month reduction in truck waiting/loading time and 216 fewer 10-ton truck visits monthly, plus shelf-transport robots and automated picking systems enhancing efficiency.

Volume consolidation generates scale economies for stable customer supply. Misumi, serving 323 thousand global clients with 30M+ items, won JILS's top 2025 Logistics Improvement Award. Future plans include joint procurement, mutual supply, leveraging Punch's precision machining with Misumi's digital technology for overseas expansion and supply chain optimization in metalworking/mechanical parts.

Mercedes-Benz Returns to Screws, Replacing Glue for Enhanced Sustainability and Repairability

Under its Tomorrow XX program, German automaker Mercedes-Benz is rethinking fastening technology by switching from glue to screw assemblies, significantly boosting vehicle sustainability and repair convenience. This addresses material waste reduction, easier part disassembly, and owners' demands for repair-friendly designs.

The first application targets headlight lenses: shifting from glued attachments to screw fixation allows damaged lenses to be replaced individually by unscrewing a few bolts, avoiding full headlamp disposal. This cuts resource use and enables easy self-repairs. For decades, adhesives were favored for lighter weight, lower fuel use, and CO2 reduction, but they complicate repairs—leading to whole assemblies landfilled—and hinder material separation for recycling.

Mercedes is also testing thermoplastic rivets for soft door panels instead of ultrasonic welding, allowing simple drilling for disassembly in repairs or end-of-life recycling. Engineers stress this screw revival balances innovation, environmental duty, and user ease. Future models will feature these solutions, upholding the century-old brand's commitment to progress and responsibility.

Southco Thailand Chon Buri New Plant Opens, Deepens Southeast Asia Fastener Market Presence

Global engineering solutions company Southco has officially opened its new facility in Chon Buri, Thailand, marking a major milestone in its Southeast Asian expansion. Spanning over 2,255 square meters, the plant focuses on manufacturing captive screws, electronic access solutions, ejectors, and Quick Disconnect Adapters, significantly reducing lead times and enhancing supply chain resilience while bringing world-class operations closer to fastgrowing markets.

Following Southco's record-breaking year of global expansion, the Chon Buri facility positions the company to deliver cutting-edge solutions across Southeast Asia while maintaining rigorous quality standards. Southco emphasized that the new plant strengthens localized production capabilities and customer service efficiency. This expansion underscores the company's long-term commitment to the Asia-Pacific region, establishing Chon Buri as a key manufacturing hub supporting rapid response and customization needs throughout Southeast Asia.

FasLab Established as Japan's First Fastener Think Tank

Japanese fastener firm Saima Corporation has announced the establishment of Faslab, a fastening technology consulting firm, to provide neutral and objective professional advisory services to mechanism designers. This move addresses the common shortage of verification and consulting resources in screw, bolt, and bolted joint design practices.

Faslab caters to designers' real-world needs by offering paid technical consulting services based on theory, testing, and analysis—including inspection analysis—without bias toward any specific vendor. Bolt-related failures directly impact product quality and safety, yet design sites often lack professional consulting channels. The company tackles designers' core challenges head-on, delivering practical solutions.

Saima Corporation's expertise in fastening technology will, through this new service model, help design teams solve tough problems and enhance manufacturing reliability. Faslab's services are slated to launch this April. This initiative ushers in a new era of technical support in Japan's fastener industry and is poised to become an indispensable professional think-tank partner for designers.

Nitto Seiko's India Vulcan New Plant Launches, Boosting Cold Forging Capacity for Japanese Clients

Nitto Seiko announced that its Indian subsidiary Vulcan Forge's Jhajjar plant in Haryana began production in December 2025. Anchored by 5S systems, it strengthens customer engagement to optimize quality, delivery, and costs, integrating with group operations to enhance local manufacturing and supply stability.

Located in Reliance MET City industrial park near the capital region—a smart city hub drawing major Japanese firms—the facility produces nuts and special cold-forged parts. Designed with second-floor expansion potential for future scaling.

Future plans include accelerating client development for reliable Japanese supply; installing solar panels to cut power costs and emissions; consolidating HQ functions for optimized staffing, shorter lead times, and lower logistics expenses; and rolling out group training to build on-site personnel cohesion.

This strategic move solidifies Nitto Seiko's Indian footprint, supporting global forging chains.

Acquisitions

Young Mobility Wins Ford Q1 Certification: First in Korean Fasteners Industry, Eyeing Global Expansion

South Korean fastener maker Young Mobility (YM) announced on November 18, 2025, that it has become the first domestic company to earn Ford Motor Company's top-tier Q1 certification. This award follows rigorous evaluation of quality, production capabilities, and supply chain management, designating YM as an official primary partner with rights to bid on new business.

YM formed a cross-functional task force last October spanning quality, production, and sales, achieving certification after about one year. Currently supplying bolts for Ford Europe's (Germany, UK) powertrains, YM now targets North America and Ford Thailand for new opportunities. Ongoing projects with global giants like Hyundai-Kia (largest ICE and EV customer), Schaeffler, LG Magna, and BorgWarner continue expanding. YM is ramping up sales with Ford, GM, and Rivian, driving steady export and revenue growth.

Applied Industrial Technologies announced on January 27 the acquisition of Thompson Industrial Supply. Thompson distributes industrial bearings, power transmission, hydraulics, pneumatics, linear motion, and lightweight belting with 40+ employees across two locations serving food & beverage, consumer products, pharma, life sciences, and more. Integrated into Applied's U.S. Service Centers, it's expected to add USD 20M in first-year sales.

President & CEO Neil Schrimsher stated: "Thompson bolsters our local service centers and motion control aftermarket support. This bolt-on enhances our footprint with technical expertise, supplier ties, and in-house fabrication boosting value-added services regionally." Applied ranked No. 7 in industrial supplies, and No. 10 in fasteners on MDM's 2025 Top Distributors list. This acquisition continues to strengthen Applied's local service center advantages, enhancing after-sales support for motion control solutions.

Japanese Seika Corporation Acquires Coating Machine Maker

Asahi Sunac

Seika Corporation announced it acquired 100% of the shares in Asahi Sunac—a manufacturer and seller of coating machines, die-casting machines, and precision cleaning equipment—on December 1, 2025, making it a subsidiary. The market has expectations of performance contributions. The two companies previously established joint ventures in Germany and Thailand. This acquisition aims to leverage Seika Corporation's expertise as a comprehensive machinery trading firm, deepening collaboration not only in sales but also in business development. The acquisition price was not disclosed.

2025 Market Periscope

German Home Improvements and Fastening Tool Market Demand

Copyright owned by Fastener World / Article by Shervin Shahidi Hamedani

Germany’s home improvement market in 2025 stayed large, but demand was uneven and selective. The most reliable near-term demand proxy for fastening tools is the DIY and home improvement retail channel’s reported turnover. Through January to September 2025, the channel reported EUR 16.08 billion, down 1.4% year on year (like-for-like down 1.2%).

The year did not deliver a clean rebound: Q2 turned positive, while Q1 and Q3 were negative.

For fastening tools, this pattern usually means essentials and consumables stay comparatively resilient, while discretionary upgrades and “nice-to-have” purchases remain under pressure. In parallel, official housing and construction indicators show early signs of improvement on permits and construction turnover toward late 2025. Those signals tend to influence fastening demand with a lag, meaning they are more relevant for 2026 planning than for explaining 2025 retail performance.

What the DIY Channel Reported in 2025

Retail sell-through matters because it captures what households and small trades are buying in real time. The latest publicly available 2025 update covers January to September.

The quarterly breakdown is the best way to understand how demand behaved:

• Q1 2025: EUR 4.57 billion, -4.0% year on year (like-for-like -3.5%).

• Q2 2025: EUR 6.47 billion, +1.2% year on year (like-for-like +1.4%).

• Q3 2025: EUR 5.04 billion, -2.3% year on year (like-for-like -2.2%).

• Jan–Sep 2025 total: EUR 16.08 billion, -1.4% year on year (like-forlike -1.2%).

This tells a practical story: demand activated in spring, but the market did not sustain momentum through late summer.

Table 1. German DIY and Home Improvement Retail Turnover (all values: gross turnover)

How to Interpret These Signals for Fastening Tools

Fastening tool demand is not a single category. It is a chain of purchases that shifts depending on whether people are doing large renovations or small fixes. In a year like 2025, three demand layers matter:

Maintenance and replacement (most stable)

Layer A:

Small projects and seasonal work (highly seasonal)

Big renovations and upgrade purchases (most volatile)

Maintenance and replacement (most stable)

This is the everyday layer. People still need to mount, repair, replace, secure, and reinforce. Even when budgets tighten, this work does not disappear. This supports steady demand for:

• core screws, anchors, plugs, washers, brackets

• basic hand tools and small kits

• consumables such as bits, blades, and abrasives

Housing and Construction: The Real Drivers Behind Project-Led Demand

Fasteners and fastening tools are downstream of housing and construction. The official indicators help explain why 2025 looked selective at retail even as some upstream signs improved.

Housing completions weakened in 2024

Germany completed 251,900 dwellings in 2024, down 14.4% year on year. Completions matter because they trigger downstream spending: fit-outs, move-ins, and a wave of installation work.

Backlog remained substantial

At end-2024, the official backlog of approved but incomplete dwellings was 759,700, including 330,000 already under construction. A large backlog supports medium-term activity, but it can also signal that delivery is stretched and demand is spread out.

Layer B:

Small projects and seasonal work (highly seasonal)

These are weekend and household projects that often activate in spring and early summer. Typical examples include fencing repairs, garden structures, outdoor fixtures, storage upgrades, and small carpentry. This layer supports demand for outdoor-rated fixings and corrosion-resistant hardware, plus the accessories that make work faster.

Layer C:

Big renovations and upgrade purchases (most volatile)

This layer drives the bigger baskets: multi-room upgrades, kitchens and bathrooms, flooring refits, large drywall work, and heavy structural improvements. It is also where discretionary power-tool upgrades happen. When the retail channel is down and choppy, this layer usually becomes selective. Many consumers either postpone, narrow scope, or trade down.

So the 2025 takeaway is that the mix likely leaned more toward Layers A and B, while Layer C remained cautious.

Permits improved in late 2025

Permits are a leading indicator. In October 2025, permits were 19,900 dwellings, up 6.8% year on year. Over January to October 2025, permits totalled 195,400, up 11.2% year on year. This is constructive, but the demand impact typically arrives later via starts, completions, and trades activity.

Construction turnover turned positive

For October 2025, nominal turnover in the main construction industry was reported at EUR 11.6 billion, up 7.0% year on year, with real turnover up 4.5%. For January to October 2025, real turnover was up 1.8% versus the prior-year period.

These indicators help separate two realities:

• Retail demand in 2025 stayed cautious and seasonal.

• Upstream signals began to improve, supporting a more stable planning case for 2026.

Table 2. Housing and Construction Indicators Relevant to Fastening Demand

Channel Dynamics: Why 2025 Was a “Precision Year”

When growth is not broad-based, execution matters more than messaging.

Availability beats variety

In selective markets, shoppers are less patient. They want the correct size, the correct anchor, and the correct tool accessory to finish a job. Out-ofstocks in core sizes can lose the entire basket, not just one item.

Promotions influence mix

A slightly declining market often triggers promotion intensity. That can move volume, but it changes what sells: buyers may shift to multipacks, entry-level ranges, or whichever accessory set is

What This Means for Suppliers and Distributors

Here are the 2025 implications that translate into concrete actions:

/// Treat consumables as your volume stabiliser

Bits, blades, anchors, and core fixings often provide the most predictable turnover in selective years. The priority is to protect service levels and reduce gaps in top movers.

/// Align assortment to common jobs, not only to categories

Retail customers do not think in “fasteners”. They think in tasks: mounting a TV, fixing a fence, hanging cabinets, repairing a hinge, reinforcing a joint. Packaging and planograms that map to jobs can lift conversion even in a soft market.

/// Improve the entry-to-mid ladder

When the market is cautious, many buyers trade down on big-ticket items while still buying reliable essentials. That is where mid-tier value positioning often outperforms premium-only positioning.

/// Expect uneven demand timing

The Q2 uplift in 2025 underlines how seasonal activation can still be strong even when the year-todate headline is negative. Supply planning should focus on spring readiness for outdoor projects and maintenance spikes.

/// Watch upstream indicators for 2026 production planning

Permit improvement and construction turnover growth suggest the project-led layer could strengthen later. If that translates into activity, demand may shift

on offer. For suppliers, this makes forecasting by SKU more volatile than forecasting the overall category.

Small-basket behaviour increases

When consumers postpone bigger upgrades, they buy more frequently in smaller baskets. That supports steady unit movement in essentials, but it also increases the importance of packaging formats and shelf clarity. In fastening, the “search cost” matters. If selection is confusing, the customer either abandons or buys the simplest option.

toward larger trade packs, anchoring systems, and higherthroughput tool usage.

/// 2026 Outlook: Clear Forecast Framing

Given that the most recent published 2025 retail update covers only the first nine months of the year, this article does not present a full-year 2025 market size projection. Instead, the 2026 outlook is framed as the most likely direction based on the latest retail trend, housing pipeline signals, and construction activity indicators.

For 2026, the most likely outcome is a stabilising home improvement market, with demand shifting gradually from pure maintenance toward a higher share of project-led work as the housing pipeline improves. In this environment, fastening tools should track at least in line with the broader home improvement channel, with consumables and core fixings remaining the most resilient, and project-linked volumes recovering more slowly as renovation confidence returns.

What this Means Operationally

• Expect steady baseline demand for essential fixings, anchors, and refills throughout the year.

• Plan for a firmer second half versus the first half, driven by gradual improvement in project timing and trades activity rather than a sudden market rebound.

• Prioritise range discipline and availability in core sizes and high-rotation accessories, because selective buying behaviour remains the defining feature even in a stabilising market.

Sources

• German DIY and garden retail trade association market reports (2024 results, 2025 updates).

• Destatis: housing completions and backlog (2024).

• Destatis: dwelling building permits (2025).

• Destatis: main construction industry turnover (2025).

Potential U.S. Fastener Demanding Markets in 2026:

DIY Fasteners

Fasteners

rarely dominate market headlines, yet they are embedded in nearly every home improvement activity. Whether a homeowner is repairing a loose deck board, installing shelving, updating cabinet hardware, or reinforcing a fence, screws, nails, anchors, bolts, and washers are essential. As the U.S. moves into 2026, the outlook for DIY fasteners is closely tied to broader housing and remodeling trends rather than to any single trade statistic. Because HS codes classify fasteners by function and physical characteristics, such as under 7318 for screws and bolts or 7317 for nails and staples, rather than by end use, it is impossible to isolate “DIY fasteners” directly from trade data. Instead, we must extrapolate likely demand from housing activity, consumer behavior, and policy conditions.

Based on current forecasts and market signals, 2026 appears to be a year of cautious stability for DIY fasteners. The market is unlikely to experience explosive growth, but neither does it show signs of collapse. Instead, demand is expected to concentrate on repair-driven projects, aging housing upgrades, and smaller-scale improvements that homeowners can justify in a still-elevated interest rate environment. At the same time, tariff uncertainty and ongoing trade measures remain critical variables that could shape pricing, sourcing, and product availability.

Remodeling Stability and the Resilience of Small Projects

The foundation of DIY fastener demand in 2026 rests on remodeling activity. Major housing research institutions project that overall homeowner improvement spending will continue to expand, although at a slower growth rate than in prior years. Annual spending is expected to reach record levels, even as year-over-year growth moderates. This suggests a large, active remodeling base that continues to consume fastening products, albeit without the urgency or speculative energy of a boom cycle. Mortgage rates are forecast to remain above historical lows, hovering around the mid-6% range. While this may limit large, financed renovations, it reinforces the “lock-in” effect: homeowners who secured lower mortgage rates in earlier years are less inclined to move and more likely to invest in maintaining or upgrading their existing properties. An aging housing stock further supports this trend. With the median age of U.S. homes exceeding four decades, repair and maintenance are not optional but rather inevitable. Aging decks need reinforcement, fences require replacement sections, doors need rehanging, drywall requires patching, and exterior trim must be secured or replaced. All of these tasks are fastener intensive.

The median age of US homes has been over 4 decades.

In my view, repair and maintenance projects represent the most reliable demand engine for DIY fasteners in 2026. These are not discretionary lifestyle upgrades; they are functional necessities. Even in slower economic periods, homeowners continue to purchase wood screws, masonry anchors, corrosion-resistant exterior fasteners, and general hardware assortments to address structural or safety concerns. Small projects may not generate high ticket values, but collectively they produce steady unit volume.

Additionally, aging-in-place modifications are quietly expanding the demand base. As more homeowners adapt properties for long-term occupancy, installations such as grab bars, reinforced railings, and accessibility fixtures require secure anchoring into studs or masonry. These projects often require highergrade anchors and structural fasteners, supporting demand for more specialized fastening solutions. Even when professional contractors perform the installations, products frequently move through the same retail channels that serve DIY customers.

Tariff Pressure, Trade Policy, and Pricing Volatility

Outdoor living and exterior upgrades also remain important contributors. When budgets are constrained, homeowners often prioritize visible improvements with manageable scope, such as repairing decks, replacing fence boards, upgrading pergolas, or assembling sheds. Exterior work typically requires corrosion-resistant screws, galvanized nails, structural connectors, and weather-treated fasteners. Seasonal demand peaks are likely to persist, particularly in spring and summer, sustaining consistent movement through retail outlets.

Transaction-driven DIY demand may also provide incremental support. While existing-home sales are not projected to surge, modest improvements in inventory and transaction volume could trigger “move-in” projects. New homeowners frequently undertake quick installations such as shelving, curtain rods, storage systems, and minor hardware replacements. These seemingly minor tasks translate into high turnover for wall anchors, cabinet screws, and assorted fastener kits. Even a slight uptick in transactions can ripple through fastener aisles.

Overall, the remodeling and housing backdrop suggests that DIY fastener demand in 2026 is more likely to be steady-to-moderately positive rather than contractionary. Growth may be uneven, but the structural need for maintenance and small-scale upgrades provides a resilient foundation.

While underlying demand appears stable, tariff dynamics introduce complexity into the 2026 outlook. Fasteners are heavily steel-dependent, and U.S. trade policy continues to shape cost structures. Section 232 steel tariffs were increased in mid-2025 from 25% to 50% on covered steel articles and derivative products from most countries, with certain exceptions such as the United Kingdom. These tariffs apply to a broad range of steel items, including many fastener classifications within Chapter 73 of the tariff schedule.

In addition to Section 232 measures, Section 301 tariffs related to imports from China remain in force and continue to evolve through scheduled modifications. Layered onto these broad tariff frameworks are product-specific antidumping duty orders, such as those covering certain steel nails and threaded rod from China. Together, these measures affect sourcing strategies, landed costs, and supply chain decisions for importers and retailers.

For DIY fasteners, which are highly pricesensitive and often sold in competitive retail environments, tariff-driven cost fluctuations can quickly influence shelf prices. When input costs rise, retailers face the choice of absorbing margin pressure or passing increases to consumers. In a cautious consumer environment, higher prices may encourage project downsizing rather than outright cancellation. A homeowner might choose to repair a deck instead of replacing it or buy value-pack screws instead of premium coated options.

The greater risk in 2026 is not a collapse in demand but a lack of pricing stability.

maintaining core inventory availability

diversifying sourcing

communicating clearly about price drivers

From my perspective, the greater risk in 2026 is not a collapse in demand but a lack of pricing stability. Tariff changes, compliance complexities related to steel-content valuation, and potential shifts in trade remedies can produce short-term supply disruptions. Smaller importers and private-label programs may feel disproportionate strain, particularly if sourcing must pivot rapidly to alternative countries. Inventory cycles could become uneven, with periods of stock buildup followed by destocking as buyers adjust to cost changes. Tariff uncertainty also influences strategic planning. Long-term contracts become more difficult to price accurately, and annual purchasing cycles may require built-in contingencies. In such an environment, supply chain agility becomes a competitive advantage. Companies capable of diversifying sourcing, maintaining core inventory availability, and communicating clearly about price drivers are likely to outperform.

Taking all factors into account, the 2026 outlook for U.S. DIY fasteners can best be described as cautiously optimistic. The remodeling base remains large, repair activity is structurally supported by aging housing stock, and small-scale projects continue to resonate with homeowners navigating higher mortgage rates. Exterior upgrades, aging-in-place modifications, and move-in installations are likely to sustain volume across common fastener categories. However, optimism must be tempered by recognition of tariff-driven volatility. Elevated steel duties under Section 232, continuing Section 301 adjustments, and existing antidumping orders mean that pricing calm cannot be assumed. Demand may remain steady, but cost structures could shift unpredictably.

In practical terms, 2026 may be characterized by steady unit movement rather than dramatic expansion. Growth is likely to cluster in repair-oriented and safety-driven categories, while large discretionary remodel-related fastener demand may remain more sensitive to financing conditions. The winners in this environment will not necessarily be those chasing aggressive volume growth, but those maintaining product availability, cost discipline, and flexible sourcing strategies. Ultimately, fasteners benefit from an inherent advantage: they are indispensable. Homes require constant upkeep, and even modest improvement cycles translate into recurring fastener consumption. If homeowners continue to repair, reinforce, and refresh their living spaces, the baseline demand for DIY fasteners in the U.S. should remain fundamentally sound in 2026, even amid the ongoing uncertainty of global trade policy.

Copyright

owned by Fastener World / Article by Sabrina Rodriguez

American News

News provided by:

John Wolz, Editor of FIN (globalfastenernews.com)

Mike McNulty, FTI VP & Editor (www.fastenertech.com)

Optimas Solutions Opens in India

Optimas Solutions opened an office in India. “This expansion reflects our continued investment in our people and our commitment to global growth, while ensuring we deliver strong, localized support to our customers,” CEO Mike Tuffy said. The India office strengthens Optimas’ global footprint and enhances its ability to support customers with engineering expertise, supply chain efficiency, and operational excellence.

Illinois-based Optimas provides fasteners and c-class components and services to OEMs and Tier 1 suppliers in the automotive, agricultural, and medical equipment markets. Optimas has locations in 19 U.S. states plus Mexico, Europe and Asia/Pacific.

Bisco Industries Opens in Mexico

Bisco Industries opened in Chihuahua, Mexico. The office marks its 53rd global location. California-based Bisco distributes fasteners and electronic components, with 52 North American sales offices, one office in Asia, and seven distribution centers. The National-Precision division sells electronic hardware and commercial fasteners to OEMs in the aerospace, fabrication and industrial equipment industries. The Fast-Cor division distributes fasteners and components exclusively to distributors.

Foley’s STAFDA Highlight: One-on-One With Reagan

After 31 years with the Specialty Tools & Fasteners Distributors Association, including 26 as CEO, one of Georgia Foley’s favorite STAFDA memories was an event prior to her first full-time job with the association. In 1990 Foley was managing another association when her father, Morrie Halvorsen, STAFDA’s first executive director, left her alone in the green room with the keynote speaker – former U.S. president Ronald Reagan.

“He had just come out of office,” Foley recalled. While Reagan had tea and honey before going on stage, the two talked “about bees, nature and other generalities. He was the nicest, most congenial man and you’d never know he was the immediate past president of the United States. We laughed and had a delightful conversation.”

Foley subsequently was hired by STAFDA and was promoted to CEO upon Halvorsen’s retirement.

Beginning in 2026, STAFDA will be managed by Frontline Co., an Illinois-based association management company. With all the member company consolidations, what will trade associations look like in a decade? “We’ll all have to pull together in order to survive,” Foley suggested.

“No doubt about it. Associations continue to have an important role, but we too need to consolidate, at least on shows and joint programs,” Foley said. Foley described the 1,900-member STAFDA as “a relationship organization” and said it “will continue to be so.’

Fastenal finished 2025 with double-digit fastener sales growth in December, closing a year in which the company’s legacy fastener sales recovered after nearly two years of declines. Fastener sales rose 10.8% to USD 186.14 million (29.6% of overall sales) in December, down from 14.6% growth in November. Fastenal has reported double-digit fastener sales gains since July.

During the fourth quarter of 2025, fastener sales gained 12.6% to USD 614.3 million (30.3% of overall sales). Direct products outpaced indirect products due to greater contribution in fastener sales from increased sales to manufacturing customers. Overall Q4 sales grew 11.1% to USD 2.03 billion, with operating income up 11.4% to USD 384.3 million and net income gaining 12.2% to USD 294.1 million.

Full-year sales rose 8.7% to USD 8.2 billion, with operating income increasing 9.6% to USD 1.65 billion and net income improving 9.4% to USD 1.26 billion. Sales were boosted by higher pricing. Meanwhile, 26% of participants reported slower supplier lead times/deliveries (up from 13% in November), though the majority (69%) continue to indicate similar levels. Lastly, 17% of respondents said customer inventories were “too high,” compared to just 3% in November.

Fastenal Announces CEO Transition

Fastenal announced that Daniel L. Florness decided to step out of his role as Chief Executive Officer (CEO) of Fastenal on July 16, 2026. On December 19, 2025, Fastenal’s Board appointed Jeffery M. Watts, Fastenal’s current President and Chief Sales Officer, to succeed Florness as CEO effective as of July 16, 2026.

“The Board of Directors would like to recognize Dan for his impressive 30 years of service to Fastenal and commend him on the shareholder value he has helped create while being CEO over the past 10 years,” said Scott Satterlee, Fastenal Board Chair. “This transition represents the next step in an orderly succession plan that began in August 2024, when Jeff Watts stepped into the role of President of Fastenal. There are the complete confidence of Dan and the entire Board for Jeff to be Fastenal’s next CEO to further lead with the cultural values Robert Kierlin and the Founders established decades ago.”

Florness will continue to serve Fastenal as a Strategic Advisor to the new Chief Executive Officer until early 2028. The Board intends to appoint Watts as a Director to fill the vacancy left by Florness.

Supply Technologies Building Ohio Center

Supply Technologies, a Park-Ohio Holdings Corp. company, announced it will build a 375,000 sq ft-North American distribution center in Ohio. Cleveland-based Supply Technologies has 70+ warehouses globally. The new facility will be their flagship location, with warehouse, quality, engineering services and an innovation center. The site will have more than 100 employees. Capital investment will exceed USD 20 million.

“The investments we are making in this facility include robotic automation, more advanced warehouse systems, and best in class equipment in our quality and engineering lab,” President Brian Norris said. Hiring will begin in early 2026, with the official opening targeted for July 1, 2026. Supply Technologies is a global supply chain management company for assembly components and fasteners.

Fastener Distributor Index Improves

The Fastener Distributor Index jumped to 56.4 in December 2025, reflecting improvement across most components of the FDI (sales, supplier deliveries, and customer inventories). The improvement marks the strongest FDI reading since before the 2024 U.S. presidential election.

Sales, supplier deliveries and customer inventories increased, while employment levels acted as a drag on the index. Although still growing, the employment index moderated to 52.9 (vs. 54.8 in November) as the share of participants noting levels “lower than seasonal norms” increased to 11% from 3%; however, the overwhelming majority (71%) still report employment is in line. Sales trends were particularly strong, with the index rising to 58.7 (compared to just 49.6 in November) and 43% of respondents reporting sales above seasonal norms (vs. 23% in November), exceeding the one-year average of 38%.

The Forward-Looking Indicator declined to 51.2 in December from 55.4 in November, driven by customer inventories (17% indicated “too high” versus only 3% the previous month), though the majority of respondents say in-line (69%). Despite the headline sequential dip, the data suggests a stable six-month outlook, with 51% of respondents forecasting better trends six months from now (was 52% in November), which is higher than the 24-month average (43%). Just 14% forecast lower activity levels in six months, drifting slightly lower from 16% in November, with the remaining 34% anticipating stable momentum (vs. 32% in November).

The 2026 outlook skewed positive. “(2025 was) our best year to date. I expect the same type of activity in the new year,” one respondent wrote. On the tariff front, one respondent summarized the consensus view. “Tariffs suck.” Higher prices are serving as an offset to lower volumes in some cases. “Passing along round two of tariffs has been a challenge.”

Tariff confusion seems to be running even higher in Canada. “Total confusion with CBP on tariff calculations has led to uncertain pricing. Importers are starting to receive letters advising them of miscalculations when CBP did virtually nothing to clarify the 232 rules.” Another respondent noted: “Canada has hastily announced and will enforce a global 25% tariff on steel derivatives and specifically, all fasteners beginning Dec. 26th. Without any real domestic sources for most parts, this will have a dramatic increase on prices.”

RivetKing Wins Assembly Fastening Product of Year

Industrial Rivet & Fastener Co., also known as RivetKing, won Product of the Year in the fastening category at the Assembly trade show in 2025. The new MTC controller provides process control and data collection for the company’s full line of FreeSet cordless tools, including the RK-777C for blind rivets, RK-787C for rivet-nuts, and RK-797C for lock bolts.

“With the MTC controller, we can count the number of fasteners installed, and give guidance to assemblers when they need it to ensure that they’re not missing any fasteners,” engineering vice president Steven Sherman said. Sherman said there are new fasteners coming out that will bring RivetKing back into its legacy infrastructure applications. “We are developing lock bolts and structural fasteners for solar farms and AI data centers,” Sherman said.

Williams to Lead YFP

Zechariah Williams of Würth Industry USA was elected as the 2026 president of the Young Fastener Professionals. Nihar Sinha of AmeriSteel Fastener is vice president and Hristijan Georgievski of IFE Americas becomes immediate past president. Continuing on the YFP board are Craig Beaty of Beawest Fasteners, Jake Glaser of Sherex Fastening Solutions, and Mallory Nichols of Advance Components. Founded in 2014, YFP seeks to empower the next generation of fastener professionals through education, collaboration and networking.

LindFast Completes AZ Wire Acquisition

LindFast Solutions Group (LSG), a Nautic Partners portfolio company, announced the acquisition of AZ Wire & Cable, a MFG Partners company. CEO Mike Spencer said the acquisition marks “a defining moment for LSG. With AZ now part of our organization, we are combining two industry leaders to create a more diversified and scalable platform.” “The acquisition expands product breadth and cross sell capabilities, Spencer said.

AZ will continue to operate under its current leadership. Founded in 1988, AZ Wire & Cable is a master distributor of industrial, commercial, and specialty wire and cable, offering services including cutting, reeling, paralleling, striping, and coiling. The Illinoisbased company and eight locations in New York, North Carolina, Florida, Texas, Colorado, Arizona, California, and Oregon. Founded in 1983, Blaine, MN-based LSG is a master distributor of specialty fasteners. Nautic Partners acquired LSG in 2019 in partnership with management.

NEFCO Acquires STS Industrial

STS Industrial supplies fasteners, pipe, valves and fittings, gaskets, pipe supports and cutting tools to refinery and chemical facilities, oil and gas operators, industrial contractors, and manufacturing customers across the U.S. NEFCO CEO Matthew Gelles noted STS had “deep roots in the Gulf region, and their expertise and culture align directly with NEFCO’s focus on speed, service, and technical solutions for contractors.” STS Industrial will introduce NEFCO’s expanded product portfolio, SHARP fabrication capabilities, value-added services, and technologyenabled solutions to its customers.

Founded in 1981, Connecticut-based NEFCO is a family-run construction supply company with more than 20 East Coast and Midwest locations. The NEFCO Fastening Solutions division provides OEM inventory management.

Faspac Closes Fastap Screw Products

Fastap Screw Products parent company Faspac Inc. ceased operations after 41 years of business. Washington-based Faspac also closed the Screw Outfitters online store. “Over four decades ago, the principals of what would become Faspac offered an otherwise technically undistinguished screw product to contractors from a small store front contractor's supply in a suburb of Seattle, Wa. Although it might have looked like the average ‘self-tapping’ screw product of the time, its one distinguishing hallmark over other screw products, was its uncompromising quality in materials used in its design and manufacture.”

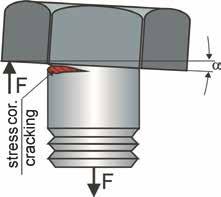

Five years later, the company relocated to California and was renamed Faspac, offering its product line as Fastap Self Tapping Screw Products. There they developed a new screw product named Fastap Plus Self-Tapping Exterior Grade Screws, with a special polymer coating Fastap trademarked as “Duracoat.” “This coating was common in automotive and aerospace manufacture and prized for its rust resistance while keeping the screw free from ‘hydrogen embrittlement’ (a problem with galvanized products), but unheard of in woodworking circles,” the company stated.

American Ring Celebrates 50 Years