HEROES green leaders in focus

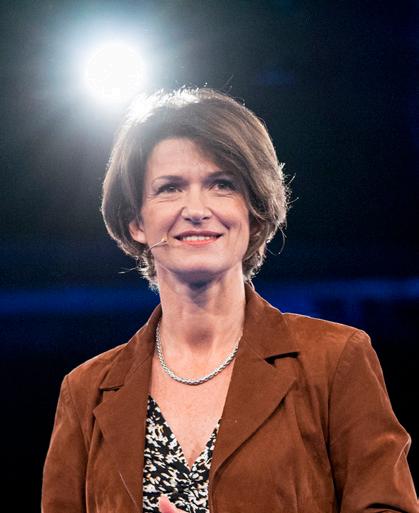

Isabelle Kocher

Turning green power on

Jean Rogers

Setting the standard

Nancy Pfund

Venture capital with impact

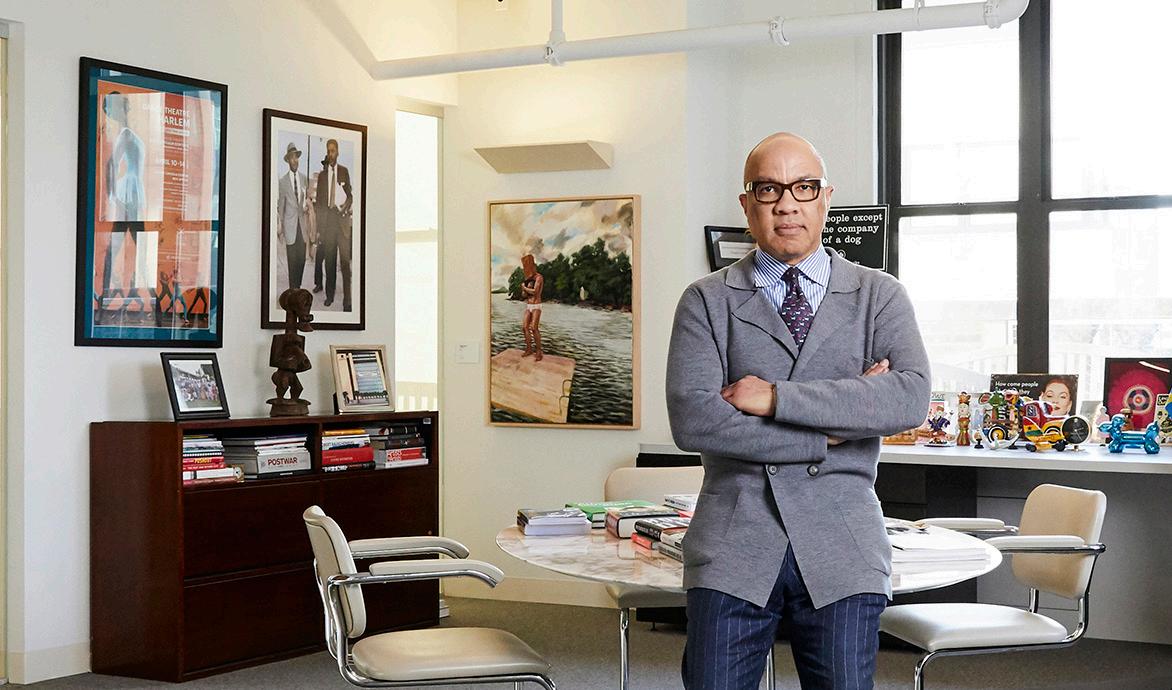

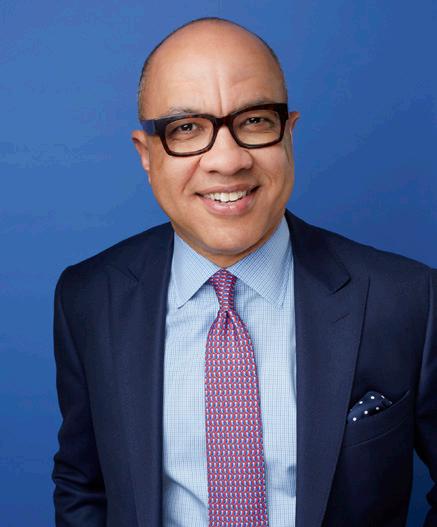

Darren Walker

Empowering the one

Rob Swan

Change in action

Editor:

Contributors:

Isabelle Kocher

Turning green power on

Jean Rogers

Setting the standard

Nancy Pfund

Venture capital with impact

Darren Walker

Empowering the one

Rob Swan

Change in action

Editor:

Contributors:

Following the positive reception of our inaugural edition, we are delighted to present the second issue of Greentech’s Sustainable Heroes magazine. We aim to engage readers with a community of heroes whose personal actions have inspired others, and who are quite simply changing the world in which we live.

In this issue, we pay homage to a corporate leader, an Arctic explorer, a highly admired policy builder, an innovative investor and an entrepreneurial foundation president - all of whom share the goal of creating a sustainable world that is more resilient as well as financially stable.

The edition includes a conversation with Isabelle Kocher, who serves as CEO of ENGIE, the largest electric utility company in Europe that is driving the sustainable transition.

We also interview Nancy Pfund, Founder and Managing Partner of DBL Partners, a venture capital firm whose goal is to combine top-tier financial returns with meaningful social and environmental returns.

We speak to the founder of the Sustainability Accounting Standards Board, Jean Rogers, whose organization aims to make capital markets more efficient by bringing clarity and transparency to sustainability reporting.

With Darren Walker, one of Time Magazine’s 100 Most Influential People in the World and President of the Ford Foundation, we discuss his stewardship of a $13 billion endowment. Darren shares his refreshing perspective on the challenges of being courageous in the face of systems that reward self-centered short-termism.

Lastly, we speak with Robert Swan, the first

person to walk both of Earth’s poles and the leader of the first expedition to the South Pole to use only renewable energy.

We don’t inherit our world from our ancestors, but borrow it from our children. So a forward-looking perspective ought to permeate our thinking and actions, guiding us as individuals, corporations, organizations, and nations. We must seek maximum positive impact – to create a sustainable world and legacies worthwhile for our children.

We encourage you on your own quest for ways to innovate, embrace sustainability and do the right thing. Become a heroine or hero to others and help us together solve the problems threatening our very survival.

To each of you heroes and heroines, there is a brighter, more sustainable future that we can build together for future generations.

It can be done!

On behalf of the entire Greentech family

P.S. We welcome nominations for people you’d like to see featured in future editions. Please send your nominations and other comments to eschaerer@ greentechcapital.com

Since assuming her position as CEO, Isabelle Kocher has truly walked the talk and positioned ENGIE as a major player in driving the sustainable energy transition forward for decades to come.

You chair the Terrawatt Initiative to reach 2.5 terawatts of renewable power by 2025. What were the main drivers behind it?

Behind this initiative, there is a paradox: political mobilization around the energy transition is increasing, clean technologies are becoming mature and capital is available. However, investments in renewables in emerging and developing countries are still too slow.

We are still a long way from what is needed to reach a two-degree Celsius scenario. To keep up with the objectives of the fight against global warming will require 15 to 20 times more investments in renewable energies in these regions of the world.

That is why it is urgent to speed things up and to remove all the barriers to mass usage of clean technologies.

Which barriers are you referring to?

First, there is the regulatory framework. It is a fact that investors are reluctant to invest in areas where regulation is uncertain and where guarantees are inadequate. Second, investors are still

Isabelle Kocher

showing little interest in small-size projects such as micro-grids. However, these projects will be an important way of structuring the electrification of isolated areas in Africa and Asia. ENGIE launched the Terrawatt Initiative project in 2015 at the COP 21 in Paris to overcome these barriers and structure the market.

The Terrawatt Initiative will soon set up a platform to link all the key stakeholders within a framework agreed on by the member countries to satisfy public needs for renewable energies. This platform, which targets 20GW of installed solar capacity, will, in particular, aggregate demand and help countries establish a common legal purchasing framework and mutual guarantees (the Common Risk Mitigation Mechanism). It will also improve the flow of information between market actors, and structure attractive guaranteed investment products for private institutional investors.

This platform can become the benchmark, the Amazon of all the infrastructure and assets of the green economy, and thereby allow mass

investments in these technologies.

As CEO of ENGIE, what do you see as the biggest challenges in driving sustainability initiatives?

As the CEO of a company leading the energy transition, I am often confronted with contradictory injunctions from investors. On the one hand, they demand that we adopt a strategy which is in keeping with the Paris Accord and is mindful of the environment. On the other hand, the very same investors have their eyes set on our quarterly results.

So my biggest challenge is to strike the right balance, where we are able to create value in the short term and still pave the way for the future and develop new, emerging business models.

And we are succeeding! Two years ago, we decided on a strategic pivot. This entailed selling 20% of our activities and focusing on those at the core of the energy transition: low-CO2

power generation, global networks, and customer solutions. We accepted that our company would shrink, and investors first expressed their surprise. Two years later, our organic growth has reached 5% per year and we have become much more profitable.

How important is it for corporations to have a sustainability strategy? What role should investors play?

We have to overcome the dichotomy between companies, which are seen as only preoccupied with profitability and economic growth, and NGOs and states, whose role is to make up for the deficiencies of corporations.

People aspire to a different model. For companies, it means that they have to implement much more ambitious corporate social responsibility policies and integrate CSR in their business offers.

People want companies to truly “walk the talk.” Tolerance for inconsistencies between words and actions – and greenwashing – has become extremely low among investors, employees, and clients. Companies have no choice other than to create a business model that is both economically viable and has a positive impact for society as a whole. That is the core of our strategy: we focus our efforts on goods and services that reconcile the common good with economic value, and contribute to more harmonious progress.

This choice was driven by our personal con-

victions, but it is also the right choice from an economic point of view: we have become much more attractive, and regained market share.

In the “new energy” environment, with the rise of distributed generation and new technologies such as blockchain, energy storage, and demand response solutions, what does the future utility model look like?

I usually talk about a 3D world to describe the future of energy. The 3Ds are: decarbonization, decentralization, and digitalization. In this world, low-carbon energy sources will become the norm. Instead of relying on big power plants for the supply of energy, we will see more and more consumers produce their own energy – by installing rooftop solar PV, for instance. Besides, decentralized systems, such as mini-grids or solar home systems, will play an essential role in the electrification of rural and remote areas in Asia and in Africa.

It is now a world of algorithms, software, Big Data, and the Internet of Things. In a world dominated by intermittent renewables, where it is increasingly difficult to balance supply and demand at every millisecond, you have to rely on data management and AI.

How important is collaboration between utilities and innovators? What initiatives at ENGIE are you most proud of?

Innovators bring agility and new ideas. Big companies bring experience, global support and connections.

We have a presence in 70 countries, with a portfolio of clients that is the biggest in the world. If a big group like ENGIE is able to combine the ability to innovate and to act with the support of a huge platform – that is to say, create an environment where you can innovate and bring that size, the sky is the limit.

Besides, now that we have a very clear purpose, we have become much more attractive to new talents and startups. Everywhere in the world, our teams receive many spontaneous proposals from startups.

What will we see next from you?

From Terrawatt, you can expect this new digital platform which will connect investors with the sponsors of renewable projects in emerging and developing countries.

At ENGIE, we are currently working on our strategic vision for the future, which we refer to as “ENGIE 2030.” We’re consulting experts both inside and outside of the company. We will share the results at the end of the year.

Dr. Jean Rogers is the founder of the Sustainability Accounting Standards Board (SASB). Established in 2011, SASB is an independent, private-sector standard-setting organization that aims to enhance the efficiency of the capital markets by fostering high-quality corporate disclosure of material sustainability information that meets investor needs.

SASB’s work is overseen by the SASB Foundation Board of Directors, which is led by Chair Emeritus Michael R. Bloomberg, the former mayor of New York City; Chair Robert K. Steel, the CEO of Perella Weinberg Partners, a global advisory and asset management firm; and Vice-Chair Mary Schapiro, the former Chair of the U.S. Securities and Exchange Commission. During its provisional standard-setting work, SASB engaged with more than 2,800 experts, representing $23.4 trillion in assets under management and more than $11 trillion of market capitalization. More recently, deep consultation on the provisional standards included 141 companies (representing $7.5 trillion of market cap) and 19 industry associations (representing hundreds of companies). Additionally, the SASB’s Investor Advisory Group (IAG) comprises 32 organizations, managing $26.2 trillion in assets, including BlackRock, CalPERS, CalSTRS, State Street Global Advisors, and others. Sustainability accounting standards for 79 industries across 11 sectors will be codified this summer for use by companies and their investors.

We laid out a blueprint in our 2010 report, From Transparency to Performance. It received an incredible level of investor interest, because for the first time sustainability issues were presented as business drivers and industry factors.

and gas companies, banks, and others. We designed our process to identify and validate the environmental, social, and governance factors most likely to have material financial impacts across every major sector of the economy.

What does “success” look like?

What inspired you to found the Sustainability Accounting Standards Board?

It was not a decision I took lightly; rather, it grew out of a long journey. I was helping international companies measure their environmental impacts, guiding them on how best to integrate sustainability into their strategy and operations. It became clear that firms were using varied metrics to address challenges unique to their own industry. So, I collaborated with researchers at Harvard University [Steve Lydenberg and David Wood, from the Kennedy School’s Initiative for Responsible Investment]. Our team conducted research by industry to see if the same metrics could be applied across the board, or if they needed to be industry-specific.

Steve Lydenberg argued that the work should not remain on the shelf, but needed to lay the foundation for an institution serving the capital markets in order to have the greatest impact. He suggested that we review the structure of the Financial Accounting Standards Board (FASB), and consider how a similar approach might be applied to sustainability information. Around the same time, an investor approached us to fund such an initiative. I had my doubts about how to start, but while I was driving home one day, I found myself behind a car with a “Be the Change” sticker on its bumper. That’s when I decided that if I wanted to see the potential of SASB realized, I had to take it forward.

We began by mapping issues to industries. While some issues are universally applicable, such as climate risk and human capital issues, others are rather unique to specific industries such as the distinct challenges faced by oil

What is unique about SASB is that, for the first time, capital markets have standards they can use to benchmark performance on material sustainability issues. Asset allocators can evaluate risks within a sustainability framework, characterize the nature of those risks, and price them accordingly. Analysts view these issues as quantifiable factors; as such, they can incorporate them into models and present them in a tangible way.

SASB finalized its first set of sustainability accounting standards for 79 industries in June 2017. We have been refining them based on market feedback since then. Naturally, they will continue to evolve as social and environmental issues are brought to the forefront.

Success will be reflected by the quality and accessibility of information – for example, having comparable, consistent, and reliable sustain-

ability fundamentals sitting right alongside financial fundamentals and being able to invest accordingly. After all, investors shouldn’t be spending their time gathering data, they should be evaluating it and using it to assess risk and identify opportunities.

SASB conducts significant research into how well companies are communicating their performance on sustainability issues in their investor filings. We conduct and publish an annual analysis of disclosure quality, and we anticipate a ramp-up now that standards are available.

How can we encourage companies to report more of this information?

It’s not so much about getting companies to report more information; it’s about getting them to report better information. It’s an issue of quality, not quantity. Contrary to popular belief, SASB wants the burden of reporting immaterial items to be reduced. Reporting well on a few material topics minimizes the need to provide information to investors in questionnaires and may also mitigate shareholder proposals, which is currently how this information changes hands.

Companies increasingly understand the materiality of these issues, and that investor demand is not abating. Investors are increasingly concerned about material environmental, social, and governance (ESG) factors, not just because they care about their environmental and social impacts, but because these factors provide crucial insight into how effectively a company is being managed to deliver longterm value.

Beyond the pure financial data, intangibles such as intellectual capital, brand value, overall footprint, and reputation are increasingly important components of corporate valuations. In addition, companies and their investors are exposed to risks from high-impact ESG-related events, such as safety incidents, ethics scandals, or natural resource shortages. Today, both asset owners and managers view ESG factors as a means of meeting or exceeding their return targets while managing risks and opportunities more holistically.

As a direct consequence, SASB has witnessed a significant market shift in the past 18-24

months - from primarily sustainability-focused investors caring about these issues, to mainstream investors adopting this approach. For example, Vanguard, Fidelity, State Street, BlackRock, and others have become more vocal about the importance of ESG, including through their proxy voting, their direct engagement with portfolio companies, and by sending open letters to corporate boards and executives.

SASB’s work is as much a response to these trends as it is a cause of them, but our efforts and those of investors have evolved side by side in a mutually supportive way. Both institutional investors and some retail investors now view these issues as critical indicators of a company’s ability to create value over the long term. As a result, they not only have a desire to see these factors reflected in their portfolios, they believe it is part of their fiduciary responsibility to do so. SASB provides the infrastructure to make those objectives actionable.

How is SASB getting investors to insist on more—or, should we say, better—reporting on these issues?

The investors are the ones really driving this, so we don’t exactly have to twist their arms. They continue to put pressure on their portfolio companies more or less regardless of what SASB does. But they do support us and we’ll continue to engage with them as we move forward.

The standards will be codified and ready for use this summer, after which we expect to see them incorporated into the next cycle of financial reporting. If our due process is as good as we believe it is, and our standards therefore hit financial materiality spot-on, there should be no issue with market uptake, because investors and companies intrinsically care about financial materiality.

We anticipate this will drive competition and improve performance. Although SASB doesn’t define what “good” or “bad” performance looks like on an issue, investors have their own strong opinions and that’s their role –demanding more effective disclosure so that they can better evaluate performance.

That said, we do encourage investors to be more vocal with the SEC. They have a right to

material information, regardless of whether it is financial data or sustainability data. In the U.S. — as in many other countries — we don’t need any new legislation or regulation for this to happen, as there is already a law in place requiring the disclosure of material information. Rather, we need support and moral persuasion. Overall, it’s encouraging to see the SEC’s commitment to better understanding the materiality of these issues, and its support for a close collaboration with SASB.

Speaking of international markets, corporate culture certainly plays an important role in sustainability disclosure. For example, European companies tend to disclose more useful information and do so voluntarily, whereas U.S. companies tend to be more skeptical. However, SASB is designed for this, because everyone can agree on financial materiality.

There is a multitude of standards and metrics. How does SASB fit in with the others and what are its unique benefits?

SASB is the only framework focused solely on the needs of investors – specifically the need for financially material, decision-useful information on industry-specific sustainability factors. Other initiatives, such as the Global Reporting Initiative (GRI), tend to focus on a broader set of stakeholders and thus a broader set of issues. These are complementary efforts, of course, and we work alongside and directly with multiple groups seeking to advance corporate disclosure on sustainability

issues – including GRI, the Climate Disclosure Standards Board (CDSB), the International Integrated Reporting Council (IIRC), the Task Force on Climate-Related Financial Disclosures (TCFD), and CDP, among others.

It’s fair to say that SASB does not cover everything – our focus on financial materiality is only one piece of the sustainability reporting puzzle. And we recognize that the proliferation of reporting frameworks has created a measure of confusion in the marketplace. We’re committed to improving our alignment with other approaches, better communicating our key differences, and furthering best practices in reporting for the benefit of both companies and investors.

The truly unique benefit of SASB is that by focusing on financial materiality, the standards help corporations better manage the subset of sustainability factors that will enable them to achieve the biggest net impact for both their shareholders and for society. It’s a win-win.

Can these standards be applied and expanded internationally?

Absolutely. The idea that the standards are only relevant to U.S. companies is a misconception. SASB’s standard-setting process is guided by the U.S. Supreme Court’s definition of materiality and the standards are designed to work within the U.S. disclosure regime. However, our process is intended to surface issues that are globally applicable and to es-

tablish performance metrics that will be globally comparable. This is because both U.S. and non-U.S. companies access capital in the U.S. markets and are subject to SEC reporting requirements. Despite potential geographic variations, we certainly attract significant interest from the international investment community, because the standards are industry-specific, not region-specific.

What will we see next from SASB, and what do you see as key milestones?

SASB will finish defining its standards this year [2018], and companies will then begin to integrate the framework into their filings. As a result, there will be more specific acknowledgment of the materiality of these issues by industry, and more effective disclosure surrounding them, particularly as more companies integrate sustainability into their enterprise risk management processes and more controls are put in place.

Key milestones will be defined by improvements in the quality of ESG disclosure over time. The baseline has already been established. Our analysis of 2016 filings revealed that most companies already address most SASB disclosure topics in their SEC filings. In fact, about three-quarters of companies disclose information on at least three-quarters of the issues we cover. However, more than 50 percent of those disclosures consist of meaningless, boilerplate language. Once the standards are codified and implemented by companies, we will re-evaluate and see how the quality of disclosure has improved.

In the meantime, SASB will continue its regular cycle of maintenance to ensure the standards remain relevant and responsive to the most important sustainability factors. Our ongoing due process will continue to involve internal research, external outreach, technical agenda-setting, public comment, and transparent oversight.

We understand you are stepping down as the Chair. What will we see next from you?

I’m proud of what SASB has accomplished as an organization and grateful for the market support we have earned. After seven years of sometimes grueling but always rewarding work, we are finally moving into the imple-

mentation phase – corporations integrating sustainability into existing systems of risk management, control, performance measurement, reporting, assurance, and more. It’s a new chapter for SASB.

I have passed the reins to Jeff Hales, previously our Vice-Chair. Jeff is an accounting professor with an impressive financial and management accounting background who has worked with SASB for the last six years. He is the perfect person to carry this work forward as SASB faces the technical rigor of working with companies on implementation.

After taking some time with my family this summer, I will be focusing on my roots in sustainable development and green finance, continuing to inspire and be inspired by what’s possible when passion and ingenuity come together to move markets. I’m excited for what’s next, but I will always be a stakeholder in SASB’s success. After all, I’m an investor, too.

Who is your personal sustainable hero and why?

My heroes are Justice Louis Brandeis, because of his advocacy for both transparency and the right to privacy depending on the situation, and Madonna, who recognized that we are living in a material world about two decades before me.

Nancy Pfund is Founder and Managing Partner of DBL Partners, a double bottom line venture capital firm, which strives to combine top-tier financial returns with meaningful social and environmental returns. She is an early investor in Tesla, SpaceX and SolarCity.

My first major sustainability investing effort took place back in 2004 when I was a Managing Director in J.P. Morgan’s San Francisco office. It was a small regional fund with outside LPs. We later spun out of J.P. Morgan in 2008 to create DBL Investors and took this fund with us.

I did not consider myself the entrepreneur type. I had worked at J.P. Morgan and its predecessor firm Hambrecht & Quist for nearly 25 years and was happy to marry my interests of venture capital and sustainability in that first fund. The ambition was to raise a second fund, but 2008 wasn’t the right time. Many portfolios were hurting, including ours at the time, so we postponed our second fund for another year. Having just spun out of J.P. Morgan in January of 2008, it was not exactly smooth sailing because of all of the fallout from the financial crisis. But we hung in there and never looked back!

DBL Partners was founded in 2015, through the combination of DBL Investors and the cleantech practice of Technology Partners. We saw increased momentum in cleantech, and in some aspects it was a dream come true – the firm’s identity was 100% aligned with impact and sustainability, we had more horsepower combining the two practices, and we had the ability to help move the world forward in a positive way, more quickly with a larger platform.

Can you share some insights on DBL’s investment in Tesla? What was your thinking around EVs back then?

It was one of the earlier investments of the 2004-vintage fund; we invested in early 2006. But it wasn’t our first sustainability investment. PowerLight was the first, which soon began preparing for

an IPO after our investment but got acquired by SunPower and is now the installation side of SunPower.

The Tesla investment reflected the mission of our fund – to promote sustainability. But it did more. As a “double bottom line” fund, one of our scoring metrics was whether or not we could help to create quality jobs in the Bay Area. Not just jobs for tech engineers and coders, but for a diverse hiring base, including lower-income earners. We were introduced to JB Straubel (Tesla CTO and co-founder) through a professor at Stanford, and were impressed by the Tesla vision and team. We had just started to think about electric vehicles ourselves and how they could transform the automotive industry. And with the Toyota NUUMI plant (now the Tesla plant) in Fremont struggling at the time, we felt there was a big gap for Tesla to fill, both on a climate and jobs level.

VantagePoint ultimately led the first institutional round, and DBL joined it. We had no prior experience with investing in car companies (who did?!), but we could bring our sustainability understanding and job orientation to the investment approach.

Did you ever imagine back then that Tesla could become this successful?

When you enter into an investment, you always

think it will be successful. However, Tesla, like so many other companies, had many neardeath experiences on its way to success, and so there were moments of doubt. It’s not easy to have to rebuild the automobile and the automotive supply chain from fossil to electric. We felt our investment had some downside protection even if the Roadster (the two-seater sports car) ended up being the only car built. We modeled that if that happened, we could sell the company to a luxury sports car manufacturer. Still, we never let go of the “big idea” that Tesla would redefine transportation to meet 21st century needs and become a hugely successful investment. We also thought it could create a ton of jobs, so we kept the faith!

Looking back on the cleantech and sustainable investing boom-bust cycle over the past 10 years, what observations can you share as an investor?

It has almost been a perfect storm in the past 10 years, starting with strong momentum in 2004-2006, and then the big crash in 2008. In its aftermath, we saw unstable financial markets, technology delays, and the politicization of renewable energy that weighed on the sector and lasted for years, with federal inquiries and bad press.

At DBL, the bumps were not as severe and the sale of Powerlight to SunPower got us off to

a good start. The momentum continued in 2010 with the IPO of Tesla and in 2012 with the IPO of SolarCity. We saw that the negativity had changed. While it never completely disappeared, we knew sustainability would begin to dominate popular opinion. We started to see growth in renewables generation capacity. U.S. job creation from the rooftop and commercial solar industry was just what the doctor ordered in terms of recovery from 2008, when many jobs were lost. There were headwinds, but the tailwinds were far stronger. Public understanding and acceptance grew, and we now started to really see that these businesses could achieve scale.

What sectors in sustainability are hot? What should we look out for?

DBL takes a very broad view on sustainability – we follow the carbon, and that takes us to many different places. We focus on areas where carbon generation is high, and where there is a problem that is not being solved by incumbents.

The era of cheap, stationary energy storage changes everything: It makes energy efficiency better, allows for monetization of assets, and makes renewables more useful. Customers can optimize their load for a variety of purposes, in real time with real information, in a way that supports the utility’s goals as well, as never before. Integrators like Advanced Microgrid Solutions are accelerating growth and carving out a strong place in the electricity ecosystem. It’s revolutionary.

We also see massive opportunity for storage in the developing world, including Africa. With over 600 million people lacking access to electricity there, Africa is a wide-open playing field. We can allow residents to skip traditional generation adoption and go straight to renewable power through distributed generation and energy storage – this is a trillion-dollar opportunity for the continent. We see increased collaboration, from Silicon Valley tech companies to local installation and marketing teams, and now also local VCs and other investors from Africa, helping these companies grow. It is an African business revolution, rather than one being imported from abroad. In an interesting twist, we may see some of the more advanced solar-and-storage advances succeed in Senegal first, rather than Sacramento. The shift will happen faster there since no incumbents are in place, and the technologies are cheaper

to deploy. We’ll see new advanced grid technologies and rooftop structures, with high functionality, scaling rapidly in these regions, regions where for many, they least expect it. People will respond with a “Wow!”

Agriculture is another hot sector. It creates over 30% of the world’s carbon. Leaders such as Cargill, Monsanto, John Deere, Syngenta, are the iconic names, but there is a real opportunity to bring new companies into this multi-trillion dollar market and create an agricultural system that meets 21st century sustainability needs as well as farmers’ needs. We see increased focus on farmer empowerment – for example, Farmers Business Network, one of our portfolio companies, allows farmers to make better decisions relying on Big Data for inputs such as weather, seed, and soil type. As Earth’s population is expected to reach 9bn, we need a healthy agricultural and farmer compensation system to feed everyone. Big Data levels the playing field for farmers visà-vis their vendors driving more resource efficiency. This is not just good news for the farmers, but also for our planet.

Other areas of interest include space tools that help us understand our planet. Before you follow the carbon, you have to find it! Technology companies that use analytics, images, intelligent mapping, nanosatellites, etc. are making a tremendous difference in how we interact with space to make life better here on earth – look at natural resource tracking and autonomous driving, for example.

We also focus on the circular economy. For example, we invested in The RealReal, a company which authenticates luxury goods sales online. It provides access to used luxury goods at a lower price for consumers, but also provides multiple lifecycles of a product for the designers. This is a huge problem for the fashion industry today that The RealReal helps to solve. We also like companies that find a way to monetize conservation: today, most of the big names in conservation today are non-profits. We aim to balance that with for-profit companies entering the picture. We’ve got to do this because conservation has a huge role to play in storing carbon and keeping it in the ground.

What are the biggest hurdles that early cleantech companies must overcome to be successful?

When investing in embryonic companies, it is more about the tenacity, the leadership of management teams and the team’s ability to inspire. It is all about the people and the culture. I am often asked, “Would you rather have an A+ management team with a B+ product or vice versa? Obviously I would rather have both be an A+, but I would pick the A+ management team if I only had one option – this is what gets you through the difficult times of an early-stage company. Technology always evolves anyway, especially as you continue to scale, so the product you first invest in morphs many times along the way. It is the strength of management teams that allows this to happen in a constructive manner.

For sustainable companies, we need to add another layer of assessment when we invest: We need to understand the regulatory mix, and determine a strategy where you win more than you lose. It’s part of the process, not something to run away from. This is what makes this sector so much fun!

How has the investor landscape changed? Is a lot of competition making it harder to get into rounds?

The cleantech investing syndicate has changed in the past couple of years, which is very exciting. Post dot.com bust, 2003-2006, we saw a lot of “tech investor tourists” who were looking for other hot sectors to invest in. This had positive effects in growing the field, but also negative ones because once the tech sector rebounded many of those investors left.

Today, we have a healthy ecosystem of investors:

Utility funds, utilities, international energy companies have started to come in, recognizing that they can help shape the future rather than just react to it;

• Foundations, family offices, and impact investors who are really out to reorient business activity toward a more sustainable future, looking to both private and public equities as well as debt markets; and,

• New cleantech funds whose founders have been through the early days and have a seasoned perspective.

All of these are very encouraging developments to see.

If you had a crystal ball, what would you expect to see 10 years from now?

We’ll see a big push towards a cleaner energy system and a move toward the electrification of everything. More renewables and use of storage will be the rule, not the exception. Electrical vehicles will become omnipresent. Countries with no grid or unreliable electricity will go straight to clean distributed energy and derive significant economic and social benefits.

Overall, I am very bullish on clean energy across all sectors. In the past, even in the recent past, we did not always see where the “cost” met the “cause.” Today costs are coming down and clean solutions are becoming more competitive; everything is coming into alignment. The public wants clean energy – this is not a partisan issue, people are voting with their investment portfolios and with their utility bills regardless of their political persuasion. We have needs we never could have predicted in the 20th century, and we will now start to reward companies that solve for these needs. These companies will create jobs for the next generation that go beyond providing paycheck to providing purpose and the peace of mind that comes from leaving the world a better place than you found it.

What about women in energy?

One of the things I get asked a lot is, “What is the role of women in clean energy?” As a clean energy professional, I am heartened by the increase in participation of women over the past 10 years. It’s been very visible across the board, including public advocates, government, public companies, funds, investors, utilities, start-ups, etc. We need everyone to work together to build a clean energy future. And that future will be brighter with a more diverse and representative workforce building it.

Who is your sustainable hero and why?

I have thousands of sustainable heroes. They are women and men who get up every morning and work to create a future that we all can thrive in and that nurtures our planet. They do this sometimes in the face of opposition, criticism, and the entrenchment of the status quo. And yet, they keep going, envisioning a better future and making it happen. These are my heroes. Some of them are famous. All of them are fierce!

We spoke with Darren Walker, President of the Ford Foundation, whose relenteless drive to stay relevant pioneered a way that successfully incorporates both social and financial returns.

How do you see the role of corporations and decision-makers in driving change?

The question of how we get companies to be forthcoming about material issues that impact climate and the environment, is hard. We need a lot of external pressure. I see it from the corporate board perspective; unless real pressure is put on companies, about recycling for example, change does not happen.

Making companies accountable on these issues is really critical, and this accountability will not be generated internally. It’s not because we are bad guys, it’s because the incentives work against us. The question is, how do we standardize SASB-like reporting requirements so that everyone will be accountable through the same lens? And then, how do we culturally value those companies that are doing the right thing – the torch bearers for corporate responsibility?

The real challenge is that market incentives work against CEOs. “Short-termism” is one of those. Making that a commitment is important for a more peaceful and prosperous world. Otherwise, everything will be at risk if we don’t change. The consequences of inaction may not be felt in the near term, but they will absolutely be felt in the future. That is an incontrovertible fact. As leaders, are we able to rise to the occasion for something we know to be a fact? Whether you are the head of a foundation or the CEO of a public company, it can be very difficult to be courageous, because the incentives often discourage courage.

Depending on the sector you’re in, you can be really vulnerable

by taking that courageous path. You are disincentivized by activist investors who think you are destroying value in some way in the near term, although we know that in the long term you are increasing value. To do what you want as a CEO is going to take really courageous leadership.

Darren Walker

You’ve taken an interesting career path, from lawyer to investment banker to philanthropist. What inspires your work?

Having a mission-centered life is very important to me. That mission, quite candidly, has evolved over time. When you grow up the way I did, one of the things you have as a mission is to never be poor. When I was in college, my mission was to be able to do the things that I would like to do. And so for me, when going to Wall Street, I had a mission to attain some level of financial security that would allow me to have the freedom to do what I wanted in the long term.

I always knew that my passion was not law – and my passion was definitely not collater-

alized mortgage obligations and securitizing credit card receivables. But, there are really positive externalities of being able to do those kinds of financings, in addition to the personal resources you are able to accumulate as a result. I knew that ultimately I wanted to do something that would have, as its highest objective, a social mission. When I was able to leave Wall Street after 10 years, I took a year off to figure out what I wanted to do in the social sector.

I had always been attracted to Harlem, in part because I read the Harlem Renaissance writers – Langston Hughes, Zora Neale Hurston and Countee Cullen. All of these writers in the 1910s, 1920s, 1930s would write about Harlem, and I was mesmerized by the idea of this place being the cultural capital for African Americans. But, of course, when I moved to New York in 1985, Harlem was not exactly an alluring place to live. In fact, most people saw it as a place you wanted to avoid, which is hard to believe in 2018, given the price of real estate today and how much the community has changed. But in the early- to mid-1990s, Har-

lem was a really tough place. When I got there I ran a community development organization, the Abyssinian Development Corporation. At the time Harlem had literally hundreds of buildings that were burnt out and abandoned, which the city owned through tax foreclosure. The organization was founded by Calvin Butts, a prominent African American minister, and I became COO and really his right hand.

What I loved about going to Harlem was that I was able to take my skills from Wall Street and apply them to a purely social objective. I understood project finance, I just had never financed low-income housing. I understood, I just had never developed a balance sheet for a supermarket on 125th street that would serve a primarily low-income population. It was great to be able to use my skills and whatever technical knowledge I had developed about the markets and finance to really build out this strategy for the redevelopment of Central Harlem, which we did.

Over eight years, we financed over 1,000 units of housing, and initiated the first big commercial retail project on 125th Street. Sometimes I worry that we were too successful. We didn’t know what happens when you make early investments that are socially focused, particularly around helping low-income people and the marginalized. We then saw the snowball effect and the aggregation of momentum, and all-of-a sudden 10 years later you have people from all over the world moving in, buying brownstones and turning Harlem into a chic and fabulous neighborhood.

What has changed at the Ford Foundation from when you started, leading to last year’s announcement of $1bn for mission-related investments?

I started at the Ford Foundation in 2010 as Vice President, and was promoted in 2013. I took over a prominent and esteemed legacy institution that had been around for eight decades with a record of impact on significant social issues, whether poverty or women’s rights or human rights or micro finance.

Although the foundation is identified with an arc of social progress in the 20th century, as with other legacy institutions, you are challenged to think about how you can have an impact and how you remain relevant in the future. Just because you were an industry leader over the last 80 years, even in a sector like philanthropy, it does not mean that your relevance will remain – certainly not, because there are so many newly minted billionaires who are starting their own foundations and who aspire to be a Ford or Rockefeller or Carnegie.

We had to really interrogate the DNA of the foundation, and find our way as we looked into the future. We determined that the biggest threat to our mission of a more peaceful world, a world where there is more opportunity and mobility, is the issue of growing inequality.

We decided we could have the most impact by focusing on inequality in all its forms: political, economic, and social inequalities. We looked at all of our assets and asked ourselves, how

are we using them to address and reduce inequality? The singular focus to generate alpha is not defensible. As a $13bn endowment and a social justice foundation, we have to deploy our capital towards a social objective. We need to go further and ask whether the portfolio performs against a set of social objectives as well as financial objectives.

That’s why last year we made the commitment of $1bn for mission-related investments. I think the trustees believed in my view of the future. If you’re going to invest in affordable housing, for example, you need to look at preservation of affordable housing, at the profiles of the kinds of people who are in those places, and strategically target particular cities, and even particular neighborhoods, to mitigate gentrification. So we are now looking at deploying capital to demonstrate the efficacy of the idea.

How else will you measure your impact?

For the financial assets, we have a set of very clear objectives around alpha that we expect to deliver on. We have a great CIO, we outperform the benchmarks, and we’re very proud and pleased about that.

We have a big footprint, so for example, right now we are renovating one of the great modern landmarks in New York City, the Ford Building, that Henry Ford II commissioned in the early 1960s. It’s a marvel of a building, but it’s not very energy-efficient. We have reimagined the building and are seeking to make it far more efficient and environmentally sustainable. We are thinking about our footprint at all 10 of our offices around the world in this same way. In Mexico City, for example, we’re moving from an old energy-inefficient building to a new green building. With our portfolio of physical assets, we’re putting in place a set of objectives as leases expire and moving to buildings that are absolutely environmentally sustainable and take us on different path.

You’ve talked about the need to bridge the gap between philanthropic impact and investments. How do we do that and what role do endowments have?

I hope other endowments see that strategies incorporating both social and financial returns are the way forward. We’ll do the pioneering

work to demonstrate the efficacy of that idea, because I think there are some in the market who simply refuse to believe that it is possible or that we should even try. There was a large foundation that had a strategy of seeking alpha (and a lot of the big foundations do), and they found they were providing grants to improve the public health of people on a river in Africa, and at the same time investing in one of the biggest polluters of that river.

There can be a stark difference between our rhetoric and what we actually do – our actual behavior. I believe that we cannot have a rhetoric of improving the climate and reducing inequality and poverty, and then have our investment behavior actually contribute to a poorer climate, more inequality, more poverty. We cannot reconcile that. And I think it is especially problematic for a foundation.

The incentives for public entities are driving in the right direction with ESG standards. For privates, I think it’s a lot harder. That is why I have encouraged, for example, TPG Rise and firms like KKR to think about how we can all network around learning platforms. I am encouraging all of us in the private space to involve senior people in developing a shared set of metrics, language and standards.

In an era of “digitization,” what technology do you think will have the biggest impact on society in the coming years?

What is happening with AI and machine learning is both exciting and frightening, depending on where you sit. For those of us in places like Greentech and Ford and TPG, technology offers a tremendous opportunity for more knowledge, to develop ideas that we never thought were possible, to help us imagine a future where the world is more connected. But it also is very problematic if you think about issues like data security, privacy, the degree to which a few large companies monopolize most of the infrastructure of the web, and the implications of that. For a capitalist like me, I like a lot of competition; so I do worry about the lack of competition and the degree to which markets are completely captured by one or two companies.

As a social justice foundation, we’re going to leverage technology by investing in technology for social good: Organizations building a

public-interest technology infrastructure, for instance, or ensuring that more low-income students have a chance to go to engineering schools, and learn how to code and prepare themselves for a digital world.

The future of work will look different. But as a foundation with our mission, we’re more concerned about ensuring that there is work. Work is essential for human dignity. We are not seeking huge transformational technology interventions – we are more focused on what’s going on out there, and how it impacts the lives of poor people and poor communities. Are we increasing inequality, and making these communities more vulnerable? How do we make them less vulnerable, more resilient in the face of what clearly is going to be transformational change?

What will we see next from you and the Ford Foundation?

We realize that none of the things we would like to achieve in this world can be achieved by working alone. So we see working with the private sector as an essential part of our success. That is a metric I am holding for myself, and that my board is holding me accountable for. Not just because we want to, but because we believe solutions will be generated through partnership with the private sector at a more accelerated rate than our working by ourselves. That way you will see some bold and creative partnerships with the private sector. We can help set tables of unusual stakeholders, from private and public and government, from the Kochs to George Soros and everyone in between.

There of course has to be some degree of inequality in the world. We should have differentiated compensation for different categories of employment; we should have incentives that encourage people to take risk and therefore be rewarded for risk-taking; we need systems that support innovation. As a capitalist, I am all-in on the idea that markets have to work, but they have to work for more people. They have to deliver shared prosperity, or we as Americans will become more cynical about our economy, about our institutions, and ultimately about our society. So for me, this notion of

the markets is not just a matter of finance, the issue of inequality is not just a matter of economics, it really is foundational to who we are as a people and what kind of society we want to live in.

I believe that people like me – those of us who had modest beginnings, but were provided with the opportunity to get on that mobility escalator, and with commitment, hard work, drive, and ambition, to ride it and ride it very far – that narrative, which is a uniquely American narrative, has to be sustained in the future. Because if that mobility escalator slows down or stops, I really question whether our democracy has a future. I am an optimistic capitalist, and it is our job at the Ford Foundation to demonstrate that we can reduce inequality in the world and have prosperity and strengthen our democracy in the process.

Opportunity correlates with inequality; the more inequality there is, the less opportunity there will be. We believe that education is important, and yet we make education more expensive. The same piece of legislation gives some of us, including me, a huge tax break, while at the same time it reduces grants and privatizes the student loan program, which we know empirically it makes a big difference; not for our own kids, because our kids don’t need those programs, but for the kids we used to be.

So if we care about those kids we used to be, with the hopes and dreams we used to have of ending up in the place we have ended up now, then into the future, we have to have policies that speak to them. If that narrative atrophies, the implications for our country are really grave.

Who is your sustainable hero and why?

My sustainable hero is Berta Caceres for the devotion and courage she exhibited in advocating for environmental justice in her community.

Robert Swan walked to the ends of the earth to increase public awareness of the environmental changes and believes that as citizens of this world, we need to act as stewards of the environment for our own survival.

What you have seen during your decades of exploration, and where did you get this passion for the environment and sustainability?

I am the first person in history to be stupid enough to walk the North and South poles, but I would never describe myself as an explorer or an environmentalist, rather I am a “survivor.” I am far too stupid to be a scientist! I did not walk on the South Pole for any particular reason more than just to do it, and to become the first in history to make the two journeys.

I was inspired by Scott, Shackleton and Amundsen, all Antarctic explorers. I was and am driven by the feeling that I have to do something for our survival on earth. During one of my walks, I walked under a hole in the ozone layer, I was not aware of it at the time but the UV light reflecting off the snow changed the color of my eyes. We had not read of this from those early explorers; it was something I experienced firsthand. Then I realized that the issue of survival is not someone else’s problem. I just had to do something about it.

Both poles told me something and I tried to listen. I had to make a choice, am I an environmentalist or a Greenpeace person? I decided that I should really work with businesses, industry and commerce: these have the power to change. As a survivor, you do not go for the easy option – you go for the option that makes you survive. Governments have very little influence. Environmentalists

were all saying the same thing and being overly negative. Industries and business, on the other hand, have longer term views, a reason to act, and a huge connection with everyday people. I made a choice to work with the industry and businesses, and that is when I became quite passionate. I believed that I could make a difference and make a change.

During your explorations, you showcased pioneering technologies robust enough to work in the world’s harshest environments. How can we translate what you have learned to business?

There are two areas, really: one is leadership, the other is convenient solutions. Leadership is essential in business. If you do not lead, you die. If people in the industry are not leading, our world will die. Leadership means being beyond words – words are easy. There are many mission statements about saving the planet, but we need to move beyond the mission statements; we are beyond An Inconvenient Truth. Business leaders also have to

put into practice convenient solutions. People are in general lazy and do not want to make a change if they do not have to, especially in the Western world. We have to create convenient solutions that are a part of making good business. This will inspire action.

We need consistency; we need long-term solutions. We need people to feel that solutions are sustainable, and that they can be a part and make a difference. Leaders have to see this as a business opportunity. The bottom line is, what we do here in the U.S. and what we do in Europe is important, however, it is critical to deploy effective strategies in places like India and China and other developing nations. I spent four years bicycling around India, visiting and talking to companies, industries, businesses, and students. There are 1.4bn people in India. If India develops in the same way we are still developing, it will not matter what we do in the Western world. We have to look outside our shores and realize that we have a responsibility to work with developing nations and share our sustainable solutions.

What solutions in your mind would be beneficial for these nations?

Solutions can do many things. Biofuels especially not only help produce less CO2, but can really help a nation. My lungs were permanently damaged in India due to the air quality. Farmers burn their crops at the end of every season. It goes into the air and causes a huge amount of extra pollution. Turning waste crops into biofuels is a fantastic solution for a country like India. Formalized recycling and garbage collection systems, and solar power technology, are other solutions which would make a significant difference for emerging nations.

You once said that “our biggest threat to our survival is that we believe somebody else is going to do something about it.” What can corporations do now to tackle environmental challenges more effectively?

I really admire CEOs, they have a hell of a job. They have to see to their shareholders and employees, but also make important business decisions, and often being sustainable could

be seen as an extra business cost. I believe that what CEOs can do better is to be an inspiration for their workforce and take action. What they tend to do is make some huge statements and commitments on sustainability, but these are lacking sustainable inspiration behind them. You have to keep the inspiration sustainable, which means CEOs have to keep re-inspiring people on the statements and commitments made, make them believe that the environment and being sustainable is part of the business, and show them its importance by rewarding those who are making an effort (via recognition or financial rewards). CEOs should stand up, be more forceful and vocal, and fight. Fight like hell. We can no longer just be comfortable and be the same we have always been. It is time for change and the time for action!

When we spoke to Darren Walker at the Ford Foundation, he argued that sometimes corporations and managers have the wrong incentives to become more sustainable. What is your perspective?

It has to be a combination. Every single human being knows that climate change is a reality. What we are not sure of yet, is exactly how much we are causing the climate to change.

Every single person that is in business is in the business of making money. There is nothing wrong with giving people financial incentives to phase out carbon or to make the company more sustainable. However, there has to be a slight change in culture and values, so that people are not doing it just for the money. We need to start to feel as a human race.

Doing the right thing needs leadership from the top. People need to be feeling that they are doing the right thing because it is the right thing. If it is just money, we are missing the point – we all need to inspire!

What we do here in the U.S. and Europe is an “engine room” for the billions of people that want what we have. Look at all the wonderful things technology has given us. There is no way people in India should not have what we have – they have every right to. The problem is, if they get it in the same way we got it, we will swim! Every year I go to the Arctic, I see what is happening. It is melting, the sea levels do rise and temperatures do rise. I have seen it over the past 32 years. It is the reality.

What legacy do you want to leave behind?

I am not finished yet! I might be 61, but what one leaves behind is what one does. Barney and I are Indiana Jones and son, we are just getting warmed up.

It was my son’s idea that we should walk to the South Pole. At the age of 61, your knees are screwed, your hips and your back are gone. He said, “Dad, we have to do this to inspire young people. We need to do something that gets their attention. We will show that father and son, generations, have to work together on this issue.” I then had to make the hardest decision of my life: to leave my son at age 23 and pull out of the journey and let him bravely complete it himself. It was like handing over the baton to the future – to the next generation.

But I said, “I am not finished yet.” I am having my hip replaced in three weeks’ time. At end of 2019, I am going back to compete that 300 miles to the South Pole that I didn’t do at the end of last year. It will mean it will have taken me 35 years to cross the whole of the Antarctica.

The message is that it is all about action, about doing it, action that grabs people’s attention in a world dominated by information and not enough inspiration. I believe people need a certain sense of feeling uncomfortable to make a change, and what we do is hard. It is not time yet to start talking about legacy. We can discuss legacy in another 30 years when I am 90.

Tell us about the “Climate Force Challenge” –what are some of the solutions you propose, how do you define success, and how do you measure progress?

Every single person who reads this interview has business targets to hit. So few people have targets in the environmental world. We started the Climate Force Challenge by making the journey to the South Pole on renewable energy to show that it works. We are going to clean up (not offset) 326mm tons of CO2 from our atmosphere in the next seven years. It is my only political statement: it (the 326mm number) also happens to be the population of America.

If we plant 326mm trees that last 40 years, our job would be done. But it is not that simple. With our challenge, we give everyone the ability to be a part of fixing the problem.

What is important, overall, is that it gets people going. If you are not feeling a little bit inspired after talking to me, I have failed. But I hope you have been inspired by me and my son. And if we can do this, what can bigger and more powerful people do? It all has to do with inspiring people.

What CEOs have to clearly understand is that there is an entire generation of young people like my son Barney (who nearly lost his toes in the adventure) who no longer are choosing to join a company just for money. They want to work for a company where they can make a difference to their world. CEOs have to take this on board for recruitment and retention. This generation will use their wallets and the power of their spending to make choices.

Who is your sustainable hero and why?

Jonathan Porritt, UK. He is a true battler and has never given up. We have worked together for nearly 30 years and his passion NEVER burns low.

info@greentechcapital.com

www.greentechcapital.com

NEW YORK

640 Fifth Avenue

New York, NY 10019

United States

Phone: +1 212 946 3360

SAN FRANCISCO

555 Mission Street

San Francisco, CA 94105

United States

Phone: +1 415 697 1550

ZÜRICH

Bahnhofstrasse 26

8001 Zürich

Switzerland

Phone: +41 44 578 3900

Aligned with the SustainableDevelopment Goals, we invest in public companies that are creating shareholder value by enabling more sustainable use of our Energy, Water, Food and Waste resources.

GCA Sustainable Growth Fund

GCA Sustainable Growth UCITS Fund