by Mr. Duckling - Headmaster of Dubai College

It would feel strange to begin without acknowledging the context in which this work has taken place This has been an extraordinarily challenging period, shaped by ongoing conflict in the Middle East that has touched our community in profound and personal ways. For many, recent events have impacted families, shaped (online) classroom conversations, and reminded us that the purpose of education is not simply to deliver content, but to develop young people who are curious, committed to giving back, and critically aware of the complexities that define the world around them.

The contributions of the speakers throughout this programme have reinforced this message in different and complementary ways, each offering valuable insight into how we might better prepare students for the realities they will inherit

In particular, the session delivered by Khatija Haque stood out as one of the most insightful and thought-provoking presentations I have attended in recent years. Her analysis was both grounded and forward-looking, combining a clear-eyed understanding of regional economic dynamics with a compelling argument for the role education must play in shaping informed, engaged citizens. Her emphasis on critical awareness via the ability to question, interpret, and understand nuance, resonates deeply with the aims of the Dubai Keynes society This foreword, then, is both a reflection and a commitment: a reflection on a difficult moment, and a commitment to ensuring that the young people in our care are equipped not only to understand the world as it is, but to shape what it might become

by Mr. Christopher - Head of Economics at Dubai College

It is with immense pride and, I must admit, a deep sense of admiration that I introduce this Term 2 edition of the Keynes Society newsletter

What makes this publication particularly special is not only the breadth and ambition of what the Society has achieved this term, but the context in which it has been produced Against the backdrop of ongoing uncertainty and strain across the Middle East, these students have continued to lead, organise, think critically, and create That, in itself, is remarkable. The resilience, commitment, and quiet determination required to sustain a thriving academic society in such circumstances should not be underestimated It speaks volumes about their character

And yet, they have done far more than simply sustain it they have expanded it. From hosting high-calibre guest speakers such as Tara Luthra and Khatija Haque, to facilitating student-led discussions on complex global issues, to launching initiatives that reach beyond our own school community, the Keynes Society has demonstrated what student leadership at its very best can look like.

The launch of the UAE-wide Ramadan Essay Competition and the Neo X Econ research initiative are particularly noteworthy These are not small undertakings they require vision, organisation, and intellectual curiosity. That they have been delivered alongside a full programme of talks, debates, and now this editorial publication is, quite simply, exceptional

What I find most inspiring, however, is the spirit behind it all. This newsletter is more than a collection of articles; it is a reflection of a community of students who care deeply about ideas, about the world around them, and about contributing thoughtfully to both Through thick and thin, they have continued to support this Society, to show up, and to produce work of real substance.

I encourage you to read these articles with that in mind They are the product of effort, collaboration, and perseverance under pressure They represent the very best of our student body.

by Aarush, Ali, Inaya, and Advik - The DKS Heads

This term was certainly an eventful one for us as Heads of Dubai College’s most prestigious and longest-running society. Over the course of the term, we were privileged to host three highly esteemed specialists in their respective fields, alongside two student-led sessions exploring low-cost airline carriers and the US–Venezuela conflict. Beyond the lecture theatre, the society also launched its first-ever National Ramadan Essay Competition, in which our members’ essays competed with submissions from students across the UAE who share an interest in Economics Finally, we were delighted to announce the DKS x NeoEcon Research Cohort, through which accepted student researchers will have the opportunity to conduct research using primary data from Polytech Masterbach. Details about everything new with the DKS are available on our webiste: https://wwwdubaikeynessocietycom/

We extend our gratitude to Mr Christopher for his guidance and steadfast support during these challenging times, and especially to our members, competitors, and article contributors Your support is what makes DKS much more than just a CDA. We hope to return to in-person sessions soon and enjoy an even more successful Term 3

Within this termly magazine are the works of DC students from Years 7-12, with each student talking about a different field in Economics, Business and Finance As you read through the thought-provoking articles contained within these pages, we would like to leave you with a quote from the man who inspired the creation of the Dubai Keynes Society:

“The difficulty lies, not in the new ideas, but in escaping from the old ones.” - John Maynard Keynes

by Aarush .V

The economic legacy of British rule in India is best understood neither as a story of pure modernisation nor as one of undiluted collapse. British rule did coincide with measurable improvements in transport and market integration, and it did not prevent all industrial growth. Yet the broader structure of the colonial economy was not organised around Indian industrial development. The central issue is whether British rule altered India’s economy in a way that weakened its capacity for selfdirected industrialisation. On balance, it did. The most defensible judgement is that colonial rule deindustrialised important parts of the Indian economy while also producing some efficiency gains whose benefits were limited by the imperial priorities within which they were created

The clearest evidence lies in textiles. In the early eighteenth century, India was a major producer and exporter of cotton textiles Clingingsmith and Williamson note that India was a major player in the world textile export market in the early 1700s, but by the middle of the nineteenth century it had lost all of its export market and much of its domestic market. Their estimates are striking: India’s share of world industrial output fell from about 25 per cent in 1750 to about 2 per cent by 1900.

Even allowing for the rise of industrial Europe, that is a substantial relative decline. It suggests that India did not merely fail to industrialise rapidly enough; it moved from a position of manufacturing significance into a far weaker industrial place within the world economy

This shift was not simply the result of neutral technological competition British mechanised textile production certainly reduced costs, and Indian handloom producers were exposed to that pressure But the competitive environment was shaped by political power. Trade policy, tariff arrangements, and the wider terms of market integration were controlled by the colonial state

Economic historians have described India’s transition from an exporter of textiles to an exporter of agricultural products and raw materials, while importing British manufactured goods That pattern matters because it indicates a change in the structure of production itself. India was increasingly inserted into an imperial division of labour in which the higher-value stages of industrial production were concentrated elsewhere. At the same time, the term deindustrialisation needs to be used carefully It would be inaccurate to suggest that all industry disappeared under colonial rule. Recent work in An Economic History of India stresses that the traditional textile sector was only one part of the wider economy and that a modern industrial sector developed from the middle of the nineteenth century That sector was more productive than the traditional one and grew steadily; by 1947, the shares of the modern and traditional sectors were roughly the same This complicates any simple claim of uninterrupted industrial collapse. A more accurate formulation is that British rule weakened established manufacturing sectors and failed to generate the kind of broad-based industrial transformation that might have followed under a state oriented towards Indian rather than imperial priorities

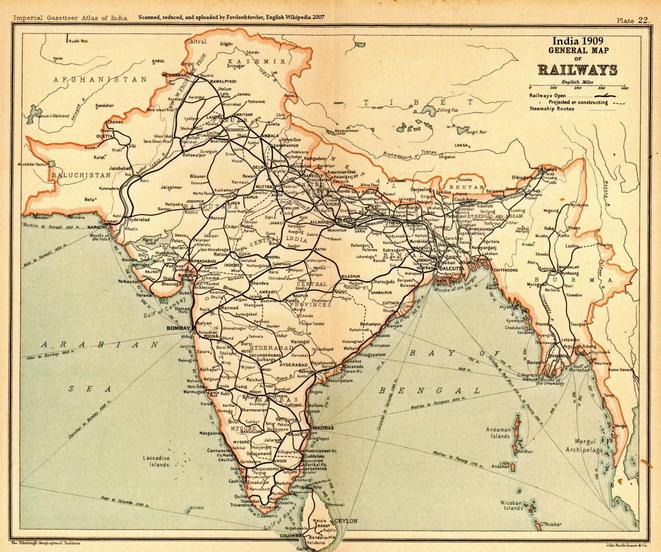

The strongest evidence on the other side concerns infrastructure, especially railways. By 1930, India had more than 60,000 kilometres of railroads Donaldson’s work shows that this network transformed transport conditions: before railways, bullocks typically carried goods at around 30 kilometres per day, whereas railways could move them about 600 kilometres per day. He also finds that railways caused a large (around 16 percent) increase in real agricultural income. These are not marginal gains The railways reduced trade costs, integrated regional markets, and generated measurable welfare benefits. Any balanced judgement has to acknowledge that colonial infrastructure had real economic effects

Those gains, however, should not be mistaken for evidence that colonial policy was developmentally neutral Infrastructure can raise efficiency without promoting autonomous industrialisation. Railways were highly effective at linking producing regions to ports and integrating India more tightly into imperial trade networks They improved commerce, but that commerce still took place within a structure in which India increasingly exported agricultural goods and raw materials while importing manufactured products. The economic question is therefore not whether railways were useful, but whether the overall pattern of investment and integration helped India move up the industrial value chain. The historical record suggests that it did so only weakly and unevenly

The longer-run institutional legacy points in the same direction Banerjee and Iyer find that areas where colonial land rights were assigned to landlords rather than cultivators had significantly lower agricultural investment and productivity in the post-independence period. Those same areas also showed significantly lower investment in health and education. This is important because industrial development depends not only on factories and trade, but also on the quality of agrarian institutions, human capital, and local state capacity Colonial rule therefore shaped some of the underlying conditions of later development. It can be said that colonial institutions left different regions with uneven developmental foundations

In conclusion, British rule did not reduce India to complete economic stagnation It oversaw the construction of major infrastructure, increased market integration, and coincided with the emergence of a modern industrial sector Yet these developments occurred within an imperial framework that weakened earlier manufacturing strength, redirected India towards externally oriented patterns of trade, and left institutional arrangements that burdened later development. The most accurate judgement is therefore not that British rule “destroyed” the Indian economy in every respect, nor that it simply modernised it. It altered India’s economic trajectory in ways that made industrialisation more constrained, more uneven, and less self-directed than it might otherwise have been

by Ali-Mansur .V

If you get someone to name the most important economic regions of the next fifty or so years, the same answers will come up. Most people will mention India, Southeast Asia, or Sub-Saharan Africa

Almost nobody will say Central Asia In fact, most people cannot name its five countries.

But, while Central Asia is being ignored by most, it is shaping up to become one of the world’s most consequential economic regions of the century

Central Asia: An Overview

Central Asia is the region in which five countries - Kazakhstan, Uzbekistan, Tajikistan, Kyrgyzstan and Tajikistan - are locked. Together they cover around four million square kilometres, roughly the size of the European Union, and hold about eighty million people.

Here are some key facts surrounding these nations :

1.All five of these nations are landlocked, meaning they entirely surrounded by land

2.All five became independent in 1991 when the Soviet Union collapsed

3 All five are young, having medium ages in the twenties

4.All five are sitting on a wealth of resources (which the rest of the world is quietly fighting over)

Beyond this, each of these countries has its own incredible statistics:

Kazakhstan: This country is giant. It has a population of around 20 million, GDP per capita around $13,000 and an economy that runs on natural resources such as oil and rare earths. It also produces around 43% of the world's uranium, more than any other country on Earth

Uzbekistan: With around 36 million people, Uzbekistan has one of the largest populations in the region. It is home to Muruntau, one of the largest open-pit gold mines in the world, and has seen growth of around 5 to 6% a year, placing it among the fastest-growing economies in Europe and Central Asia.

Turkmenistan: Holding the fourth largest proven natural gas reserves on Earth, Turkmenistan sits on a resource base that most countries can only dream of Almost all of its gas currently flows to China, and its reserves are large enough to shape energy markets for decades to come

Kyrgyzstan and Tajikistan: The two smallest countries in the region, but with extraordinary access to natural resources. Their mountains hold huge hydropower potential, and they control the headwaters of the Amu Darya and Syr Darya, the two great rivers that feed the region. Tajikistan is also building Rogun Dam, which when finished will be the tallest dam ever constructed

So, if the region is this important, why does nobody talk about it?

One part of the answer to this question is geography Central Asia is the most landlocked region on Earth. For most of the last century it was sealed inside the Soviet Union and accessible only through Moscow

Another part of the reason is its language Central Asia has more than half a dozen regularly spoken languages, and previous scholarship is scattered across all of them.

Lastly, perhaps the most crucial reason is that nothing ever demanded attention. There was no war or no crisis to talk about that could make global headlines The rest of the world was isolated from what was going on in Central Asia.

That is changing now.

Why? Well, three things have now happened at once:

When the war in Ukraine cut Europe off from Russian gas, new suppliers were needed to keep up with the demand for oil In 2023, Turkmenistan signed its first ever energy deal with an EU country, agreeing to send gas to Hungary through Iran and Turkey In March 2025, more Turkmen gas started moving to Turkey under a swap arrangement, with volumes set to grow every year. The European Commission has now designated the Trans-Caspian Pipeline, which would run gas directly across the sea to Europe, as a Project of Common Interest.

The world is running out of places to source critical minerals that are not China. Meanwhile, Central Asia is sitting on most of what is left In April 2025, the EU and all five Central Asian presidents met in Samarkand for the first ever EU-Central Asia summit They signed a joint declaration on critical raw materials and agreed to a €12 billion investment package. Kazakhstan signed a separate memorandum with the United States in the same field Uzbekistan announced a $26 billion plan to develop 76 critical mineral projects over the next three years. Kazakhstan also announced the discovery of a new rare earth deposit holding over 20 million tons of metal, which, if confirmed, would make it the third largest in the world, behind only China and Brazil.

The Middle Corridor, the route running from China through Central Asia to Europe, moved 800,000 tons of cargo in 2021. By 2024, it was moving 4.5 million tons. By 2027, it is expected to pass 10 million Kazakhstan alone has received around $23 billion of the $25 billion that China has poured into the region through the Belt and Road Initiative

None of these things are happening in isolation. Global demand from the EU to the US and China is driving investment and growth into Central Asia.

Through this Central Asia is now forecasted to become one of the few regions in the world that every major power actively needs out of necessity, becoming the next global frontier.

by Inaya .B

Modern supermarkets have evolved far beyond their original purpose: from small local grocery shops, they have developed into highly organised retail spaces They no longer respond to simple consumer demand, they shape it. Deals, discounts and limited-time offers encourage shoppers to purchase more than they originally intend, raising questions about what 'rationality’ truly means in consumerism. Whilst traditional economics defines rationality as a framework where individuals make decisions to benefit utility, this assumes that one acts in an autonomous state with self-control In reality, research in behavioural economics and marketing theory has found that strategic product placement and time-sensitive promotions significantly influence consumer behaviour and purchasing patterns

Firstly, modern supermarkets have become increasingly reliant on behavioural economic theory, but it can also be argued that consumers themselves have become reliant on behavioural cues As a result, promotional strategies (offers and loyalty schemes) are designed to capitalise on systematic cognitive biases in consumer behaviour The common ‘2-for-1’ and ‘buy-one–get-one-free’ deals exploit the psychological principles identified in Kahneman and Tversky’s (1979) Prospect Theory, which proposes that individuals evaluate outcomes relative to a reference point. In the context of consumerism, the reference point is the original price of a product (Kahneman and Tversky, 1979) Thus, in an instance where an item is reduced from £4 to £3, the £1 difference is seen as a gain relative to the reference price However, Prospect Theory also has its limitations when applied to supermarket purchasing patterns. The theory largely focuses on how consumers evaluate decisions based on a ‘reference price’, however supermarket shopping relies on habitual purchases as opposed to one-off choices. Over time, if consumers become more comfortable with frequent promotions and adjust their expectations, the ‘discounted price’ can slowly become the ‘perceived normal value’. Thus, whilst the prospect theory demonstrates insight into the initial cognitive response to discounts, it fails to account for long-term purchasing patterns. In a hyper rational world where consumers possess perfect information, such shifts in perception would likely not occur. Hyper-rational consumers would recognise the intrinsic market value and then make their decisions accordingly rather than a reference point and promotions Thus, long-term purchases that are solely driven by discounts would weaken.

Moreover, supermarket promotions further leverage heuristics (mental shortcuts) and System 1 thinking due to store layout and product placement (Kahneman, 2011) In overstimulating supermarket environments, consumers rely on mental shortcuts particularly with small-ticket items. Experimental evidence demonstrates that labelling products as ‘free’ disproportionately increases demand (Shampanier, Mazar & Ariely, 2007) because the term eliminates consumers' fear of making a wrong decision and thus removes the perceived risk of buying the product Similarly, percentage discounts, such as ‘60% off’, have a higher impact than simply stating the monetary value of the item because they rely on heuristics. Consumers tend to process relative and larger figures easier than absolute calculation, so larger discounts become more appealing and thus encourage faster purchases. However, this does not not imply that consumers are wholly irrational In a hyper-rational world, and under the assumptions of John Stuart Mill’s homo economicus – individuals who possess perfect information and represent a concept of unconditional rationality – many existing promotional techniques would lose their persuasive power as a rational consumer would be expected to calculate unit prices and compare benefits. In this model, individuals have ‘perfect information’ and the cognitive ability to evaluate every offer and choose the one that maximises utility. Transparency would trump persuasion techniques. Under perfect information, there would be little to no artificial scarcity or urgency strategies as consumers would only recognise them as marketing and advertisements rather than signals to purchase.

In their current set up, supermarkets also use deliberate choice architecture to exploit the behavioural biases of consumers. Supermarkets have visual hierarchies that direct attention towards high-margin items, and brands pay premiums to have their goods placed on a prime visual level. A study involving Kellogg’s mascots, like Tony the Tiger, found that characters on children's cereals are designed to look downward at a 96degree angle (Mulligan and Remedios, 2023). Kellogg’s pays for placement on lower shelves so that these mascots can make direct ‘eye contact’ with children and this results in ‘pester power’ - children lobbying their parents to buy the cereal (Prassad and Thomas, 2010). This behaviour is reflective of Herbet Simon’s theory of bounded rationality: a human decision-making process where we attempt to satisfice rather than optimise due to limitations in our cognitive abilities (Simon,1955). Additionally, price perception plays a key role: cheap prices create a negative assumption that quality is not guaranteed, and expensive products are considered a ‘rip off’ Thus, mid-range priced branded products are more likely to be chosen because they are considered reliable This tendency can be partially explained by bounded rationality whereby consumers make adequate decisions due to time constraints and limited information. Choosing a prominently displayed item may not necessarily demonstrate irrational behaviour, rather, a rational trade-off between minimising time and maximising price efficiency. Thus, rather than proving consumers are irrational, supermarket architecture works with rational consumers because it simplifies choice and saves time in an environment characterised by decision-making. Even in a hyper rational world, some promotional strategies may continue to persist as they help consumers make more cost effective choices

This extends to the ever-growing sphere of e-commerce Online supermarkets today exploit behavioural biases not through sensory stimuli, but through sophisticated algorithmic systems: limited-time discounts, low stock warnings, one-click checkouts, and ‘recommended for you’ sections (Thomas-Michigan, 2020) Such features capitalise on cognitive biases such as loss aversion and salience bias, encouraging impulse purchases rather than cost-benefit analysis Loss aversion is exploited by using scarcity tactics such as countdown timers and limited-stock warnings (Kahneman and Tversky, 1979). Eye-catching discounts are prominently placed to make certain products feel more valuable and lead consumers to purchase them, exemplifying salience bias (Taylor and Fiske, 1975). A key distinction from traditional supermarkets is that algorithms use customer data to detect patterns in behaviour and consumer spending, which leads to hyper-personalised marketing (Wave Grocery, 2023). As with traditional supermarkets, consumers can face decision fatigue, and the prominence of certain products can boost profit and revenue for small-ticket items, because shoppers may not want to scroll extensively to evaluate alternatives. In a hyper-rational world devoid of manipulated product placement and behavioural triggers, behaviour would theoretically become more aligned with the assumptions that rational consumers are benefit maximisers. This means that they would evaluate all their purchases, compare prices, quality and utility to maximise their satisfaction. Rational consumers may also consider their long-term benefits rather than simply make impulsive purchases.

Whilst there is much emphasis placed on the behavioural frameworks of supermarket marketing, internal human behaviour is arguably just as powerful and cannot be dismissed. In reality, consumers do not always make purchase decisions in a fully rational mental state: they may be tired, stressed, hungry or distracted High stress levels correlate to impulsive buying decisions as consumers seek instant gratification (Krstić, 2025) Moreover, hormonal changes across the life cycle (aging and pregnancy for example) can alter risk tolerance and reward sensitivity. The theory of visceral factors poses that physical and emotional states shape cognitive thinking toward short-term gratification and biased decision making, therefore challenging the very hypothesis that humans could be hyper-rational (Lowestein, 1996). Visceral factors refer to internal emotional and physical conditions such as hunger, thirst, moods and cravings that directly influence behaviour in ways that override rational decision making or longterm self-interest. These states have a disproportionate effect on behaviour and tend to produce immediate feelings of satisfaction and pleasure (Palmer, 2011)

In practical terms, when a consumer is fatigued, they are more likely to rely on shortcuts, reducing their willingness to search or scroll for optimal choices online (Palmer, 2011); when stressed they may prioritise convenience over optimisation; when hungry they may overvalue food items even without flashy promotions and strategic placement of products Neither online nor tangible supermarket environments can eliminate hunger, tiredness or stress, or indeed influence the choices that consumers make as a result of these factors This challenges the assumption that by removing behavioural tactics that manipulate consumer behaviour it would automatically make consumers fully rational

Even if supermarkets reduced excessive promotions and engineered layouts in a hyper-rational world shoppers would still be influenced by visceral factors and emotions What complexifies this debate therefore is whether or not humans could be hyper-rational in the first place. Given bounded rationality, individuals face limitations in information processing with time and self control meaning that ‘perfect rationality’ isn’t unrealistic, it is arguably unattainable. Instead, consumers rely on heuristics and are influenced by emotional states, suggesting that decisions only appear rational in a simplified framework. Thus, even in the absence of supermarket manipulation, purely rational decision making is likely to remain theoretical rather than achievable in real-life However, this also implies that supermarkets in their current form are designed to manipulate these limitations. In a hyper-rational world, where many behavioural biases wouldn’t exist, many supermarket strategies would become redundant.

by Advik .B

For the better part of a century, the US dollar has served as the foundation of the international monetary system. It functioned as the primary medium of exchange for global trade, the dominant reserve currency held by central banks, and the standard unit of account for commodities and financial contracts worldwide. Yet, it is no secret that this position has weakened considerably in recent years. From the freezing of Russian central bank assets to the accelerating push by BRICS nations to settle trade in local currencies, an increasing number of countries have actively pursued policies to reduce their dependence on the dollar, driven by concerns about not only geopolitical leverage, but economic security, and the search for alternatives to a system they perceive as overly reliant on American policy decisions. With the world’s most used currency's position globally being questioned more than ever before, it seems only appropriate to reflect on how the dollar achieved its dominant status and what factors are now driving its decline

The dollar’s path to global dominance really began after World War II In 1944, delegates from 44 countries came together in Bretton Woods, New Hampshire, to rebuild and establish a new international monetary system They created two key institutions: the International Monetary Fund (IMF) and the World Bank. More importantly, given that the U.S. had emerged as the strongest economy after the war, they placed the dollar at the centre of the system - it’s value was fixed to gold at $35 per ounce, while other countries pegged their currencies to it. This effectively made the dollar the backbone of global trade and finance, giving the United States a huge amount of economic influence. The system functioned for nearly three decades, but U.S. spending on the Vietnam War and domestic programs created inflationary pressures By 1971, dollars in circulation far exceeded available gold reserves, prompting President Richard Nixon to suspend dollar convertibility and effectively end the Bretton Woods system

Many anticipated this would diminish the dollar's international role; instead, the oil crises of 1973-1974 provided the catalyst for an alternative foundation. Following the Yom Kippur War, OPEC imposed an embargo that quadrupled oil prices

Subsequently, the United States negotiated agreements with Saudi Arabia whereby the kingdom priced oil exclusively in dollars and recycled export revenues through American Treasury securities and deposits in American “money-centre” banks (i.e petrodollar recycling). In exchange, Washington provided military protection. Other oil-producing nations very soon followed suit, and in the process established arguably the most important global financial system till date: the "petrodollar". Since oil imports were essential for every major economy, this created perpetual global demand for dollars regardless of American economic performance.

The petrodollar arrangement fundamentally transformed international commerce

The dollar became the standard invoicing currency for global trade, with transactions between non-American parties routinely conducted in greenbacks

When Japan purchased oil from Saudi Arabia, when Germany imported machinery from Brazil, when South Korea bought electronics from Taiwan - all of these exchanges were overwhelmingly dollar-denominated Both the Federal Reserve’s ability to ensure dollar liquidity and act as a backstop for financial stability, combined with the United States’ capacity to always meet its obligations in its own currency, made default risk basically negligible and reinforced strong investor confidence in the dollar as a virtually risk-free asset for global trade.This phenomenon generated a so called “network effect”: because everyone used dollars, transaction costs for alternatives remained prohibitively high, which only served to increase dollar demand feeding back into the same cycle

Central banks worldwide responded by accumulating substantial dollar reserves as protection against balance-of-payments difficulties and exchange rate volatility US Treasury securities acquired reputation as premier safe-haven assets, with investors accepting minimal yields during crises in exchange for liquidity and security The dollar's role expanded further through American financial markets, which offered depth and liquidity unmatched by alternatives. The SWIFT international payment system reinforced this dominance Though technically headquartered in Belgium, SWIFT operated under significant Western influence and processed the vast majority of cross-border transactions in dollars This infrastructure gave Washington considerable leverage, as exclusion from SWIFT effectively meant exclusion from international commerce. Together, these mechanisms petrodollar pricing, reserve accumulation, Treasury market depth, and payment system control—made the dollar extraordinarily resilient against challenges.

This dominance persisted and even strengthened through subsequent decades. The Soviet Union's collapse in 1991 left the United States as the sole superpower, enhancing the dollar's attractiveness The 1990s witnessed explosive growth in international trade, predominantly dollar-denominated, while Washington's

promotion of financial market liberalization facilitated increased dollar flows globally Even, paradoxically, the 2008 financial crisis played a role in reinforcing the dollar, as investors worldwide sought refuge in perceived safety during unprecedented instability

In the last few years, several things have happened that challenge the dollar's position One major factor is how the US has used the dollar as a political tool When Russia invaded Ukraine in 2022, the U.S. and its allies froze about $300 billion of Russia's central bank reserves and cut Russian banks off from the SWIFT system. This was meant to punish Russia, but it also scared other countries They realized that if they kept their money in dollars, the U.S. could take it away if they disagreed politically This made many countries want to reduce their dependence on the dollar.

Countries have also been building alternative payment systems China created CIPS, a payment system that uses Chinese yuan instead of dollars. Russia built its own system called SPFS More countries are making direct agreements to trade in their own currencies. The BRICS countries (Brazil, Russia, India, China, and South Africa) have been talking about creating their own currency or payment system for trade between themselves Even some US allies have looked for alternatives The European Union created INSTEX to trade with Iran when U.S. sanctions made normal trade difficult

Technology is also changing things. Many countries are developing Central Bank Digital Currencies (CBDCs), which are digital versions of their national money. Over 130 countries are working on these They could make it easier for countries to trade directly without using dollars. China has already used its digital yuan for some international trade There are also projects looking at how different countries' digital currencies could work together for international payments.

The global economy has changed in ways that reduce the dollar's importance The U.S. makes up a smaller share of the world economy than it did after World War II. Emerging economies in Asia and other regions are growing faster As more trade happens between these countries, it makes less sense to use dollars for everything. Some commodity markets are starting to use other currencies. China now has oil futures contracts priced in yuan Russia sells oil to India and China using rubles and rupees instead of dollars.

Central banks are buying more gold than they have in decades. Some countries are bringing their gold reserves back home instead of keeping them in the U.S. or Europe Cryptocurrencies, despite being volatile and controversial, offer another way to move money internationally without using the traditional banking system. Inside the US, concerns about government debt now over $34 trillion and ongoing budget deficits make some people question whether the dollar will stay strong in the long term.

While it remains the world's primary reserve currency, the combination of financial sanctions, alternative payment systems, and shifting economic power has accelerated efforts to reduce dependence on the greenback Countries are diversifying reserves, developing digital currencies, and settling more trade in nondollar terms. Despite no clear alternative currently existing, what seems certain is that the international monetary system is becoming more multipolar Therefore, the question now is not whether the dollar's dominance will decline, but how quickly.

by Naira. S

When the average home costs nearly eight times the average salary, the housing market transitions from acting as a ladder of opportunity to behaving as a barrier to entry for the entire young adult population. Today, for many young people in the UK, owning a home has become a distant aspiration but was once a realistic milestone As the average house price currently stands at approximately seven to eight times the average annual salary, the issue is no longer a simple one of consumers saving habits but has transformed into deeper structural pressures within the housing market itself. The dual role of housing, being both a source of wealth and a place to live, has made housing affordability not only a social concern but has become a macroeconomic one, possibly influencing long term growth. Through comparing Britain’s market driven system, it becomes explicit that housings are not only, shaped by demand and supply alone but also policy choices and the institutional system in that country

For an increasing number of households in the UK, acquiring stable and affordable housing is become more and more of challenge by the minute. A common benchmark that’s used implies that housing is affordable when its cost does not exceed 30% of one’s income, yet this threshold has been excelled for many renters and first-time buyers nowadays Over the past two to three decades, affordability has lost its meaning, not simply because house prices are much higher, but because they are accelerating much faster than wages, leading to the majority to feel much worser off UK house prices currently average 8 times - London being 10 - the average earnings, compared to only 3 in the 1990’s Meanwhile real wage growth has either been capped or limited since 2008, further widening the gap leading to most being at a relative disadvantage in real terms Home ownership among young adults (25-34 year olds) has fallen by 55% in the past 20 years reflecting arduous requirements and more challenging entry requirements This illustrates that housing affordability trends are not only temporary but structural in nature.

The crisis is closely linked to persistent market imbalances. From the perspective of supply, housing has become relatively unresponsive: strict planning regulations, green-belt restrictions and community opposition to construction have diminished new construction, leading to housing targets being often not met As a result of this, when demand for housing rises, supply responds much slower forcing prices much to rise much higher Due to factors like population growth and urbanisation, there has been an urgent need for more housing, while in London specifically, high-paying jobs have concentrated regional demand However, growing demand does not alone form long-term affordability problems if the supply can be adjusted efficiently, but unfortunately in the UK this is not the case Recently, housing has been viewed as not only a place to reside but as a relatively secure form of income. The expectations of rising prices reinforce demand as wealth from owning could form a substantial part of

household income This transforms housing to both a consumption good and into a financial asset, amplifying price pressures and deepening affordability challenges. The persistence of high housing prices is influenced by both market factors and political incentives A majority of voters are homeowners, suggesting rising prices increase household wealth. Therefore, policies that significantly reduce prices could become largely politically unpopular, creating tension: lower prices benefit buyers but reduce wealth for existing owners. Consequently, governments are incentivised to pursue policies that stabilise or cautiously adjust prices rather than aggressive reforms. Housing itself has now become a form of unofficial financial support, substituting for pensions or savings. This allows older generations to extract wealth from younger, acting as a safety net for some while developing a further crisis for others

The consequences of this structural imbalance are wide ranging. Firstly, it reduces labour mobility as workers may struggle to relocate to higher-productivity areas, hence distorting household spending with a growing proportion of income used towards rent or mortgage The crisis also intensifies generational inequality by widening the gap between younger and older cohorts, as well as many young adults being forced to rely on parents support due to the reduced accessible housing. In response, governments have implemented, both demand and supply side interventions, though their effectiveness has been restricted. The Help-to-Buy scheme has aimed to make ownership more achievable by governments providing equity loans to first time buyers, reducing the size of their initial deposit. Also, the modest expansion of social housing attempts to provide options for those unable to access the housing market. Nonetheless, this has been slow due to planning constraints Thus, these policies have offered temporary relief rather than addressing these deep rooted issues, underpinning the crisis.

To conclude, the UK affordability crisis discloses more than just high prices; it is the outcome of many details. While short term policies may ease these pressures, lasting solutions will require a balance of expanding supply, being able to maintain financial stability and reconsiders the role of home-owning in wealth accumulation. Without addressing these underlying causes, rising house prices will continue to persist, continuing to shape the living situations of many generations to come.

by Alizé .Z

Nature underpins the entire global economy. Tropical rainforests are a clear example of this. Often referred to as the ‘lungs of the planet,’ rainforests host a multitude of plant species with medicinal benefits and are therefore inextricably tied to the pharmaceutical sector. Likewise, the cosmetics sector relies upon the supply of natural raw materials such as shea butter to produce tropical products Not to mention, aside from their commercial function, forests have proven themselves valuable in terms of life-support systems: climate regulatory function, carbon sequestration, water filtration, and air purification. Yet, despite the bountiful benefits humans receive from it, nature rarely appears in economic calculations. Because most of these services are public goods or common pool resources provided free, they are often treated as if they have no value Economist Pavan Sukhdev argues that this “economic invisibility” is one of the main reasons ecosystems are degraded; you cannot manage what you do not measure (TEDx Talks, 2010). Should natural capital be valued?

Placing a monetary value on natural capital does remain a controversial topic, however Critics argue that the value ecosystems possess is inherently difficult to quantify in financial terms and becomes increasingly complicated when combined with ethical and cultural considerations Others argue this approach implies the ‘commodification’ of nature for trade in private markets (Costanza et al., 2014) and are concern that treating nature as an asset may distance people from the natural world, undermining the moral motivations that already encourage conservation (Oliver, 2021). Meanwhile, proponents of the idea insist that the real problem is not pricing nature but pricing it at zero; environmental economists employ valuation tools and price the benefits nature provides in an attempt to persuade individuals, businesses, and governments to expend resources on environmental protection and restoration (Chami et al, 2022)

Economists have developed several methods to estimate the value of environmental goods and services, even when no market price exists. One commonly used approach is contingent valuation, which attempts to measure the non-use value people place on nature. Individuals are questioned upon how much they would be willing to pay (WTP) to preserve an environmental resource even if they never directly use it The value is “contingent” on a hypothetical scenario presented to the respondents For example, people may be willing to contribute a certain amount towards protecting endangered species such as sea turtles or to preserving the cultural and ecological significance of Australia’s Great Barrier Reef, reflecting a moral or cultural commitment to conservation (World Economic Forum, 2020) By aggregating responses, economists could thereby assign an overall value to coral reefs.

Hedonic pricing, on the other hand, pertains to a method which values goods based on how they affect the prices of things with a market price, usually housing. Property prices can differ based on various different attributes of environmental quality including scenic views and proximity to natural sites like parks or beaches By analysing large datasets of property prices, economists can estimate how much each environmental factor contributes to the price, using this to consequently deduce the value of each feature Compared to contingent valuation, hedonic pricing utilises real market behaviour as opposed to hypothetical situations. Whilst this presents a clear empirical advantage in terms of accurate modelling, there is a key limitation where hedonic pricing cannot easily measure the value of ecosystem services such as biodiversity or endangered species which lack direct market analogues (Padder, M, 2025)

A third technique is the travel cost method, which infers the value of natural, recreational sites based on how much people spend to visit them Initially proposed by Harold Hotelling in 1949 to calculate the value of US national parks, the travel cost method collects information from visitors on distance travelled, transportation and accommodation costs, time spent travelling, and number of visits annually. By analysing patterns within this information, economists can estimate the demand curve for visiting the site

Finally, the replacement cost method estimates how much it would cost to replace a natural service with artificial infrastructure. Consider a coral reef’s role in reducing wave energy and preventing damage to coastal infrastructure. If the reef were entirely destroyed, what would be the cost of constructing and maintaining artificial sea walls and gabions to perform the same functions? Similarly, wetlands are known for their ability to improve water quality by filtering sediment and removing pollutants from water What would be the cost of installing a water treatment plant in its place? Nonetheless, this method fundamentally suffers from the fact that not all functions of natural ecosystems are known, and some cannot realistically be substituted with technical solutions: you cannot replace extinct species or the beauty of a natural landscape (Cohen, 2022). Beyond the price tag

Ultimately, the purpose of giving nature a monetary value is not to suggest that vast ecosystems, with seemingly infinite worth, ranging from spiritual connection to cultural importance, can be reduced to a mere ‘price tag.’ Instead, the valuation of nature can serve as an important step towards ensuring its importance is recognised in economic decision-making and nature’s hidden contributions guide policy calculations. In this sense, pricing nature may help protect it

by Vihaan.D

Economic growth in an economy is typically measured by the country’s GDP (Gross Domestic Product), a macroeconomic metric that “measures the total monetary value of all final goods and services produced within a country’s borders over a given period of time, usually a year” [Callen, 2025]. As the GDP grows, it generally leads to higher levels of consumption and production in the economy Economic growth has historically resulted in improved standards of living, reduction in poverty, and improved levels of employment. However, there is a distinct correlation with environmental degradation because of the increased resource consumption, waste generation, and pollution to satisfy the aggregate demand in the economy [Amir, 2025]. In recent years, as sustainability and environmental awareness have developed into a more prominent global issue, it has fueled a growing debate over whether both these macroeconomic objectives can be achieved simultaneously. This article examines the relationship between economic growth and environmental protection, exploring both the positive and negative implications while also identifying whether alternative approaches to economic growth could offer a more sustainable path

When an economy grows, it leads to higher industrial production, provided that the proportion of the country’s economy predominantly consists of the primary and secondary sectors, since increasing production in this sector requires tangible resources such as capital and land The acquisition of natural resources such as mining, agriculture, and forestry has an extensive impact on the country’s environment. These primary sector industries are heavily reliant on fossil fuels: for instance, the extraction of minerals from earth requires large machinery such as excavators, drills, and conveyor systems The majority of the practices involved in this process run on diesel and electricity, which are derived from non-renewable fossil fuels In addition to that, the transportation of these goods depends on trains and trucks, which are also fueled by fossil fuel combustion. Furthermore, the burning of fossil fuels releases greenhouse gases such as carbon dioxide, contributing to air pollution and climate change [IPCC, 2021] If an economy that is dependent on mining, such as Botswana, experiences economic growth, it will further accentuate the carbon dioxide emissions released in the country, amplifying the severity of environmental degradation. Therefore, it makes it harder to achieve both objectives simultaneously due to the environmentally damaging practices involved, establishing a trade-off between fostering economic growth and environmental protection

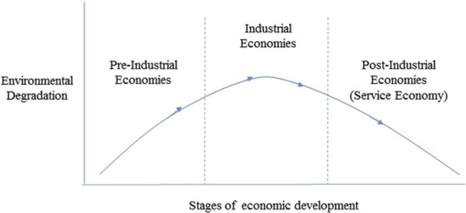

While economic growth can consequently lead to the decline of the environment, there are also some positive impacts associated with growth. This is most commonly evident in developed and developing nations The economic structure of the predominance of nations transitions from a primary/secondary sector economy to a tertiary sector, which involves the provision of services. Due to this, the damage that advanced nations induce to the environment is principally lower in comparison to less developed countries [

Service-based economies mostly rely on human labor and infrastructure rather than resource extraction or heavy manufacturing, resulting in their environmental footprint being smaller per unit of economic output. Moreover, according to the EKC (Environmental Kuznets Curve),

Stern, 2004]

it suggests that as income per capita rises beyond a certain point, countries are able to invest in cleaner technologies and stricter environmental regulations [Panayotou, 1993] This means that more developed nations can potentially invest more in renewable energy, pollution control, and environmental conservation Some real-world implementations of green practices in developed nations are Germany and Denmark, which have invested significantly in wind, solar, and hydroelectric power to minimise reliance on fossil fuels. Furthermore, the EU (European Union) has established a system of pollution permits that enable nations to buy and sell carbon allowances, which enable the country to reduce environmental impact whilst also promoting economic growth

In addition, to green practices adopted mainly by developed nations, the global economy, including primary sector nations, could integrate a circular economy The circular economy is an economic model that utilises resources for as long as possible by recycling, reusing, refurbishing, and repairing products, rather than following the traditional model of "using and disposing"; it revolves around sustainable economic growth [Ellen MacArthur Foundation, 2023]. This concept has already seen integration in EU nations such as Austria, Finland, and France The implementation of the circular economy is mostly evident in service-based economies, but they can also be employed in primary sector nations, like Ethiopia, which is reusing agricultural waste, improving resource efficiency, and reducing landfill disposal. But the drawback of this economic model is that it slows the process of economic growth, since it takes longer to produce goods when relying on recycled or reused resources instead of extracting new raw materials

In conclusion, there is a complex relationship between a country’s economic growth and environmental protection, as it is largely dependent on a nation’s economic structure and stage of development. Nations reliant on the primary sector in their economy will face a trade-off between growth and sustainable practices, while more developed nations can develop while also reducing their environmental impact, supported by the EKC. Although there are some practices that can be employed worldwide to encourage growth, it should not be at the cost of the environment. As many nations are enduring growth, deindustrialising, and moving towards a more tertiary sector economy, globally there should be reduced environmental harm As they get more advanced, they are more likely to invest in more environmentally appropriate methods of production. For this to occur, there needs to be growing awareness about the protection of the environment and a prioritisation towards well-being in the economy rather than chasing economic growth.26

by Arya. K

Covid-19 The virus that shook the world, triggering one of the most severe economic disruptions since the 2008 global recession. While countries implemented lockdowns as a preventative method, the action resulted in a drastic decrease in economic activity leaving millions without income and crippling businesses. In response, governments employed fiscal measures such as wage subsidies and business grants to stimulate economic growth. While these policies helped prevent deeper recessions, they also led to “massive increase in global debt during the pandemic in 2020” (International Monetary Fund, 2023, page XIII).

Government debt is the result of spending exceeding the revenue from taxation, resulting in the government issuing bonds, which promise repayment with interest at a future date. It is a central part of fiscal policy since it allows governments to increase government spending in order to stimulate aggregate demand However, during the global pandemic, many countries accumulated large quantities of debt due to the extensive scale of borrowing According to the International Monetary Fund (IMF), global public debt reached historic highs, especially due to declining tax revenue(IMF, 2023).

One way economists assess the severity of a country’s debt is using the debt to GDP ratio This compares government debt to the total economic output of a country A high debt to GDP ratio is problematic for countries and can be harder to manage. After the pandemic, many advanced economies faced debt to GDP ratios greater than 100%, meaning the total government debt was greater than the annual value of goods and services produced in the economy (Organisation for Economic Co-operation and Development, 2023). During the height of the pandemic, the US debt to GDP ratio increased by 25%, rising to 132% While this level of debt is still manageable, it requires extensive government planning and regulation.

Many countries implemented policies and programs targeted towards households in order to reduce the economic impact of the pandemic In the US the government passed bills which which increased unemployment benefits and reduced barriers for small business loans Similarly, in the UK, a government program called Coronavirus Job Retention Scheme was introduced, which compensated workers wages when businesses were forced to close While these programs helped reduce unemployment and increase consumer spending, governments incurred substantial costs which drastically increased government borrowing

However, while these fiscal policies resulted in a drastic increase in debt, they were also a necessary measure to prevent further economic turmoil. as necessary to prevent a deeper economic crisis According to the World Bank, without such interventions, the increase in unemployment and poverty levels would have been exacerbated especially in developing economies (World Bank, 2023). Many countries with limited resources faced the decision between avoiding further economic contraction and increasing public health spending

Furthermore, the economic slowdown as a result of Covid-19 resulted in central banks globally incurring significant financial losses. Central banks generate profits through interests on assets such as government bonds, which are then sent to governments as remittances. However, during the global pandemic, in order to increase the money supply and stimulate aggregate demand, central banks purchased bonds in large quantities. However, this action paired with the growing interest rates resulted in some central banks holding assets worth less than the money spent to acquire them. As a result, central banks “incurred heavy financial losses and have stopped distributing remittances to governments (Bank for International Settlements (2023), Page 77, box B) This trend is visible in the graph below where remittances stopped between 2022 - 2023:

This reduction in government revenue exacerbates financial limitations as governments have fewer resources to cover spending or debt

While global powerhouses have the resources to implement stimulative policies, the lack of resources for developing countries heightens the severity of the situation. According to the United Nations Conference on Trade and Development, the rising costs shows that rising interest costs, combined with weaker economic growth can result in low income countries “sink under the growing weight of unpayable debts” (UNCTAD, 2023, page 54)

Also, since most countries borrow in foreign currencies, the country may experience a depreciation of the local currency against the dollar, increasing the cost of their debt

Ultimately, the financial stability of countries is heavily dependent on long term policies. Governments must plan for future spending needs, including healthcare, infrastructure and climate adaptation, while ensuring that debt does not spiral out of control. Developing countries may rely on the help of the IMF for financial assistance and capacity development In following years we may witness the implementation of policies such as gradual fiscal consolidation, targeted investments, and reforms to improve tax collection

Arhaan. B

Professional sport has historically always been regarded as a key form of entertainment in the eyes of media corporations. The broadcast of sports in the modern era has captured both the triumphs and failures of elite athletes and emphasise the stature of extraordinary human achievement. In European football Arsenal’s ‘invincible’ season (Apollo Global Management, 2025) and in the NBA the Golden State Warriors’ dominance in the 2010’s symbolise perfection within sport. Individually Myles Garret’s record –breaking 23 - sack season and Serena Williams’ 23 grand slam titles have redefined longevity and greatness

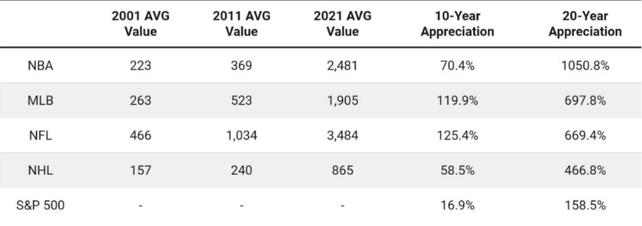

In recent years, institutions, sovereign wealth funds and private equity firms have turned their attention towards the alluring sports market. The sports industry represents a trillion-dollar market driven by expanding fanbases and heightened global media rights offers that have inflated the market significantly in recent years Revenues and valuations of major teams and leagues are rising and media rights for European women’s football coverage increased by 800% in two years (Oliver Wyman, n.d-b) Overall, NBA teams are estimated to have increased by ten-fold over the last 20 years (Apollo Global Management, 2025) and sports franchises of the US’s major four sports leagues have drastically outperformed the S&P 500 since 2011 (Birnbaum, 2022)

(Birnbaum, 2022)

The Rise of Sport as an Asset:

A primary driver into the investment of sport is the fundamental economic concept of scarcity alongside the stability of major franchise assets. Artificial scarcity is created through league structures in which many leagues provide such as the top flights of European football. Long term exclusive rights to organise and manage leagues are also a factor and this makes sports such as Formula one monopolistic market structures (Kapoor, 2025).

In an ever expanding on-demand world, sports fixtures act as the last live, appointment viewing style of media that make it undeniably valuable to distributers and broadcasters alike This can be seen by the race by many big firms to start televising matches that have resulted in major streaming services such as Amazon, Netflix and Paramount to start diversifying their offerings (PC TECH, 2025).

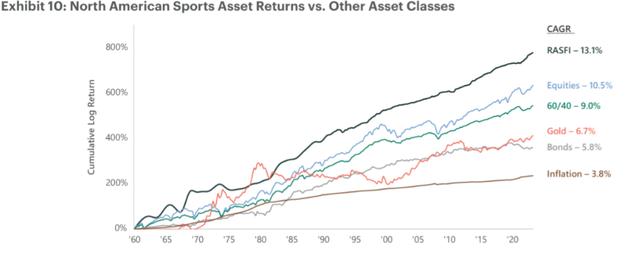

Sports leagues also reciprocate the recognition that the investment into franchises are becoming increasingly more lucrative As a result of this, leagues have restructured salaries and contract agreements to offer more to shareholders According to the UEFA regulatory body ‘spending on player and coach wages, transfers and agent fees to 90% of revenue in 2023 and 2024’ will decrease to 70% for the 2025 – 2026 (S&P global, 2024) These policies have reshaped the mindset of owners and combined with unwavering fan loyalty have shifted the mentality from creating a ‘winning organisation’ to a ‘winning businesses (Berke, 2024) Largely due to the sociocultural influence and historic significance, represent a long- term asset and 20 % of billionaire own stake in sports teams which is up from 6% in 2022 (Cuccinello, 2025) The Ross-Arctos sports franchise index (RASFI) that tracks the performance of the franchises of the US’s major 4 leagues have been found to have compounded by 13% per year in the last 60 years outperforming other assets such as Gold, bonds and equities (Apollo Global Management, 2025)

(University of Michigan, 2024)

Private and institutional investment is no longer a hypothetical within the sporting world as its implications are already being felt across continents and leagues. In the topflight of French football, Lille FC were acquired by Callisto sporting in 2020 a subsidiary of Luxembourg based investment fund Merlyn partners after the previous owner faced financial pressures (Pugmire, 2020). Although fans may have initially opposed the sale, it is considered that the decision revitalized the club as a whole The team before the sale were stagnant and struggling in League one, placing 17th in the 2017-2018 season. Immediately following the financial take-over, the club won the division in the 2020-2021 season and are strong competitors to date (CGTN,2021). The investment into the club has revitalized the finances of the team and has allowed them to make key transfers helping them develop overall with he franchise being worth 222 million euros today (Kristensen, 2025).

Private equity firms and clubs themselves have a mutualistic relationship that are interdependent. On one hand, sports organisations benefit from investment into infrastructure, technological advancements and community engagement (JP Morgan, 2025) whilst private equity corporations reap the rewards of asset appreciation as the club develops.

Conclusion:

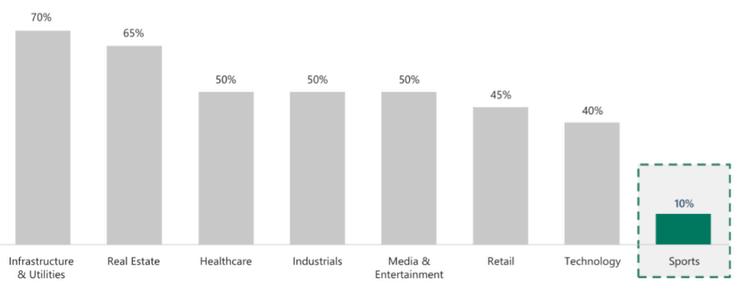

Despite the drastic rise in sports franchise valuations and growing interest amongst institutional investors, it is clear that professional sports still remain underleveraged in comparison to other asset classes Teams operate with a much lower loan-to-value ratio at 10% in comparison to other assets real estate and healthcare that operate at a ratio of 50% or above (Apollo Global Management, 2025) The conservative financial structure comes as a result of strict league regulations and the tendency for franchises to be owned by wealthy families and individuals rather than financed through external capital. As private credit markets broaden, alongside the stable cash flows of the industry largely due to expanding and lengthy media deals (Kapoor, 2025), it opens the sports industry to a 2 5 trillion-dollar opportunity (Apollo Global Management, 2025) If managed suitably, the flexibility of the industry could result in further integration into global finance and become Wall Street’s next big bet.

(Apollo Global Management, 2025).

Kabir. L

Technological advancements are increasingly being recognised as one of the primary drivers of long-term economic growth At its heart, technological innovation increases productivity by allowing firms to produce more output in a swifter fashion whilst requiring the same or less number of inputs. In recent years, the development of modern automation and data-driven software has provided large firms with the opportunity to benefit from technological economies of scale, reducing costs while expanding production capacities due to the increased efficiency and optimisation of recent production processes (McKinsey & Company, 2025).

This rise in general productivity leads to an expansion of an economy’s productive capacity and forms the basis of a sustainable practice enabling economies to thrive as productive expansions gradually accumulate and unique enhancements of existing technology are introduced into global economies

Technological advancements also drive the development of a plethora of new markets which provide many jobs to an economy New sectors of industry such as artificial intelligence, renewable energy and electric vehicles have emerged in the last decade and have attracted many consumers around the world and have proven to be great investments Companies such as Tesla and Build Your Dreams demonstrate how technological innovation can alter a specific market and transform the product. In 2025 255% of all cars purchased were electric which is a 211% increase from the year 2020 and forecasts show that electric vehicle use is set to grow 30% in 2026 with 116 million electric vehicles to hit the roads globally (EV Volumes, 2025; Our World in Data, 2024; Khaleej Times, 2025) These statistics have influenced the development of hybrid cars with many large firms such as BMW Group diversifying into electric vehicles. This process reflects a dynamic economy, and a transition into a forward-looking and adaptable global economy which can quickly react to changing global demands.

However, while the growth of industries such as electric vehicles creates new opportunity, it can also disrupt the economy in traditional sectors of the economy such as manufacturing and modes of banking that are being taken over by ‘fintech’. Companies such as PayPal offer seamless methods of transacting money which are preferred by the public. As a result, these methods of business are quickly becoming outdated. Automation can also lead to a mismatch in skills that are required in the economy as compared to the skills that are being supplied in the economy leading to structural unemployment which can create poverty and decrease standard of living in a country (McKinsey & Company, 2025)

In the past few years Quantum Computing and artificial intelligence have received vast amounts of investment in hopes for more efficient production in the future (Crunchbase News, 2025). Quantum technologies make use of the unique properties of quantum mechanics to execute complex calculations faster than any classical computer and aid financial and health related sectors of industry allowing for faster and more precise decision making enabling companies to produce more efficiently while maximising their benefit contributing to economic growth on a whole.

On the other hand, Artificial intelligence has grown exponentially and has received just over 200 billion dollars in investment in 2025 which illustrates its popularity amongst top companies as of late (Crunchbase News, 2025) It refers to computer systems that are designed toortasks that typically require human intelligence. The technological systems are able to recognise in depth patterns by utilising extensive amounts of data to make informed decisions and forecast future data to increase efficiency This improved efficiency enables firms to increase output and productivity, ultimately contributing to long term economic growth

Technological innovation will undoubtedly play a huge role in the future and will be central to long-term economic growth. It enhances productivity, accounts for structural change and introduces new markets which are growing rapidly. However, the concentration of who is able to benefit it is very disproportioante and it can disrupt traditional, low-skilled jobs of which the work force is mainly comprised of worsening inequality long-term.

Sarah. K

What happens when one company controls the entire market? What happens when they begin to dictate all the decisions we make? This is a problem that economists have been facing for over 100 years, from standard oil in the late 1800s to Google and Amazon, companies we still massively rely on today. A monopoly occurs when a single firm dominates an entire industry and holds most of the market share On the other hand, A free market is where the price of goods and services is determined by demand and supply, and multiple firms compete to win over consumers. Although monopolies can occasionally provide benefits such as economies of scale and increased research and development, it also has major disadvantages. Monopolistic firms can often exploit consumers by raising prices and as there are limited options consumers have no choice but to accept these higher prices. This article will explore the differences between monopolies and free markets and their impact on consumers and the economy as well as the role of antitrust laws in maintaining competition and protecting consumers from the harms of monopolistic behaviour.

A monopoly is a market structure where one single firm dominates an industry as they have the majority of market share and face little to no competition This dominance allows monopolistic firms to set prices and control supply without the pressure of other businesses. One of the key characteristics of monopolies is the high barriers to entry, which prevent new firms from entering the market and competing with an existing company. These barriers can include high startup costs, intellectual property rights such as patents, or legal restrictions Monopolies can come to exist in different ways: natural monopolies occur when industries require high infrastructure costs, such as electricity or water utilities, making it more efficient for a single firm to operate Additionally, monopolies can form through aggressive business tactics, such as undercutting competitors, acquiring rival companies, or using intellectual property rights to prevent competitors from entering the market and restrict innovation In the past, Standard Oil was one of the most famous examples of monopoly as at one point they controlled 90% of oil refining in the United States, before being broken up under antitrust laws by the US government In the modern era, companies like Amazon and Google dominate their industries, raising concerns about their market power and influence While monopolies can lead to increased efficiency, their control over a market often reduces choice and raises prices, making antitrust laws essential in an economy.

Monopolies, although often seen negatively, can provide various benefits to an economy One example of this is economies of scale, which is the benefit larger firms receive in the form of lowered average costs for their businesses. For example, Walmart, as one of the largest retail chains in the world, benefits from bulk purchasing, allowing it to buy products in massive quantities at lower prices from suppliers. This allows Walmart to offer lower prices to consumers while still maintaining profitability, making it difficult for smaller retailers to compete. Additionally, monopolies often have the financial resources to invest more in research and development (R&D), leading to technological advancements, such as in the pharmaceutical industry, where larger firms such as Pfizer are the ones funding drug development. However, monopolies also can present significant challenges Without competition, firms can raise prices, knowing that consumers have no other options. This lack of choice can lead to consumer exploitation and reduced innovation, as firms face little pressure to improve their products or services Ultimately, while monopolies can bring benefits, their power often comes at the cost of consumer choice and fair pricing.

On the other hand, a free market is a system where competition between businesses drives innovation and consumer choice In a free market, prices are determined by supply and demand, and multiple firms are able to compete to win over consumers This competitive market fosters innovation, as companies strive to improve their products or services to attract customers For example, the tech industry has seen constant improvements in smartphones, laptops, and other gadgets due to fierce competition between companies like Apple, Samsung, and Google Moreover, free markets provide consumers with a wide variety of choices, as there are a multitude of businesses to pick from that cater to the different needs and preferences of consumers. Increased competition can also lead to lower prices as firms want to have the lowest prices to attract the most customers. However, free markets do have certain drawbacks. Without regulation, large companies can dominate industries and overshadow smaller competitors, leading to the creation of monopolies Additionally, if some companies gain too much power, it can result in inequality and less opportunity for others to succeed. Therefore, while free markets promote competition and efficiency, they require regulations to ensure fairness and prevent all the power ending up in the hands of a few firms

Antitrust laws are put in place to promote competition and prevent monopolistic practices that can harm consumers and hinder economic growth These laws are crucial for ensuring that businesses do not abuse their power to exploit consumers through higher prices or lower-quality goods The Sherman Antitrust Act of 1890 was the first major legislation in the United States aimed at controlling monopolies, famously used to break up Standard Oil in 1911. Similarly, the European Union enforces strict antitrust regulations, such as fining Google for manipulating its search engine results to favour its own services. Case studies like the breakup of Standard Oil and the legal challenges faced by Microsoft in the 1990s, which accused the company of monopolistic practices by bundling its web browser with its operating system, show the active role antitrust laws play in maintaining market competition.

However, in today’s world, companies like Amazon and Google are often at the centre of debates regarding market power and the effectiveness of existing regulations, especially as digital platforms become increasingly dominant. While antitrust laws have had successes in promoting competition, challenges still exist, particularly in the era of globalisation, where corporations operate across borders, and in digital markets, where traditional antitrust laws struggle to address data monopolies and the issues that they present

In conclusion, although monopolies can lead to specific economic benefits, such as reduced production costs and increased investment in research and development, they often come at a significant cost to consumers High prices, limited choice, and stifled innovation are common consequences when a single firm dominates the market. In contrast, free markets encourage competition, drive innovation, and offer consumers a wider range of choices at better prices. However, they are not without their flaws; without appropriate regulation, they can allow monopolies to emerge and create inequality Antitrust laws are therefore crucial in maintaining a healthy balance between free competition and market control. As the economy becomes increasingly digital and global, these laws must continue to evolve to address new challenges, particularly those posed by data-driven tech giants. Ultimately, we should all be mindful of how market power shapes our daily lives from the prices we pay to the freedom we have to choose.

Alia. K

To some matcha is ‘a grass tasting bitter powder,’ yet, to the growing number of matcha ‘fans,’ like me, it is unapologetically addictive, and a core part of my wellness routine - a must have, a weakness.

Matcha is not a new wellness beverage, but a ceremonial grade fine tea powder which originates from Japan where it has been cultivated for over 800 years playing a huge part of history and culture However, more recently, its experienced rapid growth in consumer demand driven by a mix of non-price factors such as its - wellness benefits, social media influence and being completely rebranded as a ‘cleaner alternative’ to its more well established substitutes, such as coffee, especially among younger demographics, who view matcha as trendy and luxurious.

Somewhere between aesthetic Instagram reels and overpriced boutique cafes, there is no doubt that matcha has become, a daily ritual appreciated by many. However, over the past 12 months, that routine has become slightly pricier in the USA, largely driven by what the media calls the ‘Trump Import Tariff Wars’, which were applied to imports from many countries including Japan and China, which are the largest producers of matcha globally.

However, despite much of these tariff related price increases being passed onto the consumer, the matcha craze continues to show price inelastic demand behaviour, and market growth in the USA The demand for matcha is expected to continue to be strong, with the global market expected to grow from US$5.40bn in 2026, to US$9.20bn by 2033, or a CAGR of 7.9% (Gharte, 2026).

The production of high quality matcha is largely concentrated in Japan, exporting more than half of the 5,000 tons of matcha it produces due to the steep rise in global demand (Emilie, 2025), where specific climate conditions and traditional cultivation methods define its quality.

Japan accounts for roughly 50-55% of global matcha export shipments and continues to battle the production shortages which pushed up prices in some cases by over 150% in a single year. This is partly because the supply chain takes years to respond, as tea plants require up to 8 years before being prepared for just production alone.