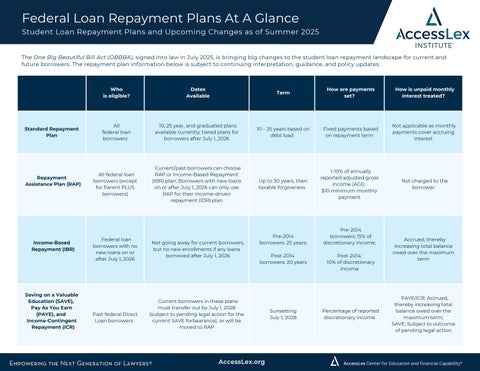

Federal Loan Repayment Plans At A Glance Student Loan Repayment Plans and Upcoming Changes as of Summer 2025 The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, is bringing big changes to the student loan repayment landscape for current and future borrowers. The repayment plan information below is subject to continuing interpretation, guidance, and policy updates.

Standard Repayment Plan

Repayment Assistance Plan (RAP)

Income-Based Repayment (IBR)

Saving on a Valuable Education (SAVE), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR)

Who is eligible?

Dates Available

Term

How are payments set?

How is unpaid monthly interest treated?

All federal loan borrowers

10, 25 year, and graduated plans available currently; tiered plans for borrowers after July 1, 2026

10 – 25 years based on debt load

Fixed payments based on repayment term

Not applicable as monthly payments cover accruing interest

All federal loan borrowers (except for Parent PLUS borrowers)

Current/past borrowers can choose RAP or Income-Based Repayment (IBR) plan; Borrowers with new loans on or after July 1, 2026 can only use RAP for their income-driven repayment (IDR) plan

Up to 30 years, then taxable forgiveness

1-10% of annually reported adjusted gross income (AGI); $10 minimum monthly payment

Not charged to the borrower

Federal loan borrowers with no new loans on or after July 1, 2026

Past federal Direct Loan borrowers

Not going away for current borrowers, but no new enrollments if any loans borrowed after July 1, 2026

Pre-2014 borrowers: 25 years; Post-2014 borrowers: 20 years

Current borrowers in these plans must transfer out by July 1, 2028 (subject to pending legal action for the current SAVE forbearance), or will be moved to RAP

AccessLex.org

Sunsetting July 1, 2028

Pre-2014 borrowers: 15% of discretionary income; Post-2014: 10% of discretionary income

Percentage of reported discretionary income

Accrued, thereby increasing total balance owed over the maximum term

PAYE/ICR: Accrued, thereby increasing total balance owed over the maximum term; SAVE: Subject to outcome of pending legal action

AccessLex Center for Education and Financial Capability®