2025

Q4

SPECIAL BELL INVESTMENTS ISSUE

BELL WEALTH

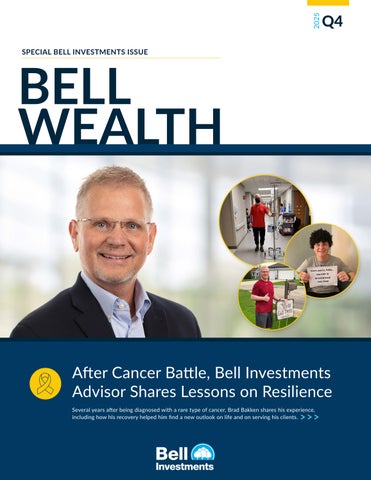

After Cancer Battle, Bell Investments Advisor Shares Lessons on Resilience Several years after being diagnosed with a rare type of cancer, Brad Bakken shares his experience, including how his recovery helped him find a new outlook on life and on serving his clients.