Should You Sell Your Stocks? Three good years in a row feels like a warning. The data suggests otherwise.

Three Good Years in a Row After three consecutive years of above-average equity returns, a question we often field from clients is some version of: “Should I be selling?” We certainly understand the instinct. The S&P 500 returned roughly 26%, 25%, and 18% in 2023, 2024, and 2025, respectively. This represents the longest streak of above-median annual returns since the mid-1990s. Including dividends, the S&P 500 delivered more than 85% cumulatively over that span, a period when a significant portion of market commentary was urging caution or outright skepticism. The result is an investor base that has been well-rewarded (for those who have not sold) but is growing increasingly anxious. This piece attempts to address that anxiety with data rather than intuition.

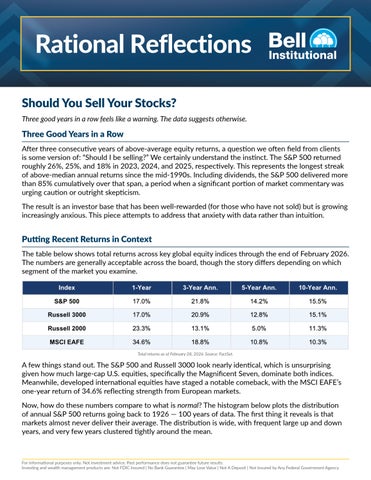

Putting Recent Returns in Context The table below shows total returns across key global equity indices through the end of February 2026. The numbers are generally acceptable across the board, though the story differs depending on which segment of the market you examine.

Total returns as of February 28, 2026. Source: FactSet.

A few things stand out. The S&P 500 and Russell 3000 look nearly identical, which is unsurprising given how much large-cap U.S. equities, specifically the Magnificent Seven, dominate both indices. Meanwhile, developed international equities have staged a notable comeback, with the MSCI EAFE’s one-year return of 34.6% reflecting strength from European markets. Now, how do these numbers compare to what is normal? The histogram below plots the distribution of annual S&P 500 returns going back to 1926 — 100 years of data. The first thing it reveals is that markets almost never deliver their average. The distribution is wide, with frequent large up and down years, and very few years clustered tightly around the mean.

For informational purposes only. Not investment advice. Past performance does not guarantee future results. Investing and wealth management products are: Not FDIC Insured | No Bank Guarantee | May Lose Value | Not A Deposit | Not Insured by Any Federal Government Agency