INGAA Foundation 2025 North American Midstream Infrastructure Report

NORTH AMERICAN MIDSTREAM INFRASTRUCTURE REPORT

Natural Gas Remains the Backbone of our Energy System

PUBLISHED MARCH 13 , 2026

PREPARED BY A CONSORTIUM

This Page Intentionally Left Blank

Executive Summary

Global energy demand is rising rapidly, and North American natural gas is an essential component of meeting that demand For natural gas to fulfill this role, pipelines and related midstream infrastructure must be developed across North America to transport molecules from production basins to end users around the world.

This report finds that, to meet energy demand through 2052, North America will require:

• More than $1 trillion in capital investment across natural gas, oil, natural gas liquids, hydrogen, and CO2 infrastructure, averaging $40-$48 billion annually.

• An estimated 12-24 million cumulative jobs over 25 years (including 2-4 million direct, 4-8 million indirect, and 6-12 million induced jobs), or roughly 414,000-828,000 jobs annually throughout the study period, varying with investment.

• A projected increase in natural gas transmission capacity of 70 billion cubic feet per day (Bcf/d), a 39 percent increase from 2022

• At least 37,000 miles of additional natural gas transmission pipelines (33,800 of which will be in the U.S.) and 103,000 miles of gathering pipelines

• An additional 8.6 to 12.4 million horsepower of compression associated with natural gas transmission, reflecting higher pipeline throughput and network expansion.

Natural gas will see strong, sustained long-term demand through the study period. Figure ES-1 summarizes the required United States’ and Canadian additional natural gas transmission pipeline capacity needed to meet demand under both a Reference Case and Low Carbon Scenario by different study periods. Figure ES-2 illustrates the cumulative natural gas transmission capacity growth over the study period, showing how those additions accumulate over time. Together, the figures distinguish between the timing of capacity additions (ES-1) and the resulting cumulative expansion of the transmission system (ES-2). These projected capacity additions represent baseline requirements and could increase if data center buildout or liquefied natural gas (LNG) exports grow faster than expected in either the report’s Reference Case or Low Carbon Scenario

Figure

The opportunities are substantial, but planning must begin now. To support that planning, The INGAA Foundation 1 commissioned a consortium of experts from the University of Houston, Wood, and ESMIA Consulting to conduct a comprehensive review of future energy needs and the required infrastructure expansion and investment needed to meet that demand. This report reflects current and anticipated market conditions for North American midstream infrastructure, and assesses the scale, location, and timing of the infrastructure expansion required through 2052. For the purposes of this report, midstream infrastructure includes:

• Pipeline systems for natural gas, natural gas liquids (NGLs), crude oil, refined products, hydrogen, and CO₂, including both transmission and, where applicable, gathering lines;

• Compression and pumping stations necessary to maintain flow, pressure, and product integrity; and

• Processing and treatment facilities, including natural gas processing plants, NGL fractionation facilities, and hydrogen conditioning or handling equipment.

The study models outcomes under two primary scenarios:

• A business-as-usual Reference Case, in which existing policies and regulations as of April 1, 2025 remain largely unchanged over the next 25 years, informed by historic and current data from leading U.S. and international energy agencies, regulatory bodies, and industry datasets and updated to reflect H.R. 1, the One Big Beautiful Bill Act of 2025, and the U.S. Energy Information Administration (EIA) Short-Term Energy Outlook (June 2025).

• A Low Carbon Scenario that reflects greenhouse gas (GHG) reduction policies adopted at the state, provincial, and international levels as of April 1, 2025, including measures scheduled to take effect over the next 25 years. It also incorporates binding subnational emissions targets in the U.S. and Canada and applies them directly as jurisdiction-specific constraints that shape fuel selection, energy demand, and infrastructure use without assuming any new nationwide federal climate mandates.

1 The INGAA Foundation was formed in 1990 by the Interstate Natural Gas Association of America (INGAA) to convene industry leaders from natural gas and additional complementary clean energy solutions to identify and address critical matters related to the development, construction, operation, and maintenance of the gas infrastructure value chain through research, engagement, and outreach.

Across both scenarios, the report finds that natural gas remains the backbone of the North American energy system. Even as renewable generation and nuclear power grow and energy efficiency expands, the demand for energy remains too large to be met without natural gas playing a central role. Two market forces dominate the long-term outlook: rapidly rising demand for electricity, particularly from data centers, and sustained growth in LNG exports serving global markets.

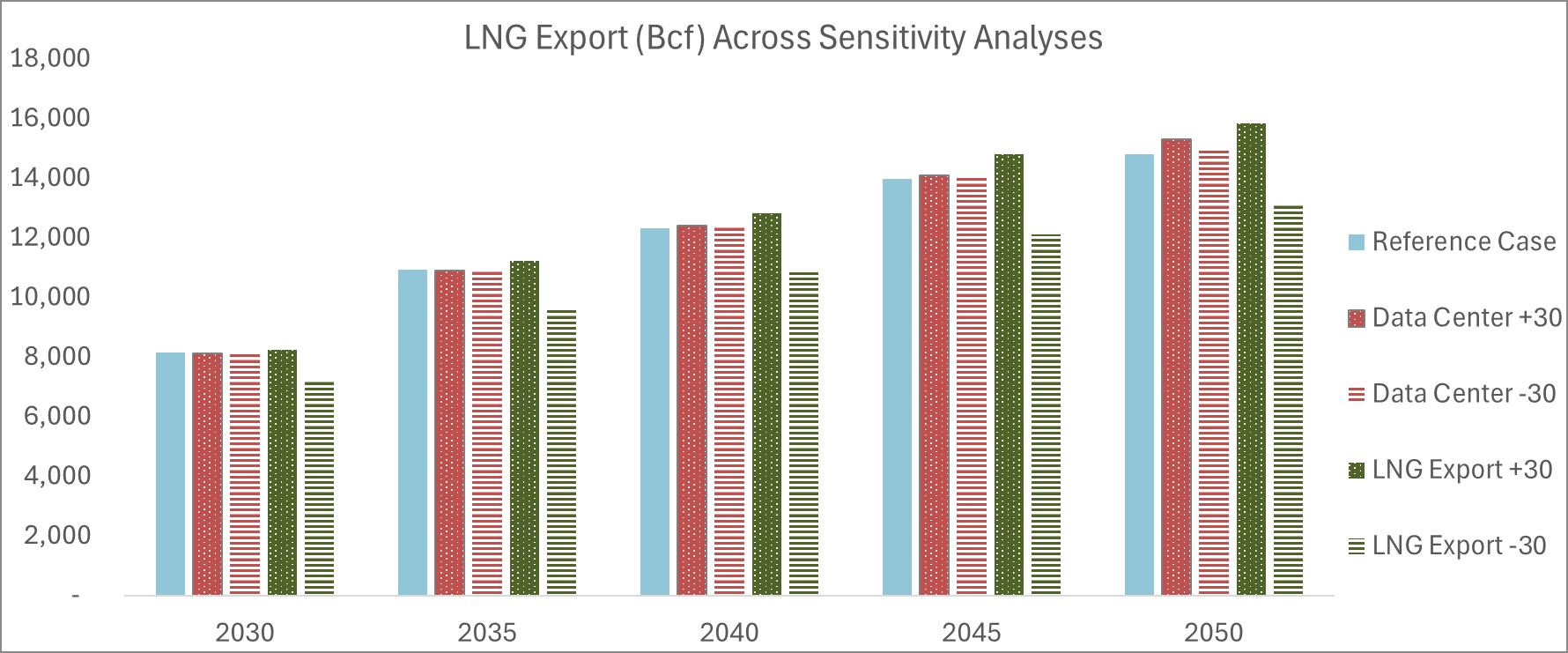

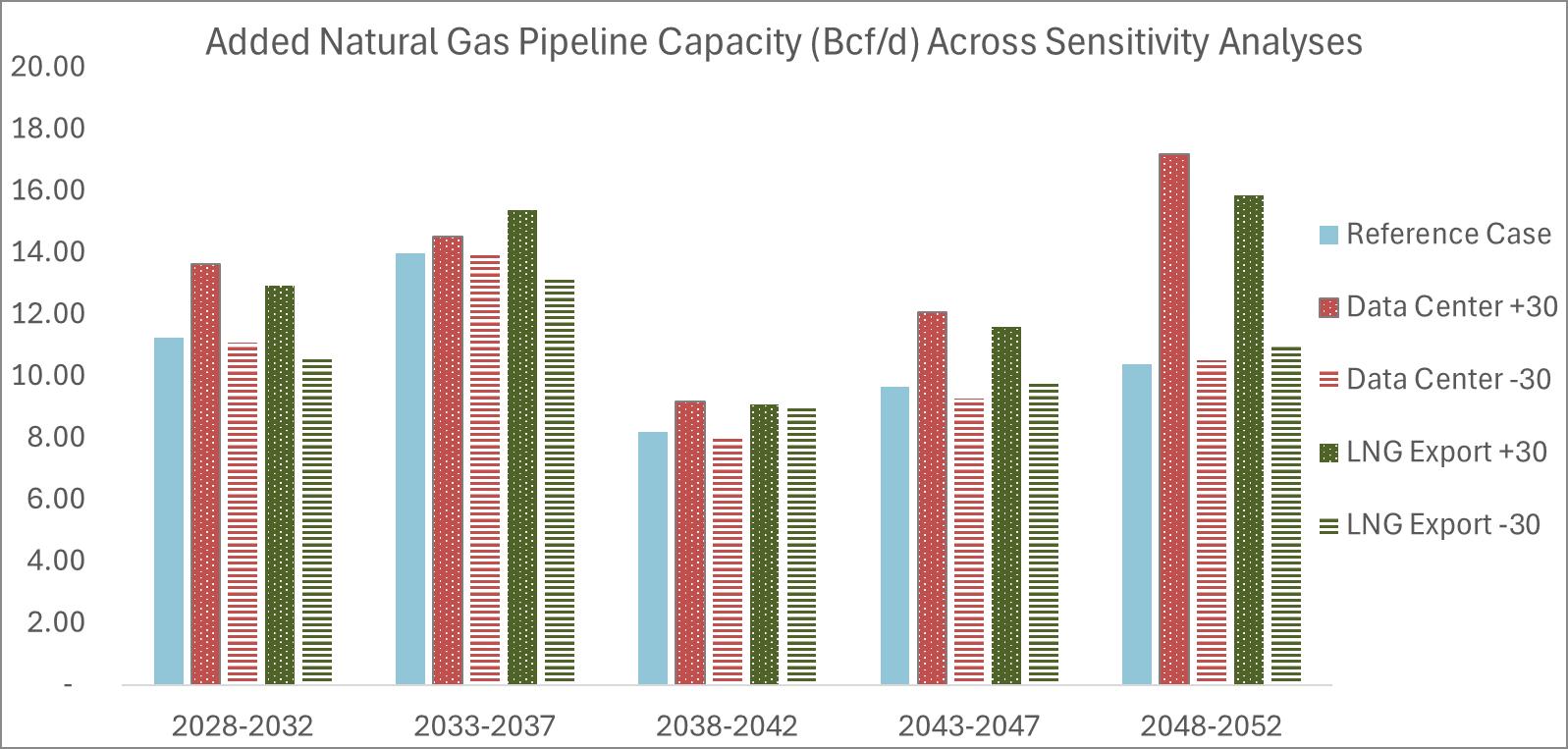

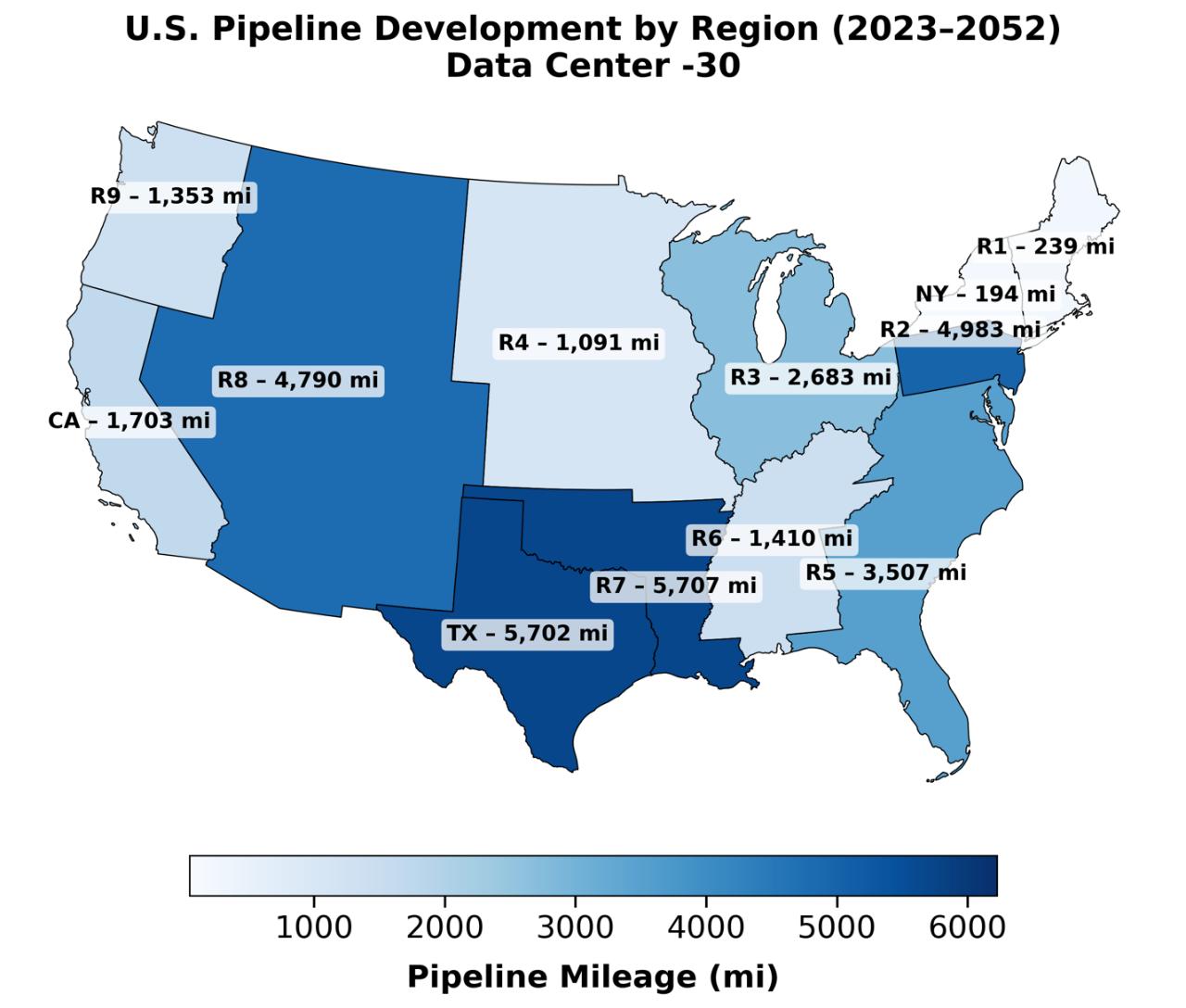

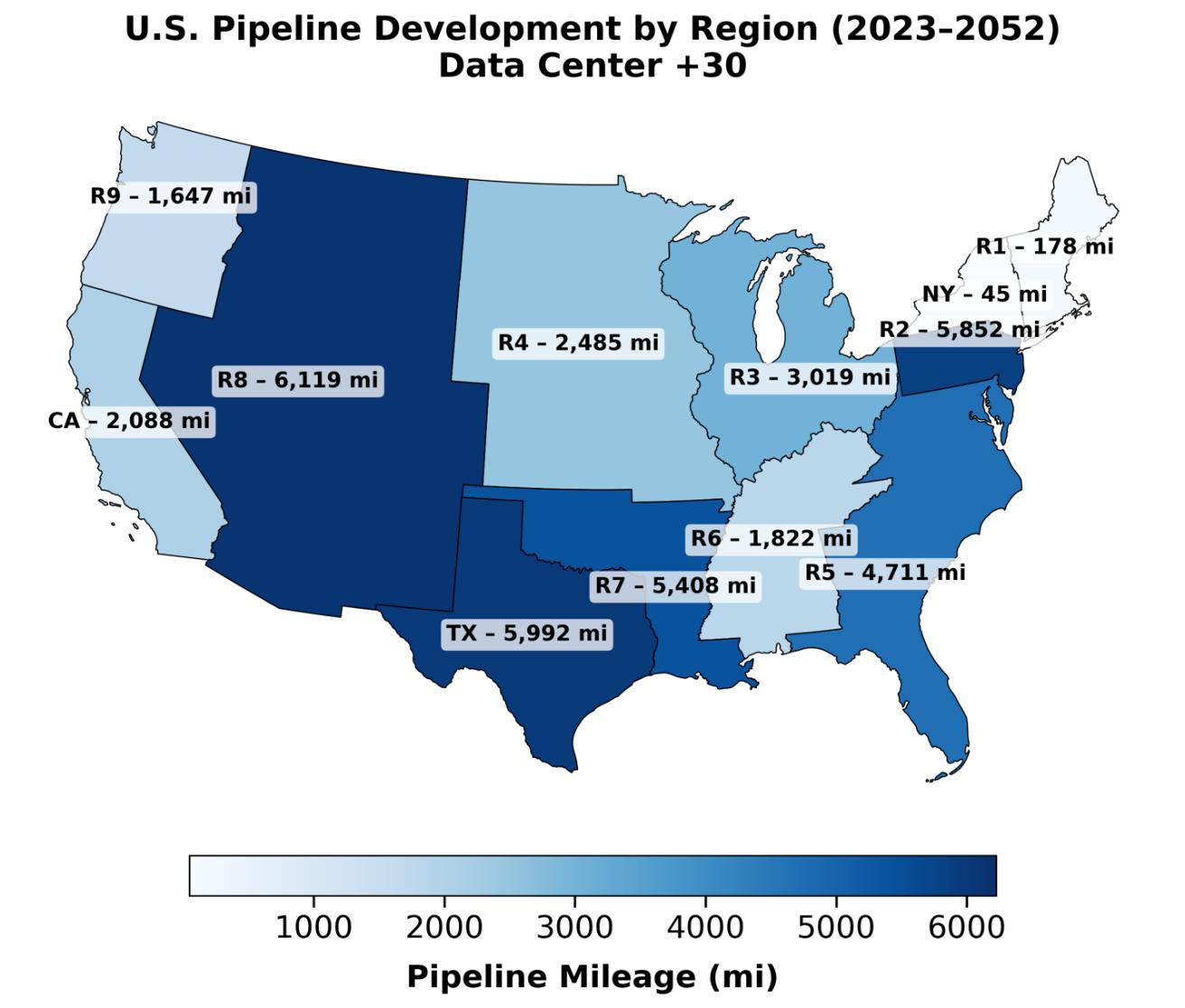

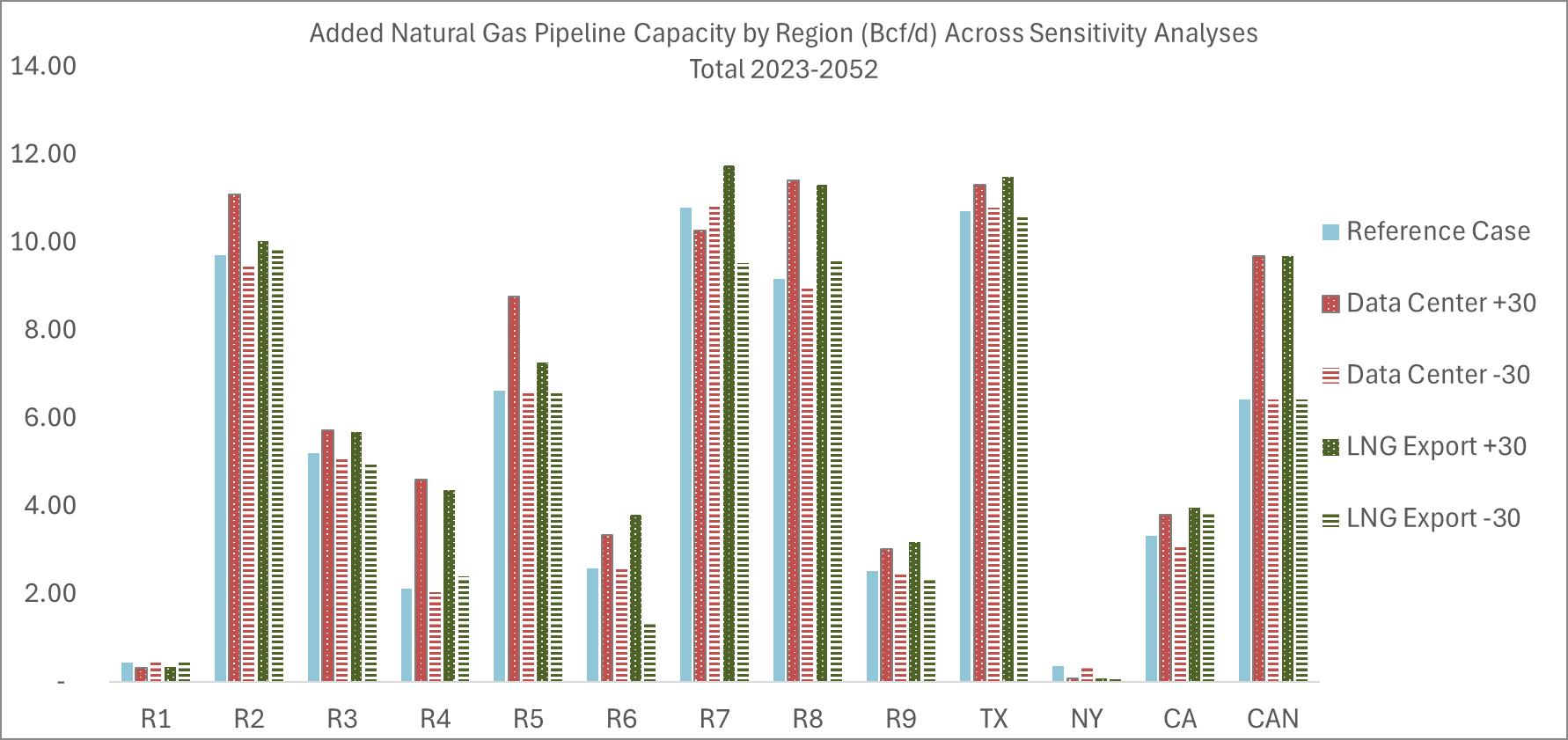

The study also includes a sensitivity analysis of the Reference Case to test how the model responds to variations in the two key market drivers that affect infrastructure requirements. These sensitivities evaluate higher- and lower-trajectory scenarios for LNG exports and data center electricity demand, confirming that natural gas pipeline and compression needs increase materially under stronger-than-anticipated demand conditions. The sensitivity analyses show that the modeled infrastructure requirements are not highly sensitive to moderate variations in key demand drivers. As a result, the estimates presented represent a stable baseline. Higher requirements would be associated with more pronounced shifts in exports, electricity demand growth, or peak demand conditions.

The 2025 Infrastructure Report also finds that:

• Electricity generation from all energy sources is projected to reach 5,900 terawatt hours (TWh) in 2052 in the Reference Case. For context, according to EIA, the U.S. total electricity consumption in 2022 was roughly 4,070 TWh, meaning projected 2052 generation would exceed total U.S. power demand in 2022 by more than 40 percent.

• Data centers are a major contributor to rising electricity demand. The U.S. Department of Energy (DOE) estimates data center energy consumption could reach 800 TWh annually by 2052, up from 300 TWh in 2025.

• Of the $1.2 trillion to $1.4 trillion (2022 USD) in total midstream investment needed over the next 25 years, natural gas pipelines and LNG export facilities account for most of this investment followed by oil pipelines, with the highest investment needs in regions with strong production growth, expanding export capacity, and rising electricity consumption.

• LNG exports represent the single largest source of incremental natural gas demand over the study horizon. Under both the Reference Case and the Low Carbon Scenario, U.S. LNG exports more than triple by 2052, supported by favorable resource availability, competitive pricing, and global efforts to displace higher-emissions fuels. In the Low Carbon Scenario, global climate policies further reinforce LNG demand as importing countries seek lower-

carbon alternatives to coal, increasing the importance of LNG export and interconnected natural gas pipeline infrastructure concentrated along the Gulf Coast.

• U.S. annual natural gas production increases from 36 trillion cubic feet (Tcf) in 2022 to 49 Tcf in 2052 in the Reference Case. Growth is concentrated in Texas, the Middle Atlantic (New Jersey and Pennsylvania), the West South Central (Louisiana, Arkansas, and Oklahoma), the East North Central (Indiana, Illinois, Michigan, Ohio, and Wisconsin), and the Mountain (Arizona, Colorado, Idaho, Montana, New Mexico, Nevada, Utah, and Wyoming) regions. According to EIA, the U.S. consumed roughly 32.50 Tcf of natural gas in 2023, meaning the projected 13 Tcf increase in annual production would account for 40 percent of the entire U.S. natural gas market in 2023

• New to this report, emerging fuels and decarbonization strategies, such as hydrogen production and carbon capture and storage (CCS), were found to incrementally contribute to infrastructure needs, particularly under the Low Carbon Scenario. While these systems remain smaller in scale than natural gas over the study period, they reinforce the need for forward-looking infrastructure planning.

Across the analyzed scenarios, natural gas is needed to meet North America’s rising energy demands through 2052. Natural gas demand continues to grow across a wide range of policy and market conditions, driven by electricity demand from data centers and global LNG consumption, and will continue to grow even as renewables and other low carbon energy sources expand simultaneously. This report provides the analysis and insights needed by the midstream infrastructure industry to begin planning today for the pipelines, compression, and related infrastructure required to meet that demand and ensure a strong, resilient, and secure energy system through 2052.

1. Introduction

1.1. Background

The INGAA Foundation’s 2025 Midstream Infrastructure Report examines the future need for and cost of developing the midstream infrastructure in North America required to meet projected energy demand through 2052. The analysis reflects anticipated economic conditions, public policy considerations, and market dynamics affecting the construction and utilization of midstream infrastructure across the U.S. and Canada.

The INGAA Foundation periodically reassesses North American midstream infrastructure needs to reflect changes in supply, demand, technology, regulation, and public policy. This report represents the ninth edition of that analysis and builds upon prior studies by updating assumptions, extending the analytical horizon through 2052, and incorporating new market developments.

For the purposes of this report, midstream infrastructure refers to the network of physical assets and associated systems that connect energy production to end-use markets by enabling the gathering, transportation, processing, and conditioning of natural gas, natural gas liquids (NGLs), crude oil, refined products, hydrogen, and CO₂ (commodities)

Within this context, midstream infrastructure includes:

• Pipeline systems for natural gas, NGLs, crude oil, refined products, hydrogen, and CO₂, including transmission and, where applicable, gathering lines;

• Compression and pumping stations necessary to maintain flow, pressure, and product integrity;

• Processing and treatment facilities, including natural gas processing plants, NGL fractionation facilities, and hydrogen conditioning or handling equipment.

Collectively, these assets form the operational backbone of the North American energy system, supporting reliable access to markets, system resilience, and the movement of energy commodities required to meet growing demand. Midstream infrastructure also plays a critical role in managing emissions through the transportation of CO₂ for CCS and in facilitating the integration of emerging fuel sources, such as hydrogen and renewable natural gas, alongside traditional hydrocarbons

The analysis covers infrastructure supporting oil, natural gas, LNG, and NGL markets, as well as emerging fuel sources and complementary infrastructure required for CCS. Demand projections consider core domestic natural gas markets, electric power generation (including growth driven by data centers and electrification), residential and commercial consumption, industrial and feedstock use, and export markets, including both pipeline transportation to LNG terminals and the potential export of hydrogen and its derivatives.

The report uses both a qualitative discussion and quantitative analysis, where feasible, to assess factors that can influence the timing, cost, and feasibility of midstream infrastructure development. These factors include permitting and regulatory uncertainty, legal and administrative challenges, jurisdiction-specific restrictions on new natural gas services, and the availability or deployment of technologies that may affect asset utilization or public acceptance. These considerations are treated as risks and uncertainties that may affect infrastructure development trajectories and, consequently, the report’s projections.

As with any long-term infrastructure assessment, the multi-decade timeframe introduces uncertainty related to future demand, costs, regulatory frameworks, and policy direction. Federal, state, and provincial governments in the United States and Canada continue to evolve their approaches to energy policy, climate objectives, and infrastructure development. While many jurisdictions have expressed support for oil, natural gas, hydrogen, CCS, and the infrastructure required to support growing electricity demand, policy positions and regulatory outcomes may vary over time and across regions. Therefore, the projections and findings in this report should be contextualized against evolving market and policy conditions.

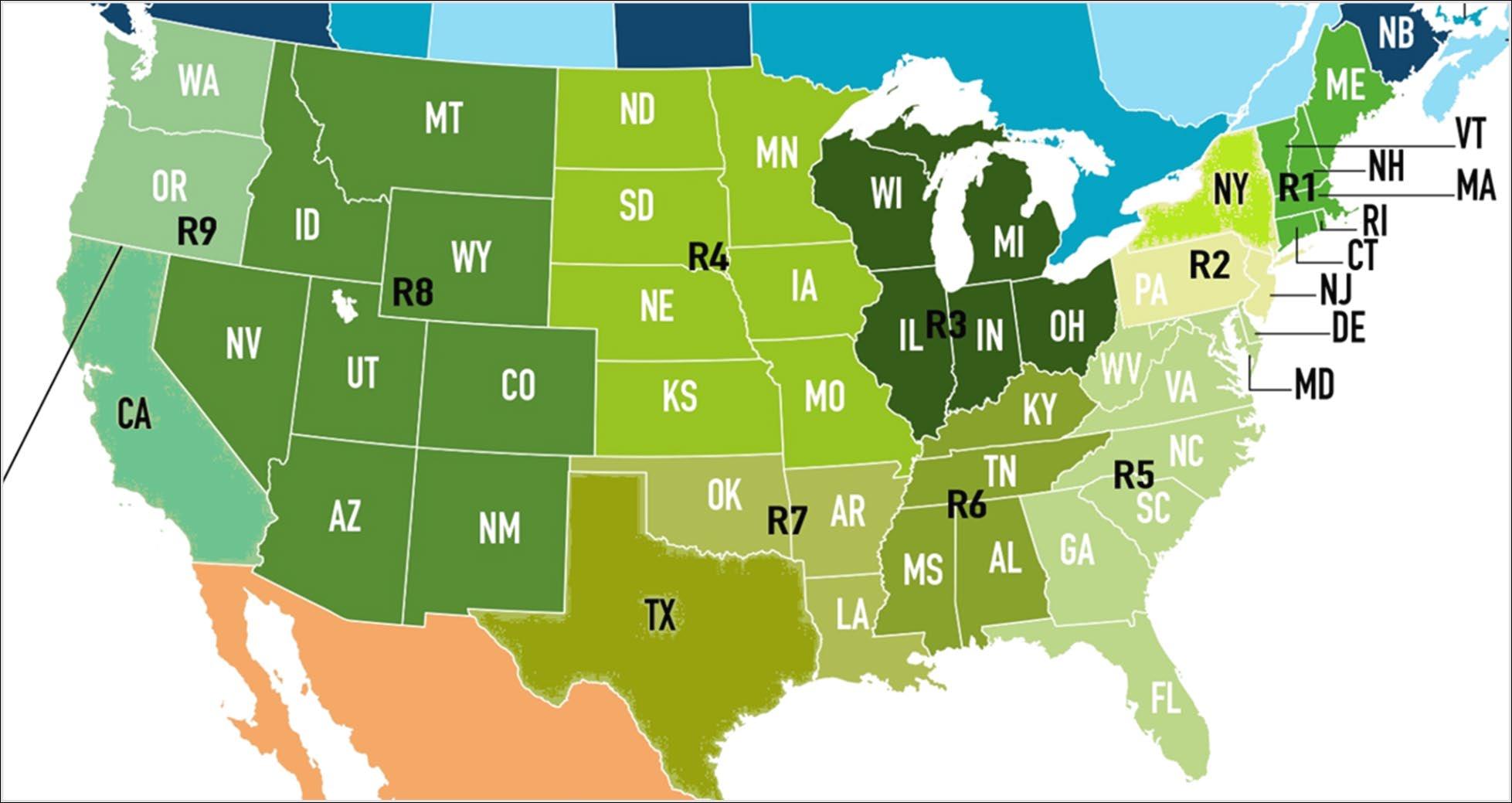

1.2. Study Regions

This report details the current and anticipated outlook and market conditions for U.S. and Canadian midstream infrastructure. It reports data in total volumes and investment dollars, aggregating data by state and province to the extent that detailed information and forecasts are available. U.S. data is assembled by region to accommodate differences in market conditions, costs, and demand across and among the various parts of the country. Those regions are defined in Table 1 and illustrated in Figure 1

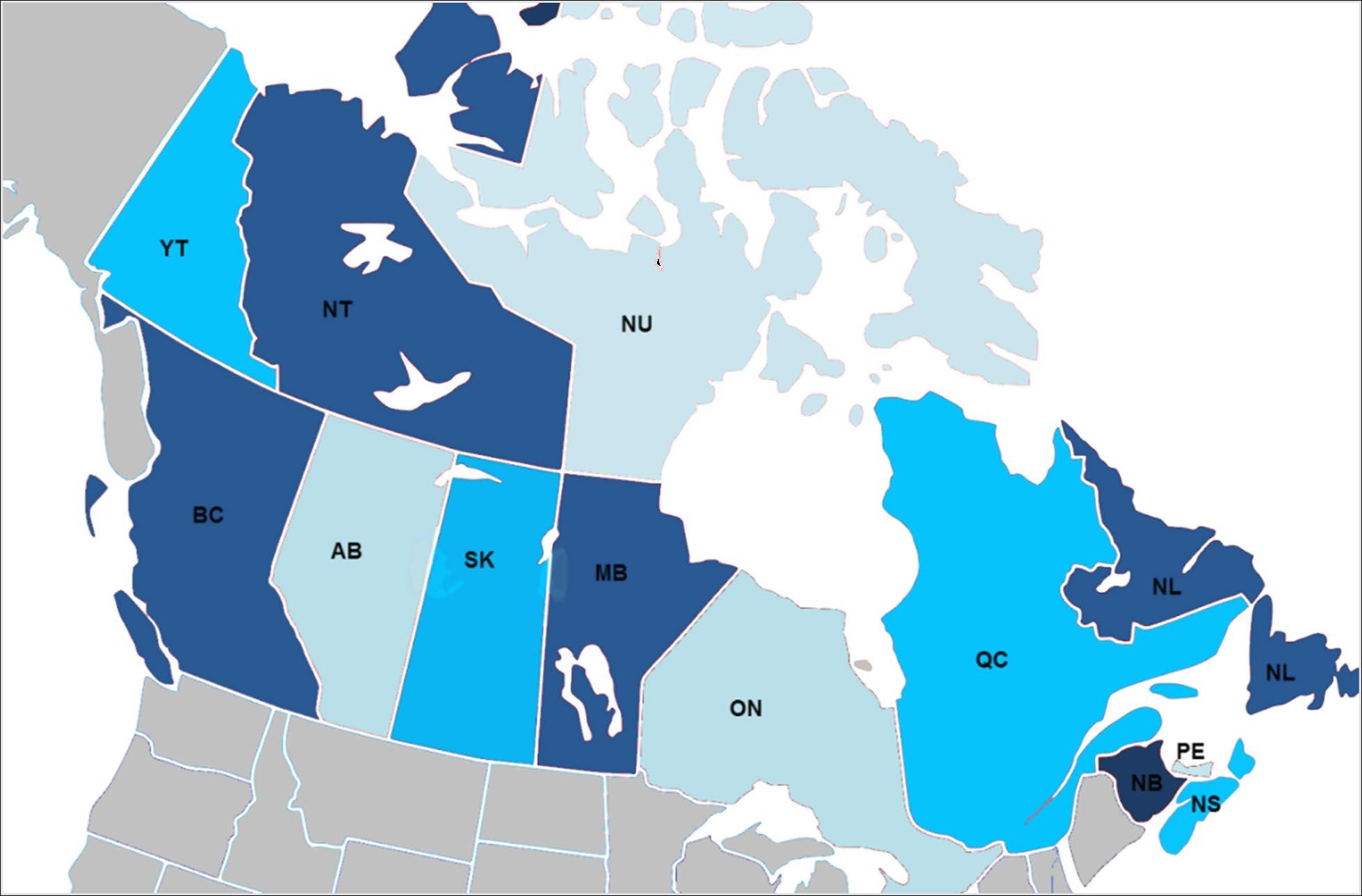

NATEM-Canada covers the 10 Canadian provinces plus the three territories, as described in Table 2 and Figure 2. While data is detailed for every Canadian province and territory, Canadian results are presented on a national basis under the single designation “CAN.”

R1 New England CT, MA, ME, NH, RI, VT

R2 Middle Atlantic NJ, PA

R3 East North Central IN, IL, MI, OH, WI

R4 West North Central IA, KS, MN, MO, ND, NE, SD

R5 South Atlantic DC, DE, FL, GA, MD, NC, SC, VA, WV

R6 East South Central AL, KY, MS, TN

R7 West South Central AR, LA, OK

R8 Mountain AZ, CO, ID, MT, NM, NV, UT, WY

R9 Pacific AK, HI, OR, WA

CA California CA

TX Texas TX

NY New York NY

Table 1 - North American TIMES Energy Model (NATEM)-U.S. Model Regions

Figure 1 - Map of U.S. Study Regions Used in NATEM Model

Table 2 - North American TIMES Energy Model (NATEM)-CANADA Model Regions

Region code

Region Name

AB Alberta

BC British Columbia

MB Manitoba

SK Saskatchewan

ON Ontario

QC Quebec

NB New Brunswick

NL Newfoundland and Labrador

NS Nova Scotia

PE Prince Edward Island

NT Northwest Territories

NU Nunavut

YT Yukon

Figure 2 - Map of Canada Study Regions Used in NATEM Model

1.3. Research Team and Data Sources

The research team consisted of senior leaders from the University of Houston (UH), Wood, and ESMIA Consultants.

The UH team was led by the Division of Energy and Innovation, with support from faculty and staff at the C.T. Bauer College of Business.

Wood, a global leader in engineering and consulting, provided key project management leadership as well as domain expertise for the midstream sector.

ESMIA Consultants, which is based in Canada, contributed a detailed economy-wide energy system model, the North American TIMES Energy Model (NATEM), which was used to model components of the North American energy system to 2052 with an emphasis on natural gas midstream infrastructure. The ESMIA team also provided expertise in the analysis and interpretation of the model results.

The University of Houston used historic and current data to support the techno-economic modeling associated with this report. The data was principally gathered from publicly available sources, including:

The United States Energy Information Agency (EIA)

The International Energy Agency (IEA)

Electric Power Research Institute (EPRI)

Datasets developed by the Oil and Gas Journal (OGJ) Research Organization

Rextag GIS Data for the Energy Sector in the U.S. and Canada

The Federal Energy Regulatory Commission (FERC)

Canadian Energy Regulator (CER)

Canadian Energy Futures Report (2023)

Various state and provincial databases

This data was supplemented to reflect changes made by the enacted H.R. 1, the One Big Beautiful Bill Act of 2025, and updated to include the analysis contained in EIA’s Short-Term Energy Outlook (June 2025). Other policy and regulatory factors were considered as they existed on April 1, 2025.

2. Methodology

The analysis was conducted by a consortium of independent technical and market experts assembled by The INGAA Foundation. The University of Houston provided academic leadership and economic analysis, Wood contributed global engineering, cost, and project development expertise, and ESMIA supplied the NATEM model, an economy-wide techno-economic optimization model used to assess long-term energy system evolution. This multidisciplinary approach integrates market fundamentals, engineering realities, and policy considerations to provide a comprehensive and objective assessment of future midstream infrastructure needs.

2.1. Techno-Economic Modeling Framework (NATEM)

NATEM is a dynamic least-cost optimization model based on the linear programming approach and contains three components:

• The first component is the objective and corresponds to minimizing the net total discounted cost of the entire energy system. A single optimization, which searches for the maximal net total surplus, simulates market equilibrium for each commodity (energy, material, demand). Maximizing the net total surplus (i.e., the sum of producer and consumer surpluses) is operationally done by minimizing the net total cost of the energy system.

• The second component is variables and corresponds mainly to future investments and activities of technologies for each period of time, the amount of energy produced or consumed by technologies, as well as energy imports and exports. An additional output is the implicit price (shadow price) of each energy form, material, and emission, as well as the reduced cost of each technology (reduction required to make a technology competitive).

• The third component is constraints and corresponds to various limits (e.g., the amount of energy resources available) and obligations (energy balances throughout the system and useful energy demand satisfaction).

ESMIA’s modeling approach considered the North American energy economy across all regions with a focus on midstream infrastructure serving the natural gas sector. In doing so:

• ESMIA used both economy-wide NATEM-USA and NATEM-Canada models for all nine census regions and, separately, California, New York, and Texas, and all of Canada (modeled by province) The modeling considered existing and committed policies and regulations affecting the oil and gas industry.

• ESMIA used its advanced representation of existing and future technologies and processes in its model for CCS, hydrogen production and use, ammonia production and use, and the ability to export emerging fuels.

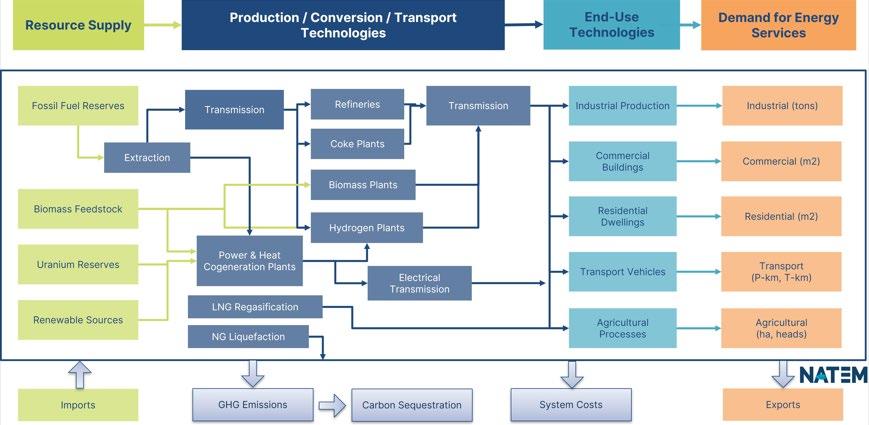

• The model represents the natural gas upstream, midstream, and downstream sectors independently through techno-economic parameters for resource supply (including imports), production/conversion, transportation, end-use technologies, and demand for energy services, including exports.

• The NATEM model was calibrated with energy data sets available from IEA, EIA, the OGJ, Rextag, and other data identified in Section 1.3.

The model runs from 2023 to 2052 in 5-year increments, with 2022 and earlier used for calibration The first modeled period is 2025, representing 2023 to 2027. Additionally, 16 subannual time periods are used to capture seasonal production fluctuations to account for electricity production and hydrogen electrolysis. These 16 time periods represent all four seasons (spring, summer, fall, and winter) and four daily periods (morning peak, midday, evening peak, and night) This temporal granularity balances the need for detail in the electricity production sector (e.g., availability of renewables) and electrolytic hydrogen production (e.g., due to Inflation Reduction Act (IRA) 45V time-matching requirements) against computational constraints.

This analysis utilizes an annual, energy system-level approach for modeling natural gas and oil, which allows the results to provide a clear, comparable view of baseline transmission expansion needs across regions and scenarios. The NATEM model evaluated average annual demand, and did not evaluate peak-day demand, non-ratable demand, seasonal variability, or the amount of additional capacity needed to serve contracted load during planned maintenance periods. The report discusses these considerations and notes that the model may understate required capacity and mileage by up to 1.8 times. The impact of these considerations on the modeled capacity additions are discussed in the results section.

Figure 3 illustrates the comprehensiveness of the NATEM model scope in representing the North American energy system, which is critical for evaluating current and future infrastructure needs. The model inherently considers competition between resources, interactions between demand and supply, and very high technological granularity including representation of thousands of technologies.

2.2. Scenarios

The report develops two core scenarios – the Reference Case and the Low Carbon Scenario – to frame the analysis of future North American midstream infrastructure needs. Together, these scenarios bind a range of plausible policy and market outcomes and provide insight into how differing regulatory environments may affect natural gas demand, infrastructure utilization, and investment requirements over the study period.

2.2.1. Reference Case

The Reference Case serves as the baseline for this analysis and represents a business-asusual outlook based on the existing energy policy environment. It reflects federal, state, provincial, and local policies and regulations in effect in the U.S. and Canada as of April 1, 2025. Under this scenario, no additional climate policies or regulatory measures beyond those already enacted or formally committed are assumed to be implemented during the study period.

The Reference Case assumes continued application of current regulatory frameworks governing energy production, transportation, and consumption, as well as prevailing technology performance and cost trends. One exception to the April 1, 2025 policy cutoff is the inclusion of

Figure 3 - Simplified Representation of North American Energy Systems

provisions contained in the H.R. 1, the One Big Beautiful Bill Act of 2025, which was enacted in mid-2025 and is treated as a committed policy. Macroeconomic conditions, fuel prices, and technology costs are modeled using median assumptions consistent with reference-case projections from publicly available sources.

Within the modeling framework, the Reference Case establishes baseline energy service demands and determines the resulting natural gas, oil, NGL, hydrogen, and CO2 flows required to meet those demands. Midstream infrastructure requirements are then derived endogenously 2 based on the least-cost combination of existing assets, expansions, and new facilities needed to satisfy projected supply and demand under current policy conditions.

2.2.2. Low Carbon Scenario

The Low Carbon Scenario explores the implications of more aggressive GHG reduction efforts in North America and globally. In the U.S., this scenario incorporates binding GHG reduction targets established by individual states that have adopted economy-wide or sector-specific emissions goals. In Canada, the scenario incorporates provincial GHG reduction targets. These constraints are implemented directly in the model by limiting emissions in the relevant jurisdictions, thereby influencing fuel choice, energy consumption patterns, and infrastructure utilization.

Unlike the Reference Case, the Low Carbon Scenario does not assume a uniform national climate policy in either the U.S. or Canada. Instead, it reflects a patchwork of state and province-level climate actions that were in place or formally adopted as of April 1, 2025. This distinction is made explicitly to avoid conflating existing subnational policies with hypothetical future federal mandates. Appendix D summarizes the states’ progress toward their clean energy targets as of the date of April 2025

In addition to domestic policy differences, the Low Carbon Scenario assumes stronger global climate action relative to the Reference Case. While specific international policies such as carbon border adjustment mechanisms, explicit carbon pricing, or tighter global emissions standards are not modeled individually, their combined effect is represented through alternative assumptions for international energy markets. These assumptions influence global natural gas

2 Endogenously refers to variables that are determined within the model based on their internal relationships, assumptions, and constraints, rather than being specified as external inputs.

demand, particularly for LNG, and therefore affect North American production, pipeline flows, and export infrastructure requirements. In this context, “higher” global climate action refers to a policy environment in which emissions constraints are more stringent and more widely adopted than in the Reference Case, altering fuel demand and trade patterns.

As in the Reference Case, technology costs and performance are modeled using central cost assumptions. Differences in outcomes between the two scenarios are driven primarily by policyinduced changes in emissions constraints, fuel demand, and market conditions rather than by assumptions about technological breakthroughs.

Together, these two scenarios provide a structured framework for evaluating how midstream infrastructure needs may evolve under differing policy and market conditions. The Reference Case illustrates infrastructure requirements under a continuation of today’s policy environment, while the Low Carbon Scenario highlights how more aggressive climate action, implemented largely through state and provincial policies and reinforced by global market shifts, could alter demand for natural gas and related midstream assets.

2.3. Assumptions and Criteria

The North American energy system is both complex and dynamic. In collaboration with The Foundation’s steering committee (see Appendix I) and with support from the study’s leadership team, ESMIA developed a set of assumptions. In order to accurately interpret the study’s results, it is essential to understand the modeling assumptions upon which the principal scenarios and sensitivities are based, including energy service demand, midstream infrastructure needs, and pipeline cost

2.3.1. Energy Service Demand

Energy service demands are the primary drivers of model outcomes and represent underlying “useful” demand, such as industrial output or building floor space requiring heating or cooling. Demand for natural gas is therefore not specified explicitly but is derived endogenously based on these service demands and other economic and technological factors. For example, higher Gross Domestic Product (GDP) growth increases projected industrial activity which, in turn, can lead to greater demand for natural gas and competing fuels.

Macroeconomic inputs for the U.S. – including GDP and population growth – are sourced from the U.S. Bureau of Economic Analysis (2023) for state-level GDP, and EIA’s Annual Energy

Outlook 2025 for population and national projections. For Canadian inputs, macroeconomic assumptions are drawn from Canada’s Energy Futures 2023 published by the Canadian Energy Regulator. These variables are not entered directly into the NATEM model; instead, they are used to develop initial projections of energy service demand. Tables 3 and 4 illustrate trends in GDP for both the U.S. and Canada, a key factor in determining future energy demand.

Source: Annual Energy Outlook 2025, EIA; Bureau of Economic Analysis

Table 4 - Projections for CAN GDP (Millions 2023 CAD)

Source: Canada’s Energy Future 2023, Canada Energy Regulator

2.3.2. Energy Prices and International LNG Demand

Energy prices, together with regional resource availability, interregional connectivity, and production costs, influence modeled import and export flows. Trade prices and volumes between domestic regions are determined endogenously within the model, with international price assumptions serving as a benchmark against which regional production and transportation economics are evaluated.

Table 5 projects global oil and natural gas prices used to represent international import and export markets and are sourced from EIA’s Annual Energy Outlook 2025. Near-term price assumptions for 2025 reflect updates from EIA’s Short-Term Energy Outlook (June 2025). These prices provide an external reference for international trade within the modeling framework.

Table 3 - Projections for U.S. GDP (Billions 2023 USD)

Table 5 - Projections for World Energy Prices (2022 USD/Mbtu for gas and 2022 USD/barrel)

Natural Gas

Source: Annual Energy Outlook 2025, EIA.

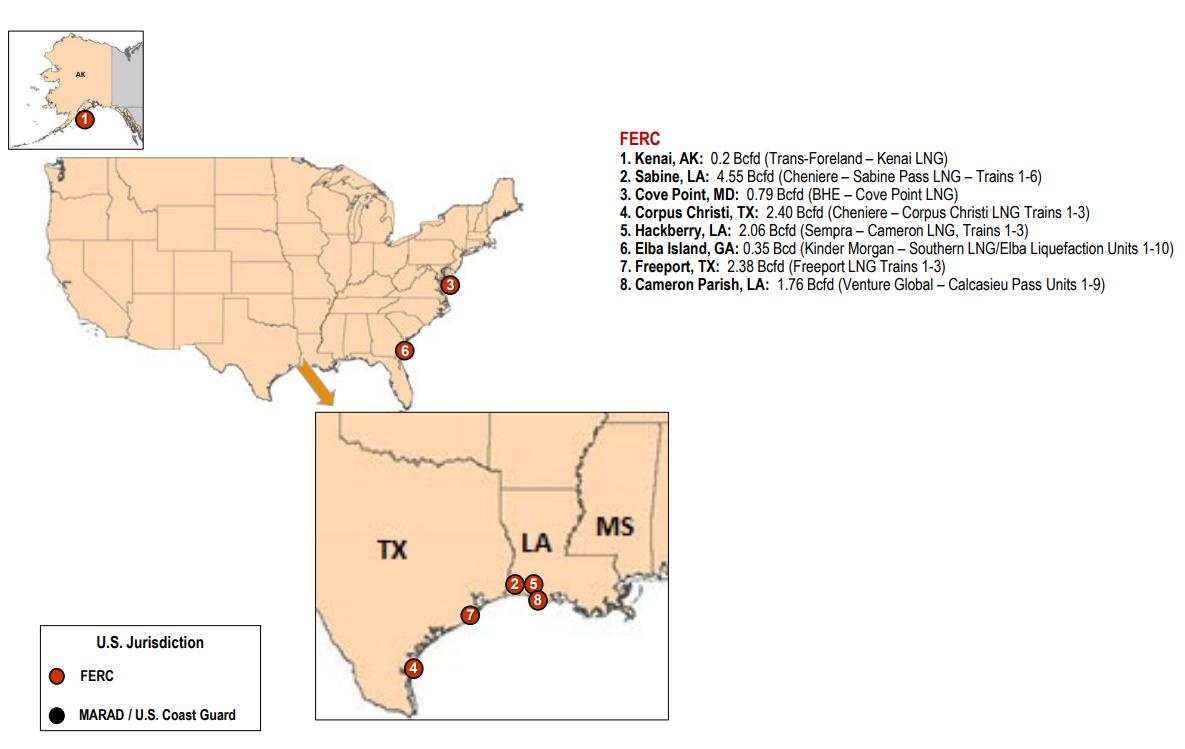

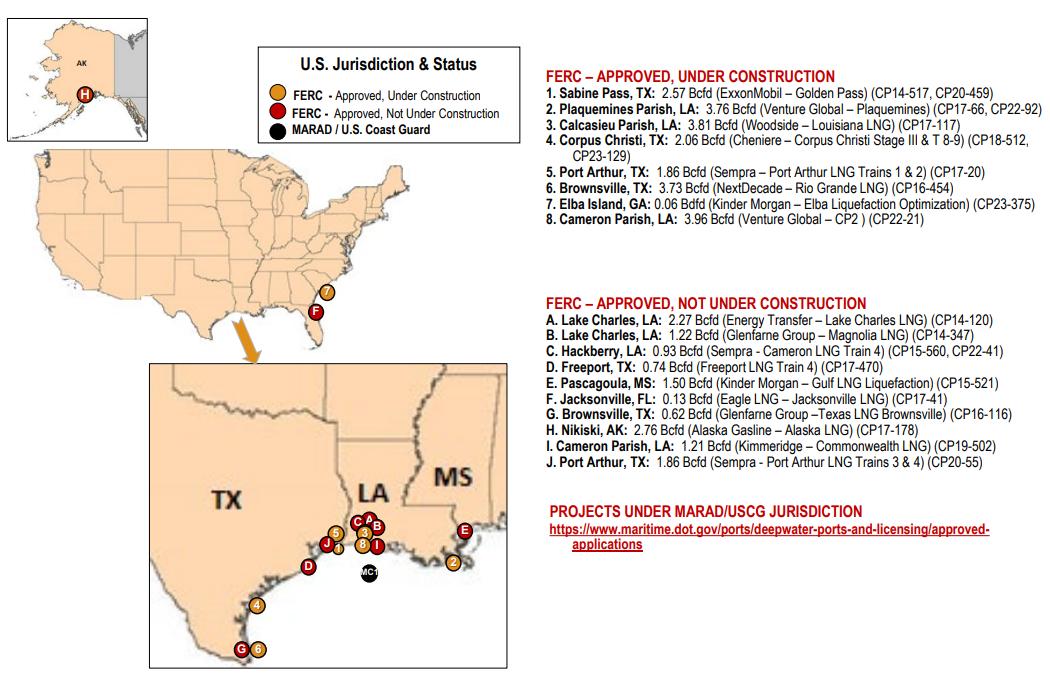

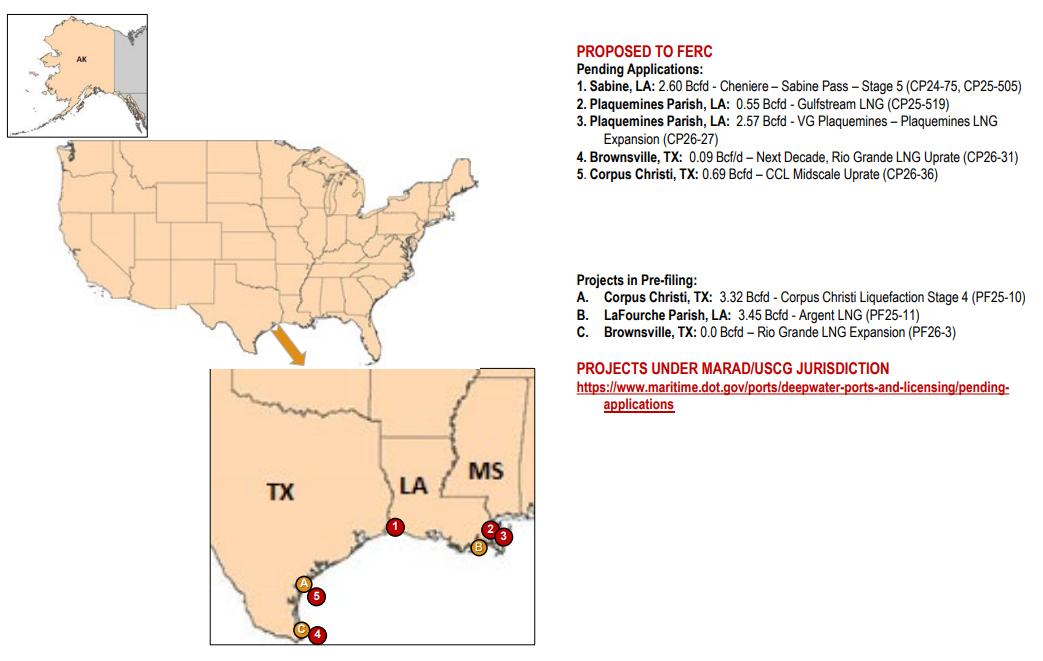

International LNG demand is assumed to be a key driver for the natural gas sector in the U.S. in the upcoming years. Based on a review of public data from FERC through April 2025, U.S. LNG export capacity was calculated from existing, proposed, under construction, and approved LNG export terminals in both scenarios. See Table 6 and Appendix K.

Table 6 - Projections for Maximum U.S. LNG Export

Source: Federal Energy Regulatory Commission, April 2025.

(Bcf/d)

This report assumes global action on climate will lead emerging countries to replace coal with less carbon-intensive fuels, including LNG. As a result, export capacity is significantly higher in the Low Carbon Scenario.

2.3.3.

Demand from Data Centers

Data centers consume significant amounts of electricity, and natural gas is the largest single fuel source used for electricity generation in the U.S. The scale of data center growth is therefore likely to impact gas use, although clean electricity targets will also affect the sector. DOE estimates that by 2052, demand from data centers could reach 800 TWh per year, as shown in Table 9 S&P Global Ratings estimates that U.S. data centers’ energy use could increase natural gas demand between 3 bcf/d and 6 bcf/d by 2030. The NATEM model optimizes the electricity mix in line with policies described in this document.

Based on recent industry trends, data center demand will continue to grow in the medium-tolong term as shown below in Table 7. Appendix J contains an image from the National Renewable Energy Laboratory (NREL) which depicts data center infrastructure in the U.S. in 2025

Source: Lawrence Berkeley National Laboratory, 2024 Report on U.S. Data Center Energy Use

The May 2024 Electric Power Research Institute (EPRI) report, “Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption,” estimates data center power consumption by region in 2023. This report utilizes EPRI’s regional analysis and assumes that the regional share of data centers’ power consumption will not change prospectively from 2023 to 2052, thus enabling demand estimations from data centers for each region through 2052. Tables 8 and 9 illustrate demand growth, which will remain concentrated in the South Atlantic region (R5), with both Texas and the Mountain region (R8) maintaining a strong share.

Table 7 – U.S. Electricity Demand from Data Centers (TWh)

Table 8 - Share of Data Center Power Consumption by Region for 2023

Source: EPRI, Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption (May 2024) Table 9 - Future Data Center Electricity Demand by Region (TWh)

2.3.4.

Midstream Infrastructure Needs

For simplicity, the model assumes as its baseline that existing midstream infrastructure is operating in equilibrium with current supply and demand conditions and, therefore, the development or expansion of new midstream infrastructure – including natural gas and oil pipelines, compression, and processing facilities – must occur to meet any increase in demand beyond current levels. Reallocation or repurposing of existing assets cannot be assumed to satisfy any incremental increase in demand in this analysis. This assumption enables the evaluation of long-term regional and inter-regional market dynamics over a 25-year study horizon.

To estimate midstream infrastructure needs in terms of physical units – such as pipeline mileage, number of compressors, and associated facilities – this study relied upon a set of standardized assumptions:

• Pipeline length and mileage per facility: Based on typical distances observed between production areas, processing plants, and transmission networks, with data gathered from Rextag.

• Pipeline diameter: Assumed average sizes tied to expected throughput requirements by commodity type (gas, oil, CO2, or hydrogen).

• Compression and pumping requirements: Calculated as horsepower (hp) or pump capacity per mile of pipeline, based on historic performance and design benchmarks.

These assumptions make it possible to scale future needs: every increase in consumption translates into a corresponding need for new natural gas, oil, CO2, or hydrogen pipelines, compressors, processing, and gathering facilities. Table 10 lists the assumptions used to estimate new midstream infrastructure development.

Table 10 - Assumptions for New Infrastructure Development

Infrastructure Component

Crude Oil and Natural Gas Gathering Lines

Processing Plants

Assumptions

Assumes an average diameter of 6 inches and a length of 6 miles.

Assumes incremental gas production will require new investment in processing capacity.

Existing and future pipeline infrastructure is categorized into 3 distinct categories:

Small/short pipelines: These have an average diameter of 12 inches and an average length of 40 miles. They typically serve as lateral pipelines connecting industrial facilities, distribution networks, or a power plant.

Crude Oil, Natural Gas, NGL Pipelines

Compressor Station Requirement for Natural Gas Pipelines

Pumping Requirement for Oil Pipelines

Medium pipelines: These have an average diameter of 24 inches and an average length of 120 miles, typically representing intrastate transmission pipelines.

Large/long pipelines: These have an average diameter of 36 inches and an average length of 250 miles, typically corresponding to interstate transmission pipelines.

Additional pipeline capacity introduced within a region must maintain the same proportional distribution as existing infrastructure.

Assumes 10,000 hp is required every 40 miles for small and medium pipelines

Assumes 25,000 hp is required every 60 miles for large pipelines.

Assumes 7,000 hp is required every 40 miles for small and medium pipelines.

Assumes 20,000 hp is required every 60 miles for large pipelines.

Small/short pipelines: average diameter of 10 inches and average length of 20 miles.

Hydrogen Pipelines

Hydrogen Compressors

CO₂ Pipelines

2.3.5. Pipeline Costs

Medium pipelines: average diameter of 14 inches and average length of 185 miles.

Large/long pipelines: average diameter of 16 inches and average length of 300 miles.

Assumes 15,000 hp is required every 60 miles

Assumes an average diameter of 12 inches and an average length of 150 miles.

The historical unit costs for oil and natural gas pipeline and compressor/pumping station construction are based on data from the Oil & Gas Journal survey of U.S. projects completed between 1980 and 2022. Due to limited cost data for 2020–2022, when pipeline construction

was near its lowest point, average pipeline construction costs for those years, and through 2023, were estimated using a regression analysis of historical trends. A statistical regression was performed between average U.S. pipeline construction costs and GDP over historical periods, with the resulting coefficients applied to forecast average U.S. pipeline construction costs from 2023 to 2052 based on projected GDP figures.

The analysis uses the 2019 national average U.S. pipeline unit cost of $351,600 per diameter inch-mile 3 (expressed in 2022 USD) as the starting benchmark. To account for regional variability, adjustment factors were derived from historical data to quantify the deviation of regional costs from the national average.

Table 11 illustrates this variability. For example, costs in R1, which corresponds to New England, are more than twice that in Texas.

R4

3 Pipeline costs are calculated from a composite unit cost based on historical project actual costs. These are simplified to “dollars per diameter inch-mile,” e.g., 100 miles of 30-inch diameter pipe would have an estimated total cost of 100 x 30 x $351,600 = $1,054,800,000.

Table 11 - Pipeline Regional Cost Factors

For gathering lines, cost estimates were also derived from Oil & Gas Journal data; only projects with pipelines less than 12 inches in diameter were included to better reflect typical gathering systems. In addition, adjustments were made to isolate and refine cost components related to right-of-way acquisition and environmental permitting. The average unit cost for U.S. gathering lines in 2019 was approximately $87,800 per diameter inch-mile, expressed in 2022 USD. Costs are not broken down by region due to the low variability between regions.

2.3.6. Compressor Costs

The report estimates and projects construction costs for natural gas compressor stations using a similar methodology. In this case, the dataset obtained from the Oil & Gas Journal was completed through 2022, eliminating the need for regression-based gap-filling for recent years. This allowed for a more direct analysis of historical cost trends and provided a robust basis for forward-looking projections

Based on available data, the average construction cost for U.S. natural gas-fired compressor stations was approximately $3,900 per hp (in 2022 USD) as of 2022. This is a national average and incorporates a range of project types and sizes. As with pipelines, regional cost differentials were accounted for using historical cost dispersion metrics, as shown in Table 12 Since there is little publicly available information regarding the costs for pumping stations as needed for oil and NGL lines, the study assumes pumping costs on average and over the entire system will approximate the cost of compression.

Table 12 - Compressor Regional Cost Factors

(New England)

R2 (Middle Atlantic)

R3 (East North Central)

R4 (West North Central)

R5 (South Atlantic)

R6 (East South Central) 0.89

R7 (West South Central) 0.92

R8 (Mountain)

2.3.7. Other Costs

Appendix C provides detailed cost assumptions for other infrastructure components, including power plant construction, residential natural gas appliances, direct air capture systems, and hydrogen production facilities with CCS. These estimates encompass capital cost breakdowns, technology-specific parameters, and relevant installation factors, offering a comprehensive view of the investment requirements across various segments of the energy system.

Gas processing costs, excluding compression, are estimated at approximately $650,000 per million cubic feet per day (MMcf/d) of processing capacity based on industry reports from Evercore and Energy Transfer Partners and project reported costs, including of the Beckville processing plant built by Enbridge Energy Partners and the Bighorn gas processing plant built by ONEOK. Capital costs for LNG export facilities, based on data from DOE export applications and other public sources, average between $5 billion and $6 billion per Bcf/d of export capacity (2022 USD)

Lease equipment costs are derived from historical EIA Oil and Gas Lease Equipment and Operating Cost data, adjusted to 2022 USD using the Producer Price Index from the U.S. Bureau of Labor Statistics. These estimates indicate average lease equipment costs of approximately

$350,000 per gas well and $520,000 per oil well. These costs escalate at the same rate as pipeline and compressor costs.

2.3.8. Key Policies

Policies are modeled in NATEM using various constraints and model parameters, such as subsidies, which can be applied for specific technologies if they meet certain conditions. Key policies and impacts modeled for this study, including those in the enacted IRA of 2022, were updated to reflect changes made in the H.R. 1, the One Big Beautiful Bill Act of 2025. Those changes are expected to considerably reduce the influence of IRA policies, as tax credits phase out for many clean energy investments. The end of the electric vehicle tax credit, for example, may support long-term demand for oil, though technology cost competitiveness will still play a role. CCS benefits under the new law, which aligns the tax credit for CO₂ used in enhanced oil recovery and commercial utilization with the higher geologic storage rate at $85/ton 4

2.4. Special Considerations

Many factors, including macroeconomic factors, may impact future demand for natural gas, oil, CO2, and hydrogen pipelines. Each has the potential to impact the cost or timing of infrastructure development, but they do not lend themselves to modeling due to the difficulty of quantifying their impact on input parameters or high uncertainty.

Nevertheless, the following factors are sufficiently important to warrant consideration. This report should be considered alongside implications of the below listed special considerations to determine if changes to costs, as well as the market, will have an impact on the industry.

4 For more detail, see Appendices C, F-J.

2.4.1. DUC Wells and DTIL Wells

“Drilled but Uncompleted” wells, often referred to as DUCs, are oil and gas wells that have been drilled to their target depth but have not been completed.

Tracking the inventory of DUC wells offers insight into industry activity levels, responsiveness to market signals, and potential future production capacity. EIA’s Drilling Productivity Report indicates 4,510 DUCs in April 2024, including 893 DUCs in the Permian Basin.

“Deferred Turn in Line” (DTIL) wells have been completed but not turned to production pending a price the operator finds sufficient. In the fourth quarter of 2024, for example, between three and four Bcf/d of gas came online rapidly from DTIL wells after cold weather increased demand and prices.

DUC and DTIL inventory indicate industry’s ability to bring natural gas wells into production quickly, necessitating infrastructure to bring this new production to market.

2.4.2. Permitting

The midstream infrastructure industry is the backbone of the energy system, ensuring the safe and efficient transportation of vital resources. Continued expansion of this sector is impacted by a complex web of federal, state, and local permitting processes. These permits govern everything from pipeline routes and construction methods to environmental impact mitigation and operational safety.

The current permitting system is characterized by lengthy delays, overlapping reviews, and inconsistent requirements across agencies, which can lead to project delays, increased costs, and uncertainty for developers. Interstate natural gas pipeline operators, for example, must obtain permits from the Federal Energy Regulatory Commission (FERC), the U.S. Army Corps of Engineers (USACE), and various state environmental agencies, which can involve extensive informal and formal public outreach and engagement, environmental analyses, and inter-agency coordination. Pipelines can spend months or years navigating this regulatory process, and litigation over government authorizations can add additional years Protracted timelines can hinder the timely development of necessary energy infrastructure, potentially impacting energy security and economic growth.

The permitting process for the midstream industry significantly impacts developers’ ability to make needed, timely, expansions and should be considered as a potential impact to achieving required buildout to meet demand. All of these elements make the current permitting process

lengthy, expensive, and uncertain. There are ongoing bi-partisan policy discussions happening in the U.S. Congress to pass a comprehensive permitting reform package that, if successful, would provide the clarity and certainty needed to build the infrastructure required to meet growing energy demand.

2.4.3. Supply Chain, Tariffs, and International Trade

Impacts to supply chains also affect midstream infrastructure development. Lead times for certain equipment, including compressors and gas turbines, have significantly lengthened, and pipeline operators report challenges in securing sufficient skilled labor for construction, safety, and related activities. If these conditions persist, they could delay project schedules and increase capital costs.

Trade policy developments, including the imposition of tariffs, may also influence midstream project economics. Tariffs on imported equipment, including but not limited to turbines, compressors, or pipeline-grade steel, may increase input costs for infrastructure projects. Tariff policy may impact longer-term domestic manufacturing capacity, but those uncertainties are not considered for this report

Retaliatory tariffs imposed by trading partners also could affect the economics of U.S. energy exports, including pipeline exports of natural gas to Mexico and Canada and seaborne exports of LNG, hydrogen, or ammonia produced from natural gas. Changes in relative costs could influence export volumes and market competitiveness.

Supply chain constraints and trade-related cost pressures represent factors that could influence the timing, cost, and scale of future midstream infrastructure development and associated energy flows.

3. Results and Interpretation

Identifying the regions in which energy production is expected to increase, and the magnitude of that growth, is essential to assessing future midstream infrastructure requirements. Interpretation of the techno-economic modeling results presented in this report requires an understanding of the key assumptions and parameters underlying the Reference Case.

• For each commodity implicated in the study, the model assumes the market is in equilibrium, i.e., the supply of natural gas to be produced or added to expected import volumes will equal the amount of natural gas needed to meet anticipated demand, including exports.

• The model assumes markets will make the most economic choice of fuels and investments to achieve the lowest energy cost. For the alternative Low Carbon Scenario, the analysis introduces constraints consistent with response to climate concerns. These include increasing government regulation of GHG emissions, which tends to limit the use of fossil fuels compared to the Reference Case.

• In any supply-demand model, it is necessary to define upper bounds for recovery of natural gas resources; the model assumes an upper limit on natural gas production consistent with EIA’s Annual Energy Outlook 2025, High-Oil and Gas Supply Scenario.

As used in the context of this report, “legacy midstream” refers to the energy commodities analyzed in previous years’ INGAA Foundation infrastructure reports – natural gas, crude oil, and natural gas liquids. In this edition, the definition of midstream has been expanded to include emerging fuels and technologies, such as hydrogen and CCS transportation. These are presented with more detail in Section 5.

3.1. Legacy Midstream Findings – Natural

Gas,

Oil, and Natural Gas Liquids

3.1.1.

Natural Gas

North America has significant natural gas resources. According to the Potential Gas Committee September 2025 report “Potential Supply of Natural Gas in the United States,” 5 total future gas supply in the U.S , as of year-end 2024, was 4,500 Tcf. That represents a 15 percent increase over the comparable year-end estimate in 2022. The Canadian Gas Association estimates that Canada has more than 1,300 Tcf of natural gas.

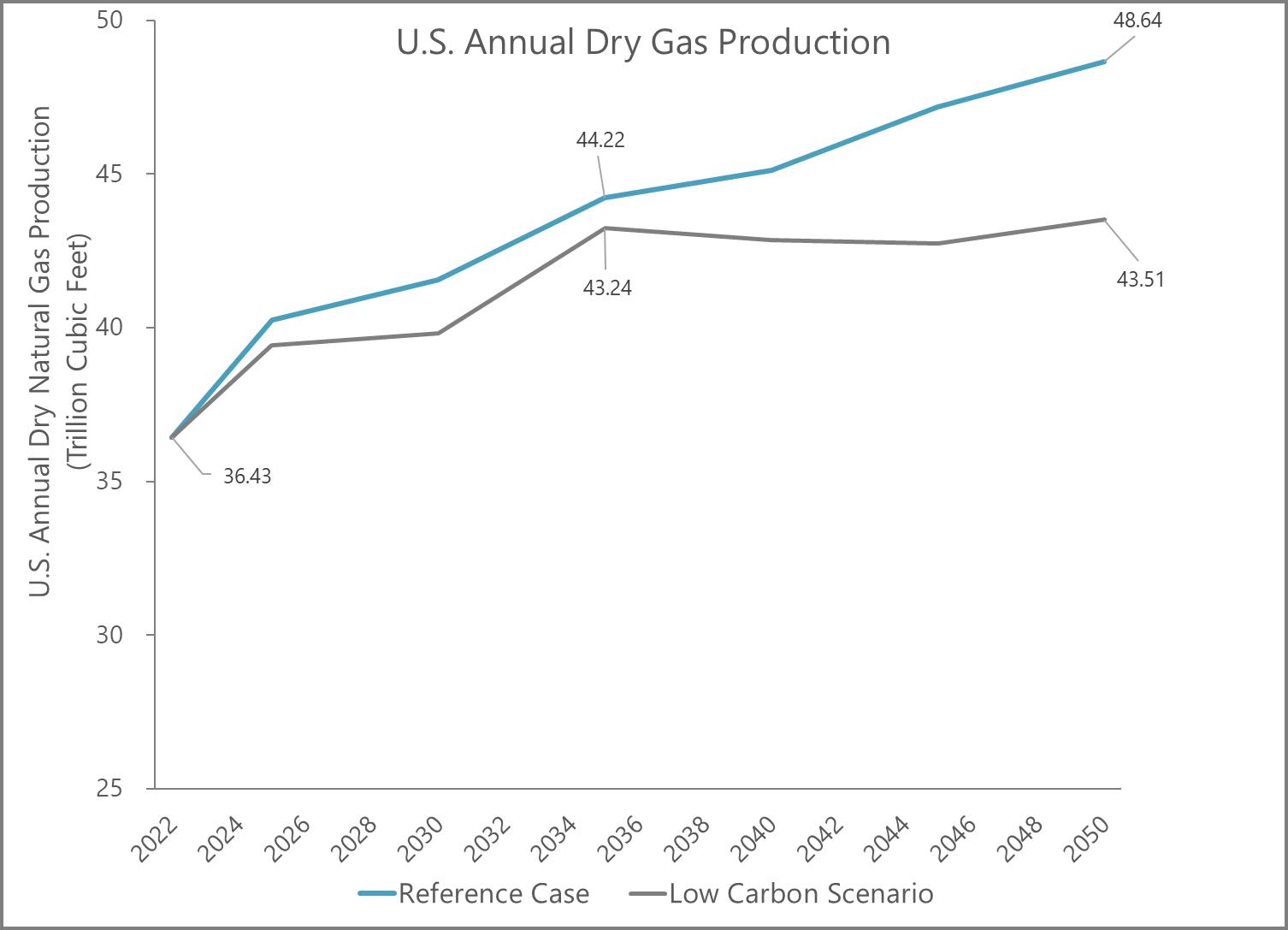

Natural gas production and consumption will continue to grow, powering the need for new infrastructure. Dry gas production in the U.S. will rise from 36 Tcf/yr in 2022 to 42 Tcf/yr in 2030 in the Reference Case. Increased LNG export capacity coming online and increased domestic consumption, namely electricity demand from data centers, drive this increase. Production grows more modestly after 2030, reaching 49 Tcf/yr in 2052, as illustrated in Figure 4 and detailed in Table 13.

The Low Carbon Scenario finds a similar significant rate of increase to 2030, when production reaches 40 Tcf/yr Production peaks in 2035 at 43 Tcf/yr, before rebounding to 44 Tcf/yr in 2052

The lower gas production in the Low Carbon Scenario is a direct result of GHG emission targets, which may reduce domestic consumption of natural gas while limiting production and downstream activities (including liquefaction).

Table 14 provides similar data for dry natural gas production in Canada for both the Reference Case and the Low Carbon Scenario.

5 The Potential Gas Committee (PGC) is a group of approximately 80 volunteer geoscientists and engineers that provides biennial assessments of technically recoverable U.S. natural gas yet-to-find resources since 1964 The PGC is supported by the Potential Gas Agency (PGA) at the Colorado School of Mines.

The analysis finds a more modest increase in dry natural gas production in Canada and less variation between the Reference Case and Low Carbon Scenario Nevertheless, the Low Carbon Scenario sees more moderate growth as a result of GHG reduction targets.

Figure 4 - U.S. Annual Dry Gas Production

Table 13 - U.S. Annual Dry Gas Production

Table 14 - Canada Annual Dry Gas Production

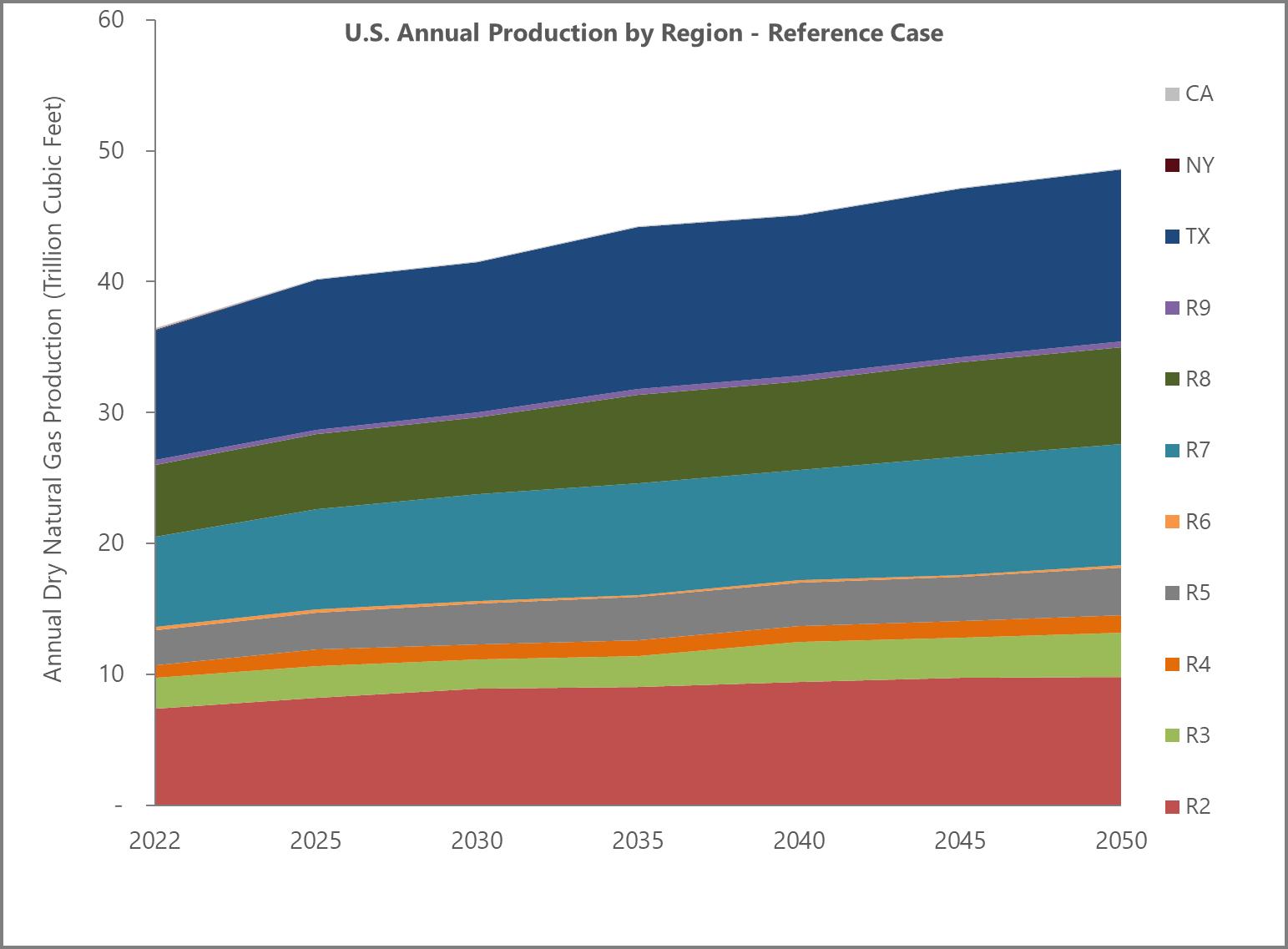

In the Reference Case, the U.S. dry natural gas market is projected to grow by approximately 34 percent between 2022 and 2052, driven by strong production increases across several key regions, as illustrated by Figure 5 and Table 15. The Northeast, particularly the Middle Atlantic and East North Central regions (R2 and R3), benefit from prolific output from the Marcellus and Utica shales. In the South, Texas and the rest of West South Central (R7) region show robust growth fueled by the Permian, Eagle Ford, and Haynesville basins. The West North Central (R4) and Mountain (R8) regions (which includes New Mexico, and Colorado), contribute to growth through plays like the Anadarko Basin, San Juan Basin, and Mancos Shale. Even Alaska (R9) is expected to see modest gains, while California and the East South Central region (R6) show more stable or fluctuating trends

This regional expansion is tied to the development of major basins that support dry gas production. The Appalachian Basin remains the largest contributor, with high-efficiency wells and proximity to demand centers. The Haynesville Shale is gaining momentum due to its proximity to LNG export terminals and high initial productivity. The Permian Basin, while primarily an oil play, is a major source of associated gas. Emerging basins like Mancos Shale within the San Juan Basin offer long-term potential, especially with infrastructure improvements. These trends reflect a dynamic shift in U.S. energy strategy, emphasizing domestic production, export capacity, and industrial demand for natural gas

Figure 5 - U.S. Annual Dry Gas Production by Region - Reference Case

Table 15 - U.S. Annual Dry Gas Production by Region, Reference Case 6

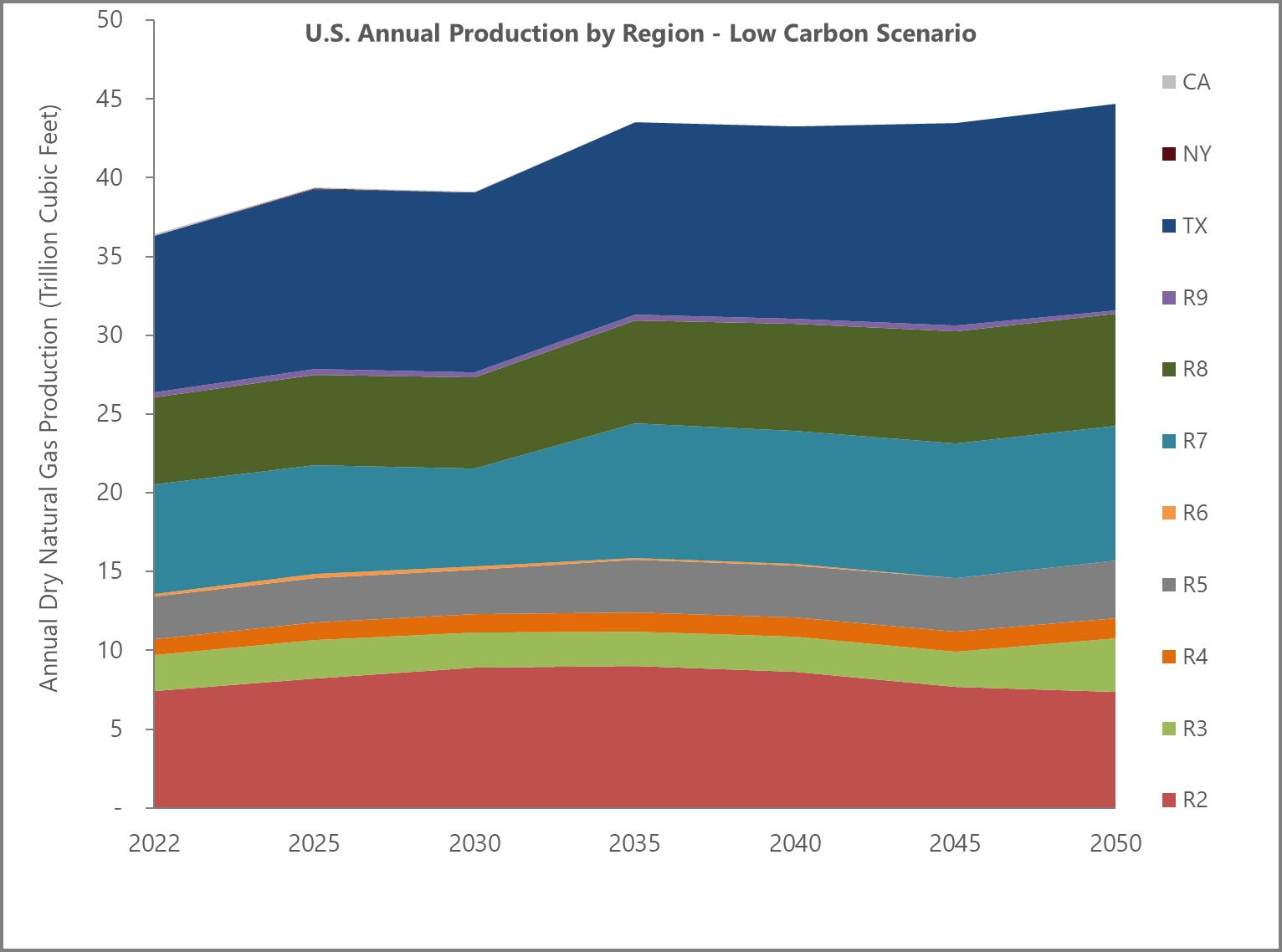

In contrast to the Reference Case, regional growth under the Low Carbon Scenario is more limited. As illustrated by Figure 6 and Table 16, although the Middle Atlantic region (R2) shows initial growth, long-term production resembles 2022 levels. This region has relatively stringent GHG reduction targets, reaching 80 percent in 2052, and neighboring regions including New England (R1) and New York do as well, which will reduce regional gas demand. The West South Central region (R7), on the other hand, reduces gas production in the short term to meet its 2030 GHG reduction target of 22 percent. Long term, natural gas production grows (albeit less than in the Reference Case) as reductions are made across other sectors, such as transportation, buildings, electricity generation, and refineries. The development of biofuels and hydrogen production with carbon capture also allows emission cuts. Texas, which has no emission reduction targets, will see long-term growth equivalent to the Reference Case. The Mountain region (R8) sees slightly more limited growth, by about 4 percent. Alaska and California both see declines in production. California has the strictest GHG regulations among the regions

6 The reader may notice small discrepancies in the data table total values presented here and the sum of the row values, due to rounding of the annual values. These small discrepancies do not alter in any way the conclusions of this report.

Figure 6 –

U.S. Annual Gas Production by Region - Low Carbon Scenario

Table 16 - Annual U.S. Gas Production by Region, Low Carbon Scenario

Carbon Scenario

3.1.2. Oil

Crude production is expected to rise to 13.1 million barrels per day (MMbp/d) in 2030, up from 11.8 MMbp/d in 2020, in the Reference Case, dropping to 11.0 MMbp/d in 2052

In the Low Carbon Scenario, crude oil demand peaks in 2030 at approximately 13.0 MMbp/d, dropping to 10.5 MMbp/d by 2052 This is primarily due to increased use of electric vehicles in the light-duty market and, to a lesser degree, more efficient internal combustion engines Table 17 illustrates these trends.

Electrification gradually reduces use of refined oil products domestically; the initial rise in oil production is sustained by a projected increase in crude oil exports, up 50 percent by 2030, and relative to 2022, up by 100 percent in 2052 under the Reference Case. The same trend is observed in the Low Carbon Scenario, although in practice more stringent global climate policies could result in demand for crude oil and oil products remaining relatively flat.

Exports will depend on trends in international oil markets: high adoption of electric vehicles globally could depress crude oil production further; conversely, a strong export market for crude oil and associated products could sustain domestic production over the medium term Demand for aviation fuel is projected to remain strong, and the model projects an increase in imports to meet this demand

Considered together, this presents a challenge for oil refineries because demand for different products, in particular gasoline vs aviation fuel, trend differently Refineries may prioritize jet fuel production, which typically requires different processing conditions. Operational implications for refineries include:

• Reconfiguration of units (e.g., hydrocrackers, distillation towers) to shift yield toward jet fuel

• Feedstock adjustments: Heavier crudes may be favored for jet fuel production.

• Economic trade-offs: Refineries may face reduced overall throughput if they are unable to balance product demand efficiently.

The downstream sector is currently grappling with these changing market dynamics.

Tables 18 and 19 illustrate anticipated oil production in various regions over the report time horizon.

Table 17 - U.S. Annual Oil Production

Table 18 - U.S. Annual Oil Production by Region, Reference Case

Table 19 - U.S. Annual Oil Production by Region, Low Carbon Scenario

Carbon Scenario

Canadian oil production data, highlighted in Table 20, demonstrates a modest decrease in 2025 followed by equally modest increases through 2052. The Reference Case and Low Carbon Scenario take different paths to the same 2052 production levels. While Canada also experiences decreasing domestic demand due to light-duty vehicle electrification, growth in the export of crude and oil products sustains continued growth in production. Canadian exports in absolute terms remain below U.S. exports.

Tables 21 and 22 reflect the amount of energy derived from the production of various oil products in both the Reference Case and Low Carbon Scenario in the U.S. While the rates of decline for each product differ through 2052, most show a decline in both the Reference Case and Low Carbon Scenario As consumer demand for both gasoline and diesel drop because of

Table 20 - Canada Annual Oil Production

the adoption of electric vehicles, reduced refinery production drives a reduction in crude production. Tables 23 and 24 reflect the same data for Canada.

Table 21 - U.S. Annual Oil Products Production by Type, Reference Case

Table 22 - U.S. Annual Oil Products Production by Type, Low Carbon Scenario

In Canada, fossil transportation fuel production goes up for the export market, with some shifts in other petroleum products over the period.

3.1.3. Electricity Demand

Electricity generation capacity in the U.S. has grown only modestly in recent years, with population growth and the increase in electric vehicles offset by increased efficiency. Data center demand, along with increasing electrification, may change that.

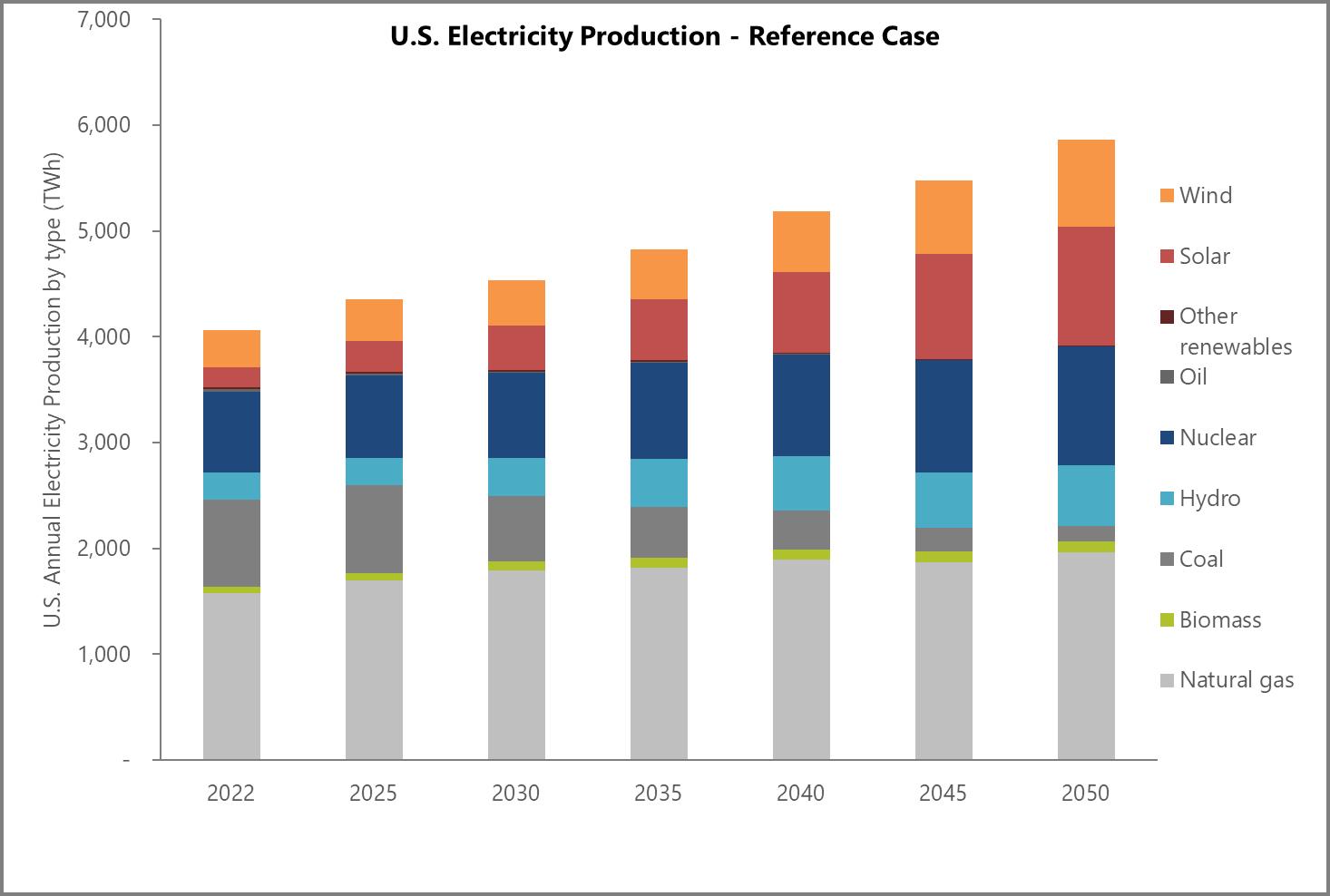

Demonstrated in Figure 7 and Table 25, electricity production from all sources was 4,063 TWh in 2022 and is expected to rise to 5,858 TWh in 2052. This electricity production is expected to be primarily met by renewables in regions with favorable wind and solar resources, such as solar in California and the South Atlantic (R5) region. Nuclear and hydro will experience significant growth as well. Even still, the analysis finds a 24 percent increase in electricity produced from natural gas (with and without CCS), rising to 1,962 TWh by 2052 from 1,582 TWh in 2022 and accounting for around 33 percent of total generation in 2052 7 The increased demand for natural gas, even as its share as a source of generating fuel drops, reflects both the growth of the total volume of electricity and the ongoing competitiveness of natural gas power plants to meet the need for reliability, resilience, renewable firming, and load-following in regions with high dependence on renewables.

Firming and load-following 8 with natural gas-fired generation requires greater natural gas deliverability, increasing the potential pipeline and storage capacity needed to meet rapidly changing demand for natural gas, even when renewables decrease daily average gas demand.

7 Natural gas accounted for 39 percent of U.S. electricity generation in 2022, according to EIA.

8 Firming refers to the use of dispatchable generation resources to ensure electricity supply is available when variable renewable generation (such as wind or solar) is unavailable or produces less output than expected. In this context, natural gas–fired generation provides firm generating capacity that can be called upon to maintain system reliability during periods of low renewable output.

Load-following describes the ability of a generation resource to adjust output in response to short-term changes in electricity demand or variability in renewable generation. Natural gas–fired power plants are commonly used for load-following due to their operational flexibility, including relatively fast ramp rates and frequent start-stop capability.

In the U.S., the Low Carbon Scenario sees electricity generation rise to 6,297 TWh by 2052, shown in Table 26, and higher natural gas electricity production than 2022 levels although less demand for natural gas-fueled generation than in the Reference Case Natural gas-fired generation will reach 1,733 TWh in 2052, which is somewhat lower than the Reference Case, largely due to stringent GHG reduction targets, and represents a growth of 10 percent relative to 2022. Under this scenario, natural gas will make up 27.5 percent of total generation in 2052. The remaining growth is primarily fueled by solar, wind, and nuclear power. Higher production relative to the Reference Case is driven primarily by increased electrification of transportation.

Table 26 - U.S. Annual Electricity Production by Type, Low Carbon Scenario

Electricity generation in Canada increases in both scenarios (Tables 27 and 28) but because carbon emissions restraints are already prevalent in Canada and its provinces, natural gas-fired generation is lower in both scenarios. In particular, the Clean Electricity Regulations encourage the use of gas for peaking purposes only, with long-term emission limits leading to a pronounced drop in natural-gas generation by 2052.

3.1.4. LNG Exports and Domestic Natural Gas Consumption

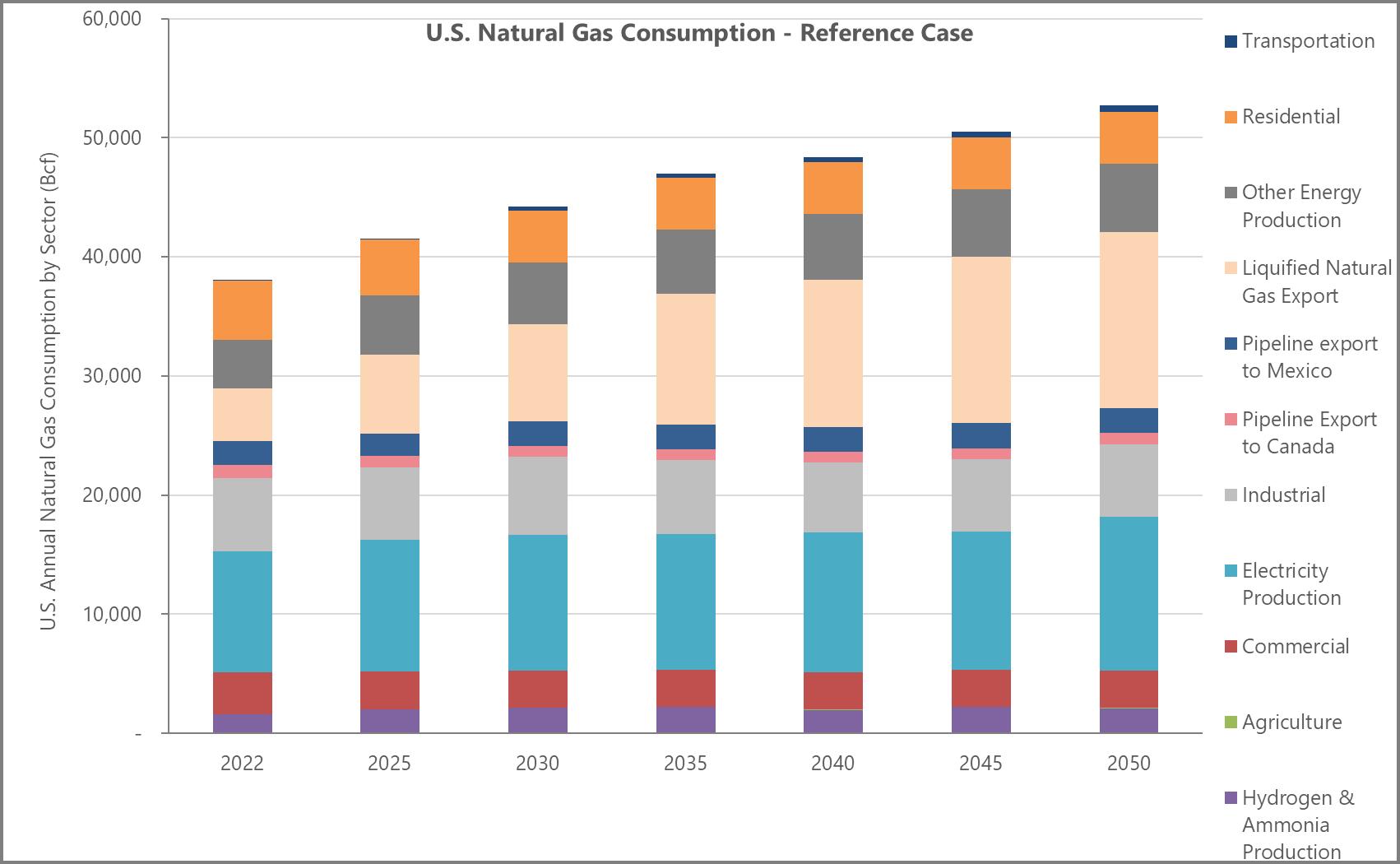

An assessment of future natural gas end-use demand is a critical input to determining the scale and scope of additional midstream infrastructure the North American industry will be required to develop over the coming years. In the Reference Case, as illustrated by Figure 8 and Table 29, natural gas consumption in the U.S. varies by sector but rises more than 38 percent overall, principally driven by LNG exports and data center demand.

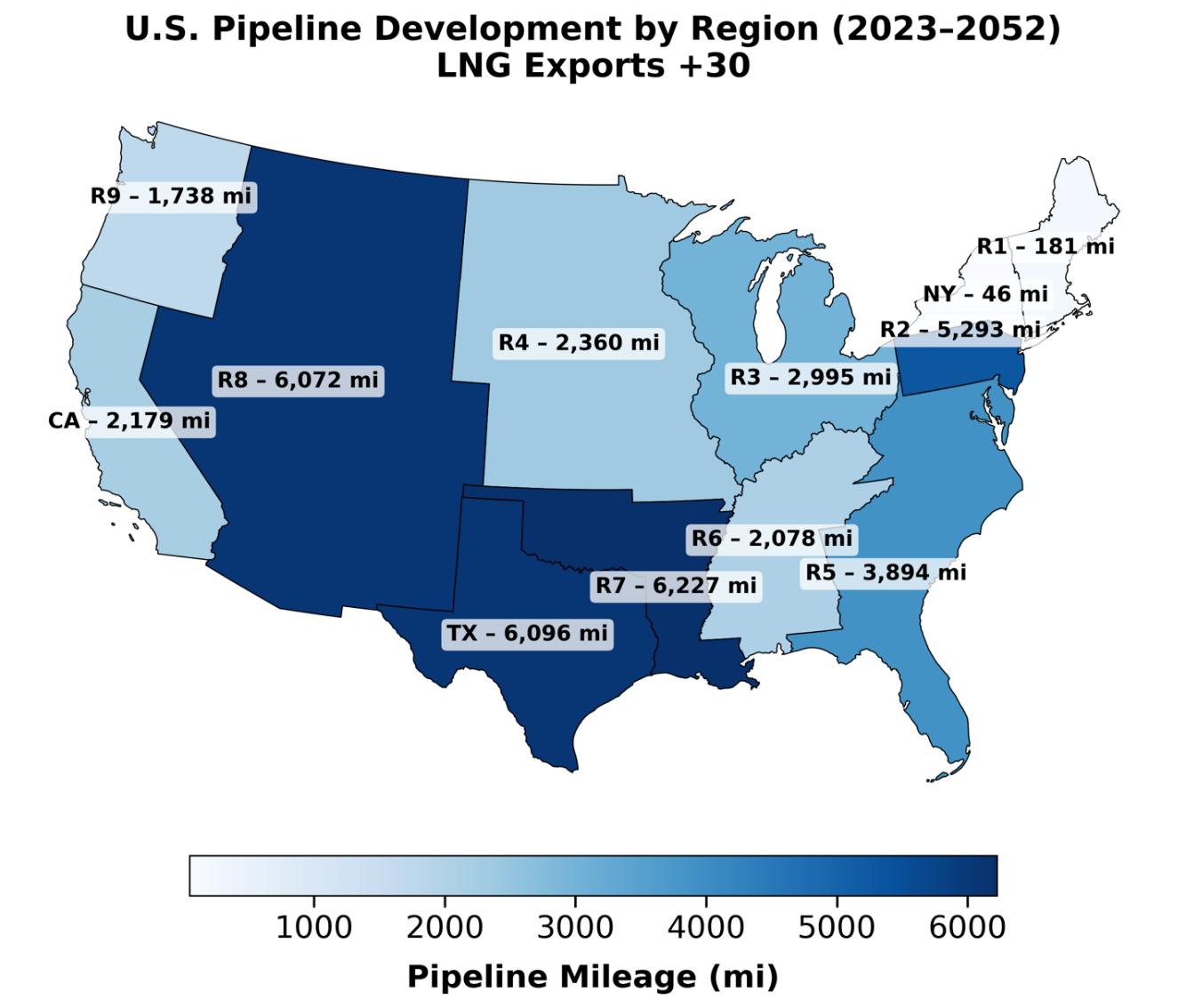

LNG exports are projected to increase substantially over the study period, rising by approximately 3.3 times from 2022 levels to reach 40.5 Bcf/d by 2052, while total electricity demand increases by roughly 27 percent. Appendix K presents maps showing existing LNG terminals, facilities under construction, and proposed projects across the U.S. as of April 2025. Growth in LNG exports reflects global market conditions and prices assumed in the modeling framework and contributes to overall increases in natural gas flows through the system.

Figure 8 - U.S. Natural Gas Consumption - Reference Case

Domestic natural gas consumption is projected to grow by approximately 14 percent over the study period. A portion of this growth occurs in the “other energy production” category, which includes natural gas used to support energy-related activities such as LNG terminal operations, compression, primary extraction, refining, and related processes. These uses increase in conjunction with overall energy system activity.

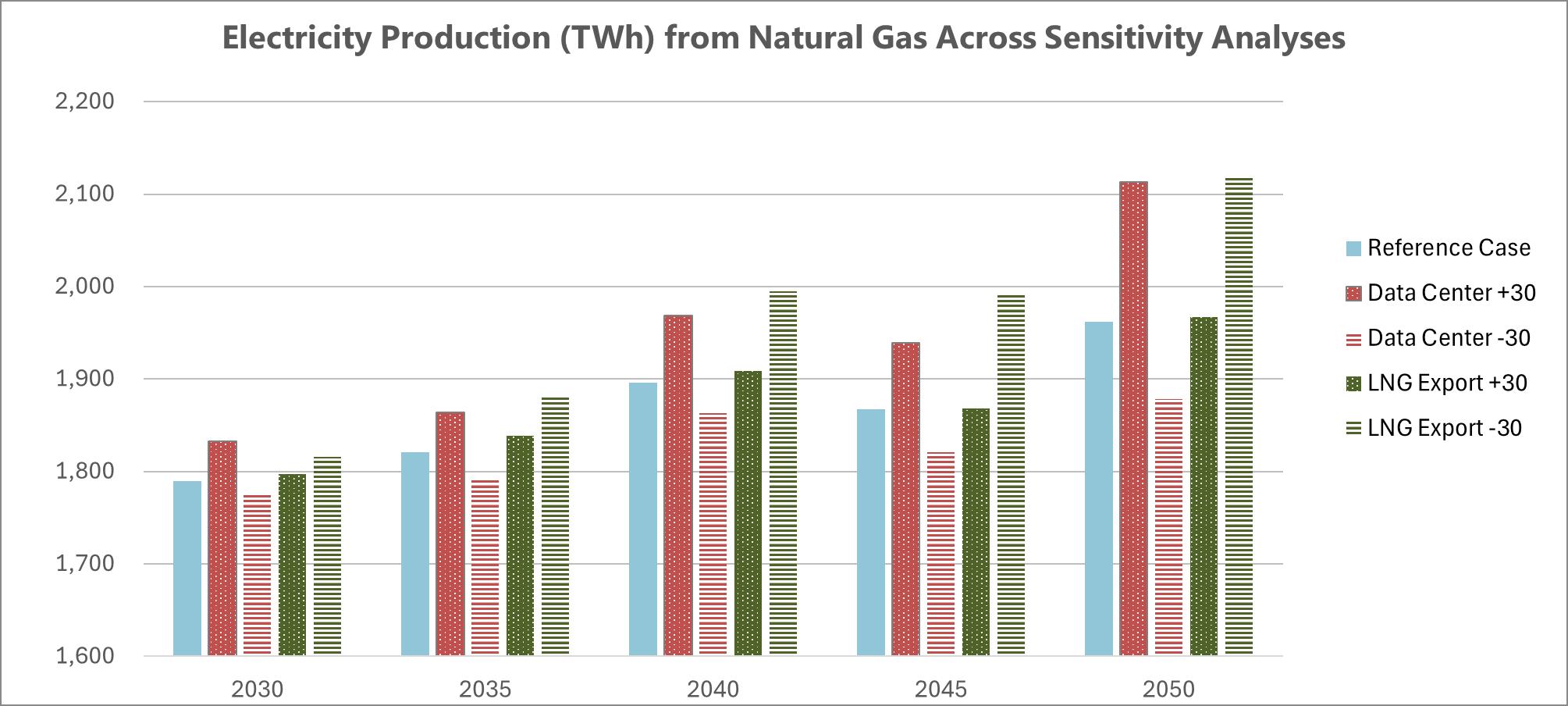

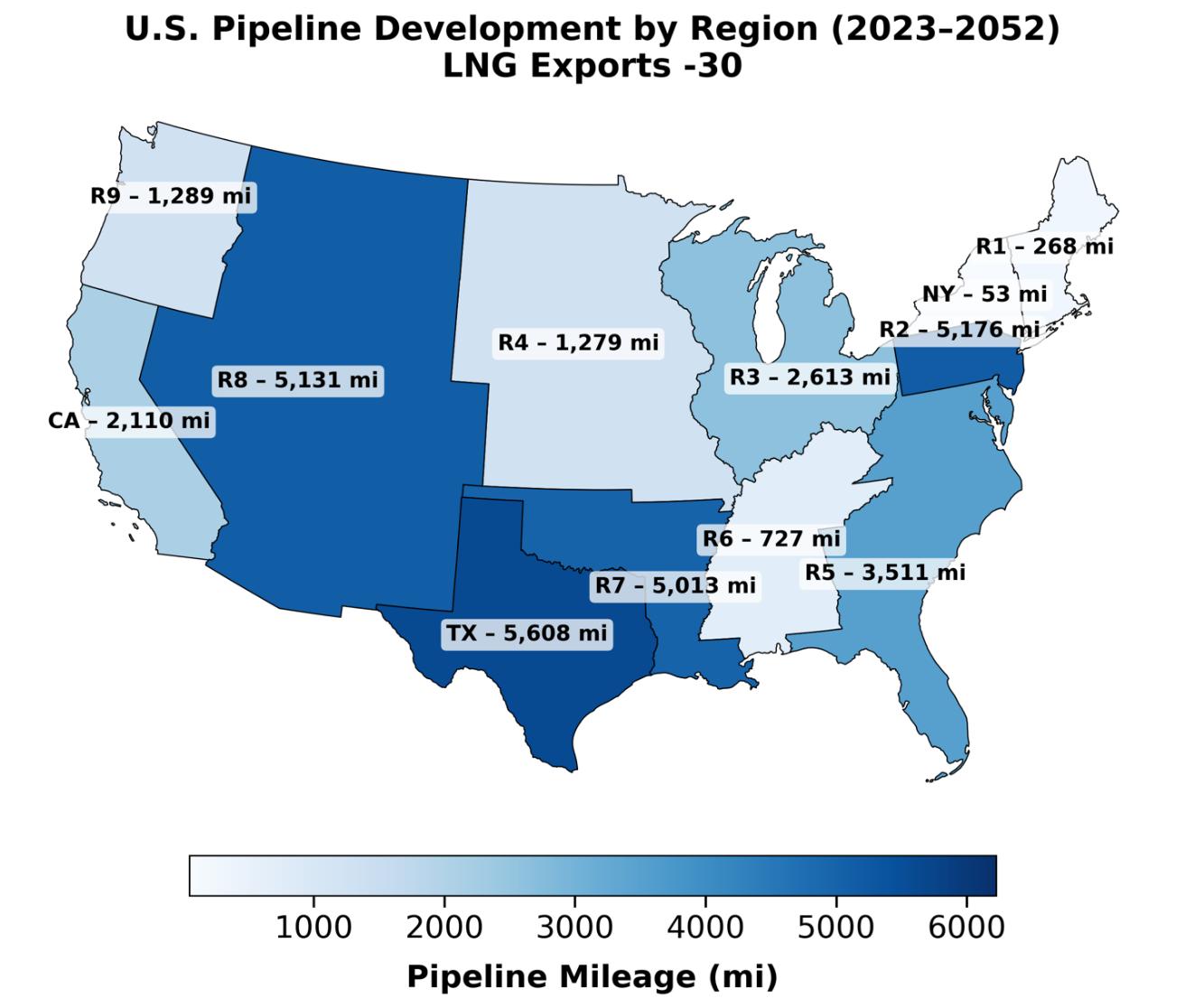

Industrial natural gas demand remains relatively stable over the study period in the Reference Case, reflecting a combination of efficiency improvements, structural changes in industrial output, and fuel flexibility across certain subsectors. The model allows industrial consumers to respond to relative fuel economics and technology availability, including the use of alternative fuels where feasible. The study’s sensitivity analysis of the LNG Export -30 scenario indicates that lower LNG export volumes would be associated with higher domestic gas availability, supporting additional growth in industrial and power sector gas demand. Electricity demand outcomes under these alternative cases are discussed further in the sensitivity analysis.

Table 29 - U.S. Natural Gas Consumption by Sector, Reference Case

Natural gas demand is lower overall in the U.S. Low Carbon Scenario, as detailed in Table 30. LNG exports more than triple, whereas gas use for electricity generation sees a more limited growth of 11 percent LNG export demand is slightly higher than in the Reference Case, reaching 41.1 Bcf/d in 2052, as natural gas shifts to exports while domestic consumption remains stable overall. Further growth of LNG exports may be limited by GHG reduction targets in certain regions, such as the West South Central (R7).

Canadian natural gas consumption also rises moderately in the Reference Case, going to 7,518 Bcf in 2052 from 5,842 Bcf in 2022 (see Table 31) with both pipeline and LNG exports leading the change. Long term, competition in demand between the U.S. and other international markets suggests Canada will respond to U.S. demand before building additional export capacity for other international markets. In practice, these dynamics will depend on price signals and how quickly the U.S. can ramp up its own production in the case of stronger-than-expected LNG market growth. Overall, while certain sectors, such as commercial buildings, see decreasing

Table 30 - U.S. Natural Gas Consumption by Sector, Low Carbon Scenario

consumption of natural gas with increasing electrification, other sectors, including industrial, increase the use of gas to sustain GDP growth – leading to a slight overall decline in domestic consumption

Table 31 - Canada Natural Gas Consumption by Sector, Reference Case Reference Case

In the Canadian Low Carbon Scenario (Table 32), natural gas consumption rises to 6,979 Bcf in 2052 from 5,852 Bcf in 2022, reflecting increases in pipeline exports to the U.S. and LNG exports to Europe and Asia Nevertheless, exports are about 7 percent lower than in the Reference Case, and domestic consumption decreases by a further 7 percent to meet GHG reduction targets.

3.2. Pipeline Expansions

Consistent with the modeling framework described earlier in this report, the analysis estimates future midstream infrastructure requirements based on average annual flows rather than peak demand While midstream operators size their infrastructure to meet peak demand rather than average annual flows, system-level, long-term models cannot directly quantify peak demand due to wide variations in contractual obligations, region, pipeline configuration, shipper mix, and end-use demand. The use of average annual flows reflects the level of detail available in longterm demand and supply forecasts and allows for a consistent comparison across modeled scenarios and regions. Using this framework, the model evaluates the capacity, investment, and timing of incremental pipeline infrastructure needed to support projected demand for all midstream products, i.e., natural gas, natural gas liquids, oil, CO₂, and hydrogen, through 2052

These capacity estimates should be interpreted as representing the additional capacity needed to provide the average annual flow estimated by the model. As explained, developers must design and build facilities to meet the peak or highest level of contracted demand. The capacity additions shown in Table 33 represent a conservative indicator of incremental infrastructure needs rather than a comprehensive design standard.

Table 32 - Canada Natural Gas Consumption by Sector, Low Carbon Scenario

This distinction between average and peak annual demand can be highlighted by observed operating data. As one example, the average throughput on the U.S. natural gas transmission system during January 2024 was approximately 103 Bcf/d, while peak daily deliveries reached roughly 184 Bcf/d, driven in part by Winter Storm Enzo. This implies an illustrative average-topeak load factor of approximately 1.8. While this relationship is based on a specific event, it reinforces why average-capacity results should not be interpreted as sufficient to meet peak hour or day conditions.

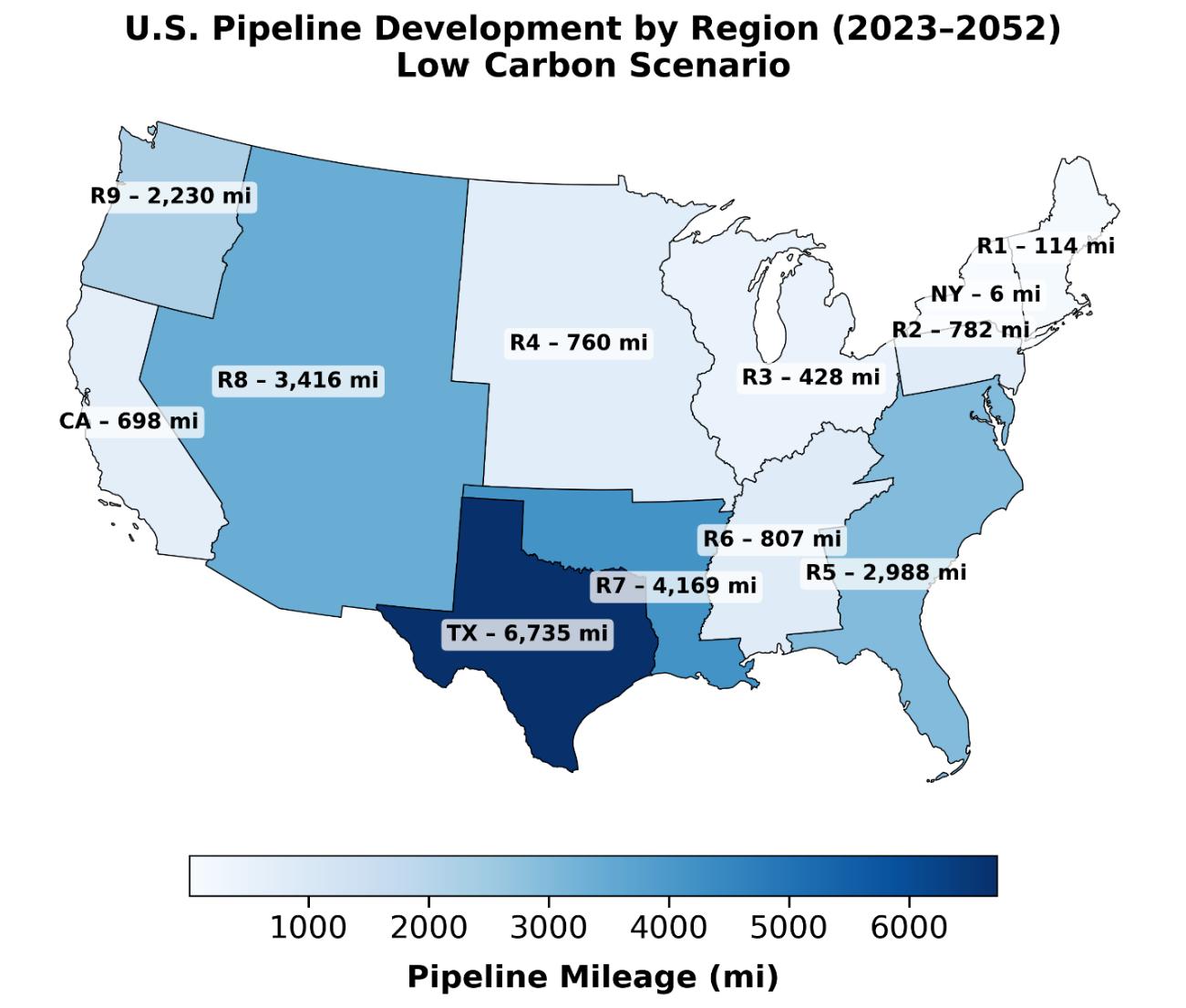

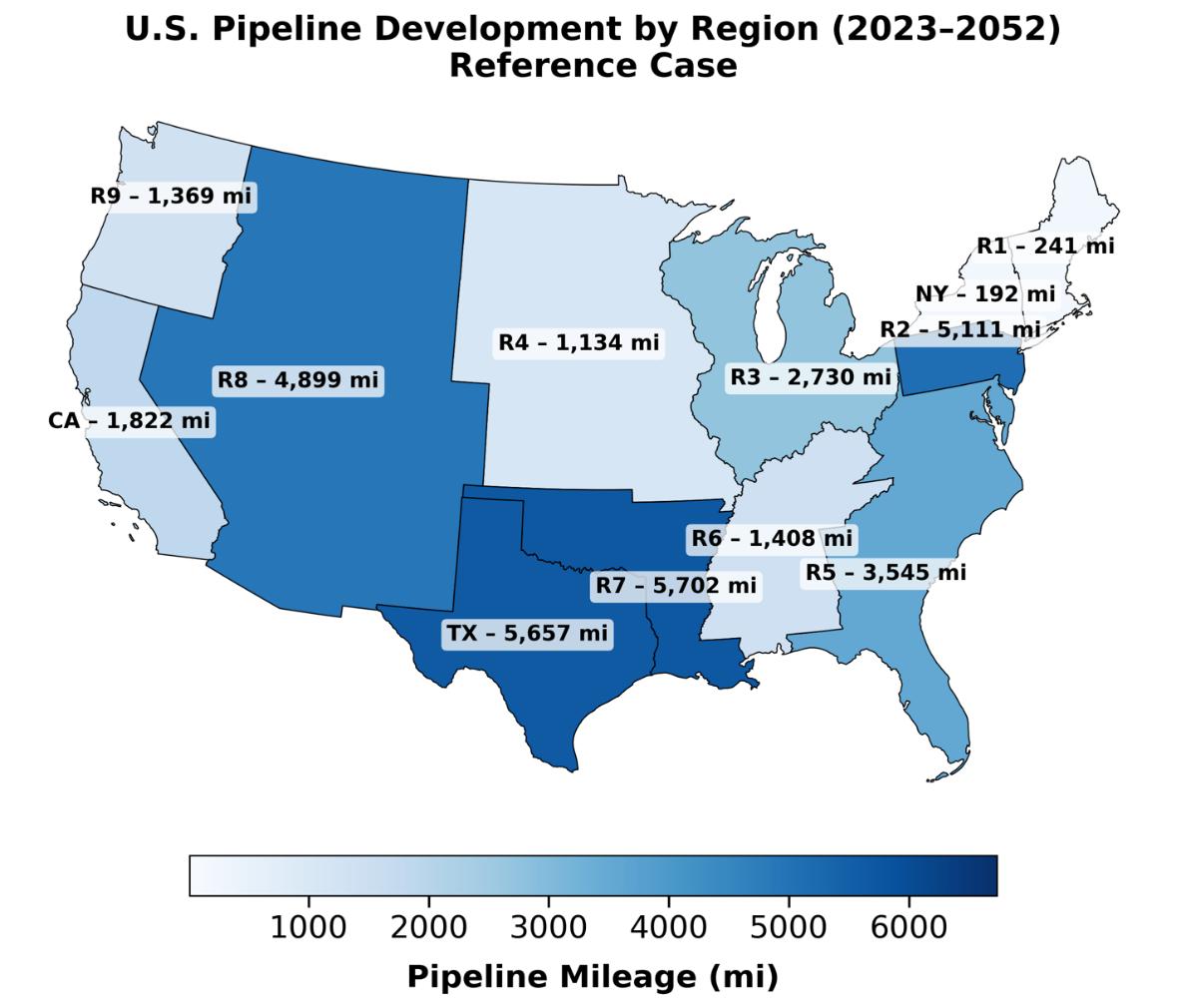

Table 33 summarizes the modeled demand for additional natural gas pipeline capacity in the U.S. and Canada under both the Reference and Low Carbon Scenario in five-year increments spanning 2023 through 2052. For natural gas transmission pipelines connecting adjacent regions, incremental capacity was allocated evenly between origin and destination regions for reporting purposes. Over the study period, the Reference Case indicates an average incremental requirement of approximately 70 Bcf/d of additional natural gas transmission capacity, including 6.4 Bcf/d in Canada. Under the Low Carbon Scenario, the analysis identifies an average need for 54.3 Bcf/d of additional capacity, including 4.5 Bcf/d in Canada, reflecting continued reliance on natural gas even as emissions targets are introduced.

Tables 34 and 35 reflect additional pipeline capacity demand by region in both scenarios The Reference Case shows significant growth in the Middle Atlantic (R2) and West South Central (R7) regions and Texas, the latter two owing to significant growth in production and LNG exports

Growth in the Middle Atlantic (R2) stems mainly from domestic trade, including the South Atlantic (R5) to support data center demand. Growth in pipeline capacity in the Mountain region (R8) is driven by trade to neighboring regions and increasing imports from Canada.

The most significant increased demand for natural gas pipeline capacity in the Low Carbon Scenario is in Texas, followed by the Mountain region (R8). The shift in pipeline capacity needs between regions is a direct result of GHG targets; Texas, which has not set targets, increases

Table 33 - U.S. and Canada Additional Natural Gas Pipeline Capacity

pipeline capacity additions to take a larger share of the LNG export market. Capacity is significantly reduced in the Middle Atlantic (R2), and moderately lower in the Mountain and West South Central regions (R8 and R7).

34 - U.S. &

(California)

The expansion of natural gas transmission pipeline mileage is projected to exceed 33,800 miles within the U.S. and reach approximately 37,160 miles when accounting for both the U.S. and Canada. Under the Low Carbon Scenario, the projected expansion is comparatively lower, amounting to roughly 25,500 miles across the U.S. and Canada. Tables 36 and 37 display findings by region for each scenario.

Based on the study assumptions, transporting the projected natural gas volumes also would require substantial compression. In the Reference Case, total demand for compression associated with natural gas transmission is estimated to exceed 12 million hp by 2052, reflecting higher pipeline throughput and network expansion. Under the Low Carbon Scenario, reduced demand for natural gas results in a lower compression requirement of approximately 8.6 million hp. Tables 38 and 39 display the results by region.

As displayed in Table 40, when combined, the U.S. and Canada require additional NGL capacity in both scenarios. Under the Reference Case, an additional 2.35 MMbp/d of U.S. and Canadian NGL pipeline capacity is needed by 2052; under the Low Carbon Scenario, an additional 2.22 MMbp/d is needed.

Table 39 - U.S. and Canada Added Compression by Region, Low Carbon Scenario

Table 40 - U.S. and Canada Added Natural Gas Liquids Pipeline Capacity

Regional and Canadian oil pipeline capacity increases are shown in Table 41 for both the Reference and Low Carbon Scenario

Table 41 - U.S. and Canada Added Oil Pipeline Capacity

Oil pipeline capacity needs over the period for both scenarios in the U.S. regions and Canada are shown in Tables 42 and 43

Table 42 - U.S. and Canada Added Oil Pipeline Capacity by Region, Reference Case

(New York)

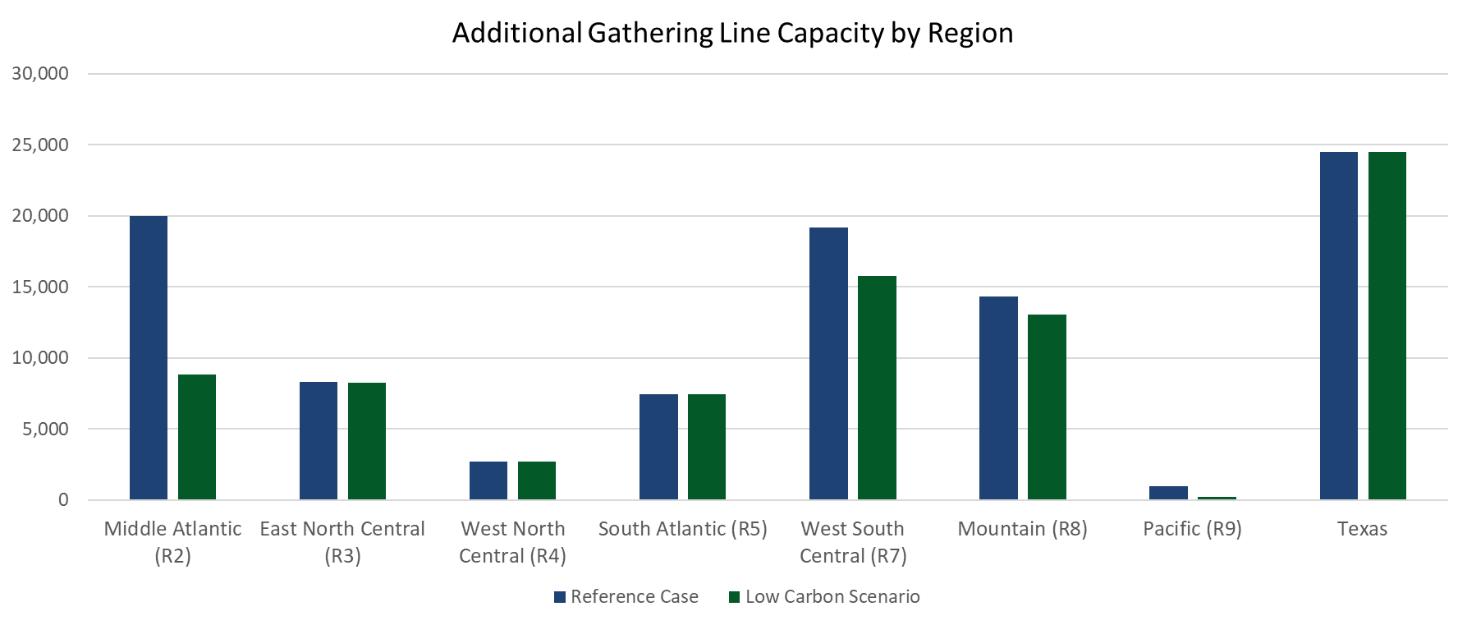

3.2.1. Gathering Lines

Gathering lines are designed to move gas from wellheads to processing plants, compression stations, or transmission pipelines, and typically handle lower volumes than interstate transmission lines. Typical average gas flow for gathering lines depends on the size of the line, pressure, and production basin.

For modeling the gathering lines and future natural gas pipeline infrastructure needs, the analysis assumes 6-inch diameter with throughput of 4 MMcf/d, over a length of 6 miles

The results of projected need for minimum gathering lines are shown in Tables 44 and 45 below Figure 9 shows the results by region.

Table 44 - U.S. and Canada Added Natural Gas Gathering Line Capacity in Miles

Table 45 - U.S. and Canada Added Natural Gas Gathering Line Capacity in Bcf/d

Figure 9 - Additional Gathering Line Capacity by Region

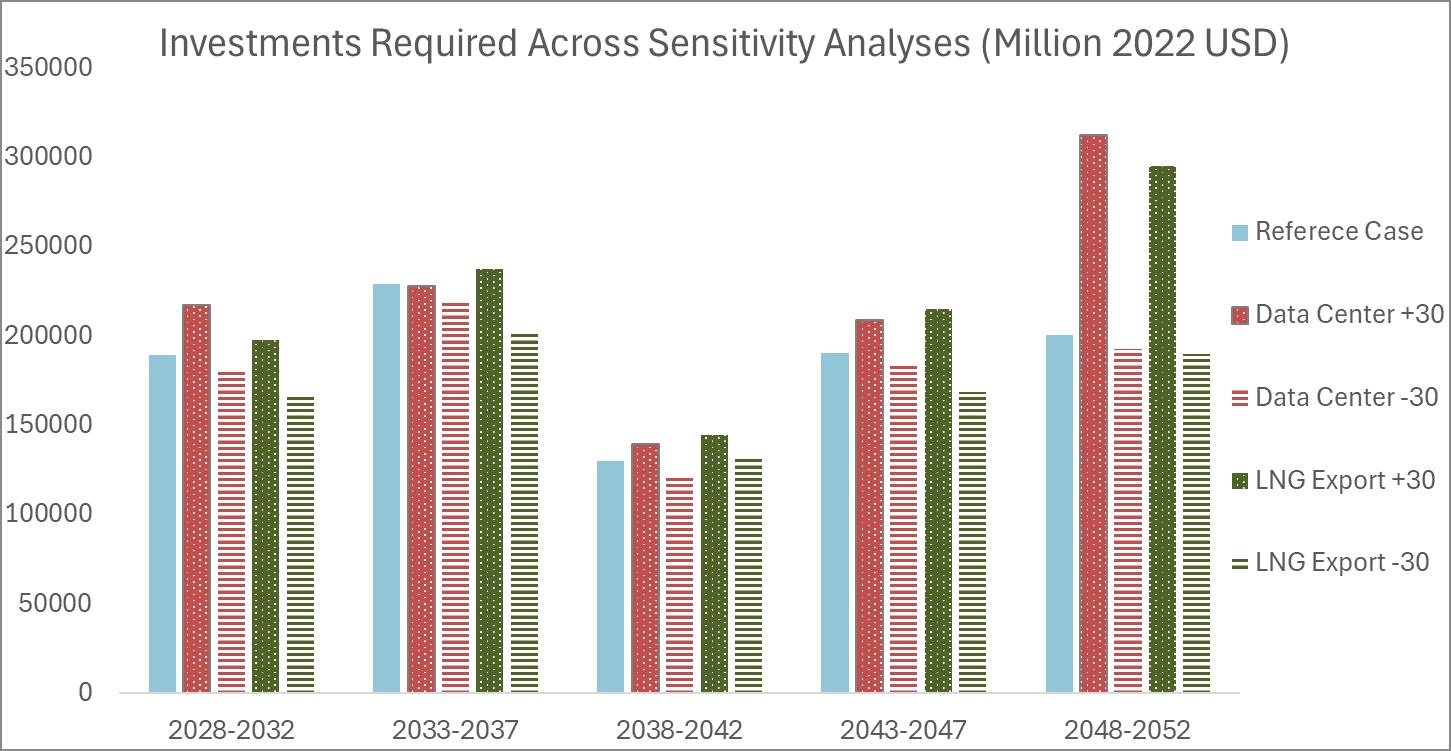

3.3. Infrastructure Investment Costs

Over the study period, this analysis predicts total investments for all commodities discussed (natural gas, oil, NGL, hydrogen, and CO2) will approach $1.2 trillion in 2022 dollars, with an annual average of $40 billion (2022 USD) in the Reference Case. The largest share of the investment costs are derived from natural gas pipelines and LNG export terminals due to anticipated corresponding demand. This includes a sharp rise in LNG export terminal investments until the mid-2030s to meet expected international demand.

Investments in natural gas pipelines, a necessary backbone for LNG expansion and for domestic distribution, follow the same trend, with an additional long-term increase in the 2052 period.

By contrast, the midstream oil sector is projected to experience significantly lower investment levels, reflecting expectations of relatively flat demand over the time horizon examined in this report. Investments in hydrogen and CO2 pipelines are modest and immaterial compared to natural gas pipelines.

Table 46 details investment expectations by infrastructure type in five-year increments in the Reference Case. Table 47 provides the same breakout for the Low Carbon Scenario.

As discussed above, the model uses average annual throughput, so the analysis does not fully reflect the investment needed to provide peak delivery. If we assume a square relationship between capacity and cost and a difference of 1.8 times between average and peak delivery, 9 then North America needs to invest 1.34 times more in natural gas transmission pipelines to meet peak delivery requirements. This may increase total investment by 15 percent in the Reference Case. While gas compression investment may increase as well (approximately 1.6 times), the proportion of total investment is less significant, increasing total investment by about 4 percent.

9 Using the example factor of 1.8 to estimate increased design capacity needs, the relationship between pipeline diameter and capacity is roughly square or greater (power of 2.5 based on the Panhandle B equation) whereas costs scale linearly with diameter (dollar per diameter inch-mile).

Table 48 provides the total North American midstream investment cost by region in the Reference Case. The majority of the investment needed will be in natural-gas producing regions, including Texas, Mountain (R8), Middle Atlantic (R2) and East North Central (R3), and LNGexporting regions such as Texas and West South Central (R7). Investments in the South Atlantic region (R5) are similar to the Middle Atlantic region (R2) due to strong demand from electricity. Investments in New England (R1) and in California remain modest, given the high costs and the stringent regulations in those regions. Table 49 provides the same data for the Low Carbon Scenario. Table 48 - Infrastructure

Investment Costs by Region, Reference Case

Total investments over the period are higher in the Low Carbon Scenario than in the Reference Case, mainly due to increased international demand for LNG and resulting added capacity in LNG export terminals and natural gas pipelines connecting the terminals to production sites. The Low Carbon Scenario predicts 20 percent lower investment in natural gas pipelines due to lower total production and consumption, and to regional shifts. At the same time, increased investment in hydrogen and CO₂ pipelines driven by the GHG reduction targets more than make up for this difference. Through 2052, total investments under the Low Carbon Scenario are expected to reach about $1.4 trillion with an average of around $49.7 billion per year.

Detailed investment estimates for major components in the pipeline system are provided in fiveyear increments for both the individual components and by region in Appendix C.

3.4. Direct and Indirect Jobs Estimates Resulting from Midstream Infrastructure Investments

Jobs estimates are typically calculated using sophisticated models, such as computational general equilibrium macroeconomic models, and reported in many public-facing studies. The analysis in this report relies on a simplified multiplier approach based on a 2015 Standard & Poor’s report on general infrastructure, an API/PwC 2012 report on the Total U.S. Oil and Gas Industry Impact Multiplier and some general data on construction and infrastructure. The report used the Google-based AI tool Gemini to summarize data available from these sources.

This analysis revealed that a $1.2 trillion investment in the midstream infrastructure industry would result in a low-end estimate of 12 million jobs and a high-end estimate of 24 million jobs over 25 years. Of these numbers, between 2 and 4 million are direct jobs, a range of 4 to 8 million are indirect jobs, and the analysis suggests induced jobs range from 6 to 12 million. An investment of the magnitude required to meet the reported infrastructure demand would produce an average of 414,000 to 828,000 jobs per year during the study period, varying with the investment

3.5. Interpretation and Summary of Key Findings

Natural gas remains a core component of the North American energy system through 2052, under both the Reference Case and Low Carbon Scenario, supporting domestic consumption, electricity generation, data centers, and LNG export demand. While growth moderates under emissions constraints, overall production and infrastructure requirements remain substantial.

• LNG exports represent the single largest source of incremental natural gas demand over the study horizon. Under both scenarios, U.S. LNG exports more than triple by 2052, supported by favorable resource availability, competitive pricing, and global efforts to displace higher-emissions fuels. In the Low Carbon Scenario, global climate policies further reinforce LNG demand as importing countries seek lower-carbon alternatives to coal, increasing the importance of export-oriented pipeline infrastructure concentrated along the Gulf Coast.

• Natural gas production increases under both scenarios, driven by domestic demand and exports. In the Reference Case, dry gas production in the U.S. and Canada rises from 42.19 Tcf/yr in 2022 to 55.57 Tcf/yr by 2052. Growth is slower in the Low Carbon Scenario, reaching approximately 50 Tcf/yr by 2052. Production gains are widespread in the Reference Case, led