WHALESIN ACCUMULATION MODE

MARKETSIGNALS

FailedBreakoutForBitcoin MACRO

RisingGeopoliticalRisksandCooling EconomicDataComplicatetheGlobal InflationOutlook

FailedBreakoutForBitcoin MACRO

RisingGeopoliticalRisksandCooling EconomicDataComplicatetheGlobal InflationOutlook

Bitcoinʼs early March rally lost momentum with a brief break to $74,047, before reversing and sending price back toward the monthly open near $67,000. The move underscores how firmly the $62,500$72,000 range continues to define marketstructurefollowingFebruaryʼscapitulation.

On-chain and order-flow data suggest the market is stabilising rather than deteriorating.RealisedlosseshavecompressedsharplysincetheFebruarycrash, indicating that forced selling has largely subsided, while spot CVD shows aggressive buying early in the month that has since been absorbed by passive supply near range highs. Meanwhile, accumulation remains concentrated among whales and long-term holders, even as retail investors continue to distribute. The result is a market in equilibrium. Downside pressure has faded, but without sustained ETF inflows or stronger spot demand, Bitcoin remains trapped in consolidationuntilthe$72,000resistancezoneisdecisivelycleared.

The US economy is entering a period of increasing macroeconomic crosscurrents, as signs of cooling domestic activity coincide with renewed inflationrisksdrivenbygeopoliticaltensionsandrisingenergyprices.

Recent labour market data point to weakening employment conditions. The February Employment Situation Report from the Bureau of Labour Statistics showedthatemployerscut92,000jobswhiletheunemploymentrateroseto4.4 percent. Payroll estimates for the previous two months were also revised down by 69,000 jobs, suggesting labour demand had been weaker than initially reported.

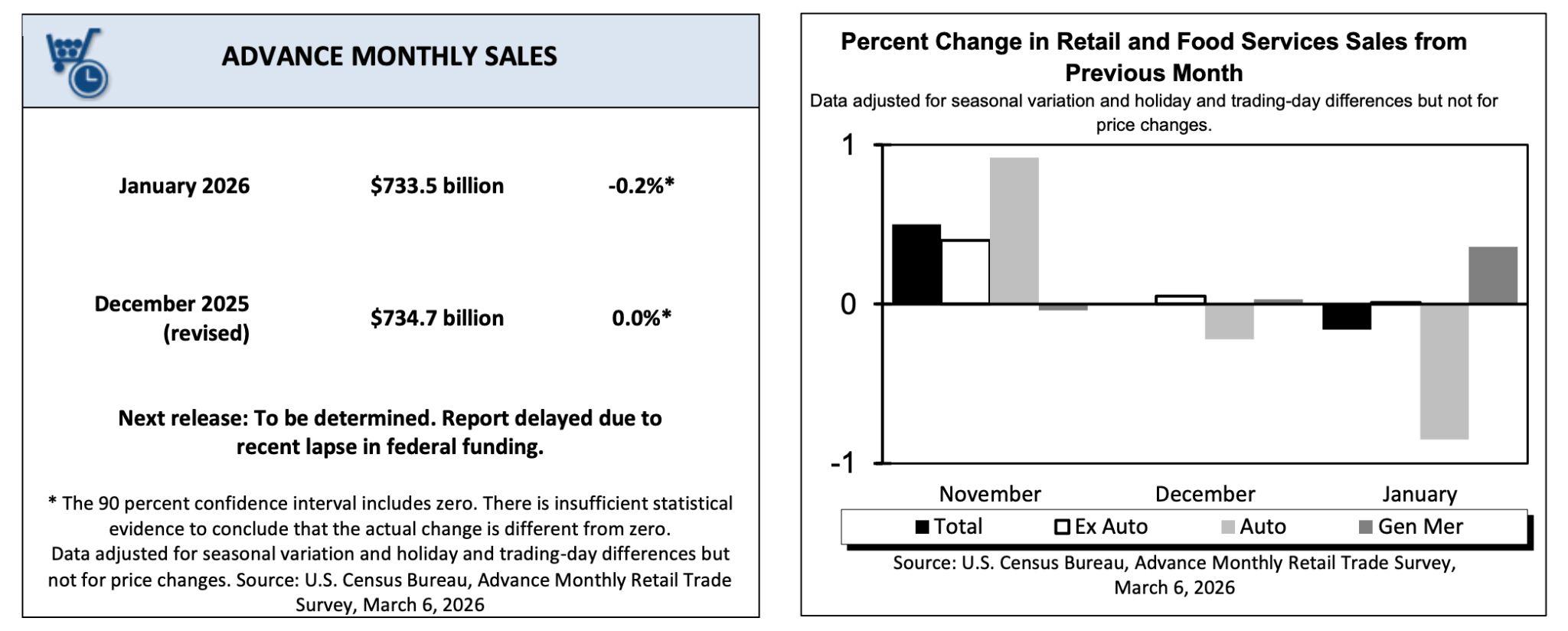

Consumeractivityisalsobeginningtoshow earlysignsofmoderation.Retailand food-services sales fell 0.2 percent month-over-month in January to $733.5 billion, although spending remained 3.2 percent higher compared with a year earlier.Theslowdownhasnotbeenuniformacrosssectors.

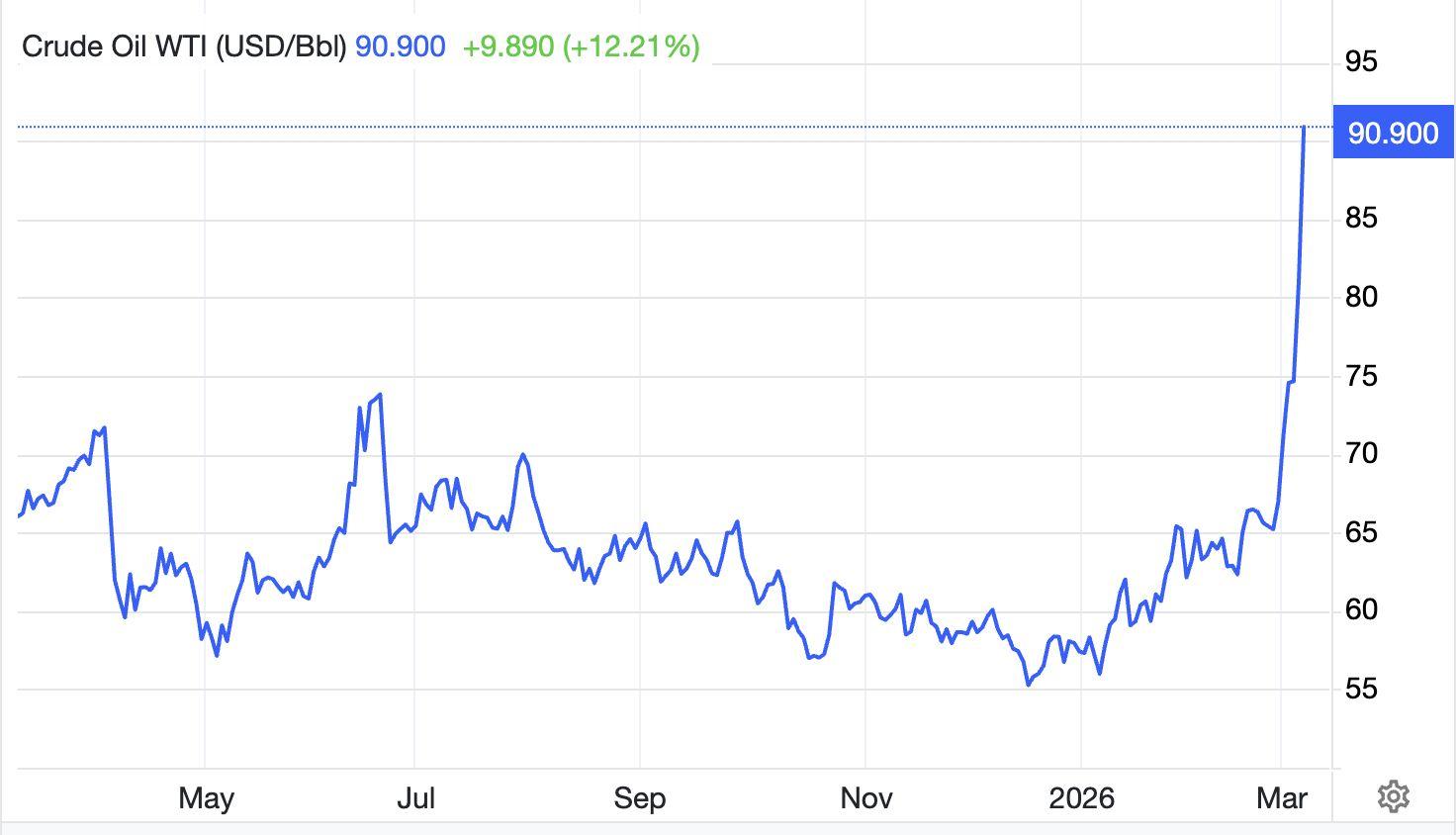

At the same time, geopolitical tensions are raising new inflation risks through energy markets. The escalating conflict involving the United States and Iran has pushedoilpriceshigher,withWestTexasIntermediatecruderisingbyroughly$20 per barrel. Higher energy costs tend to feed through into transportation, manufacturing and logistics expenses, creating inflationary pressure while also weighingoneconomicactivity.

AlthoughtheUSismoreresilienttoenergyshocksthaninpreviousdecades,due toitslargedomesticenergyproduction,risingfuelprices stillincreasehousehold costsandcanweighondiscretionaryspending.Thesedynamicscreateadifficult policyenvironmentfortheFederalReserve.Whilesofterlabourmarketconditions could support the case for interest rate cuts, the possibility that energy-driven inflationcouldreacceleratemaylimitthecentralbankʼsabilitytoeasepolicyinthe nearterm.

Against this uncertain macroeconomic backdrop, developments within the cryptocurrencysectorcontinuetoreflectthegrowingintegrationofdigitalassets intoinstitutionalbalancesheetsandfinancialmarkets.

Strategy(formerlyMicroStrategy)recently expandeditsBitcointreasurystrategy, acquiring an additional 3,015 bitcoins for approximately $204.1m at an average priceof$67,700perBTC.Thepurchaseincreasedthecompanyʼstotalholdingsto 720,737 BTC, reinforcing its position as the largest corporate holder of Bitcoin globally.

While some firms are expanding their digital asset holdings, others are adopting more flexible treasury strategies. MARA Holdings, one of the largest publicly traded Bitcoin mining companies, has updated its digital-asset policy to allow the saleofBitcoinfromitsexistingreserves.

Regulatorydevelopmentsalsoremainanimportantfactorfortheindustry.TheUS Securities and Exchange Commission recently reached a settlement with crypto entrepreneurJustinSunrelatedtoallegationsinvolvingtheTronecosystem.Under the agreement, Rainberry Inc., a company associated with the Tron network and the BitTorrent protocol, will pay a $10 m civil penalty while the SEC dismisses its claimsagainstSunandrelatedentitiespendingcourtapproval.

1.MarketSignals

● FailedBreakoutforBitcoin

2.GeneralMacroUpdate

● USLabourMarketWeakensasHiring DeclinesWhileConsumerSpending ShowsEarlySignsofSlowdown

● USIranConflictRaisesEnergyMarket RisksWhileGlobalEconomyFaces SupplyChainPressure

3.NewsFromtheCryptosphere

● StrategyExpandsBitcoinTreasurywith $204MPurchase,HoldingsReach 720,737BTC

● SECandJustinSunReachSettlementin TronFraudCase

Marchbeganwithasignificantinitialdrivehigherfor Bitcoin,movingup10.5 percentinthefirstfourtradingdays.However,despitethisinitialmomentum, BTCremainsconfinedtoitsestablishedrangeof$62,500to$72,000,withthe highof$74,047reachedonMarch4th,provingtobeafailedbreakout.

TheKeyDriversforthisRetracementAre:

1. Areversaloftheearly-monthETFinflows.

2. Arelativelylargeamountofleveragedlongsthathasbuiltlateintotheinitial 10.5percentmoveup,beingliquidated.

Following a three-session expansion in BTC ETF flows in late February totalling $1.14 billion, BTC has encountered significant resistance. The March 5 and 6 sessionsrecordedacombinedoutflowof$576.8million.

ETF flows have been a critical factor for price discovery, with IBIT trading volumesalonesurpassing$100m/dayconsistently,andonoccasionmatchingup to daily trading volumes of the top 10 Bitcoin spot trading pairs on conventional exchanges. While it is true that the first few trading sessions of every month usually see large inflows, due to systemic regular investments and fund rebalancing, the size of the reversal seen this month so far suggests, this might notbearegimechangeforETFflows,yet.

It also indicates that the institutional bid is not price-insensitive, and that early month inflows donʼt persist indefinitely. Traders should watch flows this week to seewhetherthisisareversalorjustabumpintheroad.Especiallyincaseofany positivedevelopmentsinthegeopoliticalsituation.

Sinceestablishingourcurrentlowof$60,100onFebruary5,BTChasconsistently failedtobreachtherangehighnear$72,000,despitemultiplerapidupwardprice movements. This repeated rejection affirms the $72,000 region as a significant near-termresistancelevel.

To ascertain if this price resistance reflects a fundamental degradation in demand, we have analysed the Realised Profit metric. This on-chain indicator aggregatesthetotalUSD-denominatedprofit;calculatedasthesumofnetprofits fromalltransactionsoveraperiod,lockedinbymarketparticipants.

Following the price stabilising below the $70$72,000 threshold, the level of negative realised profit being experienced by the market as a whole, also stabilised.Fromover$3bnindailylossesseenduringthesell-downonFebruary 5,itisnowatapproximately$370mperdaywithinthecurrentrange.Thissharp compression in daily-averaged negative realised profit suggests a material thinning of the cohort of holders willing to transact at a discount relative to their cost basis (likely acquired over the preceding 23 months). Consequently, buy-side liquidity is currently assessed to be at its weakest level since the August–September2024period.

Conversely,therealisedprofitmetricturnedpositivewhenthepriceapproached the $72,000 range-highs, implying that the 20.5 percent recovery following the February5lowwasutilisedbydipbuyers.Whilethishasallowedforsometraders to secure swift profits, it also indicates a net lack of long-term conviction. Furthermore, the March 6 spike in negative realised profit to approximately $900m , reveals that a substantial cohort of investors capitalised on the brief excursion above the range highs to exit their positions at a loss. Critically, even though these were loss-making positions, this exit price was nevertheless superior to the valuation they would have received near the range lows in the lower$60,000s.

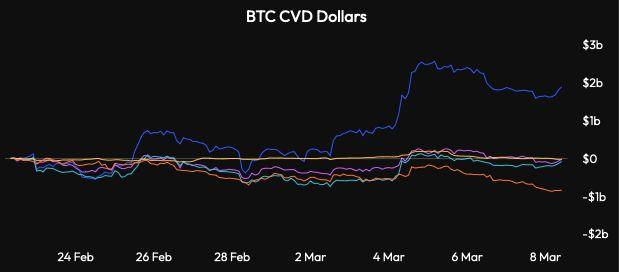

Thespotflowsonexchangesalsoshowasimilarpictureofaggressivebuying after the monthly open, as evidenced by the spot cumulative volume delta CVD)metricexpandingsharply,beforestabilisingbyMarch5.

Figure4CumulativeVolumeDeltaforBitcoinAcrossMajorExchanges andPairs.DataSource:VeloData)

This month has also not seen any significant selling pressure on exchanges, which is a pronounced shift from the aggressive and substantial selling seen in the 1012 weeks prior to the March open. A combination of passive asks (limit sells) that absorbed aggressive buying (at market price) and leveraged longs opening late into the leg higher, has prevented price from breaking out from our rangejustyet.

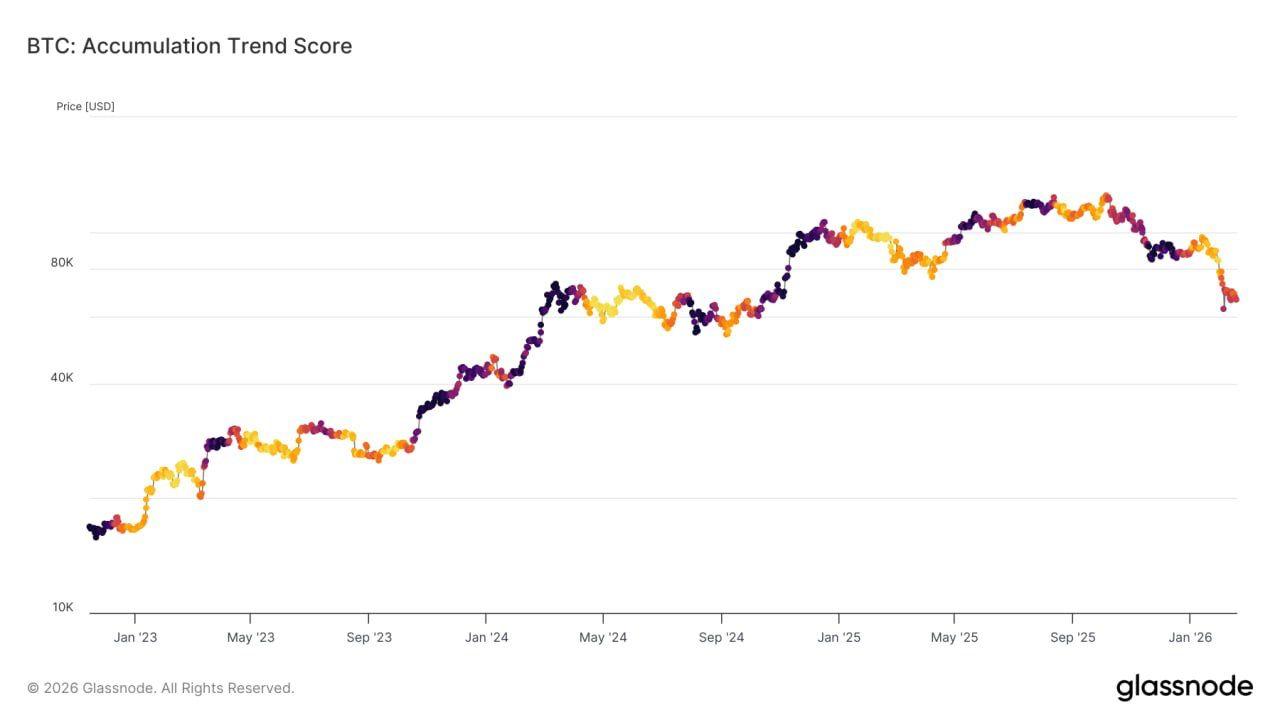

On-chain evidence suggests that the current correction is qualitatively different frompriorcyclesduetotheformationofaninstitutionalfloor.SinceBTCdropped to$80,000inNovember2025,walletsholding1,000BTCormore(whales)have beentheonlycohortinaconsistentaccumulationphase.

In contrast, retail cohorts (holding under 10 BTC) have sustained a net selling position for over two and a half months. The current Aggregate Accumulation Trend Score, sitting at approximately 0.7 (within the red zone above above), indicates that larger entities, specifically whales and long-term holders are the only cohorts with a prevailing trend of being net buyers at the current price levels. However, this level of accumulation is far from the intensity observed duringperiodsof"peakaccumulation,"suchaslate2022.

The US economy is entering a period of increasing macroeconomic crosscurrents, as slowing job growth and early signs of softer consumer spendingcoincidewithrenewedinflationrisksdrivenbyrisingenergypricesand escalatinggeopoliticaltensionsintheMiddleEast.

TherecentescalationinconflictinvolvingtheUnitedStatesandIranhaspushed globaloilpricessharplyhigher,raisingconcernsthatenergycostscouldreignite inflationpressuresevenaspartsofthedomesticeconomybegintocool.

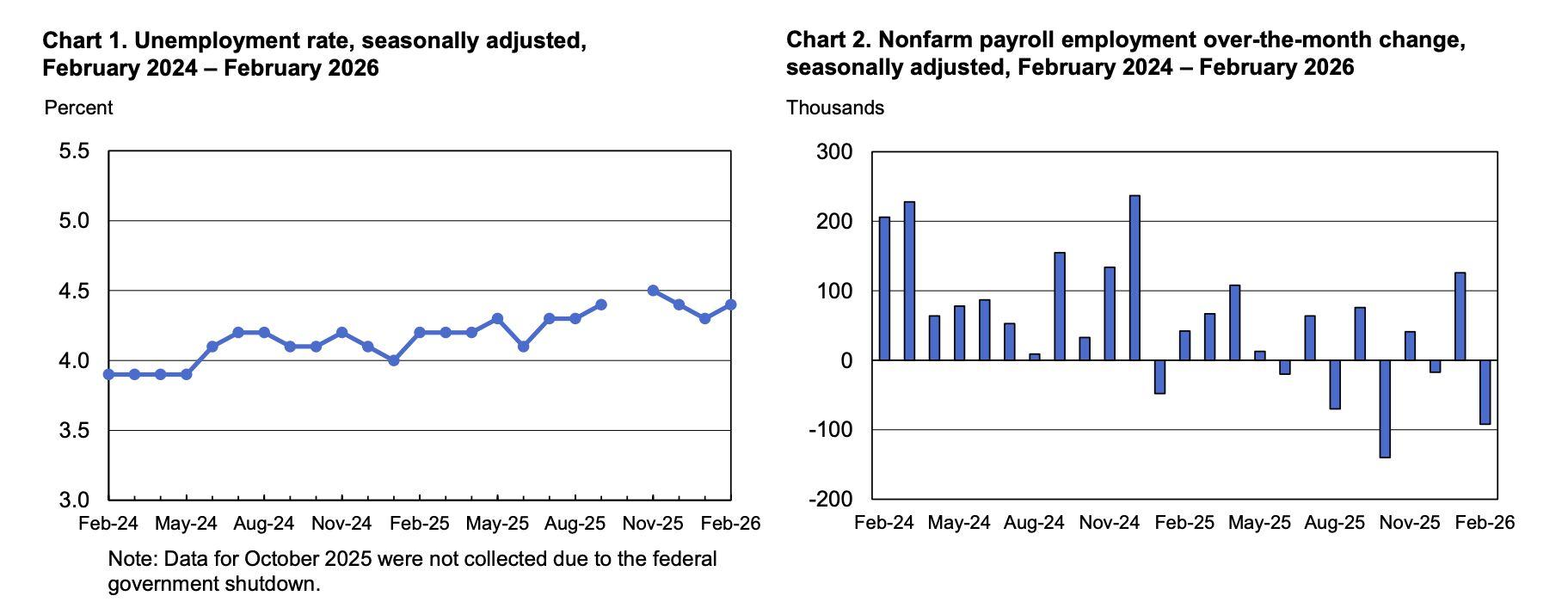

Figure6.UnemploymentRate,NonfarmPayrollemployment Source:BureauofLabourStatistics)

The February Employment Situation Report, released by the Bureau of Labour Statistics BLS) last Friday, March 6, showed that US employers cut 92,000 jobs during the month and the unemployment rate increased to 4.4 percent. The data alsoincludeda69,000downwardrevisiontoemploymentfiguresfortheprevious two months, signalling that the labour market has been weaker than earlier estimatessuggested.

Job losses were concentrated in several key industries. Manufacturing, construction, and other goods-producing sectors all reported declines, indicating persistent weakness in sectors sensitive to policy and trade conditions. Construction employment fell by 11,000 positions, manufacturing declined by 12,000, and goods-producing industries collectively shed 25,000 jobs. Federal governmentemploymentalsodecreasedby10,000roles.

The health care sector, which has been one of the strongest sources of employment growth in recent years, also recorded losses. Around 28,000 jobs were removed from the sector, partly due to strikes involving nurses and other healthworkersinstatessuchasNewYorkandCalifornia.Analystsexpectsome hiring in health care to recover once labour disputes are resolved, although broaderweaknessinothersectorsmaypersist.

Measures of labour activity also reflected a cooling trend. Average monthly job creation slowed to 6,000 over the past three months, while the labour force participation rate declined to 62 percent. The employment-to-population ratio fellto59.3percent,andthemediandurationofunemploymentincreasedto11.1 weeks,indicatingthatjobseekersaretakinglongertofindwork.

Despitetheweakerhiringenvironment,wagegrowthremainedresilient.Average hourly earnings increased 0.4 percent during the month and 3.8 percent compared with the previous year, suggesting that income growth is still supportinghouseholdfinances.

At the same time, the outlook for inflation has become more uncertain due to risingenergycosts.Oilpriceshaveincreasedsharplyfollowingtheescalationof conflict involving Iran, with West Texas Intermediate crude rising by about $20 per barrel. Higher oil prices tend to raise transportation and production costs across the economy, which can contribute to broader inflation pressures. If energy prices sustain a 10 percent increase over a year, the surge in energy pricescouldtemporarilyaddaround0.4percenttoinflation.

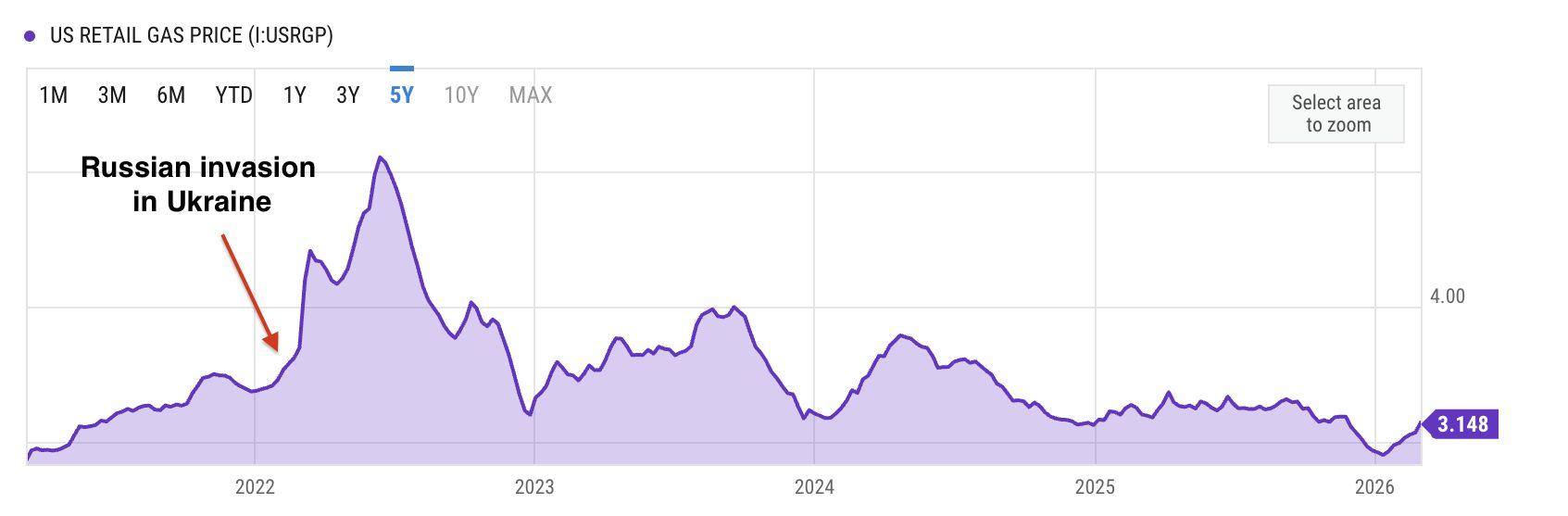

Gasolinepriceshavealreadybeguntoreflectthistrend.TheaverageUSpricefor regular gasoline has risen to about $2.77 per gallon, with expectations that it could approach $3.50 in the near term. When energy prices rise quickly, households often face higher living costs, which can influence spending behaviour.

Evidenceofmorecautiousconsumerspendingappearedinthe latestretaildata. According to advance estimates from the US Census Bureau, retail and food-services sales totalled $733.5 bn in January, representing a 0.2 percent decline from December, although sales remained 3.2 percent higher than a year earlier. Retail sales measure the total value of goods sold by retailers and are widelyusedasanindicatorofconsumerdemandintheeconomy.

Spending trends were uneven across sectors. Sales declined in pharmacies, clothing stores, and gas stations, while home-related retailers such as furniture and building-materials suppliers reported modest increases. Online retailers performed particularly well, with non-store sales rising 10.9 percent compared withthepreviousyear.Restaurantsanddrinkingestablishmentsalsorecorded3.9 percent annual growth, highlighting continued strength in service-related spending.

Theretaildataarrivedlaterthanusualafterdelayscausedbyatemporarylapsein federal funding s a result of government shutdown in January, which shifted the release schedule of several economic indicators. Such timing changes can occasionally make monthly fluctuations appear more volatile than underlying trends.

Together, the latest labour and retail data highlight the growing macroeconomic challenges facing the US economy. Employment growth has slowed and several industries remain under pressure, while consumer demand is only beginning to moderate after a period of strong spending. At the same time, rising energy prices,partlydrivenbyescalatinggeopoliticaltensionsinvolvingtheUnitedStates and Iran, are increasing the risk that inflation could remain elevated even as economicmomentumsoftens.

For policymakers at the Federal Reserve, these dynamics create a more challengingpolicyenvironment.Thecentralbanktypicallyadjustsinterestratesto balance economic growth and inflation. However, while weaker labour market conditions could support the case for policy easing, the possibility that higher energycostscouldfeedintobroaderpricepressuresmaylimittheFedʼsabilityto reduceratesinthenearterm.

As a result, upcoming inflation indicators, particularly the Personal Consumption Expenditures PCE) price index, which measures changes in the prices consumerspayforgoodsandservices,willbecloselymonitoredforsignalsabout underlying price trends. Until clearer evidence emerges, markets are likely to watch labour market conditions, consumer spending patterns, geopolitical developments, and energy prices to determine whether the current slowdown reflects a temporary adjustment or the beginning of a broader shift in economic momentum.

The escalating conflict between the United States and Iran has begun to affect global energy markets and trade routes, raising concerns about higher shipping costs and energy prices. However, the size and resilience of the US economy suggest it may absorb energy shocks more effectively than many other countries,evenasglobalinflationarypressuresincrease.

The conflict began on February 28, 2026, when the US and Israel launched airstrikes against Iran, resulting in the death of Iranʼs Supreme Leader Ayatollah Ali Khamenei and several government and military leaders. The war remains ongoing, and the economic consequences of the conflict will be closely tied to itsduration.OneofthemostimmediateriskscomesfromtheStraitofHormuz,a strategicmaritimepassageforoilandgasshipments.Althoughthewaterwayhas not been fully closed (in a formal, legal sense, as of March 9 2026, shipping companieshavestartedtoavoidtherouteduetosecurityconcerns.Asaresult, insurance costs, freight rates and delivery times have risen. These disruptions can delay shipments and create logistical bottlenecks similar to those experiencedduringtheCOVID19pandemic.

Qatarhasemergedasacriticalfactorintheunfoldingenergydisruption.Adrone strikelinkedtoIranforcedtheclosureoftheworldʼslargestliquefiednaturalgas LNG)exporthubinthecountry,amplifyingthesupplyshock.Qataraccountsfor roughly 19 percent of global LNG exports, with a large share flowing to Asian markets. Several major economies rely heavily on these shipments. The United Kingdom imports roughly 5060 percent of its natural gas, with a significant portion coming from Qatar, while Italy receives approximately 4045 percent of its LNG from the country. Higher LNG prices are likely to feed into electricity costs and inflation in economies where natural gas is widely used for power generation.

Despite these risks, the US is generally considered more resilient to energy shocksthaninpreviousdecadesduetostructuralchangesinitsenergysector. TheUSisnowoneoftheworldʼslargestproducersofcrudeoilandnaturalgas, whichhasreduceditsdependenceonimportedenergyandincreaseditsability toabsorbglobalsupplydisruptions.

Nevertheless, higher oil prices still act as a negative supply shock for the economy. Federal Reserve research shows that increases in oil prices tend to raise inflation while simultaneously weighing on economic activity, as higher energy costs raise transportation and production expenses across a wide range of industries. Macroeconomic estimates commonly used in policy analysis suggest that a sustained $10 increase in oil prices can raise inflation by roughly 0.4percentagepointswhilereducingeconomicgrowthbyasimilarmagnitude.

Highercrudepricesalsopassthroughrelativelyquicklytoconsumerfuelcosts. According to the US Energy Information Administration EIA, gasoline prices typically increase by about 2.4 cents per gallon for every $1 rise in the price of crude oil. As a result, a sustained increase in oil prices could push gasoline prices significantly higher, raising household expenses and potentially weighing ondiscretionaryconsumerspending.

Forcomparison,gasolinepricesreachedanationalaverageof$5.01pergallonin June 2022 following Russiaʼs invasion of Ukraine. That surge led many households to reduce spending, demonstrating how energy costs can influence consumerbehaviour.Currently,USgasolinepricesarenear$3.10pergallon,well below the level that typically begins to constrain broader economic activity. Nevertheless, some sectors are more sensitive to energy costs. Industries such as agriculture, manufacturing, mining and chemicals are likely to pass higher energyexpensesontoconsumersthroughincreasedprices.

The broader global economy may face greater pressure. If shipping disruptions continue or the conflict spreads, higher energy prices and logistics costs could increase inflation in multiple regions. Central banks may also delay expected interest rate cuts to prevent inflation from accelerating. Over time, prolonged supply chain disruptions could raise the cost of goods and transportation worldwide, while economies that rely heavily on imported energy may experienceslowergrowth.

Overall, the duration of the conflict will determine the scale of the economic impact.Ashortwarcouldallowenergypricesandshippingconditionstostabilise relativelyquickly.However,aprolongeddisruptionintheMiddleEast,particularly around the Strait of Hormuz and Qatarʼs LNG exports, could sustain higher energycostsandcontributetopersistentinflationacrosstheglobaleconomy.

Strategy(formerlyMicroStrategy) thatithadacquired3,015additional bitcoinsaspartofitsongoingcorporatetreasurystrategycentredonBitcoin.The purchase, disclosed in a Form 8K filing submitted to the U.S. Securities and Exchange Commission, was executed between February 23 and March 1, 2026, andcostapproximately$204.1m,withanaveragepurchasepriceof$67,700per BTC.

Following the transaction, Strategyʼs total bitcoin holdings increased to 720,737 BTC, solidifying its position as the largest corporate holder of bitcoin globally. These holdings were accumulated at a total acquisition cost of about $54.77 bn, correspondingtoanaveragepurchasepriceofroughly$75,985perbitcoin.

The latest purchase was financed through the companyʼs at-the-market ATM equity issuance programs. Strategy raised funds primarily by selling Class A common shares MSTR) and Variable Rate Series A perpetual preferred shares STRC. Specifically, the company sold approximately 1.73 m MSTR shares, generatingabout$229.9m,andissuedadditionalpreferredsharesthatproduced around $7.1 m in proceeds. This capital was then deployed to expand its bitcoin treasurywhileretainingsomeliquidity.

ThisacquisitionispartofStrategyʼsbroaderstrategyofsystematicallyconverting capital raised from equity markets into bitcoin, effectively transforming the company into a leveraged corporate vehicle for bitcoin exposure. The approach reflects the long-standing thesis championed by executive chairman Michael Saylor, who views bitcoin as a superior long-term reserve asset compared with traditionalcashreserves.

However, the aggressive accumulation strategy has also introduced significant financial volatility. Because the company now applies fair-value accounting to its digitalassets,fluctuationsinbitcoinpricesdirectlyaffectreportedearnings.Asa result, the firmʼs financial performance is closely tied to cryptocurrency market movements, with unrealised gains or losses significantly influencing quarterly results.

The US Securities and Exchange Commission SEC has reached a settlement with crypto entrepreneur Justin Sun, resolving a high-profile lawsuit tied to the TRON TRX) ecosystem. Under the agreement, Rainberry Inc., a company associated with the Tron network and the BitTorrent protocol, will pay a $10 m civilpenalty,whiletheSECwilldismissitsclaimsagainstSunandrelatedentities pendingcourtapproval.

The settlement brings an end to litigation that began in March 2023, when the SECsuedSunandseveralaffiliatedorganisations,includingtheTronFoundation andBitTorrentFoundation,forallegedviolationsofUSsecuritieslaws.Regulators accusedSunoforchestratingunregisteredsecuritiesofferingsinvolvingtheTron TRX)andBitTorrentBTT)tokens,aswellasconductingwashtradingschemes designedtoartificiallyinflatetradingvolumesinthesecondarymarket.

According to the SECʼs original complaint, Sun allegedly directed employees to executehundredsofthousandsoftransactionsbetweenaccountshecontrolled, creating the appearance of legitimate market demand and liquidity for TRX. The regulatoralsoclaimedthatSunpaidcelebrities,includingfiguressuchasLindsay Lohan and Jake Paul, to promote Tron-related tokens on social media without properlydisclosingthattheendorsementsweresponsored.

Under the terms of the settlement, Rainberry will be barred for violating certain securitiesregulationsandmustpaythe$10mfine,whileallclaimsagainstSun, the Tron Foundation, and the BitTorrent Foundation will be dismissed with prejudice, meaning the SEC cannot bring the same allegations again. The defendants did not admit or deny wrongdoing, a common condition in US regulatorysettlements.

The resolution reflects a broader shift in the US regulatory environment toward cryptocurrencies. Several enforcement actions launched during the tenure of former SEC chair Gary Gensler have been paused or resolved as policymakers reassessthegovernmentʼsapproachtodigital-assetoversight.

MARAHoldings,oneofthelargestpubliclytradedBitcoinminingcompanies,has revised its digital-asset management strategy to allow the potential sale of Bitcoin held on its balance sheet. The policy change marks a notable shift from the firmʼs earlier “HODLˮ approach, in which it primarily accumulated and retainedminedBitcoinasalong-termtreasuryasset.

Theupdatewasdisclosedinthecompanyʼs2026strategyandSECfilings,which expandedearlierrulesthatonlypermittedsellingnewlyminedbitcoin.Underthe revisedframework,MARAcannowsellportionsofitsexistingtreasuryreserves, providingmanagementwithgreaterflexibilitytorespondtomarketconditionsor liquidityneeds.

As of December 31, 2025, the company held approximately 53,822 BTC, worth about $4.7 bn at the time. A portion of these holdings is already actively deployed through financial strategies: roughly 9,377 BTC have been lent to counterparties, while 5,938 BTC are pledged as collateral for credit facilities totalingabout$350m.

The strategic shift reflects financial pressures and volatility in the crypto mining industry.During2025,MARAreporteda$422.2mdeclineinthefairvalueofits bitcoin holdings, highlighting the impact of price fluctuations on its balance sheet.Atthesametime,miningoutputdropped7percentyear-over-year,partly duetoincreasednetworkdifficultyandthe2024Bitcoinhalving,whichreduced blockrewardsforminers.

Although the company now has the option to sell bitcoin, the policy does not require liquidation. Instead, MARA stated it may buy or sell BTC “from time to timeˮ depending on capital allocation priorities, operating costs, and prevailing market conditions. The company still expects its Bitcoin holdings to generally growovertimethroughminingandoccasionalpurchases.

Overall, the new policy reflects a broader transformation in MARAʼs financial strategy.RatherthansimplyaccumulatingBitcoinasapassivetreasuryasset,the company is moving toward a more active balance-sheet management model, where its multibillion-dollar Bitcoin reserve can be used strategically to support liquidity,operations,andlong-termgrowthinitiatives.

Minnesotaintroducedregulatorymeasuresin2024toaddressfraudriskslinked tocryptocurrencykiosks.Theserulesrequiredoperatorsto:

● displaywarningsthatvirtualcurrencyisnotlegaltender

● informcustomersthattransactionsareirreversible

● clarifythatfraud-relatedlossesaregenerallyunrecoverable

Thelawalsoimposeda$2,000dailytransactionlimitfornewcustomers,defined as those with accounts less than 72 hours old, and required full refunds for fraudulently induced transactions if customers contacted both the operator and lawenforcementwithin14days.

Despite these measures, state officials said fraud persists. The Department of Commerce stated that earlier consumer protection efforts have not delivered sufficient results. HF 3642 would therefore repeal the current framework rather thanamendit.

Importantly, the proposed ban applies only to physical kiosks. Residents would stillbeabletopurchaseortransferdigitalassetsonline.

While regulators initially sought to mitigate risk through transaction limits and mandatory disclosures, lawmakers now appear prepared to remove the machinesentirelyfromthestate.

The debate highlights a broader policy shift: regulators are increasingly distinguishing between online digital asset access and physical cash-to-crypto infrastructure,whichtheyviewasmoresusceptibletoexploitation.