WHY IT’S TIME TO LOOK TO THE MARKET FOR RETIREMENT SAVINGS

GIGAWATTS & MEGADEALS: THE SHEER SCALE OF AI INFRASTRUCTURE

MEET THE TEAM

STEVE HAYSOM

Publisher 07973 483 687 steve.haysom@muckle.com

GRAEME FOSTER

Head of Sales & Marketing 07881 502 705 graeme.foster@diyinvestor.co.uk

Those of you that don’t habitually walk around with a bag on your head, will have noticed that there is rather a lot of ‘noise’ and no little excitement around artificial intelligence (AI) just now.

Those in the know will tell you that it is, without doubt, the biggest threat/greatest opportunity in town.

Supporters predict that over the next decade, AI will add £7,000,000,000,000 to global GDP and improve all aspects of human endeavour; detractors warn of a long-term existential threat to mankind from advanced, uncontrollable superintelligence.

Acknowledging that AI is still in its infancy, and that the wisdom it dispenses is only as good as the questions it is posed, it is tempting to be slightly cynical and question why nobody thought to ask ‘would Peter Mandelson be a good choice as US ambassador’?

Or wonder what advice FOMO-frenzied bitcoin investors received when the currency peaked at $126,000 in October 2025; today it is worth $63,000.

In this issue we hear from Allianz Technology Trust, and the eyewatering sums of money that are being poured into creating AI infrastructure.

Again, opinion is divided – supporters see the massive capital expenditure as reason why the ‘bubble’ won’t burst; detractors such as Arvind Krishna, CEO of IBM, say that the cost of a 3 GW data centre at anything up to $240 billion, means they will never be profitable.

Despite 61% of UK retail investors believing valuations are stretched, 67% plan to maintain or increase their exposure to AI, viewing it as a long-term growth story rather than just a trend.

Enthusiasm is high—particularly among Millennials and Gen Z— and investors are navigating the risks of a potential AI ‘bubble’ by diversifying into infrastructure plays like data centres and energy and looking for the next-big-thing in adopting the technology.

With the application of AI technology, the future of financial advice will be hybrid: AI providing speed, scale, and precision with humans providing perspective and empathy - dubbed ‘human-machine teaming’.

Retail investors have embraced AI technology, with a 2025 press release from eToro announcing ‘Retail investors flock to AI tools with usage up 46% in one year’.

This shift is driven by the desire for faster research, better decision-making, and lower costs compared to traditional fund managers; 80% of millennial investors and 79% of Gen Z have turned to AI to help build portfolios.

The phenomenal number-crunching power of AI reduces the time spent on research, provides advanced analytics to individual investors that were previously only available to institutions, and hyper-personalisation as new tools allow investors to build customised, bespoke indices based on specific criteria.

However, unlike advised clients, retail investors do not have easy access to those performing what Vanguard describes as ‘empathy-driven tasks’ - work that depends on understanding human behaviour, guiding emotions, and building trust.

AI makes ‘right’ decisions based on the information it is fed; it would not be difficult to imagine there being a ‘best’ portfolio for an investor based upon their personal circumstances and objectives.

But this is where DIY Investor comes in.

The content it provides is broadly divided between ‘explainers’ ‘experience’ and ‘expert’.

Financial education – ‘explainers’ - remains crucial and is the way to engage the next generation of investors.

‘Experience’ is how do people like you behave and respond to changing circumstances?

‘Expert’ could come from seeing a glint in the eye of the manager of one of the new ‘Active ETFs’ in a video in which he outlines his strategy to ‘outperform’.

DIY Investor has embraced a hybrid model for over a decade.

LEADING THE DIY

Denied access to advice by RDR, or unwilling to pay for something that was previously free, millions of people now take full or partial control of their finances.

Whether seeking to get on the property ladder, planning for tuition fees or taking advantage of new pension freedoms, more than ever are setting their objectives, and building a portfolio of investments that allows them to achieve their goals whilst comfortable with the level of risk their money is exposed to.

Education is the key and technology the enabler - DIY Investor delivers information to existing investors and education to those new to savings and investment; share experience and learn to make informed investment decisions.

NOBODY CARES MORE ABOUT YOUR MONEY THAN YOU

WHY IT’S TIME TO LOOK TO THE MARKET FOR RETIREMENT SAVINGS

THE

SAVINGS LANDSCAPE IS SHIFTING – AND THE BUDGET HAS SPED THINGS UP. WITH CASH

BECOMING LESS TAX‑EFFICIENT AND RATES EASING, MANY LONG‑TERM SAVERS MAY NOW NEED TO LOOK BEYOND CASH TO SUPPORT THEIR RETIREMENT GOALS.

Author Thomas Moore Investment Manager, Aberdeen Equity Income Trust plc

At first sight, Chancellor Rachel Reeves’ 2025 Budget did not appear to do long-term savers many favours. But could her announcements nudge people in the right direction?

As well as reducing the amount that people aged under 65 can save into a cash ISA each year from April 2027, from the full £20,000 allowance to just £12,000, the Budget also included plans to increase tax by 2% on both investment dividends and savings interest (from April 2026 and 2027 respectively).

The income tax rises are a clarion call for savers to make the best possible use of their annual ISA allowance as a priority. But the slashing of the cash ISA limit means that if they are to maximise the amount of savings they shelter from tax, they will need to turn to a stocks and shares ISA account for at least part of it.

‘IT

IS SET TO BECOME HARDER TO FIND SAVINGS ACCOUNTS PAYING MORE THAN 4%’

The volatility of stocks and shares ISAs may have been a reason why some savers have historically favoured the certainty of cash ISAs. However, at the same time as the allowance is slashed and the tax of cash interest is hiked, interest rates on cash ISAs are falling.

With economists anticipating more base rate cuts, it is set to become harder to find savings accounts paying more than 4%.

This further increases the incentive to venture into the stock market, assuming you have time on your side and can tie

some money up for at least three years and preferably longer. And once you’ve decided to seek exposure to stocks and shares, there is a strong argument for UK equity income as a great area to explore.

Having peaked at just under 7000 in 1999, the FTSE 100 index of the UK’s largest companies did not breach the 8000 ceiling until May 2024; it is now sitting just below the 10000 mark, having risen just under 20% during 2025. Such a strong rally indicates a change of sentiment as investors have started to return to a market unloved for over two decades.

Despite this rally, the UK equity market is still cheap in comparison with other equity markets around the world, trading at a Price/Earnings ratio of 13x compared the US equity market at 21x, Japan at 17x and Europe at 15x.

‘INVESTORS HAVE STARTED TO RETURN TO A MARKET UNLOVED FOR OVER TWO DECADES’

Although the UK’s headlines have been dominated by domestic economic weakness and political uncertainty, the corporate landscape by and large remains in good shape, with many companies growing profits and using those profits to pay down debt, invest in their operations, buy back their own shares, and pay attractive dividends.

With this backdrop, there is no shortage of well-managed businesses with strong earnings prospects for stock-picking managers such as the team at Aberdeen Equity Income Trust (AEI). Against a challenging economic backdrop, we see merit in a highly selective ‘best ideas’ approach, seeking out companies that are well placed to generate cash flows and use those cash flows to pay dividends.

The beauty of equity income investing is that shareholders potentially receive a dividend income as part of their investment returns. In the case of AEI that’s an attractive 6% p.a. at present – well above the best of the cash ISA payouts.

While dividends are not guaranteed, they can be less volatile than shares and can help shareholders visualise the make-up of their returns.

‘SHAREHOLDERS POTENTIALLY RECEIVE A DIVIDEND INCOME AS PART OF THEIR INVESTMENT RETURNS’

The Trust’s status as a “Dividend Hero” helps underline the consistency of its dividend track record. The Dividend Hero accolade is awarded by the Association of Investment Companies to trusts that have maintained or grown their dividend payouts for more than 20 consecutive years and has become a coveted badge of honour among income - focused investment trusts.

With 25 years of dividend growth under AEI’s belt, the team will do all they can to protect that hard-won record. While there is no guarantee that this dividend growth will be maintained, the fact that the Trust was able to use its reserves to keep growing the dividend during the Covid crisis - despite around half the companies on the stock market cancelling their dividends – acts as a useful indicator of its robustness.

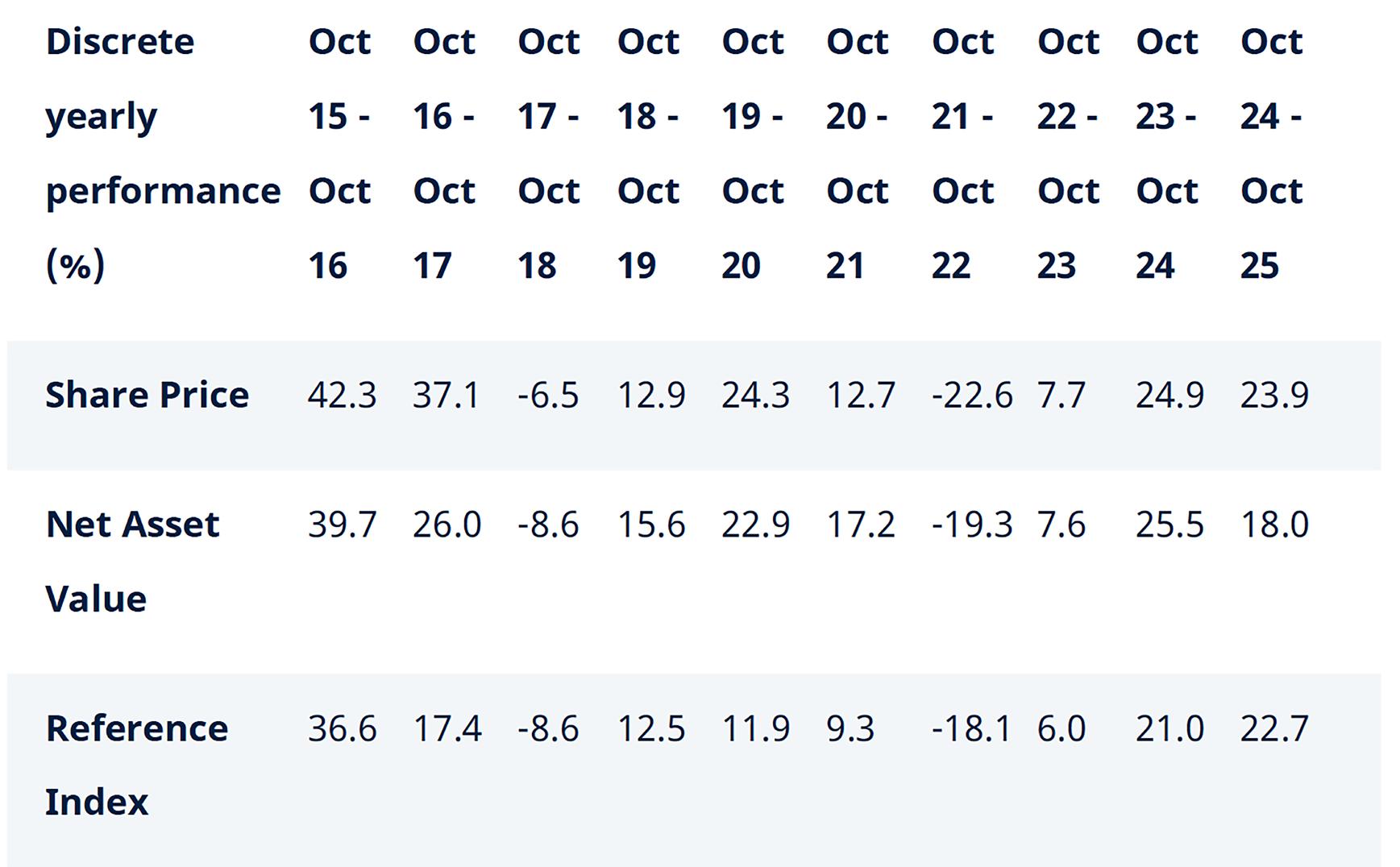

AEI’s track record provides some evidence on how the team’s stock-picking strength can underpin an attractive and growing dividend and capital growth. To 31 December 2025, the Trust beat the benchmark FTSE All-Share Index in total return terms over one, three and five years. Over the 12-month period to year-end it gained 32.5%.

‘AT A TIME WHEN THE ATTRACTIONS OF CASH SAVINGS ARE STARTING TO DIM, IT COULD BE TIME TO CONSIDER THE DIVIDEND-RICH UK

MARKET’

At a time when the attractions of cash savings are starting to dim, it could be time to consider the dividend-rich UK market. Share prices might be unpredictable, but many companies will continue to generate cash flows and pay them out in the form of dividends.

Those payouts enable investment trusts like AEI to build a portfolio that can offer a dividend yield well in excess of the rates currently available on a cash account, with the potential for capital growth over time.

VISIT ABERDEEN EQUITY INCOME TRUST >

INVESTMENT OBJECTIVE

To provide shareholders with an above average income from their equity investment while also providing real growth in capital and income.

RISK FACTORS YOU SHOULD CONSIDER PRIOR TO INVESTING IN ABERDEEN EQUITY INCOME TRUST (“THE COMPANY”):

The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested.

Past performance is not a guide to future results.

Issued by abrdn Fund Managers Limited, registered in England and Wales (740118) at 280 Bishopsgate, London EC2M 4AG. The company is authorised and regulated by the Financial Conduct Authority in the UK.

Find out more at www.aberdeeninvestments.com/aei or by registering for updates. You can also follow us on LinkedIn, Facebook, YouTube and X.

ABERDEEN EQUITY INCOME TRUST: MANAGER UPDATE VIDEO>

Watch the latest manager update video featuring Aberdeen Equity Income Trust’s portfolio manager, Thomas Moore. In this video, Thomas outlines the trusts dividend yield, sector allocation, and performance.

DIVIDEND HEROES

The AICs dividend heroes are the investment trusts that have consistently increased their dividends for 20 or more years in a row.

DUNEDIN INCOME GROWTH INVESTMENT TRUST: MANAGER UPDATE VIDEO

Rebecca Maclean, Investment Managers, Dunedin Income Growth Investment Trust PLC

Ben Ritchie, Investment Managers, Dunedin Income Growth Investment Trust PLC

WATCH THE LATEST MANAGER UPDATE VIDEO FROM DUNEDIN INCOME GROWTH INVESTMENT TRUST, FEATURING CO MANAGERS BEN RITCHIE AND REBECCA MACLEAN.

In this video, Ben and Rebecca discuss changes to the portfolio, opportunities in the midcap space, and Geopolitical forces that are shaping market outcomes.

VISIT DUNEDIN INCOME GROWTH INVESTMENT TRUST >

Aberdeen Investment Trusts

If you’re keen to capture the potential offered by global investment markets but uncertain if now is the right time, consider Aberdeen Investment Trusts. Managed by teams of experts, all of them taking a long-term, patient approach, each of our trusts are designed to bring together the most compelling opportunities we can find to generate the future investment growth or income you’re looking for.

Benefit from Aberdeen’s specialist teams covering a broad spectrum of markets and sectors. There’s plenty of choice to target your specific investment goals, whichever stage of life you’re at. And you can invest lump sums now or drip feed your investing over time.

Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested.

Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Invest in your future via leading platforms.

EVERYONE IS TALKING ABOUT AI, BUT WHAT DOES IT TAKE TO POWER THIS REVOLUTION? IN SILICON VALLEY BITESIZE, PORTFOLIO MANAGER MIKE SEIDENBERG AND HOST CHERRY REYNARD, DISCUSS THE MASSIVE INFRASTRUCTURE BUILD‑OUT HAPPENING RIGHT NOW – A WAVE OF INVESTMENT SO LARGE IT DWARFS MAJOR PUBLIC WORKS PROJECTS.

Michael A. Seidenberg Lead Portfolio Manager

Cherry Reynard, Award-winning news and features journalist, specialising in investment

FROM MULTI‑GIGAWATT DATA CENTRES THAT CONSUME THE POWER OF A SMALL CITY TO CRITICAL “PLUMBING” COMPANIES PROVIDING EVERYTHING FROM COOLING SYSTEMS TO BACKUP POWER SOFTWARE, MIKE EXPLAINS WHY AI IS ABOUT SO MUCH MORE THAN CHIPS, AND HOW ALLIANZ TECHNOLOGY TRUST TEAM AIMS TO IDENTIFY THE BEST IN CLASS COMPANIES POISED TO WIN IN THIS NEW TECHNOLOGY CYCLE.

CHERRY : I’m Cherry Reynard, and with me today is Mike Seidenberg, Fund Manager on Allianz Technology Trust. Mike, in our last conversation, you talked about the first and second derivatives of the AI theme, so beyond chip makers to companies like Amphenol, which make data centre connectors; what is the scale of this infrastructure build-out.

MIKE : Great question - the scale is really hard to digest, but a gigawatt data centre is roughly the power needed for 750,000 to 1m homes.

Companies like Meta plan multiple gigawatt data centres costing $40bn to $45bn per gigawatt; that tells me as an investor, this is not a passing fad, it is a secular theme of which like we’ve seen previously in the cloud, software as a service, etc.

It really encourages me to think about every single aspect of that data centre and how we can monetize it.

Power supply is a huge bottleneck. We have looked at various alternatives, but it’s cooling, it’s power – not just the chips you hear about on the front page of the FT, there are multiple facets.

The amount of money that is being spent is truly daunting to me, when someone throws out $250 billion – I was looking at the cost of the Elizabeth line as I was riding on it this morning because I absolutely love it – and it was £19bn.

The amount companies are spending on data centres shows the enthusiasm around artificial intelligence is real and the spend is real.

CHERRY : So, just one data centre is like a small city in terms of its energy needs.

MIKE : Not even a small city, right? Most data centres are being built in areas with proximity to power – not Silicon

Investment trust champions for generations

Allianz Global Investors and its predecessors have been managing investment trusts since 1889. Our trusts span investor aims – from income, to growth, to the specialist sector of technology – and offer a path to investment opportunities around the world. So whatever your investment goals, please take a closer look and discover what our investment trusts could bring to your portfolio.

Please note: investment trusts are listed companies, traded on the London Stock Exchange. Their share prices are determined by factors including demand, so shares may trade at a discount or premium to the net asset value. Past performance does not predict future returns. Some trusts seek to enhance returns through gearing (borrowing money to invest). This can boost a trust’s returns when investments perform well, though losses can be magnified when investments lose value. A ranking, a rating or an award provides no indicator of future performance and is not constant over time. You should contact your financial adviser before making any investment decision. 0800 389 4696 uk.allianzgi.com/investment-trusts

For further information contact the issuer at the address indicated below. This is a marketing communication issued by Allianz Global Investors UK Limited, 199 Bishopsgate, London, EC2M 3TY, www.allianzglobalinvestors.co.uk. Allianz Global Investors UK Limited company number 11516839 is authorised and regulated by the Financial Conduct Authority. Details about the extent of our regulation are available from us on request and on the Financial Conduct Authority’s website (www.fca.org.uk). The duplication, publication, or transmission of the contents, irrespective of the form, is not permitted; except for the case of explicit permission by Allianz Global Investors UK Limited. THIS IS A MARKETING COMMUNICATION. PLEASE REFER TO THE KEY INFORMATION DOCUMENT (KID) BEFORE MAKING ANY FINAL INVESTMENT DECISIONS. INVESTING INVOLVES RISK. THE VALUE OF AN INVESTMENT AND THE INCOME FROM IT MAY FALL AS WELL AS RISE AND INVESTORS MAY NOT GET BACK THE FULL AMOUNT INVESTED.

You can’t get the power and you can’t get these things spun up. They’re talking about 2026/ 2030 deliveries on a lot of this stuff, so are long lead times.

Power is of a bottleneck and there’s all kinds of bottlenecks that really preclude people from getting and running quickly. And they’re moving as fast as they can, right?

Companies are spending so much and they’re so aggressive about their spending, but it takes a while, it really does.

CHERRY : How much of that is meeting demand today and how much of it is anticipating future demand?

MIKE : A lot of the companies providing the services today, are constrained on the amount of service they can provide to their potential customers.

Over time, that’ll even out because there’ll be more competition, there’ll be more things that will come online. But today, it’s not that there isn’t demand, it’s can we supply that demand?

CHERRY : Are there any infrastructure needs that are coming next that aren’t on investors’ radars yet? You mentioned some of those bottlenecks.

MIKE : There’s just so much happening in technology; we haven’t even talked about the drones and stuff like that. Our most finite resource is our time, and I want to make sure we use it wisely. So, to me and the team, this is the biggest thing we’ve come across in a long time.

So I’m not really thinking about what else right now, because our plates are pretty full. But inevitably there will be, and that’s the great thing about the job and the great thing about the sector is you just go through these cycles where difficult problems are solved by these really innovative companies and that creates an opportunity.

CHERRY : Absolutely. Okay, great. We will wrap up there. Thank you so much, Mike.

MIKE : Great talking to you.

CHERRY : And thank you to our listeners for tuning in. You can find out more about the Trust at our website, allianzetechnologytrust.com. Until next time.

BEYOND THE HYPE: A DISCIPLINED APPROACH TO TECH INVESTING

In a market defined by AI euphoria and economic uncertainty, how do you find real value?

In this interview, ATT’s Mike Seidenberg shares his disciplined approach to tech investing. He discusses navigating the tech investing market, the enduring need for cybersecurity, and the emerging opportunities in quantum computing and blockchain that are flying under the radar.

A must-watch for a measured, long-term view on the tech landscape.

ATT UPDATE – BEYOND THE OBVIOUS: UNCOVERING TECH’S

HIDDEN BENEFICIARIES

How do you find the next big thing in tech? In this video, ATT’s Mike Seidenberg explains how Silicon Valley’s unique ecosystem of talent, capital, and ideas provides an edge in spotting secular trends.

Learn how the team looks beyond the obvious AI plays to find “second derivative” opportunities, why they remain bullish on software, and the research that led to a new investment in Spotify.

A quick look into a process-driven investment philosophy for identifying the future of innovation.

EXPLORE THE STORIES FROM INSIDE THE PORTFOLIO BELOW

Hear from the Portfolio Manager as they explore some of the Trust’s current and past holdings, illustrating how these investments reflect our strategy and decision-making process.

Disclaimer: This is a marketing communication. Please refer to the key information document or KID before making any final investment decisions.

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors might not get back the full amount invested. Past performance does not predict future returns.

The mention of any particular security or strategy should not be considered as arecommendation. For further information on the Allianz Technology Trust www.allian technologytrust.com

Valley or San Francisco, but the middle of Texas, with access to oil and power. So, using 700,000 as our example, if you build a three-gigawatt data centre that’s 2.1m households; a tremendous build out.

CHERRY : What does that look like on the ground? Are cranes and construction sites emerging?

MIKE : Data centres are not being built in high density urban areas, but in places like West Texas, with access to cheaper power and energy sources and cheaper land. Having had a really difficult time during and after COVID, places like San Francisco are now experiencing lease ups - buildings being leased back up. Big AI companies are taking large chunks of space in major metropolitan areas, and they’re hiring people.

There’s a trickle-down effect for those local economies as businesses build out teams, and there are hundreds or even thousands of employees if you think about a company like OpenAI.

It’s exciting, and you can really feel it, based upon job activity. So, I’m sure you could see cranes building data centres if you went to certain places, but it’s exciting. I mean, it really is.

You mentioned other plumbing companies benefiting from heating and cooling?

MIKE : Again, we focus on technology, so I wouldn’t buy a concrete company just because building data centres uses a lot of concrete; but the shells of these are enormous, it’s a scale.

It really is a scale business, but we’re looking at companies that go inside that data centre – backups, backup power supply software, right? A niche business that handles the backup power the centres need with software solutions.

We’re trying to understand who the various companies and various beneficiaries are, whilst remembering that ourfocus, our job and our mantra is to focus on technology investing.

CHERRY : With a huge trend like this, you obviously have lots of companies in the zone and benefiting from it. How do you exercise discernment in that environment? I mean, what separates a good business from a great business?

MIKE : Great question. What separates a good business from a great business is ultimately, how do they execute?

How good are the management running these particular businesses? In technology, the number one or two player takes disproportional share. I read a tidbit last week from Arthur Patterson at Excel talking about how companies and technology tend to dominate cycles. And it’s why we have always focused on the number one or two players in a given subsector.

Execution is a function of management, taking the solution and propagating the culture throughout, whether it’s sales, marketing, or customer service, all the things that really matter. We invest in what we think are excellent companies without being attracted to a number three or four player because, oh, well, we like this space. It’s an interesting space.

Shouldn’t we own all four competitors in that space? And we really try to remember to be disciplined because over a cycle, the number one or two players will inevitably win.

CHERRY : Is it ever possible to get as excited about a widget maker as it is about a sexy AI software company, or is it a case of having a balance in a portfolio because they’re kind of doing different things?

MIKE : Ultimately it revolves around risk reward. I covered the video game sector earlier in my career and it was fun, right? Interesting IP, sports games, but, ultimately as a portfolio manager, my job is to empower the team to bring us good risk reward ideas. And yeah, is it more fun to go visit a company that’s making some incredible AI for healthcare?

But that widget company whose total addressable market may have gone up by 4X, I mean, that’s really exciting to dive in, figure out the business, figure out where it’s going, where are they going to earn three years out.

Not every business we invest in is sexy or cool, but ultimately, I can get just as excited about a business making connectors as I can somebody making special effects software for movies.

CHERRY : How far into this infrastructure build-out cycle do you think we are?

MIKE : It’s early days. It really is, and it’s not just me saying it. If you listen to the likes of Larry Ellison talking about Oracle, or the CEO of Microsoft, they are constrained, right? And they’ve talked about being constrained. And that constraint is just getting worse.

The Brunner Investment Trust PLC

Established in 1927, The Brunner Investment Trust seeks income as well as capital growth from companies around the world. Because we’re not tied to any one country or sector, we’re free to seek potential opportunities wherever they may be: from European energy to Japanese pharmaceuticals, Swiss healthcare to French luxury goods, U.S. cloud computing to Taiwanese components. As an investment trust, Brunner enjoys other advantages too, such as being able to draw on revenue reserves to support dividend payments in tough times. Although past performance is no guide to the future, we’ve paid a rising dividend to our shareholders for 50 consecutive years, earning the Association of Investment Companies’ coveted Dividend Hero status. So visit us online to learn more or to register for regular updates and insights, and find out how Brunner could help you achieve your investment goals.

www.brunner.co.uk

INVESTING INVOLVES RISK. THE VALUE OF AN INVESTMENT AND THE INCOME FROM IT MAY FALL AS WELL AS RISE AND INVESTORS MAY NOT GET BACK THE FULL AMOUNT INVESTED.

A ranking, a rating or an award provides no indicator of future performance and is not constant over time. You should contact your financial adviser before making any investment decision. This is a marketing communication issued by Allianz Global Investors GmbH, an investment company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, D-60323 Frankfurt/M, registered with the local court Frankfurt/M under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de). The summary of Investor Rights is available at https://regulatory.allianzgi.com/en/investors-rights. Allianz Global Investors GmbH has established a branch in the United Kingdom deemed authorised and regulated by the Financial Conduct Authority. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website (www.fca.org.uk).

HOW A TOTAL RETURN MINDSET CAN HELP INVESTORS ACCESS ASIA’S LONG‑TERM OPPORTUNITIES

Asia offers some of the most compelling long-term opportunities in global equity markets, but it can also be unpredictable. Its economic growth potential is well recognised, but this doesn’t necessarily translate into positive stock market performance. The region’s income credentials may be less well understood, even though many companies now combine strong balance sheets with growing dividends and capital discipline.

In a region as large and diverse as Asia, selectivity is critical. Active managers who know the region well can add meaningful value by focusing on the most attractive businesses and managing risk carefully. This article explores why a total return approach – blending growth, income and disciplined risk management – offers a resilient way to harness Asia’s potential.

GROWTH – AN EVOLVING LANDSCAPE OF OPPORTUNITY

Many of Asia’s economies have demonstrated a consistent ability to grow faster than their more mature counterparts in North America and Europe, supported by favourable demographics, urbanisation and rising household incomes.

Alongside the region’s established export industries, a new generation of consumer, financial and technology companies has emerged in recent years to serve expanding domestic demand.

For investors, this evolution means that Asia’s opportunities now extend well beyond the familiar manufacturing-led focus of the past. Active stock pickers can access businesses with durable growth drivers across a range of sectors – from global suppliers of semiconductors to regional banks and service companies linked to rising consumption.

‘ASIA’S ECONOMIES HAVE DEMONSTRATED A CONSISTENT ABILITY TO GROW FASTER THAN THEIR MORE MATURE COUNTERPARTS IN NORTH AMERICA AND EUROPE’

The widening mix of industries and business models has, however, also brought greater dispersion in company performance, reinforcing the importance of selectivity in identifying sustainable long-term growth.

While the region’s overall growth outlook remains positive, it will not be uniform. Some larger economies may face structural challenges, whereas others continue to benefit from the rise of consumer demand, productivity gains and positive demographics. That makes selectivity critical –being in the right companies and the right markets will be essential to capturing Asia’s long-term potential.

INCOME – DIVIDENDS AS A

MARK

OF DISCIPLINE

Dividend income has become an increasingly important part of the Asian equity story. Markets such as Australia and Singapore have long demonstrated a strong dividend-paying culture, but there is growing evidence that this is spreading to other parts of the region.

Governance standards have improved markedly in several markets, including China and Korea, and many companies now recognise that regular, growing dividends signal capital discipline and effective long-term stewardship.

This shift has changed the character of Asian markets –where returns once came primarily from capital growth, an increasing share now comes in the form of dividends from companies that generate healthy cash flow and return it regularly to their shareholders.

‘MANAGEMENT TEAMS ARE FOCUSED ON DELIVERING SUSTAINABLE SHAREHOLDER RETURNS’

There is clear evidence that this discipline pays off. In markets such as Australia and Singapore, where Schroder Asian Total Return has meaningful exposure, companies

with a sustained record of dividend growth have tended to outperform those that have not demonstrated such capital efficiency. A strong dividend policy can therefore be seen not as a constraint on growth but as a marker of quality –a sign that management teams are focused on delivering sustainable shareholder returns.

For a total return investor, that combination of a good starting yield and the potential for sustained dividend growth is powerful. It provides a tangible income stream while allowing investors to benefit from the compounding of reinvested dividends over time –a stable foundation on which to build long-term wealth from Asia’s corporate progress.

ACTIVE AND SELECTIVE –TURNING DIVERSITY INTO ADVANTAGE

Asia is not a single, uniform market but a collection of economies with distinct growth profiles, sector compositions and investment characteristics. This diversity represents opportunity for active investors, but it also demands skill and discipline to navigate effectively.

The region’s financial markets have matured and are much deeper than they used to be, but they remain relatively inefficient. Research coverage and liquidity can be patchy, which often leads to valuation anomalies that experienced, well-informed managers can identify and capture.

The investment team behind Schroder Asian Total Return applies an unconstrained, benchmark-agnostic approach that is designed to take advantage of these inefficiencies.

‘THE MANAGERS FOCUS ON BUSINESSES WITH STRONG COMPETITIVE POSITIONS, ROBUST BALANCE SHEETS AND MANAGEMENT TEAMS THAT ALLOCATE CAPITAL EFFECTIVELY’

Their process begins with detailed, bottom-up research to identify companies that combine durable business models with sensible valuations and sound governance.

Supported by Schroders’ extensive research network across the region, the managers focus on businesses with strong competitive positions, robust balance sheets and management teams that allocate capital effectively.

The managers view Asia through four key clusters –China / Hong Kong, Korea / Taiwan, Australia / Singapore, and India / ASEAN – each with distinct drivers and sources of return.

By investing selectively rather than broadly, the managers can avoid areas of structural weakness and concentrate capital in businesses with clear, long-term earnings potential. This selective, research-driven approach has been central to the trust’s ability to deliver attractive total returns while carefully managing risk.

DERIVATIVES – SMOOTHING THE JOURNEY

Managing risk is an integral part of generating long-term returns, and for Schroder Asian Total Return, the use of derivatives (such as futures and options) can play a supporting role.

The portfolio managers employ a systematic, model-based framework to determine when market conditions may justify additional protection. The aim is to reduce volatility and preserve capital during downturns.

There are two strands to this approach. The strategic element draws on valuationbased models that assess the longer-term risk and return profile of each market.

When a market appears significantly overvalued, for example, the team can use index futures or options with the aim to reduce market exposure while retaining their underlying stock positions.

‘MANAGING RISK IS AN INTEGRAL PART OF GENERATING LONG-TERM RETURNS’

Meanwhile, the process also offers a tactical overlay which operates over a shorter time horizon, guided by proprietary indicators that assess sentiment and momentum across the region.

Together, these tools allow the managers to take measured, cost-effective steps to protect the portfolio without diluting its long-term growth potential.

Asian equity valuations have historically cycled through long expansions and corrections. That volatility highlights why the team’s disciplined use of derivatives remains a valuable tool – helping to smooth returns, preserve capital and allowing investors to stay invested through market cycles.

CONCLUSION – CAPTURING TOTAL RETURNS WITH DISCIPLINE

For Schroder Asian Total Return, this approach brings together the elements that can matter most in Asian equity investing: structural growth, an expanding universe of income-paying companies and the selectivity to focus on long-term value creation.

‘STRUCTURAL GROWTH, AN EXPANDING UNIVERSE OF INCOME-PAYING COMPANIES AND THE SELECTIVITY TO FOCUS ON LONG-TERM VALUE CREATION’

By combining disciplined stock selection with an effective framework for managing risk, the strategy aims to capture Asia’s potential while limiting the impact of market volatility.

For investors, that balance between opportunity and discipline offers a compelling proposition – access to Asia’s long-term growth, delivered through a strategy built to successfully navigate the inevitable ups and downs of markets.

CLICK HERE TO VISIT THE SCHRODER ASIAN TOTAL RETURN HOMEPAGE >

SCHRODER ASIAN TOTAL RETURN INVESTMENT COMPANY –DISCRETE YEARLY PERFORMANCE (%)

WHY INVEST IN ATR?

The Schroder Asian Total Return provides an unconstrained approach to investing in Asian markets, seeking to provide a total return to investors while providing an element of capital protection.

BEHIND THE TRUST: READ OUR PHILOSOPHY ARTICLE >

MARKETING MATERIAL

Please remember that the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England.

For illustrative purposes only and does not constitute a recommendation to invest in the above-mentioned security / sector / country.

Schroder Unit Trusts Limited is an authorised corporate director, authorised unit trust manager and an ISA plan manager, and is authorised and regulated by the Financial Conduct Authority.

Before investing in an Investment Trust, the latest Key Information Document (KID) at www.schroders.co.uk/investor or on request.

For help in understanding any terms used, please visit address https://www.schroders.com/en-gb/uk/individual/glossary/

INVESTING BASICS: BUY

AND HOLD

FOREVER ETFS ‑ THE SLEEP‑EASY INVESTMENT STRATEGY

HOW TO BUILD A ROCK‑SOLID, LOW‑STRESS PORTFOLIO WHERE TIME DOES THE WORK

In a world of flashing headlines, volatile markets, and chaotic change, the idea of simply buying something and never selling it can feel like a fantasy. But for long-term investors, a ‘buy and hold forever’ strategy proven to be a powerful way to grow wealth over time with minimal stress.

Investors can apply that philosophy using ETFs to create a globally diversified, lowmaintenance portfolio that delivers returns over the long haul – and helps you sleep a little better at night.

WHAT DOES ‘BUY AND HOLD FOREVER’ MEAN?

Buy and hold forever is about buying high-quality assets with the intention of holding them for decades, potentially for life.

It’s not about chasing trends or timing the market; it’s about identifying investments that are resilient, globally diversified, and capable of compounding steadily over time.

Traditionally, this approach has been associated with iconic individual stocks like Microsoft, Johnson & Johnson, or Nestlé – companies with a long history of stability, profitability, competitive advantage, and durable shareholder returns.

Yet a more accessible way to pursue this strategy is via ETFs that capture the returns of fundamentally valuable companies, without requiring you to constantly trade or change tactics.

WHY USE ETFS FOR A FOREVER STRATEGY?

For investors looking to buy and hold forever, ETFs provide:

Simplicity: Thousands of global companies in one single fund.

Diversification: Not reliant on the fortunes of one or two companies.

Strategic: Instead of micro-managing thirty or forty stocks, you can gain exposure to “forever stocks” using just a few ETFs that target the right parts of the economy.

Plus, if you want to experiment with a new tactic, you can bring a new ETF into play and track its performance.

Low maintenance: A portfolio of half a dozen ETFs is simple to follow and can be managed with minimal effort.

Choose your ETFs wisely and you can build a portfolio that grows quietly in the background while you get on with the rest of your life.

KEY FEATURES OF ‘FOREVER’ ETFS

The building blocks of long-term, hold-forever portfolio are:

Global diversification: Exposure to both developed and emerging markets.

High‑quality companies: Preference for companies with stable earnings and strong balance sheets.

Dividend sustainability: A tilt towards companies that can return consistent income over time.

Low volatility: Stocks that are resistant to economic downturns and deep market slumps.

You can tilt your portfolio to a greater or lesser degree towards each of these buy and hold forever ETF categories:

1. GLOBAL DIVIDEND STOCKS

Companies with a strong history of paying and increasing dividends.

Pros: Steady income stream.

Less volatile than growth-focused equities.

Focus on financially sound, mature companies.

Cons: May underperform during bull markets led by growth stocks.

Can be concentrated in sectors like utilities and consumer staples.

Dividend cuts can still occur during recessions.

JUSTETF TIP: To adhere to a buy and hold forever strategy, favour ETFs that select for companies with a track record of maintaining and increasing dividends. (Or some other quality screen). These approaches contrast with a pure high dividend yield methodology. High yield ETFs are more likely to contain distressed firms in their mix.

SEE OUR GLOBAL DIVIDEND STOCK INVESTMENT GUIDE FOR MORE.

2. WORLD QUALITY EQUITIES

Quality factor companies are chosen for their high return on equity, low debt, and stable earnings growth.

Pros: The ETF targets stocks with characteristics known to outperform the market over the long run.

Desirable traits indicate the firm is positioned to reap high profits in the future.

Combines growth and resilience in one approach.

Cons: Quality factor stocks have a history of outperformance, but this cannot be guaranteed in future.

These firms operate in the most ferociously competitive parts of the economy – periods of underperformance are almost certain.

For long stretches, quality firms lag the broad market; you will only collect the pay-off if you stay invested during the soft patches.

See our Quality factor ETF investment guide for more.

3. WORLD LOW VOLATILITY / MINIMUM VOLATILITY EQUITIES

These ETFs concentrate on stocks that fluctuate less than the broader market; they smooth the ride and reduce emotional pressure during downturns.

Pros: Reduce portfolio swings.

Helps investors stay the course during market stress.

Defensive exposure to stable sectors.

Cons: Likely to trail the broad market during strong bull markets.

Performance depends heavily on specific volatility filters.

Not immune to losses in major selloffs.

See our Low Volatility ETF investment guide for more.

4. CORE GLOBAL EQUITIES

Core global equity is the foundation of a forever portfolio because it’s always dominated by the market leaders.

Pros: The market cap index causes global ETFs to own the most valuable public companies in the world.

Long-term growth engine of any portfolio.

Captures the rise of revolutionary new firms as they break through.

Cons: Includes exposure to underperforming regions and sectors.

Can be volatile during global downturns.

This is the market, and every investor itches to beat the market, no matter how hard that is.

See our World ETF investment guide for more.

CUSTOMISE

YOUR “BUY AND HOLD FOREVER”

STRATEGY

How do you choose from this palette of ETFs?

Use a core global equities ETF as your baseline; the more you habitually benchmark your performance to ‘the market’, the more global equity you should hold to avoid being derailed by ‘tracking error regret’ when your other choices trail the market. It happens to everyone!

Next: which of the other objectives do you care about most?

• Having a steady stream of income to spend: Tilt towards global dividends.

• The chance to beat the market without taking excessive risk: Tilt towards the quality factor.

• Enjoying equity returns while curtailing your downside: Tilt towards low volatility.

You can always split your equity allocation between any combination of these choices.

Now choose your equity diversifier – for periods when all stocks are down. Diversify by

choosing a defensive non-equity ETF. Leading candidates for this role in your portfolio are:

• High-grade government bonds denominated (or hedged to) your home currency.

• Money market ETFs.

• Gold ETCs.

WHY PEOPLE LOVE THE ‘BUY AND HOLD FOREVER’ STRATEGY

With this equity portfolio, you’ll hold thousands of companies across the globe, from dominant US tech firms to stable European consumer brands and growing Asian businesses.

This mix can be held for decades, rebalanced once a year, and built on using monthly contributions.

Choose accumulation ETFs to reinvest your income for compounding or, later in life, distribution ETFs to fund ongoing expenses with your dividends.

Your non-equity, defensive allocation helps reduce risk and cushion volatility; because you’ve tailored the portfolio to achieve your goals, there’s less temptation to time the market or worry about FOMO.

Ultimately, the beauty of a buy and hold forever ETF strategy is that it embraces the power of time.

By owning broadly diversified, high-quality ETFs, and leaving them largely untouched, you avoid emotional decision-making, cut down on trading costs, and harness long-term compounding.

It’s not flashy. It doesn’t make headlines. But it works.

As the saying goes: “Time in the market beats timing the market.”

Choose wisely, keep it simple, and let your portfolio do the heavy lifting for years to come.

Published by our friends at:

RYE FINE WINES

WINE MERCHANT & BAR

Rye Fine Wines - an exclusive wine merchant & wine bar in the historic town of Rye in East Sussex, has partnered with DIY Investor to furnish readers with this exclusive offer. 10% off all wines purchased based on a case of 6 or more!

We will provide exceptional quality wines to suit all tastes and budgets, sourced from boutique vineyards from around the world, along with some of the finest sparkling wines that the UK has to offer.

Everybody needs a guilty pleasure in these unprecedented times, and you will always receive friendly service.

Please take a look at our website Rye Fine Wines and let us know which wines you like. Then all you have to do is message us at info@ryefinewines.uk or call us on 07881 502705 quoting the reference RFW/DIY/01 Remember ‘the best wine is the wine that you enjoy!’

THE LEADING JAPAN FUND

After tracking the strong recent performance of Japanese equities, Saltydog Investor has finally invested

A few weeks ago, I highlighted a couple of funds from the Japan sector that had recently come to our attention - WS Morant Wright Nippon Yield and Man GLG Japan CoreAlpha.

IAD’S CONTRARIAN APPROACH HAS LED TO STRONG PERFORMANCE OVER MULTIPLE TIME PERIODS…BY RYAN

LIGHTFOOT-AMINOFF

This trust has been awarded a rating by Kepler Trust Intelligence for income. Find out more:

We had just run our latest “6 x 6” report, where we search for funds that have gone up by more than 5% in each of the last six six-month periods. We did not find any, but these two funds had achieved the target five out of six times. Only one other fund that had done this, Invesco Global Equity Income.

At the time of writing, the Nikkei 225 had risen above 38,000, but not yet reached the all-time high that it set in December 1989; however, since then it has pushed through 40,000 and is currently nudging 40,400.

Until recently we have not been holding any other funds from the sectors in our Full Steam Ahead Developed group, preferring the Technology & Technology Innovations and India/ India Subcontinent sectors, which are in different groups. However, a couple of weeks ago we did buy one of the Japan funds.

There are plenty to choose from, with little difference in performance between the leading funds; we invested in the M&G Japan fund.

Whilst welcome, IAD’s strong performance increased the managers’ cautiousness, leading them to rotate the Portfolio, taking profits from better performers and deploying elsewhere, whilst mitigating the overall exposure of the trust by reducing Gearing. We believe the trust could appeal to more circumspect investors, who appreciate the long-term qualities of the Asia region, but cognisant of the strong run-up there has been over the past year.

Longer-term view, its contrarian mindset continues to make the trust stand out. This has often given the trust differentiated positioning to comparators, such as being overweight China and underweight India in 2024, leading to the latest strong outperformance and, providing investors with a differentiated option in the region, particularly given the high proportion of strategies with a quality growth focus.

So far this year, it has risen by more than 21% and last year it made 28% (both in local currency), which is also better than most other stock market indices; the FTSE 100 went up by only 3.8% in 2023.

Invesco Asia Dragon (IAD) has delivered sector beating Performance over the short and long term, as managers Fiona Yang and Ian Hargreaves’ contrarian approach, generated good alpha in a rising market. Asian equities performed well on the back of a weakening US dollar, recovery in China, and country-specific factors, which Fiona and Ian were well positioned for.

US stock markets have also had a good run recently with the Dow Jones Industrial Average, S&P 500, and the Nasdaq all setting new all-time highs this year.

The managers remain contrarian and are pivoting away from some names that drove performance, such as tech and financial firms, rotating into areas they deem better value.

In our regular weekly analysis, we look at the relative performance of the Investment Association (IA) sectors and group them based on how volatile they have been in the past. The Japan and American sectors both sit in our “Full Steam Ahead Developed” group.

IAD’s Portfolio has often looked and performed differently from many comparators, and these changes continue to drive a potential diversion. As wider market valuations have risen above long-term averages, the managers have reduced Gearing to zero to mitigate risk, but the portfolio remains at a notable discount.

IAD pays an enhanced Dividend of c. 4% of NAV in four instalments, changing from a semiannual payment following the combination with the former Asia Dragon (DGN) trust in 2025. Combined assets increased substantially, improving liquidity of the trust’s shares and to IAD having some of the lowest Charges in the peer group.

There was not much to choose between the North American and Japanese sectors over the past four weeks; the combined North America and North American Smaller Companies sector rose by 4.38% and the Japan sector by 4.37%. Over 12 and 26 weeks, the US funds are slightly ahead, but in the past couple of weeks the Japanese funds had the edge.

ANALYST’S

VIEW

We invested in the UBS US Growth fund, from the North America sector, last June and have been happy with its progress, up over 24%.

Asian equities have undergone a strong near-term, defying challenges faced by the region in the past year, contributing to strong returns for IAD (see Performance), delivering outperformance thanks to the managers’ contrarian approach, and well placed to capture turning points in markets.

Like most funds, it fell in early 2020 as markets reacted to the spreading Covid-19 virus. However, by the end of the year it had recovered and continued to grow through 2021.

It then remained relatively flat during 2022, but rose by 14% last year, and has already gone up by 9% this year.

When considering Dividend picture, IAD is not alone in paying an enhanced income, the underlying fundamentals, such as above-market yield and free cash flow, mean it has a different profile to other income trusts, as well as the growth-focussed mandates we believe are a fairer comparison, so the trust could appeal to both income and growth investors in our view, and provide a compelling choice for either.

BULL

For more information about Saltydog, or to take the two-month free trial, go to www.saltydoginvestor.com

• Numerous periods of strong performance, driven by stock selection alpha.

• Contrarian mindset offers a differentiated approach and portfolio.

• Increased asset base has led to a highly competitive charging structure.

BEAR

Strategy can struggle in momentum-led markets.

Strong share price performance has led to discount narrowing considerably more than most peers Managers note that market, on their preferred valuation metrics, is above long-term averages.

SEE THE LATEST RESEARCH ON IAD HERE >

MAKE SURE YOU DON’T MISS AN ISSUE; CLICK HERE TO RECEIVE DIY INVESTOR MAGAZINE TO YOUR INBOX

Disclaimer : Disclosure – Non-Independent Marketing Communication. This is a non-independent marketing communication commissioned by Invesco Asia Dragon (IAD). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

THE SOFTWARE SELLOFF IS INVESTORS’ REAL‑TIME REPRICING OF THE SECTOR IN THE AI AGE, ASSERTS THE CEO OF ONE OF THE WORLD’S LARGEST INDEPENDENT FINANCIAL ADVISORY ORGANIZATIONS.

The stark analysis from Nigel Green of deVere Group comes as a new AI automation tool from Anthropic sparked a $285 billion plunge in big-name stocks across the software sector.

He says: “The selloff is not about fear of AI — it’s about what software businesses can realistically charge in an AI-first world.

“When AI agents can perform legal review, data analysis, research and compliance instantly, subscription-heavy models lose pricing leverage.

“Investors are reassessing whether decades-old assumptions around recurring revenues still hold.

“The sharp falls in software stocks reflect a market recognizing that margins, not innovation, are now the battleground.”

The scale and speed of the declines underline how abruptly investor thinking has shifted.

Software companies long valued for predictable subscription income, entrenched workflows and information advantages are now being judged against a different standard: how defensible those revenues remain when AI can replicate outputs faster, cheaper and with minimal friction.

Markets are increasingly questioning whether software businesses built around information resale, process automation or labour substitution retain meaningful scarcity value.

Tasks that once justified premium pricing and long-term contracts are being compressed by AI systems that can deliver comparable results in seconds.

As a result, the traditional logic underpinning software valuations is coming under sustained pressure.

Nigel Green notes that this represents a fundamental change in how investors assess technology risk. The assumption that digital products naturally enjoy durable pricing power is being challenged as automation strips complexity out of workflows.

“It is a valuation reset driven by economics. AI forces investors to examine what customers are actually paying for, and whether those services remain differentiated when intelligent systems become widely available.”

He continues: “Markets are drawing a clear distinction between companies that genuinelycontrol AI economics and those that simply integrate AI to protect existing businesses.

“The former can potentially expand margins, while the latter risk seeing cost savings passed directly to clients.

“Markets are, it seems, penalizing firms that rely on legacy platforms, high headcount or process-heavy models that can be bypassed entirely.”

Another factor weighing on valuations is the rapid erosion of switching costs. As AI systems improve, the friction that once locked customers into long-term software contracts weakens.

Outputs become more standardised, competition intensifies and customer loyalty becomes harder to monetize.

Nigel Greens adds that the selloff reflects a growing recognition that “AI compresses value chains and concentrates returns.” A small number of firms, he explains, will “capture disproportionate gains, while a far larger group will struggle to defend pricing power.”

He concludes: “AI removes the insulation that once protected software margins. “What looked like stable, recurring revenue is increasingly exposed.

“Investors aren’t waiting for earnings warnings or guidance cues. They’re repricing now, because AI accelerates disruption faster than quarterly results can capture.”

LEADING THE DIY

Denied access to advice by RDR, or unwilling to pay for something that was previously free, millions of people now take full or partial control of their finances.

Whether seeking to get on the property ladder, planning for tuition fees or taking advantage of new pension freedoms, more than ever are setting their objectives, and building a portfolio of investments that allows them to achieve their goals whilst comfortable with the level of risk their money is exposed to.

Education is the key and technology the enabler - DIY Investor delivers information to existing investors and education to those new to savings and investment; share experience and learn to make informed investment decisions.

NOBODY CARES MORE ABOUT YOUR MONEY THAN YOU

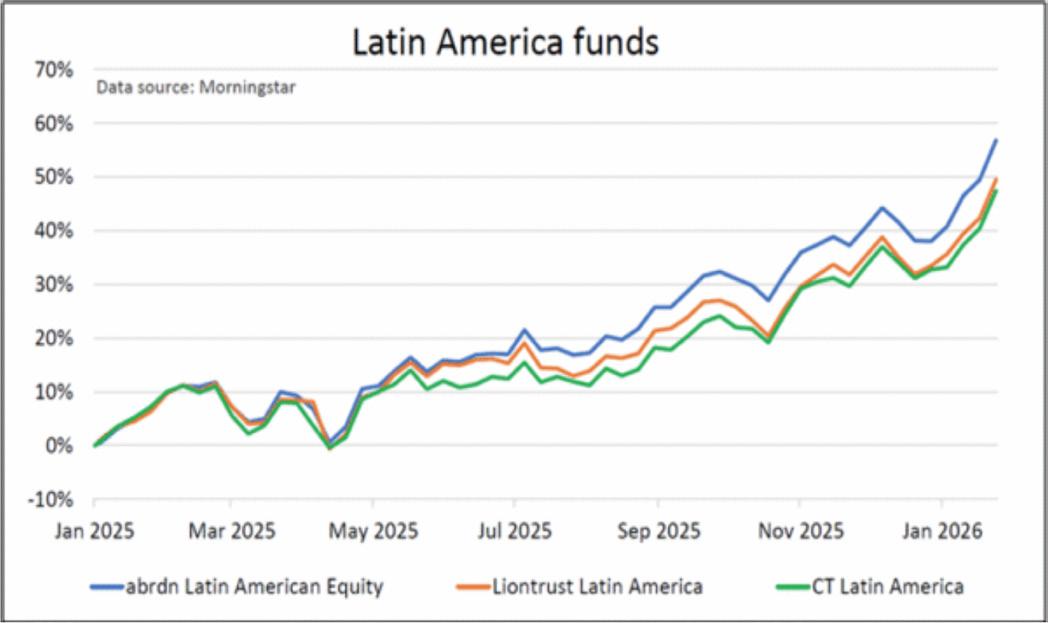

WHY LATIN AMERICA FUNDS ARE

SALTYDOG INVESTOR REFLECTS ON THE RESURGENCE OF A NICHE MARKET

Brazil’s stock market index, the Ibovespa, rose by 8.5% last week, taking its month-to-date gain to 11% and extending the momentum built up over the course of last year.

After a difficult 2024, when it fell by 10%, the Brazilian market recovered strongly in 2025.

Global interest rates had started to ease and investors were turning back towards emerging markets in search of higher returns. The index ended the year up 34%.

Overseas investors would have seen even larger gains as Brazil’s currency, the real, strengthened against the US dollar and, to a lesser extent, against the pound and the euro.

That recovery was reflected more broadly in our sector analysis. The Latin America sector was the best-performing Investment Association sector in 2025, with an average return of 38.9%.

INDIVIDUAL MARKETS

Most of the major markets in the region enjoyed a strong year.

Brazil is the largest economy and accounts for around 60% of the MSCI Emerging Markets Latin America index.

Mexicohas the next largest weighting, and its main stock market index, the IPC, also rose by around 30% in 2025. Stock markets in Chile, Peru, and Colombia did even better.

The Latin America sector is one of the newer Investment Association groupings. It was introduced in 2021 as part of a broader restructuring of the Global and Specialist equity sectors and is reserved for funds that invest at least 80% of their assets in Latin American companies.

Latin America itself is made up of more than 30 countries. These include around a dozen in South America, such as Brazil, Argentina, Colombia, Peru, Venezuela, and Chile; seven in Central America, (Mexico, Guatemala, Honduras, El Salvador, Nicaragua, Costa Rica and Panama) and a number of Caribbean nations, such as Cuba, Haiti, the Dominican Republic, and Jamaica.

THE FUNDS

We only track a small number of funds in the Latin America sector, abrdn Latin American Equity A Acc (B41QSW2), Liontrust Latin America C Acc GBP (B909HH5) and CT Latin America Z Acc GBP (B8BQ6V5). These tend to be heavily weighted towards Brazil and Mexico, with some additional exposure to the United States.

Given President Trump’s early tariff actions against Mexico, his tough stance on illegal migration, and his use of tariff threats as leverage over border security and drug trafficking, it would have been reasonable to expect the region to struggle.

The introduction of a universal 10% tariff on ‘Liberation Day’, alongside higher reciprocal rates, increased short-term volatility. However, swift bilateral negotiations secured exemptions for key exports, including agriculture, energy, and metals, which helped to restore investor confidence.

Mexico’s market benefited as nearshoring accelerated, boosting financial and industrial stocks as manufacturers shifted production away from tariff-affected parts of Asia to take advantage of the United States–Mexico–Canada Agreement. Brazil, Chile, and Peru also benefited from rising commodity prices, while Brazil had the added tailwind of a 14% appreciation in the real against the US dollar.

This year has started well. Commodity prices, currency strength, and more favourable tariff terms could continue to support the region in the short term. However, US policy remains unpredictable, and there are signs that the commodity cycle may be moving into a later phase.

For more information about Saltydog, or to take the two-month free trial, go to www.saltydoginvestor.com

SPRING IS JUST AROUND THE CORNER; HERE ARE SOME SIMPLE TIPS TO PERK UP YOUR FINANCES – BY CHRISTIAN LEEMING OF DIY INVESTOR

START WITH A BUDGET

As the cost of living continues to rise, start with your own Spring Budget. Take a fresh look at what’s coming and going and see where you might make savings.

You may find direct debits or standing orders that you no longer use and be able to reduce your outgoings.

But don’t make it all stick. Set yourself budgets for the things you enjoy in life too – whether that’s dining out, clothes or holidays – to help you stay motivated.

Budgeting could help you avoid any nasty surprises and identify any potential surplus should things get even tougher.

KEEP CALM AND CARRY ON SAVING

Regardless of where you are in your life journey, regular saving and investing is key to being able to live the life you want to in the future.

Even if you aren’t saving with a specific purpose in mind, having a nest egg is never a bad thing.

Putting a little extra away each month can soon stack up, and a Stocks and Shares ISA will protect your pot from that lady at No 11 Downing Street.

FUTURE-PROOF YOUR FINANCES

Paying down debt and building a rainy-day fund are key to financial security, and to your peace of mind.

Put together a plan to clear your liabilities and then build a fund of between 3 to 12 months

expenditure to give yourself some breathing space in the event of an emergency.

Think about protecting yourself and your loved ones in the future with life insurance or income protection.

The UK has low levels of protection compared to other major economies, but it could help you survive any nasty

shocks, such as being unable to work due to accident, or sickness.

BUFF UP YOUR CREDIT SCORE

To improve your credit score, make sure you meet your monthly commitments on debt or payment plans such as mortgage payments, credit cards, or phone contracts.

Pay off your credit card monthly and keep usage low as a percentage of your available credit.

Make sure your personal audit history is clear and that everything is registered to the address at which you are registered for electoral purposes.

Identify what debt you have, what rate of interest you are paying, and when it will become due.

Then pay down those with the highest interest rates, or late payment penalties.

Always pay down debt before you start investing if the interest rate is higher than the expected return on your savings.

Consider consolidating your debt. A single loan at possibly a lower interest rate makes your target of repaying clearer.

Finally, don’t be afraid to seek help – there is government assistance available to help those in debt work their way out.

Once you’re back in control, with a spring in your step, head over to DIY Investor.net to plan your journey to financial freedom.