This section describes how the 2025-35 Financial Plan links to the achievement of the 2021-41 Community Vision, 2025-29 Council Plan and Municipal Public Health and Wellbeing Plan, and 2025-35 Asset Plan.

The Financial Plan is part of a suite of strategic documents required under the Local Government Act 2020. It is guided by the four-year Council Plan and 20-year Community Vision and aligns with other key plans such as the 10-year Asset Plan. These plans outline the financial and non-financial resources, along with the technical elements required for managing assets to achieve the objectives set out in the Council Plan.

As these plans are developed together, council carries out a deliberative community engagement process to collectively inform them all. The outcomes of that engagement have directly shaped the priorities set out in this plan. You can review the outcomes of the community engagement process on our website here https://www.ngshire.vic.gov.au/Council/Vision-and-Goals/2025-2029-Community-Engagement/Review-theCommunity-Engagement-Report.

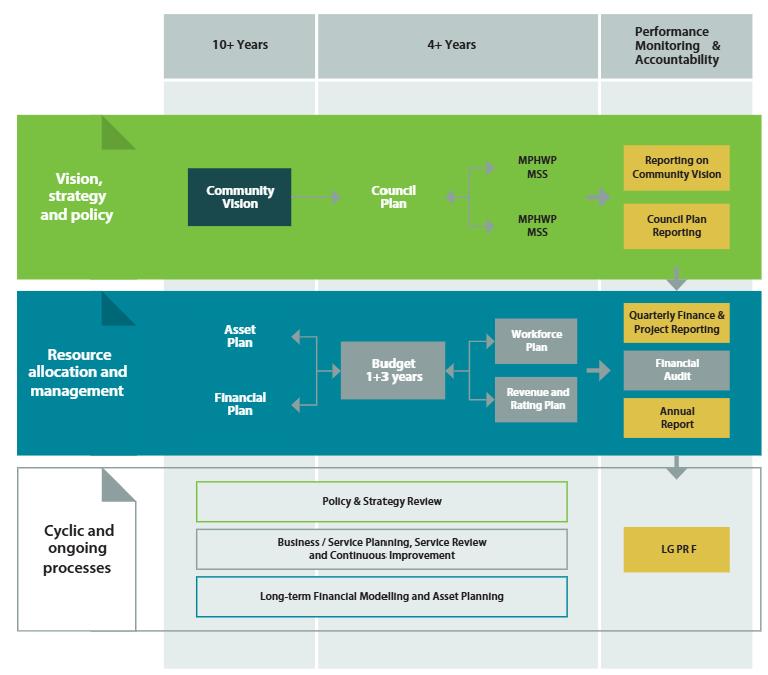

The diagram below depicts the integrated strategic planning and reporting framework that applies to local government in Victoria. At each stage of the integrated strategic planning and reporting framework there are opportunities for community and stakeholder input. This is important to ensure transparency and accountability for both residents and ratepayers. The timing of each component of the integrated strategic planning and reporting framework is critical to the successful achievement of the planned outcomes.

The Financial Plan provides a 10-year financially sustainable projection regarding how the actions defined in the four-year Council Plan can be funded to achieve the Community Vision.

The Financial Plan is developed in the context of the following strategic planning principles:

a) Council has an integrated approach to planning, monitoring and performance reporting.

b) The Financial Plan addresses the Community Vision by funding the aspirations of the Council Plan. The Council Plan aspirations and actions are formulated in the context of the Community Vision.

c) The Financial Plan statements articulate the 10-year financial resources necessary to implement the goals and aspirations of the Council Plan to achieve the Community Vision.

d) Council's strategic planning principles identify and address the risks to effective implementation of the Financial Plan. These financial risks are outlined in item b) below.

e) The Financial Plan provides for the strategic planning principles of progress monitoring and reviews to identify and adapt to changing circumstances

The Financial Plan demonstrates the following financial management principles:

a) Revenue, expenses, assets, liabilities, investments, and financial transactions are managed in accordance with council's financial policies and strategic plans.

b) Management of the following financial risks:

i. the financial viability of council (refer to section 3.1 Financial Policy Statements).

ii. the management of current and future liabilities of council (the estimated 10 year-liabilities are disclosed in section 4.2 Balance Sheet projections).

iii. the beneficial enterprises of council (where appropriate).

c) Financial policies and strategic plans are designed to provide financial stability and predictability to the community.

d) Council maintains accounts and records that explain its financial operations and financial position (refer section 4 Financial Plan Statements)

In the development of the previous 2021-31 Financial Plan, council hosted separate community engagement sessions purely for feedback needed on that plan which yielded very little interest.

As part of the engagement process this time around, we incorporated financial management sections into the broader engagement process for the 2025-29 Council Plan and Municipal Public Health and Wellbeing Plan. This is also the same approach taken for the Asset Plan, remembering that all three strategic documents inform one another.

The feedback we garnered for all plans greatly improved from this collaborative engagement approach as we were able to facilitate integrated conversations across council’s different resourcing streams, from both a financial and non-financial standpoint.

To make participation accessible we used a mix of engagement tools and channels, including:

• Community and youth surveys (both digital and paper-based);

• Pop-up in-person listening posts;

• In-person community discussion forums; and

• Stakeholder workshops.

Over 17,000 people viewed our social media posts, 60,000 people saw our newspaper features, 2,800 people visited our Council Plan website hub, 33,000 people heard our radio ads, over 950 emails were sent out, and 1,600 printed flyers were distributed. This publicity resulted in over 1,100 people participating in surveys, listening posts and workshops across the shire.

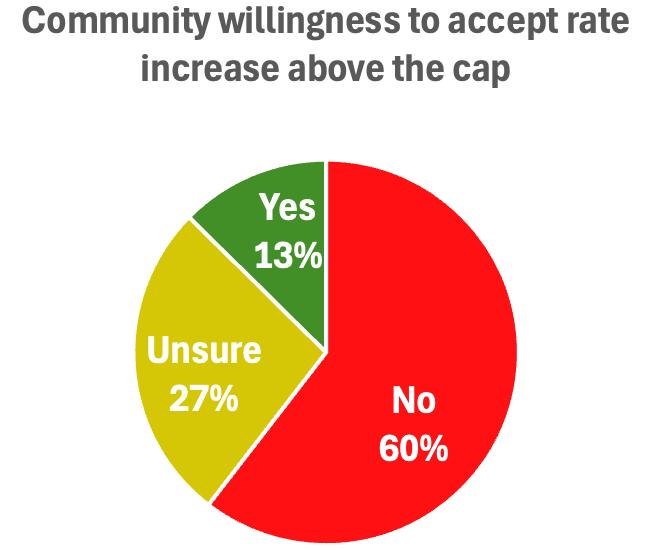

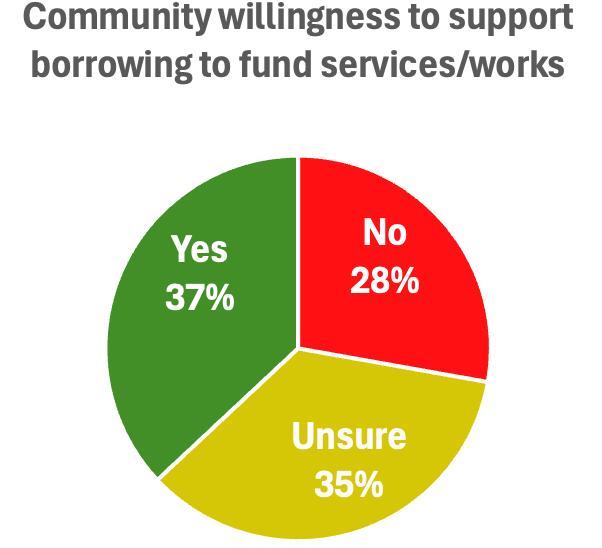

There were two poignant financial management questions included in the community survey but also discussed at the listening posts and in the community discussion forums. Of the 349 responses we received to these questions, the following insights were obtained.

If you answered YES to a rate cap increase, what services or construction projects would you like to see funded.

If you answered NO to a rate cap increase, please indicate where you feel cuts could be made to community services, infrastructure or construction works.

Council services are designed to fulfill community needs and provide value for money.

The service performance principles are listed below:

a) Services are provided in an equitable manner and are responsive to the diverse needs of the community. The Council Plan is designed to identify key services and projects to be delivered to the community. The Financial Plan provides the mechanism to demonstrate how the service aspirations within the Council Plan may be funded.

b) Services are accessible to the relevant users within the community.

c) Council provides quality services that provide value for money to the community. The Local Government Performance Reporting Framework (LGPRF) is designed to communicate council’s performance regarding the provision of quality and efficient services.

d) Council is developing a performance monitoring framework to continuously improve its service delivery standards.

e) Council is developing a service delivery framework that considers and responds to community feedback and complaints regarding service provision.

Integration to council’s 10-year Asset Plan is a key principle of council’s strategic financial planning principles.

The purpose of this integration is designed to ensure that future funding is allocated in a manner that supports service delivery in terms of the planning and the effective management of council’s assets into the future.

The Asset Plan identifies the operational and strategic practices which will ensure council manages assets across their life cycle in a financially viable manner. The plan, along with associated asset management policies, provide council with a sound base to understand the risks associated with managing its assets for the community’s benefit.

The Asset Plan is designed to inform the 10-year Financial Plan by identifying the amount of capital renewal, backlog and maintenance funding that is required over the life of each asset category. The level of funding will incorporate knowledge of asset condition and risk assessment issues, as well as the impact of reviewing and setting intervention and service levels for each asset class.

In addition to identifying the operational and strategic practices, the Asset Plan quantifies the asset portfolio and the financial implications of those practices. Together, the 10-year Financial Plan and 10-year Asset Plan seek to balance projected investment requirements against projected budgets.

The Financial Plan reports what council is projecting to spend over the course of the next ten years to continue to deliver community services, maintain and renew existing assets, as well as build new infrastructure.

Every dollar spent over the next ten years will need to be matched by an equivalent income source Sourcing sufficient income to fund projected expenditure is important to demonstrate the Financial Plan is viable over the ten-year period. Not surprising, there is more demand for expenditure than there are available sources of income, therefore prioritising the demand for expenditure within the limited income streams becomes vitally important.

Local Government has three major income streams that are available to fund ongoing service delivery. The three key income streams are:

• Rates and Charges and PiLoR – income from the ratepayers and Payment in Lieu of Rates

• Government Grants – income from Commonwealth and State Government.

• User Fees, Rentals and Fines – income from service users and the community.

While there are several additional income streams, these are either once-off or less reliable in nature and generally designed to fund once-off expenditure projects rather than ongoing service delivery.

A key objective for council is to deliver each service in the most cost-effective way while noting there are certain services and functions every council is required by law to fund.

This means one of the biggest challenges for local government such as Northern Grampians Shire Council, is to remain as efficient as possible while having to perform statutory functions and deliver required services that absorb part of the limited income we have available, resulting in a funding shortfall to support increasing community demand for new and alternative services and new community infrastructure.

While part of council’s role is to look for savings and efficiencies across all its functions and services, expenditure continues to be a significant challenge that often requires a series of compromises and prioritisation of the limited income streams we have available.

Council currently spends over $32 million to deliver more than 60 different services and functions which includes a number of legislative activities required by local government. We also manage over $680 million worth of community assets consisting of roads, drains, footpaths, buildings, sporting facilities, recreation reserves and streetscapes.

Council would need to spend over $15 million each year just to adequately maintain or replace these community assets. Due to income constraints, we are only able to fund in the order of $5 million each year, falling well below the targeted spend required. Council’s total capital works also spend in the order of $12 million each year to renew, upgrade and construct new infrastructure which includes this $5 million of renewal works.

By sharing these challenges with the community, council is arming residents with the information needed to make informed decisions about how we prioritise our limited funding streams in the future. Our community’s engagement and feedback is critical to this process and ensures we are funding the facilities, services and initiatives our people want available.

In 2020, the Victorian State Government passed a new Local Government Act that highlighted council’s role in making decisions that will achieve the best outcomes for the community, including future generations, informed by community consultation. The new legislation sets out the following principles:

• Services should be provided in a fair manner and be responsive to the diverse needs of the municipal community;

• Services should be accessible to members of the community for whom the services are intended;

• Quality and cost standards for services set by council should provide good value to the community;

• Council should seek to continuously improve service delivery to the community in response to performance monitoring; and

• Service delivery must include a fair and effective process for considering and responding to complaints about service provision

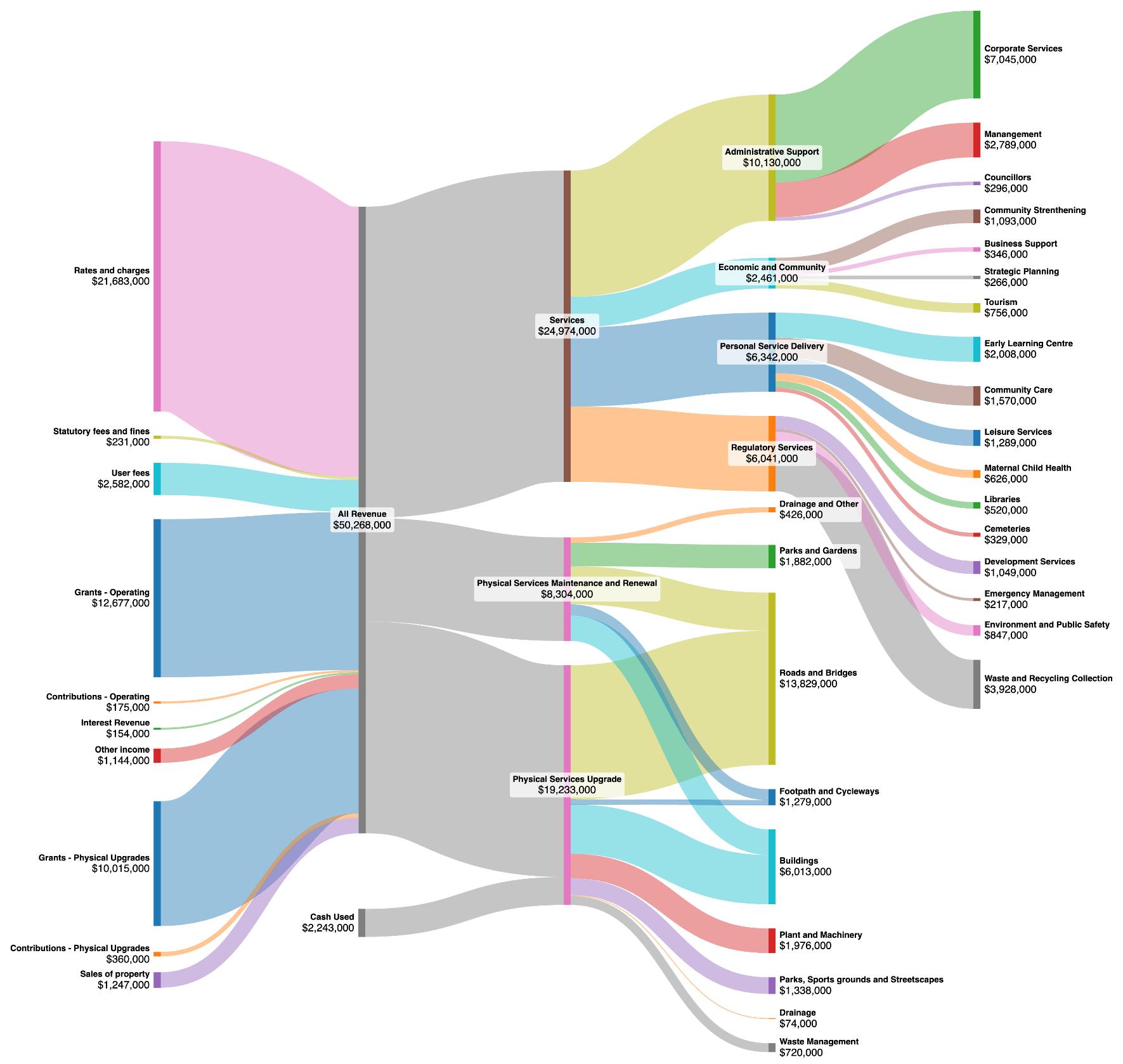

In the 2025/26 Budget, the income received by council is budgeted to be $50 million. The main source of this income comes from general rates and charges, representing 44 per cent of this figure.

Council also receives grants from State and Federal Governments that either fully or partially fund a range of community services and programs including aged care support, maternal and child health and our early learning services.

Some services are provided via a full cost recovery model which require council to charge user fees to the community as a compromise for allocating ratepayer funds. While the objective is to maximise the allocation we receive from government grants, many community services also require funding support from rates subsidy and/or user fee income to facilitate their delivery.

An example of this would be council’s servicing of the Stawell Sports and Aquatic Centre and the St Arnaud Early Learning Centre. Whilst there are membership options and user fees associated with both facilities which generate income each year, council still support their operational functions in the community with other funding support.

Where possible, council seeks external funding support for each service, usually in the form of a government grant and/or the levy of user fees and charges, however these income sources are generally insufficient to fully offset the service expenditure resulting in a net cost to council. This net cost to council is funded by a combination of:

• Rates and PiLoR – $18 million income per annum

• Financial Assistance Grants – $10 million received each year that is unallocated to one specific service or project meaning council decided where and how it is invested.

Council has a responsibility to deliver a Financial Plan that is designed to fund the necessary services and functions of council, as well as facilitate the replacement and construction of new community assets such as parks, roads and footpaths.

The balancing exercise is therefore to prioritise, in a financially viable and sustainable manner, the demands of current and future community desires including:

• Increasing expectations of a growing community and the need for new and upgraded services;

• The number, scope, and standard of services that council directly delivers;

• New infrastructure facilities at the expense of increased renewal funding; and

• The community appetite to accept an increase in rates (above the rate cap) and/or increases to user fees as a source of additional funding to achieve these objectives.

You can view all of council’s income and expenditure streams in our Annual Budget which are available on our website here https://www.ngshire.vic.gov.au/Council/Governance-and-transparency/Council-

publications/Budget You can also view an income and expenditure summary for our 2025/26 budget on the following page.

Financial viability refers to council’s ability to meet its short to medium-term financial obligations, including maintaining adequate cash flow and solvency.

In contrast, financial sustainability focuses on the long-term capacity to fund services and infrastructure without compromising the needs of future generations.

Due to limited control over council’s key revenue sources, financial sustainability is not guaranteed, however council remains committed to monitoring and maintaining efficient practices in both expenditure and revenue generation to support the delivery of essential services to the community.

Northern Grampians Shire Council is recognised as one of Victoria’s financially unsustainable councils, identified in a 2012 report commissioned by Rural Council Victoria Council’s position has not improved since then and is unfortunately becoming more of a concern.

It’s important to note this status does not reflect poor financial or asset management practices, but rather structural challenges. With a small ratepayer base and a large geographic area containing significant infrastructure needs, council faces ongoing difficulty in funding the assets and services required by the community. Despite these challenges, our team continues to work diligently to balance community needs and expectations, ensuring financial viability while striving toward long-term sustainability

One of the challenges for local government is identifying funding sources that can then be used to increase spending to expand and scale-up our services.

These funding sources would generally need to derive from either:

• A reduction or removal of an existing service; and/or

• Increasing income from user fees by adopting a user pays principle; and/or

• A rate increase in excess of the rate cap noting the rates cap increase is already applied to fund the increased cost of existing services; and/or

• Efficiencies from existing services and functions noting that, while council strives for continuous improvement, this is a short-term solution due to the impact of diminishing returns from regular service reviews.

In prioritising service expenditure, council also needs to consider the extent it wishes to recover the expenditure by increasing the charge for user fees. There are two principles that could apply, including:

• Full cost recovery model – maximise fees to eliminate any rates subsidy; or

• Partial cost recovery model – provide a subsidy to the user (i.e. 50% user fee) where the subsidised amount would need to be funded from an increase in rates subsidy.

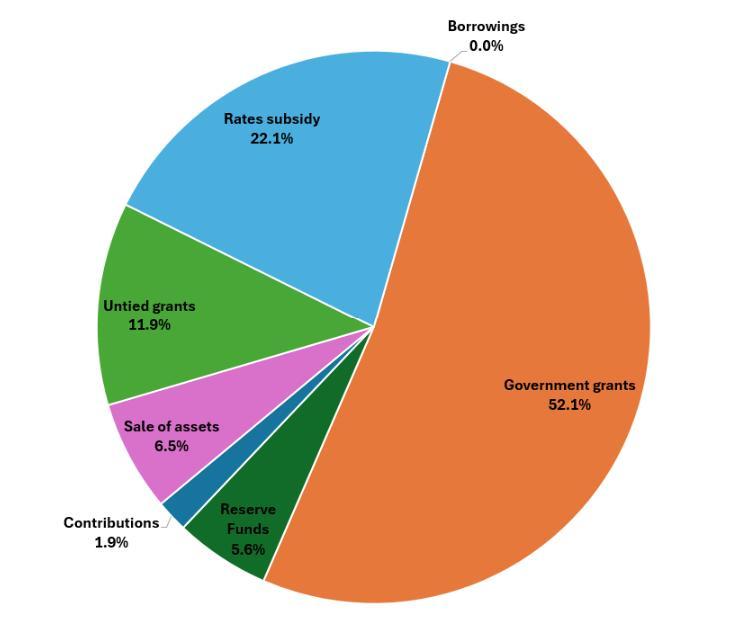

Whilst council is heavily reliant on government grants to fund its capital works program, for both renewal works and new and improved projects, there are also other sources that fund the program.

Council’s capital budget is funded from a mix of:

• Rates subsidy – funding allocation from council rates.

• Untied grants – funding allocation from Federation Assistance Grants

• Government grants – federal and state funding allocation to specific capital projects

• Contributions – external funding from a third-party excluding government (i.e. sporting club)

• Reserve funds – funding allocation from cash reserve funds

• Borrowings – funding from loan borrowings.

The majority of council’s capital (86% of it) is funded from either rates subsidy, untied grants or government grants as displayed in the graphic below (source: 2025/26 Annual Budget).

In principle, funding from the operating surplus (rates subsidy and untied grants) is limited by the extensive range of services that require these streams to fund their net cost to council.

To redirect additional rates subsidy and untied grants to capital, council would need to either:

• Increase rates income by a variation to the state government rate cap; and/or

• Remove or reduce a service; and/or

• Continue to review efficiencies across council services

Alternatives to grant funding and rates subsidy include:

• Loan borrowing, noting that council’s loan capacity is limited to 60% of total rates or approximately $12.95 million based on the current loan portfolio (as a general guide); and/or

• Once-off funding from reserve funds, noting that some reserves are restricted to specific types of capital projects and would therefore need to be assessed on a case-by-case basis.

This section of the plan describes the context, external and internal environment, and considerations in determining the 10-year financial projections and assumptions.

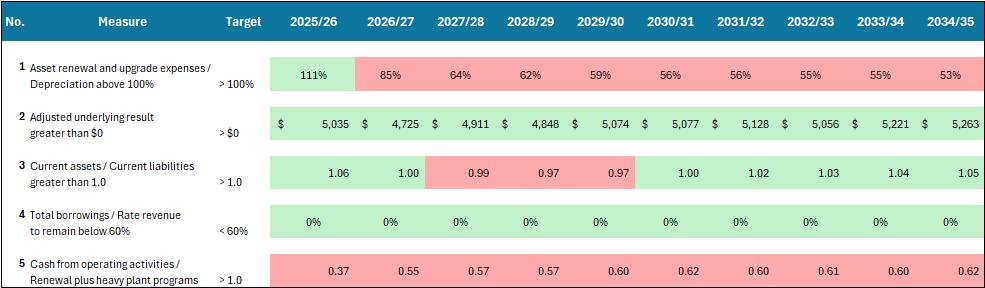

Here, we define the policy statements and associated measures which demonstrate council's financial viability to fund the aspirations of the Community Vision and the Council Plan.

The financial policy statements address the following areas:

1. Allocation of adequate funds towards renewal capital to replace assets and infrastructure as they reach the end of their service life.

2. The current underlying deficit with a view to achieving an underlying surplus result.

3. Ensuring council maintains sufficient working capital to meet its debt obligations as they fall due.

4. Ensuring council applies loan funding to new capital and maintains total borrowings in line with rate income and growth of the municipality.

5. Ensuring council generates sufficient cash surplus from operations to fund the renewal Infrastructure Program and replacement of Heavy Plant

Council acknowledges the continued challenge in meeting long-term financial sustainability targets. As outlined in Statements One and Five, key financial indicators reaffirm the concern that Council is not currently operating within a financially sustainable framework. These metrics underscore council’s limited capacity to fund the ongoing renewal and maintenance of community assets over the long-term.

While council retains the ability to borrow, both community sentiment and recognised best-practice financial management principles advise against using debt to finance recurrent operational expenditure.

Such an approach would not address the fundamental issues underlying council’s financial sustainability.

Encouragingly, our adjusted underlying result demonstrates that routine operational activities are adequately funded. However, notwithstanding this operational stability, we continue to face significant challenges in securing long-term financial resources for asset renewal. This shortfall represents a material risk to council's compliance with legislated responsibilities, and addressing it remains a strategic priority

Council has identified the following strategic actions that will support the aspirations of the Council Plan.

These strategic actions are included in the 10-year Financial Plan and, where appropriate, referenced in the commentary associated with the 10-year Comprehensive Income Statement and the 10-year Statement of Capital Works.

In an ideal world, council would aim to allocate adequate funds towards asset renewal to replace assets and infrastructure as they reach the end of their service life. However, council currently has insufficient funding to allocate to asset renewal to reduce the escalating risk and maintenance of aging infrastructure.

Council allocates $5 million annually towards its replacement infrastructure program that comprises of assets such as roads, bridges, drains and footpaths.

The infrastructure renewal program for the 2025/26 financial year is funded by $4.3 million (or 64%) from external competitive grant funding and the remaining $2.4 million from rates subsidy and untied grants The forward projections are more conservative with the average competitive grants portion of the infrastructure renewal program falling to 61% for 2026/27 to 2034/35 periods, with the remaining 39% being allocated from rates subsidy and untied grants.

In contrast, council’s annual depreciation is approaching a total of $16.6 million, of which $13 million accounts for infrastructure program assets such as those referenced above.

Ideally the investment in asset renewal (i.e. council’s infrastructure program) should be targeted to either match or provide a significant contribution towards the level of depreciation. The current $5 million allocation is considered inadequate to address the $13 million annual depreciation expense.

• Strategic action 1 – review operating expenditure and revenue streams with the objective of optimising the operating surplus. This surplus will be directed toward the sustainable funding of capital projects and asset renewal initiatives.

• Strategic action 2 – conduct a systematic review of asset service levels to identify opportunities for rationalisation. The objective is to reduce capital renewal requirements, thereby narrowing the gap between available funding and long-term asset renewal needs.

The Financial Policy Statement reports an average underlying deficit in excess of $7 million for the duration of this 10-year plan.

While it may not be feasible to eliminate this deficit in the short term, for long term financial sustainability it is important that council works towards reducing the underlying deficit. Ideally, the underlying would reflect a breakeven or hopefully a surplus result, however this position is not realistic based on current expenditure needs and revenue constraints.

The underling deficit also reinforces council’s inability to fund its infrastructure renewal needs as discussed at 3.2.1 Infrastructure Renewal.

• Strategic action 1 (as above) – review operating expenditure and revenue streams with the objective of optimising the operating surplus. This surplus will be directed toward the sustainable funding of capital projects and asset renewal initiatives.

• Strategic action 3 - where appropriate, actively advocate for reduced co-contribution requirements associated with external grant funding. This approach aims to alleviate pressure on council’s own income sources and enhances the financial viability of grant-supported projects

Council currently prepares a 10-year Financial Plan and funding model to ensure that the amount of cash available for capital is equal to or greater than the net capital spend (i.e. capital required from council contribution or rates subsidy).

This measure is used to maintain sufficient working capital by ensuring the net capital spend does not exceed the amount of cash available for capital, after funding of operations and after setting aside restricted cash including council reserves.

• Strategic action 4 – maintain a focus on generating sufficient operational cash surpluses to ensure that funds available for capital investment meet or exceed net capital expenditure on an annual basis. This strategy supports the viable delivery of infrastructure and asset renewal without reliance on external financing.

Council has limited surplus from operations (i.e. rate subsidy) to apply to new capital works.

To supplement external grant funding, that is the primary revenue source for new works, additional loan borrowings are required to be included in the 10-year Financial Plan.

• Strategic action 5 – where appropriate, apply debt funding to support the delivery of new infrastructure projects, including those involving service expansion. This targeted use of borrowings ensures intergenerational equity and enables timely investment in essential assets without adversely impacting operational sustainability.

Council previously generated a surplus from waste operations which was allocated to a discretionary waste reserve on an annual basis. This was a strategic decision to fund waste program requirements in the future

To respond to the increased pressures of recycling, the 10-year Financial Plan includes operating and capital expenditure to fund a Waste Action Plan. It is expected the majority of the waste reserve will be expended over the course of the next 10 years.

• Strategic action 6 – allocate any operational surplus generated through council’s waste management activities towards implementation of the Waste Action Plan. This approach ensures that waste-related revenues are reinvested in initiatives that support environmental sustainability, service efficiency, and long-term strategic outcomes.

The following additional strategic action are included as a result of community engagement:

• Strategic action 7 - where appropriate, council will explore opportunities to increase revenue and reduce asset renewal obligations. This may include investigating alternative revenue sources and assessing surplus assets for potential sale or decommissioning. The objective is to partially offset capital investment and ongoing service delivery costs while maintaining alignment with long-term financial sustainability goals.

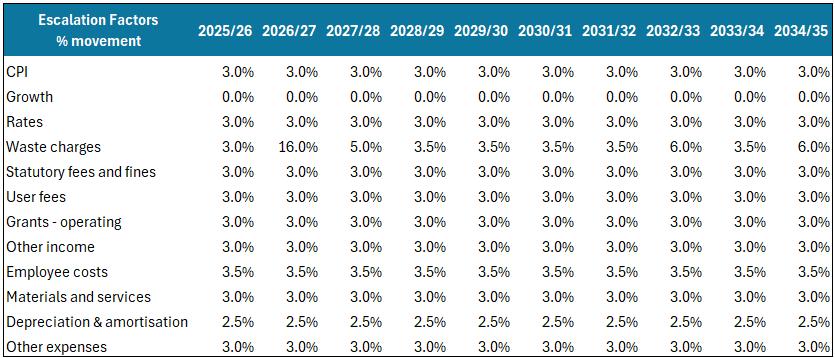

This section presents information regarding assumptions to the Comprehensive Income Statement for the 10years between 2025/26 to 2034/35. The assumptions comprise the annual escalations and/or movement for each line item of the Comprehensive Income Statement.

Base rate revenue will increase by 3% for the 2025/26 financial year based on the State Government rate cap, with estimated future annual increases of 3% per annum for the ensuing years of this long-term Financial Plan.

There is no allowance for increased revenue from growth (i.e. additional properties) because of supplementary rates.

Waste charges are proposed to increase by 3% compared to 2024/25 levels to defray the total costs of waste management incurred across the municipal district. Future years waste charges are estimated to increase in line with the Waste Action Program requirements to ensure council continues to recover the full costs of providing waste services across the shire.

Notably, there is a 16% increase expected in 2026/27 due to the introduction of FOGO and mandatory glass recycling across the shire.

Council has assumed that Payment in Lieu of Rates (PiLoR) revenues will remain broadly consistent with current levels throughout the duration of the plan, with an annual increase of 3% applied in alignment with general rate movements. Although council is aware of several proposed renewable energy developments, no assumptions regarding their commencement or contribution to PiLoR revenue have been factored into this 10-year financial outlook.

The Financial Plan indexes statutory fees, which are set by legislation, according to the estimated annual rate of CPI. This is often a best-case scenario given some fees are outside of the control by council and therefore may be subject to increases less than CPI.

Revenue increases for the ensuing years are based on a conservative annual rate of increase of 3% to reflect, as a minimum, annual increases in line with the State Government rate cap

Council currently receives grants for tied (i.e. for specific purposes and/or outcomes) and un-tied Financial Assistance Grant funding received via the Victorian Local Government Grants Commission (VLGGC). Operating grants are expected to increase on an annual basis by approximately 3%.

3.3.5

Council receives contributions from community groups, mainly for capital works funding purposes and developers.

Revenue from other income which mainly comprises of investment income, recovery income from a variety of sources, and rental income received from the hire of council facilities and buildings.

3.3.7

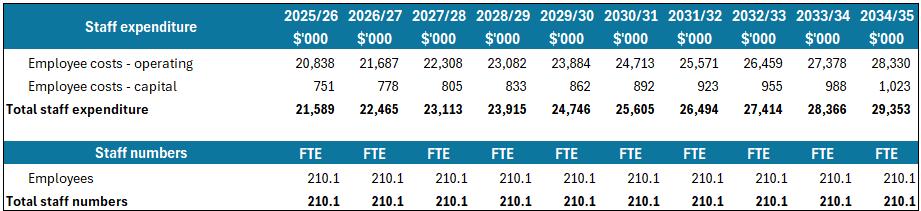

In 2025/26, employee costs are projected to increase by 3.5%, primarily reflecting salary adjustments in accordance with the Enterprise Bargaining Agreement (EBA).

This increase follows a period of lower wage growth during which staff accepted moderated adjustments in recognition of council's financial sustainability challenges.

For the period 2026/27 to 2034/35, annual increases of 3.5% have been forecast to accommodate anticipated EBA-related adjustments across council’s workforce.

3.3.8

Material costs include items required for the maintenance and repairs of council assets such as buildings, roads, drains and footpaths, which are governed by market forces based on availability more than annual CPI.

Other associated costs included under this category are utilities, materials for the supply of our meals-onwheels program, and consumable items for a range of services. Council also utilises external expertise on a range of matters, including legal services. These costs are kept to within CPI levels year on year where possible and are planned as such.

Depreciation estimates have been based on the projected capital spending contained within this document. Depreciation has been further increased by the indexing of the replacement cost of council’s fixed assets.

Borrowing costs comprise the interest expense to service council's loan portfolio that is described in Section 6.1 Borrowing Strategy.

3.3.11

Other expenses include administration costs such as councillor allowances, election costs, community grants, lease expenditure, fire services property levy, audit costs and other costs associated with the day-to-day running of council.

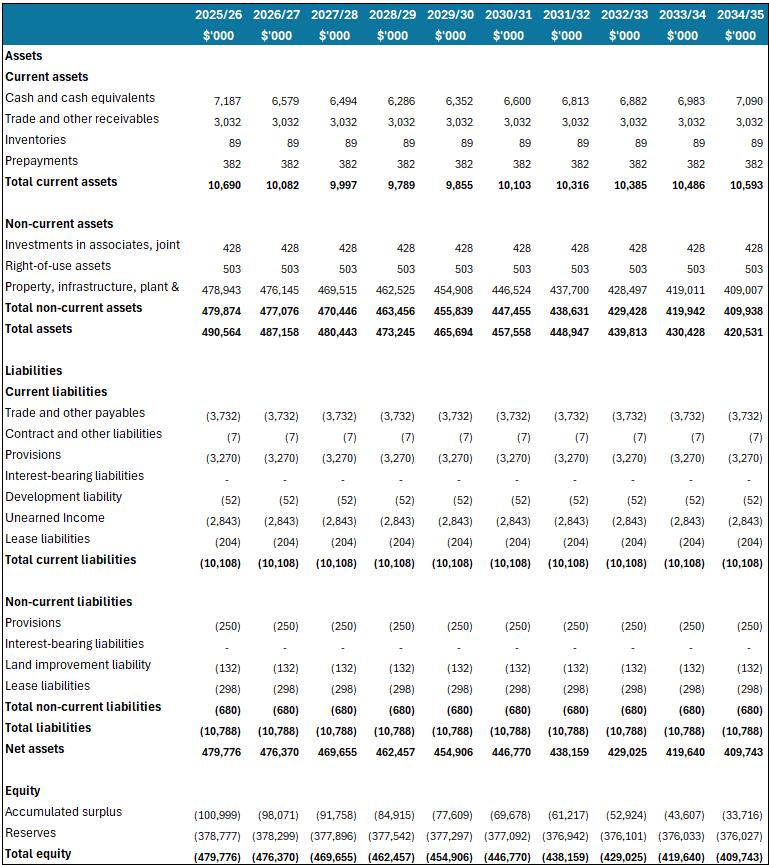

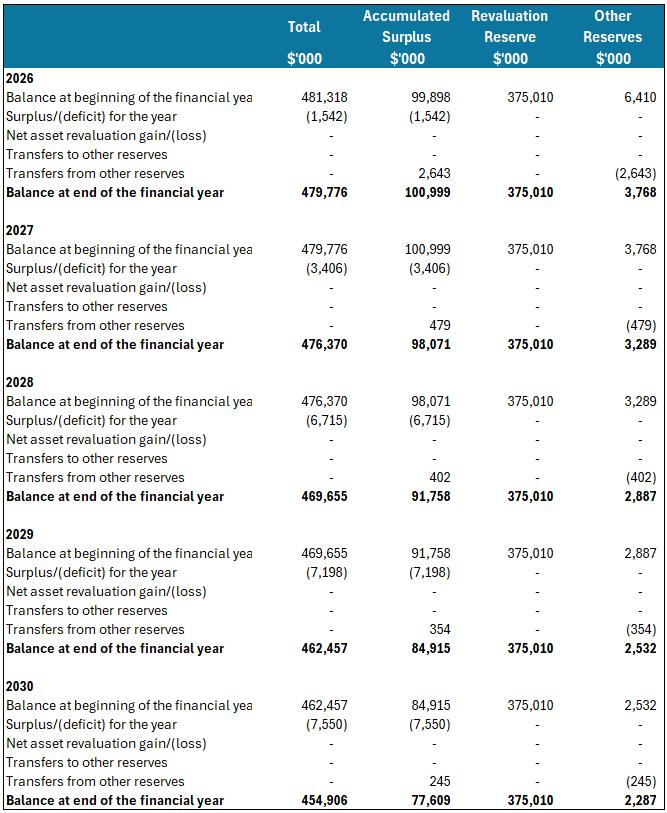

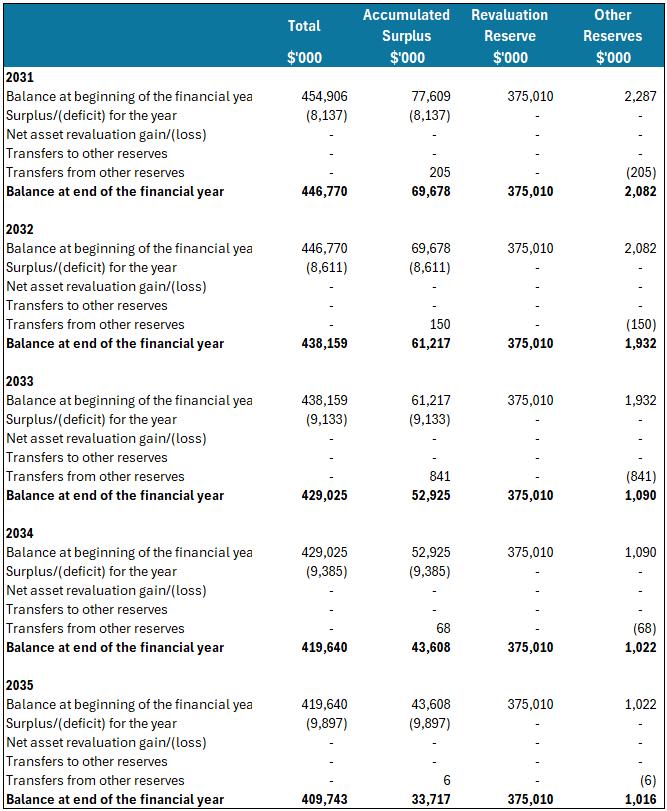

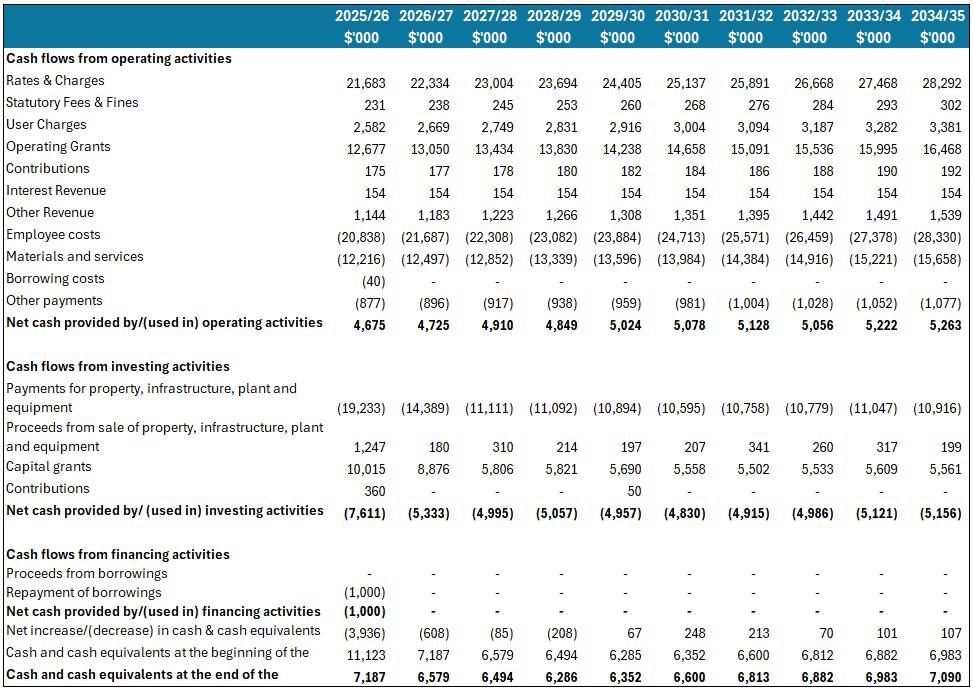

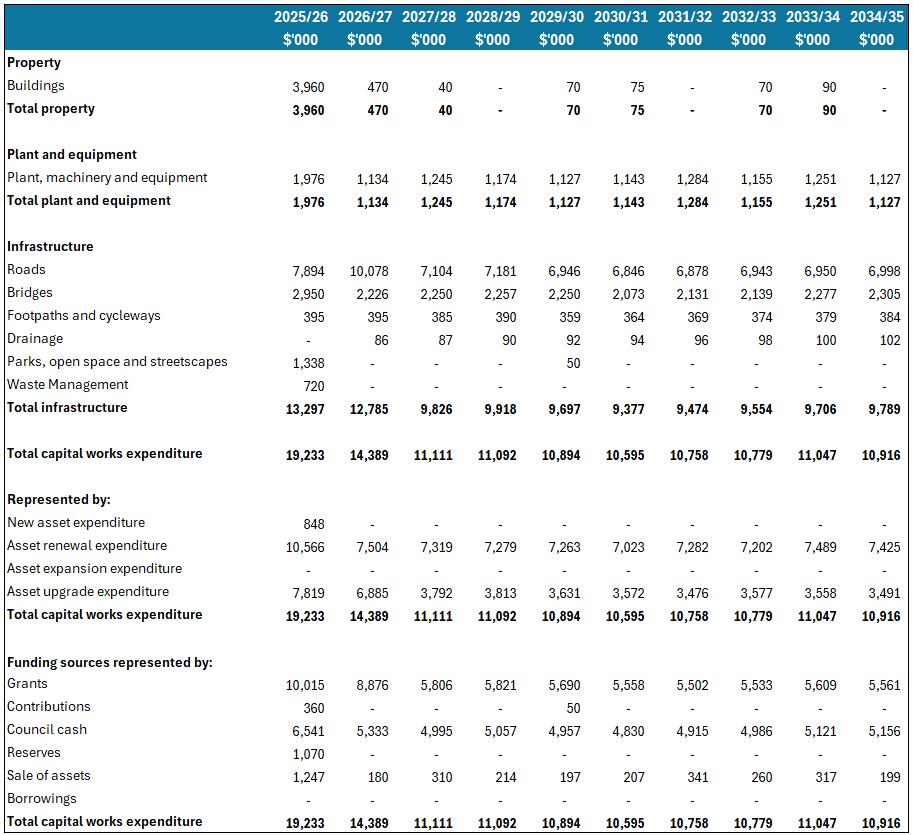

This section presents information regarding the Financial Plan Statements for the 10-years from between 2021/22 to 2030/31.

• Comprehensive Income Statement

• Balance Sheet

• Statement of Changes in Equity

• Statement of Cash Flows

• Statement of Capital Works

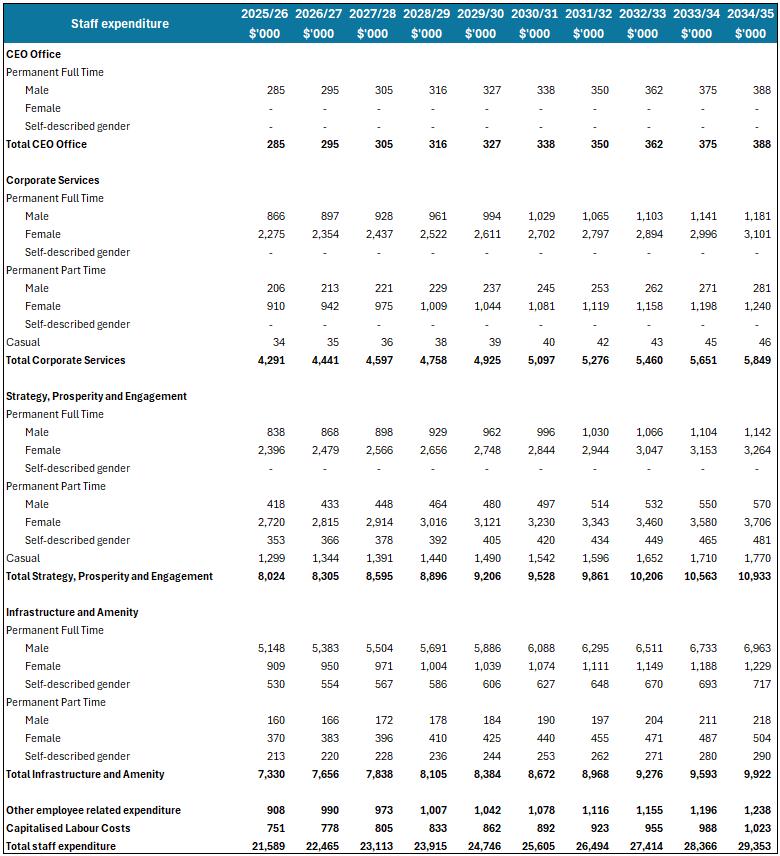

• Statement of Human Resources

Comprehensive Income Statement

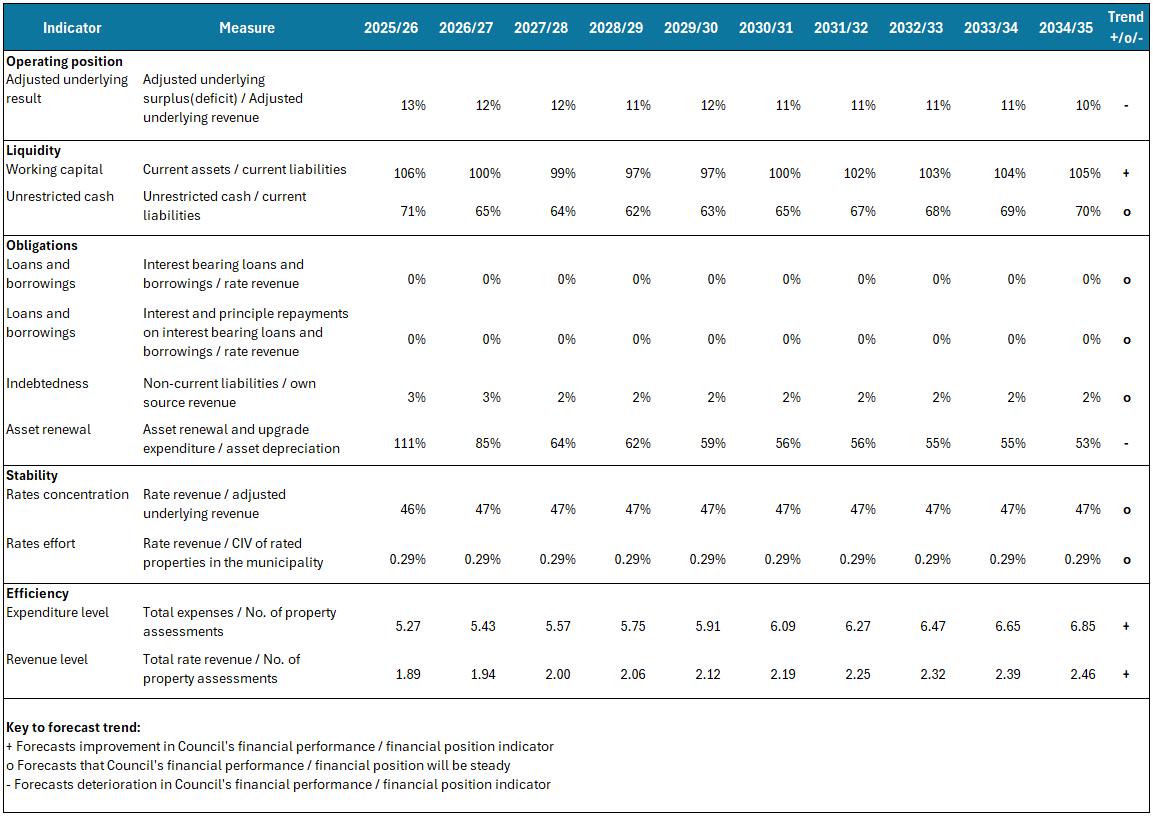

The following table highlights council’s projected performance across a range of key financial performance indicators. These indicators provide an analysis of council’s 10-year financial projections and should be interpreted in the context of the organisation’s objectives and financial management principles.

This section describes the financial strategies that support the 10-year financial projections included in this Financial Plan.

6.1.1 Current debt position

The total amount of borrowings remaining on existing loans as of June 30, 2025, is $1 million.

6.1.2 Future borrowing requirements

The following table highlights council’s projected loan balance, including any new loans and loan repayments for the 10-years of this Financial Plan.

Council hasn’t highlighted any projects it expects to fund using borrowings in the next 10-years.

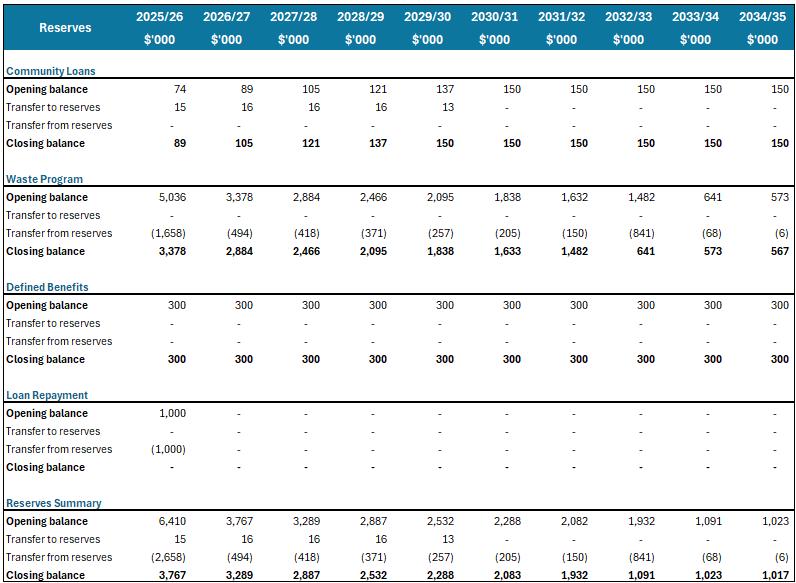

6.2.1 Current reserves

Community Loan Reserve

• Purpose – the Community Loan Reserve is for the provision of loans to community members wishing to restore and rehabilitate for the benefit of the broader community. The maximum to be held in this reserve is $150,000. The loan balance comprises of the $150,000 less the amount of loans that are currently outstanding.

• Movements – the reserve movements comprise the provision of new loans less the repayment of the outstanding loan balance owed by community members to council.

Waste Program Reserve

• Purpose – revenue from waste levies has previously exceeded the total cost of managing the waste function in a single year. The excess levy amount (i.e. surplus on operations) is allocated to the Waste Program Reserve on an annual basis. This excess is to strategically implement changes to the waste service that are required over coming years and to reduce the impact of increases to waste charges.

• Movements – following the adoption of the Waste Action Plan, council has been utilising the current surplus on waste operations as well as the proceeds from the waste reserve. This investment has started to reduce the Waste Program Reserve with further reductions outlined in this Financial Plan. The increased investment in waste services is in response to the recycling requirements with expense initiatives identified in council’s adopted Waste Action Plan

• Purpose – funds set aside in the event Vision Super advised council of an additional call triggered by an Actuary Review where insufficient funds are held in the superannuation fund to meet staff obligations.

• Movements – this reserve has reached its agreed maximum of $300,000 meaning there is no expected movement to this reserve pending an additional call from Vision Super.

• Purpose – the Loan Repayment Reserve is discretionary in nature and designed to hold funds for the repayment of interest-only loans.

• Movements – the annual contributions are equal to the deemed principal repayment so sufficient funds will be available to fund future repayments of interest-only loans. This will be utilised to pay the outstanding loan due in 2025/26.

The table below discloses the balance and annual movement for each reserve over the 10-year life of this Financial Plan. Each year the total amount of reserves is to align with the Statement of Changes in Equity.

All council reserves are classed as discretionary meaning the decision to hold reserve funds is pursuant to council’s policy position rather than a legislative requirement.