Published on behalf of the European Healthcare Investor Association by Curis Intelligence Ltd, The King’s Fund, 11-13 Cavendish, London W1G 0AN. +44 (0)20 7173 0548.

No responsibility can be taken by the publisher or contributors for action taken as a result of information provided in this publication. All rights reserved; no part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without either the prior written permission of the publisher or a licence permitting restricted copying issued in the UK by the Copyright Licensing Agency Ltd and in the USA by the Copyright Clearance Center Inc.

Introduction

Europe has seen growing demand from investors for healthcare real assets. 2025 saw a significant flow of capital into the sector from North American as well as European investors, with M&A and large portfolio deals playing a substantial role in the reported transaction volumes across Europe. Strong operational performance and positive market sentiment, as buyers seek entry points and scale amidst vendors chasing exits, suggest a potential for an active market.

Healthcare real assets are a component of what is known as social infrastructure. Social infrastructure refers to the physical assets that support the delivery of essential public and social services such as healthcare and education. This has become increasingly important due to several factors, including ageing populations and fiscal constraints. Healthcare infrastructure forms one of the more complex elements, relating to the physical environments that enable the delivery of care across the full spectrum of healthcare. Unlike more conventional real estate asset classes, healthcare real assets encompass both the physical and operational aspects of the sector, and therefore, asset performance is driven by trading performance as well as the more traditional valuation drivers.

SOCIAL INFRASTRUCTURE

HEALTHCARE INFRASTRUCTURE

Acute and specialist hospitals. General hospitals, university hospitals and specialist surgical facilities. Primary care and outpatient facilities. GP surgeries, medical centres, diagnostics hubs and medical office buildings (MOBs).

Long‑term care and supported living. Care homes for the elderly, nursing homes, dementia care, learning disability accommodation and mental health facilities.

Rehabilitation and specialist treatment centres. Covering post-acute rehabilitation, orthopaedics, oncology and neurological care.

Ancillary healthcare infrastructure. Laboratories, pharmacies and day-case clinics.

Ryan Richards

Why Healthcare? Structural Drivers of Investment

The investment case for healthcare real assets is driven by a combination of longterm structural drivers, which are influenced primarily by short-term economic cycles. It is underpinned by key drivers, which are:

• Demographics and rising co-morbidities, creating predictable, irreversible growth in demand across care.

• Assets typically benefit from long, inflationlinked leases, which provide insulation in volatile macroeconomic conditions. This has aided the sector’s resilience, with stable occupancy and performance even during the past few years of headwinds.

• Returns have remained steady, which has been majorly driven by income rather than a pure reliance on capital growth.

• Institutional capital has, in addition to conventional returns, been chasing investments that align closely with ESG and impact objectives, which is more than covered by the social and personal nature of healthcare as a sector.

Key Investor Types in European Healthcare Real Assets

The European healthcare investment landscape attracts a broad and diverse investor base:

INSTITUTIONAL INVESTORS Including pension funds and insurance companies, attracted by long income

LISTED AND PRIVATE REITS Most active in care homes, hospitals and primary care.

INFRASTRUCTURE FUNDS Increasingly allocating to “infra-like” healthcare assets as competition for traditional infrastructure intensifies.

PRIVATE EQUITY Often pursuing platform strategies, operational consolidation

SOVEREIGN FUNDS Targeting scale portfolios and operating platforms.

FAMILY OFFICE / HIGH NET WORTH Targeting entry points to operating platforms.

Deal Structures, Capital Flows and Market Attraction

Transactions utilise a range of structures, reflecting the operational nature of the sector. These include sale-and-leaseback, PropCo/ OpCo structures, Forward funding/Forward commitments, and more recently, the trend of WholeCo and management agreementstyle structures. Whether it’s allowing operators to recycle capital, separating real estate ownership from operations or investors participating directly in operating performance alongside rental income, each of these structures has numerous benefits.

Assets typically benefit from long, inflationlinked leases, which provide insulation in volatile macroeconomic conditions.”

Capital flows into European healthcare have demonstrated cyclical sensitivity, but with strong long-term momentum, Europe consistently attracts a significant share of crossborder investment. European markets are now experiencing easing interest rates, narrowing spreads and strong operational performance. All of this has contributed to a flow of capital directed at portfolios and scalable platforms, with investors seeking reasonable entry points as well as growth opportunities.

European Transactions

Recent years have seen many standout transactions as European care markets look to be consolidating. Transactions such as Assura’s purchase of NW REIT’s uk hospital, Aedifica & Cofinimmo joining to become the 4th largest healthcare REIT in the world, the merger of PHP and Assura and a run of significant corporate care platform acquisitions by Welltower (now the largest REIT globally) have demonstrated not only the long term commitment of investors to European healthcare, but healthcare’s significance within real estate.

Investors in HealthcareHealthcare Real Assets 2026

The report expands on the themes mentioned to provide a detailed outlook of European healthcare real assets. This will include:

• Analysis across care homes, hospitals, primary care and emerging asset classes such as medical office buildings. Market dynamics, regulatory frameworks and funding models as they vary geographically.

• Operator fundamentals, labour dynamics and ESG considerations. Investment structures, risk allocation and return drivers.

While the general European economic outlook remains subdued, the view on healthcare real assets remains positive. Demand is essentially non-discretionary and driven by demographics rather than sentiment. As economic conditions stabilise, capital continues to flow decisively to the sector, and healthcare should no longer be seen as a purely defensive allocation, but also as a robust sector with proven long-term income capabilities.

Welcome

European Healthcare Investor Association (“EHIA”) is the largest association of private capital providers investing in healthcare companies in Europe. Our aim is straightforward - to facilitate deals and promote the sector.

We do this by building our community and sharing knowledge through our conferences and networking events for our members, and sector focussed market data and analysis from our strategic partners and our Official Journal, Investors in Healthcare.

Whilst we do not lobby for the sector, we do promote a better understanding of investors’ contribution to the broader healthcare economy from innovation, employment and wealth creation.

Who we are

We are a not-for-profit trade association with over 70 members including private equity, infrastructure, real estate and sovereign funds, foundations and family office investors, corporate leaders, advisors and other members of the healthcare investing community, all focussed on building successful healthcare businesses.

What we do

We help our members to invest capital and expertise into building great healthcare businesses and generating returns. Our members take a long-term approach to investing in privately-held companies, injecting not only capital but dynamism, innovation and expertise. This commitment helps create healthy and sustainable companies, securing millions of jobs and delivering strong returns for their investors such as leading pension funds and insurers, whose members depend on them for their retirements.

How we work

We have an integrated strategy combining information sharing, our two EHIA conferences (“Private Capital” and “Real Assets”), networking events, and a focussed digital offering. We actively communicate with our members on LinkedIn and email, as well as online via our Official Journal, Investors in Healthcare. This is a Google News listed digital business intelligence platform delivering news, data and analytics. This knowledge creates actionable insights for

As Executive Director I am focused on delivering for our members. Central to that mission is having an ongoing dialogue directly with as many of them as possible and my door is always open. Our strategy is for the Association to be a convener of like minded people and a source of knowledge and opportunities for healthcare investors. My remit is to deliver on that strategy by providing valuable benefits for our members.

SARAH WARD Executive Director, European Healthcare Investor Association

investors, coporate leaders and advisors in the sector. Access to the journal is included with membership, with subscriptions available for non-members.

Key to delivering for our members are our partners who not only provide valuable content, but host many of our events. EHIA works closely with a range of strategic partners in the advisory community including J P Morgan (investment banking), McDermott Will & Schulte (legal), L.E.K. Consulting (strategy consulting), Compass Carter Osborne (executive search), Marwood Group (regulatory consulting), RSM Ebner Stolz (accounting), Howden (insurance) and Virgin Money (specialist funding).

Communicating with our membership

Members are time poor, and therefore focussed, relevant content available in an easily digestible format is key. Perhaps as a result of the “virtual” start to the organisation, communication has by necessity been digital – via an active LinkedIn presence; twice monthly newsletters for members and non-members covering deals, people moves and market reports; online via the website including a Resource Hub with a growing library of member-only content; and Investors in Healthcare, the association’s online journal. Investors in Healthcare now has 11,000+ LinkedIn followers and growing as well as nearly 200,000 visitors to its website as it establishes itself as the one stop destination for investors looking for deal flow, insights and news on people, companies and sector trends.

Member feedback

Something

like this is needed in a European context –I believe in the underlying purpose of EHIA’

This isn’t an industry that organizes itself well so there are some real opportunities for EHIA in Europe’

EHIA is a great concept –it’s still early in its maturity, but it’s an idea everyone can get behind’

EHIA could do a lot just by orchestrating members to share existing knowledge’

Focusing on European Healthcare Real Estate

Ed White, Head of UK Consultants ‑ MSCI

Each year, MSCI estimate the size in value terms of the professionally managed global real estate market across all sectors and geographies. The latest iteration estimated a contraction of over 4% down from 13 Trillion (USD) to 12.5 Trillion (USD) across the world and continues a trend which has existed for the last 3 years; the real estate market by value is becoming smaller.

There are a handful of reasons; the main being the impact of currency and the re-sizing of the global office market which experienced the greatest contraction over the period due to declining values (although offices still make up the largest part of the overall global real estate market by value). However, some sectors do not correlate with this contraction and have in fact experienced growth in overall value terms; residential, logistics and industrial (including data centres) and healthcare all form part of this growing and expanding market size estimate and are slowly taking a bigger share of the overall market estimate.

Source: MSCI Real Estate Market Size Estimate

European Healthcare Real Estate

MSCI estimate the current size of the professionally managed investable healthcare real estate market in Europe to be circa £100 Billion with around 80% of this market owned by either listed entities (for example REIT’s) or via an investment vehicle such as an investment fund. This does not include assets in public ownership or the development pipeline.

Diversification of ownership and investment has become a major theme within healthcare real estate more recently. An increase in international investment, particularly from major global asset owners and asset managers has started to change the dynamic (see figure 2), with an increasing proportion of the market now owned directly. This has also become increasingly apparent within the MSCI real estate datasets where MSCI’s European healthcare coverage has nearly doubled over the past decade, with healthcare real estate one of the few sectors where institutions remain selectively active led by these types of investors. Growth in coverage has been particularly pronounced post-pandemic, reflecting a reassessment of sector allocations from retail and office to more defensive sectors and/or those sectors providing growth opportunities. This means healthcare real estate has arguably transitioned to (and can be seen as) a core sector within portfolio allocations.

This growth in coverage now means MSCI

Source: MSCI Real Assets

of Capital Value

An increase in international investment, particularly from major global asset owners and asset managers has started to change the dynamic.”

receives real estate investment data from over 100 portfolios across Europe alone covering over a third of the estimated overall market size for the European Healthcare Investable market. This is a large increase from where coverage was 5 years ago and certainly a decade ago.

The data MSCI receives on these assets is aggregated and anonymized to produce a comprehensive suite of metrics. These include investment rates of return, income fundamentals such as rental growth and yield movements, and a range of additional KPIs. All metrics are directly comparable across other real assets and the broader public and private investment universes, enabling investors and owners to gain transparency and benchmark performance effectively.

The growth in coverage and consequently transparency is due to the long term attractiveness of healthcare real estate as a thematic investment which has been well documented across the European and Global Investment Universe for many years. However, the availability of data has often meant that the investment case has been more difficult to justify particularly alongside more dominant sectors such as retail, offices, residential and logistics. But, as allocations have steadily increased, availability of good quality data has also increased which in turn has enabled MSCI to produce long-term investment metrics to sit alongside the thematic opportunity of the asset class, as described above.

The availability of data has also enabled a

Source: MSCI Real Assets

more granular analysis to be undertaken beyond simply healthcare real estate. The availability of metrics across geographies and property types provides further insight into the performance of healthcare real estate both within the sector and alongside other asset classes.

So what do the performance dynamics look like?

Over the last 10 years, healthcare real estate has delivered the highest risk-adjusted total returns of all major real estate sectors across Europe.

Volatility has been materially lower than office, retail, and hotels, while returns have remained competitive or superior across all sectors apart from industrial/logistics.

Underpinning this high risk-adjusted return profile is a continual stream of stable income which on a Total Return basis is higher than all other sectors despite negative capital growth over the last handful of years.

The differential in the income return

Source: MSCI Real Assets

between healthcare real estate and the wider real estate market is typically due to the leasing structures and operating models which sit within each asset and vehicle. This is quite different to the models which exist in other parts of the wider real estate market and very different from the healthcare sectors nearest comparators.

These structures also provide a level of value protection and appear less sensitive to changing market dynamics from both an occupancy and investment perspective. The impact of pricing and valuation movements can clearly be seen in figure 5 with Europe’s top performing sector, industrials, experiencing far greater volatility due to the external impacts of supply chain dynamics and in certain geographies restricted supply. This has led to large amount of capital squeezing yields only to be unwound as interest rates rose and consequently the risk free rate.

Retail has been the main long term underperformer as customer preferences have changed in terms of accessibility and type of product. More recently offices have suffered in terms of performance, both from return to work practices as well as regulation. But perhaps the biggest feature of this chart is the stability of healthcare real estate year on year; it simply not as volatile as the other real estate providing far more predictable total returns.

Over the long term, healthcare real estate continues to produce strong solid total returns over ten years. ”

Source: MSCI Real Assets

Placing Healthcare Real Estate in the real assets universe

Historically, changes in allocations to real estate mainly meant a variation in risk appetite along the main sectors available for investment. For example an increased allocation to offices may have meant moving in to office development or specific types of retail beyond malls and shops. As newer sectors have evolved such as logistics, hotels and indeed healthcare these have offered diversification opportunities with often very different risk and performance profiles from traditional sectors and are now well understood.

More recently, the real asset investment universe has expanded still further with investors now having access to a far wider universe of risk and return opportunities across both debt and equity. Infrastructure has been a component of many portfolios for many years and more recently debt/credit funds operating across infrastructure and real estate have also become an investment option providing access to a more nuanced risk return profile.

5

Source: MSCI Real Assets

Figure 6

Multi-asset class performance

Healthcare real estate no longer just sits alongside real estate offering real estate diversification, but also infrastructure and credit. The chart below places the performance of healthcare real estate alongside performance of the equivalent indexes for real estate debt funds, infrastructure as well as public market performance metrics. Over the long term, healthcare real estate continues to produce strong solid total returns over ten years placing between infrastructure and the wider equities market.

Note: Results shown here for direct real estate and fund-level real estate are based on separate quarterly samples with specific sources indicated below.

Sources: EQUITIES: MSCI, Mid & Large Cap, Index, Total Return, GBP BONDS/FIXED INCOME: JP Morgan. GBI Broad, Traded, Index, 7-10 Year, Total Return, GBP; PROPERTY EQUITIES: MSCI, GB/Real Estate, Gross Total Return, GBP, series#115565; DIRECT REAL ESTATE (ASSET LEVEL): MSCI, MSCI UK Quarterly Property Index (and monthly index); NET FUND LEVEL REAL ESTATE: MSCI, MSCI UK Quarterly Property Fund Index. MSCI European Fund Level Debt Index – data to Q1 2025 – Euro Variable Currency. MSCI Global Infrastructure Fund Level Index_Research Release – data to Q2 2025 – USD Fixed Currency.

Assessing the key asset classes

Thomas Atherton, Strategy & Market Intelligence Manager, Savills OCM

CARE HOMES

Care Homes remain a compelling asset class, underpinned by Europe’s ageing population and a stark supply-demand imbalance.

While the sector has faced headwinds over the last few years, including a more challenging financing environment and increasing operational costs, investment volumes began to rebound in late 2024 and are set to recover further in H2 2025 and beyond, as rates ease and investor confidence returns.

This commentary frames real estate in its global context, looks at various routes to market and their relative advantages, analyses investment volumes and trends, highlights key transactions, and discusses challenges and opportunities across seven of Europe’s core Care Home markets: the United Kingdom, Germany, France, Spain, the Netherlands, Belgium and Italy.

It assesses which markets have attracted the most investor interest in recent years, as well as evaluating those that now appear best positioned for future growth.

International Expansion Up to 2022 Cheaper Debt and Attractive Risk-Adjusted Returns

In the decade leading to 2022, strong macroeconomic performance and access to cheap capital, combined with structural demand for Care Homes (ageing populations and growing supply-demand imbalances) led to the creation of large providers that were often active in multiple geographies.

Real estate investors such as Aedifica, Cofinimmo, and Healthcare Activos, alongside Care Home operators like Clariane (formerly Korian) and Emeis (formerly Orpea), significantly expanded their global footprint, in Europe and internationally.

This expansionary phase was propelled by strong Cross-border capital flows into European Care Homes, as well as the emergence of large OpCos funding their growth with sale and leasebacks.

In larger markets, national REIT platforms such as Target, Impact (now CareREIT) and Nrep, and funds such as Octopus and Civitas, also built significant portfolios with key operator relationships.

Emeis (Dagelijks Leven) 2,000 1.5% France PLC

1,672 1.3% France PLC

(Bloezem) 1,124 0.9% France PLC De Herbergier 880 0.7% Netherlands Private De Leyhoeve 557 0.4%

Source: EAC, Savills Research

Despite COVID-19, which led to reductions in profitability, rising costs, and staffing pressures, real estate in Europe’s core Care Home markets saw decade-high capital inflows between 2020 and 2022, reaching over €5 billion in 2021, compared to a pre pandemic average of around €2.1 billion (2016–2019).

This surge was underpinned by even cheaper debt than in the years prior and an active sale-and-leaseback market, with a perception that Care Homes offered attractive risk-adjusted returns relative to other real estate asset classes.

Figure 1 Top 5 Operators in Each European Market

Geopolitical Risk, Inflation and Higher Interest Rates

As occupancy was recovering and COVID driven operational pressures were easing, a new wave of global disruption emerged from 2022 onwards, with war breaking out in Ukraine, the highest inflation and interest rates in over a decade, and growing geopolitical uncertainty as governments prepared for the possibility of conflict, both military and economic.

Central banks deployed aggressive rate hikes from the second half of 2022 through 2023 and 2024.

Investment activity slowed sharply, with capital becoming harder to access and buyers retreating as investors focused on divestments, often at discounts, in order to deleverage.

Annual investment in the core European Care Home markets addressed in this report declined for three consecutive years, dropping from €5 billion in 2021 to just €2.2 billion by 2024.

Reduced Real Estate Investment Appetite

Whilst Healthcare real estate continued to offer strong returns, the illiquidity of the underlying assets, higher cost of leverage and higher bond yields, compared to vendor expectations on PropCo yields, made real estate less attractive on a risk-adjusted basis, leading institutional investors to reallocate capital to lower risk government and corporate bonds, where deeper secondarymarket liquidity and faster settlement cycles make trading and exit more efficient.

Another group of investors that historically have been very active in Healthcare, Real Estate Investment Trusts (REITs): tax efficient vehicles that own and manage incomegenerating property while distributing most of their earnings to shareholders, also reduced their capital deployment.

UK and European REITs continued to see strong rent collection, but the public markets did not draw a distinction between real estate asset classes (such as Office, Retail and Healthcare) and many traded at significant discounts to Net Asset Value (NAV), meaning the company market capitalisation was lower than the value of its underlying assets, limiting their ability to raise fresh equity to deploy.

Being unable to raise equity meant debt was also more expensive, as the risk to lenders increased, leading to a marked slowdown in transaction activity across the sector, as REITs have historically been responsible for a large proportion of capital invested.

Despite recovering Care Home occupancy across Europe, several operators encountered financial distress due to excessive debt, rising interest rates, and increasing operational costs. Many became overleveraged after aggressive expansion during the growth phase up to 2022.

Some prioritised speed of growth and volume of assets over quality, leaving them exposed when performance fell short of expectations. The culmination of these factors led to a wave of insolvencies across the sector.

Return to Growth 2024 Onwards

Sentiment and Capital Returns Care Home investment in H1 2024 was subdued, down 39% from an already low point in 2023, but it rebounded in H2 2024, with €1.50bn deployed - 22% above the same period in the previous year. Full-year volumes reached €2.24bn, only 8% down on 2023.

Momentum from H2 2024 has carried into 2025, supported by falling interest rates and a narrowing gap in buyer and seller price expectations, which had been distorted during the earlier period of international expansion. By May 2025, cumulative investment volumes

for 2025 have reached €1.76 billion, exceeding the €1.61 billion recorded over the same period in 2021, which saw the highest full year investment volumes in over a decade.

Improving operator performance and a more favourable macroeconomic environment to last year has bolstered Care Home market sentiment. In Savills European OpRE Investor Survey 2025, the proportion of respondents looking to invest in Care Homes stood at 35%, up from just 16% in 2024.

Annualising investment volumes up to May 2025 this year makes this the second highest annual investment volume in over a decade. The rebound in total volumes during H2 2024 and through 2025 was driven by the strong performance of the UK, Spanish, German and Dutch markets, with Cross-border capital continuing to be particularly active.

US REITs Leverage WholeCo Model in the UK

In 2024, the UK saw a surge in investment, with US capital playing a prominent role. One strategic approach was the use of management contracts and RIDEA structures (for US REITs), which offer greater flexibility and allow real estate investors to participate in the operational upside of the asset, enhancing return potential.

US REITs have actively used this model when acquiring UK assets and have benefited from significant weekly fee uplifts. However, REITs are subject to regulatory differences across jurisdictions. UK REITs face tighter constraints, as at least 75% of their income must come from property rental, limiting their ability to share in operational profits and making WholeCo participation more difficult.

With bid-ask spreads too wide on PropCo transactions, this gave the American REITs an advantage in the market, especially when WholeCo’s were the main deals occurring in 2024.

In another strategic approach, US REIT Omega Healthcare Investors has targeted Tier 1 and Tier 2 stock, while other investors have focused on Prime and Super Prime. As a result, Omega has faced less competition and has secured assets at attractive pricing. As of May 2025, US Healthcare REITs were trading at a 20.6% premium to NAV, positioning them to acquire UK Care Home assets at discounted valuations and capitalise on transatlantic arbitrage as their UK-listed peers remain constrained by persistent NAV discounts and difficulties raising capital.

Figure 3

Real Estatae Care Home Ownership Models

Where is the Capital Coming From?

Both domestic and cross-border capital remains active across Europe’s Care Home markets, although investor focus varies by country.

France, Spain, Belgium, and the Netherlands all show a strong domestic focus: in each, two of the top three most active investors are domestic, with only one international player represented.

This shows a balance of interest, but with a weighting towards nationally-based investors.

By contrast, in Italy all of the most active investors are France-based, underscoring the limited role of domestic capital in that market. The UK is another geography that is seeing cross-border capital inflows, but from further afield, particularly US investors.

Cross-border investment in European Care Homes has been a consistent trend for over a decade, with the sector offering investors access to a broader range of assets while reducing reliance on any single social security system or care model.

Across Europe’s core Care Home markets, cross-border capital accounted for almost half (48%) of total investment in 2024, the highest proportion since 2020 (52%) and markedly higher than the 37% in 2023.

In 2024, notable deals included UK-based Octopus entering the Spanish market, Spanish investor Healthcare Activos expanding into Germany and deepening its presence in Belgium, and Civitas making its first investment in Germany.

As we reach the halfway point of 2025, cross-border capital is driving investment volumes, accounting for the vast majority (85%) of investment in the year up to May.

The strategic value to investors of geographic diversification has been underscored by recent challenges in the French and German markets.

Cross-border investment in European Care Homes has been a consistent trend for over a decade, with the sector offering investors access to a broader range of assets while reducing reliance on any single social security system or care model.”

PRIMARY CARE

Primary Healthcare facilities, such as General Practitioner (GP) surgeries, offer investors long-term, government-backed rental income. The UK Government is prioritising care in community settings, with plans to develop Neighbourhood Health Centres and a strategic focus on prevention over treatment.

After over a decade of limited investment, Primary Care has returned to the forefront of national policy, as highlighted by the NHS’s Fit for the Future: 10-Year Health Plan for England released this month, a national strategy aimed at driving long term system reform, with Primary Care as a central focus.

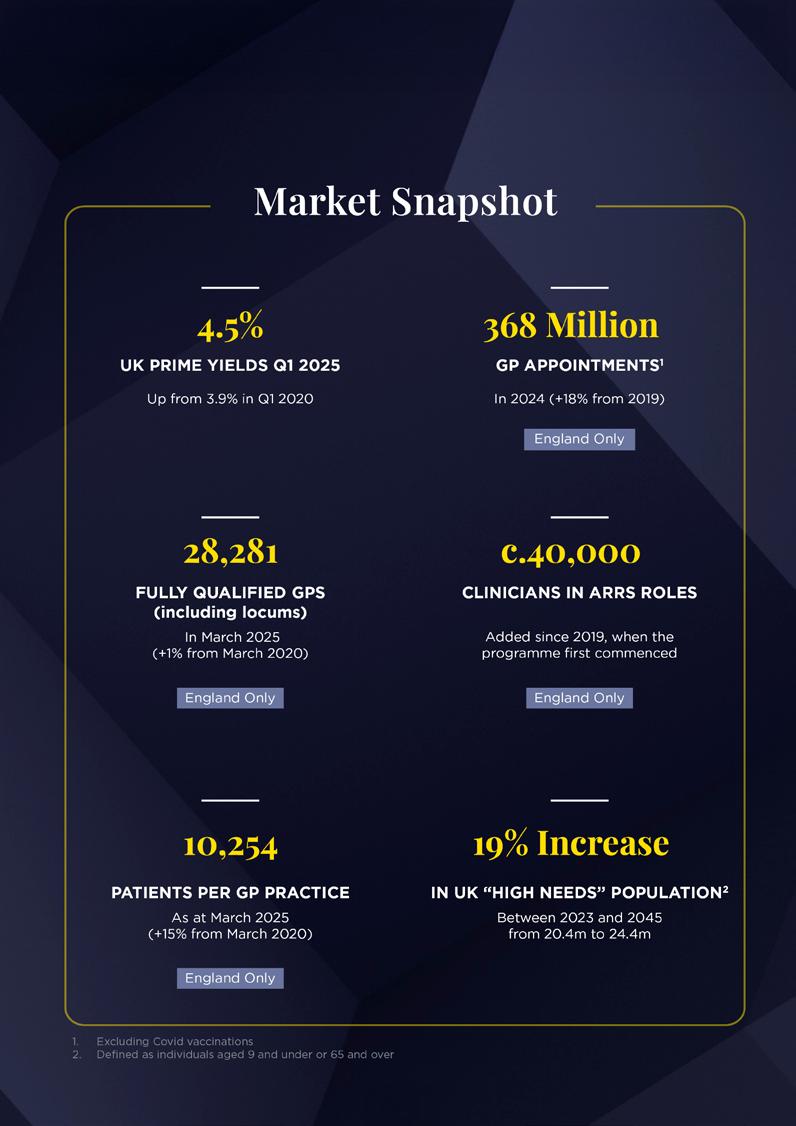

The NHS is still grappling with a major backlog of appointments following the disruption caused by Covid-19. While demand has risen, the number of fully qualified GPs has not kept pace with that demand, or with population growth.

There has, however, been the introduction of approximately 40,000 non-GP clinicians, funded through the Additional Roles Reimbursement Scheme (ARRS) by Primary Care Networks (PCNs), to support the workforce and provide more integrated, multidisciplinary care within general practice.

This includes pharmacists, physiotherapists, paramedics, and social prescribing link workers. While the introduction of these roles has helped meet rising demand, the expansion of staff and services in GP surgeries, set to accelerate through the rollout of Neighbourhood Health Centres under the NHS’s 10-Year Plan, has placed increasing pressure on an estate that is already undersized and outdated.

As the system moves towards more integrated, community-based provision, the UK’s Primary Care infrastructure will require a fundamental overhaul, with more modern, purpose-built facilities needed to support current workforce models and deliver future service ambitions.

Prime yields in the sector have been stable at 4.5%, supported by strong fundamentals and increasing investor demand, and also now driven by government backing and a renewed policy emphasis on Primary Care services across the UK

Investment is on The Road to Recovery

The past few years have been challenging for UK real estate markets. Rising interest rates have impacted investment activity across all sectors, and Primary Care has been no exception.

Stability in Primary Care

However, as the economic backdrop improves, government backing for Primary Care investment strengthens, and falling interest rates make debt more accessible, market activity is returning, and we are seeing new groups of investors enter the sector following Covid.

One of the key drivers of increased activity is the stabilisation in yields since the market shift in late 2022, with rental growth helping to offset outward movement in capital values.

The latest valuations from Primary Health Properties (PHP) and Assura provide further evidence of resilience within the sector, giving investors confidence that now is an attractive time to enter the market or expand their existing holdings, with a strong likelihood of tighter yields over the medium term.

A flight to quality and secure, long-term income property investments, which Primary Care offers, was a trend before the interest rate spike. Given the continued uncertainty in the macroeconomic environment, this trend is expected to intensify, particularly as interest rates continue to reduce.

Alongside the likes of PHP, Assura and BlackRock, who are long term investors in the market, in recent years a growing number of non-sector specialist investors have also been showing interest.

In May 2024, Assura and pension scheme USS announced that they had entered into a new £250m joint venture to support investment in essential NHS infrastructure, including GP surgeries. More recently, in May 2025, KKR and Stonepeak made an offer to acquire Assura, which was later set aside in favour of a proposed merger with PHP, subject to shareholder approval.

Figure 4

UK Prime Yields

OFFICES (LONDON CITY)

SHOPPING CENTRES HIGH STREET RETAIL

PRIMARY CARE INDUSTRIAL MULTI-LET YIELDS

Strong interest from a broadening investor base, including private equity, pension funds, institutions, REITs, infrastructure funds and private investors, highlights the renewed appeal of UK Primary Care real estate as a resilient and income-secure asset class.

Safe and Secure Government Backed Income

The asset class is particularly attractive to investors given its high degree of income security from the NHS, which provides GPs with rent reimbursement. Recently this appeal has been further strengthened by increased government health spending and a clear policy shift towards preventative care, as outlined in the NHS 10-year Plan. This is expected to drive greater reliance on Primary Care services.

Institutional lenders are seeing some, albeit limited, interest from GPs in acquiring their own real estate, which was uncommon until recently. At the same time, investors report that raising debt for large-scale acquisitions in the sector is becoming significantly easier.

There is a marked difference in the yield profile for assets depending on the remaining lease term in place. Surgeries with short dated leases, which typically include older surgeries, have yields c.75 basis points higher than those for new build investments with 20+ year leases in place.

Assets with five years or less remaining on their leases represent a relatively new segment of the market, with most properties

built between 2000 and 2010. As this market has yet to fully mature, yields remain widely spread. However, variation in yields even within similar lease profiles suggests an emerging divergence between primary and secondary assets.

Leveraging Private Sector Investment

Central to the Government’s 10-Year Plan is the creation of a national Neighbourhood Health Service, underpinned by a programme of GPled Neighbourhood Health Centres. Delivering on this vision will require substantial investment in modernising and expanding the Primary Care estate.

The plan explicitly states that it will explore new capital investment models, including greater use of private sector funding, to help unlock delivery, particularly in underserved areas.

Growing policy support for private investment in Primary Care infrastructure presents a clear opportunity for investors to contribute meaningfully to improved access and outcomes, particularly in communities facing the greatest unmet need for GP services.

Notably, while this represents a long-term strategic shift, the plan comes at a time when the NHS continues to face significant care backlogs, high demand for elective procedures, and sustained pressure on waiting lists, factors that will continue to shape service delivery in the near term.

MEDICAL OFFICE BUILDINGS

The MOB sector in Europe remains a nascent market, with adoption rates varying significantly across countries and still far less established than in the US, where outpatient healthcare real estate is long-standing and deeply institutionalised.

Within Europe, Germany represents the leading market, while the Netherlands is emerging as a key area of growth. By contrast, France and the UK remain structurally constrained by their centrally funded healthcare systems, making the development of a US-style MOB market unlikely in the near term.

These regional disparities largely reflect differences in healthcare delivery models and institutional structures within national health systems. However, in European geographies where healthcare systems make MOBs feasible, a clear shift is underway.

As healthcare provision becomes more decentralised, outpatient services are moving away from main hospital campuses and into community based settings, driving growing demand for modern, purpose-built space.

The MOB sector in Europe remains a nascent market, with adoption rates varying significantly across countries and still far less established than in the US.”

The viability of MOBs is closely tied to the degree of decentralisation within a country’s healthcare system and the balance between public, non-profit, and private providers.

A functioning MOB market relies on the separation of healthcare delivery from property ownership, where independent doctors and outpatient operators lease rather than own their premises.

This model performs best in decentralised, insurance-based systems with a strong base of independent practice, generating diverse tenant demand from clinics, diagnostic centres, and specialists seeking flexible, modern premises.

It has been most successful in Germany and the Netherlands, where insurance based frameworks and a mix of public, non-profit, and private providers enable leasing models to thrive, unlike systems that concentrate care delivery within state owned hospitals, where investor-owned MOBs are less viable.

Germany leads in both scale and maturity, supported by its mixed public–private system, a large number of self-employed physicians who prefer to rent rather than own their premises, and healthcare policies that continue to move treatments toward outpatient environments.

The Netherlands, while smaller in absolute scale, is demonstrating strong growth momentum underpinned by structural reform, insurer incentives, and an expanding base of independent treatment centres (ZBCs) and integrated health hubs.

Together, these dynamics are fostering the gradual development of the MOB market across Europe.

France is emerging as a potential future MOB market, supported by growing investment in community-based clinics and specialist outpatient centres.

However, the French healthcare system remains dominated by private clinics that are typically leased or owned by a single operator or healthcare provider, alongside publicly funded health centres, leaving few independent doctors or clinics that would lease space in an MOB format.

Similarly, the UK does not have an MOB market, reflecting the NHS’s centralised model and limited reliance on private sector outpatient services, aside from a few emerging specialties such as ophthalmology.

In the UK, independent doctors are typically contracted by private providers or, when working independently, will lease space

within private hospitals or NHS Private Patient Units (PPUs).

Key MOB Markets in Europe: Policy-Driven Demand

Germany and the Netherlands Germany’s outpatient sector has evolved from a fragmented base of small practices into a more consolidated, multi-disciplinary system. Since the 2004 introduction of Medizinische Versorgungszentren (MVZs), groups of doctors have increasingly co located within shared facilities, driving demand for larger, purposebuilt medical facilities.

The MVZ was established through the Health Modernisation Act to modernise and integrate outpatient healthcare delivery by enabling doctors from different specialties to work together within a single, jointly managed organisation.

MVZs provide a wide range of outpatient services, from general medicine and diagnostics to specialist consultations, all under one roof. Over the last two decades this has created growing demand for larger, purpose-built or refurbished premises, such as modern MOBs located near hospitals or within communities.

Germany is now undergoing another major structural transformation in healthcare delivery, shaped by two closely connected federal initiatives:

Ambulantisierung and the Krankenhausreform. Both reforms share the goal of rebalancing the healthcare system by transferring suitable medical procedures from inpatient to outpatient settings and ensuring hospitals focus on more complex, specialised treatments. Ambulantisierung refers to the ongoing shift of diagnostic, surgical, and rehabilitative procedures, traditionally performed in hospitals, into outpatient environments that do not require overnight stays.

MVZs provide a wide range of outpatient services, from general medicine and diagnostics to specialist consultations, all under one roof. Over the last two decades this has created growing demand for larger, purpose-built or refurbished premises.”

Figure 6 Germany and the Netherlands MOB

Volumes, €m, 2015 – 2025 (YTD October)

As part of this, a new reform Ambulantisierungsgesetz is expected to take effect in 2025, which expands the range of treatments eligible for outpatient reimbursement, incentivising hospitals to deliver more procedures outside inpatient settings.

Krankenhausreform, formally adopted in November 2024 and effective from 1 January 2025, restructured hospital provision by concentrating complex care in specialist centres, downsizing general hospitals, and shifting lower-acuity care into community-based settings.

The reform is expected to result in the closure of around 20% of hospitals across Germany.

As patient treatment increasingly moves out of hospitals and into outpatient environments, this reform is expected to generate sustained demand for modern MOBs and integrated health centres that can accommodate multispecialty outpatient provision.

The Netherlands represents an emerging market for MOBs in Europe, underpinned by a decentralised outpatient healthcare system and strong policy support for integrated,

community-based care. A key policy driver is the Integraal Zorgakkoord (IZA), introduced in 2022, which aims to shift appropriate hospital treatments into outpatient and independent treatment centres (ZBCs –Zelfstandige Behandelcentra) as part of a nationwide integrated-care strategy.

Dutch health insurers play a pivotal role, actively incentivising outpatient treatment to control costs and improve efficiency.

This is reinforcing the expansion of specialised clinics in areas such as ophthalmology, orthopaedics, dermatology, and diagnostics, fuelling demand for modern, flexible, and community-based medical real estate.

MOB Investment

Investor Demand Remains High but Market is Limited in Availability of High-Quality Purpose-Built Assets

Attracted by a favourable supply–demand imbalance, strong underlying growth drivers, and the emergence of modern, high-quality assets, the European MOB sector has undergone increasing institutionalisation over the past decade, supported by a growing tenant base and an influx of institutional capital.

Following the Covid period, when interest rates were at decade lows and demand for outpatient care outside hospitals accelerated sharply, investment volumes in the MOB sector reached record levels, approaching €1 billion in 2021 across Germany and the Netherlands combined.

As institutional participation in the asset class increased, a growing number of sizeable portfolios were created and brought to market. However, while portfolio activity has expanded, opportunities of scale remain limited, preventing the sector from sustaining consistent year-on-year transaction volumes.

Activity remained elevated through 2022 before declining in 2023 and 2024, largely due to rising interest rates, a higher cost of capital, broader macroeconomic uncertainty, and a shortage of high-quality portfolios being brought to market.

The slowdown in MOB investment activity reflects both the limited availability of institutional-grade portfolios and the sector’s relative immaturity as an emerging asset class in a more challenging macroeconomic environment, which constrained investor confidence and liquidity. As a result, transactional activity declined even as underlying occupational demand remained robust

Recently, the sector has attracted interest from a broad range of investors, including

pension and insurance-backed institutional capital, REITs, private equity firms, and dedicated healthcare infrastructure funds.

HIH Invest, a German institutional real estate investment manager, acquired a health centre and office building in Michendorf, Germany in September 2022. In May 2023, Cofinimmo, a Belgium-listed healthcare REIT, acquired the Baandert Medical Center in Sittard, the Netherlands at a cap rate of 6.0%. The asset was delivered as a turnkey property with a 13-year WAULT.

In June 2024, Swiss Life Asset Managers, a European insurance and pension fund manager, acquired an MOB in Wolfsburg comprising 29 rental units occupied by specialist practices and providers of medical services and products.

Additionally, TSC Real Estate is raising a €200 million fund, announced in September 2025, to invest in German outpatient medical centres, highlighting strong positive sentiment for the German outpatient real estate sector.

European VS US MOB Yields

In the United States, where the sector has long been institutionalised and benefits from an established investment track record, MSCI data indicates that MOB yields compressed steadily in the decade up to 2022, supported by entrenched structural trends in outpatient care delivery, strong fundamentals, and defensive income characteristics.

Over the last 12 months, we have advised on and transacted in excess of €5 billion of Healthcare and Senior Living real estate, in the UK and Europe.

Deals advised on range in size from €1 million to over €1.5 billion, with a broad cross-section of clients that includes institutional investors, private equity, annuity funds, banks and non-bank lenders, developers, operators, charities and NHS Trusts.

SAVILLS PAN-EUROPEAN CAPABILITIES

▪ Transaction Advisory –Disposals & Acquisitions

▪ Deal Structuring

▪ Capital AdvisoryEquity & Debt Financing

▪ Recapitalisations

▪ Valuation

▪ Consultancy

▪ Research

▪ Technical Due Diligence

▪ Planning

▪ Capital Allowances

From early 2023, US and European cap rates have experienced an expansion due to higher interest rates and tighter debt markets, increased risk premiums, and an uncertain macroeconomic outlook, with the US currently trading at c.7% and Europe trading at c.6.5%.

The long-term view shows European markets trending below the US, likely due to the lack of quality stock increasing competition for prime assets, with a convergence seen more recently.

This trend in yields, together with resilient fundamentals, a more active investment market, and a limited but increasing number of institutional-grade portfolios as investors continue to aggregate assets, should support interest from global capital and especially US capital in European MOBs going forward.

In Europe, most MOB transactions involve single assets, as the market currently lacks acquirable, institutional-scale portfolios. These smaller properties typically fall below the investment thresholds of REITs and large institutional buyers and can therefore be acquired at higher initial yields, despite offering comparable fundamentals and risk profiles to larger assets.

As a result, MOBs present an attractive entry point for smaller-scale investors seeking exposure to the healthcare sector, where the lot sizes for larger assets such as hospitals are often beyond reach.

This also offers a compelling opportunity to aggregate portfolios and ultimately exit at more attractive yields to institutional capital once scale is achieved.

MOBs

present an attractive entry point for smaller-scale investors seeking exposure to the healthcare sector, where the lot sizes for larger assets such as hospitals are often beyond reach.”

Meanwhile, consolidation in outpatient and clinic markets is gaining traction across Europe.

Many independent practices are being acquired by larger clinic chains or health service groups, particularly in segments like diagnostics and specialist outpatient care.

This trend enhances the credit quality of tenants, benefiting landlords and improving the institutional appeal of the sector over time.

MOBs represent a complementary investment opportunity for those already investing in clinics and outpatient centres, as these asset types are often sold together in portfolios across both the US and Europe and share similar investment fundamentals and tenant profiles.

Aggregating MOBs and clinics into combined portfolios can provide a route to achieving institutional scale, a strategy that has already been observed in several recent transactions.

Legal Update on Health and Social Care Investment

Candice Blackwood, Partner, Co‑Head Life Sciences & Healthcare ‑ CMS

Cameron McKenna Nabarro Olswang LLP

Investment in care assets has become an increasingly important part of institutional real estate and infrastructure portfolios across Europe. Rising life expectancy, aging demographics, declining capacity for care by families, and pressure on public healthcare systems have all resulted in more investment being needed and available for senior housing, healthcare facilities, nursing and residential care, step-down care, hospice care and home care.

CMS are an international law firm, with 10 offices covering the UK and full services provided in 45 countries worldwide including all of Europe, the Middle East, Asia, India and Africa. We have been advising investors, funders, health and social care providers for more than 30 years on all legal advice needed for significant cross border corporate, real asset and funding transactions. We advise both public and private clients, care entrepreneurs and family doctors through to public limited companies and international global Real Estate Investment Trusts (REITs) on all aspects of the sector including the acquisition and development of care assets, active portfolio management, regulatory, tax, medical malpractice claims, reputational damage, cybersecurity breaches, and capital procurement advice.

This article is focussed on Germany, France, Spain and the UK as the most developed care markets in Europe currently. We also have regard to the US and international investors. Care assets are operational real estate in all jurisdictions due to the need for active management and required regulatory oversight. These requirements might be perceived to introduce additional complexity and risk for some investors. However, care assets offer defensive characteristics for investors in turbulent markets, and support longterm demographic demand needs, while providing inflation-linked income stability.

Germany

Germany has the largest care market need by population. It is underpinned by a mandatory long-term care insurance system (Pflegeversicherung). This statutory framework Introduced in the 1990s, provides a stable and predictable funding base for care services, reducing demand risk compared with more market-driven systems.

Care assets in Germany are typically leased on long terms with conservative structures, often including inflation indexation. There are multiple care operators. Regulation is more complex than elsewhere as it is shared between federal and state (Länder) authorities. Regulations have also changed in recent years to require improved and updated facilities and service offerings and there are complex licence, staffing, and building requirements.

These increased compliance costs and timelines have challenged viability for some operators. They also create high barriers to entry that support long-term asset values and limit oversupply. This means that German care assets are being attractively priced for both domestic and international investors seeking stable, income-focused exposure. However, successful investment in Germany requires a deep understanding of regional regulatory requirements and close engagement with operators.

France

France’s care markets benefit from a highly structured regulatory and funding environment. Long-term care and healthcare facilities are regulated by regional health agencies -Agences Régionales de Santé (ARS), with quality standards monitored by the Haute Autorité de Santé (HAS). These frameworks provide regulatory clarity for investors, with consistent pricing and limited operational autonomy. Despite these

German care assets are being attractively priced for both domestic and international investors seeking stable, income-focused exposure. However, successful investment in Germany requires a deep understanding of regional regulatory requirements and close engagement with operators.”

regulations, France had some well publicised care issues in the early 2020s which affected investment and trading and from which the market is now recovering.

Investment activity is supported by the SIIC regime (the French equivalent of a REIT), which has enabled consolidation of healthcare real estate portfolios at scale. Lease structures are often closely aligned with public funding mechanisms and operator reimbursement models which reinforce income stability.

France is viewed as a lower-risk care investment market due to strong state involvement in healthcare provision. However, the highly structured regulatory and funding regimes require careful asset selection with a view to long-term investments.

Spain

Spain is now a rapidly developing market for health and social care asset investment. Historically reliant on family-based care and care provision by the Catholic church, Spain now faces increasing demand for institutional care and senior living driven by demographic ageing, urbanisation, international retirees and acceptance by the Spanish.

Regulatory responsibility for care services is decentralised to autonomous communities, resulting in fragmented standards, approval processes, and inspection regimes. This increases investor requirements for extensive due diligence and regulatory advice on the increased operational complexity. In response, lease structures in Spain increasingly include management agreements and hybrid rent models to balance risk between landlords and operators.

There is a historic structural undersupply of modern care facilities, particularly in major urban regions. Spain therefore presents higher growth potential than more mature markets, with successful investment needing careful due diligence and navigation of regional regulations and operators.

United Kingdom

The United Kingdom has followed the United States to become one of the most established markets for care asset investment, with significant participation from institutional

Poor regulatory performance can lead to occupancy decline, enforcement action, or closure, with consequential financial risk for investors and operators.”

investors, infrastructure funds, private equity and listed vehicles. In the UK, care homes, hospitals, specialist healthcare facilities, healthcare hubs for testing and vaccinations, and supported living developments are commonly structured under long leases ranging from 25 to 35 years, often with annual rent increases linked to consumer or retail price indices. These long-income structures have positioned care assets alongside other infrastructure-like investments within institutional portfolios.

The US has Healthcare REITs dominating the sector invested in senior housing, skilled nursing facilities, medical offices, and hospitals. Investors can select varying levels of operational exposure through structures such as triple-net leases or RIDEA management arrangements.

In the UK, regulatory oversight is provided by the Care Quality Commission (CQC) in England and Wales and the Care Inspectorate in Scotland. Poor regulatory performance can lead to occupancy decline, enforcement action, or closure, with consequential financial risk for investors and operators. In the US regulation is multi-layered overseen by the Centres for Medicare & Medicaid Services, and state level licences and enforcement. Despite regulatory and reimbursement risk, strong demographic demand, capital market depth, and operational innovation continue to attract investment into U.S. care.

In both jurisdictions operator business strength, structure, and regulatory records are important diligence items for transactions. Inspection ratings can materially affect operator viability and asset value.

In our experience, investors and operators in the UK liaise closely to ensure successful business operation, excellent patient care (digital wherever possible), and targeted capital expenditure and investment. The UK has also experienced strong growth in healthcare-focused REITs and social infrastructure funds. These vehicles provide

scale, liquidity, and access to capital markets while benefiting from demographic demand and policy support for private sector involvement in care delivery. Businesses are constantly evolving driven by funding and staffing requirements. Traditional residential care has moved to more intense nursing and dementia care, senior living communities are thriving, and there are more small supported living arrangements and specialist accommodation in local communities. These need to develop in parallel with the needed infrastructure support – affordable housing for care workers, good transport links, healthcare hubs for drop in attendance for vaccines, blood tests and diagnostics, eye and ear services,

Investment performance is closely linked to operator quality, regulatory compliance, and public funding stability. Care investments can also assist with institutional investors’ environmental, social and governance targets. Even the National Health Service (as one of the largest public property owners and occupiers in the UK) has ambitious Net Zero targets scheduled for delivery by the 2030s. Private capital is needed to fund, own, manage and improve care-related real estate which should result in improvements for public health and better social outcomes.

We are optimistic about the UK’s economic prospects, given the Government’s dedication to the health, social care, and living sectors, along with falling interest rates and reasonable transaction pricing. The strong influx of both global and national capital occurring from 2025 is likely to continue across these sectors, which offer sustainable, long-term value investment.

Comparative Analysis

Conclusion

Across all jurisdictions, care asset investment is shaped by demographic demand, regulatory oversight, and evolving investment structures. Care assets occupy a unique position between social policy and capital markets. While offering long-term income stability and social impact, they require sophisticated structuring, active management, and deep regulatory and regional understanding.

Care assets are a core component of social infrastructure - spaces to support shared civic life, ranging from transport, schools and healthcare to parks, libraries and community halls. These assets deliver essential services and are often supported—directly or indirectly—by public funding mechanisms. Governments increasingly rely on private capital to address funding gaps, modernise facilities, and expand capacity.

Currently the UK reflects capital markets innovation and REIT activity (particularly from the US), Germany and France offer regulatory stability and predictable funding models, while Spain is showing higher growth potential alongside greater operational complexity. Jurisdiction-specific factors and regulatory engagement and local legal advice remain important to successful investment outcomes.

We look forward to discussing these topics further at the first European Healthcare Investment Association Real Assets Conference.

Supporting clients across primary, acute, community, residential and social care including mental health, special education and children’s services. Our award winning Healthcare team provides innovative advice on transactions, claims, regulation, contracts and JVs & outsourcings between the public sector and the private sector.

So irrespective of where your real estate assets are, we can deploy specialist teams from across Europe’s largest Real Estate team to advise you immediately.

Candice Blackwood Partner, Co-Head of Life Sciences & Healthcare UK

Europe’s Healthcare Investment:

Why Ageing, Money and Technology Are Rewriting the Rules

Derek Breingan, Head of Health and Social Care Sector & Duncan Leitch, Senior Director ‑ Virgin Money

Europe’s health and social care sector is being pulled in three directions at once: people are living longer, governments are counting the pennies, and technology is changing how care, and business, is delivered. Put those together and you’ve got a most fascinating and progressive investment story.

The pressure point is elderly care and specialist services like rehab, acute care and mental health. For investors, and lenders like Virgin Money, that means steady income if you pick the right operators and keep an close eye on regulation, staffing and costs.

The Demographic Tsunami

There is no need to forecast because our ageing population is here. The elderly care market is already worth around $350 billion and growing at nearly 7% a year. Western Europe still dominates, but Central and Eastern Europe is catching up fast after decades of underinvestment. And tech such as telecare and remote monitoring is making home-based care more viable, which governments will love because it’s cheaper than institutional care.

The European Central Bank even says ageing is reshaping savings and investment patterns. This translates to more money flowing into long-term social infrastructure, and a premium on productivity tools to keep costs under control.

Investment: Back From the Brink

After the pandemic boom in 2021, the sector hit a wall when interest rates spiked and inflation and costs soared. However the rebound is here: €1.76 billion went into care homes in the first five months of 2025, outpacing even the 2021 peak. Cross-border investors are leading the charge, drawn by pricing power in the UK and supply shortages in Spain. Germany, despite recent operator distress, is back in play thanks to an insurance-backed funding model. In addition, Welltower invested £5.2 billion in UK care homes in 2025.5

Prime yields have reset to 5–5.75%, which is good news for lenders—more security cushion, less reliance on aspirational growth assumptions albeit with interest rates still comparatively high, Rent to Interest Cover is still thinner than it has been historically.

Private Equity: Slowing Down, Smarten Up

Private equity continues to love healthcare because it’s increasingly less volatile than most sectors and offers room for operational improvement. Fast roll-ups and exits are over however with borrowing costs higher, PE firms are focusing on integration, workforce investment and tech upgrades. For lenders, we believe that means more stable ‘sticky’ transactions and better-quality, longercommitted counterparties..

Private

equity continues to love healthcare because it’s increasingly less volatile than most sectors and offers room for operational improvement.”

The UK: Still the Magnet

The UK remains a principal target for international capital. This is due to pricing power, scale and investment structures that can blend property and operations. Fee increases in supply-constrained areas are continue to outpace inflation as long as operators deliver strong clinical outcomes and family satisfaction. Lender underwriting typically relies on strong, targeted diligence: CQC ratings, staffing ratios, occupancy and, in the case of new developments, building specs and local sociodemographics matter.

Spain, Germany, CEE: Opportunity With Caveats

Spain has a glaring shortage of care beds, making development attractive as long as you understand the regional nuances. Germany is stabilising after a rough patch, and CEE offers long-duration, inflation-linked assets but where political risk and regulatory maturity are still hurdles to negotiate.

Policy Tailwinds—and Watchdogs

Brussels now treats long-term care as a social priority, pushing investment in community care and digital health. That should mean more predictable reimbursement and better data integrity over time. But beware the “financialisation” backlash from general public: rapid private expansion without enough properly trained staff or insufficient governance can lead to shortcomings and scrutiny such as those seen in France in recent years. Lenders and investors then take the hit when confidence and occupancy collapses.

In terms of sustainability regulation, Jacob Hurtley, ESG Director at Elevation adds “investors and asset managers are keeping a close eye on the proposed amendments to the EU Sustainable Financial Disclosure Requirements. Following a draft proposal at the end of 2025, attention will swiftly turn to how to implement the proposed reporting requirements, as well as those for regulations being introduced or updated in other jurisdictions.

The Outpatient Shift and Digital Push

Across Europe, outpatient care is booming with day surgery, home dialysis, post operative rehab and step down care. It’s cheaper, faster and increasingly what patients want. Operational consistency is key however and lenders will seek satisfaction that outcomes are repeatable and contracts solid and sustainable.

Digitalisation isn’t a buzzword anymore because telecare, remote monitoring and AI triage are productivity tools. Give credit for proven tech, not speculative apps in infancy.

What Lenders Will Demand

Cash flow resilience: CPI-linked rent contracts, stress-tested for occupancy and wage inflation => consequent impact on earnings / rent cover

Asset standards: Dementia-friendly design, infection control, energy efficiency.

• Local expertise: Spain’s bed moratoria, Germany’s Länder rules, CEE’s political risk.

• Conservative leverage: Senior loans returned 12.5% in 2023, expected 8% in 2024—so lenders will increasingly not chase yield at the expense of discipline / safe harbour.

The UK remains a principal target for international capital. This is due to pricing power, scale and investment structures that can blend property and operations.

The Big Picture

Europe needs more elderly and specialist care capacity, delivered flexibly and built on the latest technologies and designs. The UK will stay dominant; Spain will attract development capital; Germany will grow steadily; CEE will open up slowly and selectively as the regulatory framework evolves. For lenders, the challenge is seeing beyond demographics into execution and business detail: staffing, tech readiness, governance, energy performance etc.

Jacob Hurtley, ESG Director at Elevation goes further adding, “we are seeing attention turning increasingly towards net zero targets, whether they are achievable and the route to getting there. Investors need to ensure that they have a clear and actionable plan to deliver a net zero portfolio in a given timeframe, working in partnership with operators to ensure capital is available to provide a meaningful shift in trajectory.

”The best lends will be those where money aligns with the ethics of care and dignity— buildings that maxmise and enhance wellbeing, operators that invest in people (both skills development and retention), and lenders such as Virgin Money that embed these standards in covenants. Get that right, and healthcare remains one of Europe’s most investable sectors for years to come and one which we are committed to supporting.

Footnotes

1 European elderly care market size ~USD 352.8bn (2024) with ~6.8% CAGR forecast through 2033. Source: Market research reports (2024–2025).

2 Savills European Care Home Investment Report, July 2025: €1.76bn invested Jan–May 2025, ahead of 2021 levels.

3 Cushman & Wakefield European Nursing Homes MarketBeat (2024): Prime yields stabilized at 5.0–5.75%.

4 Invesco European Credit Outlook (Jan 2024): European leveraged loans returned ~12.5% in 2023; forecast ~8% for 2024.

5 Welltower UK Care Home Investment (2025): £5.2bn committed to UK care homes. [Link](https://welltower.com/newsroom)

Getting down to business

When it comes to health and social care, we mean business – thanks to specialist products and dedicated support from our team of experienced Relationship Managers.

Here are some of the sectors we work with:

• Aged, specialist and childcare facilities

• Dentists and dental practices

• Hospitals and medical centres

For more info call:

Derek Breingan

Head of Health and Social Care

07818 454674

• Real estate and development finance

• Private equity and investment

• Doctors and medical practices

What healthcare assets are fundamental infrastructure

Ali Bahram, Associate Partner ‑ Mansfield Advisors

Why your next investor may have more experience in bridges and airports than patients

Infrastructure funds have significant capital to deploy, but a dwindling supply of traditional assets available to target. We explore what healthcare targets, including long-term care, is suitable for ‘infra-like’ investment in the current environment of a pandemic turning endemic, a major war in Eastern Europe and the return of the inflation bogeyman. The pandemic has thrust healthcare into the spotlight, and highlighted how robust and resilient the sector can be when growth in sectors like retail or travel faltered or there was suddenly no income at all.

Infrastructure investment has normally comprised two segments: economic and social. ‘Economic’ contains the core you might visualise as traditional infrastructure: transport (roads, bridges, ports and airports), energy, utilities, telecommunication and more recently, digital and cloud services. These fundamental assets are the foundation of a strong economy. These are essential services, with low risk and no real alternatives that offer strong, predictable cash flows into the longterm future. Pension funds are the typical investor example, where liabilities extend out decades into the future.

Core investments typically have effectively monopolies as they fully meet the need of the area and there’s no need for a further toll road or a power station. It would not make economic sense to build a competing asset, and there would not be backing from authorities to do so.

However, too much capital chasing these safe investments has sent prices up and encouraged fund managers to look to alternatives for their core returns, joining that smaller percentage already set-aside for higher risk/return assets.

Infrastructure investments in

Hospitals were first, then specialist care which demonstrated its predictability through the Covid pandemic

Infra-like investments

The social segment comprises services and facilities that contribute to a good quality of life, including healthcare but also housing, education, culture and recreation. There is an estimated social infrastructure funding gap in Europe of between €100bn and €150bn annually(1)(2)

Recently acute hospitals have been the busiest sector, see Exhibit 1, with specialist care seeing a number of deals. Infrastructure investors have also started to look at children’s services (special schools often with a residential element) and elderly care homes, with their property portfolios mitigating against execution risk and market growth. Mental health hospitals would also be there, but provider pricing power has been less predictable than those segments. Otherwise investors seek to own and manage the capital equipment needed in adjacent sectors such as clinical laboratories, mobile operating theatres or diagnostic imaging MRI or CT suites.

Traditional healthcare infrastructure investments would also have been in assets such as large hospitals, as part of publicprivate partnerships or what the UK called private finance initiatives. Once developed, these assets are then rented to national

Given the global uncertainty and rising inflation, healthcare is a safe option seen as an inflation hedge and has the added benefit of diversifying infrastructure funds’ portfolios.”

operators such as the NHS. This funding method has become less popular in Europe, and represents smaller investment sizes compared to most economic infrastructure investments. The most well-known example were the private finance initiatives from the nineties into the noughties, used in the UK for £13bn in new hospitals(3)

The rationale was that construction companies would build for a set price (and be accountable to their shareholders for delivering the asset on budget and in-time) and then would lease the building to the state for 30 years. Cynics argued that the state (or the UK Government in power) avoided the debt on the balance sheet but had to pay private sector interest rates for 30 years, and therefore far more in total than if construction had been funded directly by the state. The proponents would argue that without the risk being held by the construction companies, and if they were able to charge cost-plus, the original cost estimate would have always substantially exceeded and the net present value of the cost equal or greater to the taxpayer. From academic research, we can see that investors made an attractive return on capital, which we define as greater than the investors’ cost-ofcapital as calculated by those same academics. Outside some poorly negotiated early projects, we surmise the PFI hospital building program was a reasonable deal for taxpayers along with being a good opportunity for investors. Though to be sure we would need more insight into the counter-factual world where PFI had not existed, based on international or historical examples. This is only theoretical since there isn’t any apparent interest in such projects from the current UK Government. It doesn’t help that modern accounting standards (IFRS 16 to be precise) mandate that long leases be capitalised, though of course this isn’t the only factor.

Infra-like, also known as infra-adjacent or core+ investments, have a higher risk profile than traditional infrastructure investments. They must still be deemed ‘essential’, however the definition has stretched to include the operating businesses along with the physical environment and its rent.

Healthcare as infra-like Health and social (long term) care have a good story to tell the investment committee, since we are not getting any younger and until very recently at least, we were living longer with ever-growing entitlements to healthcare. Demand for healthcare is inelastic; treatments will be required regardless of economic outlook and developed countries prioritise healthcare spending.

Other sectors like care homes and retirement villages are property backed. Be warned that much UK elderly care stock is very dated and may not be suitable for a long investment period of ~20-30 years.

However there are plenty of high quality, future-proof properties, and these will remain so if maintained. Elderly care homes’ local authority and NHS payors do not default.

One Octopus Group healthcare infrastructure survey found that 60% of global healthcare infrastructure investors are focused primarily on the UK (n=100)(4)

Traditional infrastructure investments provide a rate of return between 8-15%.

Infra-like investments possess an increased risk-profile, and therefore investors demand an increased reward. Healthcare assets can achieve much higher rates of return in the realm of 20%, as targeted by private equity, however the long term goals differ.

The yields required by PE are 20%+ over a shorter investment period. The priorities of PE are to maximise the exit multiple over a 3-5 year investment period, and as such invest profits into growing businesses rapidly.