SIENA GREEN Associate 212-346-4120 siena.green@slgreen.com SLGREEN.COM Premier Park Avenue Location

GARY ROSEN

Senior Managing Director 212-216-1687 gary.rosen@slgreen.com

BRENT OZAROWSKI Executive Managing Director 212-372-2246 brent.ozarowski@nmrk.com

HOWARD TENENBAUM Executive Vice President 212-216-1685 howard.tenenbaum@slgreen.com

20,000 Square-Foot Tenant Amenity Space with Wellness Center, Hospitality-Style Lounge, Conference Center and Grab-N-Go Cafe

Surrounded by World-Class Retail, Dining and Superior Hotels

JONATHAN FANUZZI Executive Managing Director 212-372-2036 jonathan.funuzzi@nmrk.com

KEVIN SULLIVAN Director 212-850-5462 kevin.sullivan@nmrk.com

DAVID WATERMAN Associate 212-372-2216 david.waterman@nmrk.com

PARK AVENUE TOWER

3,500 - 17,000 RSF

Tower Floor Build-To-Suit Opportunities

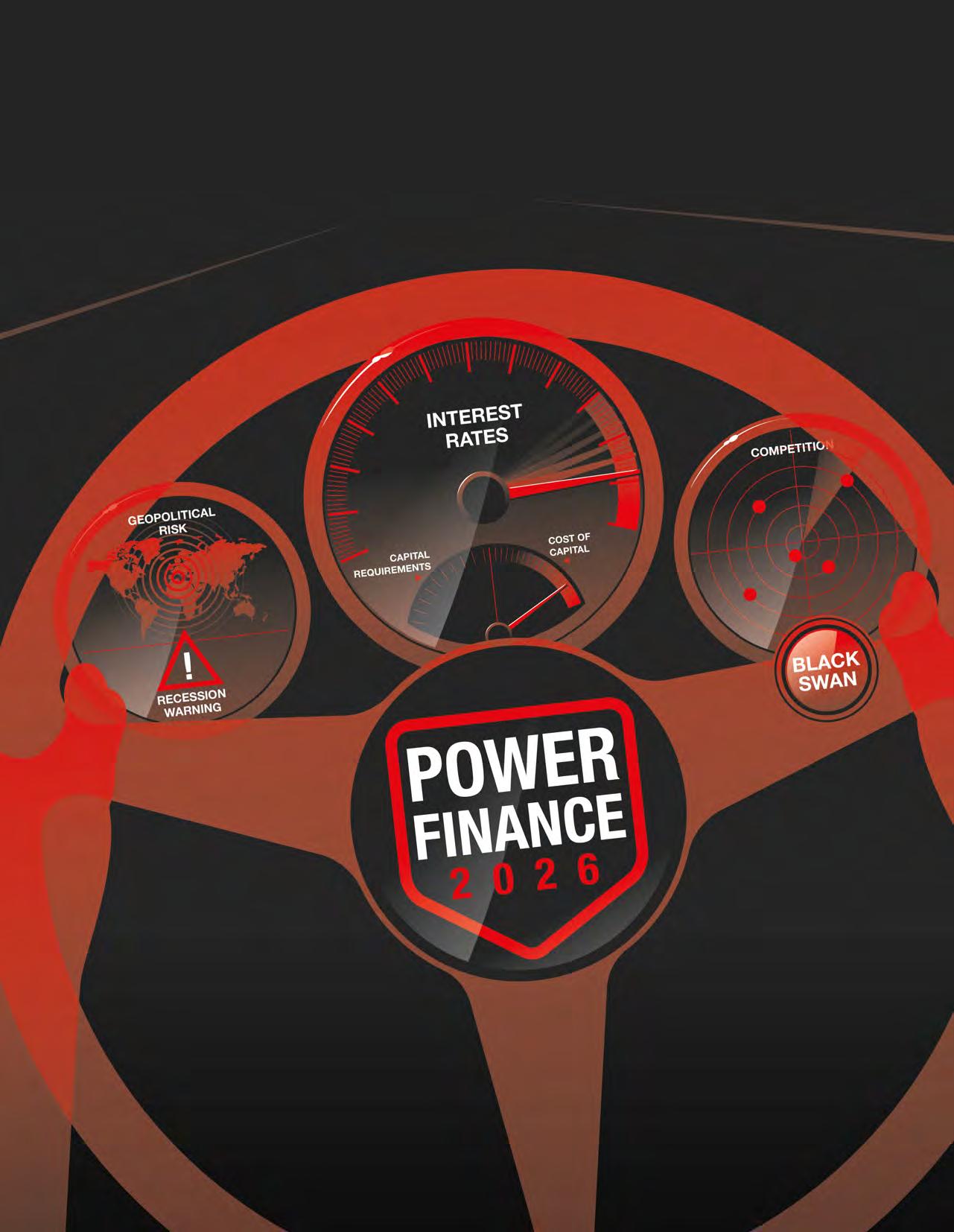

These lenders and debt brokers moved up sharply in the Power Finance rankings — while others made impressive debuts.

Max Gross Editor in Chief

Cathy Cunningham

Executive Editor

Tom Acitelli

Deputy Editor

Isabelle Durso New York Digital Editor

Greg Cornfield

Associate Editor

Skip Card

Copy Editor

Andrew Coen, Emily Davis, Julia Echikson, Mark Hallum, Brian Pascus, Amanda Schiavo Staff Writers

Larry Getlen

Contributing Editor

SALES

Brigitte Baron

Senior Partnerships Director Sona Hacherian

Strategic Account Director

Mark Rossman, Olivia Cottrell

Partnerships Director

Alina McInerney

Client Solutions Coordinator

These are the most influential lenders and debt brokers nationwide — and they’re working in one of the toughest markets in memory.

Fannie and Freddie Forgotten?

Here’s why the government-backed mortgage market giants did not make the Power Finance cut in 2026.

You Can Take It to the Bank Again

Disruptions and distress in recent years drove big, conventional banks to the commercial real estate sidelines. That’s all in the past.

Private credit lenders and funds are here to stay even as banks reclaim their share of the commercial real estate debt markets. L.A., Again With

The city’s downtown seems to be forever on the cusp of a sharp, post-pandemic comeback — why this time might be different.

MARKETING & EVENTS

Samantha Stahlman Director of Audience

Josh Rozbruch

Social Media Manager

DESIGN, PHOTO & PRODUCTION

Jeffrey Cuyubamba

Art Director

Rohini Chatterjee Senior Visual Designer

Jim Sewastynowicz

Photo Editor

Eliot Pierce SVP, Product & Operations

Ashley Roseman Director, Revenue Operations

Ramon Encarnacion IT Manager

OBSERVER MEDIA

Joseph Meyer Chairman

News

Penn Station Area Drawing Most Manhattan Office Relocations

A report last week from Cushman & Wakefield shows that almost a quarter of Manhattan office relocations in 2023, 2024 and 2025 ended up in the Pennsylvania Station submarket, and that most tenants relocated while expanding their space.

The report indicates that “between 2023 and 2025, more than 3.5 million square feet of relocations flowed into Penn Station, with the majority (83.2 percent) originating from neighboring Midtown submarkets.”

Financial services firms took 24 percent of this space, with professional services firms just behind at 23.7 percent, technology taking 18.8 percent, and media and information taking 10.7 percent. The remaining space was divided along categories that included media, legal, real estate, entertainment and more.

The report noted that 14 office buildings have been developed or renovated in the Penn Station submarket over the past decade, adding or augmenting around 23

million square feet of highly desirable office space, and expanding submarket inventory by 124.2 percent. These buildings have a current total vacancy rate of just 6.5 percent. For comparison, a separate C&W report pegged Manhattan’s overall vacancy rate at 19.9 percent by the end of March.

Lori Albert, director of tri-state research at C&W, said that this development has transformed the Penn District from an area littered with Class B and C office product to a submarket dominated by Class A space.

“Prior to this modernization of the area, there were only six Class A buildings in the Penn Station area. Now there are 20, and there’s less B and C,” said Albert. “Since Hudson Yards began in 2016, the whole area has been transformed, and then, in 2023, the renovations of Penn 1 and Penn 2 really modernized the area. It helped to alleviate a lot of overcrowdedness and just became very attractive to a lot of tenants.”

Class A space helped spur leasing.

Looking ahead, six additional conversions or new developments are currently in the works that will expand Class A inventory in the submarket by another 30.1 percent over the next seven years.

After Penn Station, the next most popular submarket for relocations has been Sixth Avenue/Rockefeller Center, with just under 2 million square feet over the report’s time period. Of the top five submarkets, only these two saw increasing relocation square footage over each of the three years.

C&W also noted that companies

Real estate investment firm Sovereign Partners was in contract last week to buy the 40-story Midtown office skyscraper at 575 Fifth Avenue from Beacon Capital Partners and MetLife

Will Silverman and Gary Phillips at Eastdil Secured had been marketing the 544,000-square-foot office building on the corner of East 47th Street and Fifth Avenue with a target price of at least $400 million.

The exact purchase price could not be learned, but it is believed to be closer to the $385 million that MetLife paid to developer Fred Wilpon’s Sterling Equities for the property in 2005, sources said.

The building was later divided into four condominium units in 2008. In 2015, MetLife sold a 50 percent stake to Beacon.

The property’s office portion — called Unit A — was reconfigured in 2015 to cover roughly 90 percent of the entire building, or around 504,000 square feet. Meanwhile, the retail units were also adjusted to account for roughly 40,000 square feet.

Eastdil — which was recently acquired by Savills in a $1.1 billion deal — was initially hired to sell the building in 2022 without the retail space, but had no success. That’s why the tower is now being sold along with the 40,000-square-foot retail space.

French sports fashion retailer Lacoste is currently open in 10,000 square feet at the building. According to a Lacoste executive’s LinkedIn post, the brand began

relocating to the Penn Station submarket are paying prime rates. Average asking rents there were 37.8 percent higher than the Midtown average, and overall vacancy was 3.1 percent lower.

The report also cited how companies relocating to the Penn District are “significantly more likely to expand their footprint rather than consolidate,” bucking current trends toward smaller leases

Albert credited the larger footprints to the availability of larger blocks of space in the Penn submarket. —Larry Getlen

negotiations in September 2022 and signed a lease in September 2023 for possession in July 2024. It finally opened its immersive flagship just one year ago on April 10, 2025.

The building is leased by Cushman & Wakefield, with its website showing less than 25,000 square feet available in three to four smaller spaces. The building was 87 percent occupied as of September, The Real Deal reported at the time

The building’s amenities include three conference rooms, a lounge and café, an on-site Starbucks, a central atrium and a bike storage area that includes lockers and showers. There is even a beehive on the roof through a partnership with the Boston-based Best Bees

It is yet unclear if the bees will have to swarm elsewhere or if Sovereign will continue the association with the honey makers.

Sovereign Partners is headed by brothers Darius and Cyrus Sakhai and includes William Gentile and Darius’s son Stephan. The brothers have been responsible for investing in 20 million square feet of office, multifamily and retail space across the U.S.

They moved from England to America in the 1980s and later acquired properties in the Southeast during the savings and loan crisis while managing the family portfolio.

None of the parties involved in the deal at 575 Fifth Avenue responded to requests for comment. —Lois Weiss

STATION MASTER: Proximity to the transit hub and fresh

DEAL DOERS: Gary Phillips (l) and Will Silverman.

Newmark Hires ExCitigroup Director to Expand Data Center Investment

Newmark hired Philip O’Bannon to lead its infrastructure capital markets business.

O’Bannon, previously a director at Citigroup, will focus on fast-growing investments for Newmark, such as data centers, energy transition assets, power and utilities, and other large-scale infrastructure sectors, according to an April 14 announcement from Newmark.

O’Bannon is equipped with more than 20 years of experience in investment banking and engineering.

As senior managing director, O’Bannon will lead the business in expanding advisory and capital-raising capabilities across the firm’s full infrastructure investment spectrum.

O’Bannon, who began his new role in March, reports to Andrew Warin, head of strategic advisory at Newmark.

O’Bannon is positioned to work closely with Newmark’s debt and structured finance and data center capital markets teams.

Citigroup declined to comment.

Emily Davis

Manhattan Investment Sales in First Quarter Strongest Since 2021

During the first quarter of 2026, Manhattan investment sales — including deals in the multifamily, office, retail, development and conversions sectors — grew by 33 percent quarter-over-quarter, totaling $3.7 billion across 92 transactions, according to a report last week from Avison Young

That was the strongest quarterly performance since 2021. And, going off that success, Manhattan’s total predicted dollar sales volume for 2026 is $14.8 billion, a 23 percent year-over-year growth when compared to 2025’s total. (Avison Young projects full-year totals based on first-quarter activity.)

“Manhattan really, really jumped off the charts,” said Brandon Polakoff, principal and head of New York investment sales at Avison Young. “This echoes what we are seeing in the market, where there is this flight to quality assets in A-plus-plus locations.”

Multifamily property sales in Manhattan hit a total of $1.07 billion in the first quarter of 2026, a 246 percent quarter-over-quarter rise across 44 deals. Multifamily sales are set to reach $4.3 billion by year’s end, a 145 percent increase compared to 2025.

Looking at New York City as a whole, Avison Young found that total dollar sales volume for the first quarter hit $5.68 billion, a 23 percent quarterly rise, across 182 total sales in all five boroughs. In all of New York City, the estimated total dollar volume for sales in 2026 is $22.71 billion, according to Avison Young, which is slightly below the 10-year average of $23.4 billion.

A lot of that activity is set to be led by the office market, which captured the most capital in the first quarter with $1.8 billion in total dollar volume across 22 sales in the city, according to the report. —Amanda Schiavo

Adam America Real Estate Picks David Brickman as CEO

Adam America Real Estate announced April 15 that it has hired David Brickman as CEO. Brickman will quarterback the New York multifamily investment and development firm’s long-term growth strategy and its investment and development platforms.

Brickman comes over from Onex Real Estate Partners and Skyview Companies, where he was a partner at each firm over the last 15 years.

Brickman told Commercial Observer that he has known the principals at Adam America, primarily Dvir Cohen Hoshen, for several years, and the parties began discussions a few months ago about bringing him on board.

“I was finishing up a project in Florida, they were wrapping up a few projects and looking for a management change with new leadership, they reached out, and the rest is history,” he said.

Brickman added, “There’s a comfort level with the founders and partners that I had, and I was very impressed with their pipeline and track record.”

Adam America Real Estate was founded in 2009 and has developed more than 5,750 residential units in the last 17 years. The firm currently has a portfolio valued at $4.2 billion, with an additional 1,600 units in its pipeline, which encompasses national multifamily and condominiums, as well as student housing and build-to-rent (BTR) projects.

Brickman believes the firm has established itself in multifamily and condos and is poised to take further hold of the student housing and BTR subsectors, bringing the firm into a third phase of its evolution.

“We’re really experts in living-sector development, and where we have been successful is developing condos and [multifamily] for two decades,” he explained. “Now over the last five years, we’ve leaned into student housing and buildto-rent development, we’ve successfully executed those, and our vision for our company going forward is leaning into those new sectors.” —Brian Pascus

Fisher Brothers Taps Former RFR Exec to Lead Capital Markets

Jonathan Frey, formerly head of debt capital markets at RFR Holding, joined Fisher Brothers in late March as the firm’s new managing director of capital markets.

Frey is tasked with advancing the firm’s capital markets strategy and supporting its continued portfolio growth. Fisher Brothers owns and operates commercial, residential and experiential retail assets in New York City, Las Vegas, Miami and Washington, D.C. The company recently secured $117.5 million to refinance a newly completed multifamily building in Miami’s Wynwood neighborhood.

Fisher’s $6.1 billion assets under management span more than 1,500 multifamily units and $1.4 billion worth of new developments since 2014, per its website.

Frey joins the firm after a more than three-year stint at RFR Holding, preceded by lengthy tenures at Pyramid Management Group and Morgan Stanley. Throughout his career, Frey has led billions of dollars in financing transactions across multiple asset classes, according to Fisher Brothers. Frey’s arrival was quickly followed by that of Kent Williams, Fisher Brothers’ new chief accounting officer. Williams joined the firm this month from his previous role as controller at East End Capital —E.D.

FAR AND WIDE: The strong investment figures extended to Brooklyn.

ADAM’S APPLE: Brickman says he’ll focus on build-to-rent and student housing.

C. TAYLOR CROTHERS/GETTY IMAGES

Charlie Rose

Managing Director Global Head of Real Estate Credit CEO of INCREF

Teresa Zien Managing Director Portfolio Manager, North America http://www.invesco.com/real-estate

Yorick Starr Managing Director Investment Officer, North America

Justin Chausse Managing Director Credit Investments, North America

Mattress Company Avocado Takes Over Entirety of 942 Third Avenue Retail

Avocado Green Mattress, a California-based mattress company specializing in eco-friendly and nontoxic mattresses, leased the entire five-story, 12,000-square-foot retail townhouse at 942 Third Avenue for a new vertical flagship.

The asking rent was $750,000 per year for the new deal in Midtown East, an area known for its design and furniture brands. The neighborhood is anchored by the nearby Decoration & Design Building and Architects & Designers Building

Previously, 942 Third Avenue, a highly visible site that sits between East 56th and East 57th streets, was occupied by Modani Furniture

Since the building is not landmarked, it provides an opportunity for expansive branding and signage for Avocado, which will also have the use of the building’s basement space.

The length of the new deal was unclear. Avocado was represented by Alex Yanoff of Brand Urban and Tess Jacoby of Rue, while Retail by MONA’s Brandon L. Singer, Sunny Woo and Jason Lloyd represented the building ownership, married couple Naomi and Andre Altholz

“This transaction reflects a broader shift in how brands are thinking about physical space,” said Singer, founder and CEO of Retail by MONA. “Avocado recognized the opportunity to create a vertically integrated flagship that goes beyond traditional retail and serves as an immersive brand environment.”

Founded in 2016, the mattress company already has brand outposts in Manhattan’s Flatiron District at 135 Fifth Avenue and in Williamsburg, Brooklyn, at 57 North Sixth Street. The mattresses are also sold through other furniture retailers. —Lois Weiss

Health Food Brand Nut Bar to Open First U.S. Location in New York City

Nut Bar, a Toronto-based health food brand with six locations in the Canadian city, is set to open its first U.S. location in New York City this fall, having signed a 10-year, 2,500-square-foot lease at 28 Greenwich Avenue in Greenwich Village.

The retail space comprises 1,100 square feet on the ground floor and 1,400 square feet on the lower level, according to RTL Real Estate, which brokered the lease on behalf of landlord the Brodsky Organization. The asking rent was around $25,000 per month, according to RTL.

“The location will serve as the brand’s first U.S. outpost, introducing its healthfocused concept to a neighborhood supported by a strong daytime and residential customer base,” RTL said in a statement announcing the lease.

It seems like Nut Bar will replace bakery Mah-ZeDahr in its new space between West 10th and West 11th streets, as the bakery is listed as permanently closed at the property.

Charles Rapuano and Steven Baker of RTL represented the Brodsky Organization in Nut Bar’s deal, while Aylin Gucalp and Cassie Durand of CBRE represented the tenant. CBRE did not respond to a request for comment.

“Demand continues to concentrate around highly visible corners in established neighborhoods, where retailers can immediately tap into existing foot traffic and co-tenancy,” RTL’s Rapuano said in a statement.

Amanda Schiavo

Urban Outfitters to Open 15K-SF Store at 575 Fifth Avenue

Clothing retailer Urban Outfitters is moving one of its stores a few blocks uptown to 575 Fifth Avenue

The popular clothing store chain, owned by retail brand corporation Urbn, is currently in 22,238 square feet at 521 Fifth Avenue

Urban Outfitters will relocate that store to its new 15,345-squarefoot space at 575 Fifth Avenue, on the corner of East 47th Street and Fifth Avenue.

News of the relocation comes as the 40-story office tower at 575 Fifth Avenue enters into new ownership. Real estate investment firm Sovereign Partners is in contract to buy the 544,000-squarefoot property from Beacon Capital Partners and MetLife for around $385 million.

Tim Duffy of the McDevitt Company represented Urban Outfitters in the store deal, while Cushman & Wakefield’s Sean Moran, Patrick O’Rourke, Steven Soutendijk and Catherine Merck brokered the deal for building ownership.

The C&W team that represented the building was able to incorporate a former L’Oreal lower-level cafeteria spanning 12,574 square feet into the ground floor’s 2,771-square-foot retail space.

The retail asking rent at 575 Fifth Avenue was $3 million per year, which breaks down to around $625 per square foot for the ground floor and $100 per square foot for the lower level.

The 12-year term also aligns with the end of the lease for the building’s corner retailer, French sports fashion brand Lacoste Work has already begun on the space, with delivery to Urban Outfitters expected this summer for their own buildout as they target an opening in the first quarter of 2027.

Urban Outfitters was also able to extend its deal at 521 Fifth Avenue through that first quarter to align with this strategy. It was also made easier as Soutendijk, Moran and O’Rourke represent 521 Fifth Avenue.

The current retail asking rent at 521 Fifth Avenue is $500 per square foot for the ground floor and $125 per square foot for the second floor. —L.W.

COUNTERINTUITIVE

NYC Commercial Rent Regulation Will Hurt the Businesses It Aims to Protect

As the New York State Legislature considers legislation to impose rent regulation on commercial properties, the proposal is gaining attention as a potential lifeline for small businesses. It may sound like a solution. It isn’t.

After more than four decades working across nearly every corner of New York’s retail ecosystem — as a broker, an attorney, a landlord and a tenant — I can say with confidence: This proposal is likely to do more harm than good. I don’t take that position lightly. I currently own and operate retail businesses in Brooklyn and have previously been part owner of multiple food establishments in New York City. I’ve sat on both sides of the table. And, even as a tenant, I oppose this legislation.

In my own experience, the landlord-tenant relationship — when both parties are operating in good faith — functions effectively. As a tenant, I’ve always paid rent on time and run strong businesses. In return, my landlords have consistently renewed my leases at reasonable terms. The only time I was not renewed was when a landlord chose to redevelop — a legitimate and necessary part of maintaining and improving the city’s building stock. That’s not a broken system. That’s a functioning one. Ironically, the businesses this legislation aims to protect may be the ones most negatively impacted.

If property owners lose flexibility at the end of a lease, they will become more cautious about who they rent to in the first place. Mom-and-pop tenants — who often carry more risk than national operators — may find themselves shut out before they even get started.

It also disrupts something essential to a healthy retail ecosystem: turnover. Not all turnover is bad. In fact, it’s what allows new businesses to enter the market, test

HOME TRUTHS

concepts and grow.

Restricting that natural cycle makes it harder — not easier — for new entrepreneurs to find space.

As someone actively leasing space for my own businesses, I can say plainly: This kind of legislation could make it harder for operators like me to secure locations.

From the ownership side, the logic is equally straightforward. Good tenants — those who pay on time and operate responsibly — are valuable and are typically renewed. Problematic tenants are not. That discretion matters. Buildings are ecosystems. One poorly run business can impact an entire property. Owners need the ability to make decisions that protect the long-term health of their assets. In over 40 years, I can’t recall a situation where I couldn’t reach a fair agreement with a good tenant. The current system already rewards stability and performance.

There’s also a broader financial reality that can’t be ignored.

Many rent-regulated residential buildings in New York City rely heavily on ground-floor retail income to remain viable. If you cap or suppress retail rents, you’re not just affecting storefronts — you’re putting additional pressure on already strained housing assets. That translates directly into lower property values. And when property values decline, so do tax revenues.

Real estate taxes often account for 25 percent to 35 percent of a building’s rent roll. Reduce retail income, and

you reduce assessed values. Reduce assessed values, and you shrink the tax base.

At a time when New York City is facing significant fiscal challenges, this is not a small issue. It’s a structural one. Neighborhoods are not static. They evolve — and retail must evolve with them.

Property owners play a key role in that process by curating and upgrading tenant mixes over time. Limiting that flexibility risks locking neighborhoods into outdated retail patterns, ultimately making commercial corridors less vibrant and less competitive. That’s not preservation. That’s stagnation.

Finally, there’s the practical reality: This will be litigated. Heavily.

Any system that introduces rent regulation into the commercial sector will create disputes, ambiguity and delay. The result? More legal costs, more friction and more uncertainty — for both landlords and tenants. The biggest winners won’t be small businesses. They’ll be attorneys.

Lawmakers’ efforts are well intentioned. But policy needs to be judged by outcomes, not intentions. This proposal risks reducing opportunities for small businesses, weakening property values, straining the city’s tax base, and creating a more rigid, less dynamic retail environment.

New York’s retail landscape doesn’t need more constraints. It needs flexibility, investment and the ability to adapt. This legislation moves us in the wrong direction.

James Wacht is managing principal at Lee & Associates NYC.

New York’s Housing Connect Lottery System Urgently Needs Reform

In 2024, the NYC Housing Connect lottery system received approximately 6 million applications for roughly 10,000 available affordable units. Competition was so fierce that each applicant had just a 0.2 percent chance of securing a place to call home.

This online portal, created to streamline the process for applicants and create a more equitable one-stop shop for application management, is clearly overwhelmed. Although the system may now be easier for city agencies to manage, it continues to create frustration, inefficiency and lost opportunities for tenants and property owners.

Units sit empty while families and individuals wait for housing, paperwork piles up, and opaque processes slow the very system that was designed to deliver homes. After years of incremental changes, Housing Connect is long overdue for comprehensive reforms that ensure it works efficiently, transparently and fairly for everyone involved.

The human cost of the system’s inefficiencies is stark.

A recent case study by the New York Housing Conference found that it took 27 months to lease 180 newly constructed affordable apartments in the Bronx — including 18 months after the lottery had closed — even after the building had a temporary certificate of occupancy and was safe for residents to inhabit.

Tens of thousands of applications were generated, yet troubling bottlenecks in eligibility review and documentation slowed every step of the process, causing would-be tenants to wait more than two years for desperately needed, high-quality new units.

This isn’t just an abstract bureaucratic quirk. It takes nearly four times longer to lease affordable housing units in New York City compared to units financed by other housing

agencies statewide and across the country.

Delays caused by extended lease-up timelines reduced the financial stability of city affordable housing projects by an estimated $4.6 million between 2019 and 2024, or roughly $386,000 per impacted development. Building owners are forced to cover these unexpected gaps with additional financing or subsidies, further straining public resources and slowing future development.

The goals of improving Housing Connect are shared across city government and within the affordable housing community. But success requires coordination — not just within the Department of Housing Preservation and Development (HPD), but citywide. Clarifying responsibility and minimizing unnecessary steps between city agencies would immediately improve outcomes for renters and owners alike.

Modern problems demand modern tools. The digital infrastructure that supports Housing Connect must be upgraded, so applications can be processed quickly and intelligently. Imagine a platform in which applicants upload verification documents once and reuse them across multiple opportunities, where redundant income certifications disappear, and where unnecessary pre-lease reviews are eliminated without undermining compliance.

Automation, real-time status updates, and a centralized repository for documentation would reduce back-andforth for families and staff and keep the process moving. Reforming the system also means rethinking how units

are marketed and filled. Units should be made available to all applicant types in parallel, verification timelines should be streamlined, and applicants should be limited to one unit size per building to reduce administrative bottlenecks.

A system in which applicants can hold multiple overlapping offers creates confusion and slows occupancy. Clear consequences for unwarranted refusals and an end to openended appeals would incentivize accountability and speed decision-making.

We must also simplify the requirements placed on applicants. Many documentation burdens — from asset verification to digital wallet account statements — are onerous, offer little insight into actual eligibility, and discourage families from applying in the first place.

Voucher holders and unhoused individuals deserve a process that moves at the pace of urgency, not bureaucracy. Property managers should be empowered to accept direct referrals from shelters to expedite placements.

These are practical reforms that would have an immediate impact on families in need.

Affordable housing is a shared mission, and every delay is yet one more day that an individual or family goes without a home. The New York State Association for Affordable Housing is fully committed to being a partner in this effort. We believe that with collaboration, innovation and determination, Housing Connect can finally deliver on its promise of fairness, efficiency and expedience for all New Yorkers.

Carlina Rivera is president and CEO of the New York State Association for Affordable Housing and a former member of the New York City Council from Manhattan.

Carlina Rivera.

James Wacht.

Office Leases of the Week

A platform company within the Apollo Global Management umbrella inked a 10-year, nearly 50,000-square-foot office lease across two full floors at 590 Madison Avenue

The deal comes after Apollo, an alternative asset management firm, finalized a nearly 100,000-square-foot lease last April at the RXR-owned building, spanning the 10th through 13th floors. The new lease will cover

Eldridge Industries

Eldridge Industries, a Miami-based asset management and insurance holding company owned by billionaire businessman Todd Boehly, signed a roughly 20,000-square-foot lease at 125 West 57th Street on Billionaires’ Row in Midtown.

The 30-story office tower is owned by Alchemy-ABR Investment Partners and Cain International. The length of the lease and the asking rent were not disclosed, but

the entire 14th and 15th floors.

This new lease will be part of an initiative to consolidate Apollo’s New York City employee headcount within 590 Madison and its headquarters at 9 West 57th Street, according to a source. Apollo will relocate employees to 590 Madison from 3 Bryant Park, and it will continue to move over employees part of its platform companies from current offices at 1350 and 1370 Avenue of the Americas

The exact asking rent was not disclosed, but the source did note that the asking rent would be “north of $120 per square foot.”

RXR’s William Elder and Daniel Birney handled the deal in-house, while Michael

the average asking rent for office space in Midtown during the first quarter of 2026 was $81.43 per square foot, according to a report from Newmark. In fact, the average office asking rent along Billionaires’ Row can exceed $300 per square foot, according to data from New York Offices

The asking rent certainly exceeded $300 per square foot at the nearby Soloviev Groupowned 9 West 57th Street, which signed a “record-setting lease deal” in early April at $327.50 per square foot. Gonzalo Hevia Baillères, the grandson of late businessman Alberto Baillères González, signed a 10-year,

Wellen, Michael Geoghegan and Stephen Siegel from CBRE represented the tenant.

“As a premier Midtown asset, 590 Madison offers the quality, location and tenant experience that today’s leading companies demand, and we look forward to building on this momentum,” Elder said in a statement.

The name of the Apollo affiliate that signed the new lease was not disclosed.

Spokespeople for CBRE and Apollo did not respond to requests for comment. — Amanda Schiavo

Global architecture and design firm Populous is securing its foundations at RXR’s Starrett-Lehigh Building

The design outfit opted to renew its current 10,158-square-foot lease by another three years at 601 West 26th Street and tack on another 6,500 square feet for seven years, according to the landlord. The transaction brings Populous’ total footprint at the 19-story Chelsea office building to 16,658 square feet on the 14th floor.

CFC USA

13,065 Relocation

CFC USA, the U.S. arm of a London-based specialist insurance provider for cybersecurity protection, signed a 13,065-square-foot lease at Haymes Investment Company’s 5 Penn Plaza in Midtown.

The seven-year deal represents a relocation for CFC USA, which currently has its New York City offices at 48 Wall Street in the Financial District. It’s unclear when the insurance firm will make the move to its new office on the second floor of 5 Penn.

Populous is known for designing major sports and entertainment venues such as Las Vegas’ The Sphere, New York City’s Citi Field and Yankee Stadium, and London’s Wembley Stadium

RXR’s Denise Rivera represented the landlord in-house, while Populous did not work with a broker. The parties declined to disclose asking rents, but Chelsea office asking rents averaged $82.27 per square foot in the first quarter of 2026, according to Cushman & Wakefield data.

“We’ve reached an exciting milestone where we’ve outgrown our current space, and there was never any question about

The asking rent was not disclosed, but the average asking rent for office space in Midtown was $84.74 per square foot in the first quarter of 2026, according to data from Colliers

“We’re thrilled to welcome CFC to 5 Penn,” Stephen Haymes, managing partner at Haymes Investment, said in a statement. “Their decision to lease space here shows how strongly the building is resonating with tenants and reflects the continued demand we are seeing from growth-oriented companies seeking a high-quality, well-located workplace.”

Joseph DeRosa and Taylor Walker of

5,063-square-foot lease on the 50th floor. Alchemy and Cain declined to comment, while a spokesperson for Eldridge Industries did not respond to a request for comment.

Completed in early 2026, 125 West 57th Street spans 173,000 square feet and features a Gensler-designed amenity floor with a lounge, a coffee area and private phone booths.

“There hasn’t been a new office building built in this market in decades, and we thought it’d be a good idea,” Brian Ray, managing partner and co-founder of AlchemyABR, previously told CO about developing an office asset on Billionaires’ Row. —A.S.

where we wanted to expand,” Jonathan Mallie, Populous’ global director, said in a statement.

Populous arrived at the landmarked office property in 2019 from its previous home at 475 Madison Avenue

“RXR is very pleased that Starrett-Lehigh has such a diverse and creative roster of tenants, including Populous,” William Elder, executive vice president and managing director of RXR’s New York City division, said in a statement. “We look forward to their continued tenancy.” — Emily Davis

CBRE represented the tenant, while JLL’s Mitch Konsker, Kristen Morgan, Christine Colley, Greg Wang, Dan Turkewitz and Kate Roush represented building ownership.

“5 Penn anticipated the demands of tenants today with a hospitality-level amenity platform that prioritizes wellness, collaboration and tenant experience,” Konsker said in a statement. “Our recent leasing success is evidence that putting people at the center of workplace design truly drives demand.”

Tenants at 5 Penn include crypto security firm Fireblocks and SiriusXM Radio —A.S.

Office Leases of the Week

Private Export Funding Corporation

9,577 Relocation

Financial institution Private Export

Funding Corporation (PEFCO) moved to a 9,577-square-foot office at Jack Resnick & Sons’ 880 Third Avenue in Midtown East.

PEFCO, which provides financing for exports from the U.S., signed a 13-year lease across the 18-story office building’s entire ninth floor, according to Resnick. The firm relocated to its new space last month from its previous spot 11 blocks away at 675 Third

Nonprofit Finance Fund

Avenue

Bradford Allen’s Gordon Ogden and Ava Beganovic represented PEFCO in the transaction, while Resnick was represented in-house by Brett Greenberg and Adam Rappaport

PEFCO also received the benefit of a termination fee from its previous landlord, Ogden told Commercial Observer.

“They gained the efficiency of a new full floor, to reposition their business over a transit node at East 53rd Street and Lexington and Third Avenue,” Ogdon said. “They are excited to have Resnick as their new landlord.”

Resnick did not disclose asking rents, but office asking rents in Midtown averaged

$84.74 per square foot in the first quarter of 2026, according to a Colliers market report. Other office tenants at the Plaza District office building include Columbia University, financial planner Beech Hill Securities and investment firm EOS Management. Retail space at the property is anchored by TD Bank, Gregorys Coffee and Pret a Manger —E.D.

There were several new deals completed at Jack Resnick & Sons’ 18-story office building at 880 Third Avenue in Midtown East last week. In addition to financial institution

Private Export Funding Corporation’s deal for 9,577 square feet on the building’s entire ninth floor, Nonprofit Finance Fund signed a 12-year lease for 8,393 square feet across the entire 12th floor of the property, according to the landlord.

FHS Risk Management

6,655 Renewal

In yet another deal at Jack Resnick & Sons’ 880 Third Avenue in Midtown East last week, insurance consulting firm FHS Risk Management renewed its offices at the 18-story building between East 53rd and East 54th streets.

FHS, which provides outsourced risk management, insurance consulting and claims advocacy for the real estate, construction and hospitality industries, signed a seven-year lease extension for its 6,655 square

8,393 Relocation Raiden Electric

6,577 Relocation

Raiden Electric, a privately owned local union electrical contractor, is moving its offices uptown to AFIAA’s 45 West 45th Street in Midtown.

The contractor inked a 10-year lease for 6,577 square feet, which spans the entire 15th floor of the 16-story Midtown office tower, according to tenant broker Avison Young Alan Zengo, principal at Raiden Electric, told Commercial Observer that the new lease at 45 West 45th Street reflects the company’s continued growth and long-term

Founded in 1980, Nonprofit Finance Fund aims to help nonprofits strengthen their financial resources to deliver social impact, according to its website. The company will relocate to 880 Third Avenue this summer from 5 Hanover Square in the Financial District.

Resnick did not provide the asking rent, but office asking rents in Midtown averaged $81.43 per square foot in the first quarter of 2026, according to Newmark data.

Open Impact Real Estate’s Lindsay Orenstein, Stephen Powers and Sasha Perlov represented the tenant, while Resnick was represented in-house by Brett

feet on the 14th floor of the property, according to Resnick.

Founded in 1995, FHS has been a tenant at 880 Third Avenue for more than two decades, the landlord said.

Savills’ Zev Holzman and Jordan Kaliner represented the tenant in its renewal, while Resnick was represented in-house by Brett Greenberg and Adam Rappaport

Jonathan Resnick, president of Jack Resnick & Sons, said the landlord is “pleased” to continue its “long-standing relationship with FHS.” He added that the transaction reflects “the resurgence of the Third

commitment to the city.

“As our team and project portfolio expand, this space will support our operations and allow us to better serve our clients across the region,” Zengo said in a statement. “We expect to begin our transition in the coming months.”

Cushman & Wakefield’s Harley Dalton, Pierce Hance and Samantha Perlman represented landlord AFIAA in the negotiations, while Avison Young’s Patrick Steffens, Martin Cottingham and Michael Gottlieb worked on behalf of Raiden Electric.

The deal marks a relocation and expansion for Raiden Electric, as the organization is currently located at 11 Broadway in the

Greenberg and Adam Rappaport

“We’re pleased to have Nonprofit Finance Fund make 880 Third its new home,” Jonathan Resnick, president of Jack Resnick & Sons, said in a statement. “This transaction reflects the resurgence of the Third Avenue corridor and the overall strength of the Midtown office market.”

Resnick’s Manhattan portfolio currently includes over 5 million square feet of commercial office and retail space, according to the firm. Spokespeople for Nonprofit Finance Fund and Open Impact did not respond to requests for comment. —E.D.

Avenue corridor and the overall strength of the Midtown office market.”

Resnick did not provide the asking rent for the renewal, but office asking rents in Midtown averaged $84.74 per square foot in the first quarter of 2026, according to a report from Colliers

Spokespeople for FHS and Savills did not respond to requests for comment. —E.D.

Financial District.

Avison Young declined to disclose the asking rent for the new space, but overall Midtown office asking rents averaged $76.96 per square foot in the first quarter of 2026, according to C&W data.

AFIAA purchased 45 West 45th Street in 2019 for more than $125 million from Vanbarton Group. Office tenants include health care marketing firm 120/80 Group —E.D.

PARTNERINSIGHTS

Navigating Complexity: Walker & Dunlop Closes $23.8B Across 158 Deals

In today’s commercial real estate market, capital hasn’t disappeared—it’s become more disciplined: prioritizing structure, certainty, and luxury-quality assets with resilient cash flow and long-term value.

Transactions that once moved efficiently now require deeper analysis, tighter execution, and greater alignment between sponsors and capital providers. In this environment, the ability to structure and close a deal has become just as important as sourcing the capital itself.

Walker & Dunlop Capital Markets Institutional Advisory, led out of New York by Senior Managing Directors Aaron Appel, Keith Kurland, Jonathan Schwartz, Adam Schwartz, Sean Reimer, and Dustin Stolly, has been operating squarely on that principle. Over the past year, the team has advised on and/or closed $23.8 billion of debt and equity transactions across 158 deals nationwide.

“Execution is what defines this market,” says Appel. “Capital is out there, but getting a transaction from start to finish requires a much more deliberate and structured approach than it did in prior cycles.”

A Market Where Precision Matters

Liquidity remains in the system, but it is increasingly disciplined. Lenders are more selective, and capital providers are focused on sponsorship, basis, and long-term viability.

This results in a fragmented landscape—one where capital is abundant, but quality is sought after.

Walker & Dunlop has remained active across all major asset classes, including multifamily, office and office-to-residential conversions, industrial, hospitality, and large-scale development. Over the past year, the team has worked with more than 75 capital providers and over 100 clients, aligning transactions with the right capital sources in a highly selective market.

“There’s still significant capital looking to be deployed,” says Kurland. “But it has to be the right deal, with the right structure, at the right basis. That’s where we’re spending our time.”

Executing Across Some of the Market’s Most Complex Transactions

Even amid market headwinds, Walker & Dunlop has continued to execute on large, highly structured transactions across the country.

The Institutional Advisory team arranged a $778.6 million construction loan for the conversion of 111 Wall Street in Manhattan, the largest single-building office-to-residential conversion financing completed in New York City at the time. The assignment also included an $88.4 million C-PACE extension, bringing total capitalization to $867 million and requiring coordination across construction risk, adaptive reuse underwriting, and sustainability financing.

In Miami, the team closed a $464.5 million acquisition and predevelopment loan for a site on the water in Brickell, the largest land acquisition financing ever completed in the market, structured around complex entitlement and future

development considerations.

In Brooklyn, Walker & Dunlop arranged a $285 million bridge loan for Greenpoint Central, a newly built multifamily asset incorporating both market-rate and affordable housing units. In Newark, the team structured a fully integrated capital stack for 22 Fulton Street, combining construction financing, tax credit equity, preferred equity, and a forward permanent loan within a Qualified Opportunity Zone development.

“These transactions require a different level of coordination today,” says Stolly. “You’re working across multiple capital sources and solving for risk in real time. That’s where experience becomes critical.”

Hospitality: Opportunity with a Higher Bar for Execution Hospitality has re-emerged as an area of investor interest, but it remains one of the most execution-sensitive sectors in today’s market.

Walker & Dunlop recently arranged $371.5 million in financing for The Nashville EDITION Hotel & Residences, a 28-story development combining a luxury hotel with branded residential units. The transaction required alignment between real estate fundamentals and hotel operations, along with institutional capital to underwrite a mixed-use hospitality asset.

“Hospitality is performing, particularly in high-growth markets, but it requires a much more nuanced underwriting approach,” says Jay Morrow, senior managing director of Hospitality at Walker & Dunlop. “You have to understand both the real estate and the operating business to get these deals financed.”

Morrow adds that capital remains active in the sector, but far more selective than in prior years. “There’s strong interest, but execution comes down to how well the deal is positioned and structured. That’s where we’re focused.”

Structuring Capital for Today’s Environment

Across all asset classes, capital structures are layered and increasingly strategic. Transactions require combinations of senior debt, preferred equity, mezzanine capital, and alternative financing tools.

Walker & Dunlop’s Institutional Advisory team has focused on delivering solutions that reflect these dynamics—structuring capital stacks that are both executable and aligned with long-term asset performance.

“Our clients are navigating more complexity than ever before,” says Jonathan Schwartz. “Our role is to bring clarity to that process and deliver a structure that actually works in today’s market.”

Positioned for What’s Ahead

As the market continues to recalibrate, opportunities are emerging through repricing, refinancing needs, and capital dislocation. Sponsors with access to flexible financing solutions are increasingly well positioned to act on those opportunities.

“We’re in a market where experience and execution matter more than ever,” says Adam Schwartz. “There’s capital available, and there are opportunities—but connecting the two requires a very intentional approach.”

With $23.8 billion in transaction volume over the past year and a team actively executing across asset classes and markets, Walker & Dunlop Capital Markets Institutional Advisory continues to play a leading role in helping clients navigate complexity and close deals in a challenging environment.

2026

It takes a lot of drive

ne sort of feels that, to navigate the finance landscape in 2026, one needs to have the dexterity of Mario Andretti.

Certainly, there is the need for speed. Private lenders have been tearing up the fast lane for years. Likewise, banks — after a very long time in first gear — decided last year that they also wanted to feel the rush.

If you were a borrower, you had an abundance of choice. The economy seemed to be humming. Liberation Day tariffs didn’t bite as hard as some feared. Job growth seemed more or less steady. There was demand for housing. Retail seemed to have turned around. The words “data centers” and “industrial outdoor storage” lit a fire in many eyes.

But then…

One after another, obstacles started appearing on the road. The chairman of the Federal Reserve was put under investigation by the Department of Justice for seemingly political reasons. Dreams of a big interest rate cut were dashed. The Persian Gulf exploded, and the inflation warning light on everyone’s dashboard went berserk. Recession looked much more plausible than it did six months ago.

Yet the lenders on this year’s Power Finance have steered their

way through crises before. And they can smell opportunity like it’s high octane.

Just look at what they did last year: There was the $10 billion worth of business that Starwood’s Jeff DiModica, Lorcain Egan and Dennis Schuh completed, including for a $500 million data center in Utah and a $500 million industrial portfolio in New York.

There’s the $23 billion that Blackstone originated on deals spanning the planet, including the United Kingdom’s very first CMBS deal.

Or there’s the $87 billion J.P. Morgan Chase injected into the debt market last year — we told you banks were back. (Chase was the lender Blackstone turned to when they wanted to finance the $3.98 billion purchase of Safe Harbor Marinas. They’re the lender’s lender.)

All the while, the wheeling and dealing has been facilitated by a ground crew of brokers and special servicers who not only beat previous records last year, but who have been quietly gearing up for the properties hitting walls of pending maturity.

But, to a certain extent, we don’t want to tease too much. Let our rankings and write-ups tell the story. These are the drivers of real estate finance — and they are revving up for more.

This package was written by Andrew Coen, Cathy Cunningham, Larry Getlen, Brian Pascus, Zoe Rosenberg, Amanda Schiavo and Patrick Sisson. It was edited by Cunningham, Tom Acitelli and Max Gross. Skip Card copy-edited it. Jim Sewastynowicz edited the photos, and Jeff Cuyubamba designed it.

1Michelle Herrick and Brian Baker Head of commercial real estate at J.P. Morgan Chase (commercial banking); global head of commercial mortgages at J.P. Morgan Securities (global investment banking)

Last year’s rank: 4

There are heavy hitters, and then there are heavy hitters.

Last year, J.P. Morgan originated a hefty $87 billion in loans. Further, in a market that ebbed and flowed, the firm remained a constant, stalwart lending force, providing liquidity to borrowers and communities from coast to coast, while also not shying away from complex financings or large-ticket deals.

Competition and volatility largely defined the past year, but J.P. Morgan didn’t waiver, leaning into its client relationships and partnerships, and acting as a strategic adviser while delivering certainty, speed of execution, creativity and the full strength of its balance sheet to borrowers big and small.

As such, “momentum” is the word Michelle Herrick would use to describe this past year, both for the industry and J.P. Morgan’s platform supporting it. “It was nice to see the transaction volume and the capital flows going in a more normalized way,” she said. “We’re always investing in our people, our product expansion, and our technology for a low-friction process for our clients, and 2025 was the first year where we really got to see how those three things function together. I was thrilled to get the positive feedback that we did from the market, and so I’d say both our industry and our platform have a lot of momentum.”

Notable deals last year included a $3.98 billion acquisition financing for Blackstone Infrastructure Partners’ purchase of Safe Harbor Marinas, the largest marina and superyacht services platform in the U.S.; $425 million for Related Companies’ first luxury residential development in Jersey City, Harborside Plaza; the preservation and rehabilitation of Bay View PACT in Brooklyn, a 1,600-unit affordable housing development, through a $196.5 million agency loan, a $198 million historic tax credit investment, $23.7 million historic tax credit bridge loan and $7.5 million letter of credit; a $191.2 million financing package for Bradley Ridge Apartments in Colorado Springs, the largest affordable housing deal in Colorado history; and a $102 million construction loan for Casa Adelante, the largest affordable housing project in San Francisco’s Mission District.

On the CMBS side, J.P. Morgan’s activities include a $2.85 billion SASB securitization for Blackstone’s Aria Resort and Casino and Vdara Hotel and Spa on the Vegas strip in the BX 2025-ARIA deal, part of a $3.45 billion whole loan; and a $2.85 billion financing for Tishman Speyer’s the Spiral in New York in the HY 2025-SPRL deal.

Oh, and did we mention the $38 billion construction financing package for Vantage Data Centers’ development of two large hyperscale campuses totaling 2,250 megawatts? All in a day’s work for J.P. Morgan.

“While there was some carryover of 2024 market issues into the beginning of 2025, as the year went on deal activity became more active and the competition became more aggressive, but we ended the year well in terms of all of the metrics: revenue, originations, client growth, all those things,” Brian Baker said.

The recent volatility from the Iran war has caused many lenders to proceed with caution, and the market has moved from a high- volume, benign, tight-spread environment to a low-volume one with spreads moving considerably wider. Not J.P. Morgan, though.

“We never root for volatility, but we try to always be

prepared for it,” Baker said. “It has tended to benefit our market share and our client impact, because while other firms get a little careful — they go to the sidelines or pull back — it’s culturally embedded in us to be there for our clients. Amid the volatility, we closed two significant deals [including the $4.3 billion financing package for One Beverly Hills]. I think things will settle back to a benign environment. There’s a lot of capital, interested investors, a lot of clients who want to deploy money in the real estate space, and we’ll be there.”

“In periods of volatility, we have a clear playbook to support our clients,” Herrick said. “Our clients expect consistency of capital and client experience. That’s what we deliver in any environment, and we contributed a significant amount of debt capital to support this industry in 2025 with no plans to change any of that commitment. We’re also scanning for unusual opportunities that create additional value, long term, for our platform.”

J.P. Morgan’s Community Development Banking

team supports efforts to increase the nation’s affordable housing supply, and last year it deployed a considerable $10 billion in debt and equity to create and preserve more than 60,000 affordable units. It was also awarded the Freddie Mac affordable license last year, which “aligns very well with a mission that is critical to our firm,” Herrick said. “If you think about Freddie and Fannie and the stability and liquidity they’re providing to help housing be more affordable for the country, that is an area where we are incredibly well aligned as the largest multifamily lender and also the largest bank. It’s an area where we spent a lot of time, proudly, in `25, and we’ll only work hard to figure out how to do more as we go forward in 2026.”

As two final reasons to celebrate, J.P. Morgan opened its new global HQ at 270 Park Avenue last year, and also shared plans for a 3 million-square-foot landmark tower in London, which is pegged to contribute $13 billion over six years to the local economy, and create 7,800 jobs across construction and other industries. —C.C.

Michelle Herrick and Brian Baker.

Your blueprint for success starts here.

Kara McShane

Head of commercial real estate at Wells Fargo

Last year’s rank: 1

For Kara McShane, 2025 was an “intentional” year.

“When I stepped into the role in 2020, the goal was to build a more collaborative, nimble and resilient platform that could perform through cycles,” McShane said. “In 2025, that meant being intentional in our decision-making — staying coordinated and disciplined and being clear about our focus in an ever-changing landscape.”

Wells Fargo was also intentional about what it didn’t do, McShane said: “We didn’t chase volume for its own sake, and we didn’t stretch on structure just to ‘win’ in a crowded market.”

Balance sheet originations totaled $41 billion, up 200 percent year-over-year, spanning term, construction, commercial and industrial lending. Its capital markets originations hit $34 billion — $21.3 billion of CMBS and $11.3 billion of agency loans — a 50 percent increase year-over-year.

McShane’s platform won in plenty of ways. Under her leadership, Wells Fargo continued to demonstrate scale and consistency, maintaining top positions in key lending and securitization markets while executing some of the industry’s most buzzed-about transactions.

It was the top-ranked global CMBS bookrunner and bank agency lender, and also took the crown for real estate loan syndications and real estate gaming, lodging and leisure. Wells Fargo also was the No. 2 agency bookrunner last year, and the No. 3 CRE CLO bookrunner.

As for notable deals, where to start? To name but a

Corporate and Investment Banking

few: Wells Fargo provided the $3.15 billion financing for StuyTown/Peter Cooper Village in New York; acted as lead adviser and a lender in Blackstone Infrastructure’s $5.65 billion acquisition of Safe Harbor Marinas; provided the $1.6 billion construction loan for Related Companies and Oxford’s 70 Hudson Yards; served as sole structuring agent and joint bookrunner for One Five One’s $1.3 billion Green Bond SASB financing; and priced the $1.4 billion floating-rate BX 2025-BCAT, secured by 67 industrial assets.

In a competitive year, “our biggest advantage is our ability to execute decisively across market conditions — deploying balance sheet, providing capital markets solutions and advice, and partnering in real time, while maintaining underwriting discipline,” McShane said. “We have size, expertise, a full suite of product offerings, and the ability to deliver and execute for our clients.”

The firm has spent years building a deeply integrated model across CRE and the broader investment banking platform, which allows it to move quickly and stay aligned when markets are selective or dislocated, McShane said.

The platform has more than $150 billion in total commitments across the corporate and investment banking CRE platform today, with multifamily representing 28 percent of its book ($37 billion) and industrial 19.6 percent. Data centers comprise roughly 2 percent of its book, a $3 billion exposure.

“In a crowded or volatile environment, dependability and trust matter more than ever,” she said. “We don’t try

3

Tim Johnson and Michael Wiebolt

to win every deal — we focus on relationships and structures that perform through cycles.”

As for 2026, McShane’s teams are busier than ever.

“From a numbers perspective, the pipeline is up materially from this time last year,” McShane said. “The 2026 pipeline reflects disciplined engagement — active where fundamentals are strong, and selective where risk remains elevated. The common thread is earlier, more substantial dialogue. Clients want partners who can help them navigate uncertainty, think holistically about the range of solutions, and execute flawlessly.”—C.C.

Global head at Blackstone Real Estate Debt Strategies and CEO and chairman at Blackstone Mortgage Trust; global chief investment officer of Blackstone Real Estate Debt Strategies

Last year’s rank: 2

Blackstone found even more ways to add value to the market in 2025, which made for a “differentiated” year compared to the previous year, Michael Wiebolt said. “Last year, markets were open and liquid, activity was strong, and one of the things that I’m most proud of is the different ways in which we were able to deploy capital across strategies around the world.”

A rolling “stone” gathers no moss, and the firm didn’t let the grass grow beneath its feet, deploying 74 percent more capital than the previous year and originating $23 billion of loans across the globe, leaning into its high-conviction sectors as market fundamentals improved. But let’s dig in a little further: First, BREDS raised an $8 billion debt fund focused on opportunities in North America, Europe and Australia. It also completed significant acquisitions of loan pools from Atlantic Union Bank ($2 billion) and First Internet Bank ($870 million), and made mega loans including a $925 million debt facility for Colovore’s new liquid-cooled data centers.

BXMT not only launched a new net lease strategy focused on real estate inked to essential retail, but it also issued over $4 billion of corporate and securitized debt including two $1 billion CRE CLOs and the very first U.K. CMBS transaction by a commercial mortgage REIT. Blimey!

“Transaction activity certainly picked up last year, but we were also firing on all cylinders across a variety of different strategies,” Wiebolt said. “If you rewind a year ago, during the more dislocated periods of the market, we were very busy with loan pool purchase activity and also on the securities side.There was less origination activity because there were fewer transactions then, but then we started to see the direct lending opportunities pick up again in

Europe and the U.S., but we also didn’t see a slowdown in the other stuff. So the past year was a really neat environment to be able to do lots of different things at once.”

When the competition heated up, Blackstone was comfortable in a range of asset classes. “Everybody likes multifamily and industrial, but there are lots of ways to deploy capital in multifamily and industrial, and having the ability to choose from amongst them is a big competitive advantage,” Wiebolt said.

Blackstone has completed more than $23 billion of bank loan portfolio acquisitions since 2020, with $5 billion of transactions last year alone. “It takes a lot of resources to source and underwrite and manage, but we’ve got 170 people across Europe, the U.S. and Australia,” Wiebolt said. “We’ve got the scale and the resources to be able to pick and choose how we play in the high-conviction themes that we have around real estate sectors and asset classes here. It’s a huge part of the differentiator and a big part of our success last year.”

This year is already off to a roaring start, with roughly $10 billion in activity already wrapped and another $10 billion in the pipeline.

“We’re seeing a continuation of the themes we saw last year, with the majority of our activity in multifamily and logistics, in data centers and in loan pools,” Wiebolt said.

While Wiebolt chose “differentiated,” to describe Blackstone’s year, he almost chose “fun.”

“I am so blessed and fortunate to get to work with the most amazing people here,” he said. “I love the team here. Everybody cares so much, and everybody rows in the same direction every day. I don’t know what else I would do every day other than this because I love what we do and I love the people that I get to do it with. I just feel super blessed.”—C.C.

Tim Johnson.

Michael Wiebolt.

Kara McShane.

Silverstein Properties is a privately-held, full-service real estate development, investment and management firm that has developed, owned and managed more than 45 million square feet of office, residential, hotel, retail and mixed-use properties.

Investment Types

•All major property types in growing urban markets

•Flexible and efficient debt structures

•Senior loans of $75 million or more

•Subordinate loans of $50 million or more

•Shovel-ready groundup construction

•Heavy value-add repositioning

•Inventory loans on completed condo projects

•Rescue capital to borrowers

See

Why Fannie Mae and Freddie Mac for the first time ever didn’t make our cut Wait and

The future of Fannie Mae and Freddie Mac has remained in limbo since President Donald Trump returned to the White House last year, causing the two mortgage market giants’ influence to be severely diminished. Or, at least, difficult to assess.

The Trump administration laid the groundwork for a privatization of the government-sponsored enterprises in August 2025. Meetings were held with the six largest banks, and plans were put in motion to sell up to $30 billion in preferred shares of Fannie and Freddie on the open market.

The federal government’s conservatorship of the GSEs has been in place since September 2008, and the timing and specifics of ending that oversight remain up in the air. The speculation alone, however, has sparked concerns about a profit-driven plan that would lead to higher mortgage rates, stricter underwriting for multifamily loans, and higher loan-to-value ratios. Fannie

and Freddie face the prospects of a prolonged purgatory, since a potential privatization would require major regulatory changes with new capital requirements that could delay such a move past the completion of Trump’s term in January 2029.

Given the growing uncertainty of Fannie and Freddie under the Federal Housing Finance Agency (FHFA), we decided to take a wait-and-see attitude in this year’s Power Finance rankings, despite both agencies long being staples on the list. It was just five years ago that the GSEs took the No. 1 and No. 2 spots in Power Finance for the stability they brought to the multifamily market during the market volatility of the COVID-19 pandemic.

Despite major staff cuts at Fannie and Freddie last year implemented by Bill Pulte, director of the FHFA who was also named head of Fannie and Freddie in March 2025, both GSEs posted sluggish earnings in the 2025 fourth quarter. Fannie Mae’s fourth-quarter net income dropped

14.6 percent from the same period in 2024, with Freddie Mac’s falling similarly at 14 percent, and both agencies spiking their provisions for credit losses.

While Fannie and Freddie’s overall power in commercial real estate has been altered over the last year, each can still play an important role in tackling housing affordability, regardless of how the entities are constructed. Their impact is based largely on what policy actions are taken at the federal level.

“Fannie Mae and Freddie Mac are essential to the availability of affordable mortgage credit across the country, for both single-family homeowners and the multifamily housing stock that serves millions of renters,” said Sam Chandan, director of the Chen Institute for Global Real Estate Finance at New York University. “The current conversation about the future of the enterprises is a consequential one, and it deserves a level of engagement that reflects their systemic importance.” —A.C.

$117

$89

$22

Scott Weiner

Partner and global head of real estate credit at Apollo

Last year’s rank: 3

Like a seasoned magician, Apollo’s Scott Weiner played tricks on the market in 2025 and still emerged as one of the premier players in CRE credit, to the tune of $24 billion.

Weiner surprised everyone in January when he led the charge to sell Apollo Real Estate Investment (ARI), the firm’s $9 billion publicly traded REIT, to Athene Holdings, Apollo’s $440 billion insurance subsidiary. Questions abounded — was Weiner cashing out of CRE credit?

Not at all. Like any good prestidigitator, Weiner was simply moving one pocket of capital he intends to play with at Apollo into another, mainly because he could.

“By no means are we getting out of the business. Those loans are still managed by me and my team,” Weiner said. He said the ARI portfolio has been undervalued by the public market for an extended period of time, and ARI is proposing a shareholder-friendly transaction by selling it to Athene.

“Athene has strong demand for CRE debt as an asset class, and is already familiar with those assets, so we believe it’s a win-win,” he added.

Weiner and his team won a lot of business in 2025. They originated $24 billion of CRE credit across 120 deals, with $15.4 billion of transactions occurring in the U.S., financing across 39 states in what was a record year of business for the firm.

“We were very active across property types and geographies, and that’s part of what makes the platform special,” said Weiner. “It wasn’t one deal, or a couple of deals, that led to our success this year, and it wasn’t one property type.”

Standout transactions included an $840 million takeout loan to finance the conversion of 25 Water Street in Manhattan, a $785 million acquisition loan for RXR and Elliott Management to buy 590 Madison in Manhattan, and an impressive $2.7 billion in U.S. data center pre-release, hyperscale construction.

Regardless if it’s ARI, Athene, Apollo’s fortress balance sheet or the capital on behalf of third-party investors, Weiner has his choice of roughly $75 billion across Apollo’s many channels for CRE credit investments.

“It’s a pretty powerful platform,” he said. —B.P.

Jordan Roeschlaub and Nick Scribani

Co-head of global debt and structured finance; vice chairman of global debt and structured finance at Newmark

Last year’s rank: 5

Newmark was full throttle once again in 2025.

Newmark’s non-agency debt volume jumped 76 percent from 2024 levels to $64 billion, while total originations soared 67 percent to $75 billion. The brokerage giant also maintained momentum with its strategic advisory joint ventures business by facilitating $8 billion in equity raising.

Much of Newmark’s debt success in 2025 during largely unfavorable market conditions was planted in previous years.

“We built a really good pipeline based on just informing our clients over the last couple of years of where the market is and more importantly where it’s going,” Nick Scribani said. “We enjoyed a lot of success by being early to let people know that you have good assets, and the time may not be now but it’s coming, and you got to trust us when we tell you to pull the trigger.”

Newmark was ahead of the curve a few years ago on the growing demand for data centers and brokered a number of large loans in the sector throughout 2025.

A signature deal closed by Newmark in the past year involved a $7.1 billion construction loan for Blue Owl Capital, Crusoe and Primary Digital Infrastructure to fund the second phase of a 1.2-gigawatt AI data

center project in Abilene, Texas. The balance sheet loan, which closed in May 2025, was originated by a consortium of lenders led by J.P. Morgan Chase.

In late 2025, Newmark brokered a $835 million debt package to a joint venture between GFP Real Estate and Metro Loft for the refinance of its newly delivered office-to-residential conversion project at 25 Water Street in Manhattan’s Financial District. Apollo and GIC supplied the loan for the 1,320unit apartment building that was formerly a 1.1 million-square-foot office complex.

The office sector was also front and center in a number of Newmark’s deals in 2025, including a $630 million CMBS loan for Cain International and OKO Group to refinance 830 Brickell in Miami. Goldman Sachs and J.P. Morgan led the refi for the 57-story building that houses Citadel as its anchor tenant.

Newmark is poised for more large transactions and to exceed its already high 2025 totals.

“We’ve consistently been ahead of where the market is and where the market’s going,” Jordan Roeschlaub said. “We’re not complacent and we’re always going to be achieving and figuring out how to stay in front of the heap, which takes a lot of effort because it’s a competitive space.” —A.C.

Nick Scribani.

Jordan Roeschlaub.

Scott Weiner.

celebrate success

Bank of America is proud to support Maria Barry, Kenneth Cohen, and Brad Dubeck. Congratulations on your well-deserved recognition.

7Alex Cabria Director of real estate finance at Sumitomo Mitsui Banking Corporation

Last year’s rank: 8

Continuing with a strategy that could be described as creating a legacy without leaning on one, SMBC showed itself to be a flexible, successful lender amid the roller coaster of 2025. One key has been banking on a 5-year-old portfolio free of the constraints of long-term holds and bets placed in a radically different market environment. Instead, it’s built on adapting amid the recent era of uncertainty.

“We’re about thoughtful, prudent lending,” said Alex Cabria. “We’ve always tried to be constructive.”

Last year, SMBC saw $22 billion in origination volume, continuing a massive multi-year growth streak that hit $18.4 billion in loans last year, and $11.6 billion in 2023. Direct lending focused in large part on the industrial sector, including a handful of nine-figure nationwide deals such as providing funding to acquire a $650 million portfolio. But the group’s overall strategy — diversifying across core sectors with a focus on the most liquid assets, like multifamily, industrial, data centers and student

David Bouton

and

Joseph

Dyckman Co-heads of U.S. CRE finance at Citigroup

Last year’s rank: 7

The challenge with superlatives is maintaining them, and over the years Citigroup’s grip on certain lending sectors has remained tight.

Still the top affordable housing and conduit lender and a leader with data center and CMBS deals, Citigroup nonetheless scored significant marquee deals throughout 2025, including $3.05 billion for the Cosmopolitan in Las Vegas and a $1.15 billion SASB refinancing of Atlantis Paradise Island in the Bahamas. Citigroup also financed trophy office assets like Brookfield’s 44-story 225 Liberty Street.

“It’s easy to be a good lender in a robust market,” said David Bouton, who leads CRE finance alongside Joseph Dyckman. “It’s much more difficult when there isn’t as much of a market. That’s when we like to provide leadership and liquidity, not just for our clients, but for the market overall.”

Last year was an active one across the business, with $4.7 billion in conduit originations alone. Nearly every single pillar of the franchise grew last year. In fact, a theme for 2025 was Citigroup’s use of its own balance sheet to provide liquidity to clients, especially in office. Bouton said their contrarian view on office started a few years ago, and they’ve continued to provide backstops for big deals ever since.

Citigroup also showed creativity within a space that’s becoming known for creative financing: data centers. Switch’s inaugural deal with Citigroup, worth $2.4 billion, was done during the market freeze caused by the emergence of Chinese AI model Deepseek.

“In other words, it wasn’t just another hyperscaler,” said Bouton. “They had a unique story about what their assets were. We had to come up with an investment thesis for the investors, and that’s where our expertise in the market really helped us through a difficult time.”

Citi also launched the first powered-shell data center SASB, and served as left lead for a $3.46 billion SASB financing for Blackstone’s QTS data center subsidiary last year. Especially notable since in 2021, Citi successfully underwrote and distributed the industry’s inaugural data center CMBS SASB, a $3.2 billion structured financing package that supported Blackstone’s take-private of QTS.

An incredibly balanced portfolio and internal support allows Citigroup to be agnostic in its financing strategy, and chase whatever solution makes the most sense. “Clients come to us with their very important signature transactions,” said Bouton. “But that’s sort of our DNA. We like to be innovative. We like to be creative, and we like to create liquidity.” —P.S.

“There’s always something going on,” said Cabria. “But, if you believe in the fundamentals and you know how real estate works, you manage through those things.” —P.S. Joseph Dyckman.

housing — led to a portfolio with a balanced mix of stabilized, transitional and construction exposure.

With so many credit funds flush with capital, Cabria saw an opportunity, surmising it might make sense to get more involved as banks were pulling out. Transaction volume ended up being driven by a warehouse/repo facility business within the real estate finance group launched in early 2025 to serve real estate owners, fund managers and global private capital platforms.

“It’s been nice seeing liquidity return,” said Cabria. “But it’s a focused liquidity, focused on top clients and top locations, and people are very selective.”

Lots of banks weren’t able to handle underwriting for deals that had dozens of assets spread across the country, but Cabria and his team found ways to craft portfolios with a balance of geographic risks, amid rocky trade policies, to create deals that were “good trades for everybody.”

A commitment to flexibility across loan sizes, structures, asset types and markets helped accommodate both large, complex transactions as well as bespoke financing in a market that became surprisingly competitive. Longterm relationships also helped SMBC stand out and seize on the upswing in activity that arrived last November.

Alex Cabria.

David Bouton.

BMO celebrates Paul Vanderslice for being named to the Power 50 list.

Thank you for Boldly Growing the Good in Business and Life. Congratulations to all the 2026 honorees on your achievement.

Kwasi Benneh

Global head of commercial real estate lending at Morgan Stanley

Last year’s rank: 6