Office Market Snapshot

Stock

Avg. Vacancy Spec. Vacancy

4,462k sqm 12.5% +0.14% yoy

-1.63 pps. yoy

Q4 2025

Net Take-up

Completion

15.9%

56,105 sqm 50,377 sqm

-1.61 pps. yoy

YTD: 217,644 sqm

DISTRIBUTION OF TRANSACTIONS (2024, 2025) Pre-lease

YTD: 55,437 sqm

New

Expansion

New Build

EUR/sqm/mth

EUR/sqm/mth

25.5

19-21

Cat. A

4,8%

17.1

EUR/sqm/mth

1,8%

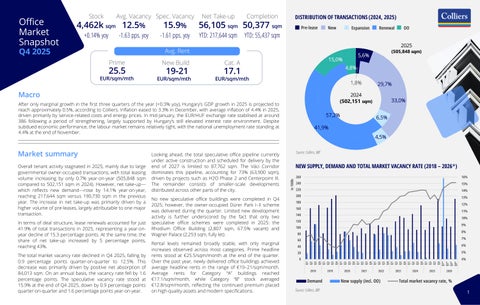

The total market vacancy rate declined in Q4 2025, falling by 0.9 percentage points quarter-on-quarter to 12.5%. This decrease was primarily driven by positive net absorption of 84,013 sqm. On an annual basis, the vacancy rate fell by 1.6 percentage points. The speculative vacancy rate stood at 15.9% at the end of Q4 2025, down by 0.9 percentage points quarter-on-quarter and 1.6 percentage points year-on-year.

Rental levels remained broadly stable, with only marginal increases observed across most categories. Prime headline rents stood at €25.5/sqm/month at the end of the quarter. Over the past year, newly delivered office buildings achieved average headline rents in the range of €19–21/sqm/month. Average rents for Category “A” buildings reached €17.1/sqm/month, while Category “B” stock averaged €12.8/sqm/month, reflecting the continued premium placed on high-quality assets and modern specifications.

33,0% 6,5%

41,9% 4,5% Source: Colliers, BRF

NEW SUPPLY, DEMAND AND TOTAL MARKET VACANCY RATE (2018 – 2026*) 260

16%

240

15%

220

14%

200

13%

180

12%

160

11%

140

10%

120

9%

100

8%

80 60

7%

40

6%

20

5%

0

4% Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1* Q2* Q3* Q4*

In terms of deal structure, lease renewals accounted for just 41.9% of total transactions in 2025, representing a year-onyear decline of 15.3 percentage points. At the same time, the share of net take-up increased by 5 percentage points, reaching 43%.

No new speculative office buildings were completed in Q4 2025; however, the owner-occupied Dürer Park I–II scheme was delivered during the quarter. Limited new development activity is further underscored by the fact that only two speculative office schemes were completed in 2025: the Rhodium Office Building (2,807 sqm, 67.5% vacant) and Wagner Palace (2,253 sqm, fully let).

57,2%

In 1000s

Overall tenant activity stagnated in 2025, mainly due to large governmental owner-occupied transactions, with total leasing volume increasing by only 0.7% year-on-year (505,848 sqm compared to 502,151 sqm in 2024). However, net take-up— which reflects new demand—rose by 14.1% year-on-year, reaching 217,644 sqm versus 190,730 sqm in the previous year. The increase in net take-up was primarily driven by a higher volume of pre-leases, largely attributable to one major transaction.

29,7%

2024 (502,151 sqm)

After only marginal growth in the first three quarters of the year (+0.3% yoy), Hungary’s GDP growth in 2025 is projected to reach approximately 0.5%, according to Colliers. Inflation eased to 3.3% in December, with average inflation of 4.4% in 2025, driven primarily by service-related costs and energy prices. In mid-January, the EUR/HUF exchange rate stabilised at around 386 following a period of strengthening, largely supported by Hungary’s still elevated interest rate environment. Despite subdued economic performance, the labour market remains relatively tight, with the national unemployment rate standing at 4.4% at the end of November.

Looking ahead, the total speculative office pipeline currently under active construction and scheduled for delivery by the end of 2027 is limited to 87,762 sqm. The Váci Corridor dominates this pipeline, accounting for 73% (63,900 sqm), driven by projects such as H2O Phase 2 and Centerpoint III. The remainder consists of smaller-scale developments distributed across other parts of the city.

(505,848 sqm)

5,6%

15,0%

Macro

Market summary

OO

2025

Avg. Rent Prime

Renewal

2018

Demand Source: Colliers, BRF

2019

2020

2021

2022

New supply (incl. OO)

2023

2024

2025

2026

Total market vacancy rate, % 1