2025 LUXURY REVIEW

FROM REAWAKENING TO REFINEMENT

The story of North America’s luxury real estate market in 2025 is not one of acceleration nor deceleration, but of evolution. Over the course of the year, the market moved through distinct phases: reengagement, recalibration, normalization, and ultimately, equilibrium.

What makes 2025 notable is not any single metric, but the way buyer and seller behavior matured in response to shifting economic conditions, expanding inventory, and a recalibrated understanding of value.

Rather than chasing momentum, the luxury real estate market in 2025 increasingly prioritized alignment: between price and quality, lifestyle and investment, timing and conviction.

Q1 2025: REENGAGEMENT WITH RESTRAINT

The opening quarter of 2025 marked a return of confidence, but not excess. Momentum from late 2024 carried into the market as interest rate relief restored optionality for buyers and sellers alike. Activity increased across primary and secondary markets, supported by rising inventory and renewed engagement from affluent households who had largely remained on the sidelines through much of 2023 and early 2024.

This reengagement, however, was tempered by realism. The brief hesitation that surfaced mid-quarter reflected how tightly luxury demand had become linked to broader financial sentiment. Volatility in equity markets and geopolitical uncertainty did not dismantle demand, but they did reshape behavior. Buyers paused, recalibrated, and then returned with greater discernment.

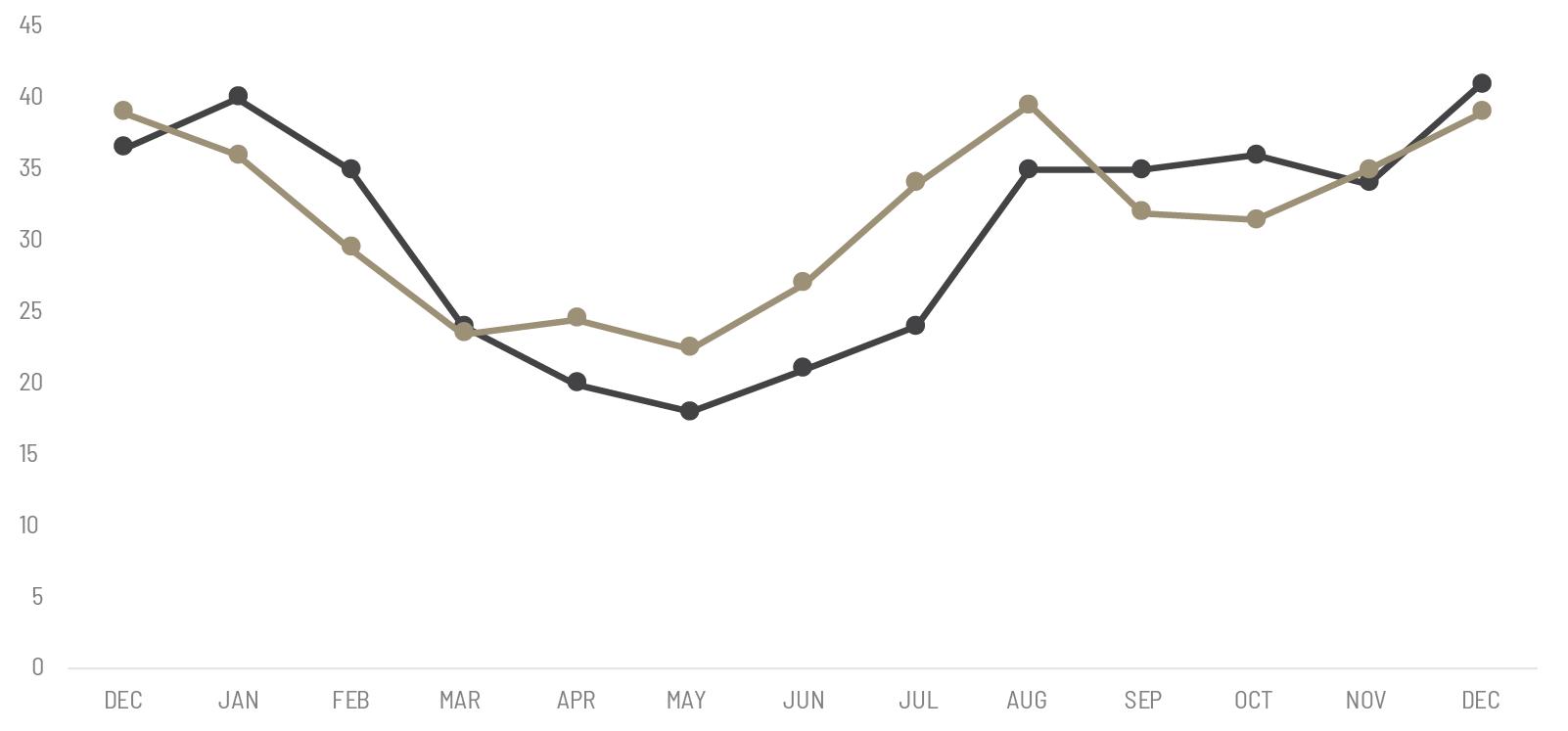

By the close of the quarter, sales volumes had recovered meaningfully, while inventory growth signaled renewed seller confidence. Sales were up 9.4% year-over-year for single-family homes and 2.4% for condominiums and townhomes, while inventory rose more than 26% across both single-family and attached segments.

Importantly, the market’s response suggested structural health rather than speculative enthusiasm.

Transactions were driven by long-term intent: relocation, lifestyle upgrades, and portfolio diversification, rather than opportunistic timing.

The first quarter established the tone for the year ahead. Luxury real estate was once again in motion, but it was moving more deliberately.

Q2 2025: RECALIBRATION WITHOUT RETREAT

If the first quarter was about re-entry, the second was about recalibration. The market slowed but in a way that felt constructive rather than concerning. Activity moderated, particularly in attached luxury properties, while single-family homes continued to attract steady demand.

April’s slowdown raised concerns, but May and June delivered stabilization rather than decline. By the end of Q2, singlefamily luxury sales rose modestly by 2.6% year over year, while attached properties declined 8.1%, revealing a growing preference for larger space, privacy, and lifestyle-driven assets.

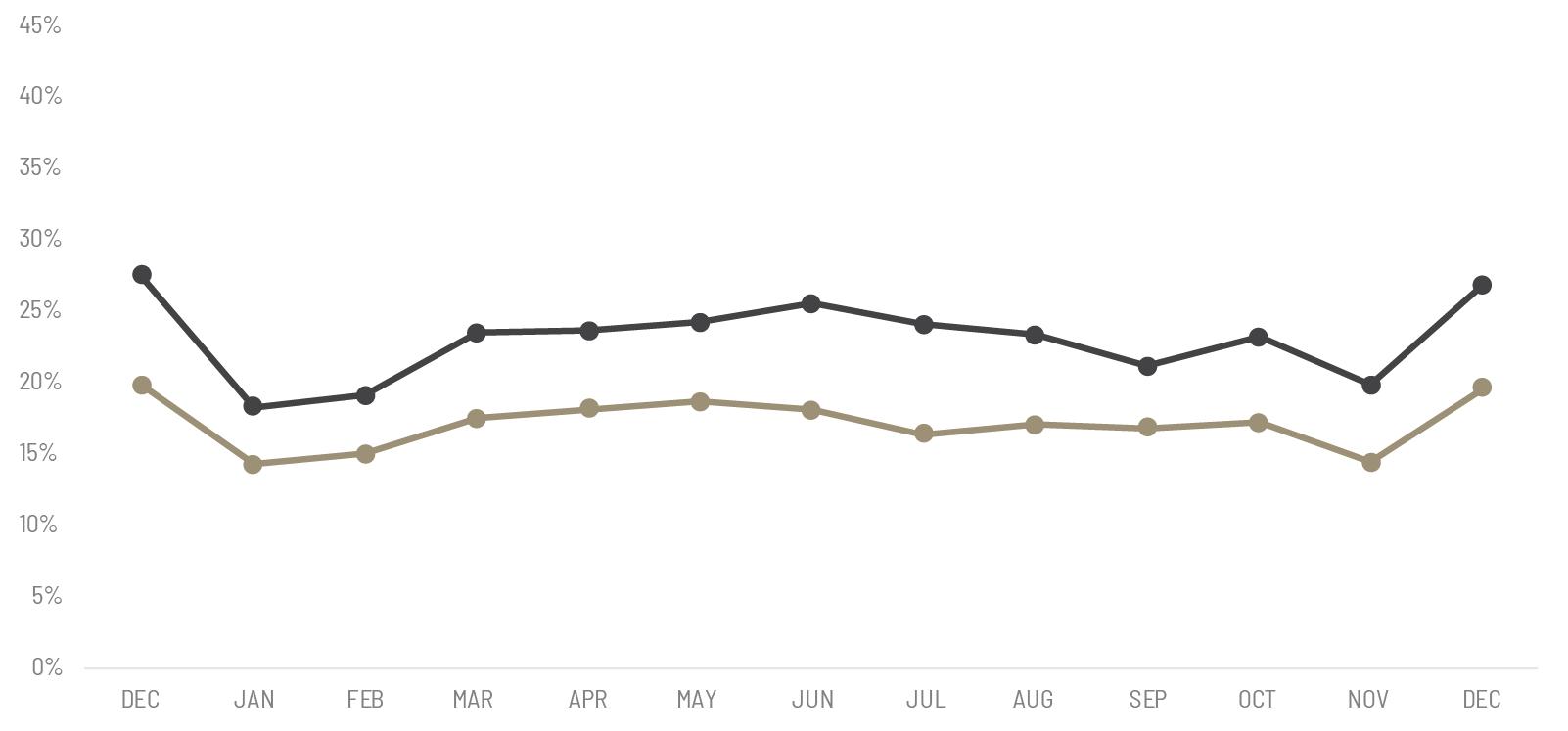

Inventory continued to rise, nearly 30% year-over-year for single-family homes, but new listings slowed after April. This divergence was critical. The market was not being flooded; rather, it was normalizing after years of constraint, revealing that it could absorb supply without undermining value as the median sold price rose 2% for single-family homes and 3.8% for attached properties year over year.

This period highlighted a shift in how luxury participants interpreted time. Properties took longer to sell, negotiations became more analytical, and buyers demonstrated a willingness to wait for alignment rather than compromise. Sellers, meanwhile, began to test the market more strategically, often choosing to delay listings rather than adjust pricing prematurely.

External pressures, including elevated construction costs, tariffs, labor shortages, and insurance constraints began to exert a more visible influence, particularly on new development. As a result, renovation and repositioning gained prominence, reinforcing the value of existing homes in strong locations.

The second quarter underscored a critical evolution: luxury real estate was no longer responding reflexively, instead, it was adapting and absorbing uncertainty without losing cohesion.

Q3 2025: NORMALIZATION TAKES HOLD

By the third quarter, the market’s recalibration had matured into stability. The period from July through September 2025 told a story of moderation, where stability met selectivity, as the market transitioned from reactive to refined, with fundamentals dictating performance.

Sales volumes strengthened, inventory growth slowed, and pricing behavior became increasingly

disciplined. Sales increased 7.5% year-over-year for single-family homes, while attached properties stabilized with a 0.5% growth. Inventory growth slowed, pricing held firm, and negotiation dynamics matured.

Buyer selectivity intensified. Quality, location, and readiness mattered more than ever, while properties that failed to meet contemporary expectations, whether in design, efficiency, or lifestyle alignment, faced longer absorption periods. At the same time, sellers demonstrated a growing understanding of value positioning, adjusting expectations in line with market realities rather than aspirational benchmarks.

The third quarter made clear that luxury real estate had entered a new phase: one defined less by cycledriven volatility and more by informed participation on both sides of the transaction.

Q4 2025: CONFIDENCE WITHOUT EXCESS

The final quarter of the year brought clarity. Rather than closing on uncertainty, the luxury market finished 2025 with resilience and quiet confidence. Activity remained healthy, inventory continued to expand at a measured pace, and pricing discipline held across both single-family and attached segments.

Luxury sales accelerated sharply in December, with single-family transactions up 7.8% year-over-year and attached sales rising 4.1%. Month-over-month gains were even stronger, reframing November as a pause, not a peak.

From October’s steady momentum, through November’s seasonal recalibration, to December’s resilient and unexpected surge, Q4 reinforced a central theme: the luxury market has entered a healthier, more sustainable cycle, grounded in confidence, discipline, and long-term value rather than short-term swings.

Seasonal moderation did little to disrupt underlying demand, and when activity reaccelerated toward year-end, it confirmed the market’s depth rather than fragility. Buyers remained engaged well beyond traditional timelines, motivated by long-term considerations rather than short-term signals. Sellers, in turn, showed restraint, listing with intention and pricing with realism.

IN CONCLUSION

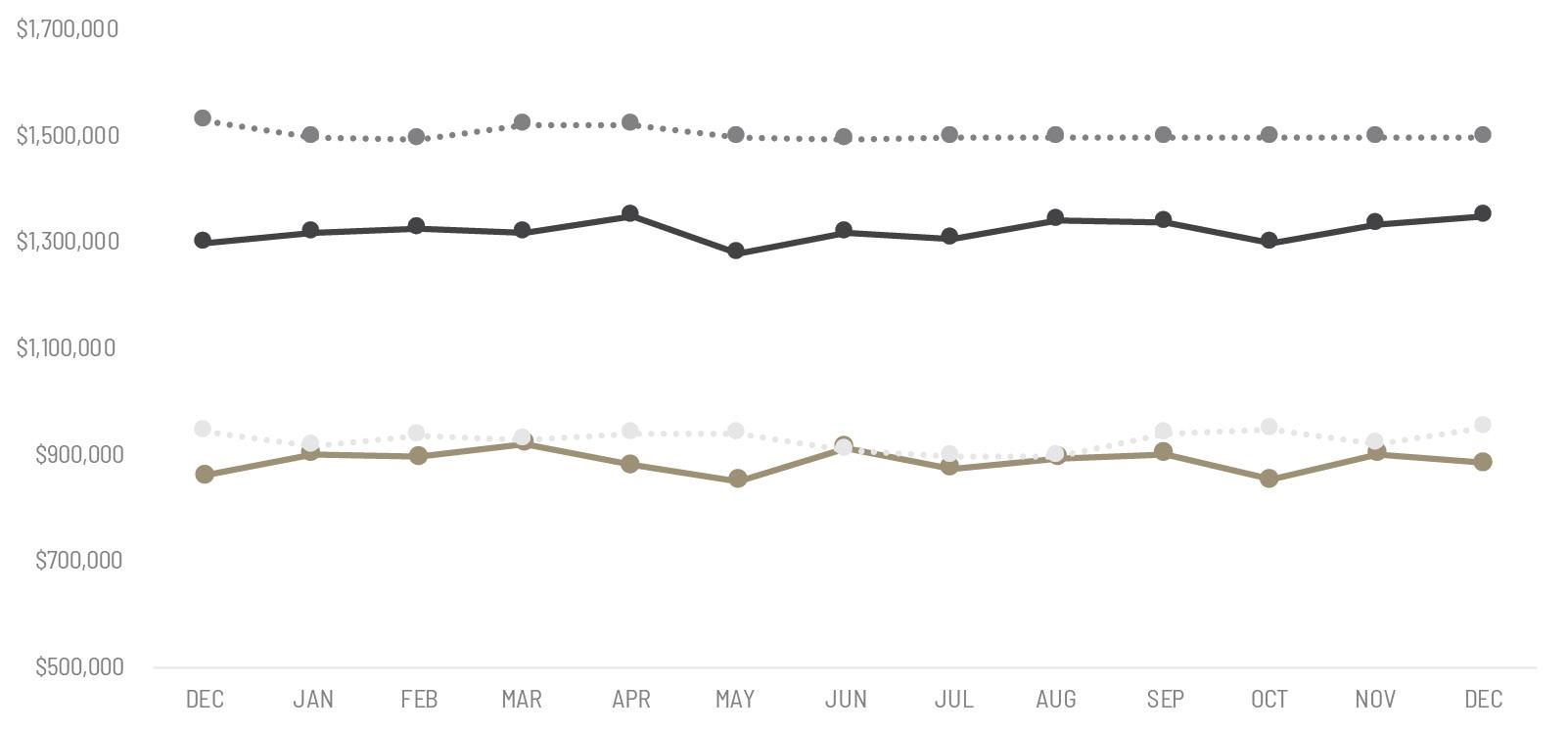

By year’s end, the luxury real estate market had achieved something rare: balance without stagnation. It was neither constrained by scarcity nor pressured by oversupply. Instead, it functioned as a rational marketplace where quality assets retained liquidity and value.

Pricing trends remained constructive, with median sold prices rising year over year across both single-family and attached segments. Inventory growth proved healthy, expanding buyer choice and improving market function without destabilizing pricing. New listing activity, however, remained selective, reinforcing seller discipline around timing and positioning. While buyer behavior throughout the year revealed a decisive shift away from speculation toward long-term value, lifestyle utility, and portfolio strategy.

Regional differentiation became more pronounced. Markets with structural supply constraints and strong economic underpinnings retained seller-leaning conditions, while areas that had seen rapid expansion earlier in the decade transitioned toward balance. This re-localization of performance reinforced the importance of market-specific expertise and nuanced strategy.

LOOKING AHEAD: THE OPENING OF 2026

As the luxury real estate market enters 2026, it does so from a position of strength. Interest rate expectations are more stable, equity markets less volatile, and buyer psychology more grounded. The conditions that defined 2025, including selectivity, strategy, and localization, are likely to persist.

Early 2026 is poised to reward precision rather than speed. Sellers who align their property’s pricing, presentation, and timing with local realities should find receptive demand. Buyers, particularly those with long-term horizons, will continue to view luxury real estate as both a lifestyle asset and a stabilizing force within diversified portfolios.

Perhaps most notably, the role of expertise has never been more central. In a market defined by nuance rather than momentum, success will belong to those who understand not just where the market is, but why it behaves as it does.

In that sense, 2025 may ultimately be remembered as the year luxury real estate found its footing againnot by moving faster, but by moving smarter.