February

High Gear, Low Visibility

Riding Between Confidence and Caution

February

Riding Between Confidence and Caution

As we mark our 20th anniversary in 2026, this economic outlook serves as both a reflection and a forward look. Over the past two decades, we have navigated market cycles, global shifts, and periods of uncertainty with a steady focus on long-term perspective and disciplined decision-making. That experience shapes how we view today’s environment and how we prepare for what comes next.

Since our founding in 2006, Clearwater Capital Partners has been guided by a clear purpose: to inspire and empower our clients to live with joy, confidence, and a spirit of abundance. That purpose defines who we are and why we exist. It is the foundation of every relationship we have built and every plan we have crafted.

As we reflect on twenty years, we do so with deep gratitude for the clients who have entrusted us with their financial futures, the colleagues who bring our mission to life every day, and the community partners who help us extend our impact. Each of you has played a role in shaping the Clearwater story.

Our journey has reinforced an enduring truth. Markets evolve, economies shift, and opportunities emerge, but enduring relationships and shared purpose are what create lasting value. These are the constants that continue to guide us into the future.

Throughout the year, we will celebrate this milestone through firm-wide initiatives, events, and more. We invite you to stay connected by visiting our website, following us on our social media channels, tuning into our Thought Leadership commentary, and connecting with your Clearwater advisory team.

Thank you for being part of our story. Here’s to twenty years of partnership, growth, and purposeful progress and to the years ahead, filled with joy, confidence, and abundance.

Katie Berganske-Frank

Katie Berganske-Frank Chief Revenue Officer

John

Chief Executive Officer

Chief Investment Strategist

Tyler

Managing Partner, Portfolio Mangement Deputy Chief Investment Strategist

Clearwater Capital Partners was founded in 2006 by John Chapman to address long standing shortcomings in the financial industry, including conflicts of interest, limited transparency, and unmet promises. From the beginning, the firm was built on the belief that investors deserve clear, honest guidance focused on real world needs, not fragmented sales driven solutions. That commitment to integrity and competence continues to guide every decision we make. Shaped by principles established at our founding, Clearwater has grown primarily through client referrals, reflecting deep trust and lasting relationships. Today, we are a well established and thriving firm, grounded in experience and driven by purpose.

Board of Directors

John Chapman

Al Krause

John Sleeting

Jeffrey DeHaan

Operating Committee

John Chapman

John Sleeting

Jeffrey DeHaan

Al Krause

James Chapman

Tyler Beachler

Katie Berganske-Frank

Danuta Garb

Wealth Advisors

John Chapman

John Sleeting

Jeffrey DeHaan

Greg Davis

James Chapman

Melissa Dailey-Newman

Valerie Hogan

Jacob Clark

Braden Maher

Kevin Rochford

Institutional Advisory Services

Kevin Carani

John Ellis

Carter King

Portfolio Management

Tyler Beachler

Rocky Byrd

Tyler Bertsche

Advanced Planning

Kevin Nolte

Conor Durkin

Global Strategies

Hunter Sims

Operations Specialists

Ty Sampson

Andrea Patterson

Phillip Richardson

Phillip McCloskey

Riki Husic

Brand and Marketing

Katie Berganske-Frank

Hayley Holmes

Human Resources and Accounting

Al Krause

Danuta Garb

Client Experience

Katie Berganske-Frank

Liza Alexanian

Hayley Holmes

Compliance and Risk Management

Jeffrey DeHaan

James Chapman

Ty Sampson

Rocky Byrd

Riki Husic

Accounting Services

Al Krause

Danuta Garb

Erica Rangel

Our team’s expertise spans with designations that include: AIF®, AWMA®, CDFA®, CEPA®, CFA®, CFP®, CPA®, CPFA®, CTFA®, CRPS®, J.D., QKA®.

It is a pleasure to share Clearwater Capital Partners’ Outlook 2026.

In preparing this report, our team reviewed research and commentary from a wide range of economists, asset managers, and independent thinkers. We respect those perspectives, but we do not accept them uncritically. We compare them to history, test them against current data, and then draw our own conclusions about what matters most for our clients.

The picture heading into 2026 is genuinely mixed. Headline growth and corporate earnings remain solid, yet parts of the labor market and several cyclical sectors have cooled. Some indicators still point clearly to expansion, while others hint at slowdown.

It is an environment of what our friend Brian Wesbury has called “data fog,” where the signals are noisy and often conflicting.

Our responsibility is to acknowledge that uncertainty without being paralyzed by it. We must be candid about what we cannot know in advance, define a reasonable range of outcomes, and still provide a practical framework for long-term decision making.

In the pages that follow, we focus on the forces that we believe will shape the year ahead and the next several years beyond: elevated equity valuations, the ongoing buildout and promise of artificial intelligence, shifting tariff and trade policy, persistent but moderating inflation, evolving Federal Reserve policy, and a contentious U.S. political backdrop in a midterm election year.

Investors face an environment that is both challenging and full of opportunity. Innovation, particularly around artificial intelligence, is reshaping industries and creating new engines for growth. At the same time, geopolitics, policy shifts, and rich starting valuations remind us that risk remains an unavoidable part of investing.

Our task is to balance those realities, to participate in progress while keeping appropriate guardrails in place.

This year also marks the twentieth anniversary of Clearwater Capital Partners. Two decades of working with families to pursue their financial goals is both a milestone and a source of deep gratitude. The most meaningful way we can celebrate that history is by continuing to do the work with clarity, discipline, and a long-term focus on your well-being.

Thank you for the trust you place in Clearwater Capital Partners. Earning that trust, year after year, through disciplined work and attentive service to you and your

We place these developments in historical context and explain how they inform the way we are positioning portfolios today.

Each January, our goal is not to predict short term market moves with precision. Markets are too complex and too humbling for that. Our purpose is to identify the most important forces shaping the economy and capital markets, outline a reasonable range of scenarios, and help clients make long-term decisions under uncertainty.

Our Outlook 2025 report, titled “A Complicated Path Forward,” tried to do exactly that. At the time, we saw a resilient economy still benefiting from the post pandemic expansion, but also a more challenging investment landscape. Valuations were elevated, a new administration was pursuing an ambitious and more confrontational policy agenda, and market leadership had narrowed their focus to a small group of large technology and AI related companies.

As 2025 unfolded, it became clear that the complications we described were not theoretical. Tariff shocks, shifting expectations around the Federal Reserve, and geopolitical tensions produced a near bear market decline and then one of the fastest recoveries on record. The economy slowed but did not contract. Artificial intelligence (AI) moved from primarily a story to a visible driver of capital spending and early productivity gains. Despite the turbulence, both the economy and equity markets ended the year in better shape than many anticipated.

Viewed with hindsight, several aspects of our framework held up reasonably well, while others deserve adjustment. Together, they shape how we are thinking about 2026.

We began 2025 with a thesis of cautious optimism. We expected the economy to continue growing, but with less margin for error. That broad view proved sound.

Real gross domestic product ultimately came in near the 2 percent range that we anticipated, even though the quarterly path was uneven. We shifted from a prior stance that favored recession over a multiyear horizon to a view that a soft landing was more likely than not for 2025, while still recognizing the possibility of a mild downturn. The year resembled a late cycle slowdown rather than a classic recession.

Key indicators such as the Conference Board Leading Economic Index and portions of retail sales and housing sent warning signals, but the overall economy did not slip into broad-based contraction.

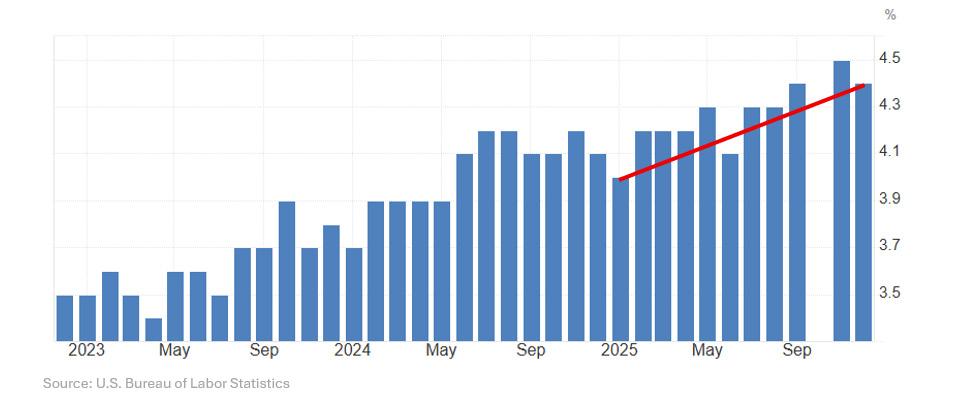

From the outset, we encouraged clients to look beneath the surface of the labor market. Headline unemployment remained in a narrow band near 4 to 4.5 percent, which created an appearance of stability.

Underneath that surface, 2025 turned out to be the weakest year for net job creation since the pandemic recovery began, once government and healthcare jobs were separated from core private sector payrolls.

“We shifted from a prior stance that favored recession over a multiyear horizon to a view that a soft landing was more likely than not for 2025, while still recognizing the possibility of a mild downturn.”

Labor participation slipped and continuing claims trended higher. That pattern supported our emphasis on the quality and composition of employment, rather than a simple focus on the top line unemployment rate.

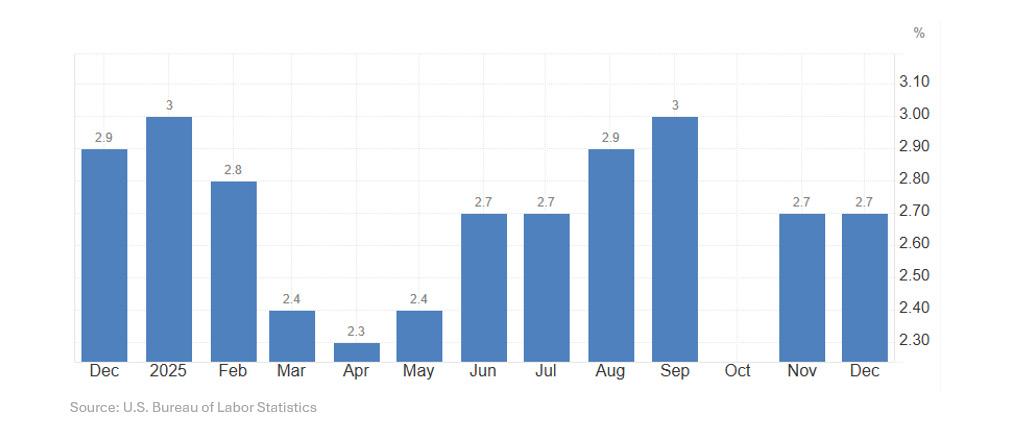

On inflation, we expected price pressures to remain above the Federal Reserve’s formal 2 percent target, and that view was broadly correct, even if our initial range was a bit high. Headline inflation finished the year near the high 2 percent area, slightly below the 3 to 4 percent band we outlined, but still meaningfully above pre-pandemic norms. Over the course of the year, we became less concerned that tariffs alone would create a fresh inflation shock and more focused on the role of money growth, credit conditions, and aggregate demand in shaping the inflation path.

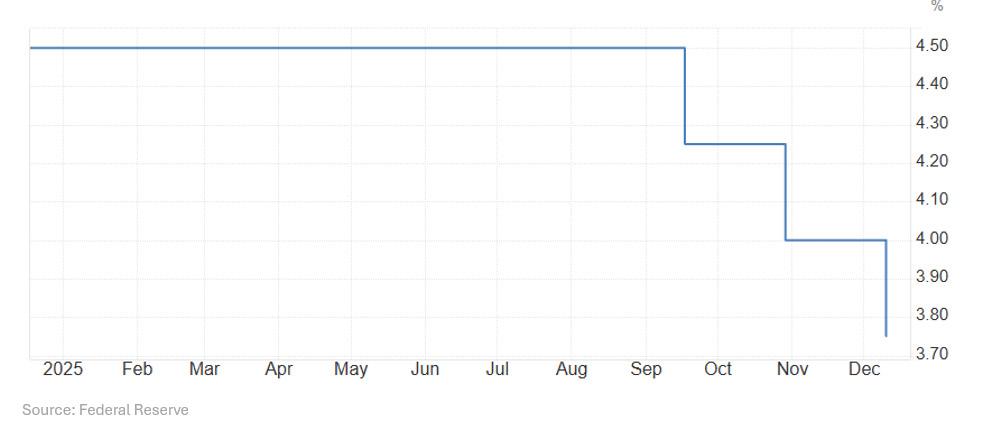

With respect to monetary policy, we described 2025 as an environment of higher rates that would likely remain in place longer than many investors expected. The Federal Reserve ultimately delivered three quarter point rate cuts late in the year, which represented more easing than our tone suggested but did not amount to an aggressive cutting cycle by historical standards. Policy moved from clearly restrictive toward a more neutral range without returning to the near zero rates that defined the previous era.

“With

respect to monetary policy, we described 2025 as an environment of higher rates that would likely remain in place longer than many investors expected.”

In summary, we believe our macro framework highlighted the right risks, described the broad economic trajectory reasonably well, and avoided anchoring our base case to an outright recession that never fully arrived.

Our clearest underestimation in 2025 was not the macroeconomy, but investor behavior.

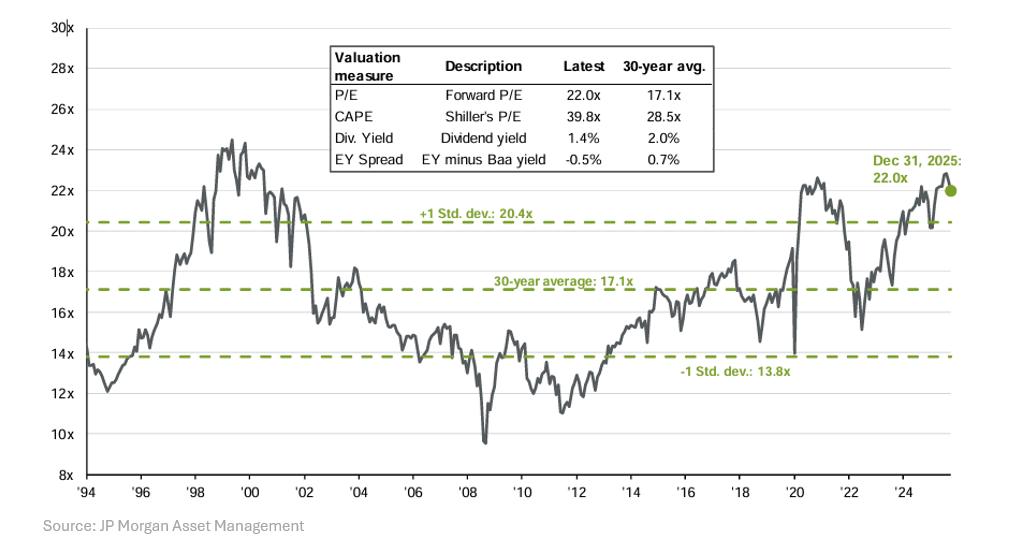

We were appropriately concerned about rich valuations, narrow leadership in mega cap technology and AI related names, and traditional warning signals such as the inverted yield curve and the reverse yield gap.

Those concerns were validated by the sharp decline following the April tariff announcement, which took the S&P 500 down nearly 19 percent from its peak and brought it within a hair of a formal bear market.

The chart below illustrates just how elevated valuations were heading into 2025 (and again heading into 2026). When the S&P 500 trades more than one standard deviation above its 30-year average price to earnings ratio, it signals statistically unusual territory and heightened vulnerability to corrections.

What we did not fully anticipate in the spring of 2025 was the speed and strength of the recovery and the willingness of investors to pay even higher multiples for resilient earnings and perceived winners in the artificial intelligence buildout. From the April low, the index recovered its losses in roughly 55 trading days, pushed through to new highs by midyear, and finished 2025 with a full year return near 18 percent.

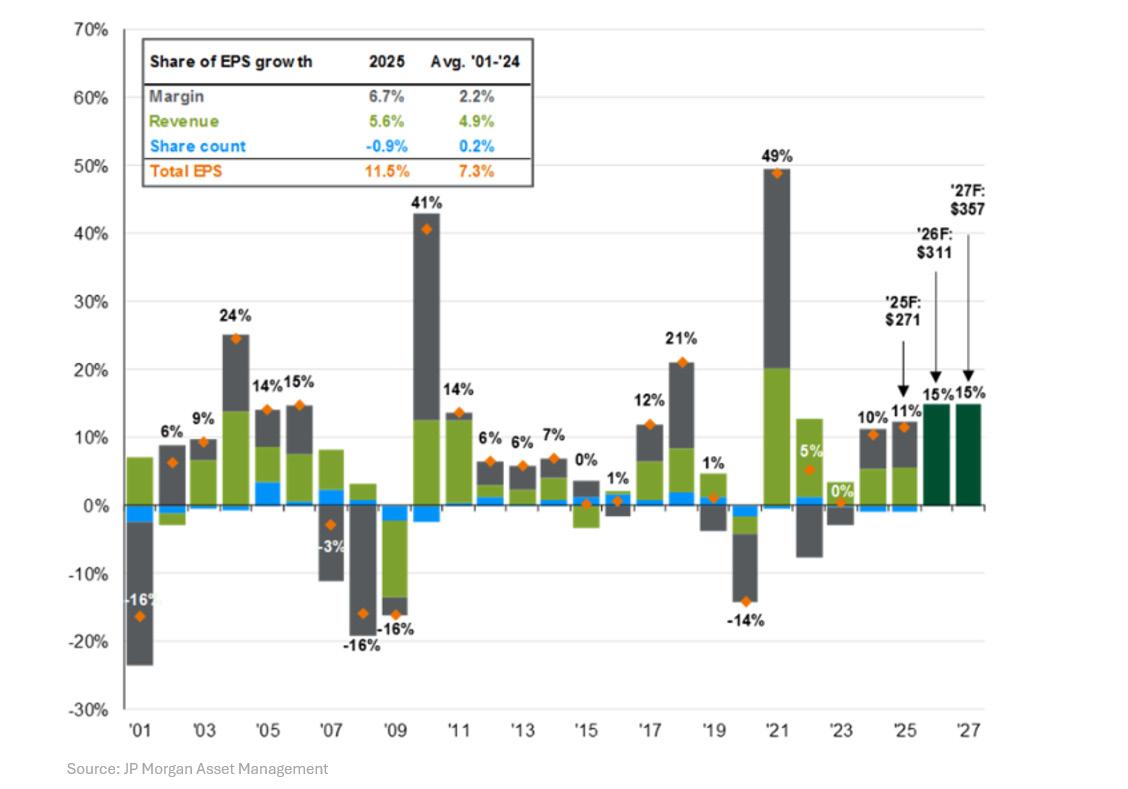

Earnings growth also surprised modestly to the upside relative to our expectations. Consensus projections in the mid-teens looked optimistic at the start of the year, and our internal work suggested something closer to high single digit growth. Actual earnings for the S&P 500 landed in the low double digits, below the initial consensus, but somewhat above our central estimate. More importantly, valuation multiples expanded instead of contracting, especially in sectors and companies tied to AI and high margin services.

“What we did not fully anticipate in the spring of 2025 was the speed and strength of the recovery and the willingness of investors to pay even higher multiples for resilient earnings and perceived winners in the artificial intelligence buildout.”

We were right to identify valuation risk, but we underestimated the extent to which strong profitability, ample liquidity, and a compelling innovation narrative would allow markets to stretch those valuations further.

On trade policy, we devoted substantial attention to tariffs throughout 2025, and that focus proved warranted. We warned that markets would experience heightened volatility as the administration pursued a more aggressive trade stance.

The April second Liberation Day announcement triggered a sharp, global selloff and a near bear market drawdown in the S&P 500.

The effective U.S. tariff rate rose to its highest level in many decades, with average rates temporarily reaching many times their January levels, and tariff receipts for the federal government surged into the hundreds of billions on an annualized basis.

At the same time, several dynamics helped to blunt the feared damage. U.S. companies accelerated efforts to diversify supply chains, shifting sourcing away from heavily targeted countries toward trade partners such as Mexico, Vietnam, and Taiwan. Many firms absorbed a portion of the tariff burden through margin compression, process efficiencies, or price discrimination across customer segments. Consumers adjusted behavior as well, substituting away from the most affected goods and toward less impacted alternatives.

We anticipated volatility and correctly identified tariffs as a central risk factor. What we did not fully appreciate was how quickly markets would learn to discount the administration’s pattern of announcing aggressive measures, then tempering or modifying those measures through pauses, exemptions, or negotiated adjustments.

Finally, 2025 reinforced an important lesson about traditional indicators. Several tools that historically have served as reliable warning systems for recessions and bear markets, including the Leading Economic Index and the shape of the yield curve, signaled heightened risk for an extended period. In earlier cycles, those signals almost certainly would have been followed by a clear recession.

This cycle unfolded differently. Structural shifts related to the post pandemic economy, a services dominated output mix, aggressive fiscal policy, and the emergence of AI driven capital spending weakened some of those historical relationships. These tools still have value, but they can no longer be used as simple on or off switches. They should be interpreted in a richer context.

The broader point is that it is possible to be broadly correct about risk and still be surprised by how long markets can look through that risk when earnings remain healthy and powerful structural themes capture investor imagination.

Several lessons from 2025 stand out, especially when structural forces such as liquidity and innovation are at work. Momentum deserves respect, not dismissal. Reflecting on 2025, the following lessons stand out and will inform us how we approach the years ahead.

• First, valuations are poor timing tools over short horizons. Rich starting valuations did not prevent the stock market from becoming even richer. They still matter a great deal for long-term return expectations, but they can be unreliable as predictors of when, or how sharply, a correction will occur.

• Second, markets proved able to absorb more policy noise than standard models would have suggested. Strong corporate profitability, expectations for growth tied to artificial intelligence, and moderating inflation combined to help investors look through even very intense volatility related to trade policy and geopolitics.

• Third, the adaptability of U.S. corporations once again showed itself to be a powerful offset to shocks. Companies were quick to adjust supply chains, pricing, and cost structures in response to changing conditions. Any serious attempt to gauge the likely impact of future disruptions will likely take this agility into account.

• Fourth, several of the traditional indicators that we and others have relied upon require reinterpretation in a changed world. Yield curve inversions, declines in leading economic indices, and some valuation measures clearly signaled elevated risk. At the same time, their historical relationships with recessions and bear markets proved weaker in this cycle. Structural shifts related to the post pandemic economy, artificial intelligence, and a much more activist fiscal environment complicate simple historical analogy.

• Fifth, thoughtful scenario planning proved to be more valuable than point forecasts. Our midyear framework of bull, base, and bear cases turned out to be the right way to think about a wide range of outcomes. Where we fell short was in the probabilities we implicitly assigned. In practical terms, we did not give enough room for the more optimistic path to play out. Going forward, we intend to be clearer about the probability ranges we attach to each scenario and more explicit about what would have to be true, both in the data and in policy, for those scenarios to materialize.

• Finally, and perhaps most importantly, the discipline of long-term investing remains paramount. Even considering our cautionary tone, our firm stayed invested in high quality, globally diversified portfolios, and resisted the temptation to react to each new headline in 2025 – and we were rewarded for our patience. Our non-hedged international equity positions performed particularly well as the U.S. dollar retreated, as did our exposure to gold mining companies.

Once again, the path turned out to be asymmetrical, volatile, and at times frustrating. As we long believed, process matters more than prediction and persistent ownership of productive assets still appeared to be the most promising way to build and preserve wealth.

Throughout 2025, our actual positioning remained disciplined and consistent, even as our narrative tone evolved. That discipline, anchored in clients’ goals and time horizons, aimed to serve them better than any attempt to outguess each twist in the market.

With that context, we turn to the year ahead.

The global economy enters 2026 growing more slowly than in the immediate post pandemic years but still expanding. The U.S. remains at the center of that growth, supported by strong corporate balance sheets, easier financial conditions than a year ago, and a powerful cycle of capital investment focused on data centers, semiconductors, and related infrastructure.

Our base case estimate is that U.S. real gross domestic product will grow at roughly 2.5 to 3 percent in 2026. Several forces support that view. Capital expenditures are robust, particularly in technology and industrial segments tied to AI and automation. The policy mix for business is friendlier than it has been in some time, with full expenditures for many investments, steps toward deregulation, and a leaner regulatory posture in several sectors. Monetary policy has shifted from clearly restrictive toward something closer to neutral. Fiscal spending on infrastructure and strategic industries continues to filter into the real economy.

Against that, we must weigh the drag from higher tariff levels than in prior decades, a labor market that is no longer as tight as it once was, and pockets of consumer stress, especially among households facing high housing costs and rising credit card balances.

There are a handful of prominent commentators who are forecasting significantly higher economic activity for the coming year. Louis Navellier stands as the most vocal advocate for 5% U.S. GDP growth in 2026, a forecast that places him well above the consensus. Mr. Navellier’s call rests on a distinctive thesis of structural tailwinds and disinflationary forces driven by four interlocking factors:

• The onshoring of manufacturing

• A narrowing of the trade deficit

• The continued AI/data center investment boom

• A deflationary backdrop enabling easy monetary policy

Such optimistic projections would require productivity growth exceeding 3% annually (vs. 1.5% historical average) and no geopolitical or financial market disruption. While theoretically possible, a 5% rate of economic expansion would most likely depend on all the above forces aligning perfectly.

On inflation, we predict price pressures to remain above the Federal Reserve’s formal target but lower than the peaks of this cycle. A reasonable expectation is for core inflation to settle in the mid 2 percent range by late 2026, in an environment where 2 percent is less a ceiling and more of a floor absent a sharp downturn. The Federal Reserve has already delivered a substantial adjustment from peak policy rates, and further moves are likely to be gradual and data dependent, with the goal of keeping real rates modestly positive without stalling the expansion.

Fiscal deficits remain large and persistent, which exerts upward pressure on long term yields and complicates the Fed’s task. Our working assumption is that the 10-year Treasury yield trades in a broad band that is higher than the pre-pandemic lows but lower than the extremes seen during the inflation scare, a range that allows fixed income finally to offer a reasonable real return without becoming a dominant headwind to equities.

In short, we expect the expansion to continue, supported by business investment, a still resilient consumer, and a more business friendly policy environment, but with less room for policy error than in prior years.

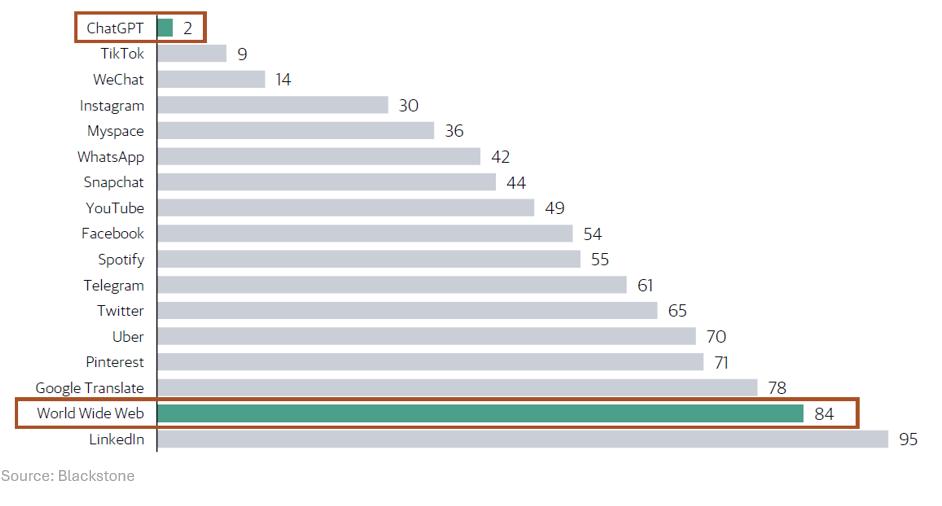

Artificial intelligence has moved from a technological breakthrough to a transformative economic force. It is beginning to reshape expectations for productivity, growth, and competitiveness across a wide range of industries.

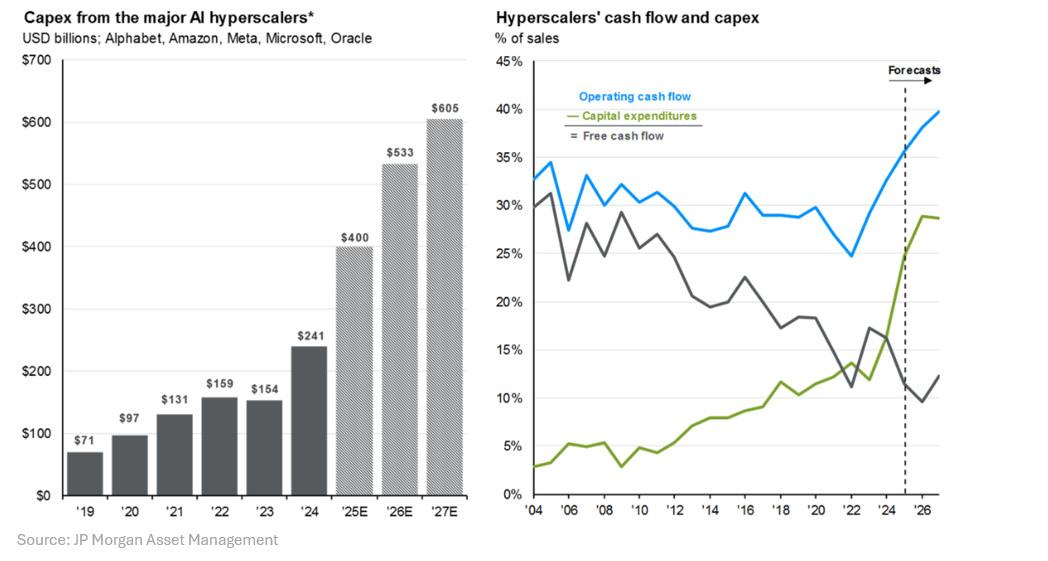

Several features distinguish the current AI cycle from past episodes of enthusiasm. First, the largest investments are being financed from the cash flows of some of the world’s strongest companies, rather than from fragile leverage or speculative excess. That fact speaks both to the strength of corporate balance sheets and to how essential these expenditures have become.

Second, capital spending on AI infrastructure has reached well over two hundred billion dollars per year and is still rising. (JP Morgan Asset Management) Third, demand for computing capacity continues to run ahead of supply. The primary constraints are physical infrastructure and power, not access to capital.

Beyond the data centers and hardware, AI is gradually changing how companies operate. Firms are compressing software development cycles, improving decision making with better analytics, automating routine workflows, and engaging with customers in more personalized and efficient ways. In many organizations, these changes are still in their early stages, but the direction of travel is clear.

The scale of capital commitment is extraordinary and continues to accelerate.

For investors, the crucial takeaway is that AI’s long-term effect on corporate profitability hinges on advancements in productivity. A recent analysis from Vanguard compared the current wave of AI related spending to earlier periods of major capital expansion, including the buildout of railroads in the nineteenth century and the late 1990s surge in information and telecommunications investment.

Those episodes delivered significant long-term gains, but the benefits were uneven. The companies that won were not necessarily those that spent the most. They were the ones that invested wisely and converted capital into higher levels of productivity and economic returns.

We see AI similarly. Valuations of AI focused companies could rise and fall, sometimes sharply. Over the long term, however, AI technology is likely to push meaningful productivity growth across the economy.

It is also a disruptive force that will pressure business models and earnings power in certain sectors. Staying ahead of that disruption, or at least not being blindsided by it, could be critical.

Our conviction is high that AI will be a major driver of economic and earnings growth over time. The investment implications could be significant and could develop rapidly in the years ahead. Capturing that opportunity requires a focus on business fundamentals and capital discipline, not simply exposure to every company that uses the letters “AI” in its marketing.

U.S. equities remain in a bull market that began in late 2022. Cumulative gains over that period are large, but still within the range of prior bull markets in both duration and magnitude, particularly when viewed in light of strong earnings and the emergence of a genuine innovation cycle.

At the index level, valuations are undeniably elevated. The S&P 500 trades around the low to mid 20s on forward earnings, compared with a historical median closer to the mid-teens. Profit margins remain near record levels, reflecting a combination of pricing power, cost discipline, and efficiency gains. Market leadership, while somewhat broader than at the start of the cycle, is still heavily influenced by a relatively small group of large companies tied to technology and AI.

These facts have two important implications. First, longterm return expectations from current levels must be more modest than they were when valuations were lower. Second, expensive markets can stay expensive for longer than many investors find comfortable when profitability is strong and liquidity is ample.

We predict earnings for the S&P 500 to grow in the high single digit to low double-digit range in 2026, somewhat slower than the more optimistic projections but supportive of continued, if less dramatic, price appreciation.

Our base case estimate is for total returns in the mid to high single digits, with the understanding that the path will likely be uneven and that index level outcomes will mask substantial differences across sectors and individual companies.

Outside the U.S., the picture differs. Valuations in developed international markets are meaningfully lower, even after adjusting for differences in growth prospects and sector composition. Earnings momentum in parts of Europe and Japan has improved from a low base. Several non-U.S. markets stand to benefit from capital spending tied to reshoring, infrastructure, and energy transition, as well as from a more favorable starting point on price and expectations.

We believe a disciplined global equity allocation remains warranted, with a continued but not exclusive emphasis on U.S. quality companies, combined with selective exposure to international businesses that are well positioned to participate in these trends.

For several years, bonds offered little in the way of real return and did not consistently serve as reliable diversifiers, that has changed.

With policy rates now well above zero and longer-term yields at more normal levels, high quality fixed income once again provides a reasonable starting yield and meaningful potential for positive after inflation returns. We do not expect a repeat of the large capital losses that bond investors experienced when rates were rising from unusually low levels earlier in this cycle. Instead, we predict 2026 is likely to be a more traditional year for fixed income, where most of the return comes from the coupon and price movements are more contained.

Within credit, corporate balance sheets remain generally healthy, but spreads in many segments have compressed to levels that leave less room for error. That argues for a bias toward quality and careful sector selection rather than a broad search for yield at any price.

Private markets continue to present attractive opportunities for appropriate clients. Private credit can offer a meaningful yield premium with better structural protection in many cases. Private equity and real assets provide access to businesses and themes that are not always well represented in public markets, including parts of the AI and infrastructure buildout, energy systems, and niche segments of healthcare and technology. Here again, manager selection, underwriting discipline, and alignment of interests are critical.

We expect the investment environment in 2026 to be shaped by several cross currents that deserve particular attention.

One is valuation and concentration. U.S. large cap equities are priced at levels that assume continued growth, high margins, and a relatively benign policy and inflation backdrop. Leadership is still concentrated among a small number of very large companies. This is not unprecedented, but it does increase the potential impact if sentiment toward these leaders changes.

A second theme is the ongoing realignment of trade and tariff policy. The effective tariff rate in the U.S. is higher than it has been in many decades. Companies have responded by diversifying supply chains, shifting production, and adjusting pricing. These moves have mitigated the immediate growth damage but contributed to persistent goods inflation and have required significant capital outlays. They have also increased the importance of geography and policy in investment analysis.

A third is the evolution of inflation and interest rates. We are unlikely to return to the combination of near zero short term rates and very low long-term yields that characterized the years following the global financial crisis. The more likely outcome is a world of moderately positive real rates, somewhat higher average inflation than the pre pandemic decade, and greater dispersion across regions and asset classes. That environment has different winners and losers than the one many investors grew accustomed to over the prior 15 years.

Finally, the consumer remains both resilient and uneven. Aggregate spending has held up, particularly in services and experiences, but stresses are more visible among younger and lower income households. Housing affordability is strained in many markets. Credit card delinquencies have risen from unusually low levels. Retail sales in real terms have grown more slowly than headline figures suggest. None of this implies an immediate collapse in consumption, but it argues for nuance. The story is not uniformly strong or uniformly weak.

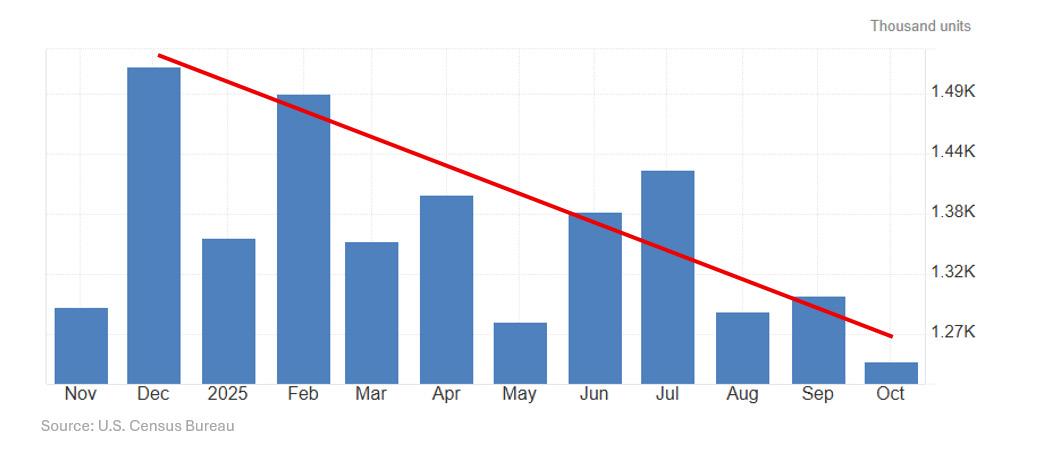

Housing activity remains one of the clearest indicators of that consumer strain. New construction has struggled to gain momentum in the face of elevated mortgage rates and persistent affordability challenges.

A contrarian view of the future glide path for the U.S. economy can be found in the Conference Board’s Leading Economic Index mentioned earlier in this report. The U.S. LEI fell again in the fourth quarter of 2025.

The Conference Board’s Leading Economic Index has long been regarded as one of the most reliable forward

indicators of U.S. economic activity, historically signaling turning points in the business cycle roughly seven months in advance. The LEI successfully predicted the 2001 recession and the 2008 financial crisis, establishing a track record that made it a cornerstone of economic forecasting for policymakers, economists, and investors alike.

This said, the indicator’s reliability has deteriorated sharply in recent years. Beginning in mid-2022, the LEI has signaled an imminent recession continuously; first for late 2022, then early 2023, mid-2023, late 2023, and into 2024 and 2025. Yet no recession materialized. Instead, the U.S. economy grew at an above-trend pace of 2.5% in 2024, faster than the decade average of 2.3%.

By late 2025, the LEI had declined for over three years straight - a pattern unprecedented in modern economic history without an accompanying recession. This divergence became so pronounced that the Conference Board itself backed away from its recession forecast in early 2024, acknowledging that “the leading index currently does not signal recession ahead”. Given the many conflicting

economic signals, it has become exceedingly difficult to develop high conviction forecasts for the economy and the markets. It is important to note that given our constructive view, the economy and the markets are not without risk. The unemployment rate has edged higher, and pockets of the economy have softened. Tariff policy, while less severe than some initially feared, has nonetheless created real headwinds for many businesses. Yet recent record highs in equities would suggest that investors are behaving as though capturing the next wave of growth matters far more than the near-term uncertainties swirling around them.

That calculus may prove sound, but it also underscores just how pivotal execution and earnings growth will be in justifying current valuations.

The upcoming U.S. midterm election adds another layer of uncertainty. Politics is not our business, and our role is not to predict electoral outcomes or advocate for a particular party. Our responsibility is to understand how potential policy paths might interact with an already complex economic and market environment.

This said, this year’s mid-term election cycle represents a principal source of macro and market risk because they sit at the intersection of fiscal policy, trade, and already elevated political polarization. As our colleagues at First Trust have noted, the new Congress elected in November “could have a massive impact on fiscal policy for years to come.” The 2026 election will not occur in a vacuum; it overlays a system that is late-cycle, unequal, and unusually sensitive to policy shifts.

On the economic side, the central risk channel we are monitoring is policy uncertainty around taxes, spending, and trade. Lawmakers are under growing pressure to make tax pledges that may box them in, while major fiscal issues remain on the table: reauthorization of the Highway Trust Fund, the long-term financing of Social Security, and the eventual fiscal “cliff” created by recent temporary tax provisions.

We believe that uncertainty over tariffs, immigration, federal employment, deficit trajectories, and the structure of tax cuts can act as a meaningful drag on growth by causing businesses to delay investment and hiring and by making the Federal Reserve more cautious about additional rate cuts.

We recognize that the U.S. has many of the ingredients of an economic boom on the supply side, but we also understand the forces that have the potential to cap real GDP growth closer to 2 percent rather than the 4–5 percent some more optimistic forecasters are predicting. Election outcomes that tilt toward larger deficits, renewed regulatory burdens, or a reversal of recent pro-investment tax rules could aggravate that tension and undermine the productivity gains we are hoping to see.

For equities, we want to be transparent about what history suggests. Mid-term years are among the most volatile points in the four-year political cycle, and current conditions suggest that 2026 is unlikely to be an exception. The average intra-year drawdown in mid-term years is roughly 19 percent, compared with about 12 percent in the other three years of the cycle. It is common to see a significant decline in the S&P 500 in the 12-18 months before election day, often 10-20 percent or more (Morningstar). Our experience has shown us that such declines themselves become buying opportunities once the political outcome is known and policy risk is repriced.

The long-run data is clear: markets tend to underperform in the 12 months leading up to midterms and outperform in the 12 months after, as uncertainty about who controls Congress and what the legislative agenda will be is eventually resolved. The risk, in practical terms, is not necessarily negative full-year returns, but a meaningful probability of a sharp and uncomfortable drawdown at some point between now and November.

This particular mid-term carries additional sources of volatility that deserve our attention because they are unusual and consequential. We are contending with a new Federal Reserve chair, a pending Supreme Court ruling on the administration’s tariff regime, and the risk of a partial government shutdown tied to disputes over funding priorities, all of which are highly politicized and likely to be weaponized in the campaign environment.

We have also observed that markets have learned how to trade the current administration’s tactics (example: treating aggressive policy headlines as opening bids rather than final outcomes), but we still expect further bouts of volatility in 2026 from policy pronouncements, geopolitical tensions, and the midterms themselves. Many of the recent economic policy moves appear aimed squarely at voter sensitivities around prices and housing rather than long-term efficiency, a dynamic that can be market-moving in the short term even if the macro effect proves more muted over longer horizons.

Finally, we want to emphasize that the composition of the post-election government matters less as a mechanical driver of returns than as a determinant of the policy path around key fault lines. Our experience with historical data shows that markets have done reasonably well under various configurations of party control, with divided governments often associated with smaller expected swings in tax and spending policy and therefore less long-run policy risk, even if it also implies more legislative gridlock.

However, 2026 is not an average mid-term: it coincides with looming fiscal deadlines, unsettled trade policy, and a late-cycle expansion that is already marked by high valuations and uneven gains across households. From our perspective, the real risk is that a contentious election year amplifies policy uncertainty at exactly the moment when the economy’s underlying momentum is most dependent on clear incentives for investment, continued deregulation, and the productive deployment of AI-related capital spending.

This combination (rich starting valuations, historical mid-term volatility patterns, and a consequential policy calendar) raises the odds that even a fundamentally growing economy could experience substantial equity market turbulence as investors attempt to handicap not just who wins in November, but what that will mean for the rules of the game in the years ahead.

As we assess the landscape heading into 2026, it becomes clear that Wall Street’s expectations for the S&P 500 this year span a notably wide range. The most bearish forecasts suggest declines exceeding 10 percent, while the most optimistic strategists project double-digit gains. What emerges from this diversity is a consensus clustering around 7,500 for year-end, representing approximately 9 to 10 percent upside from our current starting level near 6,850 to 6,900.

Yet beneath this headline figure lies genuine disagreement among thoughtful analysts. Their divergence stems largely from differing assumptions about three critical variables: whether artificial intelligence will deliver the earnings growth the market is pricing in, how the Federal Reserve will navigate the path forward, and whether current valuations can hold or must eventually compress. In our view, understanding these fault lines in the forecasting community is as important as the consensus target itself.

“In our view, understanding these fault lines in the forecasting community is as important as the consensus target itself.”

Here are what some of our favorite commentators are saying (as of mid-January):

Ed Yardeni: Yardeni maintains a constructive but measured outlook, projecting the S&P 500 will reach 7,700 by year-end 2026. His forecast rests on record corporate earnings momentum, with forward EPS approaching $309 and broadening participation beyond the "Magnificent Seven." He acknowledges valuation pressure but believes expanding earnings power across the "Impressive 493" (S&P 500 ex-mega-caps) can sustain the rally. Yardeni has also articulated a decade-end target of 10,000, emphasizing AI-driven productivity gains and resilient economic growth.

Brian Wesbury: Wesbury remains the most prominent bear, arguing that current valuations are unsustainable. Using a 4.0% 10-year Treasury yield and 10% corporate profit growth, his fair-value model suggests the S&P 500 is worth only 5,000—implying roughly 25% overvaluation at current levels. While not offering a precise 2026 target, his commentary suggests a downside scenario where the index trades around 6,200, reflecting his view that "we can't reasonably summon a forecast of a rising stock market in 2026."

Rick Reider: Rieder, as BlackRock's Global Fixed Income CIO, focuses more on credit markets but projects 1015% returns for equities in 2026, accompanied by "real volatility." He emphasizes that 2026 will favor "investors, not gamblers," warning that the era of broad-based betadriven gains is over. His equity outlook is contingent on AIdriven productivity supporting earnings, but he cautions that investor complacency and narrowing leadership create downside risk.

Bob Doll: Doll does not cite a specific S&P 500 index level but forecasts a "high-risk bull market" with equities failing to deliver double-digit returns for only the third time in a decade. His 10-prediction framework calls for modest P/E compression, earnings growth falling short of the 14% consensus, and a "coupon-ish" year for stocks. His base case implies total returns of 0-5% for 2026, with significant volatility around AI investment, sticky inflation near 3%, and widening credit spreads.

The median strategist target of 7,500 (9-10% upside) masks significant dispersion. The range from 6,200 (Wesbury) to 8,100 (Oppenheimer) reflects genuine uncertainty about whether AI can deliver enough earnings growth to justify current multiples or whether valuation gravity will reassert itself.

Most strategists expect mid-to-high single-digit earnings growth (12-14% consensus), but disagree on whether

P/E multiples will expand, hold steady, or compress under inflation and policy uncertainty.

Bottom Line: 2026 forecasts reflect a market at an inflection point—betting on AI productivity to sustain the bull run while acknowledging valuations leave minimal margin for error. volatility around AI investment, sticky inflation near 3%, and widening credit spreads.

The title of this report, “High Gear, Low Visibility,” captures how we see the coming year. The economic engine is still running at a good speed, but the windshield is less clear than in more ordinary times.

Our base case estimate is that the global expansion continues in 2026, led by the U.S. We predict real growth in the U.S. of roughly 2.5 to 3 percent, supported by strong capital investment, a more business friendly policy environment, and a still resilient, if more stretched, consumer. We predict inflation should remain above 2 percent but below the recent peaks, and interest rates should settle into a range that is more supportive than in 2023, but tighter than the ultra-easy conditions of the prior decade.

In that environment, we believe corporate earnings can grow in the high single digit to low double-digit range. Equity markets can deliver mid-to-high single digit total returns, with meaningful volatility along the way. Fixed income can finally offer positive real returns and resume its role as a stabilizer in portfolios.

The risks to this outlook are real. Elevated valuations and narrow leadership leave little margin for disappointment. Inflation could prove more stubborn than we expect, limiting the Federal Reserve’s flexibility. Tariff policy and geopolitics could trigger periods of sharp volatility or localized damage. Consumer stress may deepen more quickly than the aggregate data now suggest.

Bullish Case Factors:

• AI infrastructure spending surging past $200 billion annually

• Enterprise AI adoption moving from experimentation to workflow automation

• Record corporate profit margins supported by pricing power and cost discipline

• Fed pivot toward neutral policy (three 25bp cuts projected)

• Fiscal stimulus from infrastructure and deregulation

Bearish Case Factors:

• Elevated starting valuations (~22x forward P/E vs. historical ~16x)

• Narrow market leadership (Magnificent Seven still ~30% of index)

• Sticky inflation above Fed’s 2% target, limiting rate cut flexibility

• Tariff policy uncertainty and potential margin compression

• Consumer stress signals (rising credit card delinquencies, housing affordability)

Even so, the balance of evidence argues for a constructive, but not complacent, stance. The U.S. remains a powerful engine of innovation and corporate adaptability. The AI investment cycle is still in its early stages. Policy, while noisy, is more supportive of business investment than it was several years ago. History suggests that when capital is being deployed into productivity enhancing projects and profitability remains high, the default assumption should be continued, if slower, progress rather than imminent collapse.

Within this backdrop, our positioning for 2026 reflects constructive realism.

We intend to keep clients meaningfully invested in productive assets while aiming to maintain sensible risk controls. In practical terms, that means continuing to emphasize high quality companies with strong balance sheets, durable cash flows, and real pricing power. It means looking to maintain a balanced exposure to growth and value, rather than making an all or nothing bet on either style. It means proposing a thoughtful allocation to international markets where valuations and earnings cycles are more favorable than in prior years.

In fixed income, we will seek to lock in attractive yields in high quality bonds without reaching aggressively for incremental spread in weaker credits. In private markets, we will continue to focus on managers and strategies that align with longterm structural themes and that demonstrate discipline in capital deployment.

Most importantly, we will look to align portfolio decisions with each client’s specific goals, time horizon, cash flow needs, and tolerance for volatility. Outlooks and forecasts are tools, not anchors. When conditions change, we will adjust as needed, always with an eye toward long-term wealth creation and preservation.

“We intend to keep clients meaningfully invested in productive assets while aiming to maintain sensible risk controls.”

The investment environment at the start of 2026 is not simple, but it is not hopelessly obscure, either. It is a blend of powerful tailwinds and serious headwinds.

On one side stand, innovation, profitability, and a policy mix that is more welcoming to capital investment. On the other stand, valuations that are higher than average, political and geopolitical uncertainty, and a late cycle economy that is working through the aftereffects of an unusual period.

Our stance at Clearwater Capital Partners is sober, but upbeat. We do not dismiss risk, and we are not indifferent to price. At the same time, we have seen enough over the past twenty years to know that betting against human ingenuity and the adaptability of free enterprise has rarely been a winning long-term strategy.

The path ahead will not be straight; it rarely is. The markets will do what they do. The economy will ebb and flow. Politics will remain noisy and sadly divisive. What will not change is our commitment to the principles that have guided this firm since its founding.

We will continue to do the work. We will review the data, weigh the scenarios, and test our assumptions. We will communicate clearly, act with discipline, and stay focused on helping you and your family navigate whatever comes next.

For patient investors anchored in a thoughtful plan, 2026 offers ample opportunity to turn a time of rapid change into enduring progress.

Thank you again for the trust you place in us. It is an honor to serve you, and we are excited at the prospect of achieving great things together in 2026.

In 2006, this firm began with a single desk, a clear vision, and the belief that meaningful work is built one relationship at a time. As we step into 2026, we proudly celebrate twenty years of growth, partnership, and purpose.

What started as a team of one has grown into a team of twenty nine dedicated professionals. Along the way, we have evolved not only in size, but in perspective. This year is more than a business milestone, it is an opportunity to bring you along the journey with us. We will look back at the moments that shaped us, celebrate the people who stood beside us, and look ahead to what is still to come.

Reaching twenty years invites reflection. It reminds us to pause and appreciate how far we have traveled and why we began in the first place. For us, this is embodied in our motto this year while celebrating 20 years,

“Time, wealth, and what matters most.”

It is a principle that guides how we serve our clients, support one another, and make decisions for the future.

Over the past two decades, our team has grown with the families and businesses we are honored to work alongside. A focused vision expanded into a collaborative group of advisors, planners, and specialists united by shared values and a commitment to excellence.

This commemorative year brings together the voices and insights of our leadership team, highlighting the experience, trust, and teamwork that continue to shape our culture and business.

As we celebrate this anniversary, we do so with intention. We invite our community to stay connected through our communications and social channels for announcements, event details, and behind the scenes highlights as the celebration continues.

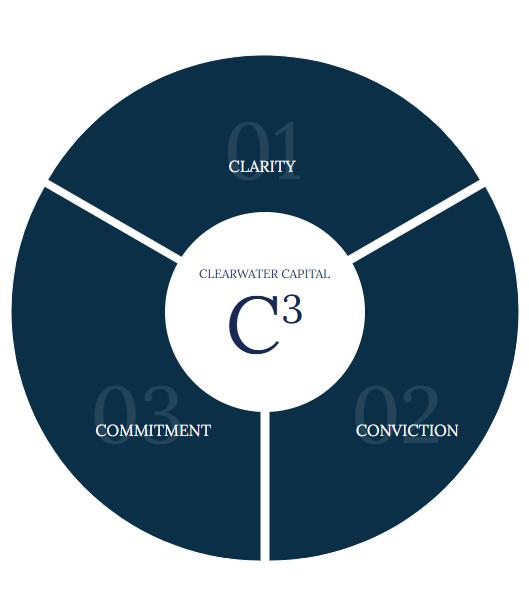

Successful wealth management is the product of clear thinking, hard work, and consistent follow-through. At Clearwater Capital, we have developed a rigorous framework for decision-making that we call C3. This disciplined process guides successful individuals and families through the prioritization of long-term objectives, the evaluation of high impact tactics, and the deliberate execution of strategies designed to endure.

Identify / Prioritize Objectives

Establish Assumptions

Collect / Organize Data

Model and Test Scenarios

Interpret Findings

Establish Path Forward

Initiate Action Plan

Implement

Monitor / Maintain

The opinions presented are those of Clearwater Capital Partners and John Chapman, Chief Executive Officer, and Chief Investment Strategist, as of January 2026 and may change, without notice, as subsequent economic and market conditions vary.

This material is presented as opinion and commentary. It is not intended to be relied upon as forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. It is strictly intended for educational purposes only.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Clearwater Capital Partners to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. Artificial Intelligence (QAI) tools were used in the sourcing of content for this report. All information originating using AI was critically evaluated, verified, and refined in the writing methodology of this report. The observations and conclusions included in this report reflect our own analysis and understanding of the economic topics covered.

Past performance does not guarantee future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. No investment or investment strategy is risk free.

International investment involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments.

Index performance is referenced for illustrative purposes only. You cannot invest directly in an index. The Dow Jones Industrial Average is owned by S&P Global, the S&P 500 is a registered trademark of The McGraw-Hill Companies, and The Russell 3,000 Index is maintained by FTSE Russell. Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

The Conference Board Leading Economic Index (LEI) is a composite index of leading, coincident, and lagging indicators produced by The Conference Board serving as summary statistics for the U.S. economy. The Conference Board Leading Economic Index (LEI) is a trademark owned by the Conference Board, Inc. in the United States and other countries.

The two main risks related to fixed-income investment are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments.

High yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Municipal bonds are subject to availability and change in price. They are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

The payment of dividends is not guaranteed. Companies may reduce or eliminate the payment of dividends at any given time.

Nothing contained herein is offered as tax advice. Please consult qualified professionals with any tax planning needs or tax questions you may have.

Please consult with a qualified investment professional before investing.

Investment Advice offered through Clearwater Capital Partners, a Registered Investment Advisor.

“We