Gerry Gaetz, former President and CEO, Payments Canada

Jean-Michel Godeffroy, former Director General of Payment Systems and Market Infrastructure, European Central Bank (retired)

Mehdi Manaa, CEO, Buna and former Deputy Director General, Directorate General Market Infrastructure and Payments, European Central Bank

Tze Hon Lau, Director & Specialist Leader (Payment Systems), Payments Department, Monetary Authority of Singapore Fiona van Echelpoel, Deputy Director General, Directorate General Market Infrastructure and Payments, European Central Bank

Ewropa Business Center, Level 3, Suite 701, Dum Karm Street, Birkirkara BKR 9034, Malta. https://cbpn.currencyresearch.com/

Our Charter Members generously subsidise annual CBPN subscriptions for central banks in 40+ global jurisdictions.

A second round of testing for Brazil’s Drex pilot, India’s UPI to expand to 20 countries by 2029, Central Bank of Ireland launches innovation sandbox, new RTGS systems for Guatemala and Sri Lanka, and other global developments 4//

15// INSIGHT

Piet Mallekoote, former member of the European Central Banks’s digital euro Market Advisory Group, highlights the background of the digital euro project and provides an overview of the state of play and challenges

20// FEATURE

The European Central Bank’s Holger Neuhaus and Mirjam Plooij detail the Eurosystem’s exploratory practical work to analyse the use of DLT for the settlement of wholesale financial transactions

24// PEOPLE ON THE MOVE

Alexis Brito to lead Banco de Cabo Verde’s payment system oversight unit, Namibia’s central bank appoints Irene Venter deputy director of digital payments oversight, licensing, and policy research, and more

Contributors

Piet Mallekoote

Former Member, Digital Euro Market Advisory Group, European Central Bank

26// BOOKS

A brief look at Neha Mehta’s One Stop, a recent book offering readers a comprehensive understanding of super apps and their transformative potential

28// INDUSTRY HAPPENINGS

Save the date for these upcoming payments events, including the AFI’s Global Policy Forum in San Salvador and the Central Bank AI Conference in London

29// REPORTS IN REVIEW

Research from Banco de Portugal on cybersecurity and Banco Central de Reserva del Perú on its retail payments interoperability strategy are among this month’s publications from global financial authorities

31// TALKING POINTS

A roundup of recent remarks from central bankers and industry experts on topics ranging from Chile’s agenda for payment systems to the Financial Stability Board on AI in finance

Neha Mehta

Holger Neuhaus

Head of Division, Market Innovation and Integration, European Central Bank

Mirjam Plooij

Team Lead, Market Infrastructure, European Central Bank LinkedIn

Brazil: New Drex Tests to Focus on Privacy, Smart Contracts

Brazil’s central bank has elected (link in Portuguese) to proceed with a second round of tests for its Drex pilot. According to Banco Central do Brasil (BCB), the privacy solutions tested during the wholesale CBDC pilot’s first phase “have not presented the necessary maturity to guarantee compliance with all legal requirements related to preserving citizens’ privacy.”

This new phase will also find BCB testing the implementation of smart contracts created and managed by the third-party participants in the DLT platform. This decision, the central bank says, is intended to allow its governance of third-party service provision to mature. In stage one, only the central bank was capable of developing contracts.

BCB will soon begin accepting applications from current participants in the Drex pilot to present use case proposals for the next round of testing, which is scheduled to commence in July. In Q3 of this year, the central bank will start accepting applications from prospective participants, who will be required to test the implementation of smart contracts no later than mid-2025.

In other news from the digital asset spectrum, BCB has indicated its next steps in the development of regulations

around crypto-assets and virtual asset service providers (VASPs). Among its activities, BCB will conduct a second stablecoin consultation later this year on the rules governing provider operations and authorisation; establish internal planning to regulate stablecoins that fall within the bank’s remit of payments, FX, and international capital flows; and develop and enhance its supplementary framework to cover entities such as VASPs. BCB’s regulatory proposals are expected by end-2024.

Meanwhile, Brazil’s wildly popular instant payment system, Pix, is being made available to foreign tourists visiting the country. PagBrasil, a Brazilian-based fintech, is launching Pix Roaming, a new feature that will integrate with the tourists’ banks and digital wallets. Tourists can scan a Pix QR code using their own banking app, and PagBrasil settles the amount with the merchant in Brazilian reais with funds taken from the payer’s digital wallet or bank.

Pix’s impact on the growth of digital payments is evident in the newly released 2023 Statistics on Retail and Card Payments in Brazil. Citing Pix as the chief source, the central bank says (link in Portuguese) the total number of cashless transactions in 2023 grew 75% from the previous year.

Bank of Japan Releases Progress Report on Digital Yen Pilot Program

In late May, Japan’s central bank published (PDF) the English version of its Progress Report on Central Bank Digital Currency Experiments, originally issued in April. Developed by the Bank of Japan's (BOJ) Payment and Settlement Systems Department, the report outlines the progress of the digital yen pilot program up to March 2024.

Since 2020, BOJ has been actively investigating a potential digital yen, completing two phases of proof-of-concept (POC) to assess its technical feasibility. POC Phase One ran from April 2021 to March 2022, followed by POC Phase Two from April 2022 to March 2023.

In April 2023, BOJ launched a pilot program to conduct further technical evaluations, while ramping up collaboration with the private sector. The pilot program focuses on two main pillars: 1) performance testing of the system developed by the central bank and conducting various desktop experiments on functions not implemented in the system and 2) the CBDC Forum, where BOJ’s Payment and Settlement Systems Department serves as the secretariat and engages private firms in discussions on retail payments issues.

BOJ describes its latest pilot program as “broader in scope” than the POCs, focusing less on the ledger in the central system and more on end-to-end coverage “ranging from endpoint devices to the central system.” Future tests will include intermediary systems, the intermediary network system, and endpoint devices, with plans for tests of the end-to-end process flow. Privacy will be a key consideration, with intermediary systems handling customers' personal information separated from those that process payments.

The system will feature a wide range of basic functions, including issuance, payout, credit transfer, acceptance, and redemption, along with additional functions to be added later like scheduled transfers, debit transfers, and balance/transaction inquiries.

More recently, the seventh meeting of the CBDC Forum took place, highlighting BOJ’s approach to a potential digital yen. The “Experts’ Meeting on CBDC” witnessed the publication (PDF, link in Japanese) of the secretariat’s presentation, a document detailing the central bank’s stance on the digital yen, the progress of the pilot tests, and the activities of the CBDC Forum to date, including the composition of its working groups. According to the document, summarised in English by Norbert Gerkhe, BOJ envisions a CBDC as a complementary payment method to cash, fostering private sector innovation in developing new and diverse payment services.

Digital Payments Slow, UPI Expands: RBI Annual Report

The Reserve Bank of India (RBI) is “increasingly becoming a catalyst of innovation in the payments’ ecosystem,” according to the reserve bank’s most recent annual report. Detailing the regulatory measures introduced during the 2023-24 fiscal year, RBI’s report provides a comprehensive overview of these regulations and includes a summary of the overall performance of India’s payments sector. Notably, it indicates a slight slowdown in the growth rate of total digital payments compared to the previous year and highlights ambitious targets for further expanding the reach of the Unified Payments Interface (UPI).

As outlined in the report’s Payment and Settlement Systems and Information Technology chapter, the country’s payment and settlement systems grew by 44% in terms of transaction volume during 2023–24, a moderate decline from the expansion of 57.8% in the previous year. By value, the registered growth was 15.8% in 2023-24, as compared to 19.2% in the previous year. At the same time, the share of digital transactions in the total volume of non-cash retail payments “increased marginally,” and RTGS transactions are up, along with the volume and value of retail transactions at 44.1% and 20.1%, respectively.

The Currency Management chapter offers valuable insights into the usage of the pilot digital rupee (e₹), both retail and wholesale (see page 157). While the current figures appear low, RBI notes that the use cases of CBDC “are still evolving.” For example, a new use case for the e₹-W pilot was introduced in October 2023 for facilitating interbank call money trades using e₹ without the involvement of the RTGS.

On a global level, the steady spread of the UPI will continue. As aligned with the goals laid out in the Indian Government’s Viksit Bharat 2047 — a new roadmap for making the country a completely developed nation by 2047 — the reserve bank and NPCI International Payments Limited (NIPL) plan to bring UPI

to 20 countries starting in 2024–25, with completion expected in 2028–29. The UPI is a made-in-India success story, with the platform surpassing 13 billion transactions in a single month in March 2024. RBI additionally intends to explore fast payment system collaboration with the European Union and South Asian Association for Regional Cooperation, as well as the potential for multilateral linkages.

The activities of RBI’s FinTech Department are showcased in the Regulation, Supervision and Financial Stability chapter, including a regulatory review of India’s fintech sector, the launch of the second edition of the HaRBInger 2023 global hackathon (the third edition was announced in early June), improvements in the account aggregator technological ecosystem, and more.

More recently, RBI Governor Shaktikanta Das launched three major fintech initiatives to boost growth in the sector: the PRAVAAH portal, the Retail Direct Mobile App, and a FinTech Repository. The PRAVAAH portal enables any individual or entity to apply online for various regulatory approvals “in a seamless manner,” the Retail Direct Mobile App provides retail investors access to the retail direct platform, and the FinTech Repository provides details on the country’s fintech sector “for a better understanding of the sector from a regulatory perspective.” Further, to encourage selfregulation, RBI has released the final draft of the Framework for Recognising Self-Regulatory Organisation(s) for FinTech Sector.

In “sustain[ing] its endeavour towards providing secure, accessible, affordable and efficient payment systems for every user of the country,” RBI is emerging as a key innovator in the global payments ecosystem. Despite a slight deceleration in digital payments growth, RBI's annual report underscores significant advancements, which are anticipated to continue as the reserve bank works towards the aims set out in its Payments Vision Document 2025 (PDF).

P.I.T. Exchange Hosts the Fed’s Mark Gould and Bank of England’s Victoria Cleland

It’s been an active month for The P.I.T. Exchange, the recently launched podcast from Currency Research. Recent guests from the Federal Reserve and the Bank of England, as well as leading industry innovators, delved into critical topics such as offline payments, AI, RTGS systems, fraud prevention, and much more.

Victoria Cleland, Executive Director for Banking, Payments and Innovation at the Bank of England, highlighted significant upgrades in the UK’s payments infrastructure, focusing on wholesale payment systems and RTGS system enhancements. She also discussed the benefits of 24/7 operating hours and promising developments such as non-bank PSPs gaining access to RTGS systems, the role of RTGS in efficient cross-border payments, and the UK’s upcoming mandate for enriched data exchange between financial institutions.

Mark Gould, Federal Reserve Financial Services Chief Payments Executive, joined the podcast to provide an overview of the Fed’s financial services group, which works to clear nearly $5 trillion in transactions every day. He emphasised the importance of ACH as the "workhorse" of the US payments system, the systemic role of FedWire, the resilience of cheques, and the rise of the FedNow instant payments service. Gould predicted that “the next ten years will be the most dynamic decade we've ever seen in payments.”

Additional insights were provided in episodes featuring the Digital Pound Foundation’s Claire Conby on digital currency use cases, Visa’s Alan Koenigsberg on global money movement, AI, and embedded finance, Crunchfish’s Joachim Samuelsson on the importance of offline payments, and FeatureSpace’s Aman Cheema on combating real-time fraud with AI and behavioural modeling.

ARTIFICIAL INTELLIGENCE

debit cards in Q2 2024. The Central Bank of the UAE will mandate all banks to issue Jaywan debit cards to their customers.”

Jaywan cards will be rolled out in phases, starting with physical card acceptance. Initially, acquirers such as Network International will activate Jaywan for merchants, with e-commerce acceptance to follow later this year. The cards will offer various benefits, including discounts on international

CARDS

CBDC

end of June.

The initiative, an addition to AEP’s growing suite of digital platforms, seeks to enhance e-commerce growth, increase payment options, and bolster the UAE's global competitiveness in the payments sector. The card scheme was developed as part of a strategic partnership with India’s NPCI International Payments Limited (NIPL), announced (PDF) in October 2023.

Commenting on the rollout, AEP Chief Operating Officer Andrew McCormack remarked, “We have an aggressive growth plan for Jaywan, to start issuing (con't in next column)

Over half of the respondents (54%) are currently experimenting with proofs-of-concept and one-third (31%) are running pilot tests. For those engaged in research (88%), efficiency, interoperability, financial inclusion, and payments safety are key concerns for retail CBDCs, while cross-border payments, programmability, and interoperability remain top considerations for wholesale CBDCs.

Meanwhile, stablecoin use is “still extremely limited” outside the crypto ecosystem, and around 60% of jurisdictions are developing regulatory frameworks for stablecoins and other crypto-assets.

BISIH’s mBridge Graduates to MVP

One of the BIS Innovation Hub’s (BISIH) flagship initiatives has advanced to a new phase, as the BISIH announced in early June that Project mBridge had progressed to the minimum viable product (MVP) stage. A collaboration between the BISIH, the Bank of Thailand, the Hong Kong Monetary Authority, the Digital Currency Institute of the People’s Bank of China, and the Central Bank of the United Arab Emirates, mBridge explores using a shared multi-CBDC platform, built on DLT, for instant wholesale cross-border payments and settlement.

Since the completion of the six-week pilot conducted in 2022, in which 164 payment and FX transactions totaling $22 million (€14.98mn) were settled directly on the mBridge platform, the participating central banks deployed validating nodes, commercial banks continued to carry out live transactions, and a governance and legal framework was developed in preparation for the MVP phase.

To expand the platform’s potential, private firms can now apply to test new solutions and use cases, work will continue on the MVP’s technology and functions and the refinement of the legal and governance frameworks, and new central and commercial banks are encouraged to join the platform. The project has now welcomed the Saudi Central Bank as a full participant in the project, and more than two dozen central banks and financial institutions are currently mBridge observers.

Ghana Executes X-Border Payments Using Digital Credentials

The Bank of Ghana (BOG) has revealed (PDF) a notable crossborder achievement as part of its ongoing Project DESFT (Digital Economy Semi-Fungible Token). In collaboration with the Monetary Authority of Singapore and financial sector participants in both Ghana and Singapore, BOG has successfully completed a proof-of-concept (POC) demonstrating the use of digital credentials in cross-border payments and international trade.

Launched in June 2023, the project’s first phase consisted of the development of a trusted credential system designed to enhance the participation of Ghanaian MSMEs in international trade. Phase Two culminated in a successful cross-border trade between Ghana and Singapore in April 2024 during BOG’s 3i Africa Summit.

The solution in Project DESFT consists of five components: 1) a digital trusted credential framework; 2) Ghana’s retail CBDC, the e-Cedi; 3) a Singapore dollar-pegged stablecoin based on the Purpose Bound Money protocol; 4) a trade marketplace with integrated cross-border connectivity; and 5) an escrow arrangement that facilitates payments upon verification of digital credentials and trade fulfilment.

According to BOG, the live transactions revealed the feasibility of using the e-Cedi platform in cross-border transactions and its potential in the future for connecting (con't in next column)

with other cross-border payment and credential platforms.

“After nearly a year and two phases of development, we have crafted a reliable information exchange solution founded on UTC standards and Semi-fungible Token technology. Furthermore, we have rigorously tested a cross-border payment solution built upon the principles of Purpose Bound Money (PBM) and conducted real trade experiments which fully align with our predetermined objectives,” remarked BOG First Deputy Governor Dr. Maxwell Opoku-Afari.

The project’s third phase will focus on automated digital credential processes, programmable payments across multiple currencies, and supply chain finance.

Iran Unveils Digital Rial Pilot on Resort Island

The Central Bank of Iran (CBI) has revealed (link in Persian) details of a new digital rial pilot test, set to roll out in July. As part of the test, residents and tourists on Kish Island, a resort island south of Iran, can use digital wallets to make QR-code based purchases and money transfers with the prototype CBDC.

CBI initiated its digital rial project in 2021, following approval from the central bank’s Money and Credit Council. Following preliminary studies and a pre-test phase in early 2022, a limited trial began in June 2023. In the latest phase, the testing on Kish Island will be undertaken with support from two domestic commercial banks, Mellat Bank and Tejarat, targeting widespread adoption.

According to CBI, the digital rial project aims to bolster Iran's digital economy, enhance payment infrastructure resilience, and support the development of micropayment tools.

BOG First Deputy Governor Dr. Maxwell Opoku-Afari. Source: BOG

Bank of Israel Opens Digital Shekel Challenge

The Bank of Israel’s exploratory work on a digital shekel continues with the recently announced Digital Shekel Challenge. Inspired by the BIS Innovation Hub’s Project Rosalind, the Challenge invites stakeholders to develop technologically innovative use cases for a digital shekel using an API layer provided by the central bank.

CROSS-BORDER

Open to anyone interested in the development of a digital shekel, the Challenge will consist of two stages. Phase One, the application stage, closes on 11 July. Selected applicants will advance to the second phase, in which “the contestant will need to present a full implementation of the proposed use case, including the front-end interface that is used by the endusers, while operating the Digital Shekel system core using the APIs layer.”

The Challenge’s timeline will proceed quickly, with selected applicants to be announced on 22 July. Product presentations before the Challenge’s judging panel will occur in late September.

Qatar Completes CBDC Infrastructure, Testing Set for October

According to the latest BIS survey results, 94% of central banks are currently exploring a CBDC. Though not among

Designed to allow payment service providers in SEPA to process instant transfers originating or terminating in countries outside of the euro area, OCT Inst dramatically improves the speed, availability, cost, accessibility, and transparency of international transfers requiring foreign exchange.

The announcement follows a three-month public consultation that opened in November 2023 and includes a Feedback Statement (PDF) on the central bank’s approach to innovation engagement in the financial sector. The Innovation Sandbox will take a thematic approach, with specific themes and a call for participants to be announced in the coming months. The program will be open to any innovators in the financial system. (con't on next page)

Qatar Central Bank. Source: Dreamstime

INFRASTRUCTURE

Sandbox Programme are important steps forward, and we were very pleased with the strong support for our proposals.”

Additionally, CBI released (PDF) its Innovation Hub 2023 Update, revealing plans to evolve and enhance the CBI Innovation Hub to deepen sector engagement in Ireland. The update notes that the Hub worked with 66 firms in 2023, a 20% increase from 2022, indicating high demand for engagement and an increase in innovation efforts across the country’s financial services sector.

BOT to Test Programmable Payments

in Enhanced Sandbox

Consistent with its stated policy of “responsible innovation,” the Bank of Thailand (BOT) has initiated (link in Thai) a new project to test programmable payments innovations. The project will occur within the bank’s Enhanced Regulatory Sandbox framework, which expands the scope of BOT’s current sandbox to include financial innovations not yet authorised by the Thai central bank.

In a September 2023 speech, BOT Governor Sethaput Suthiwartnarueput offered (PDF) a preview of the Enhanced Regulatory Sandbox and the bank’s evolving approach to innovation: “What we are planning to do is to have an additional channel, the ‘New Sandbox’ which is more flexible, to support the testing of unregulated financial activities that apply new technologies for use cases that benefit customers (e.g. tokenization that helps improve access to credit for SMEs, programmability that helps enhance efficiency of payment services).”

BOT is now accepting applications to join the programmable payments project, and interested parties and financial service providers may apply to join through 13 September.

For more on Project Meridian, see (PDF) our May 2023 issue featuring the BISIH London Centre.

Using the synchronisation operator (SO) developed in Meridian as the initiative’s launch point, and with the aim of overcoming frictions in foreign exchange transactions, Meridian FX will test the SO’s usability for various digital assets and new payments technologies, including DLT.

In the experiments, the synchronisation operator will connect to two RTGS systems in different jurisdictions and to an RTGS system with a DLT-based settlement platform, to test how the SO enables interoperability between existing and new ledger technologies.

Testing in Meridian FX is set to begin at the end of 2024 and will involve connecting the SO to the three solutions that are part of the Eurosystem’s exploratory work on new technology for wholesale settlement in central bank money. More recently, the European Central Bank (ECB) announced the selection of the second group of participants to test the three solutions, consisting of 48 private firms in the financial sector and three central banks. From July to November 2024, the second wave of participants will broaden the scope of the exploratory work, joining the first group that has been testing since mid-May. See this month’s feature article from the ECB for more.

New RTGS Systems in Guatemala, Sri Lanka

Banco de Guatemala has rolled out a new RTGS system as part of its payment system modernisation efforts. Described as a “particularly complex” implementation, the updated RTGS system replaces the Liquidación Bruta en Tiempo Real (LBTR) system launched in 2006.

Implemented by solution provider Montran, the new system supports ISO 20022 messaging, and connected participants in the Guatemalan financial system are “now exploring new possibilities” with the system’s Participant REST API service, which enables straight-through processing with banks’ core banking systems. (con't on next page)

Central Bank of Ireland. Source: Dreamstime

A similar development occurred recently in Sri Lanka, as Montran and the Central Bank of Sri Lanka (CBSL) have partnered to launch an updated RTGS system, “a crucial step in CBSL’s digital transformation journey towards innovation.” As with the updated system in Guatemala, Sri Lanka’s new RTGS system has migrated to the ISO 20022 standard, and will feature 24/7 processing capability and enhanced visibility of the entire payments lifecycle, among other functionalities. Sri Lanka first launched its RTGS system in 2003.

Lesotho Partners with EU and World Bank to Enhance Financial Infrastructure

Lesotho’s financial infrastructure is “well poised for development” with a new partnership between the Central Bank of Lesotho (CBL), the European Union (EU), the World Bank, and Lesotho’s Ministry of Finance and Development Planning. The partnership aims to foster inclusive growth and expand access to financial services, bolstered by a LSL 6 million (€306,113) investment from the EU.

The World Bank will provide technical assistance in three key

PMA Rolls Out Pioneering Unified Database Project

The Palestine Monetary Authority (PMA) recently launched a new digital payments project to enhance the integration of financial technology in Palestine’s banking sector, facilitating remote financial transactions for individuals and businesses. This initiative aligns with the PMA’s digital transformation strategy and addresses challenges “imposed by current circumstances.”

The project, developed in partnership with Greek data firm Tiresias and US-based identity firm Uniken, aims to create an advanced technological infrastructure that will include a “unified and reliable” database. This will enable customers to conduct all financial transactions, including remote account opening, using modern technology.

PMA Governor Dr. Feras Milhem highlighted the unified database as a “new phase of digital transformation” and a significant step towards enhancing financial inclusion, particularly for vulnerable groups and individuals with special needs. The Governor also noted the project's success in allowing Gaza Strip bank customers to access their accounts despite challenging conditions.

INSTANT PAYMENTS

To operate on a 24/7/365 basis, the “platform will make it possible to offer a wide range of services, aimed at simplifying users' daily transactions and stimulating financial innovation.”

Users will be able to make transfers to accounts at any institution — banks, electronic money issuers, microfinance institutions, etc. — that is connected to the interoperable system, and the funds will be available instantly. An interoperable QR code will also enable instant consumer-tomerchant payments.

The central bank has not publicly revealed how long the pilot is expected to run.

Central Bank of Lesotho. Source:

RETAIL PAYMENTS

America to adopt the globally renowned Unified Payment Interface (UPI) technology.”

The alliance will enable BCRP to establish a reliable, efficient real-time payment system in Peru, facilitating instant payments and reducing cash dependence, while also promoting financial inclusion by reaching the country’s unbanked populations.

Commenting on the collaboration, BCRP Governor Julio Velarde said, “We believe this marks a significant step in strengthening and modernizing our payments system, aiming to expand access to digital payments in Peru. The support of the Reserve Bank of India has been a cornerstone of this agreement. The BCRP aims to promote financial inclusion, security, and efficiency, and to introduce new use

basis.

The second service was rolled out on 24 June, enabling transfers using the recipient’s mobile phone number or legal identification number instead of an IBAN. Known as SPIN, the proxy service simplifies the process of making credit or immediate transfers.

The two services are accessible to providers participating in the Interbank Clearing System (SICOI), which processes the majority of daily payment transactions in Portugal. The goal, says BdP, is widespread adoption and “a more convenient, safer and more innovative payments market.”

Meanwhile, a recent study from BdP reveals that retail payment costs in 2022 amounted to €2.2 billion, representing 0.95% of the country’s nominal GDP that year. The costs increased by 20% since 2017, with 90% borne by traders and banks. Direct debits and transfers remained the cheapest retail payment options, while cheques and credit cards were the most expensive. A dashboard was also released as a supplement to the study, showing the payment habits of Portuguese consumers since 2013, “depending on variables such as age, education, region and income.”

To learn more about payments and innovation at Portugal’s central bank, stream the late-May “SPIN - Sobre Pagamentos e INovação” conference here

Banco Central de Reserva del Perú. Source: BCRP

IN BRIEF

A

AFRICA

The IFAD Remittance Innovation Toolkit from Cenfri and the International Fund for Agricultural Development (IFAD) provides practical guidance for regulators and remittance service providers on how to assess national regulatory environments, analyse contextual realities, and plan, implement, and measure innovative interventions to address barriers to remittances.

Egypt’s InstaPay, the first PSP app licensed by the Central Bank of Egypt to operate over the Instant Payment Network, has introduced QR code and payment link features for instant transfers, allowing users to share QR codes or unique links to facilitate easy and secure money transfers.

In late May, Eswatini’s Ministry of Finance released the Eswatini National Financial Inclusion Strategy 2023–2028. The framework identifies innovation, financial capability of consumers and MSMEs, and stakeholder partnership and collaboration “as critical enablers that serve as the foundation of the financial inclusion pillars.”

Ethiopia’s Council of Ministers has approved draft proclamations from the National Bank of Ethiopia proposing a legal framework to potentially introduce a digital birr and establishing a regulatory sandbox framework, among other policy changes. The proposed reforms are now being submitted to the House of Peoples Representatives for review, comment, and final ratification.

Women’s Roles in Cross-Border Remittances: A Study on South Africa’s Corridors to Malawi, Mozambique and Zimbabwe, a new report from FinMark Trust, focuses (PDF) on key corridors for cross-border remittances “to deepen our understanding of women’s roles in this financial activity.”

In a recent episode of the National Bank of Rwanda podcast, Director of Financial Sector Development and Inclusion Kimenyi Valens details the findings of the central bank’s CBDC feasibility study that was published in early May.

AMERICAS

The Application Programming Interface (API) of Reported Checks has been unveiled as part of Banco Central de la República Argentina’s Open Finance Strategy. The new tool can be used to discover if a cheque has been reported as lost, stolen, or altered, “thus preventing possible fraud or scams.”

The Bank for International Settlements (BIS) and the Bank of Canada have opened the BIS Toronto Innovation Centre, the first BIS Innovation Hub Centre in the Americas. This seventh BIS centre will focus on advancing technologies to enhance financial system efficiency and inclusivity in Canada, Latin America, and the Caribbean. View the opening ceremony here

On 27 May, Governor John Rolle announced the launch of the Live Digital Bahamas Campaign. Backed by the Central Bank of The Bahamas, the public education initiative promotes the adoption of digital financial services, with the aim to enhance commerce and boost hurricane resilience.

The Bermuda Monetary Authority and the Financial Services Regulatory Authority of the Abu Dhabi Global Market have signed an MoU for collaboration on digital assets, enabling regulatory cooperation, investigative support, and supervision of digital asset entities across the two jurisdictions.

Payments Canada’s recent response to the Bank of Canada’s public consultation on the draft supervisory guidelines for the Retail Payment Activities Act (RPAA) indicates approval for the guidelines proposed, but seeks clarification regarding the definition of a third-party service provider and recommends closer collaboration between the two entities.

A comprehensive blog post from the Central Bank of Curaçao and Sint Maarten delves into the potential impact of a digital Caribbean guilder on monetary policy transmission.

Banco Central del Paraguay has rolled out (link in Spanish) the Digital Economy Pilot Program to promote digital payments in MSMEs. The initiative aims to reduce transaction costs, enhance financial system efficiency, and support the digital transformation of Paraguay’s economy through innovation and training.

In a step forward for open banking in the US, the Consumer Financial Protection Bureau (CFPB) has finalised a rule establishing the qualifications for recognised industry standard-setting bodies under the upcoming Personal Financial Data Rights Rule. The new rule identifies essential attributes for recognition, provides a step-by-step application guide, and aims to prevent dominant firms from manipulating standards in a bid to foster fair competition.

The U.S. Faster Payments Council has published its latest survey report on Faster Payments and Financial Inclusion. Conducted in Q3 2023, the survey assessed financial institutions' readiness for faster payment solutions and their impact on financial inclusion. Key findings highlight that “only” 56% of institutions currently offer faster payments and 35% plan to.

On 21 June, the Federal Reserve Board announced it will extend the comment period on its proposal to expand the operating days of the Federal Reserve Banks' two large-value payments services, Fedwire® Funds Service and the National Settlement Service (NSS), to include weekends and holidays. The new deadline is 6 September.

ASIA

The National Bank of Cambodia has entered into three MoUs on cross-border QR code payments with South Korea’s Kookmin Bank, JB Financial Group, and Woori Bank. As per the central bank, these agreements “aim to strengthen the connectivity of payment systems emphasizing safety and efficiency between the two countries.”

Programmable Payment and Investment: Cash Management for Low Balance Retail Investors with Hypothetical e-HKD, a collaborative report from PwC, financial services platform Arta TechFin, and tech firm Emali, investigates the potential of the e-HKD to streamline financial transactions by using smart contract programmability.

In a recent meeting, the Hong Kong Monetary Authority and Bank Negara Malaysia focused on bilateral financial cooperation in strategic areas, including digital finance and fintech, green and sustainable finance, payment systems, use of local currencies for cross-border trade, and Islamic finance.

Standard Chartered has announced the successful completion of Euro-denominated cross-border transactions between Hong Kong and Singapore on the Partior network. It is the first Euro settlement bank to go live on Partior, the global unified ledger market infrastructure.

As reported in local media, Nepali consumers will be able to make Unified Payment Interface (UPI) payments in India starting in July. The first phase of the initiative was rolled out (PDF) in March and allows Indian consumers to make UPI payments in Nepal with UPI-enabled apps.

A recent circular from the State Bank of Pakistan directs (PDF) banks to develop and implement digital supply chain finance (SCF) solutions within six months. The initiative aims to enhance SMEs’ access to finance and digitise retail payments. Banks must establish effective SCF functions, either independently or through fintech partnerships, to “improve operational efficiency, reduce costs, and strengthen risk management practices.”

Bangko Sentral ng Pilipinas (BSP), in partnership with the International Finance Corporation and with support from the Government of Japan, has announced the Open Finance PH Hackathon. From 15 July to 7 August, industry experts are invited to submit innovative open finance use cases, with the winning team earning a trip to the 2024 Singapore FinTech Festival in November.

An MoU signed by the governors of the Bank of Thailand and the People's Bank of China is poised to strengthen banking and financial cooperation between the two countries, including agreements to promote local currency usage and enhance cross-border payments and settlement.

AUSTRALIA & OCEANIA

The Reserve Bank of Australia’s Payments System Board recently discussed several key issues: the assessment of RBA’s RTGS system, the upcoming review of retail payments regulation, the security of online card transactions, and industry measures to combat scams.

EUROPE

In a first for the Central Bank of the Republic of Azerbaijan, three payment service provider licences have been issued to electronic money institutions and payment institutions operating in the country. The “perpetual” licences were announced on 25 May.

The Cyprus Securities and Exchange Commission (CySEC) recently unveiled its regulatory sandbox, an initiative that “marks a significant milestone in the advancement of financial, regulatory, and supervisory technologies (FinTech, RegTech, and SupTech) in Cyprus.”

On 6 June, the European Banking (con't in next column)

Authority (EBA) released three regulatory products on governance, conflicts of interest, and remuneration under the Markets in Crypto-Assets Regulation (MiCAR). More recently, on 19 June, the EBA published the package of technical standards and guidelines under MiCAR on reporting, liquidity stress testing, and supervisory colleges, completing the delivery of EBA technical standards for MiCAR.

In 2023, TARGET2-Securities (T2S) settled over 177 million transactions worth €200 trillion, averaging 700,000 transactions daily. Find out more in the T2S Annual Report 2023 from the European Central Bank (ECB), including an update on the efficiency gains from the new T2 system launched in March 2023.

A blog post from the ECB’s Maarten G.A. Daman focuses on key privacy aspects of the proposed digital euro, including plans to implement strong data protection into the digital euro design.

The European Commission has launched a targeted consultation on artificial intelligence in the financial sector to “inform the Commission services on the concrete application and impact of AI in financial services, considering the developments in the different financial services use cases.”

The European Commission’s rules for establishing a European Digital Identity entered into force on 21 May. The rules bring Europe a step closer to the launch of the personal European Digital Identity Wallet in 2026.

Also on 21 May, the European Council gave the green light to the AI Act, a “ground-breaking law aiming to harmonise rules on artificial intelligence” across the EU’s single market.

The European Payments Council’s multi-stakeholder group on mobile-initiated SEPA (instant) credit transfers is seeking industry feedback on the draft third release of the Mobile Initiated SEPA (Instant) Credit Transfer Interoperability Guidance. Comments will be accepted until 26 July.

The European Supervisory Authorities (EBA, EIOPA, and ESMA) have signed a multilateral Memorandum of Understanding with the European Union Agency for Cybersecurity (ENISA). The agreement strengthens cooperation and information exchange, focusing on policy implementation, incident reporting, and oversight of critical ICT third-party providers.

Using existing Life Cycle Analyses (LCA) from previously published studies, a new whitepaper from Lipis Advisors “examines the ESG impacts of the most commonly used payment instruments within Europe.” The report was prepared with help from the European Automated Clearing House Association (EACHA).

On 5 June, Banca d’Italia’s Milano Hub innovation centre launched its third Call for Proposals with a focus on instant payments.

The Central Bank of Kosovo (CBK) has formally joined the European Automated Clearing House Association, a move that will “help the CBK and the payment service providers to adopt EU standards and prepare the market for integration with EU payment schemes and systems.”

Mastercard recently opened the doors of its European Cyber Resilience Center (ECRC) in Belgium. The ECRC seeks to improve defences against cybersecurity threats, accelerate response times, and serve as a hub for cybersecurity innovation.

An opinion poll conducted by the Bank of Russia reveals the majority of Russians prefer cashless payments. The most popular payment methods among those polled were bank card payments (75%), mobile and online bank payments (48%), and payments via the Faster Payment System (28%).

The National Bank of Serbia has issued (link in Serbian) draft amendments to the country’s Law on Payment Services, aiming to further encourage innovation, competition, and user protection. The draft incorporates the EU's PSD2 and introduces new services such as payment initiation and provision of account information.

The Riksbank has moved a step closer to T2 migration with the 18 June announcement that it will proceed with the process of using T2 for its RIX-RTGS payment settlement service. Contract negotiations with the ECB will commence this year and the transition is anticipated to take five years. A transition to the T2S platform is being considered for 2030. See the Riksbank’s in-depth analysis of the T2S platform here

In a speech on 20 June, Member of the Governing Board of the Swiss National Bank (SNB) Antoine Martin revealed that SNB became in early June the first central bank to use DLT to “carry out a monetary policy operation in a live production environment.” The operation was carried out as part of Project Helvetia III, which the national bank says will be extended for an additional two years and with a broadened scope.

The Central Bank of the Republic of Turkey’s new FAST Escrow Overlay Service was rolled out recently, providing a secure platform for transactions requiring confirmation or registration. The service holds funds until the necessary procedures are completed, ensuring secure transfers with a transaction limit of TRY 2 million (€57,069).

MIDDLE EAST

An IMF blog post from 18 June summarises the key points in the Fund’s departmental paper, Central Bank Digital Currencies in the Middle East and Central Asia.

Bank Al-Maghrib’s One Stop Shop Fintech is a newly launched (link in French) space dedicated to supporting Morocco’s fintechs.

The Central Bank of Oman has joined the regional AFAQ platform, operated by the Gulf Payments Company and owned by the Gulf Cooperation Council (GCC) central banks. AFAQ executes instant and low-cost financial transactions across borders in GCC local currencies.

GLOBAL

Issued in late May, the BIS’ Committee on Payments and Market Infrastructures 2024–25 work program is guided by the themes of risk management of financial market infrastructures, cross-border payments enhancement, and digital innovation in payments, clearing, and settlement.

Ripple’s recently released e-book, Trends in Regional Payments: Inside the Evolving Global Payments Landscape, explores the top payment trends throughout North America, Latin America, Europe, Asia, and Africa.

Financial System 2030: Digitalization, Nation States and (De-) Regulation as Drivers of Change, published by Springer in late May, addresses how technological developments and digitalisation will impact the future of the financial system.

Swift recently announced plans to extend ISO 20022 across the payment chain, enhancing speed and transparency for “instant and frictionless transactions.” Developed in collaboration with 25 cash management banks and 20 corporates, Swift’s plan aims to help financial institutions streamline cross-border payments for corporate customers by introducing a universal standard “that can maximise the benefit of ISO 20022’s richer, more structured data.”

Also from Swift is a series of AI-based pilots conducted with member banks to combat cross-border payments fraud. The first pilot enhances Swift's Payment Controls service using AI to detect fraud more accurately, while another experiment with 10 banks is testing how advanced AI technology can be used to analyse anonymously shared data from different sources. The initiative aims to “save billions in fraudrelated costs.”

In response to the joint Bank of England and Financial Conduct Authority digital securities sandbox consultation paper issued this spring, Commissioner Hester Peirce of the U.S. Securities and Exchange Commission proposes a crossborder sandbox that would allow firms to conduct the same sandbox activities under the same regulatory requirements in both countries.

Visa’s Money Travels: 2024 Digital Remittances Adoption report reveals humanitarian assistance as a key driver of remittances. Despite a year-over-year decline in global remittances, the survey of nearly 45,000 participants across 20 countries highlights a growing preference for digital applications, with over two-thirds favouring digital methods for their speed, ease, and security.

A life cycle analysis study conducted by Worldline reveals the “huge potential” of digital payments to decarbonise payment systems. Published in late May, the study confirms that digital payments produce significantly lower levels of CO2-equivalent emissions than cash.

Digital Euro Preparations Gain Momentum

By Piet Mallekoote, Former Member of the Digital Euro Market Advisory Group, European Central Bank

Global focus on central bank digital currency increases

Since 2020, the focus on central bank digital currency (CBDC) has increased significantly. Retail CBDC is on the agenda of more than 100 central banks, while wholesale CBDC is being explored by over 20 central banks (Kiff). More than half of the central banks are doing experiments or conducting a CBDC pilot (Kosse and Mattei). Three retail CBDC systems are now live: The Bahamas, Jamaica and Nigeria. Large-scale pilots are being conducted in China, while the United States is lagging behind, partly due to political headwinds and the recently passed CBDC Anti-Surveillance State Act.

Digital euro on the move

Substantial progress has been made in the euro area in recent years with preparations for a digital euro. A decision to introduce it depends on political decision-making. Former European Central Bank (ECB) Member of the Executive Board Fabio Panetta and his successor, Piero Cipollone, have communicated transparently on the project's progress in recent years (ECB digital euro pages). Following this, a number of Eurosystem central bank governors have recently called attention to the importance of the digital euro, with the arguments to be discussed below at their core (Hernández de Cos, Knot, Nagel, Panetta, and Beau).

This article highlights the background of the digital euro project and provides an overview of the state of play and challenges.

Declining

use of cash a key driver of the digital euro ... but increasing geopolitical fragmentation is too

The purpose of the digital euro is threefold:

• First of all, in the ongoing digitalisation of the economy, the ECB wants to ensure the role of and sufficient availability of public money. The use of cash has been declining for years (Figure 1), and the ECB wants to continue to provide a public anchor of trust and stability with the digital euro. This anchor guarantees the one-to-one exchange of private money.

Figure 1 Use of cash varies and declines Share of

Digital Euro Preparations Gain Momentum

• Second, increasing geopolitical fragmentation in the world is a source of concern for the ECB. Therefore, strengthening the single market is a key priority. In this context, Enrico Letta recently advocated for the importance of a “rapid” introduction of the digital euro. European autonomy and sovereignty that provide for European governance for payments is essential in this respect. Currently, 64% of the number of card transactions in the euro area are provided by international card schemes, and 13 of the 20 euro area countries do not have a national card scheme. This weakens European autonomy and competition and can make the system vulnerable to external disruptions. This also applies to the impact of (potentially) global developments on Europe from big techs, stablecoins and foreign digital currencies. The ECB's ambition is to make the digital euro future-proof, whereby the euro can continue to play a significant role in the progress of the digital evolution and ensure resilience.

• Third, the digital euro reduces the fragmentation of national payment solutions. While national payments markets are efficient in themselves, this efficiency does not exist on a pan-European scale without using non-European providers. Attempts to achieve a European card (and an online) scheme have never succeeded (the ECB spoke of "the black hole" in that context), unlike, the European-wide SEPA Credit Transfer (SCT), its instant variant (SCT Inst) and Direct Debit (SDD). With the digital euro, the ECB wants to aim for widely usable payment instruments that can be used anywhere in the euro area at the Point of Interaction (POI), with its own European governance. The digital euro solves this fragmentation and provides a platform for innovation. National innovations can be used across Europe by citizens through the digital euro platform.

Private initiatives alongside public initiatives

Meanwhile, private initiatives also exist to reduce fragmentation. For example, the European Payments Initiative (EPI), supported by German, French and Benelux banks, is developing a wallet called wero to be widely used across Europe. To this end, the online banking solution popular in the Netherlands, iDEAL, has been brought in. The core of the wallet is the use of the above-mentioned Instant Payments scheme in all use cases, starting this year with (cross-border) P2P transactions between German and French citizens, followed later by users in Belgium, Luxembourg and the Netherlands. This will be followed by applications for POI (point-ofsale and e-commerce).

On the southern side of Europe, we see cooperation between Spain, Portugal and Italy, which are making their systems for crossborder P2P interoperable using SCT Inst. For now, in this situation, unless these blocks start working together, fragmentation will remain. In that case, the digital euro platform offers a solution: local payment methods can get European coverage via this platform.

Digital euro project progresses steadily

The ECB launched the investigation phase of a digital euro in 2021. This was completed in October 2023, after which the Governing Council decided on a follow-up (preparation) phase to last until November 2025. The core of this phase is, among others, an exploration of the technical aspects and the realisation of the digital euro Rulebook. After this phase, a decision will be taken on whether or not to introduce the digital euro (Figure 2).

In parallel, in June 2023, the European Commission (EC) published a legal proposal for the digital euro — with the legal tender of the digital euro at its core — which, after approval by the European Parliament and the European Council, mandates the ECB to introduce the digital euro. With the election of a new European Parliament this month, it is unknown when the Parliament will consider the proposal.

Source: ECB

Investigation phase

Oct. 2021 – Oct. 2023

Concept definition, technical exploration and design proposal

P r e p a r a t i o n p h a s e Nov. 2023 – Oct. 2025

Main expected next steps:

• Finalise the scheme rulebook

• Select service providers

• Learn through experimentation

• Deeper dive into technical aspects, including further research into offline functions and developing a testing and rollout plan for the future

Next phase

From Nov. 2025

Potential development and rollout 2

Figure 2 Three phases of the digital euro project

Digital Euro Preparations Gain Momentum

What does the digital euro look like?

• The digital euro is a digital form of cash in addition to physical cash. It serves only as a means of payment, not as a store of value. The hoarding of digital euros is discouraged by not remunerating balances and tying them to a yet to be determined holding ceiling.

• The offline functionality is innovative, ensuring a high degree of privacy: payments with it are made without an intermediary and without an internet connection. This also promotes resilience in case of online networ

• Online payments, using state-of-the-art privacy-enhancing techniques, are instantly settled on the digital euro platform. Programmable payments, where a digital euro would act as a voucher only to be spent on certain products or within a specified period, are excluded. However, payment service providers can offer added value services, such as conditional payments, to their customers.

• The ECB has opted for a two-tier model where the ECB issues the digital euros (they are on the ECB balance sheet) and banks and other authorised service providers (PSPs) distribute the digital euros to their customers. Outsourcing to PSPs also means that they are responsible for onboarding with associated KYC checks and sending payment orders to the platform, customer contact and fraud prevention, etc.

• PSPs can use the digital euro app developed by the ECB or their own app for this purpose to service their customers. The ECB will also provide a payment card variant for those who prefer this to a mobile app. To the extent necessary, the digital euro app will also be made available to citizens without a bank account. For the benefit of this group, institutions will be designated at the national level to distribute this app and card and explain it to those who need it. In doing so, the digital euro contributes to digital inclusion.

• The digital euro is free of charge for citizens and has a mandatory acceptance for merchants as a consequence of the proposed legal tender status. This allows any citizen to pay with the digital euro anywhere: at the physical point-of-sale, on the internet and between citizens (P2P), both via a mobile app or with a payment card to be issued by the ECB (Figure 3). And it solves the problem of fragmentation (Figure 4).

The offline functionality is innovative, ensuring a high degree of privacy: payments with the digital euro are made without an intermediary and without an internet connection.

Figure 3 Diverse use cases, devices and technology

Digital Euro Preparations Gain Momentum

Holding limit prevents disintermediation

A holding limit should prevent excessive disintermediation and risks to financial stability. By establishing a holding limit, the ECB adopts the BIS's principles on neutrality for monetary policy and financial stability. Former ECB Member of the Executive Board Panetta has previously indicated that he envisages a maximum per capita balance of around €3000. The ECB is currently conducting research on the level of such a limit, which will be set just before the launch. The EC's legal proposal gives the ECB the mandate to do so.

Payments can exceed the limit

The limit decouples flows and holdings: payments in digital euros larger than the balance can be replenished for the excess by converting balances in commercial bank money instantly into digital euros (reverse waterfall) and vice versa (waterfall). Merchants cannot hold digital euro balances; these are converted — upon receipt — directly into commercial bank money. As a result, and due to the situation that payments made by consumers flow directly back into merchants' commercial bank accounts, fears of a high degree of disintermediation therefore seem unfounded, provided the limit is limited (Bindseil et al.).

Holding limits not uncontroversial

The European Parliament's Committee on Economic and Monetary Affairs (ECON) has asked a number of independent experts to comment on the ECB's proposals. This shows that holding limits are not uncontroversial. Cyril Monnet and Dirk Niepelt believe that the introduction of a limit does not make the digital euro more attractive. While they acknowledge the risks of disintermediation and a bank run, they expect that — after an adjustment period — disciplining behaviour in the banking sector will mitigate these risks.

Christian Hoffmann is also not in favour of limits and thinks they should, after an introductory period, disappear quickly. Seraina Grünewald argues that a system of limits leads to cash remaining the only monetary anchor for the public, and thus the ECB misses its intended target. She too shows support for increasing or removing the limit after an introductory period. Ignazio Angeloni, on the other hand, thinks a €3000 limit is on the high side given the potential disintermediation (10% of bank deposits in the euro area). Banks also opt for a low limit: the European umbrella organisation of cooperative banks (EACB), for example, mentions a limit of up to €500. ECON suggests limits be set by each bank itself, which does not contribute to transparency. If the digital euro is launched, it is conceivable that the holding limit is initially set below the intended steady state level and gradually increased to this level (Panetta). But, even thereafter, it should not be ruled out that the set limit might act as a “camel nose,” with the amount being raised later. In this context, research by Antti Heinonen shows that in crisis situations the demand for central bank money increases. In a situation of a continued decline in the use of cash, the ECB might be inclined to meet this additional demand by increasing the holding limit. Whether this is a likely scenario will have to be seen in practice.

Person-to-person payments

Point-of-sale payments

payments

Source: ECB

Privacy critical

Privacy is seen by the public as the most important aspect of a digital euro (ECB). However, the ECB is clear: complete anonymity, as is the case with banknotes, is not a viable option. Online payments with a digital euro will be subject to the same rules as current private payment methods with prevailing anti-money laundering and combating the financing of terrorism (AML/CFT) requirements. For offline payments, only the funding or defunding of the offline functionality will be visible to intermediaries; payments with it will be anonymous, equivalent to cash. The ECB has indicated that information on payments will not be shared (it simply has no insight into it via the encrypted data). While that is convincing, some form of independent oversight on this could remove remaining doubts among the public.

Figure 4 Digital euro solves fragmentation

Digital Euro Preparations Gain Momentum

Markus Brunnermeier and Jean-Pierre Landau also point to the need for adequate privacy governance. This has been taken up very recently. In a blog of 13 June the ECB indicates that an independent group of data protection officers will assess the implementation safeguards on top of the already foreseen assurance. In doing so, the ECB makes it clear that privacy must not only be done, but must be seen to be done.

Challenges

A number of challenges lie ahead. We discuss two of them.

• The first is that of the compensation model. The ECB has opted for a scheme with a four-corner model. For consumers, use will be free of charge, merchants will pay PSPs a "reasonably" determinable price for their digital euro service that is more competitive than low-cost payment methods. This will be subject to a maximum fee per transaction. Part of that fee will accrue to the distributing PSPs to compensate for the costs incurred. The Eurosystem pays its own costs (scheme management and settlement costs). However, there are doubts whether this revenue model is sufficient for banks to cover costs. After all, without a sound business model, there is no incentive for PSPs to support the (mandatory) issuance of the digital euro (Angeloni, Grünewald, Monnet, Niepelt). Banks also point this out. It should not be forgotten that merchants will also have to incur costs to accept payments in digital euros. Further research into this therefore seems desirable.

• The second challenge is that of adoption. This is not a given, especially in countries that are already highly digitised. We can learn from this that demand for new payment solutions is influenced by ease of use, better than others and lower costs. However, we do not see these elements — especially the “keep it simple” criterion — everywhere. ECON, for instance, has — unintentionally — proposed a number of complexities in the design. In addition, a survey commissioned by the ECB shows that European citizens feel they are already well served, and they express a preference for fewer rather than more payment methods unless it offers clear added value (Kantar). The proposed offline variant is considered highly innovative and attractive. At the same time, citizens surveyed doubt whether this variant will be used frequently, although it could contribute to digital inclusion (Kantar) and could provide a welcome payments alternative in the rare cases of online interruptions. However, Europe-wide adoption is needed to meet the ECB's policy goals. In practice, user perceptions can be explored with experiments and pilots. Based on this, the design can then be adjusted if necessary. Adoption could benefit from the ECB doing so.

Conclusion

With the digital euro, the ECB aims to provide a widely accessible alternative to the declining use of cash, increase European payment system autonomy and sovereignty, and overcome payment system fragmentation.

The digital euro should provide a basis for a forward-looking strategy that focuses on innovation and new technology without relying on dominant non-European technology platforms. While these macro intentions are widely supported, the crux lies in the compensation model and sufficient adoption of the digital euro by the public. Steps still need to be taken here. In all this, publicprivate partnerships remain essential.

About the Author

Piet Mallekoote worked at the De Nederlandsche Bank for almost 25 years and, as head of payments, was a member of the Payment Systems and Settlement Committee of the Eurosystem. He then served as CEO of Currence (iDEAL) and the Dutch Payments Association from 2006. He retired in 2021. From November 2021–November 2023, he was an independent member of the digital euro Market Advisory Group of the ECB. This group ended with the conclusion of the investigation phase. He is currently senior advisor on payments, a member of the Dutch Institute for Financial Disputes and a non-executive Board Member in the payments industry. Piet has a degree in economics from the University of Amsterdam.

The digital euro should provide a basis for a forward-looking strategy that focuses on innovation and new technology without relying on dominant non-European technology platforms.

Editor’s Note

Shortly before press time, the European Central Bank published its first progress report on the digital euro preparation phase, outlining progress made on key digital euro design aspects and the envisaged next steps for the project. The issues addressed echo the key themes of Mallekoote’s article, including a “cash-like” level of privacy for the digital euro, offline functionality for digital euro payments, and a calibration methodology to define holding limits.

Financial Industry Adoption of Distributed Ledger Technologies — Implications for Central Bank Money Settlement

By Holger Neuhaus, Head of Division, Market Innovation and Integration, and Mirjam Plooij, Team Lead, Market Infrastructure, European Central Bank

1. Introduction

The Eurosystem — consisting of the European Central Bank (ECB) and national central banks in the euro area — is analysing the potential impact of emerging technologies, including distributed ledger technology (DLT), on the settlement of wholesale financial transactions. This work was initiated in response to increasing interest within the financial industry in the possible applications of DLT in areas such as securities-related transactions settlement on a delivery versus payment (DvP) basis and cross-currency payments settlement on a payment versus payment (PvP) basis.

Should there be a significant adoption of DLT by the financial industry, central banks may need to take action to ensure that wholesale transactions can continue to be settled in central bank money. Possible Eurosystem responses include enabling market DLT platforms to interact smoothly with Eurosystem settlement infrastructures based on existing technology, or making central bank money available in a new form that can be recorded and transferred on a DLT platform. These responses are not mutually exclusive.

The Eurosystem has launched exploratory practical work in cooperation with market players. The aim of this work is to gain further insights into how the interaction between existing or new DLT-based infrastructures for settlement in central bank money and market DLT platforms could be facilitated.

2. Central Bank Money at the Heart of the Financial System

The importance of central bank money settlement

To preserve and strengthen financial stability, international standards prescribe that financial market infrastructures (FMIs) should conduct settlements in central bank money where practical and available.1 FMIs — that is, payment systems, central securities depositories, securities settlement systems, central counterparties and trade repositories — are the backbone of the financial system. They facilitate financial transactions between the customers of different financial institutions, and between financial institutions themselves.

Using central bank money is particularly relevant for the settlement of wholesale financial transactions, typically carried out between banks and other financial market participants, which stand out because of their high value.2 Moreover, the structure of the wholesale financial market can lead to a concentration of payment activities and associated exposures within individual banks. Settling wholesale financial transactions in central bank money, rather than in commercial bank money, reduces risks associated with such a concentration.

1 See Committee on Payment and Settlement Systems and Technical Committee of the International Organization of Securities Commissions, “Principles for financial market infrastructures”, Bank for International Settlements and OICV-IOSCO, April 2012.

2The average transaction value in T2, the Eurosystem’s large-value payment system, is €5.5 million. While half of the transactions in T2 are below €6,500, at the upper end of the distribution much higher transaction values can be found. For example, in 2022 almost 219 payments with a value of more than €1 billion were made per day, even though these accounted for only 0.05% of payment flows (in terms of number of transactions). See “TARGET Annual Report 2022”, ECB, Frankfurt am Main, June 2023.

Financial Industry Adoption of Distributed Ledger Technologies — Implications for Central Bank Money Settlement

“Wholesale central bank digital currency”?

‘Wholesale central bank digital currency (CBDC)’ is often presented as a new concept, but central bank money has in fact been available in digital form for wholesale transactions for decades. The Eurosystem enables this through its TARGET Services, which ensure the free flow of cash, securities and collateral across Europe. The debate is therefore not about whether to provide digital central bank money for wholesale transactions, but about possible technological changes in how this money is provided.

Other central banks around the world are also exploring the potential use of new technologies for wholesale central bank money settlement. A BIS survey3 of 86 central banks, carried out in late 2022, showed that the majority of these banks were involved in researching wholesale CBDC (to use the terminology of the survey), with many of these also involved in practical experimentation. Some central banks have taken the next step of testing real transactions with market participants, including the Swiss National Bank4 and the Monetary Authority of Singapore.5

3. Potential Use of DLT for Wholesale Financial Transactions

Financial industry exploration of DLT for wholesale transactions

A series of private and public initiatives has emerged globally, with the aim of exploring new business opportunities and improving the functioning of financial market processes through the use of DLT. The main potential benefits explored in these initiatives relate to the shared operation of the DLT platforms by their participants, together with the possibility of automating processes through smart contracts, which could — from a technical perspective — be deployed by any authorised user of a DLT platform. Activities for which participants currently rely on centralised operators could then be conducted by the participants themselves.

On a DLT platform, conditional transactions as well as information flows could be technically automated through smart contracts. Technical automation could potentially remove the need for a central validating entity that ensures that either both or neither of the legs of a DvP or PvP transaction is executed, and facilitate that both legs are executed as close to simultaneously as possible. Proponents argue that with such ‘atomic’ settlement there would be less counterparty risk, fewer delays linked to multiple layers of matching and validation, fewer intermediaries and, therefore, lower costs. Other conditions for the execution of transactions or the generation of information flows could be also enabled using smart contracts.

The need for reconciliation could be reduced through the use of a shared ledger, which is inherent in DLT. This could make reconciliation processes (aligning different systems and databases managed separately by each market participant and intermediary) easier, thereby fostering the traceability and auditability of transactions. Transparency could even extend to external parties such as auditors, corporate clients or even the general public (for example, to verify green investments).

These features of DLT may particularly benefit market segments that are currently facing clear inefficiencies and constraints. These include international payments and settlement and servicing of illiquid/non-listed instruments. In the longer term, DLT settlement could potentially become systemically relevant for securities in general, as part of an overall industry move towards DLTs, in which increasing numbers of assets are registered on a DLT platform.

Implications of market DLT uptake for central banks

Many market players state that, in the absence of a DLT-compatible central bank money settlement solution, they would consider using alternative settlement assets, such as commercial bank money or stablecoins. These would not provide the same level of safety as central bank money. A partial move from central bank money to other settlement assets could also increase liquidity fragmentation and have adverse implications for financial stability.

At the same time, some argue that the speed of DLT adoption, if not its success, might to some extent depend on the involvement of the central banking community. Those who require settlement in central bank money may delay DLT adoption until a suitable central bank money settlement solution is in place. In addition, central bank involvement could be perceived as support for DLT as an innovation in financial services.

Central banks should also consider the impact of DLT uptake on the structure and functioning of the market. The use of multiple DLT platforms, as well as the coexistence of DLT platforms with other infrastructures, may lead to market fragmentation and hamper the seamless processing of transactions. With a view to the overall efficiency of the market, it is therefore important to consider how such an outcome can be averted. As is the case for existing technologies, the ability to agree on industry standards will be important.

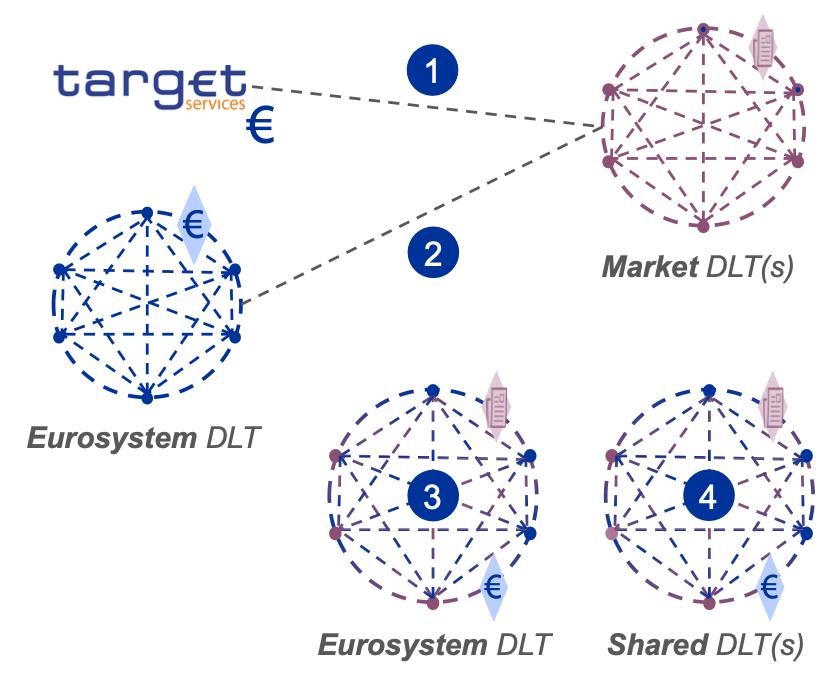

Possible Eurosystem responses

The Eurosystem has identified four conceptual solutions for central bank money settlement between banks for transactions where transfers are made using DLT. The figure below depicts these in a stylised manner, describing the example of a securities transaction, but similar solutions could also be used for foreign exchange transactions.

3 See Kosse, A. and Mattei, I., “Making headway – Results of the 2022 BIS survey on central bank digital currencies and crypto,” BIS Papers, No 136, Bank for International Settlements, July 2023.

4 See “SNB launches pilot project with central bank digital currency for financial institutions”, Press Release, Swiss National Bank, 2 November 2023.

5 See “Shaping the Financial Ecosystem of the Future”, Speech by Mr Ravi Menon, Managing Director, Monetary

16 November 2023.

Financial Industry Adoption of Distributed Ledger Technologies — Implications for Central Bank Money Settlement

Source: ECB.

1. CeBM settlement in TARGET Services based on current technology, interoperable with market DLTs for securities settlement (Trigger/Bridge)

2. CeBM settlement on Eurosystem DLT interoperable with market DLTs for securities settlement (Interoperability)

3. CeBM and securities settlement on Eurosystem DLT (Integration)

4. CeBM and securities settlement on DLTs shared between Eurosystem and other stakeholders (Distribution)

Notes: Blue lines, dots and icons represent central bank money (CeBM). Purple lines, dots and icons represent securities.

The first two options are cross-platform solutions:

1. A Trigger/Bridge solution would create a technical interface between a DLT platform on the market side and a nonDLT infrastructure (such as the existing TARGET Services) on the Eurosystem side. This technical interface should enable communication between those two infrastructures so that either both or neither of the legs (the securities leg on the market DLT platform and the cash leg in the Eurosystem infrastructure) are settled.

2. A full-DLT Interoperability solution would be a Eurosystem DLT platform for euro central bank money settlement, combined with a technical interface between that platform and market DLT platforms. The securities leg would settle on the market DLT platform, and the cash leg in a Eurosystem infrastructure. The key difference with Trigger/Bridge solutions is that in this case the Eurosystem infrastructure would be based on DLT.

The third and fourth solutions are same-platform solutions:

3. A full-DLT Integration solution would be a Eurosystem DLT platform where both euro central bank money and securities are settled. This is conceptually similar to the existing T2S platform, but based on DLT.

4. A full-DLT Distribution solution would be a platform (or several platforms) jointly operated by the Eurosystem and other parties for the settlement of both euro central bank money and securities.

Same-platform solutions are similar to the concept of a “unified ledger” proposed by the BIS in its 2023 Annual Economic Report.6 In a unified ledger, various types of assets (central bank money, commercial bank money and other assets) are represented in the form of programmable tokens to enable seamless automation and integration of complex transactions.

The governance of platforms with a wider scope in terms of assets, participants or use cases would presumably be more complex than for platforms with a narrower scope. Issuers and holders of different types of assets will each have their own requirements and may need to play their part in the governance arrangements for the platform. The design of such platforms and their governance would therefore be likely to take more time, and if requirements are too divergent, it may not be possible to come to an agreement that suits all parties.

For the Eurosystem, a key requirement is that the provision of any new solution must not come at the expense of the Eurosystem’s control over the central bank money it issues. For reference, in the current TARGET Services, the Eurosystem is responsible for the overall direction, management and control, including common cost and pricing methodology, security and policies, for example regarding which entities are allowed to hold central bank money for wholesale purposes.

6

Financial Industry Adoption of Distributed Ledger Technologies — Implications for Central Bank Money Settlement