Tax on Tips’

and ‘No Tax on Overtime’

‘One

Big Beautiful Bill Act’ enacted in 2025

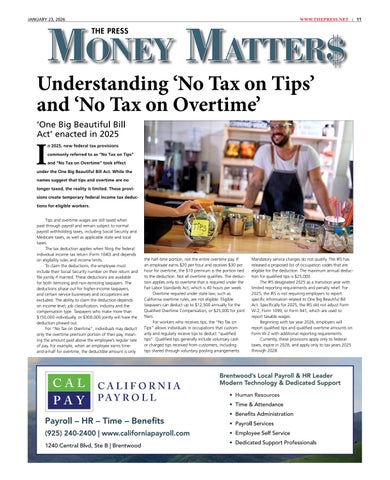

In 2025, new federal tax provisions commonly referred to as “No Tax on Tips” and “No Tax on Overtime” took effect under the One Big Beautiful Bill Act. While the names suggest that tips and overtime are no longer taxed, the reality is limited. These provisions create temporary federal income tax deductions for eligible workers.

Tips and overtime wages are still taxed when paid through payroll and remain subject to normal payroll withholding taxes, including Social Security and Medicare taxes, as well as applicable state and local taxes.

The tax deduction applies when filing the federal individual income tax return (Form 1040) and depends on eligibility rules and income limits.

To claim the deductions, the employee must include their Social Security number on their return and file jointly if married. These deductions are available for both itemizing and non-itemizing taxpayers. The deductions phase out for higher-income taxpayers, and certain service businesses and occupations are excluded. The ability to claim the deduction depends on income level, job classification, industry and the compensation type. Taxpayers who make more than $150,000 individually, or $300,000 jointly will have the deduction phased out.

For “No Tax on Overtime”, individuals may deduct only the overtime premium portion of their pay, meaning the amount paid above the employee’s regular rate of pay. For example, when an employee earns timeand-a-half for overtime, the deductible amount is only

the half-time portion, not the entire overtime pay. If an employee earns $20 per hour and receives $30 per hour for overtime, the $10 premium is the portion tied to the deduction. Not all overtime qualifies. The deduction applies only to overtime that is required under the Fair Labor Standards Act, which is 40 hours per week. Overtime required under state law, such as California overtime rules, are not eligible. Eligible taxpayers can deduct up to $12,500 annually for the Qualified Overtime Compensation, or $25,000 for joint filers.

For workers who receives tips, the “No Tax on Tips” allows individuals in occupations that customarily and regularly receive tips to deduct “qualified tips”. Qualified tips generally include voluntary cash or charged tips received from customers, including tips shared through voluntary pooling arrangements.

Mandatory service charges do not qualify. The IRS has released a proposed list of occupation codes that are eligible for the deduction. The maximum annual deduction for qualified tips is $25,000.

The IRS designated 2025 as a transition year with limited reporting requirements and penalty relief. For 2025, the IRS is not requiring employers to report specific information related to One Big Beautiful Bill Act. Specifically for 2025, the IRS did not adjust Form W-2, Form 1099, or Form 941, which are used to report taxable wages.

Beginning with tax year 2026, employers will report qualified tips and qualified overtime amounts on Form W-2 with additional reporting requirements. Currently, these provisions apply only to federal taxes, expire in 2028, and apply only to tax years 2025 through 2028.

CALIFORNIA ASSET PROTECTION: WHAT REALLY WORKS

by Martin C. Johnson, Attorney at Law, MBA, EA

Many Californians with growing incomes, rental property, or a small business start asking the same question: “How do I protect what I have built if I get sued?” The internet offers quick fixes, but most of the popular ideas are either incomplete or do not work the way people think they do in California. Start with the basics. A revocable living trust is an excellent planning tool. It can help families avoid probate, organize assets, and provide a plan if someone becomes incapacitated. But in California, a standard revocable living trust is not a shield against lawsuits for the person who created it. If you keep control of the trust and can revoke it, your creditors can generally reach those assets. So where does absolute protection come from? For most property owners and business owners, the best results come from reducing risk in layers.

through real agreements and proper bookkeeping.

Layer three is disciplined operation. Courts and creditors closely examine whether an LLC is real or merely a label. Separate bank accounts, clear contracts, consistent records, and the avoidance of commingling are not mere formalities. They are what make the structure hold up during testing.

Diversifying between stocks and bonds

Bonds can help provide balance through good times and bad

There is also a practical issue many owners miss: mortgages. Transferring a mortgaged rental into an LLC can trigger the loan’s due-on-sale clause. Sometimes lenders allow it. Sometimes they do not. A proper plan addresses this before any deed is recorded.

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

Diversifying between stocks and bonds

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

Layer one is insurance. Good coverage is often the most cost-effective protection available. The right liability limits, umbrella coverage, and well-written policies can cover legal defense costs and usually resolve claims before they become financially devastating. Layer two is the proper entity structure for “inside liability.” If a lawsuit arises from a specific rental property or a specific business activity, you want that risk contained. For rentals, this often means using an LLC so that a problem at one property does not automatically threaten other properties or personal assets. For operating businesses, it often means separating the “operating company” from valuable assets such as equipment, intellectual property, or real estate, and documenting the relationship

Bonds can help provide balance through good times and bad

If you own rental property or run a small business in California and want a practical overview, I prepared a short guide titled “Asset Protection in California: What Works and What Does Not.” It explains common structures, common mistakes, and the questions you should ask before making changes.

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Download the guide here: https:// www.360epi.com/asset-protection-ca-whatworks/

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

Diversifying between stocks and bonds

Financial needs in retirement depend on the individual. However, some key planning strategies can help individuals determine how much they might need to save to

Need an estate plan, or an update to your current plan? We offer a free 45-minute consultation at our Walnut Creek office.

Bonds can help provide balance through good times and bad

comfortably in retirement.

Diversifying between stocks and bonds

Martin C. Johnson, Law & Tax, 1255 Treat Blvd., STE. 300, Walnut Creek, CA 94597.

Phone 925-289-8837

Bonds can help provide balance through good times and bad

Bonds can help provide balance through good times and bad

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

Diversifying between stocks and bonds

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

This article provides general legal information only. It is not legal advice. The information here is not a substitute for a consultation with an attorney about your specific situation.

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

How to determine your financial needs in retirement

Diversifying between stocks and bonds

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

Diversifying between stocks and bonds

Bonds can help provide balance through good times and bad

Bonds can help provide balance through good times and bad

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Diversifying between stocks and bonds

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

The key to riding out market fluctuations lies in owning a balanced mix of quality investments.

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

The key to riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

Bonds can help provide balance through good times and bad

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

riding out market fluctuations lies in owning a balanced mix of quality investments. Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

Although studies show that stocks have historically provided better long-term returns, it’s your asset allocation — the overall mix of stocks, bonds and cash — that ultimately can determine how well your portfolio performs.

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds can help reduce risk through

NThis chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

might need to live comfortably after calling it a career.

can help reduce risk through better price stability if you hold them until maturity. If a bond is sold prior to maturity, however, it may lose principal value.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Identify your ideal retirement age

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

Aguilar Jr

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

Bonds can provide a steady stream of fixed-income payments that can help you weather stormy markets. Bond prices and interest rates may change, but you can expect to receive regular interest payments and the bond’s original principal value at maturity, provided the bond doesn’t default. Even if you don’t need the income, bonds

and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Bonds rose when stocks fell — Down stock market years (1981–2022)

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

Bonds rose when stocks fell — Down stock market years (1981–2022)

Stock and bond prices generally don’t move in tandem. In other words, when stock prices decline, bond prices may rise, and vice versa. This relationship helps a well-balanced mix of investments potentially achieve more stable returns. So if you own bonds when the stock market drops, they may help reduce your losses.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance

o one knows what the future holds. So people need to plan for the years ahead, particularly in regard to saving for retirement.

Tony Aguilar Jr Financial Advisor

Tony Aguilar Jr Financial Advisor

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

This chart shows that since 1981, bonds have provided returns nearly every year when stocks declined. Of course, past performance is not a guarantee of future results. But the fixed-income investments in a portfolio can help smooth out returns during times of volatility.

Advice abounds regarding how much money retirees will need to live comfortably in retirement. One common approach suggests retirees should aspire to replace 70 to 80 percent of their pre-retirement income, while another strategy urges retirees to save 12 times their final pre-retirement income, meaning someone making $100,000 in the year they retire will need at least $1.2 million in retirement savings to maintain their lifestyle.

Each of these approaches are just strategies, and how much a person actually needs in retirement will depend on a host of variables unique to each individual, including the age a person retires, his or her health status at the time of retirement and personal goals for their golden years.

For example, those who hope to retire at 65 and travel extensively in retirement will likely need more savings than someone who hopes to retire at 70 and travel less frequently.

Though variables unique to each person will help to determine how much to save for retirement, there are some additional ways to identify how much you

Arguably the most significant variable related to saving for retirement is the age at which a person hopes to retire. Some may have the luxury of choosing their own retirement date, while others’ personal health or employers may make that choice for them. But it’s good to remember that the longer a person continues to work, the less retirement savings that person will need.

When trying to determine how much to save for retirement, first identify your ideal retirement age and then go from there, recognizing that this important variable can change over time.

Identify the lifestyle you hope to live

If the romanticized ideal of a jetsetting retirement lifestyle appeals to you, then you’re likely going to need to save more for retirement than someone whose vision of life after working is less glamorous.

It’s possible for many retirees to live their ideal lifestyle in retirement, but

Tony Aguilar Jr

Photo courtesy of Metro Creative

live

those whose ideal is marked by expensive pursuits like regular international travel will need to start earlier and save more than someone who envisions occasional trips but more time at home.

Don’t overlook healthcare

costs

Healthcare costs for retirees are heavily dependent on individual health. But even the healthiest retiree might experience a sudden and potentially costly medical issue, so it’s best for everyone to plan for sizable healthcare expenses in retirement.

The Employee Benefit Research Institute estimates that couples will need to have saved at least $188,000 to have a 90 percent chance of covering their healthcare expenditures in retirement. That figure is subject to variables unique to each individual, but it can serve as a useful measuring stick as adults try to determine how much they need to save for retirement.

For more information, contact any of the tax and financial specialists in this Money Matters section. – Courtesy of Metro Creative

MIKE’S ESTATE PLANNING MINUTE 2025

By Michael J. Amthor, Esq.

MEDI-CAL WAKE-UP CALL: ASSET LIMITS RETURN AND PLANNING CAN’T WAIT

Long-term care is one of the most significant challenges seniors face, as Medicare does not cover custodial care such as nursing home assistance. Medi-Cal fills this gap for those who qualify, but major eligibility changes are coming in 2026.

Many people underestimate their likelihood of needing care. Life expectancy for someone age 67 extends into the midto-late 80s, and about 70% of seniors will eventually need help with daily activities. More than half of those age 65 and older will incur long-term care expenses. In Brentwood, California, the median annual cost of a private nursing home room is nearly $188,000, while in-home care averages $87,000 per year.

California previously eliminated the Medi-Cal asset limit for applications submitted after January 1, 2024. However, the California Department of Health Care Services has announced that the asset limit will return in January 2026. At that time, individuals seeking long-term care MediCal benefits will be limited to $130,000 in countable assets, plus $65,000 per additional household member. A primary residence, one vehicle, and household items remain exempt.

Although homeowners can still

qualify, Medi-Cal estate recovery rules allow the state to seek reimbursement from a beneficiary’s estate, potentially placing a lien on a home after death.

One planning option is an irrevocable Medi-Cal trust. Assets transferred into the trust are no longer countable after 30 months, income can still be received, and the home can be lived in and protected from estate recovery.

Additional Medi-Cal changes include a 2026 enrollment freeze for undocumented adults over 19, loss of non-emergency dental coverage in July 2026, and a $30 monthly premium starting in July 2027 for certain beneficiaries.

Take the next step today. Speak with an experienced elder law professional to evaluate your current plan and explore strategies to prepare for future longterm care needs. To schedule a FREE consultation, call 925-516-4888.

For more one on one information, please attend our free seminar on 1/27 or 1/29 at the Brentwood Community Center 6:30-8:30pm. To register, please visit our website at goldenlegacylaw.com or visit www. youRSVP.com, code BUWYAV or call 866748-1088. Seats are limited – don’t wait! – Advertorial

Simple ways to get back in creditors’ good graces

credit rating is a key component of a strong financial foundation. Adults who can demonstrate a track record of sound financial decision-making and responsible money management are seen as safer bets by landlords and lenders than those who have shaky payment histories. Thankfully, consumers can take simple steps to rebuild their credit.

1. Start paying on time. of the fastest ways to build debt is to skip or miss payments on consumer debts like credit cards. When that happens, consumers must pay percentage-based interest charges, which can be especially high on credit cards. When borrowers don’t pay on time, relatively small debts can quickly balloon, costing consumers sizable amounts of money and threatening their financial reputations. In addition, the financial experts at NerdWallet point out that

late payments can stay on a credit report for more than seven years, which underscores the significance of paying bills on time each month.

2. Use as little credit as possible. Credit use ratio is one of the variables reporting agencies like Experian use to determine consumers’ credit ratings. Overuse of credit hurts a credit score, so consumers with poor credit histories are urged to avoid using credit cards when they have funds available in their savings or checking accounts. Consumers now have readily available access to information that determines their credit scores, and that includes their credit utilization ratio.

Monitor that ratio and make a concerted effort to keep it low.

Data from Experian gathered in the third quarter of 2022 revealed that the average use ratio among consumers whose credit scores were considered excellent was 6.5 percent, while those whose scores were considered fair had a ratio of 56.1 percent. The disparity in these ratios underscores their significance in relation to building a strong financial reputation.