BLINC

BANKING ON THE FUTURE

BCB is building a network of partners

THE MiCA MODEL Europe’s regulatory challenge

CAPITAL IDEAS

How to attract tradfi capital

BANKING ON THE FUTURE

BCB is building a network of partners

THE MiCA MODEL Europe’s regulatory challenge

CAPITAL IDEAS

How to attract tradfi capital

Why BCB is putting regulation first

+ +

STABLECOIN: THE BUZZWORD OF 2025

INSTANT PAYMENTS ARE NOW A REALITY

We’re located at stand no.45 8-10 APRIL 2025

2025 is set to be a watershed year for the digital economy. Crypto assets have at last become an established feature of the financial landscape, the barriers between mainstream finance and the digital economy are dissolving and the world’s leading financial institutions are expanding their investments and services into the world of cryptocurrency.

This makes 2025 the ideal year for BCB Group to be launching BLINC, a magazine named after our very own instant settlements network for BCB clients, which will be a regular forum for news and insights about our business and about the wider digital economy.

In this inaugural edition, we look at key developments in the integration of mainstream and digital finance, through our own growing range of banking partnerships. We will also be delving into the Market in Crypto Assets (MiCA) regulation, which — in our view — poses significant challenges for many in our industry but also presents great opportunities for firms that embrace new standards in technology, compliance and professionalism.

Existing clients will find plenty of news about our products and services, and those less familiar with BCB will gain an insight into our capabilities and our ambitions, and most importantly into our vision for the whole industry going forward.

Welcome to BLINC. Welcome to the future of finance.

Jerome Prigent, Managing Director, BCB Europe

BCB Group, leading provider of payment and digital asset services, and BlockFills, a leading digital assets trading and market technology firm for institutions and professional traders, have announced a partnership to deliver multi-currency payments.

The agreements align BlockFills’ strength as a trading and liquidity provider with BCB Group’s international fiat currency payment rails, further developing BlockFills’ client offering and expanding BCB’s fast-growing instant payments network.

Within the terms, BlockFills has adopted BCB Group payment accounts in US Dollars (USD), Sterling (GBP), Euro (EUR), and Yen (JPY) for its fiat currency operations. BCB is also providing virtual IBANs, allowing BlockFills to efficiently manage and reconcile payments in and out of its accounts.

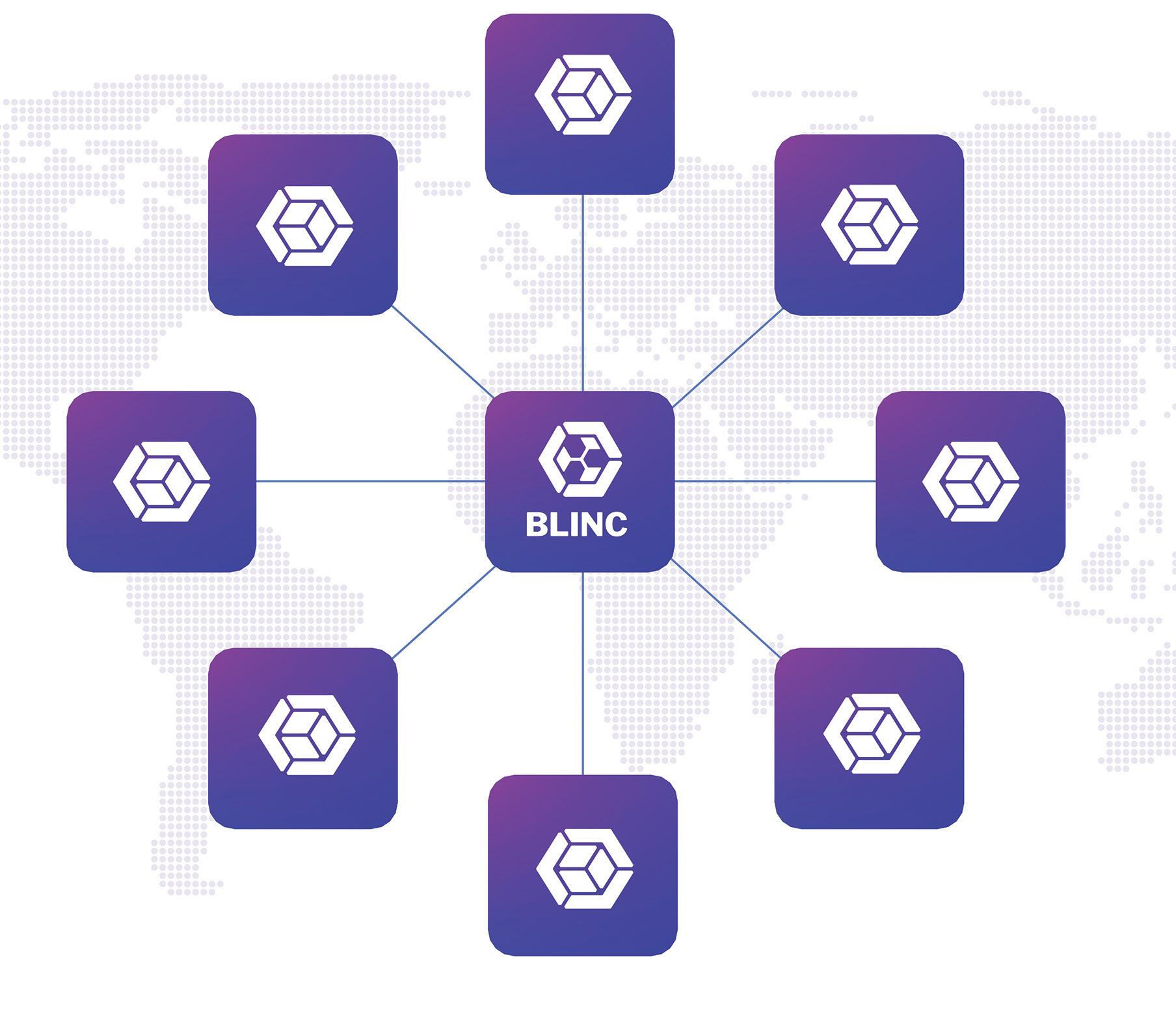

BCB Group payment accounts also have access to BCB’s proprietary payments system BLINC, which enables instant and fee-free transactions between all BCB account clients.

BCB Group has unveiled a reengineered website, putting its comprehensive product suite and regulatory-first approach front and centre of its expansion plans for 2025.

The new site has been designed for use by crypto natives and newcomers to digital assets, emphasising BCB’s focus on bridging the gap between digital assets and traditional finance.

“Working with BCB Group has enabled BlockFills to deliver streamlined payment solutions to our clients, speeding up transactions as well as on and off-boarding between crypto and fiat,” said Nick Hammer, BlockFills' CEO. “We have also increased our own operational efficiencies through multiple currency accounts and virtual IBANs.”

Oliver Tonkin, co-founder and CEO of BCB Group, said: “Getting BlockFills onboard is a valuable step forward for us into the North American crypto trading market where BlockFills is a major liquidity provider. It is also great to welcome another organisation to BLINC and its ever-expanding network of users.”

BlockFills opened its accounts with BCB Group in October 2024, accessing services through BCB’s Client Console, and is now offering the service across its global base of 1,700+ institutional clients.

EU, digital assets businesses will have to demonstrate that they are fit for the future.

It reflects the importance of regulatory standards as key to the next stage of digital assets evolution.

Oliver Tonkin, Chief Executive of BCB Group, said: “We believe 2025 is going to be a pivotal year for our industry, with a huge focus on the links between digital assets and mainstream finance. Our website is designed to reflect our role in enabling that integration.”

BCB’s Unified Platform, which allows institutional clients to store, make payments and trade in both crypto and fiat currencies, is the focus of the site, alongside the group’s ‘regulatory first’ principle.

“Our focus on meeting regulatory standards to protect our clients is fundamental to our business model. Details of our approach and our authorisations from leading financial regulators are a prominent feature of the site. We make no apology for that, because security and confidence are critical to our clients,” said Kym Routledge, BCB Group’s Head of Compliance.

The site provides a clear outline of BCB’s product suite and the real-world use cases for its systems and services, from on and off-ramping client funds to international payments and trading services across leading fiat, stablecoins and other cryptocurrencies.

With key regulatory frameworks coming into effect this year, including

With key regulatory frameworks coming into effect this year, including the wide-ranging Markets in Crypto Assets (MiCA) regulation from the

“Of course we want to attract new business through the new site,” said Tonkin, “but we also want to be the go-to place for all digital asset businesses to keep abreast of vital developments in the industry.” the

The site will also provide market insights, news and commentary from BCB’s experts in technology, trading, financial markets and compliance.

BCB Group has a major presence at this year’s Paris Blockchain Week joining more than 10,000 attendees and more than 400 speakers from 85 nations. The event is set to be bigger than ever and signals a further advance in the digital assets revolution.

Oliver Tonkin, BCB Group’s co-founder and Chief Executive, who will be among the senior team attending, said: “It's particularly exciting to see so many figures from traditional banks, exchanges and institutions in Paris this year. Paris Blockchain Week is always a fantastic opportunity for our industry to share ideas and make new connections.”

Tonkin added that the 2025 agenda was inspiring. “Between us we will be trying to catch every session.

I suspect the discussion on Markets in Crypto-Assets regulation (MiCA) on day one will draw quite a crowd as it is keeping many in the industry very busy right now.

“I am also keen to hear more about the growing interest from institutions in digital assets, which will be a focus of two of the sessions. Another area that we think will be a big growth opportunity for us is in iGaming and the sessions on Building Engagement in Web3 Gaming will make for a fascinating final session on Thursday.”

BCB Group is collaborating with two leading industry partners on a side event at this year’s conference and its senior team will be in Paris across the three days.

Sam Shrager, Chief Marketing Officer said: “We are in Paris to make new friends and partners. If you’d like to speak to one of our team and can’t spot them in the crowds, please do get in touch to arrange a meeting or head to our stand - number 45.”

BCB representatives attending include: Jerome Prigent MD, BCB Europe

Oliver Tonkin, Co-founder and CEO

Tim Renew, Deputy CEO Camille Tas, Head of Sales

Millie Tobin, Trading Abbie Wilson-Luck, Head of Account Management

Claire Barratt, Head of Strategy and Banking Partnerships

Omar Salem, Relationship Manager

Tidjane Barry, Account Executive

Sam Shrager, Chief Marketing Officer

Sarah El Jed, Account Executive

Contact: marketing@bcbgroup.io

Global fintech GSX Technologies was looking to extend and upgrade its payments services in key growth markets. Thanks to a partnership with BCB Group it has dramatically reduced settlement times and won new business.

“We are a trusted provider of payments services to our clients, and we wanted a partner to match. Working with BCB has allowed us to build on that trust with our clients and deliver even better payments services.”

Anita Luthra, Business Partnerships, GSX Technologies

The Aussie dollar challenge GSX Technologies specialises in payments solutions focused on FX and remittance solutions. With clients ranging from import/export businesses to online merchants and payroll service providers, GSX is a leading provider of payment services in India, Latin America, Africa and Asia.

It also offers on-and off-ramping services for companies using stablecoins.

A key growth opportunity was Australia, a market closely linked to the wider Asia Pacific economy, but one where on-and off-ramping into digital assets has historically been a slow process for all providers. BCB’s payment accounts and the expansion

of its payment rails into Australia provided the ideal solution.

Partnership provides solutions BCB Group and GSX have been building an ever-closer relationship, based on mutual respect and trust, since GSX opened its first account (in GBP) with BCB in July 2024.

As leading players in their respective markets, the groups both place a high importance on a compliance-first approach - GSX is authorised by India’s Financial Intelligence Unit, while BCB Group is authorised by both UK and French financial regulators.

“Having trust and confidence in your partners is vital in the digital assets market and that trust is the foundation of our relationship with BCB.”

Anita Luthra, Business Partnerships, GSX Technologies

With a partnership already in place, when BCB Group launched its local payments rails in Australia in November last year, GSX was one of the first to sign up for the service. The partnership brought almost immediate benefits.

Speeding up down under Settlement time for GSX clients in AUD has been cut by more than 50%, down from at least four hours to just two. The service also helped GSX secure a new

client in the region who had been looking for an AUD payment service.

“The whole sequence has been a great example of both GSX and BCB responding to market demand. Our partnership with GSX has widened the network and community of both our businesses and delivered to end-users. GSX is now one of our biggest users of AUD payments.”

James Mckeon, BCB Group

Following the success in AUD, GSX is opening accounts in Canadian dollars and Yen. GSX is also exploring how virtual IBANs provided by BCB could enhance the service to clients still further.

“We work really well with BCB and as partners we have developed a real trust and understanding. So, we see this as a continuous conversation between partners, where we understand what is on the BCB product roadmap and see how that can fit into our own growth plans.”

Anita Luthra, Business Partnerships, GSX Technologies

BCB Group was out in force at the Digital Asset Summit 2025 in New York last month, where presentations and debates were dominated by the growing links between digital assets and traditional finance.

Tim Renew, BCB’s Deputy Chief Executive, joined a key panel on The Maturation of Crypto Market

Structure, making the case for standardisation of regulation and for Europe’s growing importance in digital asset markets.

Renew argued that Markets in Crypto Assets regulations (MiCA) was one of the key moments in the evolution of digital assets in Europe, alongside an influx of capital from the US during the Biden administration, which had been seen as unsupportive of digital assets.

MiCA is not perfect, Renew said, but could be a benchmark for global standards in regulating crypto. "Is MiCA taking the right step on stablecoins for example? I am not sure. But everyone is waiting to see how MiCA is rolled out and maybe that is going to influence what the US does and how they regulate," Renew told the audience.

Meanwhile, fellow panellists agreed that standardisation in the broadest sense would be essential for crypto market structures to support continued expansion.

Chris Lawn, Chief Executive of Elwood Technologies, said

The Digital Asset Summit in New York was attended by more tradfi groups than ever before with speakers and delegates from global names, including Allianz, BlackRock and ARK Invest.

The presence of mainstream financial groups was indicative of the increasing convergence between tradfi and digital assets. This was also the central theme of a discussion between Michael Ippolito, co-founder Blockworks who organise the summit, and David Mercer, CEO of London-based fintech LMAX, in which Mercer emphasised the importance of attracting global institutions into the digital assets market, by adopting some of tradfi’s key pillars.

"I think what's probably wrong or what has to change in crypto today are the simple tenets of traditional finance - separation of function, segregation of funds,” Mercer said adding: “Brokerdealers are not exchanges. Exchanges don't act as principals. Custodians are not exchanges. [In tradfi] we

have separation of function and segregation of funds.”

Mercer said that by adopting such key tenets, crypto would be able to grow to its full potential.

"Let's go back to those simple tenets. Then we will have an industry that can truly flourish, that can converge within tradfi and that can become USD30 trillion, USD50 trillion, USD100 trillion, not the USD3 trillion we're talking about today.”

But while raising the challenges that crypto needs to meet, Mercer concluded on a highly positive note, arguing that major banks were set to enter directly into crypto markets in the foreseeable future.

Asked to predict the major development he expected in the coming year in the convergence of tradfi and digital, he said: “A tier one bank will start to clear major institutions into spot crypto trading. Number two, a bulge bracket bank will offer spot digital assets trading to its customers. When that happens, guess what? They all follow.”

"jurisdictional fragmentation" was a significant problem. "There are no standards. The industry has done a great job, but we need to standardise. We need to come together as an industry and with the institutions that are coming [into digital assets]."

News that the Securities and Exchange Commission (SEC) had dropped its long-running legal case against Ripple was greeted by a standing ovation at the Digital Asset Summit (DAS) in New York last month.

Ripple CEO Brad Garlinghouse announced the news live at the conference, coming on stage moments after posting the announcement on X. The news was greeted by cheers and applause from the session audience.

Garlinghouse admitted the four-year battle with the SEC over XRP sales had been a "painful journey" but declared: "I feel vindicated."

BCB Group Chief Executive Oliver Tonkin, who was attending DAS, said: "For many people here, Garlinghouse's announcement will be a standout moment from this year's New York summit. It's one of the most powerful signals yet of the total change in attitude to crypto under Trump and reinforces the view I am hearing from many people here, that we are at an inflection point for digital assets."

Extreme views on cryptocurrencies from both supporters and critics are misplaced, according to Mohamed El-Erian, Chief Economic Advisor to financial group Allianz, President of Queens' College, Cambridge and Chair of Gramercy Funds Management LLC Management.

Speaking at the Digital Asset Summit in New York last month, El-Erian said: “From day one people said it’s either a fraud or it will dominate everything, and I always said these corners are misleading. It’s going to be something in the middle.”

The key to exactly what role digital assets will play in the financial ecosystem will depend crucially on adoption, he said, noting that some mainstream finance firms who a few years ago called crypto a ‘fraud’ were now significant players in the asset class.

El-Erian’s balanced view also extends to the potential for stablecoins to replace the dollar, or for Bitcoin to become a global trade currency.

“[Stablecoin] is an important invention that deals with both the supply and the demand side so it’s a useful addition to the ecosystem - as long as they are stable. It’s going to continue to expand and it’s not going away,” he said.

However, he noted, regulators would be likely to resist stablecoins becoming dominant. “You can be part of the system but if you are going to dominate the system you are going to trigger a reaction from regulators,” he said.

A similar situation applies in the potential for Bitcoin to become a global trade currency and replace the dollar, El-Erian argued. With payment systems being “weaponised” - for example in Russian banks being excluded from SWIFT – El-Erian said authorities would remain wary of anything that undermined the potential for payments to be a tool for geopolitics.

He also argued that the addition of Bitcoin to US reserves should not yet be seen as significant. Adding seized cryptocurrency to US reserves

Illicit activity in crypto amounts to just 1% of the market, according to industry-leading compliance specialists Chainalysis.

Speaking at the Digital Asset Summit (DAS) in New York last month, Chainalysis co-founder and Chief Executive Jonathan Levin said criminal activity needed to be traced and eradicated but was lower than many people thought.

“Criminal activity on crypto is still less than 1%. Even though we talk about these big hacks or compromises it's still a very small amount, given the total amount of assets that

are out there,” Levin said.

"If you think about the industry having a USD3 trillion market cap, a few billion dollars is a lot of money but it's not in comparison to the total.”

Chainalysis provides investigation, compliance and anti-fraud software to more than 1,500 organisations, including leading financial firms as well as regulators and law enforcement services.

Based on its insights, Chainalysis produces an annual Crypto Crime Report, a survey of all illicit activity carried out through blockchain.

“We want financial institutions to

President Donald Trump threw down the gauntlet to Europe in his address to the Digital Asset Summit in New York declaring that his policies would enable the US to “dominate crypto”.

In an unscheduled address delivered remotely to the main auditorium, Trump attacked the tighter regulatory approach of the Biden administration and declared: “With the right legal framework, institutions

large and small will be liberated to invest, innovate, and take part in one of the most exciting technological revolutions in modern history.”

The comments reinforced the growing sense that the US and Europe are pulling in different directions on digital assets with the EU instituting a more structured regulatory environment.

Trump’s crypto stance will be a key topic of discussion among

amounted to a movement in the balance sheet, he said, and not a change in capital flows, which would only occur if the US substituted fiat reserves for Bitcoin.

understand that not all crypto is money laundering and to make sure that they have the data at their fingertips,” Levin told the DAS audience.

Chainalysis is used by BCB Group as part of its advanced compliance and monitoring systems and Kym Routledge, BCB’s Global Head of Compliance, said Levin’s message was a vital one. “Illicit activity is a very small part of the crypto industry, and we maintain the highest standards and ensure we have the right tools and skills to keep our clients’ assets secure,” she said.

attendees at Paris Blockchain Week, said Jerome Prigent, MD for BCB Europe.

“We are broadly supportive of the EU’s regulatory approach to crypto, but there are also some elements of the Trump agenda that we see as positive. Each market will set its own rules, but hopefully there will be enough common ground globally to allow digital assets to flourish as a truly international market.”

Virtual IBANS, fully supported by BCB Group infastructure, are an important enhancement to the IBAN identifiers used in traditional fiat account payments.

Our payment accounts can now be partitioned into any number of sub-accounts that you can label with your clients’ names, identified individually by virtual IBANs, which roll up to your account’s main IBAN.

Reduce Risk Compliance and anti-money laundering challenges are reduced, through clear segregation and improved transparency of funds.

Our vIBANs cut costs and complexity, giving businesses time back to focus on strategic goals and other vital corporate tasks.

Secure Enhancement of security through account privacy and reduction of manual processing.

Activate Virtual IBANS for your business

Speak to your BCB customer service representative or visit bcbgroup.com to find out more.

Reduce payment rejections

Better experience for your customers

Improve open banking settlement

Faster payments

Smoother transactions

Trade cross border

Mary Pennington, Head of Product, BCB Group

The first quarter of 2025 has been a big start to the year for the team at BCB, kicking off with a significant launch down under.

Following the release of our Australian dollar (AUD) payments account in 2024, clients with an AUD account can now also make payments and receive deposits through NPP (New Payments Platform), Australia’s national fast payments infrastructure that enables

real-time payments, 24/7. Access to NPP means faster payments, streamlining transactions and improving efficiency.

…and sharper pricing on trading pairs

We’re also able to offer improved pricing for AUD pairs. Whether you’re trading AUD with fiat or crypto pairs, our trading team can offer market leading pricing. Within our standard trading product is access to our trading desk as well as access to the trading console for self-serve. Get in touch if you want to know more.

Two-factor-authentication at your fingertips

Security is a vital feature of BCB products, and we wanted to put clients in control. Client administrators can now reset twofactor-authentication (2FA) for members of their team in our client console.

EUR International gets a makeover International payments via our EUR payments account have been given an upgrade, meaning transfers can be made in your own name, payment cut-off times have been extended to 1600 (UK), and we are delivering faster settlement and quicker

“If it’s April, this must be Paris!”

Sam Shrager Chief Marketing Officer, BCB Group

Last year was a whirlwind for BCB Group and 2025 is gearing up to be even busier. Our agenda for the next 12 months is already packed with product launches, a pipeline of major deals and partnerships and, of course, a global tour of the top digital assets, payments and banking conferences.

Hong Kong, London, followed by New York were our first ports of call.

NYC first for Bitcoin Investor Week followed by the Digital Assets Summit (DAS) (see our coverage of DAS on pages 4-5). Now here we are in Paris for Blockchain Week and we are out in force in the French capital.

Next up, Token 2049 in Dubai, then Consensus Toronto, Money 20/20 Europe in Amsterdam, SIBOS in Frankfurt and more...

But the conference round is just part of our activities in 2025. Amid the events, I am preparing for a raft of announcements on our current and soon-to-be-launched payment products and services across crypto and fiat currencies, and partner case studies to showcase the challenges we solve for our clients.

Details of all these events and activities will be available on our website, which we recently relaunched. The refreshed site provides a shop window to our solutions, emphasising our ‘regulation-first’ approach. We believe this will be a key point of difference for us in the year of MiCA

transaction processing, ensuring your funds settle sooner.

Continuing the theme of automation, we’ve also invested in automating trading withdrawals. Trading clients can now initiate withdrawals directly from the BCB Markets trading user interface, providing straight-through processing and faster settlement.

Giving your business access to a key market like the US has and continues to be a priority for us. Following a soft launch in December, our most recent enhancement to our USD payments account has increased the payment processing times for domestic and international payments to 2130 (UK), previously 1700 (UK). This change better aligns to US banking hours, opening up a larger operating window in a key global market.

It’s been a busy start to 2025, but at BCB we believe in continuous improvement and refinement to our services. Rest assured we will be keeping up the pace throughout the year.

and other regulatory developments.

Another key theme for 2025 will be the growing interconnection between groups both within our industry and the wider world of finance. In this developing environment, sharing ideas and insights from technology to regulation is more important than ever, which is one reason we have launched BLINC, the magazine you are holding in your hands right now.

Naturally, BLINC is an opportunity for BCB to highlight news about our business and attract new partners. But it is also about discussion and analysis; a chance for our experts – from finance to technology to compliance – to share their understanding and fuel debate across our industry and beyond.

We are in a fast-moving sector and competition is fierce. However, along with our partners, clients and other firms in the ecosystem, we are forging a new, global business and finance community. As a marketing professional, I don’t think there is much else that could be more challenging and exciting.

24-28 Feb

Bitcoin Investor Week

New York

18-20 Mar

DAS New York

New York

8-10 Apr

Paris Blockchain Week

Paris

30 Apr

Token2049

Dubai

14-16 May Consensus

Toronto 3-5 Jun Money 20/20

Amsterdam

29 Sep - 2 Oct SIBOS Frankfurt

1-2 Oct

Token2049

Singapore

13-15 Oct DAS London London 15-17 Oct

Eurpoean Blockchain Convention

Barcelona

26-29 Oct

Money 20/20

Las Vegas

Effective compliance is vital for the future of the digital assets industry, says BCB’s Kym Routledge, both for service providers and their clients.

The digital assets market is maturing at a rapid pace. Once regarded as a ‘wild west’ of finance, the sector is being embraced by mainstream institutions and integrated into regulatory frameworks. Rather than being seen as an intrusion, these developments are being welcomed by responsible service providers as an aid to risk management and a boon to businesses.

None of which is to say there are no challenges in adapting to changing regulations, not least the fact that rules are evolving at different speeds in different markets.

BCB Group has adopted a straightforward approach to the wide variety of standards across the world’s market – always taking the highest regulatory standard as the base level for compliance.

“There are obviously individual nuances that we need to meet in specific markets, but we absolutely always go to the highest regulatory level,” says Kym Routledge, BCB Group’s Head of Compliance. “If you consider onboarding, we have clients onboarding for our UK entity, our Swiss and EU entities and/or for other services and we will always adhere to the highest standard in each case, whichever regulator’s standard that might be.”

Building a trusted platform

The fast-moving nature of the digital asset world and fintech in general means some organisations try to run before they can walk – at least when it comes to compliance.

“We often see fintechs and startups that are aiming to make money very quickly, although this can be at a risk of long-term reputational cost. When you’re going to go for the quickest win or solution it often becomes a tick-box mentality towards regulation, applying or setting up where there is little to no regulation. Now that is ‘possible’ for short-term success and growth but reputable providers like BCB Group will not entertain these kind of lax controls. We are faced with multiple strict audits from banking partners, regulators and those we impose on ourselves, and I can only imagine the reports if we started allowing a tick-box mentality to breach our standards!” Routledge says.

Having superior compliance in place is vital to BCB’s risk management but also helps all clients in the BCB ecosystem. One of BCB’s objectives is to create a network of clients that can benefit from being part of that ecosystem, for example by using its fee-free instant payments system BLINC. For that system to work and continue to be a trusted success, all clients need to know that everyone else in the system has been through robust due diligence. →

We have clients onboarding for our UK entity, our Swiss and EU entities and/or for other services and we will always adhere to the highest standard in each case, whichever regulator’s standard that might be.

Kym Routledge

AMLA is going to unite Europe’s Financial Intelligence Units and that, to me, is something we all should be pushing for. There needs to be more transparency between us all to make this work, so anything that’s bringing about transparency is, for me, a winner.

Kym Routledge

BCB has an in-house team of 24 experts working on compliance and financial crime, supported by an external team of 24, covering the full client lifecycle with BCB Group.

“We operate three tiers of checks for client and transaction monitoring” Routledge explains. “The first level is getting rid of most of the noise. Any issues are escalated to the second level – our senior analysts – who are trained to challenge and to spot anything which requires full investigation. Those examples go to level three where we really dig deep and conduct interviews with the clients.”

The vast majority of issues are resolved without difficulty, but one or two cases every month raise a significant red flag. BCB naturally rejects prospective clients that have been unable to meet the compliance requirements. Similarly, this may be the case for existing clients, after internal transaction monitoring and investigation.

The regulatory and compliance agenda for the year ahead is a busy one. The incoming Markets in Crypto Assets (MiCA) regulation from the EU is imposing requirements on service providers. BCB itself is already an authorised Digital Asset Service Provider and is well on its way to meeting all the requirements of MiCA.

The other key development in the EU has been the creation of the Anti-Money Laundering Authority (AMLA), objective of which is to coordinate national authorities to ensure the correct and consistent application of EU rules on money laundering and counter terrorist financing.

Both MiCA and AMLA are examples where the EU is leading the way and are set to become the highest standards in these fields.

“AMLA is going to unite Europe’s Financial Intelligence Units and that, to me, is something we all should be pushing for. There needs to be more transparency between us all to make this work, so anything that’s bringing about transparency is, for me, a winner,” says Routledge. Routledge’s team already monitors transactions, and where appropriate raises a suspicious activity report. Routledge has also stopped some payments that looked to be in breach of international sanctions.

The other pressing issue is Authorised Push Payment (APP) fraud reimbursement, an area where the UK authorities are pressing hardest with new regulations and which they implemented in October 2024.

“We have a lot of conversations with our clients, double checking the banners they have on their website, their geoblockers in place and the controls they have in place to warn their clients of the risks of crypto investing. These ongoing checks and conversations do result in us offboarding the clients who don’t maintain rigorous standards.

“With the APP Reimbursement Policy now live, we have used this as a trigger across all of our retail exchanges to revisit them, to talk to their compliance teams to see what they are doing with regards to safeguarding themselves and their clients against this reimbursement regime.”

Again, Routledge adds that these conversations have been hugely beneficial to all sides, with positive insights and ideas being shared between everyone involved. Such sharing and cooperation are, Routledge argues, the way forward, since the APP regulations mean that a confirmed fraud will result in shared liability between the Payment Service Providers that allows the fraudulent payment to be sent and received.

The evolution of regulation is not always smooth – and sometimes regulation goes awry – but Routledge argues that it is beholden on organisations like BCB to be engaged in dialogue with other companies and regulators to build a robust compliance culture in the industry, because effective regulation is in everyone’s interest.

Routledge openly describes herself as someone who loves rules and for one simple reason: “When it comes to compliance, you have a duty to protect your own business and your clients, which, to a responsible service provider, amounts to the same thing.”

Within financial services, financial stability and regulatory compliance are always front of mind for buyers seeking solutions.

While innovation, agility and relevance are key components, too, they count for nothing if a financial provider can’t breed trust through solid compliance.

Managing Director BCB Europe, Jerome Prigent, knows this well. He spent time earlier on in his career in organisations of all sizes, from financial behemoths such as BNP Paribas and GE Capital to more agile fintechs that were finding their way.

In 2025, this experience and knowledge acquired is about to become a very precious commodity indeed.

For the unacquainted, BCB Group is a company with bold ambitions on the global payments stage. Styled as a “financial provider for the digital assets economy”, the business is roaring upwards, with the favourable winds of regulatory change in its sails.

The company has already grown a trusted client base of crypto natives but is now starting to secure strong interest from banks, platforms, payment networks and fund groups as the broader capital markets ecosystem embraces the transformational potential of digital assets.

But, while the company has been hard at work lining up a conveyor belt of deals and partnerships, Prigent has also been busy working to secure the highest possible regulatory blessings because he believes that will put daylight between BCB Group and its competitors.

“When you have a tier one licence, like France, you just tick a button and you have all 30 European nations accepting your licence for the purpose of passporting,” he explains.

“If you earn your licence from a European nation with a lower tier, there can be a delay to entering a new country within the European Economic Area.”

Making the effort

BCB Group already holds full CASP (Crypto Assets Service Provider) status with France’s regulator, the Autorité des Marchés Financiers (AMF). In doing so, the company has laid the groundwork for meeting the terms of the EU’s Markets in Crypto Assets (MiCA) regulation.

This extensive effort to be regulated and registered in France seems light years away from the approaches of some of BCB Group’s competitors only a decade ago.

“We had a period of rock and roll, with lots of innovation and diversity in the market,” Prigent recalls. “Nobody knew where we were going, but that’s not the case anymore.”

“When you are choosing a regulatory domicile, you have a choice. You can go to countries such as Lithuania or Cyprus, where the process is easier but, after that, you might find you struggle to get the type of customers that you want.”

Prigent says BCB knew that working to obtain a regulatory licence in France was going to be the more demanding option, due to scrutiny of compliance, provision of finance forecasts and the forensic detail with which assessors evaluate an application. Despite this, he believes that is the best approach for the business as the digital assets market starts to broaden.

“It’s all about trust,” he says. “If you do secure licenced status in France, you can be sure that it will help you attract new customers. In 2025, trust is the first word on my lips.”

With the MiCA regulation bringing digital assets, their issuers, and the service providers that handle them, into one pan-EU regulatory framework, traditional financial institutions within the bloc have been tipped to accelerate their own willingness to make partnerships.

After all, MiCA affords conservative compliance folk legal clarity and includes clear provisions for licensing digital asset service providers, which should help traditional firms looking to partner with specialists who offer digital asset services.

Over the past five years, banks including BBVA, Deutsche Bank, Goldman Sachs and UBS have all urged regulators to add “regulatory clarity” for them to be able to feel comfortable doing more in the digital assets arena.

For BCB Group, which already partners with organisations to offer digital asset solutions across trading, payments, and custody, its own investment in regulatory endeavours, is part of a longer-term strategy.

“To build something that is durable, you need to provide a lot of resource, time, effort and documentation,” Prigent says. “But once it is done, it is done for a long time

a lot of resource, time, effort and documentation,” Prigent says. “But once it is done, it is done for a long time and the benefits are huge.

sides understand

“It has become essential for credible market participants to understand both traditional and decentralised finance. My job is to ensure we help our clients find the common ground so that both sides understand each other.” ◆

Jerome Prigent Managing Director BCB Europe

Building bridges between the digital assets world and mainstream banks is key to the future of the digital economy.

Back in the early days of cryptocurrency the most fervent disciples of digital assets dreamt that this new financial tool would replace traditional financial institutions. But as the digital assets market has matured, it has become clear that the digital and ‘tradfi’ worlds have more to gain by working together.

BCB Group’s strategy has been to build links across the digital community and with the traditional financial system, and Claire Barratt, Head of Banking and Strategic Partnerships, is at the coal face of this endeavour.

“It is true that fintechs have completely disrupted the market, but it's also really important to have those partnerships with banks. They are the ones that have direct access to local payment rails, and so through our banking partners, we can tap into that,” says Barratt.

“There are several players in the market that have been very successful in supporting the fintech space. These banks have been expanding globally, either through acquisition or by going through the application process to obtain the appropriate licences to achieve direct connectivity to local payment rails,” she adds.

Barratt is well placed to build bridges between digital asset markets and traditional banks having spent her early career in mainstream banking. She began at Commerzbank before joining Wells Fargo, where she focused on correspondent banking – the transaction side of the business – and gained her qualifications in compliance. This experience and skillset have proved invaluable in forging ties with the banking sector. →

It is true that fintechs have completely disrupted the market, but it's also really important to have those partnerships with banks. They are the ones that have direct access to local payment rails, and so through our banking partners, we can tap into that.

Claire Barratt Head of Banking and Strategic Partnerships

Andrew Bywater Head of Enterprise Sales BCB Group

Clients want to know who we are working with, and it is really valuable to tell them we are working with high-calibre

banking partners with good creditworthiness.

Andrew Bywater

Confidence is key

Barratt’s move into the digital finance sector began when she was approached by Revolut and decided digital assets were the future. She later moved to stablecoin payments group Orbital where, as well as gaining more experience of the market, she found herself as a client of BCB. Watching BCB at work and expanding its business, she jumped at a chance to join the company when the opportunity arose.

“BCB Group has a great story to tell because it is regulation-first and heavy on compliance. Being able to articulate that to big banks is always well received,” says Barratt.

It is also well-received by BCB clients, says Andrew Bywater, Head of Enterprise Sales. “Clients want to know who we are working with, and it is really valuable to tell them we are working with high-calibre banking partners with good creditworthiness,” he says.

BCB does not advertise the names of all its banking partners but is happy to discuss such details with clients and potential clients.

Forging a global network of partnerships

BCB’s banking partnerships cover a range of business activities including treasury and safeguarding, trading and foreign exchange, and these relationships are key

to BCB’s payment accounts and FX services in more than 20 fiat currencies.

Camille Tas, Head of Sales, says that it is from such beginnings in trading services that larger and deeper relationships develop.

“Once we are giving a banking partner FX business, they can get to know us, our clients and our trading flows, and they will then consider us for a larger relationship with payment accounts and other services,” she says. “It takes time to develop these relationships, but the confidence and trust that come with time are essential.”

One of the most crucial arrangements with banks, which deliver significant benefits to BCB’s customers, are connections to payment rails within local jurisdictions, because providing ‘the last mile’ in payments is what creates a truly international payments service.

Barratt explains: "Our customers are typically international and so they want cross-border payments. But what they are also often looking for is to be able to unlock new jurisdictions for their business. For example, our banking partnerships recently enabled us to launch local rails in Australian dollars with the two local payment systems. For our clients, that means they have an easier route to launching in Australia.”

Australia is just one example of accessing local payment rails. BCB has relationships in multiple markets and continues to expand, with prospects in the Middle East and Asia expected to come to fruition this year.

The holy grail, however, will be the US banking system. Barratt admits that “regulatory uncertainty” makes the US a hard nut to crack but she is optimistic: “I’m very excited for this year. It is very complex in the US, but I think we are seeing the first movers in bigger banks starting to look at this.”

BCB’s network of banking partnerships with Tier 1 and 2 banks extends across Europe and Asia. Barratt is reluctant to give a precise number but says BCB has well over a dozen banking partnerships, making it one of the leaders in the digital assets market for building relationships with the mainstream banking sector.

It has also set itself ambitious targets. “Our aim is to be a touchpoint in one in three of all transactions linked to cryptocurrency,” says Barratt.

The calibre of banking partners is the first step to a resilient payments system and BCB requires that its banking partners are part of their respective bank deposit insurance schemes – including the European Deposit Insurance Scheme (EDIS), the UK’s Financial Service Compensation Scheme (FSCS) and the Federal Deposit Insurance Corporation (FDIC) in the US.

But resilience is also about having multiple providers to ensure continuity of service in the event that one bank backs out of the market.

“My job is to build redundancy into our services in each currency and market," says Barratt. “This is quite a volatile space, and banks’ appetites can change. So, if a bank says, ‘Actually we don’t want to bank crypto services anymore’, we’ve got alternatives and can just plug our clients back into another one of our partners.”

A watershed year ahead

Stablecoins are widely seen as a key bridge between the digital assets market and traditional banking, delivering the benefits of the blockchain to essentially fiat currency transactions (see our Stablecoin explainer on page 23).

Stablecoins’ potential is clear to both digital natives and mainstream finance and, as Barratt says, stablecoin is likely to be one of the buzzwords of 2025. The path ahead however is not entirely clear as the EU’s Markets in Crypto Assets (MiCA) regulation comes into effect over the coming 6-18 months.

Tether has said it will not be applying for USDT to be MiCA-compliant, meaning the best-known US dollar stablecoin will not be tradeable by MiCA-authorised operators in Europe. Barratt, however, believes stablecoins will still be a major force on this side of the Atlantic.

Once we are giving a banking partner FX business, they can get to know us, our clients and our trading flows, and they will then consider us for a larger relationship with payment accounts and other services.

Camille Tas

The integration of digital and traditional finance will also expand the market of potential clients beyond crypto native companies, Barratt argues, from smaller international businesses to global corporations.

“Those big corporates will be thinking about how they can leverage stablecoins for their treasury so we're now looking at these crypto-adjacent clients,” she says.

Digital and tradfi - rivals and partners

Relationships and partnerships between digital finance and mainstream banks are fast developing but there are complexity and nuance in those relationships too.

The potential for mutual gains from partnerships is clear, but at the same time, payment service providers and banks are in competition. For the foreseeable future, however, Barratt sees the benefits of partnership as the dominant factor.

“I have really seen a shift in the last year,” says Barratt. “You see a lot of banks that want to go into the digital asset space but may not have the expertise. It is about giving them the ability to access digital assets by leveraging a partnership with an organisation, such as BCB, which has the experience and is doing it safely and with a regulatory-first approach.” ◆

Digital asset leaders call for liquidity and regulatory suitability as markets start to diverge.

Companies in the digital assets ecosystem must do more to better understand the pedestrian pace of adoption among traditional asset owners, if they are to bring much-needed fresh capital into the market.

That was the message from panellists speaking at the London Digital Assets Forum on 3 February 2025 in an opening plenary session exploring macroeconomic trends and predictions for 2025.

BCB Group’s CEO, Oliver Tonkin, joined Tim Grant, CEO at Deus X Capital, Patrick Heusser, Head of Lending at Trident Digital, and Dadi Kristjansson, CEO of Viska Digital Assets.

Addressing a near-capacity room, the business leaders agreed that while support was needed from European regulators to stimulate further innovation in the market, there was also a need to work harder as an industry to attract new capital from sovereign wealth funds, insurance companies and pension funds.

Deus X Capital CEO Grant acknowledged that traditional institutional investors were more interested than ever before in the sector but said this hasn’t yet translated to a mass inflow of new capital.

He said: “The biggest issue, lubricant, determination of volume and progress in institutional crypto is leveraging capital. If I say that and you don’t know what I mean, you have to learn this. It will affect everything – what you build, who you sell to, and how you price risk.”

Grant explained that there was a need for digital asset innovators to better understand and appreciate the world of traditional institutional finance if liquidity is to significantly increase.

“Just look at the traditional model, where I raise money, I manage money and I get leverage from my prime broker.

That does not exist in crypto yet. There are hedge funds including Brevan Howard and Marshall Wace who all want to trade [crypto], but there is not enough volume in the derivatives market as yet, and not enough service providers to allow this to happen.”

Grant explained that if the market is to benefit from the ability to leverage at scale, then new capital needs to find crypto – and digital asset investments more broadly – more attractive.

“We can’t just keep re-staking because that is not leverage. We need sovereign wealth funds, pension funds and insurance companies. We have to ask, ‘how we get the next billion of fresh capital in?’ If we don’t solve that, we will have the same conversation in a year from now.”

Speakers agreed, however, that the catalyst for market growth was not solely the tapestry of the market participants. The senior leaders addressing delegates said we were entering a critical time for European regulators to move more quickly, especially now that the US has outlined plans to aggressively fuel growth.

“We know that, when the US regulation comes out, it will be quite aggressive,” said Tonkin, CEO of BCB Group.

“They are not expecting people in London or Brussels to end up in an arms race, but we need to ‘get real’ quite quickly.

“If we don’t try to compete in terms of offering regulatory certainty and an innovation- and business-friendly environment, we might well lose out. I remain optimistic, but the window is very small,” he added.

Trident Digital’s Head of Lending, Patrick Heusser, agreed that the European regulatory agenda had now slipped a considerable way behind the US and urged policymakers to act quickly to offer “regulatory clarity” to builders of new infrastructure.

With the lead-up to President Trump’s inauguration coinciding with a long bull run for Bitcoin, some speakers asked whether Western government views had notably shifted on the asset since Trump’s previous presidential term. However, speakers were unable to agree on the extent to which Bitcoin would now become accepted as a major currency in its own right.

“We have seen a lot of discussions around a National Bitcoin Reserve in the US and Bitcoin becoming a reserve asset more broadly,” said Kristjansson, CEO of Viska Digital Assets.

“The Czech Central Bank said it was exploring its use as a potential reserve asset.”

We can’t just keep re-staking because that is not leverage. We need sovereign wealth funds, pension funds and insurance companies. We have to ask, ‘how we get the next billion of fresh capital in?

Oliver Tonkin

BCB Group’s Tonkin said he would be “surprised” if the UK were to ever recognise Bitcoin as a reserve asset, however, and maintained that he was equally sceptical about its adoption by the European Central Bank.

“The chances of HM Treasury holding Bitcoin is pretty low,” he said. “Ursula von der Leyen was pretty bearish on it too. I would be pretty surprised if it happens here in any material way, but in the US, who knows?”

Oliver Tonkin CEO BCB Group

Deus X Capital’s Grant said the industry’s fascination with Bitcoin should not be the theme that leads conversations in 2025, urging digital asset pioneers to focus instead on attracting new capital into digital assets from the world’s largest asset owners.

“[Bitcoin] is a bit of a red herring,” he said. “We also talked about Central Bank Digital Currencies for a while, but they were a bit of a stupid idea. We should be talking about how to get the Abu Dhabi Investment Authority to put fresh capital into the market.

“What does the Norwegian Pension Fund need to see? What is it that they are not seeing today that is preventing them from applying risk capital? What doesn’t give them the security and comfort to allocate capital?”

Panellists explored whether the SEC’s decision to rescind the rules laid out in its Staff Accounting Bulletin (SAB)121 in January would be enough to encourage more capital into the digital assets arena, but they believed this would have a limited effect.

Trident Digital’s Patrick Heusser said: “I am not 100% sure that SAB121 would unlock the sovereign wealth funds to pour in capital, but it is another step that was needed. If banks do not have crypto within their investment schemes and can’t actually advertise it to their clients, there won’t be much happening.

“Banks will never push it from their side and there is still not enough clarity and hunger from the bank industry to push this asset class.”

BCB Group’s Tonkin said he expected stablecoins to remain central to digital asset discussions throughout 2025, although he urged European regulators to consider the suitability of new related rulesets.

“Stablecoins, their use cases, volumes and circulation have risen in the past 12 months and that will continue,” he said. “Globally, stablecoins are a massive market now and have become quite respectable. There are genuine use cases which make them very exciting.”

Tonkin added one note of caution in Europe, relating to the recently introduced Markets in Crypto-Assets Regulation, questioning how suitable the new rulesets would continue to be to this rapidly developing asset group. He urged regulators to continue to build out their frameworks to ensure they keep pace with market innovation. ◆

Lou Casteou provides the perfect setting whether you are looking for an elegant and relaxing château holiday rental, the perfect romantic wedding venue, an impressive, private location to host a corporate event, or you are looking for energetic retreats in the most beautiful environment.

A beautiful château located in the stunning Esterel mountains, five minutes from the sandy beaches of the French Riviera and the clear, blue Mediterranean sea. www.loucasteou.com Lou Casteou 850 chemin du plan Guinet 83 600 Frejus , Côte d’Azur, France +44 (0) 7990 573 287

Lou Casteou is available to rent for groups and events, and we can help you plan your stay from catering to activities.

The château also hosts several fun retreats throughout the year including Salsa, Fitness and Tennis retreats. Please get in touch for more information and booking enquiries.

Digital currencies are typically seen as a form of investment or a store of value and they can be all these things, but for many businesses one of their most valuable uses is as a route to cheaper and faster payments.

This use case for blockchain-based currencies is now coming to the fore with the growing use of stablecoins, which are set to be one of the most significant growth areas of digital currency in 2025.

Stablecoins have already been growing fast and by the end of 2024, the market capitalisation of all stablecoin reached USD$200bn. Much of this growth is being driven by their potential to transform the global payments system, not just for companies involved in the digital currency sector, but for any business that makes frequent international payments.

Stablecoins, like other cryptocurrencies, are based on blockchain technology but rather than having an entirely free-floating value determined by investors or speculators, stablecoins are pegged to a specific currency, for example the USD or EUR.

While the value of stablecoins can deviate slightly from that of their underlying currency, they do not undergo the same volatility seen with pure cryptocurrency.

It is this peg to a fiat currency, combined with the payments and transfer efficiency possible with a digital currency, that creates the unique use-value of stablecoins.

International payments

Transferring money across borders to overseas divisions or to pay suppliers can be a laborious and slow process, taking days or even weeks to complete. Banks’ protocols, regulation and creaking technology of payments systems creates delays and costs.

A typically international payment via SWIFT, for example, takes anything between two and five days. Timings vary depending on a raft of factors outside of any business’ control.

In fact, traditional international

payments are a bit like an international rail journey, involving multiple stations, connecting trains, different tickets, and a number of different rail companies.

Stablecoins can be transferred instantly, at lower costs and more transparently than traditional bankbased payments networks. In essence, payments and transfers by stablecoin cut through the multiple systems and third parties involved in traditional methods, offering a unified payments system available to any business making cross-border payments.

Simplicity security and certainty

Using stablecoins for payments is remarkably simple. All that is required is a payment account and a linked digital wallet for storing stablecoins –such as a BCB Crypto account.

BCB allows for multiple sub-accounts each denominated in a different crypto to fiat currency. Fiat currency can be exchanged into stablecoins without leaving BCB’s platform and then payments can be made to any other digital wallet in the world.

Some businesses may be nervous about making payments via a digital currency, but with the right payment service provider, stablecoin transfers can be more transparent and more secure than traditional methods.

BCB’s crypto accounts are operated to the highest regulatory standards, in line with our French Digital Asset Service Provider (DASP) registration. Your crypto assets are stored in our

institutional-grade custody solution, secured with advanced hardware secure module (HSM) technology.

BCB’s ‘regulation first’ principles, supported by our experienced compliance and transaction monitoring capability, mean all our payments are carried out in full compliance with the requirements of all jurisdictions in which we operate. This includes a clear record of all remitters and receivers of international payments as required under the Financial Action Task Force (FATF) Travel Rule.

Stablecoin choices

There are a wide range of stablecoins available globally, and the market and technology behind it continues to evolve. Regulatory consultations and planning for stablecoin are underway in many markets, including the UK, but this is a sign that regulators themselves recognise the potential of this new international payments model to revolutionise international business.

BCB aims to remain agnostic and agile, meeting all regulations in whatever market clients need to operate, while ensuring the flexibility to pivot rapidly in response to that changing market and developing regulation.

Stablecoins’ future potential

The already formidable strength of stablecoins in streamlining international payments is just the beginning. Looking ahead, it has the capacity to streamline core business operations.

Some businesses may be nervous about making payments via a digital currency, but with the right payment service provider, stablecoin transfers can be more transparent and more secure than traditional methods.

As well as providing more efficient payment rails for international remittances, blockchain technology provides an automatic record of transactions. In principle, payments and reconciliation against invoicing could be contained within a single process – or reconciliation at source. The capacity for blockchainbased currency to combine data with payment has led some to call the technology ‘programmable money’.

Fast and effective payment is the most immediate force driving the rapid growth in stablecoin today, but fiatpegged digital currencies have the potential for even greater transformation of business processes. ◆

Making transfers through traditional payment rails can be a time-consuming and expensive process, but there is another way with BCB’s proprietary payments service.

Liquidity, and the free and rapid transfer of funds, is essential for efficient business operations and trading. Delays and fees for transferring money are friction in the system, that cost time and money.

This, of course, is not news to anyone operating a company or trading in financial markets, which is why it is remarkable that traditional payment networks, such as SWIFT, Europe’s SEPA, or the UK Faster Payments System, are still beset by limited operating hours, payment delays, transaction limits and sometimes fees.

BCB Group’s BLINC solution cuts through the costs and delays. Our proprietary technology, hand in hand with our ‘regulation first’ principles, means all BCB payments account customers can transfer fiat currency to each other with unparalleled efficiency.

BLINC payments can be made:

■ 24/7

■ Fee-free

■ With no limits on size of payment

■ To any BCB customer anywhere in the world

The BLINC directory of BCB customers includes exchanges, market makers, lenders, funds, brokers and traders worldwide.

As part of a standard BCB payments account, BLINC is naturally linked to our digital currency and assets capabilities. But as a pure fiat-to-fiat system, BLINC’s capabilities are a valuable tool for any organisation, whether or not they have any involvement in the digital assets sector.

Additionally, BLINC payments can be made in all leading fiat currencies, including USD, GBP, EUR, SGD, CHF, JPY, AUD, and NZD.

Overcoming the legacy

Existing traditional payments systems have evolved through decades of technological implementation in the banking system. The result works but, as the saying goes, if you were setting out to design a payment system, you would not start from here.

Most of us are familiar with the almost instant payments possible in our personal bank accounts, but such instant transfers are not possible when the sums of money are larger.

In the UK, the Faster Payments System regulation does not allow instant transfers of more than £1 million. In Europe’s SEPA, the limit is even lower at €100,000.

Even when smaller sums are involved, cross-border payments can incur fees through some networks.

Timing also becomes a factor, with each bank operating its own schedules and cutoff times for payments - request a transfer late in the afternoon and it might not begin processing until the following day. Time zone differences between sending and receiving banks can add to the delay, and with time differences also comes exposure to financial market risk in FX rates.

The grit in the system of traditional payments stems from two sources. The first is legacy banking technology. Banking systems that were once the leading edge of technology are now creaking museum pieces that hamper rather than facilitate the payments network.

The second is regulation, which rather than being built into systems at the outset, are naturally an addon that creates further friction in the system. This is not to decry regulation – at BCB we pride ourselves on our authorisations from leading regulators and take a ‘regulation first’ approach. The difference is that all our products and solutions, including BLINC, are created to work with regulation rather than to rub up against it.

Compliance and technology hand-in-hand BLINC is possible because we have built our technology stack and our compliance frameworks together –each strengthens the other rather than creating a clash. At the same time, as a crypto-native company we have had to design our payments systems from scratch, meaning they have been designed without the hurdles that beset legacy banking systems.

Existing traditional payments systems have evolved through decades of technological implementation in the banking system. The result works, but if you were setting out to design a payment system, you would not start from here.

Our onboarding process is streamlined but rigorous, meaning that anti-money laundering checks have already been taken place. This means we have confidence in our clients, and they can have confidence in each other.

With those regulatory issues addressed at the very outset, it is possible to create a technology system that allows instant transfers without jumping through regulatory hoops for each transaction.

BLINC comes as a standard feature for all our payments account customers, meaning they can transfer fiat currency between each other – at no cost, 24/7 and with absolutely no limits on the sums involved.

How our customers are using BLINC

Many households operate a bills account, setting aside a certain amount of income each month to pay regular outgoings and perhaps adding a little extra for those inevitable unknowns.

BLINC can be used in exactly the same way. BLINC is a separate basket that sits alongside your core payments account. Transferring money into BLINC is not immediate, but once money is there it can be sent to

Many households operate a bills account, setting aside a certain amount of income each month to pay regular outgoings and perhaps adding a little extra for those inevitable unknowns. BLINC can be used in exactly the same way.

any other BCB customer instantly.

Many of our clients know their typical regular outgoings to other BCB customers and so hold appropriate funds in their BLINC basket, enabling those payments to be made instantly when they are due.

Others may have fewer regular transactions, so they simply hold sums in their BLINC basket to enable payments to be made instantly whenever needed.

All BLINC users enjoy the key benefits of being able to receive payments faster, thus improving their cash flow and liquidity and ensuring they can deliver payments instantly to other BCB clients, building better business relationships.

When entering a phase of aggressive growth, it helps to have an experienced management team leading the charge.

Since the start of the year, BCB Group has been building an increasingly global brand presence through tactical activations, awards, content and highly targeted events.

The company arrives at this year’s Paris Blockchain Week in high spirits, having raised its profile through some co-ordinated outreach efforts, having successfully secured its European E-Money Institution and Digital Assets Service Provider status (in France) a year earlier.

Throughout 2025, the business is keen to tell the next chapter of its story and will be showcasing new products and solutions at Token2049 Dubai and Money 20/20 in Amsterdam, among others.

But first, the crypto world descends on Paris and BCB is arriving with brand presence, market momentum, a larger commercial team and exciting plans for product development, partnerships and news of a string of corporate wins.

Last year, the Group onboarded a new playmaker to drive forward the group’s aggressive expansion plans. Taking the role of Deputy Chief Executive Officer, Tim Renew is a hire that reflects BCB’s intent. Renew’s surname is somewhat appropriate in that he has a track record of refreshing the commercial appeal of businesses, having previously developed fintechs to a position where they’ve successfully enticed investment from Bank of America, Citibank, National Australia Bank and others.

Target driven, he is all about discipline and high stakes achievement. And, in BCB Group, he’s found a business that mirrors his own ambitions.

“My background is building companies from nothing,” he says. “I’ve always loved the crypto industry and wanted to get into it. I’d seen that BCB Group was already extremely successful and had attracted interest from some of the biggest names in the industry.

“It’s exciting, now, as the markets are changing and more competition builds, to be responsible for building structure and scaling that. BCB has a great customer base, supported by talented staff.” →

It’s exciting, now, as the markets are changing and more competition builds, to be responsible for building structure and scaling that. BCB has a great customer base, supported by talented staff.

The first time I went to the US to pitch my last company, we had a meeting with a major US bank and we were told ‘it’s never going to be a thing’. 12 months later, we were told ‘it’s definitely a thing but it’s not coming to the US’. Six months after that, they signed the contract.

Tim Renew

→ The company’s new Deputy CEO has the profile of a restless high achiever. As a youngster he wanted to join the military and, more recently, joined the Army Reserves to later be selected for officer training. A keen sportsman, Renew has competed in ultra marathons, Ironman triathlons and he is also an accomplished climber.

At the same time, however, he also likes to embrace nature and likes to balance his family commitments with his two daughters with time alone.

“I like discipline,” he says, noting that it is not uncommon for him to jump out of bed at 5am and go for a run. But he readily admits that this is equally applicable to his approach to work.

“I expect people to work hard but also to have fun while they’re doing it,” he jokes. For those who have worked at California-based fintechs (as Renew has), this work hard, play hard culture is engrained into the workplace mentality.

Renew’s workplace philosophy is not the only thing he is bringing to BCB. He brings substantial experience and a persistent approach to commercial vitality.

“The first time I went to the US to pitch my last company, we had a meeting with a major US bank and we were told ‘it’s never going to be a thing’. 12 months later, we were told ‘it’s definitely a thing but it’s not coming to the US’. Six months after that, they signed the contract.”

He explains that these stages on the buyer’s journey are typical for buyers of emerging technology as many potential clients can be slow to recognise the business need.

“They weren’t lying,” he says. “They just weren’t ready. The same is the case now with much of what BCB offers. It is a matter of time, and it is about making sure that we are in the right place. What BCB does is a game changer.”

Communicating that innovation through a marketing lens will be key to the commercial team’s success as it goes into this next period of growth. During his career, Renew has been at this stage before.

At Cloud.IQ, he worked as Chief Revenue Officer between 2013 and 2018 in London before moving to San Jose in California for another two years. There, he oversaw business growth that led to the company scaling to 150 people before securing an investment from PayPal.

In 2020, he moved to take up a CRO position with Banked, a business that would later become a market leader with investment from the aforementioned banks including Citi and Bank of America.

“The Chief Revenue Officer role was once one of those ‘made up’ roles from Silicon Valley, but it is becoming more established,” he says, noting that this was the original role he landed at BCB Group, before becoming Deputy CEO promptly after that.

“It is about looking holistically at a business, across product, customer experience and marketing and spotting what needs to happen to help achieve the customer objective.”

Listening and understanding

When asked how he intends to use his experience to affect change at the business, he is keen to underscore that success comes only from gathering information when beginning any new role.

“The first thing I do is shut up and I listen,” he says. “To identify any opportunities or inefficiencies, you need to watch first. Only once you’ve done that, you can act. It’s important to look for areas where you can make fast wins and streamline some of the processes.

“There are several levers you can pull to optimise growth. It is all about taking the vision of the CEO from the boardroom and making it happen,” he adds.

The prospect of Paris Blockchain Week holds real appeal to Renew who describes the community at the event as “valuable” noting that having decision makers in one room across multiple sectors is the perfect platform to begin new commercial relationships.

“It is invaluable to have that level of knowledge in one place, at one time,” he says. “Realistically, business gets done when people talk to people.

“I’ve done a huge number of shows in my time. I try to do something in each geographical region because if you do the same events, in the same region, you only get the same people.

“If you want to meet bankers, there is no better place than SIBOS. If you want to meet fintechs, you go to Money 20/20. Paris Blockchain Week has a mixture of everybody.”

Renew explains that events like this are key to BCB understanding its target markets more deeply by establishing stronger relationships.

“If we are going to get the growth… you have to understand who to sell to, why we sell to them and what the ROI is versus someone else. BCB is in a great position. It doesn’t have to do anything different, we just need to do it better.

“The cherry on top, of course, is going into the crypto adjacent industries such as fintech, gaming and marketplaces.”

Renew is hoping to make the most BCB’s in-house analytical capabilities too, to measure whether new commercial approaches are succeeding.

“We need to get the analysis, the data, and run specific campaigns around when products are being released

If we are going to get the growth… you have to understand who to sell to, why we sell to them and what the ROI is versus someone else. BCB is in a great position. It doesn’t have to do anything different, we just need to do it better.

Tim Renew

and when events are happening,” he says. “Only then can we understand how we are going to pursue a segment.

“I believe you should have a continuous feedback loop. Compliance is a big one for the industry we are in.

So we need to be certain that we can onboard clients and know how quickly we can do that.

“Having done so, we need to be able to capture all those different touch points and then analyse the data. There is a division of BCB called revenue operations. It has an extraordinary ability to soak up this information and come out with new suggestions.

That’s really useful.” ◆

The EU’s Markets in Crypto Assets (MiCA) regulation will be a baptism of fire for some crypto businesses, but for established players already embracing regulation, it will be a huge opportunity.

Businesses of any kind rarely welcome the arrival of new regulations, but for the crypto sector, MiCA, which took effect on December 30, 2024, represents a major step forward and a spur to growth.

The implementation of MiCA will not be painless and will place significant new burdens on crypto service providers. For smaller companies, meeting the terms of MiCA may stretch their resources, even perhaps to breaking point.

But MiCA also represents a coming of age for crypto in Europe. It is a recognition from the European Securities and Markets Authority (ESMA) as well as the European Commission and Parliament that

crypto is an established part of our financial infrastructure.

It also represents an opportunity for crypto service providers themselves, creating standards for licensing and prudential regulation, which will provide crypto investors with confidence in their service provider and coin issuers.

“This is the MIFID for crypto,” says Marie Arras, Head of Compliance for BCB payments and BCB markets in the EU. “The law harmonises the way we treat customers and how we do business. It will help the crypto business and will help the market grow.”

While welcoming MiCA, Arras recognises that for some smaller operators it may prove a challenge.

“MiCA has a lot of requirements and you need quite a few resources to address it. If you don’t have broad enough shoulders, it will take a lot of time, and some businesses might not survive.”

BCB, meanwhile, has been at work on MiCA ever since the first consultations were launched and Arras is confident that BCB will meet the requirements very soon after their implementation.

Proving your prudence

The central pillar of MiCA is the requirement for full licensing of Crypto Assets Service Providers (CASPs).

Licensing is overseen at national level by the relevant National Competent

Authority. For BCB that means France’s Autorité des Marchés Financiers (AMF).

For larger groups, such as BCB Group, that are already registered as digital asset service companies, upgrading to full CASP will be more straightforward and BCB is already well on its way to that licence.

The key aspect of a licence that some crypto service providers may find challenging is the prudential requirement. Firms must demonstrate they have capital buffers in place to enable them to continue to operate in the event of market problems and so ensure they can continue to return assets to clients.

The sums required vary and according to Arras, meeting the requirement may be a shock to those who have no existing licence. Businesses that are already authorised as electronic money institutions (EMI) are used to such guardrails. “If you are not used to these types of guardrails, this is something that is really going to change the game. It’s great for clients, but it comes with a lot of obligations and oversight from the regulators.”

A second key component, according to Arras, is the requirement that firms ensure cybersecurity. On the one hand, this may appear to be a moving target, with ESMA calling for modifications in the regulations as recently as October that will require CASPs to provide an external audit of their cybersecurity.