FUELING PROGRESS

In the

By Katie Schroeder

John

a

is expanding equipment compatibility, data tools and policy engagement to help farmers connect their crops to growing biofuel markets like SAF.

Keith Loria

For ethanol producers, the key to unlocking sustainable aviation fuel eligibility and premium pricing lies in lowering carbon intensity

By Sylvain Riba

At the recent Clean Fuels Conference, leaders from across the aviation and clean fuels value chain examined how production realities, infrastructure constraints and evolving policy frameworks are shaping

next phase of deployment.

By Veronica Bradley

Anna Simet EDITOR asimet@bbiinternational.com

Despite Challenges, the Beat Goes On

It’s tough to argue that the past couple of years haven’t been tumultuous for the sustainable aviation fuel industry. When the U.S. SAF Grand Challenge debuted in 2021, the sector was riding an exciting wave of announced investments, partnerships and project development. Momentum was strong, and optimism toward meeting 2030 targets was widespread. But just a few years later, storm clouds rolled in.

A recent report by Boston Consulting Group highlights that shift: “While SAF supply increased 1,150% worldwide over the past three years, project announcements for new SAF facilities declined 50% to 70% from 2022 to 2023, due primarily to economic uncertainty and higher energy and operating costs that squeezed company margins.” So, even though production volumes were rising, the project pipeline began to thin.

Compounding the challenge has been ongoing policy uncertainty, particularly in the U.S., where long-delayed guidance on the 45Z clean fuel production tax credit left developers and investors waiting for clarity. For a very capital-intensive industry that heavily leans on long-term offtake agreements and stable policy signals, that uncertainty has caused many final investment decisions to hit the brakes. Many industry players are in observation, or wait-and-see mode, and that 2030 targets are unlikely to be achieved under current conditions, the BCG report suggests.

Indeed, offtakes from airlines are a major factor. While airline involvement in SAF agreements is still growing, contract lengths are shrinking. Until 2023, according to the International Air Transport Association, the average announced duration exceeded six years. But as of January 2024, it fell to average a paltry two years.

Production paints a clearer picture of the deviation of ambition and execution. A January 2025 progress report from the U.S. Department of Energy’s Bioenergy Technologies Office showed that 30 million gallons of SAF were produced domestically in the first three quarters of 2024, up from 5 million gallons in 2021. At the same time, announced domestic projects represented more than 3 billion gallons per year of potential capacity by 2030, tied to $44 billion in announced funding. On paper, if 100% of that an-

nounced capacity comes online as planned, domestic production would meet or even exceed the 3 billion gallon annual target. In reality, that outcome is extremely unlikely, as industry data suggests that only about a quarter of announced SAF capacity comes online on time, and roughly half of projects ultimately reach operation. That gap between press releases and production can often seem like the Grand Canyon.

Difficulties persist and likely will for some time. But that does not mean the outlook is bleak. Shifting gears, there are indeed bright spots—45Z will be finalized, some commercial plants are ramping up, states are enacting policy to support SAF, new pathways are advancing through ASTM approval, and more countries are setting targets or mandates for SAF adoption. Those in the biofuels industry understand that progress isn’t linear. Cycles of expansion and contraction are part of the maturation process, and the SAF sector is still very much in that evolution.

As for a specific bright spot, the Pacific Northwest has become a hot spot for SAF. In our page-12 feature article, “Accelerating Innovation,” associate editor Katie Schroeder reports on the Cascadia Sustainable Aviation Accelerator in Washington state, a coalition focused on driving SAF development and adoption forward with the ultimate goal of producing 1 billion gallons in the region by 2035. Made of up powerful industry stakeholders including Boeing, Washington State University, Alaska Airlines and the Port of Seattle, exciting things are on the horizon for this region of the U.S., and the accelerator’s members intend to demonstrate what can be replicated elsewhere. Said Josh Heyne, director of the Bioproducts Sciences and Engineering Lab at WSU, “Washington has many of the key attributes to accelerate that market and push it forward into something bigger, not only for the state but globally as well.”

On that note, we’re excited to share that the North American SAF Conference & Expo is moving to Tacoma, Washington, in 2026, after three consecutive years in the Minneapolis/St. Paul area. More will be shared in the upcoming months, but be sure to mark your calendars for Aug. 25-27.

EDITORIAL

DIRECTOR OF CONTENT & SENIOR EDITOR

Anna Simet | asimet@bbiinternational.com

SENIOR NEWS EDITOR

Erin Voegele | evoegele@bbiinternational.com

CONTRIBUTIONS EDITOR

Katie Schroeder | katie.schroeder@bbiinternational.com

MAP DATA & CONTENT COORDINATOR

Chloe Piekkola | chloe.piekkola@bbiinternational.com

DESIGN

VICE PRESIDENT, PRODUCTION & DESIGN

Jaci Satterlund | jsatterlund@bbiinternational.com

SENIOR GRAPHIC DESIGNER

Raquel Boushee | rboushee@bbiinternational.com

PUBLISHING & SALES

CEO

Joe Bryan | jbryan@bbiinternational.com

PRESIDENT

Tom Bryan | tbryan@bbiinternational.com

CHIEF OPERATING OFFICER

John Nelson | jnelson@bbiinternational.com

SENIOR ACCOUNT MANAGER

Chip Shereck | cshereck@bbiinternational.com

SENIOR ACCOUNT MANAGER

Bob Brown | bbrown@bbiinternational.com

SENIOR MARKETING & ADVERTISING MANAGER

Marla DeFoe | mdefoe@bbiinternational.com

Subscriptions to SAF Magazine are free of charge distributed biannually. To subscribe, visit www.SAFMagazine.com or submit a mailing address to SAF Magazine

Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. Back Issues & Reprints Select back issues are available for $3.95 each, plus shipping. Article reprints are also available for a fee. For more information, contact us at 866746-8385 or service@bbiinternational.com.

Advertising SAF Magazine provides a specific topic delivered to a highly targeted audience. We are committed to editorial excellence and high-quality print production. To find out more about SAF Magazine advertising opportunities, please contact us at 866-746-8385 or service@bbiinternational.com.

Letters to the Editor We welcome letters to the editor. Send to SAF Magazine Letters to the Editor, 308 2nd Ave. N., Suite 304, Grand Forks, ND 58203 or email to asimet@ bbiinternational.com. Please include your name, address and phone number. Letters may be edited for clarity and/or space.

2026 International Biomass Conference & Expo

March 31 - April 2, 2026

Gaylord Opryland Resort & Convention Center | Nashville, TN

Now in its 19th year, the International Biomass Conference & Expo is expected to bring together more than 900 attendees, 160 exhibitors and 65 speakers from more than 25 countries. It is the largest gathering of biomass professionals and academics in the world. The conference provides relevant content and unparalleled networking opportunities in a dynamic business-to-business environment. In addition to abundant networking opportunities, the largest biomass conference in the world—powered by Biomass Magazine—is renowned for its oustanding programming and maintains a strong focus on commercial-scale biomass production, new technology, and near-term research and development. Join us at the International Biomass Conference & Expo as we enter this new and exciting era in biomass energy.

(866) 746-8385 | www.biomassconference.com

2026 Sustainable Fuels Summit: SAF, Renewable Diesel and Biodiesel

June 2-4, 2026

America's Center | St. Louis, MO

The Sustainable Fuels Summit: SAF, Renewable Diesel and Biodiesel is a premier forum designed for producers of biodiesel, renewable diesel, and sustainable aviation fuel to learn about cutting-edge process technologies, innovative techniques, and equipment to optimize existing production. Attendees will discover efficiencies that save money while increasing throughput and fuel quality. This worldclass event features premium content from technology providers, equipment vendors, consultants, engineers, and producers to advance discussions and foster an environment of collaboration and networking. Through engaging presentations, fruitful discussions, and compelling exhibitions, the summit aims to push the biomass-based diesel sector beyond its current limitations.

(866) 746-8385 | www.sustainablefuelssummit.com

2026 North American SAF Conference & Expo

August 25-27, 2026

Greater Tacoma Convention Center | Tacoma, Washington

The North American SAF Conference & Expo is designed to promote the development and adoption of practical solutions to produce SAF and decarbonize the aviation sector. Exhibitors will connect with attendees and showcase the latest technologies and services currently offered within the industry. During two days of live sessions, attendees will learn from industry experts and gain knowledge to become better informed to guide business decisions as the SAF industry continues to expand.

(866) 746-8385 | www.safconference.com

SAF Magazine News | By Erin

Treasury, IRS Release Proposed 45Z Regulations

The U.S. Department of the Treasury and Internal Revenue Service on Feb. 3 released proposed regulations for the 45Z Clean Fuel Production Credit, as updated by the One Big Beautiful Bill in mid-2025.

The proposed regulations are intended to help domestic producers of clean transportation fuel determine their eligibility for and calculate the value of the 45Z credit in line with changes made under the OBBB. The proposal provides guidance on credit determination, emissions rates, certification and registration requirements.

According to the IRS, 45Z provides businesses with an income tax credit for clean fuel produced domestically after Dec. 31, 2024, and sold by Dec. 31, 2029. To claim the credit, taxpayers must be registered with the IRS using Form 637 at the time of production.

To qualify for the 45Z credit, taxpayers must: produce transportation fuel that meets requirements for sustainability, emissions rates, coprocessing and prevention of double crediting; produce the fuel at a qualifying facility in the U.S., including its territories; be registered as a clean fuel producer under Section 4101 at the time of production; and sell the fuel to an unrelated person in a qualified sale during the taxable year. Transportation fuel produced after Dec. 31, 2025, must be derived exclusively from feedstock produced or grown in the U.S., Mexico or Canada to qualify.

The proposed regulations also confirm that the 45Z credit cannot be stacked with the 45Q tax credit for carbon capture, utilization and storage.

For fuel produced on or before Dec. 31, 2025, the credit begins at 20 cents per gallon for nonaviation fuels and 35 cents per gallon for sustainable aviation fuel. Facilities that satisfy prevailing wage and apprenticeship requirements may qualify for up to $1 per gallon for nonaviation fuels and $1.75 per gallon for sustainable aviation fuel. The SAF premium is eliminated beginning Jan. 1, 2026, with the credit capped at 20 cents per gallon, or $1 per gallon for qualifying facilities, for all eligible fuels.

For calendar years after 2024, the credit value is adjusted for inflation. In July 2025, the IRS announced the 2025 inflation adjustment factor would increase the credit to 21 cents and $1.06 per gallon for non-SAF fuels and 37 cents and $1.86 per gallon for SAF, depending on compliance with prevailing wage and apprenticeship requirements. The agency has not yet announced the 2026 inflation adjustment.

Eligible fuel must be suitable for use in a highway vehicle or aircraft and have a lifecycle greenhouse gas emissions rate of no more than 50 kilograms of carbon dioxide equivalent per

mmBtu. Eligible fuels cannot be derived from coprocessing an applicable material with a nonbiomass feedstock, nor can they be produced from a fuel for which a Section 45Z credit is allowable.

Within the regulations, the IRS states that if one fuel is used as a primary feedstock to produce a second fuel, and the first fuel qualifies as a transportation fuel under Section 45Z, the second fuel would not qualify for the credit.

“For instance, SAF produced from ethanol as a primary feedstock, and hydrogen produced from RNG as a primary feedstock, may not qualify as transportation fuel for purposes of Section 45Z,” the IRS continued. “However, a fuel could still qualify if a transportation fuel is used solely as a process fuel or other nonprimary feedstock input.”

As directed by the OBBB, the proposed regulations eliminate indirect land use change from lifecycle emissions calculations for fuels produced after Dec. 31, 2025. The proposal also indicates lifecycle greenhouse gas emissions rates for fuel derived from animal manure may be less than zero beginning in 2026.

Taxpayers may determine lifecycle greenhouse gas emissions rates by using the annual emissions rate table published by Treasury and the IRS or by obtaining a provisional emissions rate determination.

Under the proposal, transportation fuel is divided into two categories for emissions rate purposes: non-SAF transportation fuel and SAF. For non-SAF fuels, lifecycle emissions rates must be based on the U.S. Department of Energy’s latest GREET model. For SAF, emissions rates must be determined using the most recent CORSIA methodologies adopted by the International Civil Aviation Organization or a comparable methodology.

The IRS noted that some stakeholders requested the ability to lock in a lifecycle emissions rate tied to the year construction began on a facility. Under such an approach, a facility that began construction in 2025 could use the 2025 emissions rate table for all future taxable years. The proposed regulations do not adopt that approach; eligible taxpayers must update emissions rates annually.

The IRS is seeking stakeholder input on feedstock tracking approaches to ensure only fuels derived from feedstocks produced or grown in the U.S., Canada and Mexico qualify for the credit.

A 60-day public comment period will open following publication of the proposed regulations in the Federal Register. A public hearing is scheduled for May 28. A prepublication version of the notice of proposed rulemaking is available on the Federal Register website.

Montana Renewables, World Energy Partner to Scale SAF Deliveries

Calumet subsidiary Montana Renewables LLC and World Energy Clean Fuels LLC on Feb. 19 announced an agreement that will deliver more than 70 million gallons of SAF to the market over three years, reducing as much as 600,000 metric tons of CO2 emissions.

Montana Renewables is one of the largest SAF producers in North America and is set to significantly increase SAF production capacity with its MaxSAF 150 expansion. World Energy has been a leader in advanced bioenergy and low carbon solutions over three decades and is the world's first commercialscale SAF producer. The company is a pioneer in the carbon insets market, which enables corporate clients to acquire the environmental attributes derived from SAF to decarbonize their global aviation operations. Through this deal, MRL and World Energy will be accelerating SAF and emissions credit supplies to meet growing demand.

“MRL's MaxSAF expansion project is progressing rapidly and is on track to deliver economic benefits to the region's farmers, ranchers, and energy-related economy this spring,” said Bruce Fleming, CEO at Montana Renewables. “Market demand for SAF remains strong, and this agreement is another signal of our commitment to American energy independence and Montana agriculture.”

World Energy's long-term contract helps validate the significant new capital investments that Montana Renewables is making to scale the SAF industry.

In late October, Montana Renewables and parent company Calumet Montana Refining commissioned onsite blending and shipping facilities to offer a nominal 50/50 blend of renewable and fossil jet fuel certified under ASTM D7566 and ASTM D1655 specifications.

Treasury’s Proposed 45Z Guidance Draws Concerns Over Alcohol-to-Jet SAF

The issuance of proposed guidance on the 45Z Clean Fuel Production Credit by the United States Treasury Department in February finally offered some clarity for program participants who have spent months in the dark on the status and scope of their returns. While the proposed guidance addresses issues over the definition of a “qualified sale” in the scheme, in recent weeks, sources have said that the final package should also clarify issues with using one finished fuel to create another.

Under the guidance offered by Treasury on Feb. 3, the agency noted that, “if one fuel is used as a primary feedstock to produce a second fuel, and the first fuel qualifies as a transportation fuel for purposes of section 45Z, the second fuel would not qualify for a section 45Z credit.

“For instance, SAF produced from ethanol as a primary feedstock, and hydrogen produced from RNG as a primary feedstock, may not qualify as transportation fuel for purposes of section 45Z,” the agency continued. That language could sully the long-term plans for certain SAF pathways that rely on finished fuels, such as LanzaJet’s patented alcohol-to-jet process. LanzaJet became the first domestic producer to offer SAF using ethanol as a feedstock after opening its Freedom Pines Fuels facility in Soperton, Georgia, in November 2025.

And while that facility currently only produces about 10 million gallons per year, in recent years, major ethanol proponents have put notable stock into the potential expansion of operations that turn their fuel into SAF. In a fact sheet from 2024, the Renewable Fuels Association noted that “ethanol is a readily available low-carbon, low-cost feedstock for the production of SAF. With the right mix of policy, investment and science, the sky is the limit for ethanol-based SAF," RFA said at the time.

The idea even found support in 2023 from former President Joe Biden, who, at an event in Maine, told attendees that in 20 years, “farmers are going to be providing 95% of all the sustainable airline fuel.”

But with waning market incentives for SAF over other renewable fuels, momentum toward a significant expansion of SAF produced from other biofuel sources could be in peril under current guidance. Some of those waning incentives stem from changes made to 45Z last summer under the One Big Beautiful Bill Act, which put SAF on the same pricing tier of 20 cents to $1 per gallon, as all other biofuels for 45Z.

With the guidance also offering other positive developments for the ethanol industry, such as getting rid of indirect land use change from emissions calculations, producers of the biofuel could gain more from selling their fuel through traditional pathways than by sending it to be converted into SAF. In commentary offered on Feb. 13, global tax firm Latham & Watkins noted that the proposal allows “a fuel to qualify for the 45Z credit if its production process uses a transportation fuel solely as a process fuel or other nonprimary feedstock input.”

[Treasury’s guidance] was just implementing what was in the law, which is that only one of the parties can be the taxpayer...you cannot get on both sides of it,” said Anthony Reed, a partner with FGS Global, in regard to the proposed guidance.

The final destination for a 45Z credit is not purely of concern to certain SAF producers. As stated by the Renewable Natural Gas Coalition following the issuance of the proposal, the organization is “eager to address certain limitations around the use of RNG as a process input, or feedstock for the production of other qualifying transportation fuels.”

The Treasury could ultimately alter its guidance in the final package to better clarify the current landscape for SAF produced from other finished biofuels, explained Shia Sahay, a partner with Bracewell PRG, a day after the release. “There is going to be a disadvantage for certain technologies,” due to the language on double counting credits,” Sahay said.

This could have been done differently, Sahay added. “[Treasury] could have just said, ‘Well, if you sell feedstock to someone else who uses that feedstock to produce fuel, you cannot take 45Z.’”

Others more informed on the ethanol side of the equation also shared concerns over the dynamic. Monte Shaw, executive director of the Iowa Renewable Fuels Association, said “in terms of 45Z pushing alcohol-to-jet forward, we are at best in neutral.”

The parties who are concerned over the final recipient of a 45Z credit in production processes that use a finished fuel will have ample time to craft their arguments, as the agency scheduled its public hearing on the proposal for May 28.

A final package is expected sometime this summer.

Patrick Newkumet

OPIS Biofuels

Spotlight | Vista Projects

De-Risking SAF with the Right Design

As the sustainable aviation fuel (SAF) industry continues to scale, project viability depends on much more than promising chemistry. While new pathways and technologies continue to emerge, many projects struggle to bridge the gap between laboratory validation and reliable, large-scale operations—especially when multiple first-ofa-kind elements are integrated into a single facility.

For Vista Projects, a Calgary, Albertabased engineering and project delivery firm, that reality has defined its growing role in the SAF sector. “We’ve seen firsthand: Just because the chemistry works doesn’t mean the commercial project will work,” says Arman Hassan, a project manager at Vista Projects. “Scaling and integrating a process into a continuously operating commercial plant is a very steep climb.”

Digital Execution to SAF Engineering

Vista was initially brought into a SAF project to establish a digital project execution environment integrating engineering, construction and operations.

That engagement quickly expanded. “What started as front-end engineering support and advisory services evolved into full detailed engineering, procurement support and owner’s engineering,” Hassan says. The project—an electro-SAF (eSAF) facility using a first-of-a-kind technology configuration— presented both technical and commercial challenges. Vista ultimately assumed most of the engineering scope after the previous contractor struggled to manage the project’s complexity. According to Hassan, success depended on ensuring all plant systems and interfaces could be delivered and run as one integrated facility.

Vista has since expanded into a commercial-scale gas-to-liquids project using the Fischer-Tropsch pathway and expects to support multiple pathways as demand evolves, helping owners clear key project gates by bringing execution discipline, integration capability and delivery experience.

Compounding Complexity

Across pathways, Hassan says it’s often underestimated how quickly complexity compounds when new SAF technologies

are integrated with utilities/offsites, hydrogen, storage and blending, and stringent fuel specifications—often simultaneously.

Adding to that challenge are interface gaps between licensors, EPC firms and vendors. Scope splits that appear logical during development can create significant risk once projects enter detailed engineering. “Late design validation, late HAZOPs and late operational requirements are all symptoms of insufficient front-end discipline,” Hassan says. “So, it’s really important to pick the right partners and licensors.”

Even when engineering is optimal, external constraints—permitting timelines, labor availability and construction constraints—can still derail schedules.

Much More Than Drawings

Vista views itself as a project developer’s engineering partner—an approach it believes is critical for SAF projects, especially those led by startups or new entrants. “A lot of projects fall apart when there isn’t a strong owner team managing interfaces, risk and decision-making,” Hassan says. “Owner’s engineering is about protecting the owner’s interests, not just delivering drawings.”

That role includes overseeing licensors and EPC contractors, managing change, driving cost and schedule transparency, aligning stakeholders and ensuring technical decisions connect back to commercial reality. Vista also supports partner selection, providing an impartial view on licensors, EPCs, fabricators, constructors and key vendors grounded in execution track record.

One of the most common pitfalls Vista sees is inadequate front-end definition, particularly when teams move quickly past feasibility. “Strong front-end definition—a clear design basis, realistic yields and structured cost estimates—is critical to avoid sticker shock as projects move forward,” Hassan says.

Another risk area is scale-up strategy. Many SAF projects attempt to leap from lab proof-of-concept to commercial operation without sufficient intermediate validation, limiting opportunities to confirm performance and operability under pilot or demonstration conditions.

Feedstock: A Core Design Basis

As competition for SAF feedstocks in-

tensifies, Vista urges developers to rethink how feedstock is treated during project development. “Feedstock is a core design basis that affects pretreatment, catalysts, corrosion, wastewater, reliability and overall economics. So, you have to design for it deliberately.”

Seasonality, quality variation, supplychain logistics and local constraints should be reflected in plant design from the outset, along with a realistic understanding of how impurities affect performance and maintenance. Hassan notes that downstream requirements can be overlooked early, including product specifications and certification expectations that influence design and operations.

While many developers seek maximum feedstock flexibility, Vista cautions that flexibility comes at a cost. “You can design for a range within a targeted envelope, but you can’t design a plant to handle everything while meeting the project’s economic drivers,” Hassan says.

De-Risking with the Right Partners

As SAF development continues, Vista is strengthening its repeatable delivery playbook by incorporating lessons learned, standardized risk frameworks and improved execution strategies. The company also leans on modularization and digital execution expertise to reduce field costs, improve transparency and manage complexity—especially in high-cost jurisdictions where labor constraints can dominate project economics.

“We’re applying what we’ve learned from projects over the years—we’re very strong around hydrocarbon processing and complex energy projects, including startupled development—to help future developers de-risk their approach,” Hassan says.

For companies entering the SAF space, Vista’s advice is straightforward. “Don’t shortcut feasibility,” Hassan adds. “Define your feedstock and offtake early, choose partners with execution experience, and design for real-world operating conditions— not lab science. It’s a technically exciting space with real potential, but you have to derisk early with disciplined execution and the right partners.”

vistaprojects.com

Owner’s Engineering Services

Independent Oversight | Trusted Guidance | Proven Value

Supporting Owner’s Teams with Confidence

Vista Projects provides independent owner’s engineering services to ensure your projects are delivered with quality, transparency, and efficiency. Acting as an extension of your team, Vista safeguards your interests through services including oversight of Engineering, Procurement and Construction (EPC) contractors, reviewing and validating designs, and ensuring best practices are applied throughout the project lifecycle. Achieve better project outcomes with Vista’s unique combination of technical experience and pragmatic execution approach.

• 40+ years of experience

• Over 1,400 projects

Oversight of EPC Contractors

• TIC exceeding $30B

Large, multi-discipline projects delivered through external EPC companies demand strong orchestration to maintain alignment and sound decisions. As the Owner’s Engineer, Vista deploys experienced leaders who drive teams, extract value, and keep execution practical. We unify technical, schedule, and commercial oversight into a single control point, validating deliverables, progress, and costs against benchmarks to limit scope growth, manage risk, and reinforce accountability.

Value Improvement Program (VIP)

Vista’s Value Improvement Program (VIP) applies structured, early-stage reviews to reduce total installed cost (TIC) while maintaining safety, quality, and operability. By identifying value opportunities early, VIP helps owners improve decisions, schedules, and execution certainty

VIP helps owners:

•Reduce TIC and operating costs to achieve positive final investment decisions (FID)

•Reduce construction phase risk

•Optimize schedules

Optimization focus areas:

•Execution and schedule strategies

•Modularization optimization

•Process simplification

• Plot plan refinement

On recent projects, VIP reviews have delivered TIC savings of 10-15%, ensuring owners capture maximum value from their capital investments.

Cost Assurance & Estimating Support

Backed by decades of cost estimating expertise, Vista ensures project budgets are realistic, traceable, and defendable. We integrate AACEi estimate classes into our reviews, providing owners with confidence at every project stage from conceptual screening to late-stage validation.

ACCELERATING INNOVATION

In the Pacific Northwest, a new coalition has mobilized to accelerate sustainable aviation fuel production, confronting the challenges shaping this emerging industry.

By Katie Schroeder

The Cascadia region, also known as the Pacific Northwest, covers thousands of miles of forests, mountains and cities, from northern California to the Alaskan Panhandle, ranging from the coastline of the Pacific Ocean in the West to Montana in the East. Isolated geographically from the rest of the United States, local communities have built pipeline infrastructure independent from the network of pipes that serve the rest of the country. In the middle of this region is the state of Washington; its economy entwined with aerospace companies and global corporations such as Amazon and Microsoft.

The aerospace industry plays a significant role in the state’s economy, generating $71 billion in revenue for its businesses,

according to the Association of Washington Businesses. Capitalizing on the region’s localized fuel infrastructure and a strong aviation industry, the Cascadia Sustainable Aviation Accelerator launched in January 2026, planning to drive the adoption of sustainable aviation fuel (SAF) in Washington and throughout the Pacific Northwest. “We have a unique opportunity in the region we call Cascadia, to really take advantage of some of the uniqueness of our region. We’re completely cut off from the rest of the supply chain for fuel products that travel through the network of pipelines that crisscross the nation and supply refining operations, and so we have to produce what we use here,” says Tim Zenk, managing director of Earth Finance and an early founder of CSAA.

The Cascadia Sustainable Aviation Accelerator aims to produce 1 billion gallons of SAF by 2030. One of its members, Alaska Airlines, serves more than 140 destinations across North America, Central America, Asia and the Pacific, according to the airline’s website. IMAGE: ALASKA AIRLINES

Local Impact

The coalition seeks to drive SAF development and adoption forward with the ultimate goal of producing 1 billion gallons of SAF in the region by 2035. As the home of aviation giant Boeing and the nation’s first state SAF tax credit, CSAA will leverage local aviation interests to increase local SAF capacity, reduced technological uncertainty, more regional economic value and improved air quality.

A group of Washington state’s deep bench of aviation expertise, fuel refining experience, sustainability goals and corporate interests inspired the creation of CSAA. The Port of Seattle, Snohomish County, Alaska Airlines, Boeing, Washington State University, Microsoft, Earth Finance and Amazon all played a role in the coalition’s creation. “We brought this idea to leadership of the companies who are aboard, which is Boeing, Amazon and Washington State [University] and were able to convince the legislature to invest $10 million ... and the legislature was matched by a family office, philanthropic contribution of another $10 million,” Zenk says.

Headquartered in Seattle since the 1960s, Alaska Airlines is well established in the state, according to Ryan Spies, managing director of sustainability for Alaska Airlines. “We really feel integrated into the state, more than any airline certainly, and obviously also having Boeing up the street,” Spies says. “We have a tremendous partnership with the premier aerospace developer in the world. They call Seattle ‘Jet City,’ and we’re happy to be a part of that."

Boeing manufactures its airplanes in Snohomish County, and 65,024 of its 181,984 employees live in the state as of December 2025. According to Ryan Faucett, vice president of sustainability partnerships with Boeing, SAF plays a critical role in the company’s decarbonization strategy. SAF’s emission profile is compelling: The base model used by the aircraft industry estimates that 30% to 70% of emissions reductions will come from SAF alone, according to Faucett. The company joined CSAA to contribute its technical expertise, policy guidance and aviation leadership.

Besides being home to Boeing, another factor that upped Washington’s appeal to serve as the organization’s headquarters was the state’s SAF production incentives, Zenk explains. The SAF tax credit, which came into effect in 2023, stands at $1 per gallon of SAF with a minimum of 50% carbon intensity reduction, increasing by two cents for each percentage point CI reduction above 50%, reaching a max potential total of $2 per gallon.

Now, CSAA aims to educate, equip and enable increased SAF production throughout the Pacific Northwest. Earth Finance estimates that spending on SAF projects will have a return on investment 14 times over the initial amount. The region is the fifth-largest refining center in the U.S., and Zenk believes that the refiners are the “fastest path” to bringing fuels such as SAF there.

Most of Pacific Northwest’s liquid fuels—including gasoline, diesel and jet fuel—are supplied via the 400-mile Olympic Pipe -

line, which runs from Whatcom County in northern Washington to Portland, Oregon. “The realities of the infrastructure that we have to deal with today means that we need to figure out a way to be self-sufficient as a region,” Spies says. “I think the other piece is just the concentration of high technology organizations that have an interest in and charge to address climate. We are in a region where people care about this and understand the realities of the challenges ahead.”

Supporting SAF adoption also entails de-risking the permitting process for SAF producers and enhancing feedstock access. Spies also identifies Washington’s permitting process as one area in need of improvement, because currently, for new products and new producers, the process is challenging to navigate. “Reducing those technical barriers to [leverage] our own feedstocks is really critical for woody materials, waste agriculture, RNG and all the other sources of carbon that we think are potentially economically viable, but require some technical work,” Zenk adds.

Industry Intent

Airlines and manufacturers are pursuing sustainability as a next chapter of aviation innovation. As airlines pursue net-zero emissions goals and more sustainable operations, they are working within a narrow profit margin, Spies explains. According to data from the Bureau of Transportation statistics released in 2025, net income margins systemwide in 2024 stood at 2.7%.

These margins make fuel cost a critical factor in finding a suitable, low-carbon replacement for conventional jet fuel. Spies

Boeing supports the aviation industry’s goal of reaching net zero by 2050, according to Ryan Faucett, vice president of sustainability partnerships. Because SAF plays an important role in meeting that goal, Boeing takes leadership in catalyzing SAF scaling, he adds.

Partnerships

explains that Alaska Airlines follows a five-part sustainability plan. The first step is to maximize operation efficiency, utilizing each drop of fuel as effectively as possible. The second area for consideration is the airplane fleet, retiring older planes and replacing them with new ones that are 15% to 25% more efficient. SAF is the third part of the plan and is especially important over the next 15 to 20 years, according to Spies. Alaska Airlines pursues new technologies and utilizes carbon offsets as the fourth and fifth components of the company’s sustainability strategy.

“SAF is a drop-in fuel, so that means we don’t have to change planes or how planes operate to use it,” he says. “We don’t have to change traditional fueling infrastructure to use it, which are all highly capital intensive things, and so if we can avoid having to change those, SAF is a really great option.”

Boeing also sees SAF’s value as a near-term carbon reduction opportunity that doesn’t require changing aircraft design or airport infrastructure, Faucett explains. It’s unlikely that airplanes powered by electricity or hydrogen will be available for widespread use before 2050—especially not for long-haul flights.

Technical Innovation

CSAA partner Washington State University drives innovation forward through research. Josh Heyne serves as the director of the Bioproducts Sciences and Engineering Lab at WSU Tricities and co-director of the WSU PNNL Bioproducts Institute. As the Federal Aviation Administration’s official prescreening lab, Heyne and his team assess fuel samples from SAF innovators around the world, testing each one for the qualities critical to airplane engine operability. The tests examine “the ability of a fuel to maintain combustion or burn in an engine, and the ability to ignite or relight under kind of extreme thermodynamic conditions at altitude,” Heyne says.

Based on the results, he and his team provide feedback to the companies, educating them on how to best move forward. This insight includes identification of the areas that would likely

prevent a sample from being certified by ASTM and as a viable jet fuel.

Because many of the fuels sent to the lab are in early stages of development with limited volumes available, the 36 pieces of equipment used there were selected due to their ability to get results with only a small sample, and all function to help new technologies develop. For those unmeasurable data points that require larger samples, Heyne and his team develop predictions based on the chemical composition of the fuel. “Our lab has developed the ability to take pretty detailed chemical compositions and predict properties that there are not enough volume of to measure,” Heyne says. “We call that tier alpha within the group for prescreening, and we’re able to predict other properties that we don’t have enough volume to measure.”

Due to the lab’s work with the National Jet Fuels Combustion Program, lab staff are able to extrapolate how the qualities observed in the samples would behave in an airplane and impact the jet engine. One such consideration is the assessing the potential of a “flame blowout,” which occurs in the air when a pilot pulls back the thrust at altitude and the flame goes out. Fuel sensitivity is connected to this occurrence, Heyne explains. In such a scenario, the pilot will reignite the engine, so the ability of the fuel to relight when at altitude is critical.

“Fuel properties are really important in terms of how easy it is to ignite a fuel in an engine,” he says. “So that ... is what we’ve really specialized with historically, and being able to provide that type of information to producers has been valuable.”

According to Heyne, the prescreening works as a step toward a key issue for the SAF industry: fungibility, meaning the creation of 100% drop-in SAF. Faucett also discusses the importance of 100% drop-in fuel from the aircraft manufacturer perspective, expressing that Boeing is “excited” about moving beyond the current requirement capping SAF use at a 50% blend with conventional jet fuel. The creation of a 100% drop in SAF would eliminate the need for blending equipment and reduce the cost of using SAF. “We’re trying to do our part to understand

Posing for a photo during the launch event for the Cascadia Sustainable Aviation Accelerator at the Boeing Future of Flight in Mukilteo, Washington, on Jan. 8, are, from left: Bill McSherry, vice president of state and local government operations at Boeing; Guy Palumbo, director of public policy at Amazon; Joe Nguyễn, director of the Washington State Department of Commerce; Elizabeth Cantwell, president of Washington State University; Bob Ferguson, Washington governor; Dave Somers, Snohomish County executive; Marko Liias, Washington state senator; Tim Zenk, managing director at Earth Finance and board vice chair of the Cascadia Sustainable Aviation Accelerator; Ryan Spies, managing director of sustainability at Alaska Airlines; and Mia Gregerson, Washington state representative. IMAGE: CSAA

from a R&D and supply chain perspective, what it takes to use higher blends of SAF,” he says.

Though there are many steps between the current reality and 1 billion gallons of SAF, Heyne sees an opportunity to rise to the challenge. “This is a developing market,” he says, “and Washington has many of the key attributes to accelerate that market and push it forward into something bigger, not only for the state but globally as well.”

Finding Feedstock

The forests of the Cascadian region potentially offer a lowcarbon feedstock for SAF production due to the volume of waste residues available. Zenk explains that the sheer degree of wood waste available could be comparable to the Midwest’s ethanolto-jet opportunity. Earth Finance estimates that the supply of woody biomass could be enough to make 6 billion gallons of SAF each year. Alongside woody biomass, the agricultural commodities that flow through the state could also serve as a plentiful feedstock source.

Spies calls the feedstock obstacle SAF’s “big question,” one that CSAA plans to address by doing a feedstock assessment for the region. Currently, any and all feedstocks are under consideration, but “at some point we’ll need to make bets,” he says. Assessing feedstocks helps the industry determine what will work at the scale needed to make billions of gallons of SAF in future.

Several projects are underway across the region, using a variety of feedstocks. Currently under development in Washington is SkyNRG’s Project Wigeon, located in eastern Washington at the Port of Walla Walla’s Wallula Gap Industrial Business Park. SkyNRG intends to produce 50 MMgy of SAF from syngas. In Oregon, NXTClean Fuels is in the process of developing an SAF and renewable diesel facility on the Columbia River, which would produce up to 50,000 barrels of clean fuel per day. The facility intends to use waste oils and greases as its feedstock.

Both Zenk and Heyne point to the positivity surrounding CSAA’s efforts as something that excites them regarding the future of SAF in Cascadia. “I think Washington really does have a phenomenal ecosystem in this space right now,” Heyne adds.

“And I don’t see anything but a continuation of the development of that ecosystem and the support systems for new producers looking at the state. So, I have a ton of optimism about it here in Washington.”

Author: Katie Schroeder Associate Editor, SAF Magazine katie.schroeder@bbiinternational.com

A NEW CHAPTER IN Farm-Driven Biofuels

John Deere is emerging as a quiet catalyst in the bioenergy transition, expanding equipment compatibility, data tools and policy engagement to help farmers connect their crops to growing markets for biodiesel, renewable diesel and sustainable aviation fuel.

By Keith Loria

Biofuels continue to expand beyond road transportation into sectors such as aviation, marine, industrial and power markets, with original equipment manufacturers emerging as influential and often underreported players in the biomass value chain.

Among them is John Deere, a global manufacturer of agricultural equipment and engine systems serving farmers worldwide, which is taking a more visible role in shaping how farmers participate in renewable fuel markets, from biodiesel and ethanol to emerging sustainable aviation fuel (SAF) pathways.

Through expanded equipment approvals, fuel-flexible engine development, digital data platforms and deeper policy engagement, the company is positioning itself as both a technology provider and a market signaler in the bioenergy transition.

The B30 Decision

In fall 2025, John Deere announced approval of B30 biodiesel across its entire Tier 4 engine portfolio, which marked a significant step beyond its previous B20 guidance. Josh Garetson, director of renewable fuels and corporate strategy at John Deere, says the decision was about more

than technical confidence—it was about strengthening demand for the crops farmers grow and reinforcing the circular nature of modern agriculture. “At the time, it was a good move. It was probably pushing the envelope a little bit from where certain policy was,” Garetson says. “We started thinking about what more we could be doing to help customers with sustainability.”

Internal discussions led the company to engage with fuel providers and trade associations while evaluating how biodiesel standards and product quality had evolved. “We worked through how the standards have improved and how product quality has improved, and that got us comfortable saying, ‘Hey, we think this is going to work,’” Garetson says.

Beyond technical validation, the move was designed to reinforce the “farm gate” value proposition. “This is an opportunity to help with the farm gate, which is really the most important part of this,” Garetson says. “We are committed to supporting and growing the use of renewable fuels in our equipment, and renewable fuels play a critical role in supporting the agriculture economy.”

By approving B30, John Deere is allowing customers the option to leverage higher biodiesel blends in their own operations,

John Deere approved B30 biodiesel use across its entire Tier 4 engine lineup in 2025, marking a significant expansion beyond its previous B20 guidance.

IMAGE: JOHN DEERE

especially those who grow renewable fuel feedstocks.

All Tier 4 engines are now approved for B30, with earlier Tier 3 and lower-tier engines approved up to B100 biodiesel, and all engines capable of running RD100 renewable diesel. What’s more, John Deere’s spark-ignition turf and utility equipment is approved for E10, and the company is exploring higher ethanol blends, including a concept 9.0L engine designed to operate on E98.

For farmers operating heavy equipment, B30 approval means the blend can be used in Tier 4 engines without equipment modification, provided fuel quality and storage best practices are followed. Garetson notes John Deere’s confidence stems from improved biodiesel standards and product quality over the past decade. At the same time, he stresses that adoption requires attention to tank cleanliness, seasonal considerations and coordination with fuel suppliers.

Market Signals and Biomass Demand

While off-road biodiesel utilization remains relatively modest, the company views equipment approvals as a catalyst for incremental adoption. “We think it’s probably not a very high level of utilization in off-road applications today,” Garetson says. “We’re hoping to move that up and get a few more people interested in B30.”

Following the B30 announcement at the 2025 Farm Progress Show, Garetson notes that the industry took notice. “We

were having conversations with fuel distributors not long after that,” he says. “It was a positive shock to the system.”

That reaction underscores a central thesis: OEM approvals function as market signals. When a major manufacturer validates higher blends, fuel distributors, blenders and infrastructure providers reassess product offerings and investment plans.

Greater compatibility can, over time, support stronger demand for feedstocks such as soybean oil, corn oil and animal fats, which are all critical inputs for biodiesel and renewable diesel, as well as increasingly for SAF.

Garetson also points to John Deere’s willingness to demonstrate real-world success. This spring, the company plans to work with farmers using B30 to establish best practices and dispel persistent myths. “We want to help tell their story of what they need to do to be successful and how challenging it was,” he says. “That farmer-to-farmer storytelling is vital for broader adoption.”

Policy, Platforms and the SAF Connection

John Deere’s engagement extends beyond engine approvals into policy advocacy and digital infrastructure. The company has supported renewable fuels policy for decades, dating back to the early 2000s. Today, it is seeking a more visible seat at the table.

“We recognize how important it is to the industry and to our customers,” Garetson says. He cites support for measures

such as E15 expansion and acknowledges the importance of robust renewable volume obligations (RVOs). Weak RVOs in recent years, he notes, strained biodiesel economics. “Supportive policy is really important in making sure there’s a good economic foundation,” he says.

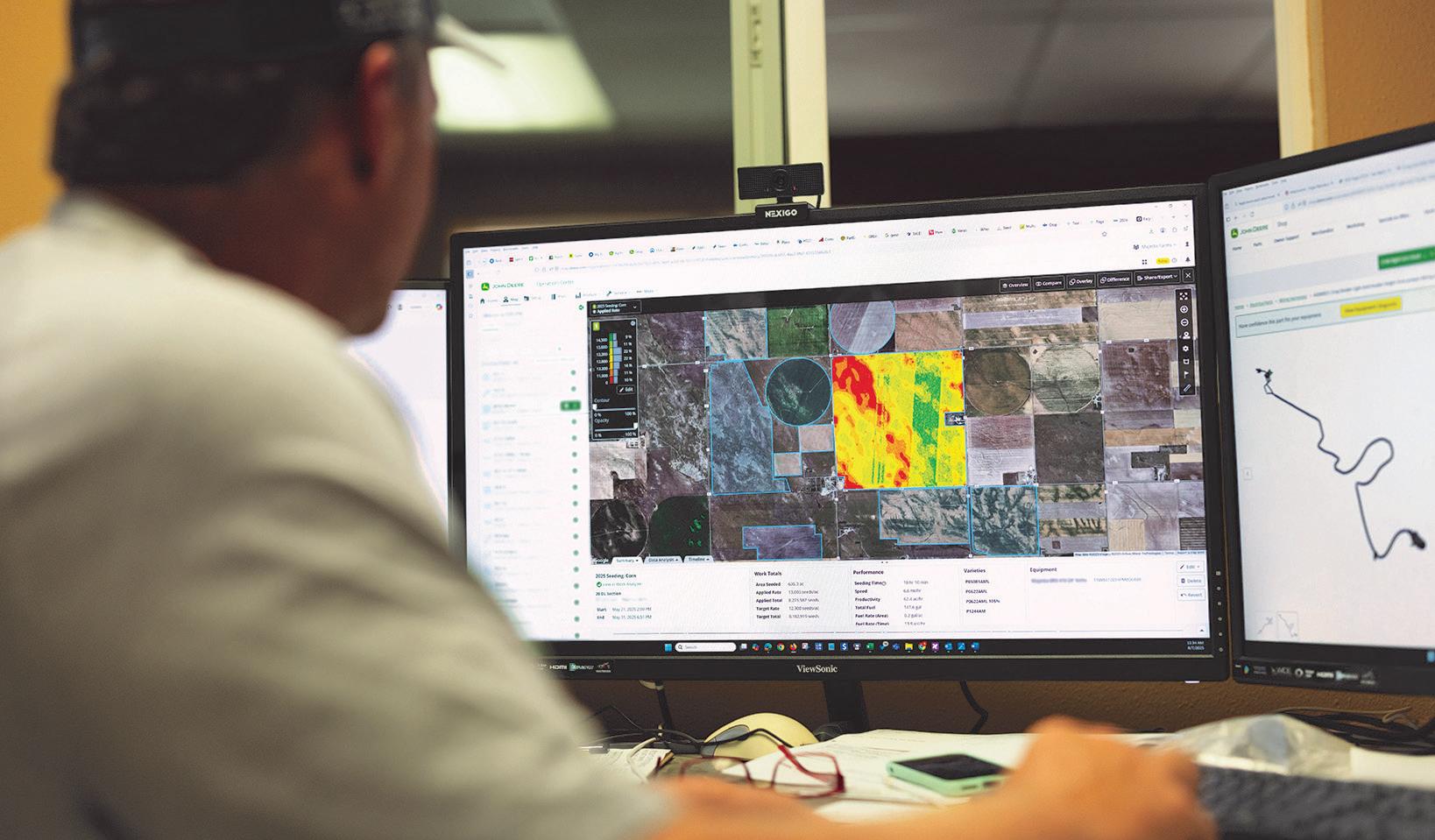

Beyond policy, John Deere sees data as a bridge between farm practices and downstream fuel markets. Its Operations Center platform allows farmers to document field activities, enabling efficiency gains and potentially facilitating participation in low-carbon fuel incentives.

As tax credits such as 45Z (successor to 45C/45Z discussions in renewable fuel production) emphasize carbon intensity, Garetson notes documentation will be critical. “Operations Center is a platform that’s going to enable that data sharing in a very streamlined, cost-effective way,” he says.

For SAF, this is especially relevant. As aviation fuels increasingly depend on low-carbon feedstocks, growers who can document reduced carbon intensity may gain access to premium markets. John Deere’s role, then, is not just in engine compatibility, but in enabling traceability and carbon accounting at scale.

The Sustainability Mindset

Renewable fuels also intersect with John Deere’s Scope 3 emissions strategy. In its updated sustainability ambitions, the company reaffirmed its commitment to reducing value-chain emissions.

From the company’s perspective, however, Scope 3 is inseparable from farmer economics. “It’s really about the value proposition to the farmer,” Garetson says. “Where renewable fuels help growers lower carbon intensity scores and potentially capture higher crop values, we aim to provide compatible solutions.”

Fuel represents a varying share of carbon intensity depending on geography and cropping systems. For U.S. corn and soybean producers, fuel may be a smaller slice of total emissions compared to fertilizer or land use. Still, renewable fuels provide a tangible pathway to improvement, especially as carbon markets and SAF demand evolve.

John Deere positions renewable fuels alongside precision agriculture as com-

Field performance data and crop variability can be viewed through John Deere’s digital platform, Operations Center, illustrating how precision agriculture tools can document farm practices and support participation in low-carbon fuel and sustainable aviation fuel supply chains.

IMAGE: JOHN DEERE

plementary tools. After all, precision technologies reduce input use and improve efficiency, while biofuels create circular economic loops.

Garetson describes a “flywheel” effect: Stable renewable fuel policy supports crop prices, strengthening farm economics and enabling reinvestment in advanced practices.

Addressing Misconceptions

Despite progress, misconceptions linger. Early biodiesel experiences are often linked to inconsistent quality and storage challenges, and have left some operators wary. “Product quality has improved quite a bit,” Garetson says, “but lingering memories of past issues persist.”

John Deere’s educational efforts emphasize proper storage and handling. Biodiesel interacts differently with metal than petroleum diesel, making tank cleanliness critical. “If the tank doesn’t have the right level of cleanliness, that’s where problems can arise,” he says. “Temperature considerations also matter. High bio -

diesel blends may be less suitable in extremely cold conditions, underscoring the importance of working closely with fuel providers to select appropriate blends seasonally.”

In the near term, knowledge-sharing is a primary barrier. “Approving and announcing the ability to use B30 is kind of lighting the fuse, but we can’t just walk away,” Garetson says. “Farmer-to-farmer engagement will be key to scaling confidence.”

Looking Ahead

Electrification remains part of John Deere’s long-term portfolio, but Garetson acknowledges practical constraints. At high horsepower levels, batteries alone may not be feasible due to size and weight limitations. In those segments, liquid fuels such as diesel, biodiesel, renewable diesel and potentially high-ethanol blends remain central.

The company’s concept E98 tractor reflects its broader philosophy as it provides options that align with customer ap -

plications. In regions with strong ethanol production, the ability to deliver corn to a plant and bring ethanol back to the farm creates an appealing circularity story.

Whether the fuel is biodiesel, renewable diesel, ethanol, SAF or synthetic aviation fuel, Garetson believes multiple pathways will coexist. “Those are all fuel sources that are going to have places in the market,” he says.

John Deere’s objective therefore is to help farmers remain integral players in that evolving landscape. By aligning equipment compatibility, digital platforms, sustainability goals and policy advocacy, the company is signaling that OEM decisions can shape biomass demand and emissions outcomes far beyond the field.

Author: Keith Loria Contributing Writer, SAF Magazine

Shared Skies, Shared Seas

Commonalities and Competition for Marine Biofuels and SAF

Technological pathways, feedstocks and refining infrastructure are linking sustainable aviation fuel and marine biofuels as both sectors compete for limited lipid and waste-based resources, policy support and market priority.

By George Hale

The aviation and maritime industries have both set ambitious decarbonization goals for the coming decades, and their growing reliance on fuels derived from biological feedstocks is bringing new overlap— and potential competition—into focus. As aviation works to meet future targets, its interactions with the maritime sector are becoming more apparent. Despite key differences, both industries depend on energy-dense liquid fuels to move people and goods over long distances, making biofuels such as SAF, biodiesel and ethanol natural options. Still, questions remain about whether sufficient biofuel production capacity and feedstock supply will be available to meet the needs of either sector, even as differing technologies and fuel requirements may allow both to progress without direct conflict.

In the past, these sectors have been treated as separate markets, but aviation and maritime industry demands for vast amounts of feedstock raises concerns about who would get access to these resources. Market pressures and policy demands will likely influence competition and prioritization; however, critical differences between the two industries and innovations in biofuel production have the potential to shape biofuel markets over the next one to two decades.

The Quest for Decarbonization

‘Innovation has made ethanol production quite efficient, and I’m optimistic costs will come down for biojet, too.’

Jack Saddler, professor of bioenergy and biofuels, University of British Columbia.

Growing concern over carbon emissions and climate change has motivated the aviation and maritime industries to set ambitious emissions reduction goals. The International Civil Aviation Organization set a goal of reducing aviation’s carbon emissions by 5% by 2030 and reaching net-zero carbon emissions by 2050. Similarly, the International Maritime Organization established a set of regulations to reduce greenhouse gas emissions from ships known as the IMO Net-Zero Framework. The most viable way to meet these goals is through the large-scale adoption of biofuels like SAF for aviation and biodiesel, sustainable diesel, and other options like methanol or ammonia for shipping.

On-road biofuels like biodiesel, sustainable diesel and ethanol set the stage for biofuel adoption starting in the early 2000s. On-road fuels today consist of a blend of petroleum-based and biomass-derived fuels. For example, most of the gasoline sold in the United States contains around 10% ethanol. “In the U.S., we use ethanol made from corn, while Brazil uses sugar,” says Jonathan Lewis, Director of Transportation Decarbonization at the Clean Air Task Force, an organization focused on technological and policy-based solutions to carbon emissions. “That market has mostly plateaued.”

There is now a growing emphasis on using biofuels for long-distance transport like aviation and shipping. However, unlike light-duty on-road vehicles, aircraft and ships are highly optimized for long-distance travel and have certain design and operation constraints that control the use of alternative fuel sources.

Same But Different

One potential cause for conflict between aviation and shipping when it comes to biofuel is that both industries have specific fuel requirements. Both aircraft and ships must be able to travel long distances without refueling, but have limited space for fuel. The use of batteries would be impractical for any sort of long-distance travel, either at sea or in the air, because of space, weight and energy capacity. Any fuel source has to be energy dense and compatible with existing equipment, meaning that hydrogen is also not useful for shipping or long-distance flying, though batteries and hydrogen could have a place in short-distance applications. “Hydrogen is great on an energy-per-mass basis, but it’s horrible on an energy-per-volume basis,” says Steve Csonka, executive director of the Commercial Aviation Alternative Fuels Initiative. “Volume requirements in an airplane turn into drag and weight so you’d have to significantly restrict the range on new aircraft.”

Supply and Demand

As we close in on decarbonization target dates set by the IMO and ICAO, the growth in biofuel demand is becoming obvious. Independent advisory organization DNV projected that by 2050, the maritime industry will have an energy demand of up to nearly twice the current global level of biofuel production. Aviation is expected to have an even higher demand for biofuels.

On the supply side, in a 2022 report, the International Energy Agency says that the global supply of biofuel could triple between 2021 and 2030. However, this increase is not enough to meet aviation’s demands for biofuel by 2030, and the picture is even less favorable by 2050. “Even with a threefold increase, we’ll only have enough to meet half of the aviation sector’s energy demand,” Lewis says.

At the same time, biofuels cost more than petroleum-based fuel. Estimates from the low-carbon fuels consortium BC-SMART show that SAF, sometimes also referred to as biojet, is currently two to three times more expensive than conventional jet fuel. Policies that nudge SAF production—like those used to get ethanol production going in the early 2000s—may be needed. “Innovation has made ethanol production quite efficient,” says Jack Saddler, professor of bioenergy and biofuels at the University of British Columbia. “And I’m optimistic costs will come down for biojet, too.”

SAF can be made from a variety of feedstocks that include starches like corn and sugarcane and lipid feedstocks like soybeans, animal fat or waste oils and grease. However, lipid feedstocks are an area where biofuels for planes and ships can come into conflict.

“There’s a natural tug back and forth for a producer to ask whether it’s more profitable to produce biodiesel or if they should go after SAF production,” Csonka says.

Markets

Profitability will come down to policy choices and market forces. Specifically, an industry’s willingness to pay more for a resource will determine how feedstocks get used. And with fewer fuel options available, the aviation industry will likely be willing to pay far more. Fortunately, the maritime industry can turn to energy sources other than biofuels. “One of the main punchlines of our research is that the marine sector has a variety of different fuel options,” Saddler says.

Multiple Choice

One option some are turning to is natural gas. While natural gas is a fossil fuel, it has a slightly lower carbon intensity than fuel oil and is better from an emissions perspective. Other options that shipping companies are looking into include bio-liquid natural gas, which is derived from renewable natural gas, as well as methanol. Green methanol can be made using biogenic feedstocks like wood waste or by combining hydrogen from water with carbon dioxide collected from the air. However, these processes are expensive and require lots of electricity, while the least expensive way to make methanol relies on fossil fuels, Saddler says.

As with aviation, hydrogen is another possible fuel source; however, the maritime industry runs into similar issues with energy density that make hydrogen less appealing as a long-range fuel. Another possible fuel source that is attracting atten-

tion in the maritime world is ammonia. An ammonia molecule contains no carbon, so burning it produces no carbon dioxide. “The best option for shipping, as far as we can tell, is ammonia,” Lewis says.

Ammonia can’t be used as a drop-in fuel, but marine engines can be modified to use it, and it is easier and cheaper to store than hydrogen. However, ammonia is less energy dense than fuel oil, so ships would need larger storage tanks. Ports would also need to upgrade infrastructure to handle ammonia fueling. Lastly, ammonia is toxic, meaning that ships would need additional safety measures. But since the maritime industry has transported ammonia as cargo for decades, there are already safe-handling procedures in place, and ammonia tankers would be good candidates for large-scale trials of ammonia as a marine fuel.

Everything Changes

The lower energy density of ammonia, while a challenge for shipping, would be a deal breaker for aviation due to tighter constraints on weight and volume. Aviation also needs a direct replacement for fossil-based jet fuel, as engines can’t be easily modified to run on ammonia. At the same time, airports would have a far harder time adding ammonia fueling infrastructure than ports, and the safety risks the fuel poses make it a nonstarter for aviation.

“We have issues around physical asphyxiation in the event of a tank leak, which is why we’re not enamored with ammonia,” Csonka says.

Despite recent advances in SAF production and potential breakthroughs with ammonia, the aviation and maritime industries are still at the mercy of supply and demand. What the industries need are more feedstocks and innovative strategies like the use of wood and agricultural waste as feedstocks. Additionally, more intensive production of biofuel feedstocks raises questions about land use changes that increase the overall carbon intensity of the finished product and concerns about diverting food crops to fuel production.

This last concern is what has driven the European Union to pursue what they refer to as fuels of nonbiological origin. Instead of using biogenic feedstocks like corn or soy to make biofuel, European producers take carbon captured from the air and hydrogen produced through electrolysis of water and stitch those molecules together to make fuel. This process requires a lot of energy, but if done with renewable electricity sources, it can make sustainable fuels. However, fuels made this way are even more expensive than those made with biological feedstocks. Additionally, it is possible that renewable electricity will be more useful for powering air conditioning and other parts of modern life than for making jet fuel.

“We’re talking about adding a factor of two or three times more,” Saddler says. “That’s why they’ve put a mandate in place.”

The United Kingdom in late 2025 signaled it may be softening its stance on crop-based SAF, with the government gathering stakeholder input that could provide a pathway to open the country’s SAF mandate program to crop-based biofuels.

Looking Ahead

While the aviation and maritime industries can no longer be seen as completely separate markets, they aren’t necessarily in direct competition for fuels to meet their decarbonization targets. With smart policies, continued development of new technologies to make methanol, ammonia, SAF and other fuels could lead to lowered costs. If done right, developing a so-called bioeconomy could drive reduced emissions, improve rural economies and address farming sustainability issues. “Growing a bioeconomy lowers prices for every product produced from those resources,” Csonka says.

Achieving net-zero carbon emissions in shipping and aviation will take a nuanced approach that looks at interactions between industries and an assortment of solutions. This will involve closer looks at technology, land use, feedstock production and distribution networks for different types of fuel.

“Every approach has pluses and minuses,” Saddler adds. “There is no silver bullet.”

Author: George Hale SAF Magazine Contributing Writer

SAF’s Next Flight: Aligning Scale, Policy and Climate Impact

- By Veronica Bradley

Sustainable aviation fuel (SAF) is transitioning from aspiration to implementation, a shift that was on full display during a recent session at the Clean Fuels Conference held in Orlando in January. Leaders from across the aviation and clean fuels value chain examined how production realities, infrastructure constraints and evolving policy frameworks are shaping SAF’s next phase of deployment.

Aviation’s decarbonization challenge is daunting. Fuel is the second-largest operating cost for airlines after labor, and aircraft are long-lived assets, often remaining in service for 25 to 30 years. While each new generation of aircraft delivers meaningful efficiency gains, wholesale changes in propulsion technology will take decades to penetrate the fleet. As a result, low-carbon, drop-in fuels remain the only realistic pathway for achieving near- and midterm emissions reductions at scale.

At the same time, aviation demand continues to grow. Global jet fuel consumption totals roughly 100 billion gallons annually and is increasing at 1.5% to 2% percent per year, according to Sean Newsum, managing director of environmental affairs at Airlines for America. Even with efficiency improvements, demand is projected to reach 130 billion to 150 billion gallons by midcentury as the global fleet expands. As Newsum emphasized during the conference discussion, this growth underscores the urgency of scaling SAF alongside—rather than in opposition to—industry demand.

SAF is not a recent experiment. The aviation sector has spent decades developing and certifying alternative fuels, beginning with the first commercial biofuels flight in 2008. Since then, the industry has embraced a technology- and feedstock-neutral ap-

proach, recognizing that long-term emissions reductions will require a portfolio of pathways optimized for lifecycle performance, regional feedstock availability and infrastructure compatibility. Newsum said this framework supports aviation’s commitment to net-zero carbon emissions by 2050.

Scaling Supply While Maintaining Integrity

Conference panelists highlighted that U.S. SAF production is expanding from a small but meaningful base. In early 2024, domestic capacity stood at approximately 84,000 gallons per day from two facilities. By the end of the year, new and expanded operations brought total production capacity to roughly 1.6 million gallons per day.

This growth has broader implications across the clean fuels ecosystem, noted Tom Michels, director of government affairs at United Airlines. As some facilities reallocate capacity from renewable diesel to SAF, biodiesel production is backfilling displaced volumes, reinforcing demand across agricultural and feedstock supply chains. From a systems perspective, Michels says these shifts highlight the interconnected nature of clean fuel markets and the importance of policies that account for economy-wide emissions outcomes.

While hydroprocessed esters and fatty acids pathways dominate current volumes, emerging technologies such as ethanolto-jet are nearing commercial production. Continued investment in next-generation pathways remains essential to diversify feedstocks, manage long-term costs and reduce carbon intensity. However, moving from demonstration to commercial scale re-

(From left) Sean Newsum, Airlines for America; Tom Michels, United Airlines; Tim Pohle, Beveridge & Diamond; and Michael AuBuchon, Saffron Consulting

PHOTO: CLEAN FUELS ALLIANCE AMERICA

mains a critical hurdle, requiring confidence in both policy durability and market demand.

Affordability, Reliability and Demand Signals

Affordability, not immediate price parity, will determine SAF adoption, explained Michael AuBuchon, president of Saffron Consulting and former managing director of fuel strategy and management for Southwest Airlines. Producers are increasingly expected to demonstrate a credible path toward cost reduction over time, recognizing that scale is essential for meaningful emissions reductions.

Operational reliability is equally important. SAF must be blended with conventional jet fuel and transported, often by rail, to airports that may lack dedicated infrastructure. As production expands geographically, logistics planning becomes a core component of environmental performance, ensuring that emission reductions achieved at the production stage are preserved through delivery and use.

AuBuchon said corporate customers are also shaping the market. Sustainability commitments increasingly require SAF purchases to meet specific environmental criteria, particularly in the European Union and the United Kingdom. These requirements are driving greater scrutiny of feedstocks, certification pathways and lifecycle analysis from logistics customers and business travelers. There is a growing openness to agricultural feedstocks such as corn and soy, once largely absent from aviation discussions, as stakeholders balance sustainability goals with the need for scale and availability.

Policy Certainty and Infrastructure Challenges

Policy design remains central to SAF’s trajectory. While incentive-based approaches have played a key role in building the U.S. biofuels industry, SAF transactions today rely on stacking multiple mechanisms, including federal and state incentives, corporate con-

tributions and airline premiums. Long-term policy certainty is essential for attracting the capital required to build and operate SAF facilities.

Mandates were discussed as one potential tool to provide demand certainty, particularly for investors evaluating older infrastructure. However, international experience illustrates that mandate design matters. When obligations fall on fuel suppliers rather than producers, value may be captured without incentivizing new capacity or improving environmental outcomes. Well-structured incentives can directly support production, innovation and emissions performance.

Panelists also identified infrastructure as an emerging bottleneck. Storage capacity, blending requirements and pipeline access vary widely by region, and regulatory frameworks have not always kept pace with SAF’s unique characteristics. In some cases, rules intended to reduce emissions risk actually constrain the fuels needed to achieve those reductions. Addressing these challenges will require continued engagement with regulators grounded in technical understanding and data-driven analysis.

Looking Ahead

The Clean Fuels Conference discussion made clear that SAF has moved beyond proof of conept. Production is scaling, demand signals are strengthening and policy tools are beginning to align. However, the industry remains in an early stage, where careful attention to lifecycle emissions, logistics and long-term policy certainty will determine success.

For SAF to fully deliver on its promise, growth must be both rapid and responsible. Striking that balance between scale and integrity will define the next chapter of aviation’s decarbonization journey.

Author: Veronica Bradley Director of Environmental Science

Clean Fuels Alliance America

Onsite Carbon Capture and Storage: A Strategic Path for Ethanol Producers to Access the SAF Market

- By Sylvain Riba

For ethanol producers, the key to unlocking sustainable aviation fuel (SAF) eligibility and premium pricing lies in lowering carbon intensity (CI) scores. Airlines and refiners are pursuing SAF to meet decarbonization targets, and California’s Low Carbon Fuel Standard offers strong incentives for low-carbon fuels.

One of the most effective strategies is onsite or nearby carbon capture and storage (CCS)—a solution that leverages ethanol’s unique advantage: a high-purity CO2 stream from fermentation that can be dehydrated and compressed at relatively low cost and injected into suitable saline formations via Class VI wells.

This article explores the permitting, policy, incentives and practical steps for implementing CCS at ethanol facilities, drawing on Geostock Sandia’s experience and current U.S. regulatory frameworks.

Why CCS for Ethanol?

Capturing CO2 from ethanol fermentation is relatively straightforward because the gas stream is already high in purity. Lifecycle modeling shows that CCS can significantly reduce ethanol CI, enabling compliance with SAF requirements and California LCFS. Projects like Blue Flint Ethanol in North Dakota demonstrate feasibility, capturing and injecting more than 200,000 metric tons of CO2 annually into deep saline formations.

Onsite CCS is ideal where geology supports injection, such as the Arbuckle Formation in Kansas or Broom Creek in North Dakota. Where local geology is unsuitable, producers can rail or truck CO2 to a nearby storage hub if it is economically feasible.

Regulatory Framework: UIC Class VI and MRV

CCS projects in the United States require a Class VI permit under the U.S. Environmental Protection Agency’s Underground Injection Control program, in effect since the 1970s. These wells are specifically designed for geologic CO2 sequestration and must meet stringent standards to ensure underground sources of drinking water aquifers are preserved and that no induced seismicity will occur.

The process begins with site characterization, which includes a detailed assessment of geology, sealing formations and any legacy wells that could affect containment. Operators must also perform Area of Review (AoR) modeling to predict the movement of the CO2 plume and pressure front over time.

Well construction is subject to rigorous integrity testing to ensure safe injection and long-term containment. Continuous monitoring, verification and accounting is required throughout the life of the project to track injection performance and detect any anomalies. In addition, operators must demonstrate financial

An Illinois ethanol producer engaged Geostock Sandia in the winter of 2025 to drill a 4,500-foot stratigraphic test well as part of a carbon capture and storage project. PHOTO: GEOSTOCK SANDIA

responsibility and prepare for post-injection care, which includes monitoring after injection ceases and eventual site closure.

EPA permitting timelines typically range from 18 to 24 months, although states with Class VI primacy—such as North Dakota, Wyoming, Louisiana and Texas—may process applications more quickly. Beyond the Class VI permit, operators must also submit a an MVA plan to the EPA for greenhouse gas reporting. This plan ensures transparent accounting of injected CO2 volumes and is essential for claiming federal incentives like the 45Q tax credit for carbon capture and storage or utilization.

Economic Drivers

The financial case for CCS is strong because multiple incentives can be combined along the value chain that far exceeds the cost to sequester CO2 onsite.

First, the federal 45Q tax credit provides $85 per ton of CO2 permanently stored in geologic formations, creating a direct revenue stream from the captured emissions. In addition, California’s LCFS rewards low-CI ethanol, generating credits that can be sold in the LCFS market.

Beyond these programs, ethanol that qualifies for conversion into SAF earns a premium price and 45Z Clean Fuel Production Tax Credits per gallon, reflecting its compliance with stringent lifecycle greenhouse gas reduction requirements and low CI. It is important to note, however, that the 45Z and 45Q tax credits cannot be stacked for the same facility.