BUYING YOUR HOME WITH THE

Bonnie Smith Group

Theresa Adams REALTOR®

Kathryn Gilbert REALTOR®

Haley Lenker Operations Manager

Bonnie Smith Team Lead & REALTOR®

Specializing in North Atlanta Real Estate, the Bonnie Smith Group is a top producing team with Atlanta Fine Homes Sotheby’s International Realty.

As a fourth-generation Atlanta native, team leader Bonnie Smith possesses a wealth of market knowledge and local expertise. Bonnie’s data-driven, highly optimized approach to industry research, trends, pricing, marketing and negotiation sets her apart and delivers stellar results for her clients. Years of experience, along with the group’s guiding principles of passion and integrity make for a winning combination for their clients. Having a dedicated team of professionals in place to help execute and manage all the moving parts creates a seamless experience for our clients.

No. 1

Volume Sold, Small Team North Atlanta, 2023 & 2024

Top 5%

Atlanta REALTORS® Association Units Sold & Volume 2016-2024

Top Performing

Real Estate Agents

The $20+ Million Club, 2025 The Atlantan Magazine

No. 3

Volume Sold, Small Team Company-wide, 2024

All Stars

Atlanta Magazine Real Estate All Stars 2021-2025

RealTrends

Verified Top 1.5% Team Nationwide Sales & Volume 2025

Certified Pricing Strategy Advisor (PSA)

Best of North Atlanta

Appen Media

Best REALTOR® Runner-Up, 2024 & 2025

Best Real Estate Team Runner-Up, 2025

Real Estate Awards

Best OTP Team, 2025

Modern Luxury Interiors Magazine

Member

of National Association of REALTORS®

Georgia Association of REALTORS® & Atlanta REALTORS® Association

Luxury Home Specialist (ALHS)

Our Areas of Expertise

Who better than the team led by a 4th Generation Atlantan to help you find the perfect area for you and your family to call home.

ALPHARETTA - Alpharetta is now Georgia’s 12th most populous city, and boasts some of the best schools in the United States.

BROOKHAVEN - Located in Dekalb County and known for its tree-lined Old Atlanta residential streets.

CANTON - Offers exciting and new possibilities for growth within an authentic, inviting community.

CUMMING - It is a community bustling with vibrant life while remaining rich in history and tradition.

DUNWOODY - As a northern suburb of Atlanta, Dunwoody was incorporated as a city on December 1, 2008.

EAST COBB - Located between Marietta and Roswell and is in an unincorporated area.

JOHNS CREEK - They purchased land along McGinnis Ferry Road and Medlock Bridge Road to develop a secondary Technology Park campus.

MILTON/CRABAPPLE - The City of Milton was incorporated in 2006, and borne of the unincorporated northernmost part of northern Fulton County.

PEACHTREE CORNERS - Conveniently located on major highways I-85, I-285, and GA 400 and just 30 minutes northeast of Atlanta. Founded on July 1, 2012.

ROSWELL - The City of Roswell is in north Fulton County and is Georgia’s eighth-largest city.

SANDY SPRINGS - With big-city excitement just minutes away, and the great restaurants, shopping, arts facilities, and strong public school system.

WOODSTOCK - Woodstock is a bustling suburb of Atlanta, and its downtown has recently experienced wonderful revitalization.

Roswell

Dunwoody

Marietta

Chastain Park

Chamblee

Smyrna

Mableton

Kennesaw

Duluth

Brookhaven

Vinings

Tucker

Midtown

Decatur

Acworth

Sandy Springs

Lithia Springs Douglasville

Druid Hills Westside

Woodstock

Holly Springs

Canton

Johns Creek

Alpharetta

Cumming

Buford

Ball Ground

Snellville

Stone Mountain

Suwanee Milton

Buckhead

Norcross

Kennesaw

Lake Allatoona

Lake Lanier

Greater Atlanta

ABOUT ATLANTA

You may know Atlanta as the unofficial capital of the South, but there is more to this city than its southern location.

As you make your home in the Peach City, you will find an undeniable mix of Southern charm, urban sophistication and deeply rooted traditions.

There are intriguing destinations to explore at every turn, from the trendy boutiques and Craftsman-style bungalows of Virginia-Highland and Decatur to the theater and museum district and historic Piedmont Park in Midtown. From the charming town squares of Roswell, Alpharetta, Norcross and Acworth to the shores of Lake Lanier, Atlanta truly has something for everyone.

Atlanta is also home to 16 Fortune 500 companies, including The Home Depot, United Parcel Service (UPS), The Coca-Cola Company and Delta Airlines. Atlanta was known and envied for its access to several rail lines in its earliest days as a city.

Atlanta continues its reputation as a transportation hub with the Hartsfield-Jackson Atlanta International Airport — the world’s busiest airport — along with convenient access to I-75, I-85 and rail lines.

A PREMIER LOCATION FOR PROFESSIONALS AND FAMILIES

The Metro Atlanta region is home to over 5.2 million people and nearly 150,000 businesses, offering a top-tier quality of life for those who choose to create their destiny here. From its diverse economy, global access, abundant talent and low costs of business and lifestyle, Metro Atlanta is a great place to call “home.” Residents have easy access to arts, culture, sports and nightlife, and can experience all four seasons, with mild winters that rarely require a snow shovel.

In addition to our business-friendly environment, Metro Atlanta also offers many activities to foster personal and family growth, including:

• Public parks with green space and trees

• Jogging trails and sports facilities

• World-class museums, theaters and cultural venues

• Internationally recognized restaurants and shopping

THE ADVANCING ECONOMY

Throughout the Atlanta area, various counties are making strides to improve their economic conditions, which in turn is benefiting the Atlanta community as a whole. From business expansions and job creation to new initiatives and prospective projects, these counties — Cherokee, Cobb, DeKalb, Gwinnett, Forsyth and Fulton — exemplify some positive economic changes in Atlanta.

LITTLE - KNOWN FACTS ABOUT ATLANTA

• The city was first named Terminus, then Marthasville.

• General William T. Sherman’s capture of the city during the Civil War in 1864 got Abraham Lincoln re-elected as president. Joseph Johnston, the Confederate general who fought against Sherman in Atlanta, later served as a pallbearer at Sherman’s funeral, where Johnston caught pneumonia and died a short time later.

• Al Capone did time in the federal prison here.

• Babe Ruth hit his final home run for the Braves — No. 714 was the last of three that Ruth hit that afternoon in an 11-7 Boston Braves loss to the Pirates. It was at Forbes Field in Pittsburgh.

• We are one of few cities with three interstate highways running through it.

• The Georgia State Capitol in Atlanta is gilded with pure gold leaf from the site of America’s first gold rush in Dahlonega, Georgia.

What to Expect at Our Initial Consultation

An initial meeting is crucial to understand your homebuying needs and develop a strategy to help you successfully make a purchase.

ASSESSING YOUR NEEDS + PRIORITIES

• “Top 10” Exercise: Clarify your most important wants and needs.

• Discuss your purchase time frame and any past buying experiences.

• Review your financing/pre-approval status, if applicable.

• Talk through your communication style and decision-making preferences.

UNDERSTANDING THE MARKET

• Current market conditions, inventory, and pricing trends.

• How your goals align with what’s available.

• What to expect in terms of competition and timing.

MAPPING OUT THE PROCESS

• Step-by-step overview of the buying journey.

• What happens after today, and how we’ll move forward.

• Defining roles, responsibilities, and expectations.

STRUCTURING YOUR PURCHASE

• Exploring how you’ll buy: financing, cash, or contingent sale.

• Understanding risk tolerance and negotiation strategies.

• Ensuring your investment is well-protected.

The Mortgage Pre-Approval Process

GETTING PRE-APPROVED

At the beginning of the home-buying process, you need to consider how you will finance the purchase. Knowing how much you will be able to borrow before you start looking at homes is essential. It is the basis upon which you can determine the feasibility of buying a particular home and will allow me to show you only the homes in your price range. It will also place you in a much stronger negotiating position.

You can address this part of the home-buying process by getting pre-qualified or pre-approved. While these terms sound the same, they have some important differences.

PRE-QUALIFICATION

Pre-qualification is a non-binding estimate of your ability to borrow based on informal questions about your income, job stability, credit history and current monthly expenditures. As an experienced real estate professional, I will refer you to lenders offering these informal preliminary services. There are no fees involved. Your loan approval may not be guaranteed, and you are not obligated to choose the services of the lender who pre-qualifies you. Pre-qualification will allow me to tell prospective sellers that your chances of loan approval are good when a formal application is made. This will be to your advantage when you negotiate for the home, as the seller can be reasonably assured you will qualify. Remember, however, that your loan is not guaranteed. Pre-qualification is based on the accuracy of the information you provide to the lender.

PRE-APPROVAL

Pre-approval goes one step further as it represents a formal loan commitment. Most lenders offer pre-approval. It allows the homebuyer to process the loan application while shopping for a home. Two to three weeks may be needed for pre-approval, depending on the documentation required for your situation. Most lenders will charge a fee with the understanding that the money will be applied to your closing costs when approved. The fee is nonrefundable if you choose a different lender for your loan. Once the loan is approved, the lender will issue a formal credit approval in writing up to a specified dollar amount. With this written approval in hand, your bargaining position will be greatly enhanced when making an offer. Sellers will be motivated because you are a qualified buyer who can close in a very short period of time.

For a Cash Purchase

REQUEST FOR PROOF OF FUNDS VERIFICATION

Please provide this document to your financial advisor so they can prepare an official letter verifying your available funds. This letter may be required by sellers or listing agents before you can tour a home or submit an offer. In competitive markets, it’s best to have this verification ready before beginning your home search.

THE PROOF OF FUNDS LETTER SHOULD INCLUDE:

• Date (updated monthly to reflect current balances)

• Buyer’s name

• Financial advisor’s name and contact information

• Available balance(s)

MOST RECENT BANK STATEMENT

• Last 4 digits of the account(s) used for verification

• Type of account(s)

• Name of the financial institution(s)

• Financial advisor’s signature

Please also include the most recent bank statement for the referenced accounts that includes the buyer’s name, with all account numbers blacked out except for the last 4 digits (a screenshot is okay).

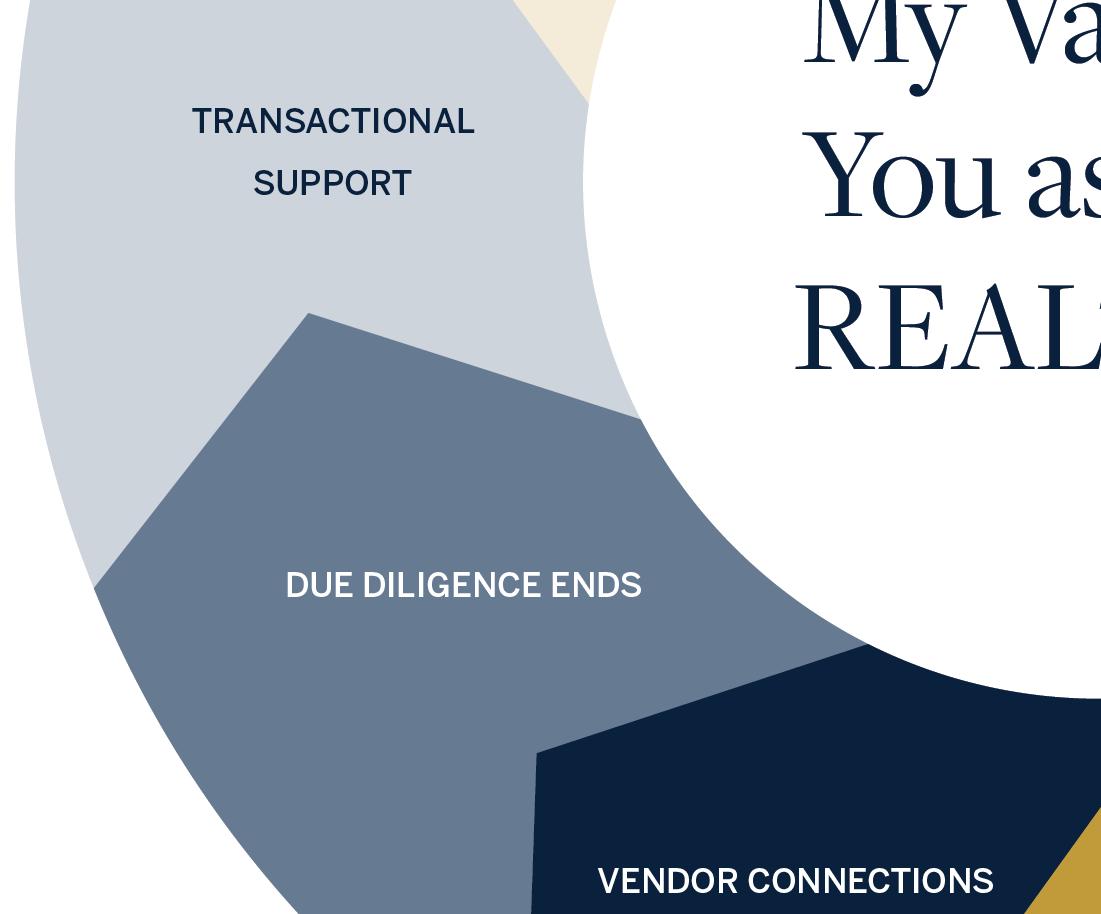

Finding Your New Home

LOCATING AND VIEWING PROPERTIES

We are continually previewing properties and staying attuned to local market trends to guide you in finding the right home. The Bonnie Smith Group will also:

• Set up automated listing alerts that meet your search criteria

• Reach out to specific neighborhoods of interest via customized mailers and/or agent network

• Network with other top North Atlanta agents across brokerages

• Present off-market or pre-market listings as they arise

• Communicate with agents to schedule and set up private showings

• Map out and tour properties together

• Recommend properties that are available to view at open houses

• Provide monthly Market Reports

• Review the pros and cons of each home after viewing

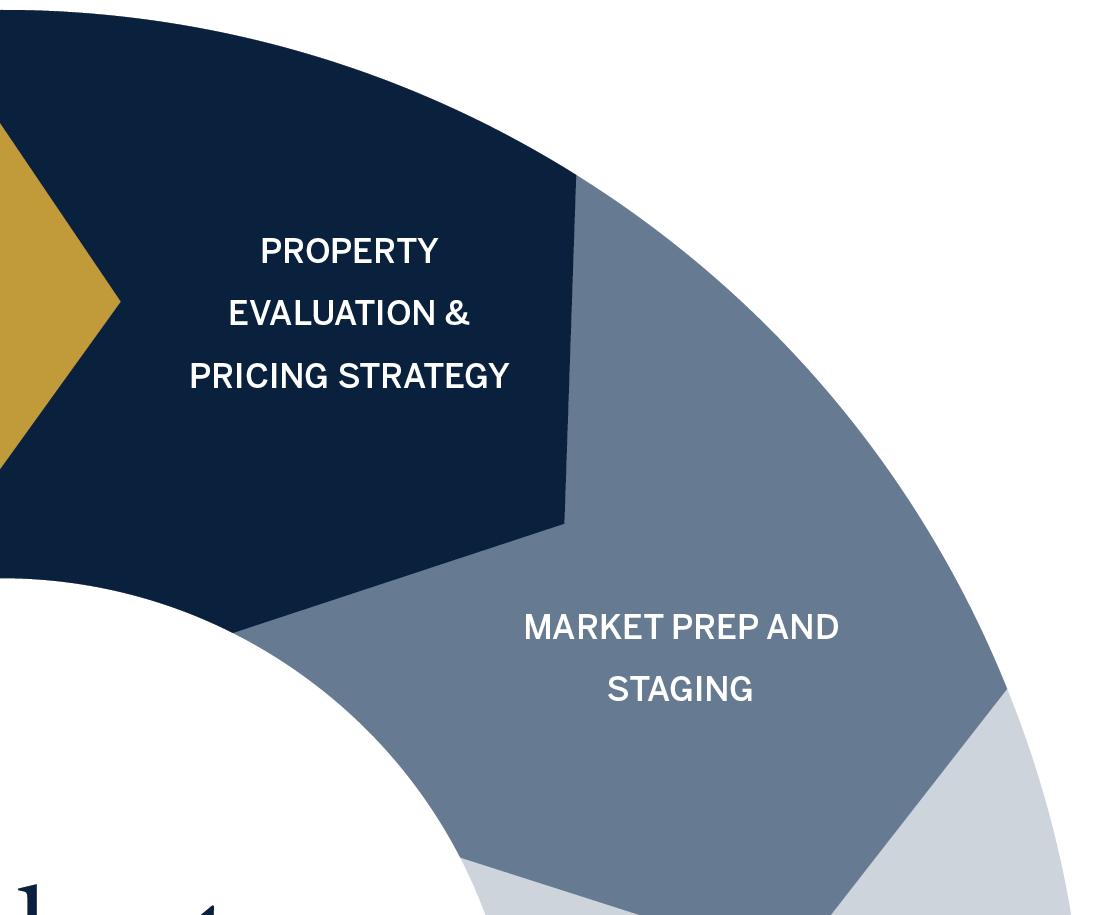

EVALUATING SELECTED PROPERTIES

We will help you assess how your selected property compares to others on the market and to homes recently sold. A benefit of having us as your trusted real estate advisor at Atlanta Fine Homes Sotheby’s International Realty is our familiarity with required disclosures, inspection recommendations and experience reviewing reports.

We will also:

• Request and review the disclosure package and any additional information from the listing agent

• Advise on additional inspections and guide you in determining the appropriate time frame for contingencies

• Assist in reviewing covenants, by-laws, budgets and insurability if the home is in a HOA or condominium

The Funnel Process

Finding your new home is a process of narrowing down options - from many possibilities to the one that’s just right for you.

How it works:

• We’ll start wide: Exploring listings from every source — MLS, online portals, drive-bys, internal listings, FSBOs, expireds, and more.

• We’ll narrow together: Some homes we’ll look at online, some we’ll drive by and some we’ll tour in person. You’ll always be in control of which homes make the cut.

• We’ll identify favorites: Our goal is to narrow to your Top Three Favorites. I’ll prepare a market analysis on each so you can make an informed decision.

• We’ll protect your investment: I’ll ensure you don’t overpay and that your purchase aligns with your goals.

Viewed

The Contract Process

GLOSSARY OF TERMS

APPRAISALS: The Purchase and Sale Agreement does not contain a preprinted appraisal contingency. However, most lenders will only offer the buyer a loan if the property appraises for the contract price. The buyer and seller may choose to renegotiate to the lesser appraised value. Where a buyer has added an appraisal contingency to the special stipulations, the disposition of the contract will follow the terms of contingency.

BINDING AGREEMENT:

A binding contract is created when one party presents a signed written offer to purchase or sell property to a second party and that party accepts the same request in writing and delivers written acceptance back to the offering party before the time limit in the offer expires. In the GAR Purchase and Sale Agreement, the date the parties reach mutual agreement is referred to as the acceptance date, and the date the offering party receives the written notice of acceptance is referred to as the binding agreement date. The party receiving the written notice of acceptance is responsible for notifying the other party of the binding agreement date. Once the binding agreement date is established, all timerestricted obligations begin the following day.

CLOSING DATE AND POSSESSION:

The Purchase and Sale Agreement provides that the closing shall be on a specific date or such earlier date as agreed to in writing by both parties. It also states that both parties agree that should the loan be unable to be closed on the proposed date or that the seller fails to satisfy title, either party, upon written notice provided before the agreed-upon closing date, can extend the contract closing date up to seven days. The parties agree that the buyer will allow the seller to retain possession through closing, through X number of hours after closing or within X number of days after closing.

DUE DILIGENCE PERIOD:

In the current Purchase and Sale Agreement, the inspection occurs during due diligence. The buyer has an agreed-upon amount of time from the binding agreement date to conduct any evaluations, inspections, appraisals, examinations, surveys or testing at the buyer’s sole expense during this period.

The buyer may terminate the agreement during this time for any reason and receive a refund of their earnest money (1.5%5%). In order to terminate the agreement, the buyer must give written notice to the seller prior to the end of the due diligence period. However, the buyer may want to proceed after the inspection. If so, the buyer may give the seller an amendment to address concerns (i.e., repairs) with the property, which can then be negotiated between the buyer and seller. Once that is done and the due diligence period has expired, the buyer must proceed with the sale.

EARNEST

MONEY

DEPOSIT:

The earnest money or “good faith” money that accompanies the Purchase and Sale Agreement or offer is typically one percent to five percent of the sales price (this amount may be negotiated). A secure link will be sent to you with wiring instructions or ACH deposit instructions for the selling broker’s escrow account within five banking days of reaching the Binding Agreement Date. It is always a good business practice for you to verbally verify wiring instructions with the recipient. The Purchase and Sale Agreement does state that if the buyer breaches any of the buyer’s obligations or warranties under the contract, the holder or seller may have the right to retain earnest money as liquidated damages.

PURCHASE

AND SALE AGREEMENT: The document that creates a valid, enforceable contract between a buyer and seller in Georgia is called a Purchase and Sale Agreement. This contract has been created and preapproved by attorneys and the Georgia Association of REALTORS® (GAR). It includes but is not limited to terms related to the legal description of the property, purchase price, buyer’s intended loan terms, buyer’s earnest money (1.5%-5%), closing date and possession, inspection and agency.

SAMPLE BUYER FORMS

Scan the QR code to view samples of the following:

• Exclusive Buyer Brokerage Engagement Agreement

• Purchase and Sale Agreement

• Broker Compensation Agreement

Purchase Offer Terms Outline

This document outlines the terms that are to be included in the Purchase & Sale Agreement submitted to the seller as your official offer. Below you will find guidelines simply for reference as to what we are typically seeing in today’s market. You must evaluate the risks and benefits with the terms and make the best offer that you feel comfortable making,

PROPERTY ADDRESS

LIST PRICE

PURCHASE PRICE

CLOSING ATTORNEY

CLOSING COSTS PAID BY SELLER

CLOSING DATE

typically 30 days for conventional loan or 45 days for jumbo loan

POSSESSION DATE & TIME same as closing date unless seller wants temporary occupancy

EARNEST MONEY

EARNEST MONEY TIMING

OPTION MONEY

DUE DILIGENCE PERIOD

TIME LIMIT OF OFFER

COMMON EXHIBITS

• Legal Description

• Seller’s Property Disclosures

• Conventional Loan Exhibit or All Cash Sale with No Financing Contingency

Typically 24 hours

• Community Association Disclosures

• Temporary Occupancy

• Buyer’s Pre-approval Letter or Proof of Funds

Buying New Construction

Purchasing a newly built home can be an exciting opportunity — but it’s important to understand how to protect yourself throughout the process.

CHOOSING THE RIGHT BUILDER

The salesperson in a builder’s office represents the builder, not the buyer. Their contracts are written to favor the builder, and each one is different. Working with your own agent ensures someone is looking out for your best interests, helping you evaluate the contract terms, potential risks, and issues such as price changes during construction. In most cases, builders cover the buyer’s agent commission, either in full or in part

LOT RELEASES

Because of supply chain challenges, many builders release homesites in phases. Make sure you understand the release schedule and how the selection process works. Some builders require buyers to be pre-approved through their preferred lender before making an offer, while others invite multiple buyers to submit their highest and best bids. Knowing these rules ahead of time will increase your chances of securing the lot you want.

DESIGN OPTIONS

Material shortages have limited design flexibility with some builders, who now offer homes with preset packages instead of fully customizable finishes. If selections are available, buyers usually make them before construction begins. The further along the build, the fewer changes are possible — cabinetry, for example, is often ordered by the framing stage. Exterior elevations are usually locked in at the time a community is approved, meaning they cannot be changed until after the neighborhood transitions to HOA control (if permitted by the covenants).

DEPOSITS AND UPGRADES

Earnest money for resale homes is typically 1–2% of the purchase price. New construction usually requires a larger deposit — often around 5% — and builders also ask for a percentage of design selections (about 25%) to be paid upfront. If a buyer cancels the contract or defaults, these funds are usually non-refundable. It’s essential to be certain about your purchase before signing.

FINANCING

Builders often offer closing cost assistance or incentives when buyers use their preferred lender, though the loan terms may not always be the most competitive. In some cases, interest rates are locked for a set period after closing (six to 24 months), preventing immediate refinancing. Buyers are typically required to complete a loan application with the builder’s lender to confirm qualification, but it’s always wise to compare rates and incentives with outside lenders.

TIMELINE

Construction timelines vary. A custom home may take six to eight months for permitting and an additional six to 12 months to complete. Larger planned communities built by national builders often move faster. Always ask for an estimated build time so you know what to expect.

DURING CONSTRUCTION

Visit the property regularly to ensure work aligns with your contract. Many buyers hire an independent inspector at key phases — especially before drywall and again before closing. While builders aren’t obligated to address outside inspection findings, most will correct issues related to code compliance. Testing for radon is also recommended, as builder responsibilities differ widely regarding remediation.

WARRANTIES

Builder warranties vary but often include coverage such as: one year for cosmetic items and appliances, five years for HVAC, and 10 years for major structural components. Cosmetic repairs (like nail pops or drywall cracks) are typically offered once, near the end of the first year, after the home has settled. Be sure you understand what is covered and how to file a claim.

BUYER BEWARE

New construction homes can be exciting, and it is enticing knowing you are the original owner. Before getting caught up in the new home smell, educate yourself and know that Georgia is a buyer beware state. It is a buyer’s responsibility to research the home they are purchasing and evaluate the risk factors.

The Inspection Process

WHY SHOULD I INSPECT?

According to the Purchase and Sale Agreement, you can have the home inspected by a professional inspector during the due diligence period outlined in the contract. You can avoid, or at least anticipate, costly repairs to structural or mechanical systems by having an inspection. The sales contract specifies when the inspection will occur after the offer is accepted and that closing is contingent upon satisfactory inspection. Inspection costs can be as low as $350 or as much as $1,000, depending on the size of the home.

SPECIAL NOTE: If you are purchasing a stucco home, inspect the condition of the stucco further. The cost is approximately $600 – $1,500 depending on the size of the home for this separate inspection.

USE A PROFESSIONAL INSPECTOR

The inspection requires specific technical skills. You may be familiar with common problems, but a professional home inspector can give you a better overview of the entire structure of a home and its potential problems. We strongly encourage you to accompany the inspector who examines your house. They can point out potential issues and help you locate special devices, such as the items listed below:

• On/off switch on furnace, air conditioner, etc.

• Pilot light on water heater, oven, etc.

• Fuse box

• Main water shut-off controls

• Plumbing and electrical systems

• Heating, ventilation, air conditioning systems

• Septic tank, well or sewer line

FREQUENTLY ASKED QUESTIONS

WHAT IS A HOME INSPECTION?

A home inspection is a visual inspection of the structure and components of a home to find items that are not performing correctly, items that are unsafe and items that violate the code at the time the house was built or remodeling occurred. If a defect or a symptom of a defect is found, the home inspector will include a description of the defect in a written report and may recommend further evaluation.

WHY IS A HOME INSPECTION IMPORTANT?

Emotion often affects the buyer and makes it hard to imagine any problem with their new home. A buyer needs a home inspection to find out all the possible problems with the house before purchasing the home.

WHAT SHOULD I EXPECT FROM A HOME INSPECTION?

A home inspection is not protection against future failures. Stuff happens! Components like air conditioners and heating systems can and will break down. A home inspection tells you the condition of the component at the time of the inspection. For protection from future failure, consider a home warranty. A home inspection is not an appraisal that determines the value of a home. Nor will a home inspector tell you if you should buy this home or what to pay for it.

WHAT DOES A HOME INSPECTION INCLUDE?

A home inspector’s report will review the condition of the home’s heating system, central air conditioning system (temperature permitting), interior plumbing and electrical systems, the roof, attic and visible insulation, walls, ceilings, floors, windows and doors, the foundation, basement and visible structure. Many inspectors will also offer additional services not included in a typical home inspection such as mold, radon and water testing.

SHOULD I ATTEND THE HOME INSPECTION?

It is recommended to be there so the home inspector can explain their findings in person and answer any questions about the home you may have. This is an excellent way to learn about your new home, even if no problems are found. But be sure to give the home inspector time and space to concentrate and focus so they can do the best job possible for you. It is always recommended that the home inspector be given a copy of the seller’s property disclosure and the Georgia wood infestation report before their inspection. It will assist them in their evaluation of the home.

WHAT IF THE REPORT REVEALS PROBLEMS?

All homes (even new construction) have problems. Every problem has a solution. Solutions vary from a simple fix of the component to an adjustment of the purchase price. A home inspection allows the problems to be addressed before the sale closes.

CAN I ASK THE SELLER TO MAKE REPAIRS?

The due diligence paragraph allows the buyer to amend the seller to “address concerns” with the property, which would be repaired. The buyer gives this amendment to the seller, and the parties can negotiate a satisfactory solution to the areas of concern. Inspections after the due diligence period are for the buyer’s informational purpose only and cannot be used as a means to terminate the contract.

WHAT TYPE OF REPORT CAN I EXPECT TO RECEIVE?

A home inspection should include a report that describes what was inspected and the condition of each inspected item. The best reports are created using home inspection software that includes color pictures and comments specific to your home. Inspectors using home inspection software can often deliver the report on-site or via the Internet for quicker delivery.

WHAT CRITERIA SHOULD I USE TO CHOOSE A HOME INSPECTOR?

The state of Georgia now requires inspectors to be licensed. Your home inspector should be a member of a professional home inspection organization. The inspector must abide by standard practices and a code of ethics that require professionalism in the industry. National home inspector organizations like the American Society of Home Inspectors (ASHI), National Association of Certified Home Inspectors (NACHI) and National Association of Home Inspectors (NAHI) require their members to adhere to strict standards of practice and attend continuing education.

WHAT IS THE LEAST EXPENSIVE? INSPECTORS ALL LOOK AT THE SAME THINGS, RIGHT?

Every inspector is different and comes with strong points and weak points. You may save money by choosing a cheaper inspector; they could miss some problems. Usually, the best inspectors are not the cheapest. A thorough and experienced inspector is the best route to take.

INSPECTION FORM MECHANICAL SYSTEMS

INTERIOR SPACES

HEATING WALLS, CEILING AND FLOORS

Age, Condition and Operation of Main System(s):

Thermostat(s): Room-by-Room Heating:

Overall Condition: Water Stains: Cracks: Settlement: Decay:

COOLING BASEMENT

Age, Condition and Operation of Main System(s):

Thermostat(s): Room-by-Room Heating:

Walls: Floors:

Water Penetration: Other:

ELECTRICAL KITCHEN

Adequacy of Service: Light Switches: Door Bells: Exterior Lighting:

PLUMBING

Overall (Water Pressure): Water Heater(s): Other:

WASTE (SEWER OR SEPTIC)

Flush Toilets:

Consult Owner(s) on Condition: Obtain Service Records:

APPLIANCES

Range:

Oven: Dishwasher: Exhaust Fan: Other:

Compactor: Disposal: Microwave: Refrigerator:

Cabinets: Countertops: Other:

BATHROOMS

Toilet(s): Shower(s): Tub(s): Tile:

GARAGE

Door(s): Door Opener(s): Floor(s): Walls:

EXTERIOR CONDITIONS

Roof: Siding: Windows/Doors: Steps and Stairs: Decks/Porches:

Pool and Accessories: Sprinkler: Landscaping: Drainage: Other:

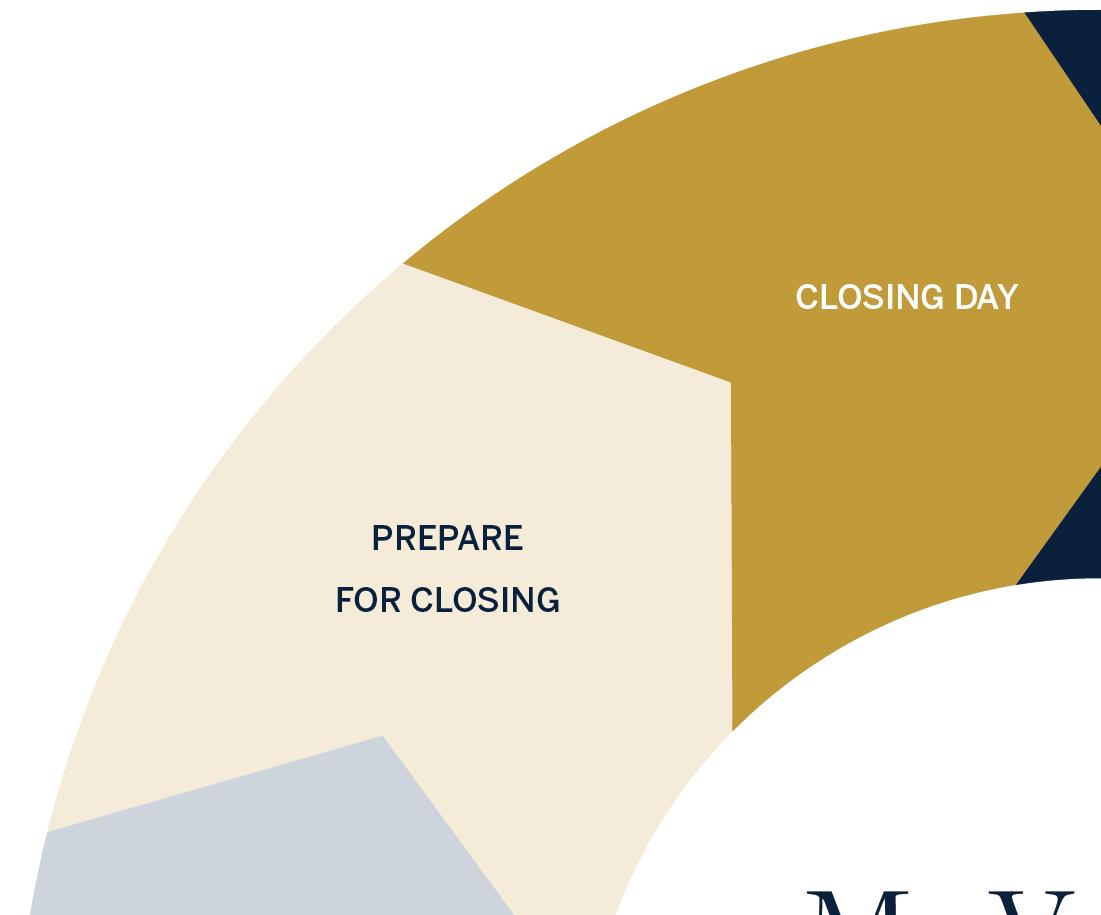

The Closing Process

REPRESENTATION

Residential real estate closings are handled in several ways among the various states. In some states, title companies manage the process; escrow companies manage the process in others. In Georgia, most closings occur with the assistance of an attorney who specializes in real estate transactions.

Regardless of whether a choice is permitted, the attorney represents only the lender. Because of ethical considerations due to a possible conflict of interest among the various parties to a closing, an attorney representing the lender should not represent any other party to the closing. Therefore, if the borrower desires representation, independent counsel should be obtained. Of course, if a lender is not involved in financing the transaction, the purchaser will select an attorney to represent their interest.

FUNCTIONS OF A CLOSING ATTORNEY

An attorney selected after the signing of the contract of sale to handle the closing customarily will examine the title to the property, prepare the sale and loan closing documents, conduct the closing, arrange for the recording of the closing documents, issue the lender’s and, if desired, owner’s title insurance, and disburse the lender’s and/or purchaser’s funds.

CLOSING COSTS

Initially, payment of and limitations on the amount of closing costs are determined by the contract of sale. If a lender finances the transaction, the purchaser will be responsible for negotiating the precise amount of the closing costs. Most lenders will be subject to specific federal regulations governing disclosure of a “good faith estimate” of settlement charges to be given to the borrower within three business days following loan applications. To prevent unpleasant surprises at closing, the purchaser should become familiar with and understand the limitations of such an estimate. If a purchaser requires more precise figures, it should be requested at the time of loan application since the good faith estimate is the limit of federal requirements. Closing costs are collected at the time of closing, usually by payment of a net purchase figure, which includes the purchaser’s equity, the closing costs, prorations and other adjustments. For tax purposes, the lender must usually approve payment of discount points in advance with a separate check. Closing costs do not include escrows for property taxes and insurance. Furthermore, closing costs quoted by a lender usually do not include the cost of an owner’s title insurance policy.

OWNER’S TITLE INSURANCE

Owner’s Title Insurance is designed to insure the owner against loss suffered because of claims made against the title to the property. The policy typically insures against matters that were not or could not have been discovered by a proper title examination of the property, subject to specific exceptions to coverage detailed in the policy. As with all types of insurance, deciding to purchase is only part of the job; determining, for example, whether certain exceptions to coverage are acceptable or by the contract of sale takes additional consideration, and an attorney’s advice may be helpful in such a decision. A new survey is highly recommended. Without a current survey, the homeowner’s title insurance policy contains an exception for all survey matters so that the risk of financial loss due to survey problems rests solely with the buyer who opts not to purchase a survey at closing.

PROPERTY SURVEY

Whenever there is a period of rising interest rates, mortgage lenders search for ways to keep down the costs of obtaining a home loan. Some lenders no longer require homebuyers who borrow money to purchase a home to get a survey. Obtaining a survey is for the buyer’s protection. Buyers who do not obtain a survey may discover too late that their decision was “penny-wise and pound foolish.” A survey is the process of evaluating land to locate boundaries and other features. The surveyor draws a map to communicate their findings. A typical residential survey will show boundary lines, the house’s location with respect to the boundaries, setback lines, easements, fences or any other encroachments relating to the property and a statement of whether the property lies in a floodplain. Depending on the lot size, a residential survey can cost between $350 - $1,000.

FREQUENTLY ASKED QUESTIONS

HOW SERIOUS WOULD A CLAIM AGAINST MY HOME BE TO ME PERSONALLY IF I DIDN’T HAVE OWNER’S TITLE INSURANCE?

It could be very serious. It would mean you would have to withstand all expenses involved with the defense of your rights and could even result in complete loss of your equity if your defense proved unsuccessful.

WHAT SHOULD I LOOK FOR IN SELECTING A COMPANY TO INSURE MY TITLE?

Look for financial strength, experience in all phases of title insurance and efficient and dependable service to policyholders.

WHAT TO BRING TO CLOSING

• Proof of homeowner’s insurance (check with your lender for details).

• Photo ID (driver’s license, passport).

• Power of attorney information, if applicable, prepared by the closing attorney. Check with your lender first for approval.

• Georgia law requires all funds over $5,000 to be sent directly to the closing attorney via wire.

The Moving Process

THE MOVING CHECKLIST

EIGHT WEEKS BEFORE MOVING

• Call several movers for estimates. Remember, on-site estimates are always more accurate.

• Be sure to get references from prospective movers.

• Once you’ve chosen your mover, discuss costs, packing, timing and insurance.

• Create a “move file” to store important information and collect receipts for moving-related expenses.

• Ask the Internal Revenue Service for information about tax deductions on moving expenses and what receipts you will need to keep.

SEVEN WEEKS BEFORE MOVING

• Prepare an inventory of everything you own. Divide this inventory into three separate categories: (1) items to be handled by the mover, (2) items to be handled by yourself and (3) items to be left behind.

• Stock certificates, wills and other one-of-a-kind items (jewelry, photos and home videos) are difficult or impossible to replace. Plan to carry them with you instead of packing them.

• Two good ways to eliminate unnecessary items are (1) hosting a garage sale or (2) donating to charities. These two techniques can help you to raise a little cash or serve as a tax deduction.

• Arrange for disposal of items not sold or donated.

• Contact your insurance agent to transfer property, fire, auto and medical insurance.

• Organize dental and medical records. Be sure to include prescriptions, eyeglass specifications and vaccination records.

• Inquire about changes in your auto licensing and insurance when moving. Notify your children’s school(s). Make arrangements for records to be forwarded to the new school district.

SIX WEEKS BEFORE MOVING

• Contact any clubs or organizations you are associated with for information on transferring, selling or ending your memberships.

• Start becoming acclimated to your new community. Familiarize yourself with your new shopping districts and the location of hospitals, police and fire departments. Contact the Chamber of Commerce or the Visitor’s Bureau to request any desired information on schools, parks and recreation, community calendars and maps.

FIVE WEEKS BEFORE MOVING

• Start including your children in the process. Make it exciting and fun by having your kids do some of their packing and labeling.

• If you plan to do any part of the packing, start collecting suitable containers and packing materials.

• If no longer required, cancel local deliveries.

• If you have pets, call your new township to determine if there are any specific requirements for pet ownership. In addition, transfer veterinarian records.

• Register your children in their new schools.

• Check specific medical forms required for Georgia schools that must be filled out.

FOUR WEEKS BEFORE MOVING

• If you are moving out of a multi-story building, contact building management to inquire about scheduling your move date and time. Certain buildings may have date and/or time restrictions on when moving can be done. Remember to keep this in mind when planning to move, especially if you are doing your packing. You can accumulate additional costs if you cannot finish packing by the move-in day and time allotted.

• Contact your moving company to schedule your move date. Changing your move date is always easier than rescheduling at the last minute.

• Visit USPS.com to fill out a change of address form. Notify magazine subscriptions, stocks, mutual funds, banks, credit card companies, newspapers, doctors, lawyers, accountants, REALTOR®, state and federal tax authorities, workplaces, schools, alma mater, voter registration offices and motor vehicle bureau of change of address. For anything mailed to you the month before you move, insert a change of address card with the effective date.

• Close any local charge accounts.

• Make airline and hotel reservations (if necessary).

• Notify insurance companies of your move. Transfer all insurance on your home and possessions.

• Contact utilities for disconnection or transfer (electric, gas, phone, cable, etc.). Be sure to have them still connected on a moving day. Please arrange to have them disconnected from your present home or schedule a last reading after your scheduled move-out.

THREE WEEKS BEFORE MOVING

• If necessary, arrange a babysitter to watch your children on moving day. You may need someone to keep your children occupied and ensure they remain safe during the busy loading process.

• While sorting through your belongings, remember to return library books and anything else you borrowed. Also, remember to collect all items being cleaned, stored or repaired (clothing, shoes, furs, watches, etc.).

TWO WEEKS BEFORE MOVING

• Call ahead to have utilities connected to your new home.

• Make final packing decisions. Start packing items you don’t use often.

• Clean and clear your home, including closets, basements and attics.

• Call to find out how to transfer your bank accounts.

• Each year, many people move without clearing their safety deposit boxes. Do not be one of them.

• Carry valuables with you. If you have hidden any valuables around the house, be sure to collect them before leaving. Some state laws prohibit the moving of house plants. Consider giving your plants to a friend or local charity.

• Plan meals that will use up the food in your freezer and refrigerator.

• Have your automobile serviced if you are traveling by car.

• Transfer all current prescriptions to a drugstore in your new town if needed.

• Dispose of flammable items such as fireworks, cleaning fluids, matches, acids, chemistry sets, aerosol cans, paint, ammunition and poisons such as weed killer.

• Drain all the oil and gasoline from your lawn mower and power tools to ensure safe transportation. Refer to your owner’s manual for specific instructions.

ONE WEEK BEFORE MOVING

• This is your week to tie up loose ends. Check back through this guide to make sure you have noticed everything.

• Your moving company should have provided you with various labels for your goods. These can include “Do Not Load,” “Load First,” “Load Last” and “Fragile.” Take special care to label your goods appropriately.

• Pack your suitcases and confirm your family’s travel arrangements (flights, hotel, rental cars, etc.). Try to keep your plans as flexible as possible in the event of an unexpected schedule change(s).

• Ensure your moving agent knows the address and phone number where you can be reached if you are not going directly into your new home.

• At least one day before moving, empty, defrost and clean your refrigerator and freezer. If necessary, prepare your stove to be moved. Try using baking soda to get rid of odors.

• Prepare a “Trip Kit” for moving day. This kit can contain snacks, beverages and games for the kids to keep them occupied during the move. If you are stopping overnight, be sure to pack items such as toothbrushes and other essentials you will need while your belongings are in transit.

• Plan on returning rented cable receivers.

• Strip your beds, and make sure the bedding goes into a “Load Last” box.

• Make sure to be on hand when the movers arrive. It is important that an adult be authorized to take your place if you cannot be present at any time while the movers are there. Let the agent know to whom you have given this authority. Be sure that your chosen representative knows exactly what to do. Remember – this person may be asked to sign documents obligating you to charges.

• Confirm the delivery date and time at your new address. Write directions to your new home for the van operator, provide the new phone number and include cell phone numbers where you can be reached in transit. Make sure to take along the destination agent’s name, address and telephone numbers.

• Always try to spend as much time with the mover as possible. If you have special instructions (like what to load first and last), make sure it is communicated to your mover. Communicate well with the movers. Tell the mover in advance if you choose to have your mover handle your valuables or other fragile goods.

• When the van operator arrives, review all details and paperwork. Accompany the driver as they inspect and tag each piece of furniture with an identifying number. These numbers and a detailed description of your goods and their condition at the time of loading will appear on the inventory sheets.

• Your responsibility is to see that all your goods are loaded, so remain on the premises until loading is completed. To ensure that everything gets noticed, always do a final inspection of the premises. Only sign releases after completing this inspection.

• If you get to the destination before the mover, be patient. They might have encountered traffic or some other type of delay.

• Since you will probably want to clean before the furniture is unloaded, make sure your vacuum is packed last so it can be unloaded first.

MOVE - IN DAY

• The van operator will contact you or the destination agent 24 hours before the expected arrival time. This allows time to locate you and arrange for unloading. If, for some reason, you cannot be reached, it is then your responsibility to contact the destination agent.

• Be sure you are there when the movers arrive. Please plan to stay around while they unload if they have any questions. If you cannot be there personally, be sure to authorize an adult to be your representative to accept delivery and pay the charges. Inform the destination agent of your chosen representative’s name. Your representative will be asked to note any change in the condition of your goods mentioned on the inventory at the time of loading and to note any items missing at the time of delivery.

• Have payment on hand for your moving charges. Unless other billing arrangements were made in advance, payment is required upon delivery in cash, traveler’s checks, money order or cashier’s check. Most of the time, personal checks are not accepted.

• Ensure the utilities have been connected, and follow up on any delays.

• Confine your pets to an out-of-the-way room to help keep them from running away or becoming agitated by all of the activity.

• Review your floor plan so you can tell the movers where to place your furniture and appliances is a good idea. Please plan to be available to direct them as they unload. To prevent possible damage, televisions, stereos, computers, other electronic equipment and major appliances should not be used for 24 hours after delivery, allowing them to adjust to room temperature.

• Get some rest and enjoy your new home!

SCHOOLS

• Niche.com

• Schooldigger.com

• Schoolgrades.georgia.gov

• Greatschools.org

VENDORS

INSPECTORS

• At Ease Inspections

770.765.6869

ateaseinspections.net

• ALLVIEW Inspections

Lucas - 678.525.2194

allviewhomeinspections.com

• Cingo Home Inspections

855.797.0189

cingohome.com/home-inspections

• BPG Inspections

888.972.7146

bpginspections.com/home-inspections

SURVEYORS

• McClung Surveying

770.434.3383

mcclungsurveying.com

• Survey Land Express Eugene Stepanov - 404.252.5747 surveylandexpress.com

• Survey Systems Atlanta Gail Mooney - 404.301.8493 surveysystemsatlanta.com

LENDERS

• Call for recommendations