THE A.P. MOLLER GROUP

The A.P. Moller Group is a diversified group of industry companies. While independently run with dedicated boards and executive teams, we encourage and facilitate collaboration, networking, and sharing of best practices across our portfolio companies. A.P. Moller Holding is the parent company of the Group, investing in and building businesses with a positive impact on society – ‘nyttig virksomhed’.

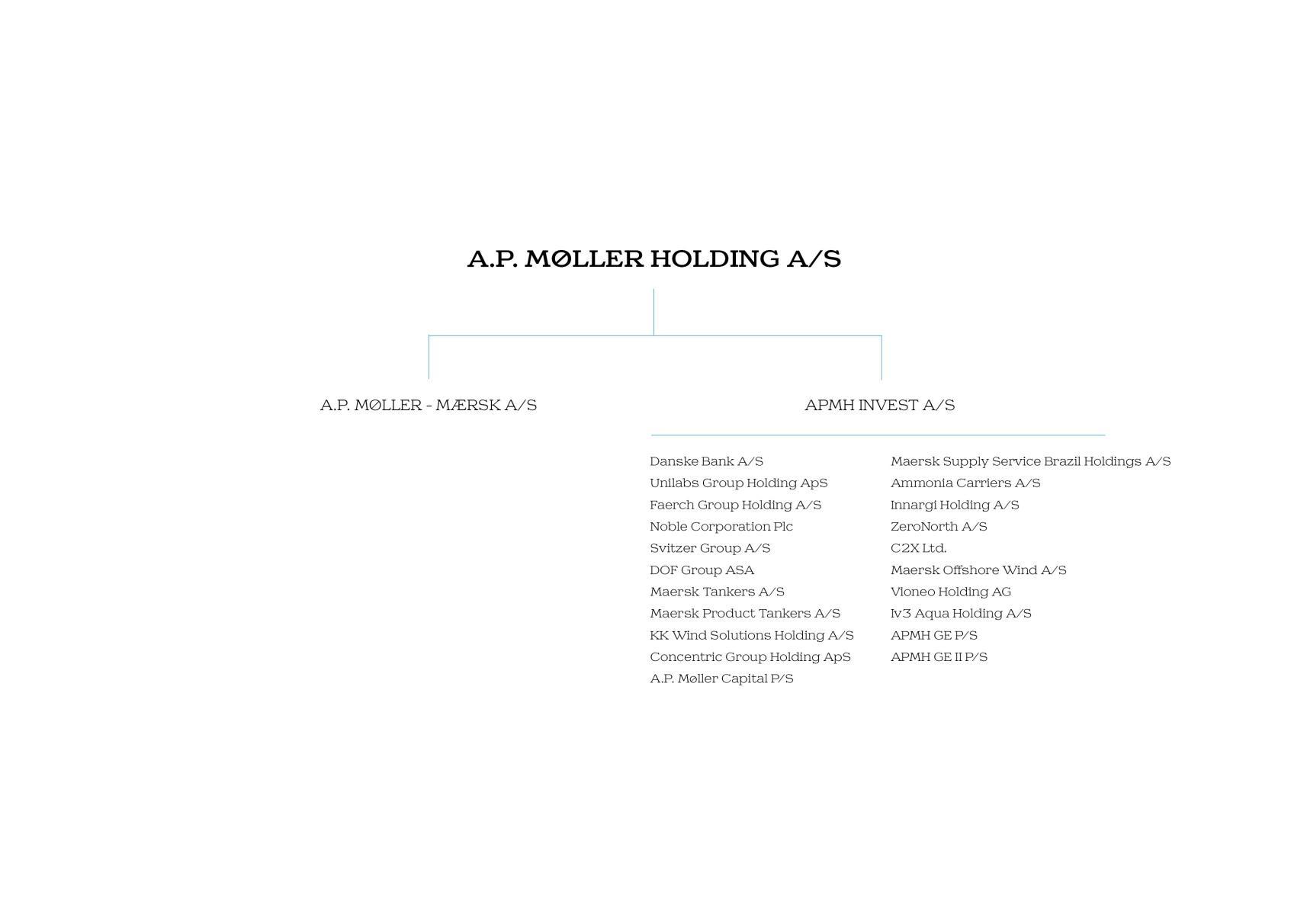

A.P. Møller Holding A/S (hereafter referred to as A.P. Moller Holding) is the parent company of the A.P. Moller G roup (the G roup). The Annual Report of A.P. M oller Holding includes management review, consolidated f inancial statements , and parent company financial statements . The term A.P. Moller Holding group (the group) is used in the A nnual R eport for controlled and consolidated companies. In A.P. Moller Holding’s investment activities, investments owned by APMH Invest A/S are included.

The 20 24 compara tive figures are stated in brackets , except in ‘Letter from the CEO’

Møller Holding

MANAGEMENT REVIEW

LETTER FROM THE CEO

ROBERT M. UGGLA CEO

The A.P. Moller Group developed satisfactorily in 2025 and largely in line with expectations. The Group ended the year with a revenue of DKK 401bn (USD 61bn), EBITDA of DKK 68bn (USD 10bn), a net result of DKK 24bn (USD 4bn), and total assets of DKK 770bn (USD 121bn). At the end of 2025, A.P. Moller Holding remained debt free, with a full year cash inflow of DKK 19bn (USD 3bn). The net asset value increased by 22% to DKK 281bn (USD 44bn) , with our liquid public markets portfolio valued at DKK 52bn (USD 8bn)

CREATING LONG-TERM SHAREHOLDER VALUE

In the last ten years, since we restructured our Group and started building an investment organisation, A.P. Moller Holding’s net asset value has almost tripled, from DKK 107bn end 2015 to DKK 281bn end 2025 (or DKK 174bn created). During this period, the portfolio also became more diversified: In 2016, 100% of A.P. Moller Holding’s net asset value consisted of A.P. Moller - Maersk and Danske Bank , while t oday these two assets represent approximately 50% of our net asset value .

More recently, 2025 proved to be a mixed year, especially for the shipping related activities. Some of our offshore affiliates performed well, tankers had a reasonable year, but the container line activities of A.P. Moller - Maersk had a more challenging d evelopment in freight rates. On the other hand, we continue d to see strong results for APM Terminals, as container volumes were strong and the team delivered industry leading operating performance in many ports. During the year, APM Terminals successfully renewed concessions in Port Elizabeth, New Jersey, and Pier 400, Los Angeles, and secured new greenfield projects in Vietnam and Bangladesh, positioning the business for growth in important markets.

Danske Bank continued to deliver strong results with a net profit of DKK 23bn (USD 3bn) and is now performing in line with Nordic peers. It is a testament to the relentless efforts and turnaround since 2018, involving many leaders and Directors, to bring the bank back to its pole position in Nordic financial services. During this period, A.P. Moller Holding has been a highly engaged and unwavering shareholder despite the headwind s the bank has faced.

Unilabs and Faerch welcomed new CEOs during 2025. Unilabs exceeded our operating expectations for the year. Although the external market challenges in IVD (laboratory based diagnostics) remain, we also acknowledge how AI deployment, in particular in radiol ogy and pathology, is providing far better diagnostics accuracy, and thereby better patient outcomes, as well as interesting growth opportunities for Unilabs.

The future implications of AI are also a central consideration for our growth equity team, which has invested in 13 different technology companies since 2022, of which four investments were concluded in 2025. These are minority investments in next generation ventures, where we seek to leverage and strengthen our Group knowledge and network while targeting attractive returns on the capital deployed.

N otable transactions in the Group include Svitzer, which was successfully taken private during the year. At the end of 2025 , Svitzer acquired a majority shareholding in Buksér & Berging in Norway, as part of its growth strategy. We look forward to working closely with the founding family. A.P. Moller Holding’s industrial activities also continued to grow with Concentric acquiring Officine Mazzocco Pagnoni to strengthen its position as a tier one supplier to leading OEMs within construction equipment and trucking.

A.P. Moller Capital pursued several investments in 2025 across energy and logistics related activities. The team also pursued new partnerships with Berge Logistics in Spain and with the Ayala Group in the Philippines, expanding our Group’s network with str ong local partners and family owners. During the year, A.P. Moller Capital sold its shareholding in the grain port operator Mass Cereales in Morocco at an attractive return, after delivering operational improvements and growth. It is always bittersweet to sell a high performing and impactful business: While capital returns are redeployed in other useful activities, it is difficult to say farewell to colleagues and valued activities like the Morocco operation.

In line with our Group’s purpose, A.P. Moller Holding has also supported the development of scale -ups since its inception. In this respect, in 2025, Innargi opened its first geothermal heating facility , heating the equivalent of 6,500 households in Aarhus through the district heating network , targeting another 29,500 households equivalent to 110 MW. Innargi’s plant in Aarhus reduces dependency on imported biomass, at a time of geopolitical uncertainty, and provides a sustainable source of base load energy. Innargi also signed an agreement to develop a plant in Virum. Moreover, Iv3 Aqua completed the development of the Qurayyat Desalination Company Project, a modern desalination plant in Oman, providing 15% of all desalinated water to Oman’s national grid in a region with limited freshwater reserves.

MACRO AND REGULATORY DEVELOPMENTS

Geopolitical pundits have stressed that 2025 was characterised by an accelerated shift towards a multipolar world. Despite this development, global trade proved highly resilient and trade flows grew at a faster rate in 2025 than in the previous year, despi te an increase in US tariffs. More specifically, container volumes grew by 5.2%, outpacing global GDP growth.

As governments become increasingly concerned about supply chain related dependencies, the pressing question to political leaders is not just trade policy, but also how to enhance competitiveness of domestic industries. When Mario Draghi in 2024 articulated the EU’s competitive challenges, it resonated well with the views of its member states. The European Round Table for Industry and many business leaders have been vocal for a long time that the EU needs to reduce regulatory burdens to turn around its econo my. This also applies to the financial services industry: If capital requirements of Europe’s banks were reduced to the levels of their American counterparts, the absolute financing capacity of European businesses and households would be increased by an estimated EUR 1.9 trillion to EUR 2.7 trillion. In addition, there is opportunity to stimulate investments in growth and innovation by reducing the overlay of local legislation, e.g. Danish banks would be able to provide an additional DKK 200bn of funding to the local economy if the Danish government aligned its financial services regulations with EU rules.

For companies dependent on a global talent market, some of the regulatory headwinds are exacerbated by local tax rules, such as exit taxation, which makes it difficult to attract talent to certain countries. Several of our portfolio companies are experienc ing these challenges first hand. As we now embrace nascent and highly impactful technologies, including AI, the race for talent becomes even more consequential. Ultimately, the cost of not being competitive internationally is carried by countries, as corpo rate activities, know -how, and investments risk moving abroad.

As governments become increasingly concerned about supply chain related dependencies, the pressing question to political leaders is not just trade policy, but also how to enhance competitiveness of domestic industries.

ACKNOWLEDGING OUR COLLEAGUES ACROSS THE GROUP

Armed conflicts remain a major concern for our Group. With approximately 60 ongoing interstate and civil wars worldwide, not counting a number of unresolved disputes that risk erupting near term, conflicts are at their highest level since World War II.

Freedom of navigation is undermined and supply chains are attacked during these conflicts, adding to the human suffering. In the Middle East, our Group has approximately 8,000 colleagues, who provide essential services to local communities, from water desalination to logistics. The latter does not only cover the exports of hydrocarbons for the global energy markets, but there is also a pressing need for the import of agricultural products with reefer containers. As a Group, we do our utmost to develop and p rovide reliable solutions for our customers and the local communities we serve, while also keeping the safety of our colleagues and assets at the forefront of our minds.

As written by Arnold Peter Møller in 1946 in a letter to his son: ‘no loss should hit us which can be avoided with constant care’.

As we finalise our accounts for 2025, I convey my sincere gratitude to our Group’s Directors, Executives , and colleagues across the globe for their leadership and extensive efforts in the year that passed. A special note is sent to our colleagues in conflict areas, acknowledging the societal impact of their activities.

2025 marked the 50th anniversary of Maersk’s first container vessel sailing. On 5 September 1975, Adrian Mærsk departed on her maiden voyage from Newark, New Jersey. This new form of liner shipping enabled Maersk to provide a faster and more reliable service to customers. The history of the container serves as inspiration in our Group’s constant quest to stay relevant for the future.

‘No loss should hit us which can be avoided with constant care.’ A.P. MØLLER, 1946

FIVE-YEAR SUMMARY

CASH FLOW STATEMENT

HIGHLIGHTS

The A.P. Moller Group delivered a solid result in 202 5, despite economic headwinds in some of our larger segments, a continued complex geopolitical landscape, and shifting trade policies.

A.P. Moller Holding made a voluntary purchase offer for all issued shares in Svitzer. The company was delisted at the end of May 2025.

A.P. Moller - Maersk experience d continued pressure on freight rates but manag ed to improve reliability mainly due to the implementation of the Gemini Cooperation. APM Terminals continued to see solid growth and delivered a strong result in 2025.

The merger between Maersk Supply Service and DOF was successfully completed . DOF continues to see a solid improvement in its order backlog, mainly driven by activity in Brazil.

In June 2025, Concentric acquired OMP. We see a strong value proposition in the combined company.

Innargi opened its first geothermal district heating facility, expected to deliver heat to more than 36,000 households in Aa rhus when fully developed.

In December 2025, Danske Bank ended its three year probation period with the US authorities.

Our growth equity portfolio expanded during the year. The portfolio counted 13 investments at the end of 202 5

Net asset value increased by 2 2% to DKK 28 1bn, primarily attributable to the rise in share prices of A.P. MollerMaersk, Danske Bank, and DOF, in addition to cash inflow from shareholder distributions.

FINANCIAL PERFORMANCE

A.P. Moller Holding delivered a consolidated result of DKK 24bn, representing a return on equity of 4%. We benefited from a cash inflow of DKK 19bn and saw an increase in net asset value of DKK 51bn to DKK 281bn, primarily driven by a higher valuation of our larger listed portfolio companies.

A.P. Moller Holding is the parent company of the A.P. Moller Group, investing in ‘nyttig virksomhed’ – building and investing in businesses that have a positive impact on society. As a purpose -driven investment company leveraging more than 120 years of entrepreneurship, our focus is to build and buy platforms within our four thematic investment areas: Global trade; Energy transition; Circularity, water & waste recovery; and Demographic & societal change .

2025 proved to be yet another eventful year with high activity across our organisation. Among other things, the continued complex geopolitical landscape and advancing technology keep us vigilant.

Throughout the year, maintaining financial stability amid volatile markets has remained a key priority for the group . By sustaining a strong liquidity position , we are well prepared to deliver on our objectives and seize the opportunities we expect will arise in volatile markets while continuing to focus on our positive contribution to the society.

A.P. Moller Holding delivered a consolidated revenue of DKK 401bn and a net result of DKK 24bn, ending the year with a total equity of DKK 511bn. Operating profit and earnings fell compared to 2024, mainly due to a lower rate environment in the shipping segment . Our industrial businesses showed organic growth and have successfully integrated companies acquired in 202 4, but they were affected by inflation and volatility due to shifting trade policies . The results are significantly impaired by a 4% drop in th e average USD exchange rate compared to 2024.

A.P. Moller Holding recorded a cash inflow from our portfolio companies of DKK 19 bn, leading to growth in our liquidity , which reached D KK 5 2bn at year end.

Total assets and equity de creased due to the weakened USD exchange rate . This was partly offset by positive results, mainly driven by Danske Bank and our financial portfolio.

Net asset value increased by 22 % to DKK 28 1bn, primarily attributable to the rise in share prices of A.P. Moller - Maersk , Danske Bank , and DOF , in addition to cash inflow from shareholder distributions.

The valuation of our privately held portfolio companies remained largely stable over the year, though there were variations at individual company level. The privately held shipping assets were impacted by the weaker USD exchange rate.

OPERATING ACTIVITIES

In 2025, revenue fell by 6% to DKK 401bn, mainly due to a 4% drop in the average USD exchange rate. Energy transition and D emographic & societal change grew steadily, while G lobal trade businesses struggled in a market facing geopolitical and trade uncertainties

OPERATING COSTS

Operating costs matched 2024 levels, driven by sustained business activit ies and effective cost management However, inflationary pressure and expenditure related to strategic acquisitions and transformation initiatives continued to negatively affect costs.

EBITDA

Our operating profit declined from DKK 91bn in 2024 to DKK 68bn, primarily due to the drop in the USD exchange rate and reduced earnings from our shipping activities. However, this was partially balanced by increased profitability in Towage & marine services and businesses within Energy transitio n.

EBIT

EBIT fell by 20bn to DKK 28bn in 202 5, mainly attributed to reduced freight rates with in the container segment and a weaker USD. This decline was partially mitigated by lower impairment losses across the group

FINANCIAL ITEMS

Net financial expenses amounted to DKK 1bn, down from last year's net income of DKK 7bn, mainly reflecting a lower return from the liquidity portfolio and foreign exchange losses due to the lower USD exchange rate

TAX

Corporate income taxes comprise taxes calculated in accordance with various countries’ tax regimes. Land -based activities, which are subject to normal corporate income tax, include terminals, logistics, services and shipping agencies, sale of industrial pr oducts, diagnostics services, and financial profit from other equity investments. The taxation of shipping income is based on tonnage tax regimes and applies to a significant part of the group’s activities. Given tonnage taxation is not impacted by financ ial profits and is payable even in loss making years, the effective tax rate metric can fluctuate significantly over the years.

Tax for the year was DKK 4bn, down from DKK 5bn in 2024 drive n by lower profit levels. The effective tax rate increased from 10% to 13% in 2025, mainly due to the introduction of the Global Minimum Taxation (OECD Pillar Two).

RESULT FOR THE YEAR

Result for the year dropped from DKK 49bn in 2024 to DKK 24bn, mainly reflecting the headwinds within the container segment.

Result attributable to the owner of A.P. Møller Holding A/S was DKK 12bn compared to DKK 22bn in 202 4, positively impacted by the group’s share of the result in associated companies.

The DKK/USD average exchange rate was 4% lower than in 2024 and 11% lower when comparing end 2024 with end 2025

O ur expectations for the result for the year, as outlined in the Annual Report 2024 , were surpassed , largely attributable to improved market condition s for our shipping businesses compared with the financial outlook at the beginning of the year.

FINANCIAL RESULT FOR THE PARENT COMPANY

As the parent company of A.P. Moller Group, we strive to maintain an efficient and agile organisation with a constant focus on securing the necessary resources and capabilities to support our purpose.

Result for the year was DKK 7bn (DKK 23bn), reflecting lower earning s in our subsidiaries compared to 2024, mainly attributed to headwinds in Global trade .

As of 31 December 2025, total assets amounted to DKK 293 bn (DKK 302bn), with DKK 291 bn (DKK 300bn) attributed to investments in subsidiaries. The decrease in total assets was primarily due to the 11% decline in the USD exchange rate.

Equity at year end totalled DKK 292 bn (DKK 301bn), with DKK 179 bn (DKK 172bn) allocated to retained earnings.

FINANCIAL

DEVELOPMENT IN PORTFOLIO COMPANIES

2025 was marked by persistent macroeconomic uncertainty and geopolitical disruption, including prolonged Red Sea challenges that reshaped global trade lanes, and volatility in US trade driven by shifting trade policies. Even though freight rates remained under pressure, A.P. Moller - Maersk continued to expand freight volumes and improved reliability through the EastWest network via the Gemini Cooperation. Logistics & Services sustained margin expansion , and T erminals delivered record volumes, revenue, and profitability. In total, A.P. Moller - Maersk delivered a revenue of DKK 3 57 bn and a profit for the year of DKK 19bn

A.P. Moller - Maersk approved a dividend of DKK 480 per share , corresponding to a payout ratio of 40% in line with its dividend policy . A share buy -back programme of up to DKK 6bn has been initiated to be executed over a period of 12 months. The purpose of the programme is to adjust the capital structure through the cancellation of shares repurchased.

In December 2025, Danske Bank ended its three -year probation period with the US authorities, marking the closure of the Estonia case. The bank is executing well on its Forward ’28 strategy and is catching up to peers. The bank reported a net profit of DKK 23bn , down 3% from 2024 . Solid customer activity and the good financial health and resilience of their customers supported the financial result but were offset by higher loan impairment charges – though still at low levels – compared to 2024, which record ed a net impairment reversal of DKK 0.5bn .

Danske Bank continue d to have a robust capital and liquidity position with significant buffers well above regulatory requirements. At the end of 202 5, Danske Bank reported a CET1 ratio at 17 3%, which is well above regulation and the bank’s internal target of 16% and ensures a sufficiently prudent buffer to the capital requirement.

The dividend payment for 2025 amounted to DKK 22.72 per share , and Danske Bank has announced a new share buy -back programme of DKK 5bn. Total capital distribution ( dividend s and share buy -back programmes ) of DKK 23bn is equivalent to a dividend payout of 100% of net profit for 2025.

T he European clinical laboratory services market continued to face significant pricing pressure. Regulatory reforms, cost containment measures, and reimbursement constraints intensified competition and further compressed margins across the sector. Despite these headwinds, Unilabs demonstrated resilience, delivering 1% organic revenue growth. This solid performance stands out in a broader market slowdown, where many peers reported flat or declining revenues amid pricing erosion and rising operational costs.

Overall, Unilabs’ operational results for 2025 were in line with expectations, underscoring the company’s ability to navigate a challenging market environment as well as deliver on the business ’ ongoing transformation plan to support organic growth and improve profitability in the coming years .

Faerch experienced a challenging market backdrop in 2025 , shaped by continued geopolitical uncertainty and persistently

high food prices. Consumers adjusted their spending, and interest in alternative packaging grew as markets sought more efficient resource use. The company focused on portfolio optimisation and structural changes throughout the year. Despite these headwinds, Faerch delivered a n acceptable performance and successfully defended its leading market position and competitiveness. Operating margin has been maintained despite continued cost inflation as a result of disciplined cost management and operational efficie ncy.

Noble reported acceptable 2025 financial results with 8% yearover -year growth, driven by an improved utili sation rate, higher backlog , and more contracts despite declining day rates. Unfortunately, the backlog for 2026 remains challenging, but it is reported higher for 2027 . Noble returned approx imately DKK 2.3bn to its shareholders through a combination of dividends and share buy -backs.

In 2025, Svitzer experienced a volatile market impacted by geopolitical challeng es leading to changing trade routes and friendshoring , resulting in a lower than expected performance in the first half. However, improved cost management and efficiency measures, along with a recovery in shipping volumes, led to a strong second half. Overall, Svitzer achieved solid full -year results, with revenue up 4% on constant exchange rates and operating profit rising 5% to DKK 2bn compared to 2024.

DOF continue d to see strong activity in the subsea segment , and during 2025 it significantly g rew the order backlog, up 57%, securing roughly 77% of the 2026 revenue guidance. Its strong financial performance was supported by efficient operations and fleet optimisation. DOF delivered an EBITDA margin of 34%. Dividends for 2025 amounted to DKK 2.1bn corresponding to a dividend yield of 11%. DOF continues to see strong project activity and service demand.

Average Time Charter Equivalent (TCE) in Maersk Product Tankers fell significantly short of 2024 but remained above historic al averages. Relatively high but volatile spot market rates and a ttractive asset markets that enabled the company to sell

older tonnage at attractive prices had a positive impact on the result during the year .

In 2025, KK Group grew revenue by 4%, despite ongoing global challenges, ending the year with a record -high positive result. The company further integrated acquisitions, rebranded under the ‘Powering Change’ strategy, expanded in Asia with its largest manufacturing site , located in Bangalore, and set up a new US division to drive growth. KK Group expects continued industry headwinds in 2026 .

Concentric, acquired in October 2024, saw lower volumes throughout 2025 , mainly driven by the US market . The electrification division was affected by reduced North American government support for electric vehicles and transit bus supply chain disruptions. Although contribution margins remained stable, overall profitability declined due to lower sales volumes and increased capacity costs associated with continued resource investments, which were partially linked to the acquisition of Officine Mazzocco Pagno ni ( OMP )

EQUITY

As of 31 December 2025, total equity amounted to DKK 51 1bn , down from DKK 562bn – a decrease of 10 %. This drop was primarily due to the USD exchange rate falling by 11% compared to the end of 2024, as well as dividend payments to shareholders and non -controlling interests. The group saw benefits from improved annual results. Return on equity was 4%, compared to 9% previously, and the equity ratio declined from 68% to 66%.

A.P. Mol ler Holding’s share of equity fell to DKK 307 bn, from DKK 310bn.

DIVIDEND

Based on the financial result for 202 5, the Board of Directors proposes a dividend of DKK 1.0bn to A.P. Møller og Hustru Chastine Mc -Kinney Møllers Fond til almene Formaal (A.P. Moller Foundation). In 202 5, a dividend of DKK 1.0bn was paid.

INVESTMENT ACTIVITY

In April 2025, we announced a recommended voluntary purchase offer for all issued shares in Svitzer, with the aim of taking the company private to better support its long -term ambitions. As the largest shareholder, we saw that the listing had not created t he desired platform for growth, which is essential for maintaining Svitzer’s market position in a competitive and fragmented industry undergoing consolidation. The company was delisted at the end of May 2025.

In November 2025, Svitzer announced the acquisition of a 66.6% shareholding in Bu ksér og Berging AS, a leading Norwegian towage offshore and marine contracting company. The transaction was concluded on 2 January 2026.

In Ju ne 2025, C oncentric announced its strategic acquisition of OMP , a leading manufacturer of advanced oil pumps and fluid management components, headquartered in Funo, Italy. This acquisition provides Concentric with OMP's leading vane pump technology used by global OEMs and is expected to boost Concentric’s annual revenue by over 35% , as well as enhance performance and efficiency. We see a strong value proposition in the combined company, and the integration is progressing as planned.

In October 2025, Innargi opened its first geothermal district heating facility, expected to deliver heat to more than 36,000 households in Aarhus when fully developed. The next stage focuses on regulatory processes for the upcoming site. Innargi aims to finish the project before 2030. The project pipeline in Innargi continues to grow in both Denmark and Northern Europe, supporting the green energy security agenda in Europe.

Before year -end, an approval for geothermal research and extraction of geothermal heat in Virum, ano ther town in Denmark, was received, expected to supply heating to 10,000 households when fully developed.

Iv3 Aqua achieved C ommercial O peration D ate (COD) in November 2025 on the Qurayyat Desalination Company Project (acquired in 2024). The project now has an agreement with Oman’s government until 2047. The plant has an operating capacity of 200,000 m 3 per day and is able to supply over 15% of all desalinated water to Oman’s national grid.

By the end of 2025, our growth equity portfolio comprised 13 investments, including four new additions made during the year. We remain confident in the strategic value of investing in latestage growth companies and anticipate appealing risk -adjusted finan cial returns. To further support our investment team, we have opened an office in Singapore.

Our other portfolio companies have signed and completed a number of acquisitions, including the takeover of Panama Canal Railway Company by A.P. Moller - Maersk.

The c ash flow used for investing activities was mainly impacted by our investments in portfolio companies as well as activity in our financial portfolio. The total capital inflow from dividends, share buy -back programmes, and our financial portfolio was DKK 19 bn (DKK 17 bn), positively impacted by dividends , mainly from A.P. Moller - Maersk and Danske Bank , and share buyback programmes from Danske Bank

NET ASSET VALUE

At the end of 202 5, the net asset value increased to DKK 28 1bn, up 22% from the end of 2024. The development was mainly driven by the rise in the share price s of Danske Bank by 56% and of A.P. Moller - Maersk by 23%

We experienced a small 5% drop in the value of Noble , impacted by lower average day rates and rig utilisation ratio, while DOF rose 7% , supported by its strong financial performance and a significant ly improved order backlog

The net asset value is a volatile measure, not least over a shorter period, given our significant exposure to a few main portfolio companies. The net asset value calculation is based on different valuation methods. Our listed portfolio companies are assess ed using their share prices at the stock exchange. The privately held companies are assessed based on recognised valuation methods, and the financial portfolio on market capitalisation, primarily quoted prices.

FINANCIAL OUTLOOK

A.P. Moller Holding and its portfolio companies are exposed to global economic activity levels as well as development s in the global financial markets. Based on our expectations and financial guidance for our portfolio companies and current exchange rates, we expect that the 2026 EBITDA will be positive but lower than in 2025

The above statement is, by nature, subject to several uncertainties, including but not limited to, geopolitical uncertainties that will challenge global supply chains and global economic growth, and the rapid rise of economic nationalism and protectionism. This could cause actual results and performance to differ materially from our expectations. In addition, financial performance depends on several factors subject to uncertainties related to the uncertai n macroeconomic conditions as well as the future deve lopment of freight rates and volumes, import duties, demographic and societal changes, demand for sustainable solutions, commodity prices, including but not limited to, oil and energy prices, inflation, and interest rates.

Svitzer Ingrid, Denmark's first electric tugboat, was christened by Her Majesty Queen Mary of Denmark in September 2025.

BUILDING A PORTFOLIO OF PLATFORMS FOR THE FUTURE

Our investment strategy is anchored in an ambition to build scalable platforms in areas where we have relevant experience and expertise so we can help drive long-term value and impact. We focus on long-term mega trends, and, as owners, we utilise and leverage the strengths and capabilities accumulated across our Group throughout more than 120 years. In doing this, we strive to fulfil our Group’s long-standing purpose of ‘nyttig virksomhed’ (having a positive impact on society).

Our strategy implies that we devote our time and resources to identifying and executing investments across sectors and countries, and within four themes that we believe will be relevant for multiple business cycles:

Global trade

Global trade is key to prosperity as it enables income and growth for people and societies. Our businesses enable global trade in different ways, for example by facilitating more efficient logistics across the globe and by building critical infrastructure. Financial services and the proliferation of efficient capital allocation are also drivers as well as beneficiaries of increased global trade.

Energy transition

Our societies depend on a steady and reliable supply of energy. At the same time, we need to migrate from the fossil sources that propelled the industrial revolution and drove wealth creation and consumption for many decades and move towards energy generation from non -fossil and renewable sources. Our focus is on this transition which will not happen overnight and maintaining access to energy is a necessity for our societies.

Circularity, water & waste recovery

Global consumption of resources and products is not in balance with our planet ’s ability to regenerate the resources consumed , nor to absorb the substantial generation of waste. Sustainable replacements are being adopted , and the use and utilisation of resources must be optimised. We are committed to the development of circular rather than linear production and consumption models.

Demographic & societal change

Across both mature and emerging economies, population demographics continue to change, which is creating challenging conditions for societal welfare models. These slow -moving but largely inevitable demographic and societal factors are transforming our soci eties. Absent continuous improvements in efficiency and new business models, the welfare imbalance in our societies will create unsustainable levels of inequality. We invest in digital and automated ways of working to address the welfare challenges arising from demographic change.

INVESTMENT MANDATES

We leverage our knowledge, expertise, and experience across four different mandates:

Principal holdings

Large control -oriented investments in companies backed by solid long -term trends. We prefer our principal investments to be platforms where we have the optionality of deploying additional capital over time for organic and inorganic expansion.

Growth equity

Patient minority investments in late -stage growth businesses. In addition to generating attractive financial returns, the objective is to leverage and continue to enhance domain knowledge within our core areas of expertise and investment themes .

Scale-ups

Rooted in our entrepreneurial legacy and spirit, we selectively initiate incubation projects and actual building of new businesses. Such greenfield projects and business building are based on internally generated ideas, a few of which are, after an extensive vetting process, pushed forward and initially funded by us. Over time, we typically bring in other investors.

Public markets

We apply active concentrated global strategies across various asset classes seeking to generate financial results above or in line with external market benchmarks.

ENGAGED AND ACTIVE LONG-TERM OWNERS

In the spirit of our founder, A.P. Møller, we are engaged and active long -term owners with a point of view on key matters. Stewardship and a continued focus on the quality of interactions between management, Board of Directors, and owner(s) are therefore c ritical to our success. In recent years , we developed and implemented a set of principles and guidelines defining our ownership model, and how we exercise it. These principles are rooted in our legacy, and we will continue to optimise our stewardship and o wnership model in the years to come.

A.P. Moller - Maersk Danske Bank Unilabs Faerch

A.P. MOLLER - MAERSK is an integrated transport and logistics company working to connect and simplify its customers’ supply chains. The company is a global leader in shipping activities.

DANSKE BANK is Denmark’s largest bank. Its core business includes private, business, institutional customer segments, and other financial services to the Nordic markets.

UNILABS is a leading diagnostics services provider in Europe, focusing on laboratory testing, pathology, and radiology. The company services both public and private healthcare providers across multiple countries.

FAERCH is a leading supplier of circular packaging solutions to the global food industry, serving leading food manufacturers and retailers around the world.

NOBLE is a leading offshore drilling company for the oil and gas industry. The company owns and operates one of the youngest and most advanced fleets in the offshore drilling industry.

CEO: Vincent Clerc

CFO: Robert Josef Erni

Representatives

• Robert M. Uggla (Chair)

Key figures end of 202 5

• Market cap: DKK 215 bn

• Ownership: 4 4.4 % / 5 2.3 % voting share

(USDm)

CEO: Carsten R. Egeriis

CFO: Cecile Hillary

Representatives

• Martin N. Larsen (Vice Chair)

Key figures end of 202 5

• Market cap: DKK 260 bn

• Ownership: 21.3% TOTAL INCOME (DKKm)

CEO : Badhri Srinivasan

CFO: Carsten Højlund

Representatives

• Jan T. Nielsen (Vice Chair)

CEO: Pernille Lind Olsen CFO: Sonja Østergaard

Representatives

• Henrik Poulsen (Chair)

• Jan T. Nielsen (Vice Chair)

CEO: Robert W. Eifler

CFO: Richard B. Barker

Representatives

• Claus V. Hemmingsen

Key

•

(EURm)

(EURm)

Svitzer DOF

SVITZER is a global leader in sustainable marine services , provid ing critical towage infrastructure and maritime solutions across Europe, AMEA, Australia, and the Americas.

DOF is a leading provider of global offshore marine services for the energy sector, including oil and gas companies, offshore renewable companies , and subsea contractors.

Maersk Product Tankers KK Group

MAERSK PRODUCT TANKERS is an

asset company, owning tankers transporting energy products worldwide for large energy companies and trading houses.

KK GROUP is a global technology partner delivering power electronics, controls, cooling, monitoring, and service solutions for renewable energy and energy intensive industries.

CONCENTRIC is a global leader in pump, fan , and thermal management solutions for the commercial vehicle market, helping customers increase fuel efficiency, reduce emissions , and improve engine control.

CEO: Kasper Friis Nilaus

CFO: Knud Winkler

Representatives

• Robert M. Uggla (Vice Chair)

• Louise Løn

CEO: Mons S. Aase

CFO: Martin Lundberg

Representatives

• Erik Bergöö (Vice Chair)

Key figures end of 2025

• Market cap: DKK 15 bn

• Ownership: 25.0%

REVENUE (DKKm)

REVENUE

(USDm, includes only DOF up to the merger with Maersk Supply Service in 2024)

CEO: Tina Revsbech

CFO: Christian Huss

Representatives

• Martin N. Larsen (Chair)

• Birgitte Schou

• Erik Bergöö

CEO: Mauricio Quintana

CFO: Bjørn R. Mogensen

Representatives

• S imon K. Ibsen ( Vice Chair)

CEO: Josh Meyer

CFO: Marcus Whitehouse

Representatives

• Simon K. Ibsen (Vice Chair)

• Jan T. Nielsen

REVENUE (USDm)

REVENUE (DKKm)

REVENUE (USDm)

Maersk Tankers A.P. Moller Capital Maersk Offshore Wind Innargi

MAERSK TANKERS is a service company providing commercial management solutions for shipowners in the tanker industry. The company operates one of the largest tanker fleets in the world.

A.P. MOLLER CAPITAL is an infrastructure fund manager focusing on high growth markets, combining attractive risk adjusted return s with a positive societal impact.

MAERSK OFFSHORE WIND is a provider of installation services to the offshore wind market accelerating the rollout of offshore wind farms .

INNARGI is a geothermal heating company aiming to heat millions of urban homes while leaving zero impact on our planet.

ZERONORTH is a technology company providing a range of software solutions that enable the shipping industry to reduce its impact on the climate while maintaining commercial performance.

CEO: Tina Revsbech

CFO: Christian Huss

Representatives

• Robert M. Uggla (Chair)

• Maria Pejter

• Martin N. Larsen

CEO: Kim Fejfer

CFO: Joe Nielsen

Representatives

• Robert M. Uggla (Chair)

CEO: Michael Reimer Mortensen

CFO: Jesper H øybye

Representatives

• Martin N. Larsen (Chair)

• Maria Pejter

CEO: Samir Abboud

CFO: Lars Heineke

Representatives

• Claus V. Hemmingsen (Chair)

• Steffen Risager

CEO: Søren Andersen

CFO: K arsten Gregory

Representatives

• Maria Pejter

Iv3 Aqua C2X Vioneo

IV3 AQUA is a water management company owning and operating water, wastewater, reuse plants, concessions , and related water utility businesses.

C2X is a green methanol production company aiming to develop and operate green methanol production facilities to supply both the chemical and shipping sectors.

VIONEO was established to be the world’s first large -scale producer of fossil -free plastics based on green methanol.

CEO: Olaf N. Krohg

CFO : Frederick Hung

Representatives

• Jan T. Nielsen (Vice Chair)

• Paulius Urbonas

CEO: Brian Davis

CFO: Alastair Maxwell

Representatives

• Jan T. Nielsen (Chair)

• Steffen Risager

CEO: Alex Hogan

CFO: Arnaud Cachard

Representatives

• Simon K. Ibsen (Vice Chair)

RISK MANAGEMENT

Our risk management setup is closely related to our investment strategy and allows us to safeguard the longevity of our portfolio companies by understanding the inherent risks associated with each of them and by supporting the companies in managing these risks in a changing environment.

Risk management reporting is an integrated part of our business processes, allowing A.P. Moller Holding to respond appropriately to the changing environments our businesses are operating in. The Board of Directors receives portfolio performance reports inc luding risk management measures on a regular basis throughout the year.

Being an investor focusing on capital risk, we continuously develop our risk framework, and we have embedded controls and operational risk mitigation processes in our critical daily operations. We have a constant focus on good governance, and we have implemented procedures to continuously assess and ensure that we follow market standards and developments. Further, in line with the purpose of the A.P. Moller Foundation, and to ensure t he long -term viability and longevity of A.P. MollerMaersk, our portfolio companies are structured as visualised on page 79

OUR PORTFOLIO COMPANIES

Having a long -term ownership horizon, our ambition for each investment is defined in a clear ownership strategy, considering sector specific market parameters and developments , as well as current and emerging risks.

Risks related to our portfolio companies include business and financial risks associated with operations and performance. The management of such risks is effectively anchored with the Board of Directors in each of the portfolio companies. Each entity has defined and implemented their own risk management framework, ma naging specific, defined risks. As owners, we monitor business performance in the portfolio companies closely as part of our ownership aspiration. We report on business and risk related issues to our Board of Directors as appropriate.

Our investment team focuses on large and long -term investments and brings valuable global investment expertise. As we evaluate investment opportunities, the investments will undergo committees and investment gates , where thorough risk analysis, due diligence, and mitigation are natural parts of the investment

evaluation process. Our risk management framework allows us to critically evaluate such risks . Investments will be abandoned where risks/rewards are not deemed attractive and in line with our values , as well as our financial and strategic beliefs.

As our investments are expected to have a long -term ownership horizon, we focus on the inherent risks related to such investments. At all times, it is part of our strategic beliefs to invest in and build businesses that have a positive impact on society. Hence, we strive to ensure that all our partners acknowledge our values and share our commitment to conduct business in an ethical, legal, and socially responsible manner.

PUBLIC MARKETS

A.P. Moller Holding has a financial portfolio primarily with exposure to global equity markets managed by our own public markets team. The overall objective of the portfolio is i) to create economic value in line with our values , ii) to ensure a part of our financial portfolio remains highly liquid, acting as a buffer for the company to be flexible and able to react as needed in relation to our portfolio companies or to significant changes in our cash flows , and iii) to deliver performance in line with a fi xed benchmark.

The Board of Directors approves the investment policy and defines the acceptable risk limits including a variety of risk management factors such as single line limits, currency exposures , and asset class weights. These, in combination with internal investment principles, guide the financial investments on a daily basis. We manage the market, credit, liquidity, and currency risks related to our financial portfolio by limiting maximum exposure to individual asset classes and underlying assets. The guidelines are reviewed regularly to ensure they reflect the market situation and our financial situation at any given time.

CORPORATE SOCIAL RESPONSIBILITY

A.P. Moller Holding invests in and builds businesses with a positive impact on society – ‘nyttig virksomhed’ – as defined by our founder A.P. Møller.

‘Nyttig virksomhed’ is a key element in our investment strategy, and we are open to reconsider our ownership of a business if its business model does not have a positive impact on society. Hence, social responsibility is integrated into our purpose and is core to everything we do.

As part of good governance practice, we have implemented policies and systems to secure a solid basis for our activities as an engaged investment company. We focus on mitigating the key risks of essential compliance areas including money laundering & financing of terrorism and bribery & corruption. As reflected in our Code of Ethics and business conduct , engaging in any kind of fraud , bribery, and corruption is strictly prohibited, which is one of the cornerstones in our overall framework for how to exercis e due care to prevent fraud, bribery and corruption internally , as well as in relation to third parties acting on behalf of A.P. Moller Holding. This is especially relevant in relation to our investments, where we, prior to investing, conduct thorough due diligence measures on the target and relevant counterparties su ch as advisors, co -investors, etc.

STATUTORY REPORT CF. SECTION 99B OF THE DANISH FINANCIAL STATEMENTS ACT

As an international investment company with a broad range of investment activities, A.P. Moller Holding has a significant influence on society. We acknowledge the responsibilities that this entails and make an effort to ensure that we are recognised as a trustworthy group of companies.

The Board of Directors of each of our portfolio companies define their own specific policies and Codes of Conduct. We are represented on each board in companies where we hold a minimum of 50% of the votes, and our representatives ensure that relevant policies, including those related to human rights, climate change, and environmental impact, are implemented and enforced.

For A.P. Moller Holding’s statutory statement on CSR in accordance with section 99 b of The Danish Financial Statements Act, please refer to: https://apmoller.com/wpcontent/uploads/2026/03/APMH -CSR -Report -2025.pdf

STATUTORY REPORT CF. SECTION 99D OF THE DANISH FINANCIAL STATEMENTS ACT

In line with our core values, responsible use of information and data is part of our overall aim to adhere to high ethical standards. Pursuant to the requirements and with an outset in our daily operations and activities, A.P. Moller Holding has implemented a D ata E thics P olicy based on five principles reflecting how we use and process both personal and non -personal data as well as general data and information. The policy addresses our aim to be transparent as appropriate and acting responsibly with respec t and dignity both towards our employees and when working with third parties. The policy complements our policies and procedures on handling of personal data, IT -security, etc.

SUSTAINABILITY HIGHLIGHTS

The companies in the A.P. Moller Group define and execute their own sustainability initiatives. In 2025, numerous activities were launched of which a few are highlighted here. For more details, please refer to the respective sustainability reports.

A.P. Moller - Maersk took delivery of 10 new dual -fuel methanol vessels bringing its fleet to 19, advanced its multi -fuel portfolio approach through a liquefied biomethane supply agreement , and completed successful trials using blended e -methanol and ethanol fuels.

C2X signed an agreement with Microsoft to deliver 3.6 million metric tonnes of carbon removal units over 12 years from its Beaver Lake project in Louisiana, expected to produce over 500,000 metric ton ne s of bio -methanol annually and capture and store around 1 million metric tonnes of CO 2 annually.

Concentric installed 80,000 sq uare feet of solar panels at its Pune factory site in India, generating approx imately 900 kW of renewable energy and bringing the total to 200,000 square feet of solar panels installed across its sites.

Innargi began operations of its first geothermal district heating plant in Aarhus, Denmark. Once completed, the city's geothermal heating system is expected to supply 20% of its heating needs by 2030 while reducing the city's CO 2 emissions by approximately 165,000 tonnes annually.

KK Group ’s power converters and control systems, which are at the heart of each wind turbine, enabled 18 gigawatts of wind power in 2025, roughly equivalent to the power it would take to fast -charge 120,000 EVs at the same time.

Iv3 Aqua 's subsidiary, Qurayyat Desalination Company, reached the C ommercial O peration D ate of its desalination plant in Oman in November, three months ahead of schedule. The plant now has the capacity to produce up to 200 million litres of potable water per day, supplying over 15% of all desalinated water delivered to the national grid.

Unilabs partnered with Oxipit to implement AI assisted chest X -ray solutions across key European markets, speeding up diagnoses and improving accuracy to deliver faster, more reliable patient care.

A.P. Moller - Maersk ’s first dual -fuel methanol vessel, Laura Mærsk, received the first e -methanol from the newly inaugurated Kassø facility in Denmark in May 2025.

Svitzer launched Denmark's first electric tugboat, Ingrid. The tug will perform most tasks using electrical power, thereby reducing annual CO₂ emissions by 600900 tonnes. In December, Svitzer also committed to purchasing four electric, 26 metre TRAnsverse tugs.

BOARD OF DIRECTORS

Ane M.M. Uggla Chair

Chair of the Board of Directors

• A.P. Møller og Hustru Chastine Mc -Kinney Møllers Fond til almene Formaal

• Den A.P. Møllerske Støttefond

Other management duties

• Estemco III ApS (CEO)

• Timer ApS (CEO)

Claus V. Hemmingsen

Chair of the Board of Directors

• DFDS A/S

• Innargi Holding A/S

• HusCompagniet A/S

• Rambøll Gruppen A/S

Member of the Board of Directors

• A.P. Møller og Hustru Chastine Mc -Kinney Møllers Fond til almene Formaal

• Den A.P. Møllerske Støttefond

• Noble Corporation PLC

• Det Forenede Dampskibs -selskabs Jubilæumsfond

• Fonden Mærsk Mc -Kinney Møller Center for Zero Carbon Shipping

• Global Maritime Forum Fonden

Other management duties

• CVH Consulting ApS (CEO)

• Committee for Corporate Governance, Denmark (member)

Jan Leschly

Member of the Board of Directors

• UTR Sports LLC

• The Leschly Tennis Foundation

• Nightingale Veterinary Partners

Other management duties

• Adjunct Professor at Copenhagen Business School

Lars-Erik Brenøe

Member of the Board of Directors

• A.P. Møller og Hustru Chastine Mc -Kinney Møllers Fond til almene Formaal

• A.P. Møller og Hustru Chastine Mc -Kinney Møllers Familiefond

• Monjasa Holding A/S

• Odense Havn A/S

• Operaparkfonden

Other management duties

• LEBrenoe (personally owned law firm)

EXECUTIVE BOARD

Robert M. Uggla Chief Executive Officer

Other management duties, etc.

• A.P. Møller - Mærsk A/S (Chair)

• A.P. Møller Capital P/S (Chair)

• Maersk Tankers A/S (Chair)

• Svitzer Group A/S (Vice Chair)

• IMD (Director of the Foundation Board)

• International Business Leaders’ Advisory Council of the Mayor of Shanghai , IBLAC (Member)

• Agata ApS (CEO)

• Estemco XII ApS (CEO)

Robert M. Uggla is appointed to the Board of Directors in a number of entities controlled by A.P. Møller Holding A/S.

Jan T. Nielsen Chief Investment Officer

Other management duties, etc.

• C2X Ltd. (Chair)

• Faerch Group Holding A/S ( Vice Chair )

• Iv3 Aqua Holding A/S (Vice Chair)

• Unilabs Group Holding ApS (Vice Chair)

• Concentric AB (Board member)

• LEGO A/S (Board member)

• Copenhagen International School ( M ember of the Board of Governors)

• Thorsgaard Holding ApS (CEO)

Jan T. Nielsen is appointed to the Board of Directors in a number of entities controlled by A.P. Møller Holding A/S.

Martin N. Larsen Chief Financial Officer

Other management duties, etc.

• Ammonia Carriers A/S (Chair)

• Maersk Offshore Wind A/S (Chair)

• Maersk Product Tankers A/S (Chair)

• Navigare Capital Partners A/S (Chair)

• Assuranceforeningen SKULD (Gjensidig) (Vice Chair)

• Danske Bank A/S (Vice Chair)

• Danmarks Eksport - og Investeringsfond (EIFO) (Board member)

• Maersk Tankers A/S (Board member)

• MVKH ApS (CEO)

Martin N. Larsen is appointed to the Executive Board and Board of Directors in a number of entities controlled by A.P. Møller Holding A/S.

FINANCIAL STATEMENTS

CONSOLIDATED INCOME STATEMENT FOR 1 JANUARY TO 31 DECEMBER

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

CONSOLIDATED BALANCE SHEET

AS OF 31 DECEMBER

CONSOLIDATED CASH FLOW STATEMENT FOR 1 JANUARY TO 31 DECEMBER

Cash and bank balances include DKK 6.0bn (DKK 7.0bn) relating to cash and bank balances in countries with exchange rate control or other restrictions. These funds are not readily available for general use by the parent company or other subsidiaries.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

BASIS OF PREPARATION

Note 1.1: General accounting policies

This note sets out general accounting policies for A.P. Møller Holding A/S that relate to the financial statements as a whole. Where an accounting policy is generally applicable to a specific note to the financial statements, the policy is described within that note.

BASIS OF PREPARATION

The consolidated financial statements for 202 5 for A.P. Møller Holding A/S have been prepared on a going concern basis and in accordance with the IFRS Accounting Standards as adopted by the EU (IFRS) and additional Danish disclosure requirements for large enterprises in class C.

The consolidated financial statements are presented in DKK million (DKKm), and all values are rounded to the nearest thousand except when otherwise stated.

The accounting policies are consistent with those applied in the consolidated financial stat ements for 202 4, except for the changes to accounting standards that were effective from 1 January 202 5 and endorsed by the EU. The changes have not had a material impact on the financial statements.

CONSOLIDATION

The consolidated financial statements comprise the parent company A.P. M øller Holding A/S , its subsidiaries , and proportionate shares in joint arrangements classified as joint operations.

Subsidiaries are entities controlled by A.P. M oller Holding. Control is based on the power to direct the relevant activities of an entity and the exposure, or right , to variable returns arising from it. In that connection, relevant activities are those that significantly affect the investee’s returns. Control is usually achieved by directly or indirectly owning or in other ways controlling more than 50% of the voting rights, or by other rights, such as agreements on management control.

Joint arrangements are entities in which A.P. Moller Holding, according to contractual agreements with one or more parties, has joint control. The arrangements are classified as joint ventures if the contracting parties’ rights are limited to net assets in separate legal entities, and as joint operations if the parties have direct and unlimited rights to the assets and obligations for the liabilities of the arrangement.

Note 1.1:

General accounting policies

– continued

Entities in which A.P. Moller Holding exercises a significant but non -controlling influence are considered associated companies. A significant influence is usually achieved by directly or indirectly owning or controlling 20 -50% of the voting rights. Agreements and other circumstances are considered when assessing the degree of influence.

Consolidation is performed by summarising the financial statements of the parent company and its subsidiaries in accordance with A.P. Moller Holding’s accounting policies. Intra -group income and expenses, shareholdings, dividends, intra -group balances , and gains on intra -group transactions are eliminated. Unrealised gains on transactions with associated companies and joint arrangements are eliminated in proportion to A.P. Moller Holding’s ownership share. Unrealised losses are eliminated in the same way, unless they indicate impairment.

When the group ceases to consolidate or applies equity accounting for an investment because of a loss of control, joint control, or significant influence, any retained interest in the entity is remeasured to its fair value, with the change in the carrying amount recognised in profit or loss. This fair value becomes the initial carrying amount for the purpose of subsequently accounting for the retained interest as an associate, joint venture, or other equity investment. In addition, any amounts prev iously re cognised in other comprehensive income in respect of that entity are accounted for as if the group had directly disposed of the related assets or liabilities. Therefore, amounts previously recognised in other comprehensive income are reclassified to profit or loss .

Non -controlling interests’ share of the result for the year and of equity in subsidiaries is included as part of A.P. Moller Holding’s result and equity , respectively , but shown as separate items.

FOREIGN CURRENCY TRANSLATION

The functional currency of the parent company is USD. DKK has been selected as the presentation currency as the ultimate owner of the group, A.P. Moller Foundation, is located in Denmark.

In the translation to the presentation currency of the parent company, subsidiaries, associated companies, or joint arrangements with functional currencies other than DKK, the total comprehensive income is translated into DKK at average exchange rates, and the balance sheet is translated at the exchange rates as of the balance sheet date Exchange rate differences arising from such translations are recognised directly in other comprehensive income and in a separate reserve of equity.

The functional currency v aries from business area to business area. For the group’s global trade activities, the functional currency is typically USD. This means, among other things, that the carrying amounts of property, plant and equipment and intangible assets and, hence, depreciation and amortisation , are maintained in USD from the date of acquisition. For other activities, the functional currency is generally the local currency of the country in which such activities are performed, unless circumstances suggest that a different currency is appropriate

Transactions in currencies other than the functional currency are translated at the exchange rate prevailing on the date of the transaction. Monetary items in foreign currencies not settled by the balance sheet date are translated at the exchange rate as of the balance sheet date. Foreign exchange gains and losses are included in the income statement as financial income or expenses.

STATEMENT OF COMPREHENSIVE INCOME

Other comprehensive income consists of gains and losses not recognised in the income statement, including exchange rate adjustments arising from translation from the functional currency to the presentation currency, fair value adjustments of other equity investments (at FVOCI), cash flow hedges, forward points and currency basis spread , and actuarial gains/losses on defined benefit plans, etc. The group’s share of other comprehensive income in associated companies and joint ventures is also included.

On disposal or discontinuation of an entity, the group’s share of the accumulated exchange rate adjustment relating to the relevant entity with a functional currency other USD, is reclassified to the income statement. Accumulated value adjustments of equity instruments classified as equity instruments at fair value through other comprehensive income will remain in equity upon disposal.

Other comprehensive income includes current and deferred income tax to the extent the items recognised in other comprehensive income are taxable or deductible.

Note 1.1: General accounting policies –

continued

NEW FINANCIAL REPORTING REQUIREMENTS

In 2025, A.P. Moller Holding adopted the amendments to IAS 21 - The E ffects of Changes in Foreign Exchange Rates, which introduced requirements to assess when a currency is exchangeable into another currency and when it is not. The amendments have had no material effect on the consolidated financial statements.

A.P. Moller Holding has not yet adopted the following new or amended accounting standards and requirements that have not yet become effective :

• Amendments to IFRS 9 and IFRS 7 – amendments to the classification and measurement of financial instruments

• IFRS 18 Presentation and Disclosure in Financial Statements

The amendments to IFRS 9 and IFRS 7 clarify derecognition of financial liabilities on the settlements date with an optional policy for early derecognition via electronic payments. They provide additional guidance on assessing contractual cash flows for financial assets with ESG and similar features, clarify the treatment of non -recourse and contractually linked instruments, and introduce enhanced disclosures for contingent features and equity instruments measured at fair value through OCI. The amendments ar e effective from 1 January 2026 and are not expected to have any significant impact on recognition and measurement.

IFRS 18, which will be effective from 1 January 2027, replaces IAS 1 and introduces new requirements for presentation within the income statement, including specified totals and subtotals.

Furthermore, the standard requires all income and expenses to be classified within the income statement in one of five categories: operating, investing, financing, income taxes, and discontinued operations.

A.P. Moller Holding is currently working to identify all the impacts that IFRS 18 will have on the financial statements and notes to the financial statements. The initial expected material impacts on the consolidated financial statements are as follows:

• The tax line item in the current income statement will be classified either under operating or income tax categories based on whether they are under the scope of IAS 12 or not

• Foreign exchange differences will be classified in the same category as the related income and expenses from the items giving rise to the foreign exchange differences

• Interest received will be classified under investing activities on the cash flow statement

• A new note to the financial statements for the required disclosures on management -defined performance measures will be included

Other new standards, amendments, and interpretations that are not yet effective have not been disclosed, as we do not anticipate them having a material impact on the group’s consolidated financial statements.

DEFINITIONS OF FINANCIAL RATIOS

Return on equity is calculated as result for the year in proportion to the average total equity for the year.

Equity ratio is calculated as total equity end of year in proportion to total assets end of year .

Note 1.2: Significant accounting estimates and judgments

This note describes the significant accounting estimates and judgments that management has identified as having a potentially material impact on the group’s consolidated financial statements.

The preparation of the consolidated financial statements requires management to make estimates and judgments on an ongoing basis and form assumptions that affect the reported amounts. Management forms its estimates and judgments based on historical experience, independent advi ce, external data points , in-house specialists , and on other factors believed to be reasonable under the circumstances.

In its assumption setting, management deals with various aspects of uncertainty. One aspect of uncertainty is the assessment of control over investments classified a s associates, joint ventures, and subsidiaries, where the assessment forms the basis for classifica tion. Another aspect is the measurement of uncertainty, where management makes assumptions that derive the value of recognised assets and liabilities. These assumptions concern the timing and amount of future cash flows as well as the risks inhere nt in these.

In certain areas, the outcome of business plans, including ongoing negotiations with external parties to execute those plans or the outcome of negotiations to settle claims that are raised against the group, is highly uncertain. Therefore, assumptions may change, or the outcome may differ in the coming years, which could require a material upward or downward adjustment to the carrying amounts of assets and liab ilities.

The areas and their related impact in which the group is particularly expose d to material uncertainty over the carrying amounts as at the end of 202 5 are included in the individual notes as outlined below:

Note Significant accounting estimates and judgments Estimate/ Judgment Impact

Note 2.2 EU Emissions Trading Systems (ETS) classification determination Judgment L

Note 2.5 Recognition and measurement of deferred tax assets and uncertain tax positions Estimate M

Note 3.1 Cash -generating unit determination

Note 3.1 Impairment testing key assumptions

Note 3.2 Useful life and residual value estimates

Note 3.8 Provisions for legal dispute assumptions

Note 3.9 Measurement of acquired assets, liabilities, and contingent liabilities Judgment H

Note 5.4 Operations in countries with limited access to repatriating surplus cash assumptions Judgment L

Level of potential impact to the consolidated financial statements:

• L = Low

• M = Medium

• H = High

CLIMATE-RELATED RISKS

When preparing the consolidated financial statements, management considers climate -related risks , including where these could potentially impact reported amounts materially , and continuously monitors regulatory changes and developments. The areas in which the group has assessed climate -related risks at the end of 2025 are included in the individual notes including note 2.2, 3.1, and 3.2. Management is of the opinion that climate -related risks have not had a material impact on the group’s significant account ing estimates and judgments.

CHANGE IN ACCOUNTING ESTIMATES

As a result of the annual useful life review at the end of 2025, the useful lives of vessels will increase from 20 years to 25 years and will be applied prospectively as a change in the accounting estimate, effective 1 January 2026. The change is expected to result in reduced depreciation of around DKK 4.5bn in 2026. The change in useful lives has not impacted the financial position or results for 2025 or any previous periods.

OPERATING PROFIT

Note 2.1: Revenue

TYPES OF REVENUE

Types of revenue have been organised according to our four investment themes:

• Global trade includes shipping activities, sale of bunker oil, integrated transportation, fulfilment and management solutions, including landside and air transportation, warehousing and supply chain management offerings, gateway terminal activities, towage and related marine activities, and trading, etc.

• Energy transition includes sale of goods and services for renewable solutions

• Circularity, water & waste recovery includes sale of food packaging solutions, recycled plastic, and operators of water utility businesses

• Demographic & societal change includes mainly diagnostic services within laboratory, imaging, and pathology specialities

CONTRACTS WITH CUSTOMERS

Set out below is the reconciliation of the revenue from contracts with customers to the amounts disclosed as total revenue

Note 2.1: Revenue – continued

CONTRACT BALANCES

Amounts in DKKm

T rade receivables in the balance sheet include accrued income and contract assets comprising unbilled amounts representing the group’s right to consideration for the services transferred to date. All deferred income is recognised in the income s tatement within 12 months.

Under the payment terms generally applicable to the group’s revenue generating activities, prepayments are only received to a limited extent. Typically , payment is due upon or after completion of the services.

Part of the deferred income presented in the balance sheet constitutes contract liabilities , which represent advance payments and billings in excess of the recognised revenue.

There were no significant changes in accrued and deferred income during the reporting period.

Impairment losses disclosed in note 4.3 relate to receivables arising from contracts with customers.

PERFORMANCE OBLIGATIONS

Performance obligations are products and services that are to be completed under existing customer contracts. There is no performance obligations after five years.

ACCOUNTING POLICIES

Revenue is recognised when the performance obligation has been satisfied, which happens upon the transfer of control to the customer at an amount that reflects the consideration to which the group expects to be entitled in exchange for the goods and servic es.

Revenue from shipping activities is recognised over time as the performance obligation is satisfied, including a share of revenue from incomplete voyages at the balance sheet date. Invoiced revenue related to an estimated proportion of remaining voyage tim e and activities at the destination port is deferred. The percentage of completion is calculated as the remaining number of days of a voyage, as a percentage of the total number of days a voyage is estimated to last. Detention and demurrage fees are recogn ised over time until the customers’ late return or pick -up of containers.

Revenue from terminal operations and towing activities is recognised upon completion of the service. In container terminals operated under certain restrictive terms of pricing and service , etc., the value of tangible assets constructed on behalf of the concession grantor is recognised as revenue during the construction.

Revenue from most freight forwarding activities is recognised over time.

Revenue from the sale of goods is recognised upon the transfer of control to the buyer.

Contract work in progress and services are included in revenue based on the stage of completion so that revenue corresponds to the selling price of the work performed and service s completed in the financial year (the percentage -of-completion method) .

No significant element of financing is deemed present , as sales are made with credit terms which are consistent with market practice. Revenue from sales is recognised based on the price specified in the contract, net of the estimated volume discounts. Accumulated experience is used to estimate and provide for the discounts, using the expected value method, and revenue is only recognised to the extent that it is highly probable that a significant reversal will not occur.

Note 2.2: Operating costs

1 Includi ng DKK 114m (DKK 7 3m) related to research and development expenditures

Customary agreements have been entered into with employees regarding compensation in connection with resignation w ith consideration for local legislation and collective agreements.

The remuneration expense for share -based payments included in wages and salaries amounts to DKK 296m (DKK 256m). Please refer to note 5.1 for further information about share -based payment s.

FEES AND REMUNERATION TO THE EXECUTIVE BOARD AND BOARD OF DIRECTORS

The Executive Board of A.P. Moller Holding is considered key management personnel. The group has a cash -settled incentive plan to members of the Executive Board and grants have been awarded on a yearly basis . The incentive plan provides an annual bonus and long -term incentive programmes, which are determined by the development in the value creation of the underlying investments . The main part s of the long -term incentive programmes are capped.

TO STATUTORY AUDITORS

Note 2.2: Operating costs – continued

SIGNIFICANT ACCOUNTING JUDGMENTS

Climate-related risks

The group is subject to the new EU Emissions Trading System (ETS), a cap -and -trade system to reduce emissions via a carbon market. Implementation of the EU ETS requires the group to purchase EU allowances (EUAs) representing the right to emit a specific amount of greenhouse gases.

The group has purchased EUAs as spot, future , or forward contracts. EUA futures and forwards satisfy the conditions for the ‘own use ’ exemption and are off -balance -sheet items.

EUA contracts are classified as other current assets upon delivery of certificates. They are measured at cost of settlement and are not subject to remeasurement until surrender. The cost of settlement includes all purchase, conversion , and other directly attributable costs such as transaction costs.

The accrual is recognised as fuel is burnt in the group’s applicable shipping activities, measured at expected cost for the required EUAs, based on actual emissions and the price of the EUAs, which is calculated as a weighted average price of EUA spots, futures , and forwards. The corresponding cost is presented as bunker cost.

Note 2.3: Depreciation, amortisation and impairment losses, net

1 In 2024, a reversal of impairment of DKK 18m related to assets held for sale is included

For more information, reference is made to note 3.1, 3.2, and 3.3.

Note 2.4: Gain on sale of non-current assets, etc., net

Gains include the sale of vessels and equipment DKK 1.5bn (DKK 2.3bn) and sale of businesses DKK 0. 1bn (DKK 1.9bn).

Losses are related to the sale of vessels and equipment DKK 0. 5bn (DKK 0.4bn) and sale of other non -current assets DKK 0.1bn (DKK 0.5 ).

ACCOUNTING POLICIES

Operating costs comprise costs incurred in generating revenue for the year, including costs for crew, labour, raw materials and consumables, repair and maintenance, and sales and administrati on

Note 2.5: Tax and deferred tax

T he group generates profit across multiple business sectors and countries. Corporate income taxes comprise taxes calculated in accordance with various countries’ tax regimes, including global minimum taxation (OECD Pillar Two).

The land -based activities, which are subject to normal corporate income tax, include terminals, logistics, services and shipping agencies, sale of industrial products, diagnostics services, and financial profit from other equity investments.

The taxation of shipping income, generated by vessels providing services on the high seas, calling at multiple ports across the globe, is outlined in the OECD Model Tax Convention, Article 8 (Shipping Article). Under the Shipping Article, activities are taxable in the jurisdiction where the ship owning and operating entity is resident. Within ou r group, this is predominantly in Denmark and Singapore.

To encourage ship registration in Europe and ensure global competitiveness of the European Maritime Industry, the EU has approved a specific shipping regime. This is normally referred to as tonnage tax which calculates corporate income tax, based on the ne t tonnage of the fleet. Consequently, under the tonnage tax regime, no credit is given for losses and, despite massive capital investments in containers and vessels, no tax deductions are granted for depreciation or operating expenses.

Tonnage tax regimes apply to the main part of the group’s activities within global trade and result in a stable annual tax liability. Given the liability to tonnage tax is not impacted by financial profits, and is payable even in loss making years, the eff ective tax rate (ETR) metric can fluctuate significantly.

Note 2.5: Tax and deferred tax – continued

Three elements are key to understanding how the global minimum taxation rules will impact the g roup. First, the g roup does not set up artificial structures in low -tax jurisdictions for tax purposes or earn significant profits in such jurisdictions, which means that the group’s business structure itself is not impacted significantly by the rules, but some additional tax may become payable where services are provided in low -tax jurisdictions. Second, tax incentives given to capital projects, such as critical infrastructure, will be considered less effective going forward , as it will impact the effective tax rate and thereby the basis for potential top -up tax. Third, although the rules exclude ‘international shipping income ’, the definition is more restrictive than the global definitions usually applied under a tax treaty following the OECD Model Tax Convention or under Danish tonnage tax.

Assets Liabilities Net liabilities

The unrecognised deferred tax assets have no significant time limitations. There are no substantial unrecognised tax liabilities on investments in subsidiaries, associated companies , or joint ventures.

SIGNIFICANT ACCOUNTING ESTIMATES

Deferred tax assets