EVOLUTION OF THE GLOBAL SHIPPING INDUSTRY

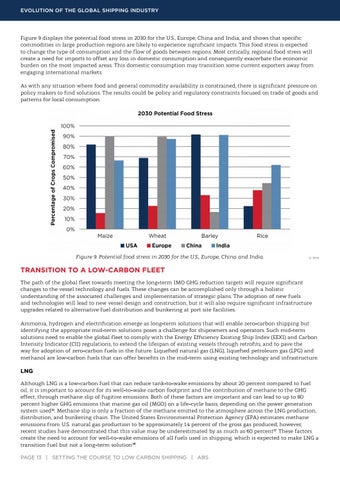

Figure 9 displays the potential food stress in 2030 for the U.S., Europe, China and India, and shows that specific commodities in large production regions are likely to experience significant impacts. This food stress is expected to change the type of consumption and the flow of goods between regions. Most critically, regional food stress will create a need for imports to offset any loss in domestic consumption and consequently exacerbate the economic burden on the most impacted areas. This domestic consumption may transition some current exporters away from engaging international markets. As with any situation where food and general commodity availability is constrained, there is significant pressure on policy makers to find solutions. The results could be policy and regulatory constraints focused on trade of goods and patterns for local consumption.

Figure 9: Potential food stress in 2030 for the U.S., Europe, China and India.

© RMI

TRANSITION TO A LOW-CARBON FLEET The path of the global fleet towards meeting the long-term IMO GHG reduction targets will require significant changes to the vessel technology and fuels. These changes can be accomplished only through a holistic understanding of the associated challenges and implementation of strategic plans. The adoption of new fuels and technologies will lead to new vessel design and construction, but it will also require significant infrastructure upgrades related to alternative fuel distribution and bunkering at port site facilities. Ammonia, hydrogen and electrification emerge as long-term solutions that will enable zero-carbon shipping but identifying the appropriate mid-term solutions poses a challenge for shipowners and operators. Such mid-term solutions need to enable the global fleet to comply with the Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) regulations, to extend the lifespan of existing vessels through retrofits, and to pave the way for adoption of zero-carbon fuels in the future. Liquefied natural gas (LNG), liquefied petroleum gas (LPG) and methanol are low-carbon fuels that can offer benefits in the mid-term using existing technology and infrastructure.

LNG Although LNG is a low-carbon fuel that can reduce tank-to-wake emissions by about 20 percent compared to fuel oil, it is important to account for its well-to-wake carbon footprint and the contribution of methane to the GHG effect, through methane slip of fugitive emissions. Both of these factors are important and can lead to up to 80 percent higher GHG emissions that marine gas oil (MGO) on a life-cycle basis, depending on the power generation system used36. Methane slip is only a fraction of the methane emitted to the atmosphere across the LNG production, distribution, and bunkering chain. The United States Environmental Protection Agency (EPA) estimates methane emissions from U.S. natural gas production to be approximately 1.4 percent of the gross gas produced; however, recent studies have demonstrated that this value may be underestimated by as much as 60 percent37. These factors create the need to account for well-to-wake emissions of all fuels used in shipping, which is expected to make LNG a transition fuel but not a long-term solution38. PAGE 13 | SETTING THE COURSE TO LOW CARBON SHIPPING | ABS